Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - Moelis & Co | a2219569zex-23_1.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO COMBINED FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on April 8, 2014

Registration No. 333-194306

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 4

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

MOELIS & COMPANY

(Exact Name of Registrant as Specified in Its Charter)

| DELAWARE (State or Other Jurisdiction of Incorporation or Organization) |

6199 (Primary Standard Industrial Classification Code Number) |

46-4500216 (I.R.S. Employer Identification Number) |

399 Park Avenue, 5th Floor

New York, New York 10022

(212) 883-3800

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant's Principal Executive Offices)

Osamu R. Watanabe Esq.

General Counsel

Moelis & Company

399 Park Avenue, 5th Floor

New York, New York 10022

(212) 883-3800

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

| Copies to: | ||

Joseph A. Coco, Esq. Richard B. Aftanas, Esq. Skadden, Arps, Slate, Meagher & Flom LLP Four Times Square New York, New York 10036 (212) 735-3000 |

Jay Clayton, Esq. Glen T. Schleyer, Esq. Sullivan & Cromwell LLP 125 Broad Street New York, New York 10004 (212) 558-4000 |

|

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

CALCULATION OF REGISTRATION FEE

|

||||||||

| Title of Each Class of Securities to be Registered |

Amount to be Registered(1) |

Proposed Maximum Offering Price Per Unit(2) |

Proposed Maximum Aggregate Offering Price(2)(3) |

Amount of Registration Fee(4) |

||||

|---|---|---|---|---|---|---|---|---|

Class A common stock, par value $0.01 per share |

8,395,000 | $29 | $243,455,000 | $31,358 | ||||

|

||||||||

- (1)

- Includes

1,095,000 shares the underwriters have the option to purchase.

- (2)

- Estimated

solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(a) under the Securities Act.

- (3)

- Includes

the offering price of the 1,095,000 shares the underwriters have the option to purchase.

- (4)

- Previously paid.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS (Subject to Completion)

Dated April 8, 2014

7,300,000 Shares

![]()

Class A Common Stock

We are offering 7,300,000 shares of Class A common stock. This is our initial public offering and no public market currently exists for our shares. We anticipate that the initial public offering price will be between $26 and $29 per share.

We have applied to list our Class A common stock on the New York Stock Exchange under the symbol "MC."

We are an "emerging growth company" under applicable Securities and Exchange Commission rules and will be subject to reduced public company reporting requirements.

Investing in our Class A common stock involves risks. See "Risk Factors" beginning on page 16.

The Securities and Exchange Commission and state securities regulators have not approved or disapproved these securities, or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

|

||||||

| |

Price to public |

Underwriting discounts and commissions(1) |

Proceeds to us |

|||

|---|---|---|---|---|---|---|

Per Share |

$ | $ | $ | |||

Total |

$ | $ | $ | |||

|

||||||

- (1)

- See "Underwriting" for a description of the compensation payable to the underwriters.

We have granted the underwriters the right to purchase up to an additional 1,095,000 shares of Class A common stock at the initial public offering price less the underwriting discounts and commissions.

The underwriters expect to deliver the shares of Class A common stock to purchasers on or about , 2014.

| Goldman, Sachs & Co. | Morgan Stanley | ||||

Moelis & Company |

J.P. Morgan |

UBS Investment Bank |

|||

Keefe, Bruyette & Woods A Stifel Company |

Sanford C. Bernstein |

JMP Securities |

, 2014

Through and including , 2014 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer's obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

We and the underwriters have not authorized anyone to provide any information or to make any representations other than those contained in this prospectus, any amendment or supplement to this prospectus or in any free writing prospectuses we have prepared. We and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. Neither the delivery of this prospectus nor the sale of our Class A common stock means that information contained in this prospectus is correct after the date of this prospectus. This prospectus is an offer to sell the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so.

The industry, market and competitive position data referenced throughout this prospectus are based on research, industry and general publications, including surveys and studies conducted by third parties. Industry publications, surveys and studies generally state that they have been obtained from sources believed to be reliable. We have not independently verified such third party information. While we are not aware of any misstatements regarding any industry, market or similar data presented herein, such data involve uncertainties and are subject to change based on various factors, including those discussed under the headings "Special Note Regarding Forward-Looking Statements" and "Risk Factors" in this prospectus.

In this prospectus, we use the term "independent investment banks" or "independent advisors" to refer to investment banks primarily focused on advisory services and that conduct limited or no commercial banking or sales and trading activities. We use the term "global independent investment banks" to refer to independent investment banks with global coverage capabilities across all major industries and regions. We consider the global independent investment banks to be our publicly traded peers, Evercore Partners Inc., Greenhill & Co., Inc., Lazard Ltd, and us.

Map Legend

•Moelis & Company office

- /*\

- Strategic alliance

i

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our Class A common stock, you should carefully read this entire prospectus, including our financial statements and the related notes thereto and the information set forth under the sections "Risk Factors," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and the historical financial statements and related notes, in each case included in this prospectus. Some of the statements in this prospectus constitute forward-looking statements. See "Special Note Regarding Forward-Looking Statements." Unless the context requires otherwise, the words "Company," "we," "us" and "our" refer to Moelis & Company and its subsidiaries, and for periods prior to the reorganization described herein, the advisory business of Moelis & Company Holdings LP. Unless the context otherwise requires, references to (1) "Moelis & Company" refer solely to Moelis & Company, a Delaware corporation, and not to any of its subsidiaries, (2) "Group LP" refer solely to Moelis & Company Group LP, a Delaware limited partnership, and not to any of its subsidiaries, (3) "Partner Holdings" refer to Moelis & Company Partner Holdings LP, a Delaware limited partnership, and (4) "Old Holdings" refer to Moelis & Company Holdings LP, a Delaware limited partnership.

Moelis & Company is a leading global independent investment bank that provides innovative strategic and financial advice to a diverse client base, including corporations, governments and financial sponsors. We assist our clients in achieving their strategic goals by offering comprehensive, globally integrated financial advisory services across all major industry sectors. Our team of experienced professionals advises clients on their most critical decisions, including mergers and acquisitions ("M&A"), recapitalizations and restructurings and other corporate finance matters.

Since our inception, we have achieved rapid growth by hiring high-caliber professionals, expanding the scope and geographic reach of our advisory services, developing new client relationships and cultivating our professionals through training and mentoring. Today we serve our clients with over 300 advisory professionals, including 87 Managing Directors, based in 15 offices around the world. We have advised on over $1 trillion of transactions, including three of the ten largest announced global mergers and acquisitions and four of the ten largest announced global recapitalizations and restructurings in 2013.

Moelis & Company was founded in 2007 by veteran investment bankers to create a global independent investment bank that offers multi-disciplinary solutions and exceptional transaction execution combined with the highest standard of confidentiality and discretion. We create lasting client relationships by providing focused innovative advice through a highly collaborative and global approach not limited to specific products or access to particular regions. Our compensation model fosters our holistic approach to clients by emphasizing quality of advice and is not a commission-based structure where employees are compensated on a defined percentage of the revenues they generate. We believe our discretionary approach to compensation leads to exceptional advice, strong client impact and enhanced internal collaboration.

We have demonstrated strong financial performance, achieving revenues of $411 million and pre-tax income of $73 million in 2013, our sixth full year of operations. We have also won numerous awards for our client focus and innovation, including "Most Innovative Independent Investment Bank" by The Banker in 2010, 2011 and 2013 and "Best Global Independent Investment Bank" by Euromoney Magazine in 2010 and have served as financial advisor to our clients on many noteworthy assignments, including the following transactions.

1

2

Our Market Opportunity

We believe that we will continue to grow revenues and gain market share as a result of being well positioned to benefit from the following market forces:

Growing Demand for Independent Advice: During the past decade, the demand for independent advice has increased dramatically. In 2013, 80% of the top 10 announced M&A deals and 75% of the top 20 announced M&A deals included independent advisors. This is up significantly from 2003, when 30% of both the top 10 and top 20 announced M&A deals included independent advisors. We believe the shift toward independent advice has been driven largely by the actual or perceived conflicts at the large financial conglomerates where sizable sales and trading, underwriting and lending businesses coexist with an advisory business that comprises only a small portion of revenues and profits. We expect the momentum of the independent firms to continue as clients seek uncompromised confidential advice free of conflicts. We believe we are well positioned amongst the independent investment banks to deliver this advice given our global reach and product and industry depth.

Ongoing Dislocation at Large Financial Conglomerates: We will seek to continue to take advantage of growth opportunities arising from the ongoing dislocation at large financial conglomerates. These firms face increasing regulation and the pressure of managing large disparate business divisions, leading to confidentiality challenges, higher operating costs, compensation limitations and increased capital constraints, all of which we believe adversely affect their ability to serve clients and compete for talented professionals. As these firms continue to struggle with these issues, we see tremendous opportunities to enhance our industry coverage, expand our geographic reach and add new advisory expertise.

Anticipated Upturn in Mergers & Acquisitions Activity: While announced M&A volume has been relatively restrained since the global financial crisis, we believe a stronger M&A environment should return based on a stabilizing global macroeconomic environment, strong corporate balance sheets, attractive financing markets, a trend toward global consolidation and increased financial sponsor activity. We expect a more robust M&A environment to increase deal flow and enhance our growth. In addition, the recovery in Europe since the global financial crisis has lagged that of the U.S. We have made substantial investments in Europe, with over 60 advisory professionals in the region, while some of our competitors have scaled down their operations in Europe, and we expect to be well positioned when the European M&A market rebounds.

Continued Activity in Recapitalization and Restructuring Market: We believe that, given the amount of leverage (including floating rate instruments) that companies have issued in recent years, a steady recapitalization and restructuring market will continue to exist if interest rates rise or credit markets become more difficult to access, even with an improving macroeconomic environment and an anticipated upturn in M&A activity. Both 2012 and 2013 represented record years of leveraged finance issuance in the U.S., as companies took advantage of historically low borrowing costs to leverage their capital structures. We believe we are well positioned to assist companies through our holistic approach, which combines sector expertise with M&A, recapitalization and restructuring and other advisory capabilities, to provide solutions to clients in both robust and challenging economic environments.

3

Our Key Competitive Strengths

With 15 offices located around the world, capabilities in all major industries and deep advisory expertise, we believe we are well positioned to take advantage of the strong market opportunity for independent investment banks. Furthermore, we believe our business is differentiated from that of our competitors in the following respects:

Globally Integrated Firm with Innovative Advisory Solutions: We provide the high-touch and conflict free benefits of an independent investment bank with the global reach, sector depth and product expertise more commonly found at larger financial institutions. With 15 offices located in North and South America, Europe, the Middle East, Asia and Australia, we combine local and regional expertise with international market knowledge to provide our clients with highly integrated information flow and strong cross-border capabilities. We harness the deep industry expertise and broad corporate finance experience of our 87 global Managing Directors, which include 52 former sector and product heads from major investment banks. We reinforce our model with a discretionary compensation structure that encourages a high degree of collaboration and our "One Firm" mentality.

Advisory Focus with Strong Intellectual Capital: We primarily focus on advising clients, unlike most of our major competitors who derive a large percentage of their revenues from lending, trading and underwriting securities. We believe this independence allows us to offer advice free from the actual or perceived conflicts associated with lending to clients or trading in their securities. In addition, our focus on advisory services frees us from the pressure of cross-selling products, which we believe can distract from the dialogue with clients around their long-term strategy, compromising the advice. We provide intellectual capital based on our judgment, expertise and relationships combined with intense senior level attention to all transactions. The business of delivering intellectual capital allows us to operate a low risk and capital light model with attractive profit margins. We are not exposed to the financial risk and regulatory requirements that arise from, or the capital investments required in, balance sheet lending and trading activities.

Fast Growing Global Independent Investment Bank: Since our inception in 2007, we have achieved rapid growth, earning revenues of $411 million and pre-tax income of $73 million in 2013. During this time however, the global financial crisis contributed to a 51% decrease in global completed M&A volume from the peak levels of 2007. We took advantage of the dislocation in the financial services industry following the global financial crisis and capitalized on the unique opportunity to hire Managing Directors who have on average 20 years of investment banking experience. We believe the quality and scale of our global franchise and the speed at which it has been achieved would be a challenge to replicate today.

Strong Financial Discipline: We have remained financially disciplined with an intense focus on managing growth in a profitable manner, as demonstrated by the $73 million of pre-tax income achieved in our sixth full year of operations. We hired aggressively during the global financial crisis to take advantage of the dislocation among our competitors and recently have taken a more measured approach to hiring as the markets and compensation levels have stabilized. We incentivize our bankers as owners by awarding equity compensation in order to align the interests of our employees and equityholders, and our employees currently own over three quarters of our Company. Additionally, we have focused on entering new regions and sectors through creative and cost efficient strategies. We intend to maintain our financial discipline as we continue to grow our revenues, expand into new markets and increase our areas of expertise.

Significant Organic Growth Opportunities: We have made significant investments in our intellectual capital with the hiring of 44 Managing Directors and promotion of 22 internal professionals to Managing Director since 2010. In addition, we have invested time and resources in our recruiting and training programs. We established a meaningful presence at the top undergraduate programs

4

in our first year of operations, which has resulted in the hiring of over 200 analysts from campus since our inception. We are poised to continue realizing meaningful organic growth from these investments. We have achieved critical size in key industry sectors and regions around the globe, as well as recognition for advising on innovative transactions, which have enhanced our brand globally. We are positioned to continue to grow revenues as a result of increased individual productivity as our investments in people mature and as we continue to leverage our global platform through enhanced connectivity and idea generation and expanded brand recognition.

High Standard of Confidentiality and Discretion: Due to the highly sensitive nature of M&A discussions where confidentiality is of paramount importance to clients, the M&A business is most effectively operated on a "need to know" basis. We believe that large financial conglomerates with multiple divisions, "Chinese Walls" and layers of management have a significantly greater number of employees who have access to sensitive client information, which can increase the risk of confidential information leaking. Such leaks can materially impair the viability of transactions and other strategic decisions. We have established a high standard of confidentiality and discretion, as well as instituted procedures designed to protect our clients and minimize the risk of sensitive information leaking to the market.

Diversified Advisory Platform: Our business is highly diversified across sectors, types of advisory services and clients. Our broad corporate finance expertise positions us to advise clients through any phase of their life cycle and in any economic environment. We focus on a wide range of clients from large public multinational corporations to middle market private companies to individual entrepreneurs, and we deliver the full resources of our firm and the highest level of senior attention to every client, regardless of size or situation. In addition, we have no meaningful client concentration, with our top 10 transactions representing only 23% of our revenues in 2013. Our holistic "One Firm" approach also reduces dependence on any one product or banker and allows us to leverage our intellectual capital across the firm as necessary to offer multiple solutions to our clients, increase our client penetration and adapt to changing circumstances.

Partnership Culture: We believe that our momentum and commitment to excellence have created an environment that attracts and retains high quality talent. Our people are our most valuable asset and our goal is to attract, retain and develop the best and brightest talent in our industry across all levels. We strive to foster a collaborative environment, and we seek individuals who are passionate about our business and are a fit with our culture. We have established a compensation philosophy that reinforces our long-term vision and values by rewarding collaboration, client impact and lasting relationships and encourages employees to put the interests of our clients and our Company first. Above all, the "Moelis Standard" nurtures a culture of partnership, passion, optimism and hard work, which inspires the highest level of quality and integrity in every interaction with our clients and each other.

Preliminary Financial Results for the Quarter Ended March 31, 2014

The following information reflects our preliminary expectations of our financial results for the quarter ended March 31, 2014, based on currently available information. We have provided ranges, rather than specific amounts, for the financial results for the quarter ended March 31, 2014 primarily because our financial closing procedures for this period are not yet complete. As a result, our final results upon completion of our closing procedures may vary from the preliminary results provided below. For instance, we have not finalized and completed our review of certain account reconciliations and accruals, or prepared notes to our financial information.

We expect to report revenues of between $113.0 million and $115.0 million for the quarter ended March 31, 2014, compared to $59.8 million for the quarter ended March 31, 2013. We also expect to report income before income taxes of between $21.0 million and $23.0 million for the quarter ended

5

March 31, 2014, compared to $0.7 million for the quarter ended March 31, 2013. An increased number of clients contributed to our revenue growth, and during the first quarter of 2014, we earned revenues from approximately 110 clients (24 of which paid fees equal to or greater than $1 million) as compared with 97 clients (20 of which paid fees equal to or greater than $1 million) during the same period in 2013. In the first quarter of 2014, global completed M&A volume was roughly flat from the first quarter of 2013, and the number of global completed M&A transactions was 16% lower than in the first quarter of 2013.

The preliminary financial information included in this prospectus reflects management's estimates based solely upon information available to us as of the date of this prospectus and is the responsibility of management. The preliminary financial results presented above are not a comprehensive statement of our financial results for the quarter ended March 31, 2014, and we have not presented a range of our expected net income. In addition, the preliminary financial results presented above have not been audited, reviewed, or compiled by our independent registered public accounting firm, Deloitte & Touche LLP. Accordingly, Deloitte & Touche LLP does not express an opinion or any other form of assurance with respect thereto and assumes no responsibility for, and disclaims any association with, this information. The preliminary financial results presented above are subject to the completion of our financial closing procedures, which have not yet been completed. Our actual results for the quarter ended March 31, 2014 will not be available until after this offering is completed and may differ materially from these estimates. Therefore, you should not place undue reliance upon these preliminary financial results. For instance, during the course of the preparation of the respective financial statements and related notes, additional items that would require material adjustments to be made to the preliminary estimated financial results presented above may be identified. There can be no assurance that these estimates will be realized, and estimates are subject to risks and uncertainties, many of which are not within our control. Additionally, our revenues and income before tax can fluctuate materially depending on the number and size of completed transactions on which we advised and other factors. Accordingly, the revenues and income before tax in any particular period may not be indicative of future results. See "Risk Factors" and "Special Note Regarding Forward-Looking Statements."

Risk Factors

Investing in our Class A common stock involves risks. You should carefully consider the risks described in "Risk Factors" beginning on page 16 before making a decision to invest in our Class A common stock. If any of these risks actually occurs, our business, financial condition or results of operations could be materially adversely affected. In such case, the trading price of our Class A common stock would likely decline, and you may lose all or part of your investment. The following is a summary of some of the principal risks we face:

- •

- our future growth will depend on, among other things, our ability to successfully identify, recruit and develop talent and

will require us to commit additional resources;

- •

- changing market conditions can adversely affect our business in many ways, including by reducing the volume of the

transactions involving our business, which could materially reduce our revenue;

- •

- our revenue in any given period is dependent on the number of fee-paying clients in such period, and a significant

reduction in the number of fee-paying clients in any given period could reduce our revenue and adversely affect our operating results in such period;

- •

- our ability to retain our Managing Directors and our other professionals, including our executive officers, is critical to the success of our business; and

6

- •

- substantially all of our revenue is derived from advisory fees and as a result, our revenue and profits are highly volatile on a quarterly basis and may cause the price of our Class A common stock to fluctuate and decline.

Implications of Being an Emerging Growth Company

As a company with less than $1.0 billion in revenues during our last fiscal year, we qualify as an "emerging growth company" pursuant to the Jumpstart Our Business Startups Act of 2012 (the "JOBS Act"). An emerging growth company may take advantage of specified exemptions from various requirements that are otherwise applicable generally to public companies in the United States. These provisions include:

- •

- reduced compensation disclosure requirements; and

- •

- an exemption from the auditor attestation requirement in the assessment of the emerging growth company's internal control over financial reporting.

The JOBS Act also permits an emerging growth company such as us to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies.

When we are no longer deemed to be an emerging growth company, we will not be entitled to the exemptions provided in the JOBS Act discussed above. We will remain an emerging growth company until the earliest of:

- •

- the last day of our fiscal year during which we have total annual gross revenues of at least $1.0 billion;

- •

- the last day of our fiscal year following the fifth anniversary of the completion of this offering;

- •

- the date on which we have, during the previous three-year period, issued more than $1.0 billion in non-convertible

debt securities; or

- •

- the date on which we are deemed to be a "large accelerated filer" under the Securities Exchange Act of 1934, as amended (the "Exchange Act"), which would occur if the market value of our common stock that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter.

We have availed ourselves in this prospectus of the reduced reporting requirements described above with respect to executive compensation disclosure requirements. We expect to continue to avail ourselves of the emerging growth company exemptions described above. As a result, the information that we provide to stockholders will be less comprehensive than what you might receive from other public companies. We have not elected to avail ourselves of the exemption that allows emerging growth companies to extend the transition period for complying with new or revised financial accounting standards.

Moelis & Company was incorporated in Delaware on January 9, 2014, in contemplation of this offering. Our principal executive offices are located at 399 Park Avenue, 5th Floor, New York, NY 10022, and our phone number is (212) 883-3800.

7

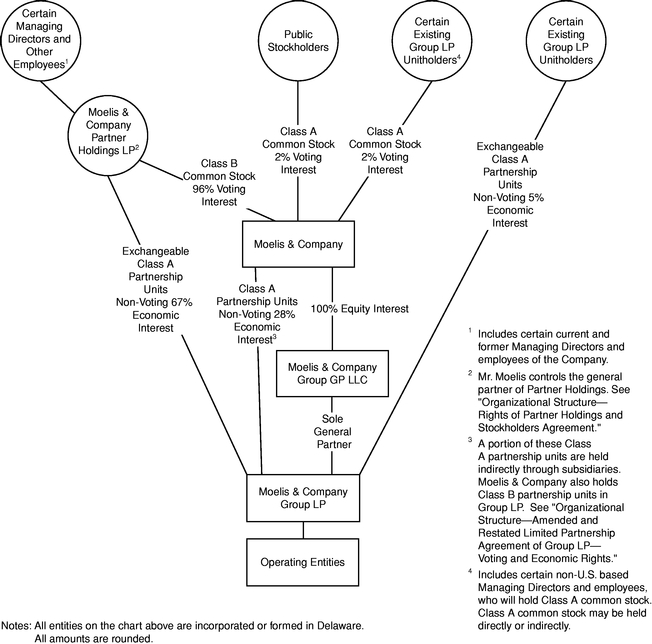

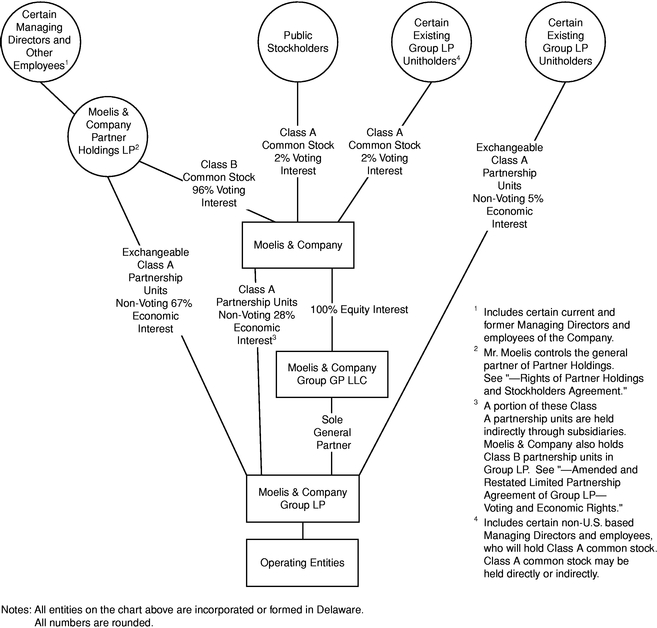

Prior to this offering we will effect the reorganization described in "Organizational Structure." Following the reorganization and this offering, Moelis & Company will be a holding company and its only assets will be its partnership interests in Group LP, its equity interest in the sole general partner of Group LP, Moelis & Company Group GP LLC, and its interests in its subsidiaries. Moelis & Company will operate and control all of the business and affairs of Group LP and its operating entity subsidiaries indirectly through its equity interest in Moelis & Company Group GP LLC.

The diagram below depicts our organizational structure following this offering.

8

Immediately following this offering:

- •

- Moelis & Company will hold Class A partnership units in Group LP representing 27.9% of the total

number of Class A partnership units in Group LP (or 29.3% if the underwriters exercise their option to purchase additional shares in full);

- •

- certain of our existing Class A partnership unitholders (including all of our Managing Directors (other than

certain non-U.S. based Managing Directors) indirectly through Partner Holdings) will hold Class A partnership units in Group LP representing 72.1% of the total number of Class A

partnership units in Group LP (or 70.7% if the underwriters exercise their option to purchase additional shares in full);

- •

- certain of our existing Group LP Class A partnership unitholders (including certain non-U.S. based Managing

Directors and employees) will, directly or indirectly, own approximately 51.8% of the Class A common stock (or 48.3% if the underwriters exercise their option to purchase additional shares in

full);

- •

- public stockholders will own 48.2% of the Class A common stock (or 51.7% if the underwriters exercise their option

to purchase additional shares in full); and

- •

- Partner Holdings will own all of our Class B common stock.

9

Class A common stock offered by us |

7,300,000 shares (8,395,000 shares if the underwriters exercise their option to purchase additional shares in full). | |

Class A common stock to be outstanding immediately after this offering |

15,155,804 shares (16,250,804 shares if the underwriters exercise their option to purchase additional shares in full). |

|

|

This number excludes 39,210,693 shares of Class A common stock issuable in exchange for Group LP Class A partnership units and upon conversion of shares of our Class B common stock, each as described under "—Exchange Rights." If all outstanding Group LP Class A partnership units were exchanged and all outstanding shares of Class B common stock were converted, we would have 54,366,497 shares of Class A common stock outstanding immediately after this offering. |

|

Class B common stock to be outstanding immediately after this offering |

36,328,307 shares. |

|

Use of proceeds |

Our net proceeds from this offering will be approximately $176 million (or approximately $205 million if the underwriters exercise their option to purchase additional shares in full) after deducting underwriting discounts and commissions and estimated offering expenses payable by us (assuming the Class A common stock is sold at $27.50 per share, which is the mid-point of the estimated initial public offering price range set forth on the cover page of this prospectus). |

|

|

Moelis & Company will use a portion of the net proceeds from this offering to purchase Class A partnership units directly from Group LP and the remaining net proceeds to make one-time payments to the partners of Old Holdings who received, directly or indirectly, shares of Class A common stock in exchange for the Group LP Class A partnership units they would have otherwise received in connection with the reorganization. See "Organizational Structure—The Reorganization." |

|

|

Group LP will use a portion of the net proceeds it receives from this offering to make a one-time cash distribution to the partners of Old Holdings who hold Group LP Class A partnership units as of the day prior to the closing of this offering and the remaining net proceeds that it receives for general corporate purposes. |

|

|

See "Use of Proceeds." |

|

|

10

Voting rights |

Each share of our Class A common stock will entitle its holder to one vote on all matters to be voted on by stockholders generally. |

|

|

The shares of our Class B common stock will entitle Partner Holdings to (i) for so long as the Class B Condition (as defined below in "Organizational Structure") is satisfied, ten votes per share, and (ii) after the Class B Condition ceases to be satisfied, one vote per share. Partner Holdings will have a number of shares of Class B common stock in Moelis & Company that is equal to the aggregate number of vested and unvested Class A partnership units in Group LP held by Partner Holdings. Based on Mr. Moelis's control of Partner Holdings, until the Class B Condition ceases to be satisfied, Mr. Moelis will have all of the voting power of the Class B common stock. |

|

|

Holders of our Class A common stock and Class B common stock will vote together as a single class on all matters presented to our stockholders for their vote or approval, except as otherwise provided in our amended and restated certificate of incorporation or as required by applicable law. See "Description of Capital Stock—Class B Common Stock." |

|

|

Upon completion of this offering, holders of our Class A common stock who are not affiliated with our directors and executive officers will own approximately 84.6% of Moelis & Company's Class A common stock and will have approximately 3.4% of the voting power in Moelis & Company (or approximately 85.6% and 3.6%, respectively, if the underwriters exercise their option to purchase additional shares in full). |

|

Exchange Rights |

Subject to the terms and conditions of the Group LP limited partnership agreement and the lock-up restrictions described below, each Group LP Class A unitholder will have the right to exchange Group LP Class A partnership units, either for shares of our Class A common stock on a one-for-one basis, or cash (based on the market price of the shares of Class A common stock), at Group LP's option. If Group LP chooses to exchange such units for our Class A common stock, Moelis & Company will deliver an equivalent number of shares of Class A common stock to Group LP for further delivery to the exchanging holder and receive a corresponding number of newly issued Group LP Class A partnership units. The exchanging holder's surrendered Group LP Class A partnership units will be cancelled by Group LP. As Group LP Class A unitholders exchange their Group LP Class A partnership units, Moelis & Company's percentage of economic ownership of Group LP will be correspondingly increased. Following each such exchange, Partner Holdings will be required to surrender to Moelis & Company a corresponding number of shares of Class B common stock, |

|

|

11

|

and such shares will be converted into shares of Class A common stock at a conversion rate based on the ratio of the subscription price for such shares of Class B common stock to the initial public offering price of the Class A common stock, which will be delivered to Partner Holdings. Group LP will also convert an equivalent number of Class B partnership units held by Moelis & Company into Class A partnership units based on the same conversion rate. See "Organizational Structure—Amended and Restated Limited Partnership Agreement of Group LP—Exchange Rights." |

|

Lock-up |

Group LP Class A partnership units and Moelis & Company Class A common stock held by our Managing Directors (including through Partner Holdings) are subject to lock-up agreements for four years from this offering. After this period, Group LP Class A partnership units held by a Managing Director will become exchangeable into Class A common stock or cash as described above and Moelis & Company Class A common stock held by a Managing Director will become transferable, in each case in three equal installments on each of the fourth, fifth and sixth anniversary of this offering. If a Managing Director terminates his or her employment with the Company prior to the end of the lock-up period, the Company will be entitled to extend the lock-up period until up to the tenth anniversary of this offering. Group LP Class A partnership units and Moelis & Company Class A common stock held by our non-Managing Director employees and other existing Group LP unitholders are generally subject to lock-up agreements under which 50% of such securities will become transferable 180 days after the date of this prospectus and the remainder of such securities will become transferable following the one year anniversary of the consummation of this offering. |

|

Stockholders Agreement |

In connection with the completion of this offering, Moelis & Company will enter into a stockholders agreement with Partner Holdings pursuant to which, for so long as the Class B Condition is satisfied, Partner Holdings will have certain approval rights. |

|

|

After the Class B Condition ceases to be satisfied, for so long as the Secondary Class B Condition is satisfied, Partner Holdings will have certain more limited approval rights. |

|

|

See "Organizational Structure—Rights of Partner Holdings and Stockholders Agreement." |

|

Registration Rights |

In connection with the completion of this offering, Moelis & Company will grant registration rights pursuant to which: |

|

|

• Moelis & Company will be required to use its reasonable best efforts to file a shelf registration statement within six months of the consummation of this offering, providing for the exchange of Group LP Class A partnership units |

|

|

12

|

held by certain Group LP non-Managing Director Class A unitholders for an equivalent number of shares of its Class A common stock and the resale of shares of Class A common stock held by certain non-Managing Directors at any time and from time to time thereafter, subject to applicable restrictions imposed by Moelis & Company; |

|

|

• Moelis & Company will be required to use its reasonable best efforts to file a shelf registration statement within three months of the expiration of the lock-up period relating to our Managing Directors described above, providing for the exchange of Group LP Class A partnership units held by such Managing Directors for an equivalent number of shares of Moelis & Company Class A common stock and the resale of shares of Moelis & Company Class A common stock by our Managing Directors at any time and from time to time, subject to applicable restrictions imposed by Moelis & Company; |

|

|

• certain Group LP Class A unitholders will have the ability to cause Moelis & Company to register the shares of its Class A common stock they could acquire upon exchange of their Group LP Class A partnership units, subject to certain contractual restrictions; and |

|

|

• certain Group LP Class A unitholders will have the ability to cause Moelis & Company to register the shares of its Class A common stock they could acquire upon exchange of their Group LP Class A partnership units, subject to certain contractual restrictions, in any public underwritten offerings by Moelis & Company after the expiration or earlier termination (if any) of the lock-up agreements referred to above, subject to customary pro rata cutbacks. |

|

|

See "Organizational Structure—Registration Rights." |

|

Board Representation |

Our board of directors will nominate individuals designated by Partner Holdings equal to a majority of the board of directors, for so long as the Class B Condition is satisfied. See "Organizational Structure—Rights of Partner Holdings and Stockholders Agreement." |

|

Dividend Policy |

Following this offering and subject to applicable law, we intend to pay a quarterly cash dividend initially equal to $0.17 per share of Class A common stock, commencing with the third quarter of 2014. Any declaration and payment of future dividends to holders of our Class A common stock will be at the sole discretion of our board of directors and will depend on many factors, including our financial condition, earnings, cash flows, capital requirements, level of indebtedness, statutory and contractual restrictions applicable to the payment of dividends and other considerations that our board of directors deems relevant. See "Dividend Policy." |

|

|

13

Conflicts of Interest |

Moelis & Company controls Moelis & Company LLC, a participating underwriter in this offering. Therefore, Moelis & Company LLC is deemed to have a "conflict of interest" within the meaning of Financial Industry Regulatory Authority, Inc. ("FINRA") Rule 5121(f)(5)(B). In addition, Moelis & Company and other affiliates of Moelis & Company LLC will be deemed to receive more than 5% of net offering proceeds and will have a "conflict of interest" pursuant to FINRA Rule 5121(f)(5)(C)(ii). This offering is being made in compliance with the requirements of FINRA Rule 5121. Since Moelis & Company LLC is not primarily responsible for managing this offering, pursuant to FINRA Rule 5121(a)(1)(A), the appointment of a qualified independent underwriter is not necessary. Moelis & Company LLC will not confirm sales to discretionary accounts without the prior written approval of the customer. See "Underwriting." |

|

Risk Factors |

See "Risk Factors" for a discussion of risks you should carefully consider before investing in our Class A common stock. |

|

Proposed New York Stock Exchange Trading Symbol |

"MC." |

The number of shares of our Class A common stock to be outstanding after this offering is based on 7,855,804 shares of our Class A common stock outstanding immediately prior to completion of this offering. This number excludes 39,210,693 shares of Class A common stock issuable in exchange for Group LP Class A partnership units and upon conversion of shares of our Class B common stock, each as described under "Organizational Structure—Amended and Restated Limited Partnership Agreement of Group LP—Exchange Rights." If all outstanding Group LP Class A partnership units were exchanged and all outstanding shares of Class B common stock were converted, we would have 54,366,497 shares of Class A common stock outstanding immediately after this offering.

The number of shares of Class A common stock to be outstanding after this offering:

- •

- excludes shares of Class A common stock reserved for issuance under our 2014 Omnibus Incentive Plan described in

"Executive Compensation—Moelis & Company 2014 Omnibus Incentive Plan," including 3,332,968 shares issuable upon outstanding options with an exercise price equal to the initial

public offering price for this offering and 1,877,715 shares issuable upon settlement of restricted stock units outstanding immediately prior to completion of this offering;

- •

- excludes 160,150 unvested restricted shares of our Class A common stock held by certain employees, which are

treated by us as equivalents of restricted stock units; and

- •

- includes 280,490 shares of our Class A Common stock issuable upon exercise of nil-strike options held by certain non-U.S. employees.

Unless otherwise indicated, the information in this prospectus assumes the following:

- •

- the filing of our amended and restated certificate of incorporation and the adoption of our amended and restated bylaws,

forms of which are filed as exhibits to the registration statement of which this prospectus forms a part, which will occur immediately prior to the closing of this offering;

- •

- an initial public offering price of $27.50 per share of Class A common stock, which is the mid-point of

the estimated initial public offering price range set forth on the cover page of this prospectus; and

- •

- no exercise by the underwriters of their option to purchase additional shares.

14

Summary Historical Financial and Other Data

The summary historical financial and operating data as of December 31, 2013 and 2012 and for the years ended December 31, 2013, 2012 and 2011 presented below have been derived from our audited combined financial statements included elsewhere in this prospectus.

The summary historical financial data as of December 31, 2011 presented below have been derived from our audited combined financial statements which are not included in this prospectus.

You should read the summary historical financial and operating data set forth below in conjunction with the sections entitled "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our combined financial statements and notes thereto included elsewhere in this prospectus.

| |

Year Ended December 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| ($ in thousands) |

2013 | 2012 | 2011 | |||||||

Statement of Operations Data |

||||||||||

Revenues |

$ | 411,386 | $ | 385,871 | $ | 268,024 | ||||

Expenses: |

||||||||||

Compensation and benefits |

264,944 | 274,941 | 200,368 | |||||||

Non-compensation expenses |

76,333 | 72,885 | 78,526 | |||||||

| | | | | | | | | | | |

Total operating expenses |

341,277 | 347,826 | 278,894 | |||||||

Operating income (loss) |

70,109 | 38,045 | (10,870 | ) | ||||||

Other income and expenses |

(771 | ) | 333 | 245 | ||||||

Income (loss) from equity method investment |

3,681 | (658 | ) | 5,737 | ||||||

| | | | | | | | | | | |

Income (loss) before income taxes |

73,019 | 37,720 | (4,888 | ) | ||||||

Provision for income taxes |

2,794 | 2,498 | 3,642 | |||||||

| | | | | | | | | | | |

Net income (loss) |

$ | 70,225 | $ | 35,222 | $ | (8,530 | ) | |||

| | | | | | | | | | | |

| | | | | | | | | | | |

Statement of Financial Condition Data (period end) |

||||||||||

Total assets |

$ | 443,463 | $ | 402,668 | $ | 204,929 | ||||

Total liabilities |

134,093 | 142,560 | 92,754 | |||||||

Equity |

309,370 | 260,108 | 112,175 | |||||||

Other Data and Metrics |

||||||||||

Bankers at period-end |

317 | 340 | 335 | |||||||

Managing Directors at period-end |

86 | 80 | 76 | |||||||

Number of fee-paying clients |

263 | 236 | 182 | |||||||

Number of fee-paying clients ³ $1M |

109 | 107 | 72 | |||||||

% of total revenues from top 10 transactions |

23 | % | 22 | % | 34 | % | ||||

15

Investing in our Class A common stock involves a high degree of risk. You should carefully consider the following risks and all other information contained in this prospectus, including our financial statements and the related notes thereto, before investing in our Class A common stock. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, also may become important factors that affect us. If any of the following risks materialize, our business, financial condition and results of operations could be materially adversely affected. In that case, the trading price of our Class A common stock could decline, and you may lose some or all of your investment.

Risks Related to Our Business

Our future growth will depend on, among other things, our ability to successfully identify, recruit and develop talent and will require us to commit additional resources.

We have experienced rapid growth over the past several years, which may be difficult to sustain at the same rate. Our future growth will depend on, among other things, our ability to successfully identify and recruit individuals and teams to join our firm. It typically takes time for these professionals to become profitable and effective. During that time, we may incur significant expenses and expend significant time and resources toward training, integration and business development aimed at developing this new talent. If we are unable to recruit and develop profitable professionals, we will not be able to implement our growth strategy and our financial results could be materially adversely affected.

In addition, sustaining growth will require us to commit additional management, operational and financial resources and to maintain appropriate operational and financial systems to adequately support expansion, especially in instances where we open new offices that may require additional resources before they become profitable. See "—Our growth strategy may involve opening or acquiring new offices and expanding internationally and would involve hiring new Managing Directors and other senior professionals for these offices, which would require substantial investment by us and could materially and adversely affect our operating results." There can be no assurance that we will be able to manage our expanding operations effectively, and any failure to do so could materially adversely affect our ability to grow revenue and control our expenses.

Changing market conditions can adversely affect our business in many ways, including by reducing the volume of the transactions involving our business, which could materially reduce our revenue.

As a financial services firm, we are materially affected by conditions in the global financial markets and economic conditions throughout the world. For example, our revenue is directly related to the volume and value of the transactions in which we are involved. During periods of unfavorable market or economic conditions, the volume and value of M&A transactions may decrease, thereby reducing the demand for our M&A advisory services and increasing price competition among financial services companies seeking such engagements. In addition, during periods of strong market and economic conditions, the volume and value of recapitalization and restructuring transactions may decrease, thereby reducing the demand for our recapitalization and restructuring advisory services and increasing price competition among financial services companies seeking such engagements. Our results of operations would be adversely affected by any such reduction in the volume or value of such advisory transactions. Further, in the period following an economic downturn, the volume and value of M&A transactions typically takes time to recover and lags a recovery in market and economic conditions.

Our profitability may also be adversely affected by our fixed costs and the possibility that we would be unable to scale back other costs within a time frame sufficient to match any decreases in revenue relating to changes in market and economic conditions. The future market and economic climate may

16

deteriorate because of many factors beyond our control, including rising interest rates or inflation, terrorism or political uncertainty.

Our revenue in any given period is dependent on the number of fee-paying clients in such period, and a significant reduction in the number of fee-paying clients in any given period could reduce our revenue and adversely affect our operating results in such period.

Our revenue in any given period is dependent on the number of fee-paying clients in such period. We had 109 clients and 107 clients paying fees equal to or greater than $1 million in 2013 and 2012, respectively. We may lose clients as a result of the sale or merger of a client, a change in a client's senior management, competition from other financial advisors and financial institutions and other causes. A significant reduction in the number of fee-paying clients in any given period could reduce our revenue and adversely affect our operating results in such period.

Our ability to retain our Managing Directors and our other professionals, including our executive officers, is critical to the success of our business.

Our future success depends to a substantial degree on our ability to retain qualified professionals within our organization, including our Managing Directors. However, we may not be successful in our efforts to retain the required personnel as the market for qualified investment bankers is extremely competitive. Our investment bankers possess substantial experience and expertise and have strong relationships with our advisory clients. As a result, the loss of these professionals could jeopardize our relationships with clients and result in the loss of client engagements. For example, if any of our Managing Directors or other senior professionals, including our executive officers, or groups of professionals, were to join or form a competing firm, some of our current clients could choose to use the services of that competitor rather than our services. There is no guarantee that our compensation and non-competition arrangements with our Managing Directors provide sufficient incentives or protections to prevent our Managing Directors from resigning to join our competitors. In addition, some of our competitors have more resources than us which may allow them to attract some of our existing employees through compensation or otherwise. The departure of a number of Managing Directors or groups of professionals could have a material adverse effect on our business and our profitability.

We depend on the efforts and reputations of Mr. Moelis and our other executive officers. Our senior leadership team's reputations and relationships with clients and potential clients are critical elements in the success of our business. The loss of the services of any of them, in particular Mr. Moelis, could have a material adverse effect on our business, including our ability to attract clients.

Substantially all of our revenue is derived from advisory fees. As a result, our revenue and profits are highly volatile on a quarterly basis and may cause the price of our Class A common stock to fluctuate and decline.

Our revenue and profits are highly volatile. We derive substantially all of our revenue from advisory fees, generally from a limited number of engagements that generate significant fees at key transaction milestones, such as closing, the timing of which is outside of our control. We expect that we will continue to rely on advisory fees for most of our revenue for the foreseeable future. Accordingly, a decline in our advisory engagements or the market for advisory services would adversely affect our business. In addition, our financial results will likely fluctuate from quarter to quarter based on the timing of when fees are earned, and high levels of revenue in one quarter will not necessarily be predictive of continued high levels of revenue in future periods. Because we lack other, more stable, sources of revenue, which could moderate some of the volatility in our advisory revenue, we may experience greater variations in our revenue and profits than other larger, more diversified competitors in the financial services industry. Fluctuations in our quarterly financial results could, in turn, lead to

17

large adverse movements in the price of our Class A common stock or increased volatility in our stock price generally.

Because in many cases we are not paid until the successful consummation of the underlying transaction, our revenue is highly dependent on market conditions and the decisions and actions of our clients, interested third parties and governmental authorities. For example, we may be engaged by a client in connection with a sale or divestiture, but the transaction may not occur or be consummated because, among other things, anticipated bidders may not materialize, no bidder is prepared to pay our client's price or because our client's business experiences unexpected operating or financial problems. We may be engaged by a client in connection with an acquisition, but the transaction may not occur or be consummated for a number of reasons, including because our client may not be the winning bidder, failure to agree upon final terms with the counterparty, failure to obtain necessary regulatory consents or board or stockholder approvals, failure to secure necessary financing, adverse market conditions or because the target's business experiences unexpected operating or financial problems. In these circumstances, we often do not receive significant advisory fees, despite the fact that we have devoted considerable resources to these transactions.

In addition, we face the risk that certain clients may not have the financial resources to pay our agreed-upon advisory fees. Certain clients may also be unwilling to pay our advisory fees in whole or in part, in which case we may have to incur significant costs to bring legal action to enforce our engagement agreement to obtain our advisory fees.

Our joint ventures, strategic investments and acquisitions may result in additional risks and uncertainties in our business.

In addition to recruiting and internal expansion, we may grow our core business through joint ventures, strategic investments or acquisitions.

In the case of joint ventures, such as our 50% investment in our Australian joint venture, Moelis Australia Holdings Pty Ltd (the "Australian JV"), we are subject to additional risks and uncertainties relating to governance and controls, in that we may be dependent upon, and subject to, liability, losses or reputational damage relating to personnel, controls and systems that are not fully under our control. In addition, disagreements between us and our joint venture partners may negatively impact our business. Although our Australian JV must abide by certain market risk limits approved by us with respect to its trading activities, there is a risk that such limits will be insufficient to protect us against significant losses. In addition, investments made by our Australian JV could be unprofitable.

In the event we make further strategic investments or acquisitions, we would face numerous risks and would be presented with financial, managerial and operational challenges, including the difficulty of integrating personnel, financial, accounting, technology and other systems and management controls.

If the number of debt defaults, bankruptcies or other factors affecting demand for our recapitalization and restructuring advisory services declines, our recapitalization and restructuring business could suffer.

We provide various financial recapitalization and restructuring and related advice to companies in financial distress or to their creditors or other stakeholders. A number of factors affect demand for these advisory services, including general economic conditions, the availability and cost of debt and equity financing, governmental policy and changes to laws, rules and regulations, including those that protect creditors. In addition, providing recapitalization and restructuring advisory services entails the risk that the transaction will be unsuccessful, takes considerable time and can be subject to a bankruptcy court's discretionary power to disallow or discount our fees. If the number of debt defaults, bankruptcies or other factors affecting demand for our recapitalization and restructuring advisory services declines, our recapitalization and restructuring business would be adversely affected.

18

Our failure to deal appropriately with actual, potential or perceived conflicts of interest could damage our reputation and materially adversely affect our business.

We confront actual, potential or perceived conflicts of interest in our business. For instance, we face the possibility of an actual, potential or perceived conflict of interest where we represent a client on a transaction in which an existing client is a party. We may be asked by two potential clients to act on their behalf on the same transaction, including two clients as potential buyers in the same acquisition transaction, and we may act for both clients if both clients agree to us doing so. In each of these situations, we face the risk that our current policies, controls and procedures do not timely identify or appropriately manage such conflicts of interest.

It is possible that actual, potential or perceived conflicts could give rise to client dissatisfaction, litigation or regulatory enforcement actions. Appropriately identifying and managing actual or perceived conflicts of interest is complex and difficult, and our reputation could be damaged if we fail, or appear to fail, to deal appropriately with one or more potential or actual conflicts of interest. Regulatory scrutiny of, or litigation in connection with, conflicts of interest could have a material adverse effect on our reputation which could materially adversely affect our business in a number of ways, including a reluctance of some potential clients and counterparties to do business with us.

Employee misconduct, which is difficult to detect and deter, could harm us by impairing our ability to attract and retain clients and by subjecting us to legal liability and reputational harm.

There is a risk that our employees could engage in misconduct that would adversely affect our business. For example, our business often requires that we deal with confidential matters of great significance to our clients. If our employees were to improperly use or disclose confidential information provided by our clients, we could be subject to regulatory sanctions and suffer serious harm to our reputation, financial position, current client relationships and ability to attract future clients. It is not always possible to deter employee misconduct, and the precautions we take to detect and prevent misconduct may not be effective in all cases. If our employees engage in misconduct, our business could be materially adversely affected.

We may face damage to our professional reputation if our services are not regarded as satisfactory or for other reasons.

As an advisory service firm, we depend to a large extent on our relationships with our clients and reputation for integrity and high-caliber professional services to attract and retain clients. As a result, if a client is not satisfied with our services, it may be more damaging in our business than in other businesses.

We face strong competition from other financial advisory firms, many of which have the ability to offer clients a wider range of products and services than those we can offer, which could cause us to fail to win advisory mandates and subject us to pricing pressures that could materially adversely affect our revenue and profitability.

The financial services industry is intensely competitive, and we expect it to remain so. Our competitors are other investment banking and financial advisory firms. We compete on both a global and a regional basis, and on the basis of a number of factors, including depth of client relationships, industry knowledge, transaction execution skills, our range of products and services, innovation, reputation and price. In addition, in our business there are usually no long-term contracted sources of revenue. Each revenue-generating engagement typically is separately solicited, awarded and negotiated.

We have experienced intense competition over obtaining advisory mandates in recent years, and we may experience further pricing pressures in our business in the future as some of our competitors may seek to obtain increased market share by reducing fees.

19

Our primary competitors are large financial institutions, many of which have far greater financial and other resources than us and, unlike us, have the ability to offer a wider range of products, from loans, deposit taking and insurance to brokerage and trading, which may enhance their competitive position. They also regularly support investment banking, including financial advisory services, with commercial lending and other financial services and products in an effort to gain market share, which puts us at a competitive disadvantage and could result in pricing pressures or loss of opportunities, which could materially adversely affect our revenue and profitability. In addition, we may be at a competitive disadvantage with regard to certain of our competitors who are able to and often do, provide financing or market making services that are often a crucial component of the types of transactions on which we advise.

In addition to our larger competitors, over the last few years a number of independent investment banks that offer independent advisory services have emerged, with several showing rapid growth. As these independent firms or new entrants into the market seek to gain market share there could be pricing pressures, which would adversely affect our revenues and earnings.

As a member of the financial services industry, we face substantial litigation risks.

Our role as advisor to our clients on important transactions involves complex analysis and the exercise of professional judgment, including rendering "fairness opinions" in connection with mergers and other transactions. Our activities may subject us to the risk of significant legal liabilities to our clients and affected third parties, including shareholders of our clients who could bring securities class actions against us. In recent years, the volume of claims and amount of damages claimed in litigation and regulatory proceedings against financial services companies have been increasing. These risks often may be difficult to assess or quantify and their existence and magnitude often remain unknown for substantial periods of time. Our engagements typically include broad indemnities from our clients and provisions to limit our exposure to legal claims relating to our services, but these provisions may not protect us in all cases, including when a client does not have the financial capacity to pay under the indemnity. As a result, we may incur significant legal expenses in defending against or settling litigation. In addition, we may have to spend a significant amount to adequately insure against these potential claims. Substantial legal liability or significant regulatory action against us could have material adverse financial effects or cause significant reputational harm to us, which could seriously harm our business prospects.

Our management has not previously managed a public company.

Our management team has historically operated our business as a privately-owned company. The individuals who now constitute our management have not previously managed a publicly traded company.

Compliance with public company requirements will place significant additional demands on our management and will require us to enhance our investor relations, legal, financial reporting and corporate communications functions. These additional efforts may strain our resources and divert management's attention from other business concerns, which could adversely affect our business and profitability.

In addition, the reorganization to take place in connection with the consummation of this offering will involve separating our advisory business from the asset management business of Old Holdings. These two businesses have historically utilized common management and operational structures, including facilities and technology platforms as well as legal, compliance, marketing and other support personnel and senior management oversight. The process of separating these businesses, and of operating our advisory business on a stand-alone basis, may result in increased costs and inefficiencies

20

and other impediments to the regular operations of our business, the occurrence of any of which could adversely affect our business and profitability.

Extensive and evolving regulation of our business and the business of our clients exposes us to the potential for significant penalties and fines due to compliance failures, increases our costs and may result in limitations on the manner in which our business is conducted.

As a participant in the financial services industry, we are subject to extensive regulation in the U.S. and internationally. We are subject to regulation by governmental and self-regulatory organizations in the jurisdictions in which we operate. As a result of market volatility and disruption in recent years, the U.S. and other governments have taken unprecedented steps to try to stabilize the financial system including providing assistance to financial institutions and taking certain regulatory actions. The full extent of the effects of these actions and of legislative and regulatory initiatives (including the Dodd-Frank Wall Street Reform and Consumer Protection Act) effected in connection with, and as a result of, such extraordinary disruption and volatility is uncertain, both as to the financial markets and participants in general, and as to us in particular.

Our ability to conduct business and our operating results, including compliance costs, may be adversely affected as a result of any new requirements imposed by the Securities and Exchange Commission ("SEC"), FINRA or other U.S. or foreign governmental regulatory authorities or self-regulatory organizations that regulate financial services firms or supervise financial markets. We may be adversely affected by changes in the interpretation or enforcement of existing laws and rules by these governmental authorities and self-regulatory organizations. In addition, some of our clients or prospective clients may adopt policies that exceed regulatory requirements and impose additional restrictions affecting their dealings with us. Accordingly, we may incur significant costs to comply with U.S. and international regulation. In addition, new laws or regulations or changes in enforcement of existing laws or regulations applicable to our clients may adversely affect our business. For example, changes in antitrust enforcement could affect the level of M&A activity and changes in applicable regulations could restrict the activities of our clients and their need for the types of advisory services that we provide to them.

Our failure to comply with applicable laws or regulations could result in adverse publicity and reputational harm as well as fines, suspensions of personnel or other sanctions, including revocation of the registration of us or any of our subsidiaries as a financial advisor and could impair executive retention or recruitment. In addition, any changes in the regulatory framework could impose additional expenses or capital requirements on us, result in limitations on the manner in which our business is conducted, have an adverse impact upon our financial condition and business and require substantial attention by senior management. In addition, our business is subject to periodic examination by various regulatory authorities, and we cannot predict the outcome of any such examinations.

Our business is subject to various operational risks.

We face various operational risks related to our business on a day-to-day basis. We rely heavily on financial, accounting, communication and other information technology systems, and the people who operate them. These systems, including the systems of third parties on whom we rely, may fail to operate properly or become disabled as a result of tampering or a breach of our network security systems or otherwise, including for reasons beyond our control.

Our clients typically provide us with sensitive and confidential information. We are dependent on information technology networks and systems to securely process, transmit and store such information and to communicate among our locations around the world and with our clients, alliance partners and vendors. We may be subject to attempted security breaches and cyber-attacks and, while none have had a material impact to date, a successful breach could lead to shutdowns or disruptions of our systems or

21

third-party systems on which we rely and potential unauthorized disclosure of sensitive or confidential information. Breaches of our or third-party network security systems on which we rely could involve attacks that are intended to obtain unauthorized access to our proprietary information, destroy data or disable, degrade or sabotage our systems, often through the introduction of computer viruses, cyber-attacks and other means and could originate from a wide variety of sources, including unknown third parties outside the firm. Although we take various measures to ensure the integrity of our and third-party systems on which we rely, there can be no assurance that these measures will provide adequate protection. If our or third-party systems on which we rely are compromised, do not operate properly or are disabled, we could suffer a disruption of our business, financial losses, liability to clients, regulatory sanctions and damage to our reputation.

We operate a business that is highly dependent on information systems and technology. Any failure to keep accurate books and records can render us liable to disciplinary action by governmental and self-regulatory authorities, as well as to claims by our clients. We rely on third-party service providers for certain aspects of our business. Any interruption or deterioration in the performance of these third parties or failures of their information systems and technology could impair our operations, affect our reputation and adversely affect our business.

In addition, a disaster or other business continuity problem, such as a pandemic, other man-made or natural disaster or disruption involving electronic communications or other services used by us or third parties with whom we conduct business, could lead us to experience operational challenges, and our inability to timely and successfully recover could materially disrupt our business and cause material financial loss, regulatory actions, reputational harm or legal liability.