Attached files

| file | filename |

|---|---|

| EX-23.2 - EX-23.2 - Range Resources - Louisiana, Inc. | d658814dex232.htm |

| EX-99.3 - EX-99.3 - Range Resources - Louisiana, Inc. | d658814dex993.htm |

| EX-23.1 - EX-23.1 - Range Resources - Louisiana, Inc. | d658814dex231.htm |

Table of Contents

As filed with the Securities and Exchange Commission on April 4, 2014

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

MEMORIAL RESOURCE DEVELOPMENT CORP.

(Exact name of registrant as specified in its charter)

| Delaware | 1311 | 46-4710769 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

1301 McKinney Street, Suite 2100

Houston, Texas 77010

(713) 588-8300

(Address, including zip code, and telephone number, including area code, of registrants’ principal executive offices)

Kyle N. Roane

Vice President, General Counsel and Corporate Secretary

Memorial Resource Development Corp.

1301 McKinney Street, Suite 2100

Houston, Texas 77010

(713) 588-8300

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With copies to:

| John Goodgame Shar Ahmed Akin Gump Strauss Hauer & Feld LLP 1111 Louisiana Street, 44th Floor Houston, TX 77002 (713) 220-5800 |

Douglas E. McWilliams Vinson & Elkins L.L.P. 1001 Fannin, Suite 2500 Houston, TX 77002 (713) 758-2222 |

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of each class of securities to be registered |

Proposed maximum aggregate offering price(1)(2) |

Amount of registration fee | ||

| Common Stock, $0.01 par value per share |

$700,000,000 | $90,160 | ||

|

| ||||

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Includes shares issuable upon the underwriters’ exercise of its overallotment option. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED APRIL 4, 2014

PRELIMINARY PROSPECTUS

Shares

Memorial Resource Development Corp.

Common Stock

$ per share

This is our initial public offering. We are selling shares of common stock, and Memorial Resource Development LLC is selling shares of our common stock. We expect the public offering price to be between $ and $ per share. Memorial Resource Development LLC has granted the underwriters a 30-day option to purchase up to an additional shares of common stock. We will not receive any proceeds from the sale of shares by Memorial Resource Development LLC, including any shares that it may sell pursuant to the underwriters’ option to purchase additional shares of common stock.

Currently, no public market exists for our common stock. We intend to apply to list our common stock on the NASDAQ Global Market under the symbol “MRD.” Following the completion of this offering, we will be a “controlled company” as defined under the NASDAQ listing rules because the group consisting of affiliates of Natural Gas Partners will beneficially own over 50% of our shares of outstanding common stock. See “Principal and Selling Stockholders.”

Investing in our common stock involves risks that are described in the “Risk Factors” section beginning on page 24 of this prospectus.

We are an emerging growth company as that term is used in the Jumpstart Our Business Startups Act of 2012, and as such, we have elected to take advantage of certain reduced public company reporting requirements for this prospectus and future filings. See “Risk Factors” and “Summary—Emerging Growth Company Status.”

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||||

| Initial Public Offering Price |

$ | $ | ||||||

| Underwriting Discounts and Commissions |

$ | $ | ||||||

| Proceeds, Before Expenses, to Us |

$ | $ | ||||||

| Proceeds, Before Expenses, to Memorial Resource Development LLC |

$ | $ | ||||||

The underwriters expect to deliver the shares of common stock on or about , 2014.

Citigroup

The date of this prospectus is , 2014.

Table of Contents

[Inside cover art to be provided]

Table of Contents

| Page | ||||

| 1 | ||||

| 24 | ||||

| 50 | ||||

| 52 | ||||

| 53 | ||||

| 54 | ||||

| 55 | ||||

| 57 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

60 | |||

| 86 | ||||

| 120 | ||||

| 130 | ||||

| 132 | ||||

| 136 | ||||

| 140 | ||||

| 144 | ||||

| 146 | ||||

| 150 | ||||

| 155 | ||||

| 155 | ||||

| 156 | ||||

| F-1 | ||||

| A-1 | ||||

| B-1 | ||||

| B-14 | ||||

You should rely only on the information contained in this prospectus. Neither we, Memorial Resource Development LLC, nor the underwriters have authorized any person to provide you with any information or represent anything about us or this offering that is not contained in this prospectus. If given or made, any such other information or representation should not be relied upon as having been authorized by us. Neither we nor Memorial Resource Development LLC are making an offer in any jurisdiction where an offer or sale is not permitted. The information contained in this prospectus is current only as of its date.

i

Table of Contents

Commonly Used Defined Terms

As used in this prospectus, unless we indicate otherwise:

| • | “the Company,” “we,” “our,” “us” and “our company” or like terms refer collectively to (i) Memorial Resource Development Corp. and its subsidiaries (other than MEMP and its subsidiaries) for periods after the restructuring transactions described below and (ii) our predecessor (as described below) other than MEMP and its subsidiaries for periods prior to the restructuring transactions; |

| • | “Memorial Production Partners,” “MEMP” and “the Partnership” refer to Memorial Production Partners LP individually and collectively with its subsidiaries, as the context requires. Following the restructuring transactions described below, we will own the general partner of MEMP as well as 5,360,912 subordinated units representing an 8.7% limited partner interest in MEMP and 50% of MEMP’s incentive distribution rights; |

| • | “MEMP GP” refers to Memorial Production Partners GP LLC, the general partner of the Partnership, which we will own following completion of the restructuring transactions described below; |

| • | “MRD LLC” refers to Memorial Resource Development LLC, which has historically owned our predecessor’s business and will own shares of our common stock following completion of the restructuring transactions described below; |

| • | “WildHorse Resources” refers to WildHorse Resources, LLC and its subsidiaries, which owns our interest in the Terryville Complex and will be our 100% owned subsidiary following completion of the restructuring transactions described below; |

| • | “our predecessor” refers collectively to MRD LLC and its consolidated subsidiaries, consisting of Classic Hydrocarbons Holdings, L.P., Classic Hydrocarbons GP Co., L.L.C., Black Diamond Minerals, LLC, Beta Operating Company, LLC, MEMP GP, BlueStone, MRD Operating LLC, WildHorse Resources and each of their respective subsidiaries, including MEMP and its subsidiaries; |

| • | “the Funds” refers collectively to Natural Gas Partners VIII, L.P., Natural Gas Partners IX, L.P. and NGP IX Offshore Holdings, L.P., which collectively own MRD LLC; |

| • | “restructuring transactions” means the transactions described beginning on page 13 that will take place in connection with the closing of this offering and pursuant to which we will acquire assets of MRD LLC (not including its interests in BlueStone, MRD Royalty or MRD Midstream) that comprise substantially all of the assets of MRD LLC; |

| • | “BlueStone” refers to BlueStone Natural Resources Holdings, LLC, which sold substantially all of its assets in July 2013 for approximately $117.9 million; |

| • | “NGP” refers to Natural Gas Partners, a family of private equity investment funds organized to make direct equity investments in the energy industry, including the Funds; |

| • | “MRD Royalty” refers to MRD Royalty LLC, which owns certain immaterial leasehold interests and overriding royalty interests in Texas and Montana; and |

| • | “MRD Midstream” refers to MRD Midstream LLC, which owns an indirect interest in certain immaterial midstream assets in North Louisiana. |

Industry and Market Data

The market data and certain other statistical information used throughout this prospectus are based on independent industry publications, government publications or other published independent sources. Some data is also based on our good faith estimates. Although we believe these third-party sources are reliable and that the information is accurate and complete, neither we nor MRD LLC have independently verified the information.

Equivalency

This prospectus presents certain production and reserves-related information on an “equivalency” basis. When we refer to oil and natural gas in “equivalents,” we are doing so to compare quantities of oil with quantities of natural gas. In calculating equivalents, we use a generally recognized standard in which one Bbl of oil and/or NGLs is equivalent to six Mcf of natural gas. This calculation is based on an approximate energy equivalency and does not imply or reflect a value or price relationship.

ii

Table of Contents

This summary highlights information appearing elsewhere in this prospectus. You should read the entire prospectus carefully, including “Risk Factors” beginning on page 24 and the historical and pro forma financial statements and the related notes to those financial statements. Certain oil and gas industry terms, including the terms proved reserves, probable reserves and possible reserves, used in this prospectus are defined in the “Glossary of Oil and Natural Gas Terms” in Appendix A of this prospectus.

Because we control MEMP through our ownership of its general partner, we are required to consolidate MEMP for accounting and financial reporting purposes even though we only own a minority of its limited partner interests. Our financial statements include two reportable business segments: (i) the MRD Segment, which reflects all of our operations except for MEMP and its subsidiaries, and (ii) the MEMP Segment, which reflects the operations of MEMP and its subsidiaries. Except with respect to our consolidated and combined financial statements or as otherwise indicated, the description of our business, properties, strategies and other information in this summary does not include the business, properties or results of operations of BlueStone, MRD Royalty, MRD Midstream (the assets of which are included in our predecessor but will not be conveyed to us in the restructuring transactions) or MEMP. Our proved reserves as of December 31, 2013 have been prepared by Netherland, Sewell & Associates, Inc., our independent reserve engineers (“NSAI”), and our probable and possible reserves as of December 31, 2013 have been prepared by our internal reserve engineers and audited by NSAI, all of which are reflected in our reserve reports (which we collectively refer to as our “reserve report”), summaries of which are included in Appendices B-1 and B-2 of this prospectus.

Information expressed on a pro forma basis in this summary gives effect to certain transactions as if they had occurred on December 31, 2013 for pro forma balance sheet purposes and on January 1, 2013 for pro forma statements of operations purposes. For a description of these transactions, please read “Summary Historical Consolidated and Combined Pro Forma Financial Data” and “—Our Structure and Restructuring Transactions.” Where applicable, we have assumed an initial public offering price of per share, the midpoint of the price range set forth on the cover page of this prospectus.

Overview

We are an independent natural gas and oil company focused on the exploitation, development, and acquisition of natural gas, NGL and oil properties with a majority of our activity in the Terryville Complex of North Louisiana, where we are targeting overpressured, liquids-rich natural gas opportunities in multiple zones in the Cotton Valley formation. Our total leasehold position is 347,458 gross (205,818 net) acres, of which 60,041 gross (51,522 net) acres are in what we believe to be the core of the Terryville Complex. We are focused on creating shareholder value primarily through the development of our sizeable horizontal inventory. As of December 31, 2013, we had 1,297 gross (892 net) identified horizontal drilling locations, of which over 1,146 gross (796 net) identified horizontal drilling locations are located in the Terryville Complex. These total net identified horizontal drilling locations represent an inventory of over 26 years based on our expected 2014 drilling program. We believe our inventory to be repeatable and capable of generating high returns based on the extensive production history in the area, the results of our horizontal wells drilled to date, and the consistent reservoir quality across multiple target formations.

As of December 31, 2013, we had estimated proved, probable and possible reserves of approximately 1,126 Bcfe, 800 Bcfe and 1,034 Bcfe, respectively. As of such date, we operated 98% of our proved reserves, 71% of which were natural gas. For the three months ended December 31, 2013, 45% of our pro forma MRD Segment revenues were attributable to natural gas production, 28% to NGLs and 27% to oil. For the year ended December 31, 2013, we generated pro forma MRD Segment Adjusted EBITDA of $173 million and pro forma net income of $ million, and made pro forma total capital expenditures of $204 million, including $70 million

1

Table of Contents

for wells coming online in 2014. Please see “—Summary Historical Consolidated and Combined Pro Forma Financial Data—Adjusted EBITDA” for an explanation of the basis for the pro forma presentation and our use of Adjusted EBITDA to measure the MRD Segment’s profitability.

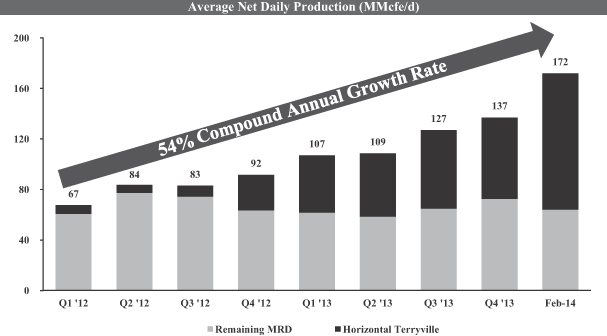

Our average net daily production for the three months ended December 31, 2013 was 137 MMcfe/d (approximately 70% natural gas, 22% NGLs and 8% oil) and our reserve life was 23 years. As of December 31, 2013, we produced from 95 horizontal wells and 800 vertical wells. The Terryville Complex represented 83% of our total net production for the three months ended December 31, 2013. Our estimated average net daily production for the period from February 1 through February 28, 2014 was 172 MMcfe/d, of which 69% was from natural gas. Our estimated average net daily production from our properties in the Terryville Complex for the same period was 150 MMcfe/d, or 87% of our total production. In the Terryville Complex, we completed and brought online two additional horizontal wells during the first quarter of 2014, bringing our total number of producing horizontal wells to 23 in our primary formations. The 30-day initial production rates of our two most recent wells averaged 15.9 MMcfe/d, which compares to an average 30-day initial production rate of 15.1 MMcfe/d for all of our Terryville Complex horizontal wells drilled to date.

The following chart provides information regarding our production growth and the increasing proportion of our horizontal well production since the beginning of 2012.

Our Properties

Cotton Valley—Overview

The Cotton Valley formation extends across East Texas, North Louisiana and Southern Arkansas. The formation has been under development since the 1930s and is characterized by thick, multi-zone natural gas and oil reservoirs with well-known geologic characteristics and long-lived, predictable production profiles. Over 21,000 vertical wells have been completed throughout the play. In 2005, operators started redeveloping the

2

Table of Contents

Cotton Valley using horizontal drilling and advanced hydraulic fracturing techniques. To date, operators have drilled over 600 horizontal Cotton Valley wells. Some large, analogous redevelopment projects in the Cotton Valley include the Nan-Su-Gail Field in Freestone County, East Texas, where over 40 horizontal wells have been drilled by operators such as Devon Energy Corporation and Marathon Oil Corporation, and the Carthage Complex in Panola County, East Texas, where operators such as ExxonMobil Corporation, ConocoPhillips and Anadarko Petroleum Corporation have drilled over 153 horizontal wells.

Cotton Valley—Terryville Complex Horizontal Redevelopment

We are currently engaged in the horizontal redevelopment of the Terryville Complex in Lincoln Parish, Louisiana utilizing horizontal drilling and completion techniques similar to those employed at the Nan-Su-Gail Field, Carthage Complex in East Texas and other major resource plays across the United States. We have assembled a largely contiguous acreage position in the Terryville Complex of approximately 60,041 gross (51,522 net) acres as of December 31, 2013. The majority of our current and planned development is focused in and around what we believe to be the core of the Terryville Complex.

We entered the Terryville Complex via an acquisition from Petrohawk Energy Corporation in April 2010, with the goal of redeveloping the field with horizontal drilling and modern completion techniques. Since that acquisition, we have completed multiple bolt-on acquisitions and in-fill leases to build our current position. We believe the Terryville Complex, which has been producing since 1954, is one of North America’s most prolific natural gas fields, characterized by high recoveries relative to drilling and completion costs, high initial production rates with high liquids yields, long reserve life, multiple stacked producing zones, available infrastructure and a large number of service providers.

After initially drilling eight vertical pilot wells in the Terryville Complex, we commenced a horizontal drilling program in 2011 to further delineate and define our position. In 2013, we shifted our operational focus to full-scale horizontal redevelopment of the Terryville Complex, going from two rigs to four rigs by the end of that year. Additionally, in the fourth quarter of 2013, we moved to drilling on multi-well pads that allow us to more efficiently drill wells and control costs as we develop our stacked pay zones. We intend to dedicate approximately $264 million of our $316 million drilling and completion budget in 2014 to develop multiple zones within the Terryville Complex, where we expect to drill and complete 35 gross (30 net) wells. Our horizontal redevelopment program in the Terryville Complex will be focused on increasing our well performance and recoveries.

Within the Terryville Complex, as of December 31, 2013, we had 945 Bcfe, 688 Bcfe and 966 Bcfe of estimated proved, probable and possible reserves, respectively, and a drilling inventory consisting of 1,146 gross (796 net) identified horizontal drilling locations, including 91 gross (72 net) drilling locations to which we have attributed proved undeveloped reserves as of December 31, 2013. Since initiating our horizontal drilling program in 2011, we have drilled 23 gross (18.4 net) horizontal wells, growing our gross daily production in the Terryville Complex by 294% from 53.0 MMcfe/d for the three months ended March 31, 2010 to 208.6 MMcfe/d for the month ended February 28, 2014. For the three months ended December 31, 2013, 42% of our revenues from the Terryville Complex were attributable to natural gas, 29% to NGLs and 29% to oil. Within the Terryville Complex, on a proved reserves basis, we operate approximately 99% of our existing acreage and hold an average working interest of approximately 74% across our acreage. Our high operating control allows us to more efficiently and economically manage the redevelopment of this extensive resource.

We believe seismic data, as well as information gathered from the results of our existing 275 vertical and 23 horizontal wells throughout the field, support the existence of at least ten stacked pay zones across the Terryville Complex. Our redevelopment program currently targets four of the stacked pay zones in the Cotton Valley formation—zones we term the Upper Red, Lower Red, Lower Deep Pink and Upper Deep Pink, all of which we

3

Table of Contents

are developing with horizontal wells through pad drilling. These four zones have an overall thickness ranging from 400 to 890 feet across our acreage position. We believe the overpressured nature of this section of the Cotton Valley formation is highly productive when accessed through horizontal drilling and fracture stimulation technologies. These qualities, when combined with the liquids-rich nature of the natural gas, high initial rates of production and competitive well costs, produce what we believe to be amongst the highest rate of return wells in the nation.

The table below details certain information on estimated ultimate recoveries and production for the 23 horizontal wells currently producing in the Terryville Complex. Our well results have shown consistency in initial production, decline rates and estimated ultimate recovery. The consistency of these results gives us confidence that the full-scale redevelopment of the Terryville Complex we began in 2013 will be successful as we move from four to five rigs in 2014. Please see “Business—Our Properties—Cotton Valley—Terryville Complex Horizontal Redevelopment” for more detail on our properties in the Terryville Complex and the table on page 92 for more detail on the average EUR and cumulative production of our properties in the Terryville Complex.

| Lateral Length (Feet) |

Producing Wells | First Production |

Days Producing |

Cumulative Production (Bcfe) |

Gross Wellhead Flow Rates After Processing (MMcfe/d) (3)(4) |

D&C ($MM) |

||||||||||||||||||||||||||||||||||||||

| Well Name (1) |

EUR Bcfe(2) |

EUR Bcfe/ 1,000’ |

0-30 | 0-90 | 91-180 | 181-360 | ||||||||||||||||||||||||||||||||||||||

| Upper Red Zone |

||||||||||||||||||||||||||||||||||||||||||||

| LD Barnett 23H-2 |

4,015 | 13.6 | 3.4 | 1/30/12 | 761 | 4.2 | 14.5 | 12.0 | 7.7 | 5.5 | 6.7 | |||||||||||||||||||||||||||||||||

| Colquitt 20 17H-1 |

4,357 | 11.2 | 2.6 | 7/30/12 | 579 | 3.6 | 17.5 | 12.6 | 7.2 | 5.1 | 7.7 | |||||||||||||||||||||||||||||||||

| Dowling 22 15H-1 |

5,376 | 16.8 | 3.1 | 9/22/12 | 525 | 4.8 | 16.3 | 15.6 | 11.1 | 8.2 | 8.8 | |||||||||||||||||||||||||||||||||

| Nobles 13H-1 |

4,216 | 11.6 | 2.8 | 11/17/12 | 469 | 3.9 | 21.5 | 16.7 | 9.9 | 6.5 | 7.8 | |||||||||||||||||||||||||||||||||

| Sidney McCullin 16 21H-1 |

4,604 | 16.9 | 3.7 | 1/19/13 | 406 | 4.1 | 17.4 | 14.2 | 10.8 | 8.2 | 8.1 | |||||||||||||||||||||||||||||||||

| Wright 14 11 HC-1 |

5,250 | 18.0 | 3.4 | 5/27/13 | 278 | 4.0 | 19.6 | 18.1 | 16.1 | 8.8 | ||||||||||||||||||||||||||||||||||

| BF Fallin 22 15H-1 |

5,122 | 15.6 | 3.0 | 6/17/13 | 257 | 2.8 | 14.8 | 13.7 | 11.8 | 7.5 | ||||||||||||||||||||||||||||||||||

| Dowling 20 17H-1 |

4,327 | 8.9 | 2.1 | 7/22/13 | 222 | 1.7 | 15.2 | 11.0 | 5.6 | 10.7 | ||||||||||||||||||||||||||||||||||

| Gleason 31H-1 |

3,692 | 2.5 | 0.7 | 8/12/13 | 201 | 0.4 | 3.5 | 2.7 | 1.8 | 9.4 | ||||||||||||||||||||||||||||||||||

| Burnett 26H-1 |

2,405 | 4.2 | 1.7 | 9/22/13 | 160 | 0.7 | 6.9 | 5.5 | 6.6 | |||||||||||||||||||||||||||||||||||

| Drewett 17 8H-1 |

4,010 | 14.0 | 3.5 | 11/13/13 | 108 | 1.9 | 22.1 | 18.7 | 7.7 | |||||||||||||||||||||||||||||||||||

| Wright 13 12 HC-2 |

6,009 | 18.1 | 3.0 | 12/21/13 | 70 | 1.5 | 24.0 | 7.9 | ||||||||||||||||||||||||||||||||||||

| LA Minerals 15 22H-2 |

5,814 | N/A | N/A | 1/21/14 | 39 | 0.7 | 18.0 | 8.4 | ||||||||||||||||||||||||||||||||||||

| Lower Red Zone |

||||||||||||||||||||||||||||||||||||||||||||

| TL McCrary 14H-1 |

4,544 | 12.8 | 2.8 | 5/1/12 | 669 | 3.9 | 14.4 | 11.7 | 8.3 | 5.4 | 7.7 | |||||||||||||||||||||||||||||||||

| Nobles 13H-2 |

4,060 | 9.2 | 2.3 | 11/17/12 | 469 | 2.9 | 16.0 | 11.9 | 8.4 | 5.2 | 7.8 | |||||||||||||||||||||||||||||||||

| LA Methodist Orphanage 14H-1 |

3,637 | 12.1 | 3.3 | 2/15/13 | 379 | 3.3 | 14.0 | 13.0 | 9.7 | 6.3 | 9.1 | |||||||||||||||||||||||||||||||||

| Dowling 21 16H-1 |

4,590 | 9.4 | 2.0 | 3/18/13 | 348 | 2.3 | 13.0 | 10.1 | 6.5 | 6.6 | ||||||||||||||||||||||||||||||||||

| Drewett 17 8H-2 |

3,700 | 3.7 | 1.0 | 11/13/13 | 108 | 0.6 | 8.7 | 6.2 | 6.8 | |||||||||||||||||||||||||||||||||||

| Wright 13 12 HC-1 |

5,409 | 8.2 | 1.5 | 12/21/13 | 70 | 0.9 | 15.6 | 9.0 | ||||||||||||||||||||||||||||||||||||

| LA Minerals 15 22H-1 |

5,926 | N/A | N/A | 1/21/14 | 39 | 0.5 | 13.8 | 7.9 | ||||||||||||||||||||||||||||||||||||

| Lower Deep Pink Zone |

||||||||||||||||||||||||||||||||||||||||||||

| LA Methodist Orphanage 14H-2 |

3,550 | 12.2 | 3.4 | 2/15/13 | 379 | 2.8 | 14.3 | 11.6 | 7.6 | 5.7 | 6.1 | |||||||||||||||||||||||||||||||||

| Wright 13 12 HC-3 |

5,706 | 6.3 | 1.1 | 12/21/13 | 70 | 0.8 | 13.2 | 7.1 | ||||||||||||||||||||||||||||||||||||

| Wright 13 12 HC-4 |

5,010 | 5.0 | 1.0 | 12/21/13 | 70 | 0.7 | 12.6 | 6.0 | ||||||||||||||||||||||||||||||||||||

| Averages |

||||||||||||||||||||||||||||||||||||||||||||

| All Wells |

4,580 | 11.0 | 2.5 | 290 | 2.3 | 15.1 | 12.1 | 8.8 | 6.2 | 7.8 | ||||||||||||||||||||||||||||||||||

| Upper Red |

4,554 | 12.6 | 2.7 | 313 | 2.6 | 16.3 | 12.8 | 9.1 | 6.7 | 8.2 | ||||||||||||||||||||||||||||||||||

| Lower Red |

4,552 | 9.2 | 2.2 | 297 | 2.1 | 13.6 | 10.6 | 8.2 | 5.6 | 7.8 | ||||||||||||||||||||||||||||||||||

| Lower Deep Pink |

4,755 | 7.8 | 1.8 | 173 | 1.4 | 13.4 | 11.6 | 7.6 | 5.7 | 6.4 | ||||||||||||||||||||||||||||||||||

| (1) | The wells in this table are included within our proved developed producing reserve category in our reserve report as of December 31, 2013. LA Minerals 15 22H-1 and LA Minerals 15 22H-2 both started producing in January 2014 so they have not been included in the year-end reserve report. |

| (2) | EUR represents the Estimated Ultimate Recovery or sum of total gross remaining reserves attributable to each location in our reserve report and cumulative sales from such location. EUR is shown on a combined basis for oil/condensates, gas and NGLs after the effects of processing. |

4

Table of Contents

| (3) | Production data is as of February 28, 2014 and shown gross on a combined basis after the effects of processing. |

| (4) | Periodic flow rates start on day 4, with days 1 through 3 used to allow clean up associated with well completion. The 30-day flow rates therefore start on day 4 and continue 30 days to day 33 and the 90-day flow rates go from day 4 to day 93. |

East Texas

We own and operate approximately 24,458 gross (19,776 net) acres as of December 31, 2013 in Panola and Shelby Counties in Texas, where we are currently producing primarily from the Cotton Valley, Travis Peak and Bossier formations and targeting the Cotton Valley formation for future development. From January 1, 2011 through December 31, 2013, we have drilled and completed 28 gross (10.3 net) wells and are operating one rig in East Texas as of December 31, 2013. In 2014, we plan to invest $36 million to drill and complete 8 gross (6 net) wells in East Texas in the Joaquin Field of Panola and Shelby Counties. As of December 31, 2013, we had approximately 108 gross identified horizontal drilling locations in East Texas, including 54 gross (43 net) drilling locations to which we have attributed proved undeveloped reserves as of December 31, 2013. For the three months ended December 31, 2013, our average net daily production from our East Texas properties was 21 MMcfe/d, of which 76% was natural gas. Within our East Texas properties, on a proved reserves basis, we operate approximately 94% of our existing properties.

Rockies & Other

We own approximately 162,375 gross (66,191 net) acres as of December 31, 2013 in our Rockies & Other region and for the three months ended December 31, 2013 our average net daily production from this region was 1 MMcfe/d. In 2014, we plan to operate one rig and invest $12 million to drill 3 gross (3 net) vertical wells in the Tepee Field of the Piceance Basin targeting the Mancos and Williams Fork formations. We also plan to invest $4 million to participate in 12 gross horizontal wells (1.1 net) operated by SandRidge Energy Inc. in the Mississippian oil play of Northern Oklahoma. As of December 31, 2013, we had approximately 174 gross identified vertical drilling locations in the Tepee Field in our Rockies & Other area.

5

Table of Contents

Reserves

Our estimates of proved reserves are prepared by NSAI, and our estimates of probable and possible reserves are prepared by our management and audited by NSAI. As of December 31, 2013, we had 1,126 Bcfe, 800 Bcfe and 1,034 Bcfe of estimated proved, probable and possible reserves, respectively. As of this date, our proved reserves were 71% gas and 29% NGLs and oil. Additionally, the PV-10 of our proved reserves was $1,469 million, the PV-10 for our probable reserves was $1,052 million and the PV-10 for our possible reserves was $1,342 million. The following table provides summary information regarding our estimated proved, probable and possible reserves data by area based on our reserve report and our average net daily production by area for the three months ended December 31, 2013:

| Proved Total (Bcfe) |

% Gas | % Developed |

Proved PV-10 (in millions)(1) |

Probable Total (Bcfe)(2) |

Probable PV-10 (in millions)(1) |

Possible Total (Bcfe)(2) |

Possible PV-10 (in millions)(1) |

Average Net Daily Production (MMcfe/d) |

||||||||||||||||||||||||||||

| Terryville Complex |

945 | 71 | % | 33 | % | $ | 1,341 | 688 | $ | 1,032 | 966 | $ | 1,339 | 115 | ||||||||||||||||||||||

| East Texas |

175 | 75 | % | 29 | % | 110 | 109 | 18 | 66 | 3 | 21 | |||||||||||||||||||||||||

| Rockies & Other |

6 | 49 | % | 100 | % | 18 | 2 | 2 | 2 | 1 | 1 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Total |

1,126 | 71 | % | 33 | % | $ | 1,469 | 800 | $ | 1,052 | 1,034 | $ | 1,342 | 137 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| (1) | In this prospectus, we have disclosed our PV-10 based on our reserve report. PV-10 is a non-GAAP financial measure and represents the period-end present value of estimated future cash inflows from our natural gas and crude oil reserves, less future development and production costs, discounted at 10% per annum to reflect timing of future cash flows and using SEC pricing assumptions in effect at the end of the period. SEC pricing for natural gas and oil of $3.67 per Mcf and $93.42 per Bbl was based on the unweighted average of the first-day-of-the-month prices for each of the twelve months preceding December 2013. PV-10 differs from standardized measure, the most directly comparable GAAP financial measure, because it does not include the effects of income taxes. Moreover, GAAP does not provide a measure of estimated future net cash flows for reserves other than proved reserves. Because PV-10 estimates of probable and possible reserves are more uncertain than PV-10 and standardized estimates of proved reserves, but have not been adjusted for risk due to that uncertainty, they may not be comparable with each other. Nonetheless, we believe that PV-10 estimates for reserve categories other than proved present useful information for investors about the future net cash flows of our reserves in the absence of a comparable GAAP measure such as standardized measure. Because of this, PV-10 can be used within the industry and by creditors and securities analysts to evaluate estimated net cash flows from proved reserves on a more comparable basis. In addition, investors should be cautioned that estimates of PV-10 for probable and possible reserves, as well as the underlying volumetric estimates, are inherently more uncertain of being recovered and realized than comparable measures for proved reserves, and that the uncertainty for possible reserves is even more significant. Our PV-10 estimates of proved reserves and our standardized measure are equivalent because, prior to the completion of this offering, we were not subject to entity level taxation. Accordingly, no provision for federal income taxes has been provided because taxable income has been passed through to our equity holders. After this offering, we will be treated as a taxable entity for federal income tax purposes and our future income taxes will be dependent upon our future taxable income. Neither PV-10 nor standardized measure represents an estimate of fair market value of our natural gas and oil properties. We and others in the industry use PV-10 as a measure to compare the relative size and value of estimated reserves held by companies without regard to the specific tax characteristics of such entities. |

| (2) | Substantially all of our estimated probable and possible reserves are classified as undeveloped. |

6

Table of Contents

Drilling Inventory and Capital Budget

We intend to develop our multi-year drilling inventory by utilizing our significant expertise in horizontal drilling and fracture stimulation to grow our production, reserves and cash flow. For 2014, we have budgeted a total of $316 million to drill and complete 49 gross (39 net) operated wells and to participate in 12 gross (1.1 net) non-operated wells. We expect to fund our 2014 development primarily from cash flows from operations. The majority of our drilling locations and our 2014 development program are focused on the Terryville Complex, where we plan to invest $264 million on drilling and completing 33 gross (28 net) horizontal wells and 2 gross (2 net) vertical wells. Approximately $5.0 million of our Terryville Complex budget is allocated towards the drilling of vertical wells and routine facilities maintenance. In East Texas, we plan to invest $36 million on drilling and completing 8 gross (6 net) horizontal wells. In our Rockies & Other area we plan to invest $12 million on drilling and completing 3 gross (3 net) vertical wells in the Tepee Field and $4 million to participate in 12 gross (1.1 net) horizontal wells operated by SandRidge Energy Inc. in the Mississippian oil play of Northern Oklahoma.

The following table provides information regarding our acreage and drilling locations by area as of December 31, 2013, except for projected 2014 information:

| Net Acreage |

WI% | Gross Horizontal Drilling Locations(1)(2) | Net Horizontal Drilling Inventory (years) |

2014 Projected Operated Net Wells to be Drilled(3) |

2014 Projected Capital Budget ($MM) |

|||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

Total | ||||||||||||||||||||||||||||||||||||||||

| Proved | Probable | Possible | Management | Gross | Net | |||||||||||||||||||||||||||||||||||||||

| Terryville Complex |

96,733 | 74 | % | 91 | 147 | 165 | 743 | 1,146 | 796 | 28 | 30 | $ | 264 | |||||||||||||||||||||||||||||||

| East Texas |

42,894 | 79 | % | 54 | 39 | 15 | — | 108 | 92 | 15 | 6 | 36 | ||||||||||||||||||||||||||||||||

| Rockies & Other |

66,191 | 41 | % | — | 23 | 20 | — | 43 | 4 | — | 3 | 16 | ||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Total |

205,818 | 59 | % | 145 | 209 | 200 | 743 | 1,297 | 892 | 26 | 39 | $ | 316 | |||||||||||||||||||||||||||||||

| (1) | The above table excludes 192 proved vertical drilling locations in our reserve report in the Terryville Complex and 174 identified vertical locations based on management estimates in the Rockies & Other region. |

| (2) | Please see “Business—Our Operations—Drilling Locations” for more information regarding the process and criteria through which these drilling locations were identified. The drilling locations on which we actually drill will depend on the availability of capital, regulatory approval, commodity prices, costs, actual drilling results and other factors. Please see “Risk Factors—Risks Related to Our Business—Our identified drilling locations, which are scheduled out over many years, are susceptible to uncertainties that could materially alter the occurrence or timing of their drilling.” Proved, probable and possible locations are based on our reserve report. Management locations are based on management estimates of additional identified drilling locations. |

| (3) | Represents net operated wells only. Excludes 12 gross (1.1 net) non-operated wells to be drilled in our Rockies & Other area in 2014. |

7

Table of Contents

Our extensive inventory and horizontal drilling program in the Terryville Complex is currently focused on four zones within the Cotton Valley formation—the Upper Red, Lower Red, Lower Deep Pink and Upper Deep Pink. The table below sets forth our drilling locations by zone as of December 31, 2013 along with the average results for the wells we have drilled within each zone. Please see “Business—Our Properties—Cotton Valley—Terryville Complex Horizontal Redevelopment” for more detail on our properties in the Terryville Complex and the table on page 92 for the 30 day initial production rate and EUR condensate volumes.

| Average Historical Results(2) | ||||||||||||||||||||||||||||||||

| Lower Cotton Valley Zone |

Gross Horizontal Drilling Locations(1) | Producing Wells Drilled(1) |

EUR (Bcfe)(3) |

Drilling and Completion Costs ($MM) |

||||||||||||||||||||||||||||

| Proved | Probable | Possible | Management | Total | ||||||||||||||||||||||||||||

| Upper Red |

47 | 42 | 40 | 313 | 442 | 13 | 12.6 | $ | 8.2 | |||||||||||||||||||||||

| Lower Red |

40 | 40 | 36 | 276 | 392 | 7 | 9.2 | $ | 7.8 | |||||||||||||||||||||||

| Lower Deep Pink |

4 | 28 | 47 | 79 | 158 | 3 | 7.8 | $ | 6.4 | |||||||||||||||||||||||

| Upper Deep Pink |

— | 37 | 42 | 75 | 154 | — | — | — | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Total Terryville Complex |

91 | 147 | 165 | |

743 |

|

1,146 | 23 | 11.0 | $ | 7.8 | |||||||||||||||||||||

| (1) | Please see “Business—Our Operations—Drilling Locations” for more information regarding the process and criteria through which these drilling locations were identified. The drilling locations on which we actually drill will depend on the availability of capital, regulatory approval, commodity prices, costs, actual drilling results and other factors. Please see “Risk Factors—Risks Related to Our Business—Our identified drilling locations, which are scheduled out over many years, are susceptible to uncertainties that could materially alter the occurrence or timing of their drilling.” Proved, probable and possible locations are based on our reserve report. Management locations are based on management estimates of additional identified drilling locations. |

| (2) | Relates to the 21 horizontal wells in the Terryville Complex included in our reserve report as proved developed reserves as of December 31, 2013. Drilling and completion costs include costs associated with two additional wells that have come online since year-end. |

| (3) | EUR represents the Estimated Ultimate Recovery or the sum of total gross remaining reserves attributable to each location in our reserve report and cumulative sales from such location. EUR is shown at the wellhead on a combined basis for oil/condensates and wet gas. |

Our Terryville horizontal development program in 2014 has an average working interest of 87% and our total horizontal development inventory has an average working interest of 69%.

For the Terryville Complex, our 2014 budget assumes an average cost of $8.6 million for gross horizontal wells ($7.5 million per net well) and is based on an average lateral length of 6,270 feet. As part of our long-term development plan, the lateral length of our planned wells is expected to increase and we expect wells within the Terryville Complex to cost on average $9.3 million for gross wells ($8.1 million per net well) drilled with a 7,000 foot lateral length.

8

Table of Contents

Business Strategies

Our primary objective is to build shareholder value through growth in reserves, production and cash flows by developing and expanding our significant portfolio of drilling locations. To achieve our objective, we intend to execute the following business strategies:

Grow production, reserves and cash flow through the development of our extensive drilling inventory. We believe our extensive inventory of low-risk drilling locations, combined with our operating expertise, will enable us to continue to deliver production, reserve and cash flow growth and create shareholder value. As of December 31, 2013, we had assembled an aggregate drilling inventory of 1,297 gross identified horizontal drilling locations, 88% of which are in the Terryville Complex, representing a drilling inventory of over 28 years based on our expected 2014 drilling program. We believe that the risk and uncertainty associated with our core acreage positions in the Terryville Complex has been largely reduced through our development activity, and because those positions are in areas with extensive drilling and production history. Since initiating our horizontal drilling program with one rig in 2011, we have invested over $288 million in the Terryville Complex through December 31, 2013. With four rigs running in the Terryville Complex as of December 31, 2013, we are one of the most active drillers in the Cotton Valley formation. We intend to dedicate approximately $264 million of our $316 million drilling and completion budget in 2014 to develop the overpressured liquids-rich Terryville Complex through multi-well pad drilling. We believe multiple vertically stacked producing horizons in the Terryville Complex can be developed using horizontal drilling techniques, thus enhancing the economics of this field.

Enhance returns through prudent capital allocation and continued improvements in operational and capital efficiencies. We continually monitor and adjust our drilling program with the objective of achieving the highest total returns on our portfolio of drilling opportunities. We believe we will achieve this objective by (i) minimizing the capital costs of drilling and completing horizontal wells through knowledge of the target formations, (ii) maximizing well production and recoveries by optimizing lateral length, the number of frac stages, perforation intervals and the type of fracture stimulation employed, (iii) targeting specific zones within our leasehold position to maximize our hydrocarbon mix based on the existing commodity price environment and (iv) minimizing operating costs through efficient well management.

Exploit additional development opportunities on current acreage. Our existing asset base provides numerous opportunities for our highly experienced technical team to create shareholder value by increasing our inventory beyond our currently identified drilling locations and ultimately by growing our estimated proved reserves. In the Terryville Complex, we are currently targeting multiple stacked horizons. We also believe our East Texas region has a significant inventory of low-risk, liquids-rich horizontal drilling locations. Finally, we continue to evaluate our leasehold positions in the Rocky Mountains and have preliminarily evaluated over 170 potential vertical locations.

Maintain a disciplined, growth oriented financial strategy. We intend to fund our growth primarily with internally generated cash flows while maintaining ample liquidity and access to the capital markets. Furthermore, we plan to hedge a significant portion of our expected production to reduce our exposure to downside commodity price fluctuations and enable us to protect our cash flows and maintain liquidity to fund our drilling program. Since approximately 76% of our acreage in the Terryville Complex was held by production as of December 31, 2013 and no significant drilling commitments are needed to hold our remaining acreage in the near term, we are able to allocate capital among projects in a manner that optimizes both costs and returns, resulting in a highly efficient drilling program.

Make opportunistic acquisitions that meet our strategic and financial objectives. We will seek to acquire oil and gas properties that we believe complement our existing properties in our core areas of operation. In

9

Table of Contents

addition to our focus on the Terryville Complex, we are pursuing other properties that provide opportunities for the addition of reserves and production through a combination of exploitation, development, high-potential exploration and control of operations. We follow a technology driven strategy to establish large, contiguous leasehold positions in the core of prolific basins and opportunistically add to those positions through bolt-on acquisitions over time. We entered into the Terryville Complex through strategic acquisitions and grassroots leasing efforts, amassing a land position of 96,733 net acres, 51,522 net acres of which we believe to be in the core of the play. We will continue to identify and opportunistically acquire additional acreage and producing assets to complement our multi-year drilling inventory.

Competitive Strengths

We believe that the following strengths will allow us to successfully execute our business strategies.

Large, concentrated position in one of North America’s leading plays. We own approximately 60,041 gross (51,522 net) acres in what we believe to be the core of the Terryville Complex in Lincoln Parish, which we believe to be one of North America’s most prolific liquids-rich natural gas fields, characterized by consistent and predictable geology and multiple stacked pay formations confirmed by extensive vertical well control. Through December 31, 2013, our drilling program in the Terryville Complex has produced some of the top performing gas wells in the United States in the previous two years, with single horizontal well results having achieved average 30-day initial production rates of 15.1 MMcfe/d, EURs averaging 11.0 Bcfe and average drilling and completion costs of $7.8 million per well. Approximately 76% of our acreage in the Terryville Complex was held by production at December 31, 2013 and there are no significant lease expirations until 2017. Additionally, all of our acreage in this play can be held by running a one rig program over the next 18 months.

De-risked acreage position with multi-year inventory of liquids-rich drilling opportunities. As of December 31, 2013, we had a drilling inventory consisting of 1,297 gross identified horizontal drilling locations, of which approximately 145 are gross proved undeveloped locations. Based on our expected 2014 drilling program and net identified drilling locations, we have over 26 years of liquids-rich drilling inventory. The majority of our drilling activity has been and will continue to be focused in the Terryville Complex, where we produce liquids-rich natural gas from the overpressured Cotton Valley formation. We have used subsurface data from our vertical wells coupled with 3-D seismic data to identify and prioritize our inventory based on returns. This liquids-rich gas formation allows for NGL processing that, when coupled with the condensate produced, results in strong well economics. For the three months ended December 31, 2013, 45% of our pro forma MRD Segment revenues were attributable to natural gas, 28% to NGLs and 27% to oil.

Significant operational control with low cost operations. On a proved reserves basis, we operate 99% of our properties and have operational control of all of our drilling inventory in the Terryville Complex. We believe maintaining operational control will enable us to enhance returns by implementing more efficient and cost-effective operating practices, through the selection of economic drilling locations, opportunistic timing of development, continuous improvement of drilling, completion and stimulation techniques and development on multi-well pads. As a result of the contiguous nature of our leasehold in the Terryville Complex and its geologic continuity, we are able to drill consistently long laterals, averaging over 4,200 lateral feet, which helps us to reduce costs on a per-lateral foot basis and increase our returns. We expect the average lateral length of the 35 gross wells that we expect to drill in the Terryville Complex in 2014 to be 6,400 feet per well. Operating in mature basins in North Louisiana and East Texas allows us to take advantage of the available and extensive midstream infrastructure and accelerate our development plan without encountering significant constraints in either takeaway or processing capacity. Our operational control allows us to focus on operating efficiency, which has resulted in our MRD Segment lease operating costs declining 31% from $0.77 per Mcfe for the year ended December 31, 2012 to $0.53 per Mcfe for the year ended December 31, 2013.

10

Table of Contents

Proven and incentivized executive and technical team. We believe our management and technical teams are one of our principal competitive strengths due to our team’s significant industry experience and long history of working together in the identification, execution and integration of acquisitions, cost efficient management of profitable, large scale drilling programs and a focus on rates of return. Additionally, our technical team has substantial expertise in advanced drilling and completion technologies and decades of expertise in operating in the North Louisiana and East Texas regions. The members of our management team collectively have an average of 22 years of experience in the oil and natural gas industry. John A. Weinzierl, our Chief Executive Officer, has 24 years of oil and natural gas industry experience as a petroleum engineer, a strong commercial and technical background and extensive experience acquiring and managing oil and natural gas properties. Our management team has a significant economic interest in us directly and through its equity interests in our controlling stockholder, MRD LLC. We believe our management team is motivated to deliver high returns, create shareholder value and maintain safe and reliable operations.

Our relationship with MEMP. We currently own 5,360,912 subordinated units representing a 8.7% limited partner interest in MEMP and a 0.1% general partner interest in MEMP through our ownership of its general partner. We also own 50% of MEMP’s incentive distribution rights. MEMP’s objective as a master limited partnership is to generate stable cash flows, allowing it to make quarterly distributions to its limited partners and, over time, to increase those quarterly distributions. As a result of its familiarity with our management team and our asset base and our track record of prior “drop-down” transactions, we believe that MEMP is a natural purchaser of properties from us that meet its acquisition criteria. We believe this mutually beneficial relationship enhances MEMP’s ability to generate consistent returns on its oil and natural gas properties, provides us with a growing source of cash flow from our partnership interests in MEMP and allows us to monetize producing non-core properties. Since MEMP’s initial public offering, we have consummated “drop-down” transactions with MEMP totaling approximately $376 million. In addition, we may have the opportunity to work jointly with MEMP to pursue certain acquisitions of oil and natural gas properties that may not otherwise be attractive acquisition candidates for either of us individually. While we believe that MEMP would be a preferred acquirer of our mature, non-core assets, we are under no obligation to offer to sell, and it is under no obligation to offer to buy, any of our properties.

Financial strength and flexibility. During 2013, we generated $173 million of pro forma MRD Segment Adjusted EBITDA and made pro forma total capital expenditures of $204 million, including $70 million on wells coming online in 2014. We intend to continue to fund our organic growth predominantly with internally generated cash flows while maintaining ample liquidity for opportunistic acquisitions. We will continue to maintain a disciplined approach to spending whereby we allocate capital in order to optimize returns and create shareholder value. We seek to protect these future cash flows and liquidity levels by maintaining a three-to-five year rolling hedge program. Pro forma as of December 31, 2013 for this offering and the restructuring transactions (including the redemption of the PIK notes for approximately $363 million 30 days after the closing of this offering), we expect our total liquidity, consisting of cash on hand and available borrowing capacity under our new revolving credit facility, to be in excess of $ million.

Recent Developments

In December 2013, MRD LLC issued $350,000,000 of its 10.00%/10.75% Senior PIK toggle notes due 2018, which we refer to as the PIK notes. MRD LLC used the net proceeds from that issuance to repay outstanding indebtedness, to fund a debt service reserve account for the payment of interest on the PIK notes, to pay a distribution to the Funds, and for general company purposes. In connection with the closing of this offering, we will assume the PIK notes and use a portion of the proceeds of this offering to redeem the PIK notes in their entirety, to pay any applicable premium in connection with such redemption and to pay accrued and unpaid interest, if any, to the date of redemption. MRD LLC will receive the cash released upon the termination of the debt service reserve account in connection with the redemption of the PIK notes.

11

Table of Contents

In April 2014, we sold approximately 15 Bcfe of proved reserves located in East Texas to MEMP for cash consideration of approximately $34.0 million, subject to customary post-closing adjustments.

In connection with the closing of this offering, we intend to enter into a new $ million revolving credit facility. Immediately prior to the closing of this offering, we will borrow approximately $ million from our new revolving credit facility to pay off and terminate in their entirety WildHorse Resources’ revolving credit facility and second lien term loan, which we refer to collectively as WildHorse Resources’ credit agreements.

Acquisition History

We built out our leasehold positions in North Louisiana, East Texas and the Rocky Mountains primarily through the following acquisition activities:

| • | In November 2007, we acquired interests in the Joaquin Field, which is the core of our East Texas acreage; |

| • | In December 2007, we acquired interests in the Tepee Field in the Piceance Basin in Colorado; |

| • | In April and May 2010, we acquired interests in the Terryville Complex and other North Louisiana fields, which are the core of our North Louisiana acreage; |

| • | In November 2010, we acquired interests in the Spider and E. Logansport Fields in North Louisiana; |

| • | In May 2012, we acquired interests in the Terryville Complex and Double A Field in North Louisiana and East Texas; |

| • | In April 2013, we acquired interests in the West Simsboro and Simsboro Fields of the Terryville Complex in North Louisiana; |

| • | In November 2013, we acquired the remaining equity interests in Classic Hydrocarbons Holdings, L.P., Classic Hydrocarbons GP Co., L.L.C. and Black Diamond Minerals, LLC, which hold oil and natural gas properties in East Texas, North Louisiana and the Rocky Mountains; and |

| • | In February 2014, we repurchased net profits interests in the Terryville Complex from an affiliate of NGP for $63.4 million after customary adjustments. These net profits interests were originally sold to the NGP affiliate upon the completion of certain acquisitions in 2010 by WildHorse Resources. |

Our Principal Stockholder

Our principal stockholder is MRD LLC, which is controlled by the Funds, which are three of the private equity funds managed by NGP. Upon completion of this initial public offering, MRD LLC, the selling stockholder in this offering, will own approximately % of our common stock (or approximately % if the underwriters’ option to purchase additional shares from MRD LLC is exercised in full). The Funds also collectively indirectly own 50% of MEMP’s incentive distribution rights. We are also a party to certain other agreements with MRD LLC, the Funds and certain of their affiliates. For a description of these agreements, please read “Certain Relationships and Related Party Transactions.”

Founded in 1988, NGP is a family of private equity investment funds, with cumulative committed capital of approximately $10.5 billion since inception, organized to make investments in the natural resources sector. NGP is part of the investment platform of NGP Energy Capital Management, a premier investment franchise in the natural resources industry, which together with its affiliates has managed approximately $13 billion in cumulative committed capital since inception.

12

Table of Contents

Our Interest in Memorial Production Partners LP

Through our ownership of its general partner, we control MEMP. We also own 5,360,912 subordinated units representing an 8.7% limited partner interest in MEMP and 50% of its incentive distribution rights. MEMP is a publicly traded limited partnership engaged in the acquisition, exploitation, development and production of oil and natural gas properties in the United States, with assets consisting primarily of producing oil and natural gas properties that are located in East Texas/North Louisiana, the Permian Basin, offshore Southern California, the Rockies, the Eagle Ford and South Texas. Most of MEMP’s properties are located in large, mature oil and natural gas reservoirs with well-known geologic characteristics and long-lived, predictable production profiles and modest capital requirements. Because we control MEMP, we are required to consolidate MEMP for accounting and financial reporting purposes, even though we and MEMP have independent capital structures.

During the year ended December 31, 2013, we received approximately $11.2 million in cash distributions from our ownership of the subordinated units in MEMP. Less than $0.1 million of distributions were made in respect of the MEMP incentive distribution rights during the year ended December 31, 2013. Please see “Business—Relationship with Memorial Production Partners LP” for further information on our interest in MEMP.

Risk Factors

Investing in our common stock involves risks that include the speculative nature of oil and natural gas exploration, competition, volatile commodity prices and other material factors. For a discussion of these risks and other considerations that could negatively affect us, including risks related to this offering and our common stock, please read “Risk Factors” beginning on page 24 of this prospectus and “Cautionary Note Regarding Forward-Looking Statements.”

Our Structure and Restructuring Transactions

We are a Delaware corporation formed by MRD LLC to own and acquire oil and natural gas properties. In connection with the closing of this offering, the following transactions, which we refer to as the restructuring transactions, will occur:

| • | MRD LLC will contribute to us substantially all of its assets, comprised of: |

| • | 100% of the ownership interests in Classic Hydrocarbons Holdings, L.P., Classic Hydrocarbons GP Co., L.L.C., Black Diamond Minerals, LLC, Beta Operating Company, LLC and MRD Operating LLC; |

| • | 99.9% of the membership interests in WildHorse Resources, the owner of our properties in the Terryville Complex; and |

| • | MEMP GP (including MEMP GP’s ownership of 50% of MEMP’s incentive distribution rights) and 5,360,912 subordinated units representing an 8.7% limited partner interest in MEMP; |

| • | We will issue shares of our common stock to MRD LLC; |

| • | Certain former management members of WildHorse Resources will contribute to us their outstanding incentive units in WildHorse Resources, as well as the remaining 0.1% of the membership interests in WildHorse Resources, and we will issue shares of our common stock and pay cash consideration of $ to such former management members of WildHorse Resources; and |

| • | We will enter into a registration rights agreement and a voting agreement with MRD LLC and certain former management members of WildHorse Resources, and a services agreement with an entity managed by certain former management members of WildHorse Resources. |

13

Table of Contents

In connection with the restructuring transactions, MRD LLC will retain:

| • | BlueStone, which sold substantially all of its assets in July 2013 for $117.9 million; MRD Royalty, which owns certain immaterial leasehold interests and overriding royalty interests in Texas and Montana; and MRD Midstream, which owns an indirect interest in certain immaterial midstream assets in North Louisiana; and |

| • | The $32 million in cash (net of $18 million to be used to pay accrued interest on the PIK notes on June 15, 2014) to be released from its debt service reserve account in connection with the redemption of the PIK notes (which we expect will be 30 days after the closing of this offering). |

Contemporaneous with the restructuring transactions, we will assume the PIK notes and use a portion of the net proceeds from this offering to redeem all outstanding PIK notes, including paying any applicable premium and accrued and unpaid interest, if any, to the date of redemption (which we expect will be 30 days after the closing of this offering). We will use any remaining proceeds, together with borrowings under our new revolving credit facility, to repay and terminate WildHorse Resources’ credit agreements. Please read “Use of Proceeds” and “Restructuring Transactions” for more information about the application of the net proceeds from this offering and the restructuring transactions. For more information regarding BlueStone, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations—MRD Segment.”

14

Table of Contents

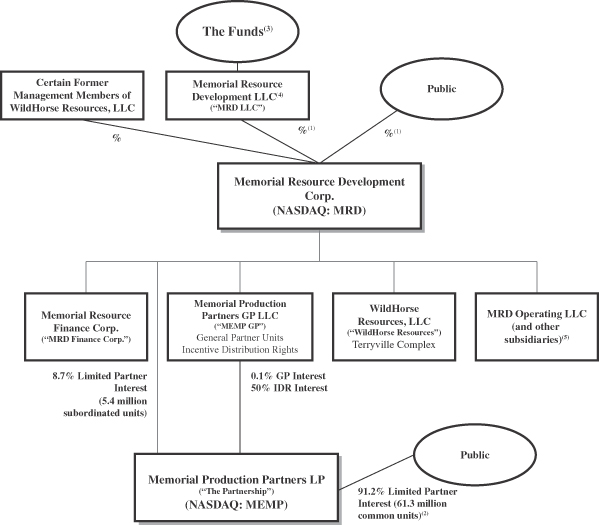

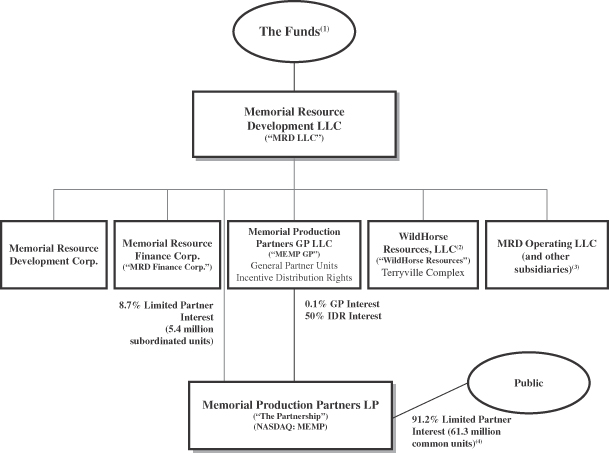

The following diagram shows our ownership structure after giving effect to the restructuring transactions and this offering, assuming no exercise of the underwriters’ option to purchase additional shares from MRD LLC and does not give effect to shares of common stock reserved for future issuance under the Memorial Resource Development Corp. 2014 Incentive Award Plan (described in “Management—2014 Incentive Award Plan”). For information regarding our ownership structure before giving effect to the restructuring transactions and this offering, see the diagram on page 138 in “Restructuring Transactions.”

| (1) | If the underwriters exercise in full their option to purchase additional shares of common stock from MRD LLC, the ownership interest of the public stockholders will increase to shares of common stock, representing an aggregate % ownership interest in us, and MRD LLC will own shares of common stock, representing an aggregate % ownership interest in us. |

| (2) | As of December 31, 2013. |

| (3) | “The Funds” refer collectively to Natural Gas Partners VIII, L.P., Natural Gas Partners IX, L.P. and NGP IX Offshore Holdings, L.P., which collectively own all of the membership interests in MRD LLC. Please read “Principal and Selling Stockholders” for information regarding beneficial ownership. The Funds collectively indirectly own 50% of the Partnership’s incentive distribution rights. |

| (4) | Subsidiaries of MRD LLC following the restructuring transactions will include BlueStone Natural Resources Holdings, LLC (“BlueStone”), MRD Royalty LLC (“MRD Royalty”) and MRD Midstream LLC (“MRD Midstream”). Also, please see the “Principal and Selling Stockholders” table on page 130 for the beneficial ownership of our shares by our executive officers and directors. |

| (5) | Includes Classic Hydrocarbons Holdings, L.P. (“Classic”), Classic Hydrocarbons GP Co., L.L.C. (“Classic GP”), Black Diamond Minerals, LLC (“Black Diamond”), and Beta Operating Company, LLC (“Beta Operating”). |

15

Table of Contents

Corporate Information

Our principal executive offices are located at 1301 McKinney St., Suite 2100, Houston, Texas 77010, and our phone number is (713) 588-8300. Our website address is www.memorialrd.com. We expect to make our periodic reports and other information filed with or furnished to the Securities and Exchange Commission, which we refer to as the SEC, available free of charge through our website as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. Information on our website or any other website is not incorporated by reference into, and does not constitute a part of, this prospectus.

Emerging Growth Company Status

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act (the “JOBS Act”). For as long as we are an emerging growth company, unlike other public companies that are not emerging growth companies, we are not required to:

| • | provide an auditor’s attestation report on management’s assessment of the effectiveness of our system of internal control over financial reporting pursuant to Section 404 of the Sarbanes-Oxley Act of 2002; |

| • | provide more than two years of audited financial statements and related management’s discussion and analysis of financial condition and results of operations; |

| • | comply with any new requirements adopted by the Public Company Accounting Oversight Board, or the “PCAOB,” requiring mandatory audit firm rotation or a supplement to the auditor’s report in which the auditor would be required to provide additional information about the audit and the financial statements of the issuer; |

| • | provide certain disclosure regarding executive compensation required of larger public companies or hold shareholder advisory votes on executive compensation required by the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”); or |

| • | obtain shareholder approval of any golden parachute payments not previously approved. |

We will cease to be an “emerging growth company” upon the earliest of:

| • | the last day of the fiscal year in which we have $1.0 billion or more in annual revenues; |

| • | the date on which we become a “large accelerated filer” (the fiscal year-end on which the total market value of our common equity securities held by non-affiliates is $700 million or more as of June 30); |

| • | the date on which we issue more than $1.0 billion of non-convertible debt over a three-year period; or |

| • | the last day of the fiscal year following the fifth anniversary of our initial public offering. |

In addition, Section 107 of the JOBS Act provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933, as amended, or the Securities Act, for complying with new or revised accounting standards, but we have irrevocably opted out of the extended transition period and, as a result, we will adopt new or revised accounting standards on the relevant dates in which adoption of such standards is required for other public companies.

16

Table of Contents

The Offering

| Common stock offered by us |

shares. |

| Common stock offered by MRD LLC |

shares (or shares, if the underwriters exercise in full their option to purchase additional shares). |

| Common stock to be outstanding immediately after the offering |

shares. |

| Option to purchase additional shares |

MRD LLC has granted the underwriters a 30-day option to purchase up to an aggregate of additional shares of our common stock held by MRD LLC to cover over-allotments. |

| Common stock voting rights |

Each share of our common stock will entitle its holder to one vote. |

| Use of proceeds |

We intend to use the estimated net proceeds of approximately $ million from this offering, based upon the assumed initial public offering price of $ per share (the midpoint of the price range set forth on the cover of this prospectus), after deducting underwriting discounts and commissions and fees and expenses associated with this offering and the restructuring transactions, to redeem the PIK notes in their entirety and to pay any applicable premium in connection with such redemption and accrued and unpaid interest, if any, to the date of redemption (which we expect will be 30 days after the closing of this offering); together with borrowings of approximately $ million under our new revolving credit facility, to make a cash payment to certain former management members of WildHorse Resources in connection with their contribution to us of their membership interests and incentive units in WildHorse Resources; to repay borrowings outstanding under WildHorse Resources’ credit agreements; and for general corporate purposes. Until the redemption date of the PIK notes, we will use the amount to be paid to the holders of those notes to temporarily reduce amounts outstanding under our new revolving credit facility. See “Use of Proceeds.” |

| We will not receive any of the proceeds from the sale of shares of our common stock by MRD LLC, including pursuant to any exercise by the underwriters of their option to purchase additional shares of our common stock. MRD LLC is deemed under federal securities laws to be an underwriter with respect to the common stock it may sell in connection with this offering. |

| Dividend policy |

We currently intend to retain all future earnings, if any, for use in the operation of our business and to fund future growth. The decision whether to pay dividends in the future will be made by our board of directors (our “Board”) in light of conditions then existing, including factors such as our financial condition, earnings, available cash, business opportunities, legal requirements, restrictions in our debt agreements and other contracts and other factors our Board deems relevant. See “Dividend Policy.” |

17

Table of Contents

| Risk factors |

You should carefully read and consider the information set forth under “Risk Factors” beginning on page 24 of this prospectus and all other information set forth in this prospectus before deciding to invest in our common stock. |

| Listing and trading symbol |

We intend to list our common stock on the NASDAQ Global Market (“NASDAQ”) under the trading symbol “MRD.” |

18

Table of Contents

Summary Historical Consolidated and Combined Pro Forma Financial Data

MRD LLC and its consolidated subsidiaries, our accounting predecessor, controls MEMP through its ownership of MEMP GP, the general partner of MEMP. Because MRD LLC controls MEMP through its ownership of the general partner, MRD LLC is required to consolidate MEMP for accounting and financial reporting purposes even though MRD LLC owns a minority of its partner interests and MRD LLC and MEMP have independent capital structures. MRD LLC receives cash distributions from MEMP as a result of its partner interests and incentive distribution rights in MEMP, when declared and paid by MEMP. In connection with the closing of this offering, MRD LLC will contribute substantially all of its existing assets to us in exchange for shares of our common stock. Through our ownership of MEMP GP, we will continue to control MEMP and therefore will continue to consolidate the results of MEMP into our consolidated financial statements in future periods.

Our predecessor has two reportable business segments, both of which are engaged in the acquisition, exploitation, development and production of oil and natural gas properties:

| • | MRD—reflects all of MRD LLC’s consolidating subsidiaries except for MEMP and its subsidiaries. |

| • | MEMP—reflects the consolidated and combined operations of MEMP and its subsidiaries. |

We will continue to have two reportable segments following the completion of this offering. For more information regarding reportable business segments, please see the predecessor’s audited historical financial statements and related notes.

The following tables include the summary historical financial data of our predecessor, as well as the MRD Segment as of and for the periods indicated. The summary historical financial data of our predecessor as of and for the years ended December 31, 2013 and 2012 were derived from the audited historical financial statements of our predecessor included elsewhere in this prospectus. The summary historical financial data of the MRD Segment as of and for the years ended December 31, 2013 and 2012 were derived from certain financial information used in the preparation of our predecessor’s audited financial statements.

The summary unaudited pro forma data as of and for the year ended December 31, 2013 has been prepared to give pro forma effect to: (i) the exclusion of BlueStone, which is not being conveyed to us in connection with this offering, (ii) the offering of our shares of common stock contemplated hereby and the use of the net proceeds therefrom as described in “Use of Proceeds,” (iii) incremental federal income tax expense, and (iv) the restructuring transactions.

19

Table of Contents

We derived the data in the following tables from, and the following tables should be read together with and is qualified in its entirety by reference to, our predecessor’s historical financial statements and our pro forma financial statements and the accompanying notes included elsewhere in this prospectus. You should also read “Restructuring Transactions,” “Use of Proceeds,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our pro forma and historical consolidated financial statements, all included elsewhere in this prospectus. Among other things, those historical consolidated and combined financial statements and pro forma financial statements include more detailed information regarding the basis of presentation for the following data.

| MRD LLC (Predecessor) |

Memorial Resource Development Corp. Pro Forma |

|||||||||||

| Year

Ended December 31, |

Year Ended December 31, |

|||||||||||

| 2013 | 2012 | 2013 | ||||||||||

| (unaudited) | ||||||||||||

| (in thousands) | ||||||||||||

| Statement of Operations Data: |

||||||||||||