Attached files

| file | filename |

|---|---|

| EX-1.1 - EX-1.1 - Paycom Software, Inc. | d609623dex11.htm |

| EX-5.1 - EX-5.1 - Paycom Software, Inc. | d609623dex51.htm |

| EX-3.2 - EX-3.2 - Paycom Software, Inc. | d609623dex32.htm |

| EX-3.1 - EX-3.1 - Paycom Software, Inc. | d609623dex31.htm |

| EX-4.1 - EX-4.1 - Paycom Software, Inc. | d609623dex41.htm |

| EX-23.2 - EX-23.2 - Paycom Software, Inc. | d609623dex232.htm |

| EX-23.1 - EX-23.1 - Paycom Software, Inc. | d609623dex231.htm |

| EX-10.6 - EX-10.6 - Paycom Software, Inc. | d609623dex106.htm |

| EX-10.4 - EX-10.4 - Paycom Software, Inc. | d609623dex104.htm |

| EX-10.5 - EX-10.5 - Paycom Software, Inc. | d609623dex105.htm |

Table of Contents

As filed with the Securities and Exchange Commission on March 31, 2014.

Registration No. 333-194462

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Paycom Software, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 7372 | 80-0957485 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

7501 W. Memorial Road

Oklahoma City, Oklahoma 73142

(405) 722-6900

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Craig E. Boelte

Chief Financial Officer

Paycom Software, Inc.

7501 W. Memorial Road

Oklahoma City, Oklahoma 73142

(405) 722-6900

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Greg R. Samuel, Esq. Ryan R. Cox, Esq. Haynes & Boone, LLP 2323 Victory Avenue, Suite 700 Dallas, TX 75219 (214) 651-5000 Fax: (214) 200-0577 |

Christian O. Nagler, Esq. Kirkland & Ellis LLP 601 Lexington Avenue New York, NY 10022 (212) 446-4800 Fax: (212) 446-4900 |

Barbara L. Becker, Esq. Gibson, Dunn & Crutcher LLP 200 Park Avenue New York, NY 10166 (212) 351-4000 Fax: (212) 351-6202 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of each class of securities to be registered |

Amount to

be |

Proposed Maximum Offering Price Per Share |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee(3) | ||||

| Common Stock, $0.01 par value per share |

7,641,750 |

$20.00 |

$152,835,000 | $19,686 | ||||

|

| ||||||||

|

| ||||||||

| (1) | Estimated pursuant to Rule 457(a) of the Securities Act of 1933, as amended. |

| (2) | Includes additional shares subject to the underwriters’ option. |

| (3) | The registrant previously paid $12,880 of the registration fee in connection with a prior filing of this registration statement. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. Neither we nor the selling stockholders may sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, dated March 31, 2014

Preliminary Prospectus

6,645,000 Shares

Paycom Software, Inc.

Common Stock

This is the initial public offering of Paycom Software, Inc. We are offering 4,606,882 shares of our common stock and the selling stockholders are offering 2,038,118 shares of our common stock. We will not receive any proceeds from the sale of shares by the selling stockholders. Currently, no public market exists for the shares. The estimated initial public offering price is between $18.00 and $20.00 per share.

Our common stock has been approved for listing on the New York Stock Exchange, or the NYSE, under the symbol “PAYC.”

We are an “emerging growth company” as defined under the federal securities laws and, as such, may elect to comply with certain reduced public company reporting requirements in future reports after the completion of this offering.

Investing in our common stock involves risks. See “Risk Factors” beginning on page 12.

| Per share | Total | |||||||

| Initial public offering price |

$ | $ | ||||||

| Underwriting discounts and commissions |

$ | $ | ||||||

| Proceeds, before expenses, to us |

$ | $ | ||||||

| Proceeds, before expenses, to the selling stockholders |

$ | $ | ||||||

To the extent that the underwriters sell more than 6,645,000 shares of common stock, the underwriters have the option to purchase up to an additional 996,750 shares of common stock from the selling stockholders at the initial public offering price less underwriting discounts and commissions.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares on or about , 2014.

| Barclays | J.P. Morgan |

| Pacific Crest Securities | Stifel | Canaccord Genuity | ||

Prospectus dated , 2014

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| 1 | ||||

| 12 | ||||

| 29 | ||||

| 30 | ||||

| 31 | ||||

| 32 | ||||

| 33 | ||||

| 34 | ||||

| 35 | ||||

| 37 | ||||

| UNAUDITED PRO FORMA CONDENSED CONSOLIDATED FINANCIAL INFORMATION |

39 | |||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

47 | |||

| 66 | ||||

| 80 | ||||

| 86 | ||||

| 100 | ||||

| 105 | ||||

| 107 | ||||

| 112 | ||||

| MATERIAL U.S. FEDERAL INCOME AND ESTATE TAX CONSIDERATIONS FOR NON-U.S. HOLDERS |

114 | |||

| 117 | ||||

| 124 | ||||

| 124 | ||||

| 124 | ||||

| F-1 |

You should rely only on the information contained in this prospectus or in any free writing prospectus we have prepared. We, the selling stockholders and the underwriters (and any of our or their affiliates) have not authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectus we have prepared. We, the selling stockholders and the underwriters (and any of our or their affiliates), take no responsibility for and can provide no assurance as to the reliability of any other information that others may give you. We are offering to sell and seeking offers to buy shares of our common stock only in jurisdictions where offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of shares of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

Until , 2014 (25 days after the date of this prospectus), all dealers that buy, sell or trade shares of our common stock, whether or not participating in our initial public offering, may be required to deliver a prospectus. This delivery requirement is in addition to the obligation of dealers to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

For investors outside the United States: We, the selling stockholders and the underwriters (and any of our or their affiliates), have not done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about and observe any restrictions relating to the offering of the shares of our common stock and the distribution of this prospectus outside of the United States.

i

Table of Contents

This summary highlights selected information contained elsewhere in this prospectus, but it does not contain all of the information that you should consider before deciding to invest in our common stock. You should read the entire prospectus carefully before making an investment in our common stock, including “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes thereto, which are included elsewhere in this prospectus. Some of the statements in this prospectus constitute forward-looking statements. For more information, see “Special Note Regarding Forward-Looking Statements.”

Unless we state otherwise or the context otherwise requires, the terms “Paycom,” “we,” “us,” “our” and the “Company” refer, prior to the Reorganization discussed in the section entitled “The Reorganization,” to Paycom Payroll Holdings, LLC, or Holdings, and its consolidated subsidiaries and, after the Reorganization, to Paycom Software, Inc., or Software, a recently formed Delaware corporation, and its consolidated subsidiaries, including Holdings. Software is a recently formed company that did not engage in any business or other activities prior to the Reorganization, except in connection with its formation. Accordingly, all financial and other information herein relating to periods prior to the Reorganization is that of, or derived from, Holdings. See “The Reorganization.”

Overview

We are a leading provider of a comprehensive, cloud-based human capital management, or HCM, software solution delivered as Software-as-a-Service, or SaaS. We provide functionality and data analytics that businesses need to manage the complete employment life cycle from recruitment to retirement. Our solution requires virtually no customization and is based on a core system of record maintained in a single database for all HCM functions, including talent acquisition, time and labor management, payroll, talent management and human resources, or HR, management applications. Our user-friendly software allows for easy adoption of our solution by employees, enabling self-management of their HCM activities in the cloud, which reduces the administrative burden on employers and increases employee productivity.

Organizations need sophisticated, flexible and intuitive applications that can quickly adapt to their evolving HCM requirements, streamline their HR processes and systems and enable them to control costs. We believe that the HCM needs of most organizations are currently served either by legacy providers offering outdated on-premise products or multiple providers that partner together in an attempt to replicate a comprehensive product. These approaches often result in large up-front capital requirements, extended delivery times, high costs, low scalability and challenges with system integration. According to the International Data Corporation, or IDC, the U.S. markets for payroll services and HCM applications will collectively total approximately $22.5 billion in 2014, and we believe there is a substantial opportunity for our solution to address these HCM needs.

Because our solution was developed in-house and is based on a single platform, there is no need to integrate, update or access multiple databases, which are common issues with competitor offerings that use multiple third-party systems in order to link together their HCM offerings. Additionally, our solution maintains data integrity for accurate, actionable and real-time analytics and business intelligence and helps clients minimize the risk of compliance errors due to inaccurate or missing information. We deliver feature-rich applications while maintaining excellence in information security and quality management standards as evidenced by our International Organization for Standardization, or ISO, certifications. As a part of our client retention effort, a specialist within a dedicated team is assigned to each client to provide industry-leading, personalized service.

The key benefits of our differentiated solution as compared to competing products are:

| • | Comprehensive HCM solution; |

1

Table of Contents

| • | Core system of record enabling data analytics maintained on a single database; |

| • | Personalized support provided by trained personnel; |

| • | Software-as-a-Service delivery model; |

| • | Cloud-based architecture; and |

| • | Scalability to grow with our clients. |

We sell our solution directly through our internally trained, client-focused and highly skilled sales force based in offices across the United States. We have over 10,000 clients, none of which constituted more than one-half of one percent of our revenues for the year ended December 31, 2013. We believe that as a result of our focus on client retention, we enjoy high client satisfaction as evidenced by an average annual revenue retention rate of 91% from existing clients for the three years ended December 31, 2013. We believe our revenue retention rate understates our client loyalty because this rate also includes former clients that were acquired or otherwise ceased operations.

Since our founding in Oklahoma City in 1998, we have focused on providing an innovative SaaS HCM solution. As of December 31, 2013, we had 840 employees across the United States. For the years ended December 31, 2013, 2012 and 2011, our revenues were $107.6 million, $76.8 million, and $57.2 million, respectively, representing year-over-year growth in revenues of 40% and 34%, respectively. We currently derive most of our revenues from our payroll and tax management applications, which we refer to as payroll processing. We realized net income of $7.7 million, $4.2 million and $1.4 million for the years ended December 31, 2013, 2012 and 2011, respectively.

Industry Background

Large Market Opportunity for HCM Technologies

According to IDC, the U.S. market for HCM applications is comprised of software that automates business processes covering the entire span of an employee’s relationship with his or her employer. IDC estimates that this market, excluding payroll services, will total $5.8 billion in 2014. According to IDC, the U.S. market for payroll services will be an estimated $16.2 billion in 2014. IDC estimates that the international market for HCM applications (excluding the United States) will be $4.1 billion in 2014.

Economic and Technological Trends Are Driving Demand for HCM Solutions

Organizations operating in today’s global economy are continually under pressure to reduce operating costs in order to maintain or improve their competitive positions. As a result, businesses are increasingly making the strategic decision to leverage HCM technologies in order to improve the effectiveness and efficiency of their internal HR and accounting functions and capture opportunities for cost savings. According to IBISWorld, companies often outsource administrative services, such as time and labor management, after initially outsourcing payroll. We believe that businesses increasingly view data concerning their human capital as a critical strategic resource that can result in more informed decision-making.

Organizations are also managing internal costs and administrative burdens by transitioning technological assets from on-premise to the cloud. The rise of cloud computing has supported the SaaS delivery model. According to IDC, the global SaaS market is projected to grow from $23 billion in 2011 to $67 billion in 2016, at a compounded annual growth rate, or CAGR, of 24%.

Incumbent HCM Products Struggle To Meet the Needs of Businesses

We believe that a majority of businesses and organizations in the United States are using multiple HCM systems from more than one vendor, thereby impeding their ability to share data across these systems. Several

2

Table of Contents

incumbent payroll and HCM vendors offer product sets that are comprised of separate systems that require integration. In certain cases, this disparate product offering across several vendors is the result of several acquisitions which often leads to a loosely coupled product set that is marked by significant architectural differences and weak data integration. We believe that this type of offering increases the risk of user or system error and reduces overall effectiveness. Finally, we believe that vendors who pursue market segmentation strategies based on organization size or industry create difficulties for clients who grow, either in size or industry scope, beyond the confines of those vendors’ offerings. A scalable HCM solution based on a core system of record allows for an organization to grow in size and scope without transitioning to a new user interface or back-end database.

The Paycom Solution

We offer an end-to-end SaaS HCM solution that provides our clients and their employees with immediate access to accurate and secure information and analytics 24 hours a day, seven days a week from any location. We believe that our solution delivers the following benefits:

| • | Comprehensive HCM Solution. Our solution offers functionality that manages the entire employment life cycle for employers and employees, from recruitment to retirement. Our user-friendly applications streamline client processes and provide clients and their employees with the ability to directly access and manage administrative processes, including applications that identify candidates, onboard employees, manage time and labor, administer payroll deductions and benefits, manage performance, offboard employees and administer post-termination health benefits such as COBRA. |

| • | Core System of Record. Our solution is based on a core system of record that contains payroll and HR information in one convenient database, thereby reducing costs and eliminating the need for multiple software products and vendors and the maintenance of employee data in numerous databases. In addition, our core system of record helps clients minimize the risk of compliance errors due to inaccurate or missing information that results from maintaining multiple databases. |

| • | Data Analytics. Our solution allows clients to analyze accurate employee information to make business decisions based upon actionable, real-time, point-and-click analytics provided through our client dashboard. This functionality helps our clients operate with a more complete and accurate picture of their organization as our solution’s embedded analytics capture the content and context of everyday business events, facilitating fast and informed decision-making from any location. |

| • | Personalized Support Provided by Trained Personnel. Our applications are supported by one-on-one personal assistance from trained specialists. We strive to provide our clients with high levels of service and support to ensure their continued use of our solution for all of their HCM needs. We have maintained high client satisfaction, as evidenced by an average annual revenue retention rate of 91% from existing clients for the three years ended December 31, 2013. |

| • | Software-as-a-Service Delivery Model. Our SaaS delivery model allows clients with a geographically dispersed and mobile workforce to operate more efficiently, and allows these clients to implement, access and use our client-oriented Internet solution on demand and remotely through standard web browsers, smart phones, tablets and other web-enabled devices. |

| • | Secure Cloud-Based Architecture. Our cloud-based architecture allows our solution to be implemented remotely with minimal client interaction, allowing our clients to make a smaller investment in hardware, personnel, implementation time and consulting. |

| • | Scalability to Grow with our Clients. Our solution is highly scalable. We have served a diversified client base ranging in size from one to more than 8,000 employees. Our clients are able to use the same solution while their businesses grow by deploying applications as-needed in real-time. |

3

Table of Contents

Our Strategy for Growth

Our strategy is to continue to establish our solution as the HCM industry standard. To accomplish this, we intend to:

| • | Increase Our Presence in Existing Markets. Although we have clients in all 50 states, we believe a significant opportunity exists to expand our presence within markets where we currently have a sales office. We have a sales office in 24 of the 50 largest Metropolitan Statistical Areas, or MSAs, in the United States based on 2010 U.S. census data, only one of which is served by multiple sales teams. We believe that the 50 largest MSAs in the United States could collectively support at least 100 additional sales teams. Each sales office is typically staffed with one sales team, with each team comprised of approximately seven to nine sales professionals. We plan to increase our presence in our existing markets by adding sales offices and increasing the number of our sales teams to further penetrate and effectively capture these markets. |

| • | Expand Into Additional Markets. We plan to continue expanding our sales capability by opening sales offices in certain metropolitan areas where we currently have no sales teams. We have identified 50 untapped metropolitan areas where we can potentially open a new sales office staffed with at least one sales team. Since September 2012, we have opened sales offices in Baltimore, Detroit, Indianapolis, Minneapolis, New York, Philadelphia, San Francisco, Seattle and Silicon Valley. We intend to open six to eight additional offices over the next two years, as well as potentially expand over the longer term into international markets. |

| • | Enlarge our Existing Client Relationships. We believe a significant growth opportunity exists in selling additional applications to our current clients. During the year ended December 31, 2013, all of our clients, including our new clients, on average utilized 5.2 of our 18 then available applications. During that same period, however, new clients on average utilized 6.2 applications. We believe that there is a significant opportunity to sell additional applications to our existing clients. As we extend and strengthen the functionality of our solution, we will continue to invest in initiatives to increase the adoption of our solution and maintain our high levels of client satisfaction. |

| • | Target Larger Clients. We believe larger employers represent a substantial opportunity to increase the number of clients and to increase our revenue per client, with limited incremental cost to us. To further capitalize on this opportunity, we intend to target larger businesses opportunistically. |

| • | Maintain Our Leadership in Innovation by Strengthening and Extending our Solution. We intend to continue to use our in-house development efforts, which are heavily based upon proactive research and client input, to extend the functionality and range of our solution in the future. |

Selected Risks Associated with Our Business

Our business is subject to a number of risks and uncertainties, including those highlighted in the section “Risk Factors” immediately following this prospectus summary. Some of these risks include:

| • | Our business depends substantially on our clients’ continued use of our applications, their purchases of additional applications from us and our ability to add new clients. |

| • | The market in which we participate is highly competitive, and if we do not compete effectively, our business, operating results or financial condition could be adversely affected. |

| • | We have historically derived a majority of our revenue from payroll processing and our efforts to increase the use of our other HCM applications may not be successful and may reduce our revenue growth rate. |

4

Table of Contents

| • | If our security measures are breached or unauthorized access to data of our clients or their employees is otherwise obtained, our solution may not be perceived as being secure, clients may reduce, limit or stop using our solution and we may incur significant liabilities. |

| • | If the SaaS market develops more slowly than we expect or declines, our growth may slow or stall, and our business could be adversely affected. |

| • | If we are not able to develop enhancements or new applications, keep pace with technological developments or respond to future disruptive technologies, our business could be adversely affected. |

| • | Our business and operations are experiencing rapid growth and organizational change and if we fail to manage our growth effectively, we may be unable to execute our business plan, maintain high levels of satisfaction or adequately address competitive challenges. |

| • | Our financial results may fluctuate due to many factors, some of which may be beyond our control. |

Our Principal Stockholders

Following the completion of this offering, Welsh, Carson, Anderson & Stowe X, L.P., or WCAS X, WCAS Capital Partners IV, L.P., or WCAS Capital IV, and WCAS Management Corporation, together with WCAS X and WCAS Capital IV, the WCAS Funds, which are affiliates of Welsh, Carson, Anderson & Stowe, L.P., or Welsh, Carson, Anderson & Stowe, will own approximately 57.8% of our outstanding common stock, or 55.8% if the underwriters exercise in full their option to purchase additional shares. In addition, following the completion of this offering, the WCAS Funds and the other parties to the Amended and Restated Stockholders Agreement, or the Stockholders Agreement, will own approximately 81.7% of our outstanding shares of common stock, or 79.7% of our outstanding shares of common stock if the underwriters exercise in full their option to purchase additional shares. As a result of this ownership and the provisions of the Stockholders Agreement, the WCAS Funds will have control over votes on fundamental and significant corporate matters and transactions.

So long as the parties to the Stockholders Agreement own a majority of our outstanding shares of common stock, we will be a “controlled company” under the NYSE Listed Company Manual. Under these standards, a company of which more than 50% of the voting power for the election of directors is held by another company or group is a “controlled company” that is not required to comply with certain corporate governance requirements. We intend to rely on certain exemptions following the offering, and may rely on any of these exemptions for so long as we are a “controlled company.” See “Risk Factors—Risks Related to This Offering and Ownership of Our Common Stock” and “Certain Relationships and Related Party Transactions—Stockholders Agreement.”

Welsh, Carson, Anderson & Stowe is a leading U.S. private equity investor focused on information/business services and healthcare. Welsh, Carson, Anderson & Stowe has raised and managed $20 billion in capital and has a current portfolio of over 30 companies.

Corporate Information

We were founded in 1998. Software is a Delaware corporation that was formed in October 2013 to undertake this offering. Our principal executive offices are located at 7501 W. Memorial Road, Oklahoma City, Oklahoma 73142 and our telephone number is (405) 722-6900. Our website is www.paycom.com. Information contained on our website or that can be accessed through our website is not incorporated by reference in this prospectus.

“Paycom,” the Paycom logo and other trademarks or service marks of Paycom appearing in this prospectus are the property of Paycom. Trade names, trademarks and service marks of other companies appearing in this prospectus are the property of their respective holders.

5

Table of Contents

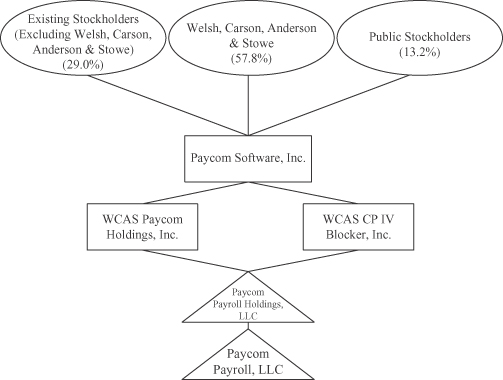

The Reorganization

Software is a newly formed Delaware corporation. In anticipation of this offering, we consummated the Reorganization (as defined herein), effective as of January 1, 2014. For additional information concerning the Reorganization, see “The Reorganization.”

The following diagram depicts our corporate structure immediately after the completion of this offering. We will directly or indirectly hold 100% of the ownership interests in each of our subsidiaries:

6

Table of Contents

THE OFFERING

| Common stock offered by us |

4,606,882 shares |

| Common stock offered by the selling stockholders |

2,038,118 shares |

| Option to purchase additional shares of common stock |

The selling stockholders have granted the underwriters an option, exercisable for 30 days after the date of this prospectus, to purchase up to an additional 996,750 shares of common stock. |

| Shares outstanding after the offering |

50,333,739 shares |

| Use of proceeds |

We estimate that our net proceeds from the sale of the common stock that we are offering will be approximately $78.0 million, assuming an initial public offering price of $19.00 per share, which is the midpoint of the price range on the cover page of this prospectus, and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. We intend to use the net proceeds from this offering for (i) the repayment of a 10% Senior Note due 2022 issued by us to an affiliate of Welsh, Carson, Anderson & Stowe in the amount of approximately $18.8 million, (ii) the repayment of a 14% Note due 2017 issued by WCAS Paycom Holdings, Inc., or WCAS Holdings, that we assumed in connection with the Reorganization in the amount of approximately $46.2 million (including certain payments made pursuant to a contribution agreement) and (iii) general corporate purposes, including additions to working capital and capital expenditures. See “Use of Proceeds.” |

| We will not receive any proceeds from the sale of shares offered by the selling stockholders, who include a director and entities affiliated with members of our board of directors. |

| Dividend policy |

We do not currently plan to pay a regular dividend on our common stock following this offering. See “Dividend Policy.” |

| Risk factors |

See “Risk Factors” beginning on page 12 and the other information included elsewhere in this prospectus for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

| Directed Share Program |

At our request, the underwriters have reserved for sale at the initial public offering price up to 5% of the shares offered hereby for our officers, directors, employees, clients, suppliers, vendors and friends and relatives of our employees. The number of shares available for sale to the general public will be reduced to the extent such persons purchase such reserved shares. Chad Richison, our president, chief executive officer and director, Craig E. Boelte, our chief financial officer, William X. Kerber III, our chief information officer, and |

7

Table of Contents

| Frederick C. Peters II, our director, on behalf of themselves and certain of their affiliates, have indicated an interest in purchasing an aggregate of up to approximately $1.3 million in shares of our common stock in this offering pursuant to the Directed Share Program. Any reserved shares not so purchased will be offered by the underwriters to the general public on the same basis as the others offered hereby. Any participants will be prohibited from selling, pledging or assigning any shares sold to them pursuant to this program for a period of 180 days after the date of this prospectus. The Directed Share Program will be arranged through our lead underwriter, Barclays Capital Inc. |

| NYSE trading symbol |

“PAYC” |

In this prospectus, unless otherwise indicated, the number of shares of common stock outstanding and the other information based thereon:

| • | exclude 8,081,447 shares of restricted common stock that are subject to time-based or performance-based vesting conditions, including 217,378 shares of restricted stock that vest upon the sale of our common stock in the initial public offering; |

| • | exclude 3,269,434 shares of our common stock reserved for future issuance under the Paycom Software, Inc. 2014 Long-Term Incentive Plan, or the 2014 Plan, that we adopted in connection with the Reorganization; and |

| • | do not reflect any exercise by the underwriters of their option to purchase 996,750 additional shares of our common stock from the selling stockholders. |

8

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL DATA

The following table summarizes our consolidated financial data as of the dates and for the periods indicated. We have derived the summary consolidated statements of income data for the years ended December 31, 2013, 2012 and 2011 and the summary consolidated balance sheet data as of December 31, 2013 and 2012 from our audited consolidated financial statements included elsewhere in this prospectus. Historical results are not necessarily indicative of results for any future period. We have derived the summary unaudited pro forma condensed consolidated financial data for the years ended December 31, 2013, 2012 and 2011 from the unaudited pro forma condensed consolidated financial statements set forth under “Unaudited Pro Forma Condensed Consolidated Financial Information.”

The summary consolidated financial data set forth below should be read together with “Capitalization,” “Selected Consolidated Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Unaudited Pro Forma Condensed Consolidated Financial Information” and our consolidated financial statements and the related notes thereto, which are included elsewhere in this prospectus. The following tables summarize our consolidated and pro forma results:

| Pro forma(4) | ||||||||||||||||||||||||

| Year Ended December 31, |

Year Ended December 31, |

|||||||||||||||||||||||

| 2013 | 2012 | 2011 | 2013 | 2012 | 2011 | |||||||||||||||||||

| (in thousands, except per unit and share data) | ||||||||||||||||||||||||

| Consolidated statement of income data: |

||||||||||||||||||||||||

| Revenues |

$ | 107,601 | $ | 76,810 | $ | 57,206 | $ | 107,601 | $ | 76,810 | $ | 57,206 | ||||||||||||

| Expenses(1) |

||||||||||||||||||||||||

| Cost of revenues: |

||||||||||||||||||||||||

| Operating expenses |

19,070 | 14,895 | 12,287 | 19,070 | 14,895 | 12,287 | ||||||||||||||||||

| Depreciation |

1,821 | 1,431 | 987 | 1,821 | 1,431 | 987 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total cost of revenues |

20,891 | 16,326 | 13,274 | 20,891 | 16,326 | 13,274 | ||||||||||||||||||

| Administrative expenses: |

||||||||||||||||||||||||

| Sales and marketing |

42,681 | 29,255 | 22,244 | 42,681 | 29,255 | 22,244 | ||||||||||||||||||

| Research and development |

2,146 | 1,632 | 1,225 | 2,146 | 1,632 | 1,225 | ||||||||||||||||||

| General and administrative |

28,884 | 19,450 | 14,707 | 29,191 | 19,452 | 14,714 | ||||||||||||||||||

| Depreciation and amortization |

3,682 | 4,092 | 4,300 | 3,682 | 4,092 | 4,300 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total administrative expenses |

77,393 | 54,429 | 42,476 | 77,700 | 54,431 | 42,483 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Operating income |

9,317 | 6,055 | 1,456 | 9,010 | 6,053 | 1,449 | ||||||||||||||||||

| Interest expense |

(2,805 | ) | (2,171 | ) | (134 | ) | (683 | ) | (774 | ) | (134 | ) | ||||||||||||

| Other income, net |

1,199 | 354 | 108 | 553 | 36 | 108 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Income before income taxes |

7,711 | 4,238 | 1,430 | 8,880 | 5,315 | 1,423 | ||||||||||||||||||

| Provision for income taxes |

— | — | — | 3,462 | 2,068 | 573 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net income |

7,711 | $ | 4,238 | $ | 1,430 | 5,418 | $ | 3,247 | $ | 850 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Less: Distribution to Series C Preferred Unitholder |

|

(6,467 |

) |

(4,806 | ) | — | ||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||

| Net income (loss) available to Series A Preferred Unitholders and common unit holders |

1,244 | $ | (568 | ) | $ | 1,430 | ||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||

| Net income (loss) per Series A Preferred Unit and common unit/share(2) |

||||||||||||||||||||||||

| Basic |

$ | 1.30 | $ | (0.60 | ) | $ | 1.53 | $ | 0.11 | $ | 0.06 | $ | 0.02 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Diluted |

$ | 1.22 | $ | (0.57 | ) | $ | 1.49 | $ | 0.10 | $ | 0.06 | $ | 0.02 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Weighted average units/shares outstanding(2) |

||||||||||||||||||||||||

| Basic |

955,983 | 948,181 | 935,750 | 51,107,379 | 51,107,379 | 51,107,379 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Diluted |

1,018,305 | 1,004,436 | 960,611 | 51,792,542 | 51,792,542 | 51,792,542 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Other financial data: |

||||||||||||||||||||||||

| EBITDA(3) |

$ | 16,019 | $ | 11,932 | $ | 6,851 | $ | 15,066 | $ | 11,612 | $ | 6,844 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Adjusted EBITDA(3) |

$ | 19,700 | $ | 12,751 | $ | 7,016 | $ | 18,747 | $ | 12,431 | $ | 7,009 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

9

Table of Contents

| As of December 31, | ||||||||

| 2013 | 2012 | |||||||

| (in thousands) |

||||||||

| Consolidated balance sheet data: |

||||||||

| Cash and cash equivalents |

$ | 13,273 | $ | 13,435 | ||||

| Restricted cash |

369 | 368 | ||||||

| Working capital (deficit)(5) |

(7,933 | ) | 5,096 | |||||

| Property, plant and equipment, net |

38,671 | 25,139 | ||||||

| Deferred revenue |

12,572 | 8,393 | ||||||

| Long-term debt, including current portion |

21,090 | 14,110 | ||||||

| Long-term debt due to related party |

14,682 | 14,440 | ||||||

| Member’s capital |

63,645 | 63,542 | ||||||

| Common stock |

— | — | ||||||

| Accumulated deficit |

(13,385 | ) | (8,871 | ) | ||||

| Total members’ equity |

50,260 | 54,671 | ||||||

| (1) | Incentive-based compensation expense included in the consolidated statements of income data above was as follows: |

| Year Ended December 31, |

||||||||||||

| 2013 | 2012 | 2011 | ||||||||||

| (in thousands) | ||||||||||||

| Cost of revenues (operating expenses) |

$ | 222 | $ | 87 | $ | 36 | ||||||

| Sales and marketing |

114 | 83 | 57 | |||||||||

| Research and development |

345 | 100 | 25 | |||||||||

| General and administrative |

253 | 233 | 47 | |||||||||

|

|

|

|

|

|

|

|||||||

| $ | 934 | $ | 503 | $ | 165 | |||||||

|

|

|

|

|

|

|

|||||||

| (2) | Net income (loss) per Series A Preferred Unit and common unit and weighted average units outstanding represent the earnings per unit reported in the consolidated statements of income for the years ended December 31, 2013, 2012 and 2011 that are included elsewhere in this prospectus. Pro forma net income per share of common stock and the weighted average shares of common stock outstanding reflect the estimated number of shares of common stock we expect to have outstanding upon the completion of this offering as discussed in Note (4) below. |

| (3) | We use earnings before interest, tax, depreciation and amortization, or EBITDA, and Adjusted EBITDA as supplemental measures to review and assess our performance. We define EBITDA as net income, plus interest expense and depreciation and amortization and Adjusted EBITDA as net income, plus interest expense, depreciation and amortization, incentive-based compensation expense and certain transaction expenses that are not core to the Company’s operations. EBITDA and Adjusted EBITDA are metrics that we believe are useful to investors in evaluating our operating performance and facilitating comparison with other peer companies, many of which use similar non-GAAP financial measures to supplement results under accounting principles generally accepted in the United States of America, or U.S. GAAP. |

EBITDA and Adjusted EBITDA are not measures of financial performance under U.S. GAAP, and should not be considered a substitute for net income, which we consider to be the most directly comparable U.S. GAAP measure. EBITDA and Adjusted EBITDA have limitations as analytical tools, and when assessing our operating performance, you should not consider EBITDA or Adjusted EBITDA in isolation, or as a substitute for net income or other consolidated statements of income data prepared in accordance with U.S. GAAP. EBITDA and Adjusted EBITDA may not be comparable to similar titled measures of other companies and other companies may not calculate such measures in the same manner as we do.

The following table reconciles net income to EBITDA and Adjusted EBITDA and pro forma net income to pro forma EBITDA and pro forma Adjusted EBITDA:

| Pro forma(4) | ||||||||||||||||||||||||

| Year Ended December 31, |

Year Ended December 31, |

|||||||||||||||||||||||

| 2013 | 2012 | 2011 | 2013 | 2012 | 2011 | |||||||||||||||||||

| Consolidated statements of income data: |

(in thousands) | |||||||||||||||||||||||

| Net income |

$ | 7,711 | $ | 4,238 | $ | 1,430 | $ | 5,418 | $ | 3,247 | $ | 850 | ||||||||||||

| Interest expense |

2,805 | 2,171 | 134 | 683 | 774 | 134 | ||||||||||||||||||

| Taxes |

— | — | — | 3,462 | 2,068 | 573 | ||||||||||||||||||

| Depreciation and amortization |

5,503 | 5,523 | 5,287 | 5,503 | 5,523 | 5,287 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| EBITDA |

16,019 | 11,932 | 6,851 | 15,066 | 11,612 | 6,844 | ||||||||||||||||||

| Incentive-based compensation expense(a) |

934 | 503 | 165 | 934 | 503 | 165 | ||||||||||||||||||

| Transaction expenses(b) |

2,747 | 316 | — | 2,747 | 316 | — | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Adjusted EBITDA |

$ | 19,700 | $ | 12,751 | $ | 7,016 | $ | 18,747 | $ | 12,431 | $ | 7,009 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

10

Table of Contents

| (a) | Represents incentive-based compensation expense reflected in Note (1) above. Pro forma incentive-based compensation expense is the same as that reported under the historical periods as there are no pro forma adjustments to incentive-based compensation expense recorded in our consolidated statements of income for the years ended December 31, 2013, 2012 and 2011. |

| (b) | Represents one-time transaction expenses associated with the April 2012 Corporate Reorganization (as defined herein) and indirect incremental legal and accounting costs and expenses included in general and administrative expenses in the anticipation of and planning for this offering. |

| (4) | The pro forma data reflects: (i) the Reorganization, and (ii) the effect of a portion of the net offering proceeds which will be used to repay the 10% Senior Note due 2022 issued by us to an affiliate of Welsh, Carson, Anderson & Stowe in the amount of approximately $18.8 million and the 14% Note due 2017 issued by WCAS Holdings that we assumed in connection with the Reorganization in the amount of approximately $46.2 million (including certain payments made pursuant to a contribution agreement). Any additional net offering proceeds have been excluded for the purposes of the pro forma financial information. |

| (5) | Working capital (deficit) is defined as current assets, excluding restricted cash, less current liabilities, excluding current portion of deferred revenue. |

11

Table of Contents

Investing in our common stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below before making a decision to invest in our common stock. Our business, operating results or financial condition could be adversely affected by any of these risks, as well as other risks not currently known to us or that we currently consider immaterial. The trading price of our common stock could decline due to any of these risks, and, as a result, you may lose all or part of your investment. Before deciding whether to invest in our common stock, you should also refer to the other information contained in this prospectus, including our consolidated financial statements and the related notes.

Risks Related to Our Business and Industry

Our business depends substantially on our clients’ continued use of our applications, their purchases of additional applications from us and our ability to add new clients. Any decline in our clients’ continued use of our applications or purchases of additional applications could adversely affect our business, operating results or financial condition.

In order for us to maintain or improve our operating results, it is important that our current clients continue to use our applications and purchase additional applications from us, and that we add additional clients. Our clients have no obligation to continue to use our applications, and may choose not to continue to use our applications at the same or higher level of service, if at all. In the past, some of our clients have elected not to continue to use our applications. Moreover, our clients generally have the right to cancel their agreements with us for any or no reason by providing 30 days prior written notice.

Our client retention rates may fluctuate as a result of a number of factors, including the level of client satisfaction with our applications, pricing, the prices of competing products or services, mergers and acquisitions affecting our client base, reduced hiring by our clients or reductions in our clients’ spending levels. If our clients do not continue to use our applications, renew on less favorable terms, fail to purchase additional applications, or if we fail to add new clients, our revenue may decline, and our business, operating results or financial condition could be adversely affected.

The market in which we participate is highly competitive, and if we do not compete effectively, our business, operating results or financial condition could be adversely affected.

The market for HCM software is highly competitive, rapidly evolving and fragmented. We expect competition to intensify in the future with the introduction of new technologies and market entrants. Many of our current and potential competitors are larger and have greater brand name recognition, longer operating histories, more established relationships in the industry and significantly greater financial, technical and marketing resources than we do. As a result, some of these competitors may be able to:

| • | adapt more rapidly to new or emerging technologies and changes in client requirements; |

| • | develop superior products or services, gain greater market acceptance and expand their product and service offerings more efficiently or rapidly; |

| • | bundle products and services that we may not offer or in a manner that provides our competitors with a price advantage; |

| • | take advantage of acquisition and other opportunities for expansion more readily; |

| • | maintain a lower cost basis; |

| • | adopt more aggressive pricing policies and devote greater resources to the promotion, marketing and sales of their products and services; and |

| • | devote greater resources to the research and development of their products and services. |

12

Table of Contents

Some of our principal competitors offer their products or services at a lower price, which has resulted in pricing pressures. Similarly, some competitors offer different billing terms, which has resulted in pressures on our billing terms. If we are unable to maintain our pricing levels and our billing terms, our operating results would be negatively impacted. In addition, pricing pressures and increased competition generally could result in reduced sales, reduced margins, losses or the failure of our solution to achieve or maintain widespread market acceptance, any of which could adversely affect our business, operating results or financial condition.

We compete with firms that provide HCM solutions by various means. Many providers continue to deliver legacy enterprise software, but as demand for greater flexibility and access to information grows, we believe there will be increased competition in the delivery of HCM cloud-based solutions by other SaaS providers. Our competitors offer HCM solutions that overlap with one, several or all categories of applications offered by our solution. Our talent acquisition and talent management applications compete primarily with Cornerstone OnDemand, Inc., Oracle Corporation, SAP AG and Workday, Inc. Our payroll applications, including payroll processing, compete primarily with Automatic Data Processing, Inc., or ADP, Ceridian Corporation, Concur Technologies, Inc., Intuit, Inc., Paychex, Inc. and The Ultimate Software Group, Inc. Our HR management applications compete primarily with ADP, Ceridian Corporation, Oracle Corporation, Paychex, Inc., SAP AG, and Workday, Inc. Our time and labor management applications compete primarily with ADP, Ceridian Corporation and The Ultimate Software Group, Inc. All of our larger competitors compete with us across multiple application categories. In addition, our HCM solution continues to face competition from in-house payroll and HR systems and departments as well as HR systems and software sold by third-party vendors.

Competition in the HCM solutions market is primarily based on service responsiveness, product quality and reputation, breadth of service and product offering and price. Many of our competitors are able to devote greater resources to the development, promotion and sale of their products and services. In addition, many of our competitors have established marketing relationships, access to larger client bases and major distribution agreements with consultants, software vendors and distributors. In addition, some competitors may offer software that addresses one or a limited number of HCM functions at a lower price point or with greater depth than our solution. As a result, our competitors may be able to respond more quickly and effectively than we can to new or changing opportunities, technologies, standards or client requirements. Further, some potential clients, particularly large enterprises, may elect to develop their own internal solutions. If we are unable to compete effectively, our business, operating results or financial condition could be adversely affected.

We have historically derived a majority of our revenue from payroll processing and our efforts to increase the use of our other HCM applications may not be successful and may reduce our revenue growth rate.

To date we have derived a majority of our revenue from payroll processing. For the years ended December 31, 2013, 2012 and 2011, payroll processing represented approximately 58%, 60% and 68% of our total revenues, respectively. Compared to payroll processing, our participation in other HCM applications markets is relatively new, and it is uncertain whether our revenue from other HCM applications will continue to grow. The relatively limited extent to which our other HCM applications have been adopted by our clients, and the uncertainty regarding the adoption of any new applications beyond our existing applications, may make it difficult to evaluate our business because the potential market for such applications remains uncertain. Our HCM solution may not achieve and sustain the high level of market acceptance that is critical for the success of our business. The failure to increase the use of our HCM applications and any new applications developed by us may reduce our revenue growth rate, which could adversely affect our business, operating results or financial condition.

If our security measures are breached, or unauthorized access to data of our clients or their employees is otherwise obtained, our solution may not be perceived as being secure, clients may reduce the use of or stop using our solution and we may incur significant liabilities.

Our solution involves the collection, storage and transmission of clients’ and their employees’ confidential and proprietary information, including personal or identifying information, as well as financial and payroll data. Unauthorized access or security breaches could result in the loss of information, litigation, indemnity obligations

13

Table of Contents

and other liability. While we have security measures in place to protect client and employee information and prevent data loss and other security breaches, if these measures are breached as a result of third-party action, employee error, malfeasance or otherwise, and someone obtains unauthorized access to our clients’ data, our reputation could be damaged, our business may suffer and we could incur significant liability. Because the techniques used to obtain unauthorized access or to sabotage systems change frequently, we may not be able to anticipate these techniques and implement adequate preventative measures. Cyber liability insurance may be inadequate or may not be available in the future on acceptable terms, or at all. In addition, our cyber liability insurance policy may not cover all claims made against us, and defending a suit, regardless of its merit, could be costly and divert management’s attention.

Any actual or perceived breach of our security could damage our reputation, cause existing clients to discontinue the use of our solution, prevent us from attracting new clients, or subject us to third-party lawsuits, regulatory fines or other action or liability, which could adversely affect our business, operating results or financial condition.

If the SaaS market develops more slowly than we expect or declines, our growth may slow or stall, and our business could be adversely affected.

The SaaS market is not as mature as the market for on-premise enterprise software, and it is uncertain whether SaaS will achieve and sustain high levels of demand and market acceptance. Our success will depend not only on strong demand for HCM services in general, but also to a substantial extent on the widespread adoption of SaaS. Many companies have invested substantial personnel and financial resources to integrate traditional enterprise software into their businesses, and therefore may be reluctant or unwilling to migrate to SaaS. It is difficult to predict client adoption rates and demand for our solution, the future growth rate and size of the SaaS market or the entry of competitive products. The expansion of the SaaS market depends on a number of factors, including the cost, performance and perceived value associated with SaaS, as well as the ability of SaaS providers to address security and privacy concerns. If other SaaS providers experience security incidents, loss of client data, disruptions in delivery or other problems, the market for SaaS applications as a whole, including our solution, may be negatively affected. If SaaS does not achieve widespread adoption, or there is a reduction in demand for SaaS caused by a lack of client acceptance, technological challenges, weakening economic conditions, security or privacy concerns, competing technologies and products, decreases in corporate spending or otherwise, our growth may slow or stall, and our business could be adversely affected.

Any interruption or failure of our data centers could impair our ability to effectively provide our solution and adversely affect our business.

We serve all of our clients from our two data centers located in Oklahoma and Texas. These locations are vulnerable to damage or interruption from severe weather, tornados, terrorist attacks, earthquakes, floods, fires, power loss, telecommunications failures, computer viruses or cyber-attacks. They are also subject to break-ins, sabotage, intentional acts of vandalism and other misconduct. Our solution depends on the continuing operation of our data centers and any damage to or failure of our data centers could result in interruptions in our services. Any interruption in our service could damage our reputation, cause our clients to terminate their use of our solution and prevent us from gaining new or additional business from current clients, which could have an adverse effect on our business, operating results or financial condition.

Any significant disruption in our SaaS network infrastructure could harm our reputation and expose us to significant costs.

Our SaaS network infrastructure is a critical part of our business operations. Our clients access our solution through standard web browsers, smart phones, tablets and other web-enabled devises, and depend on us for fast and reliable access to our solution. In the future, we may experience disruptions in our computing and communications infrastructure. Factors that may cause such disruptions include:

| • | human error; |

14

Table of Contents

| • | security breaches; |

| • | telecommunications failures or outages from third-party providers; |

| • | computer viruses or cyber-attacks; |

| • | acts of terrorism, sabotage or other intentional acts of vandalism; |

| • | unforeseen interruption or damages experienced in moving hardware to a new location; |

| • | tornados, fires, earthquakes, floods and other natural disasters; and |

| • | power loss. |

If our SaaS network infrastructure or our clients’ ability to access to our solution is interrupted, client and employee data from recent transactions may be permanently lost and we could be exposed to significant claims by clients, particularly if the access interruption is associated with problems in the timely delivery of funds due to employees. Any significant instances of system downtime could negatively affect our reputation and ability to retain clients and sell our solution, which would adversely impact our revenue.

We have also experienced significant growth in the number of clients, transactions and client and employee data that our network infrastructure supports. We seek to maintain sufficient excess capacity in our network infrastructure to meet the needs of all of our clients and their employees and to facilitate the rapid provision of new client deployments and the expansion of existing client deployments. Any changes in the service levels at our data centers or any errors, defects, disruptions or other performance problems with our network infrastructure could adversely affect our reputation and may result in lengthy interruptions in the availability of our solution. Any interruptions in the availability of our solution might reduce our revenues, cause us to issue refunds to clients or adversely affect our retention of existing clients.

If our solution fails to perform properly, our reputation could be adversely affected and our market share could decline.

Our solution is inherently complex and may in the future contain, or develop, undetected defects or errors. Any defects in our applications could adversely affect our reputation, impair our ability to sell our applications in the future and result in significant costs to us. The costs incurred in correcting any application defects may be substantial and could adversely affect our business, operating results or financial condition. Any defects in functionality or that cause interruptions in the availability of our applications could result in:

| • | loss or delayed market acceptance and sales of our applications; |

| • | termination of service agreements or loss of clients; |

| • | credits or refunds to clients; |

| • | breach of contract, breach of warranty or indemnification claims against us, which may result in litigation; |

| • | diversion of development and service resources; and |

| • | injury to our reputation. |

Because of the large amount of data that we collect and manage, it is possible that hardware failures or errors in our systems could result in data loss or corruption, or cause the information that we collect to be incomplete or contain inaccuracies that our clients regard as significant. Furthermore, the availability or performance of our solution could be adversely affected by a number of factors, including the failure of our network system or solution or security breaches. We may be liable to our clients for damages they may incur resulting from certain of these events. In addition to potential liability, if we experience interruptions in the availability of our solution, our reputation could be adversely affected and we could lose clients.

15

Table of Contents

Our clients might assert claims against us in the future alleging that they suffered damages due to a defect, error, or other failure of our solution. Our errors and omissions insurance may be inadequate or may not be available in the future on acceptable terms, or at all. In addition, our policy may not cover all claims made against us, and defending a suit, regardless of its merit, could be costly and divert management’s attention.

If we do not effectively expand and train our sales force and our support teams, we may be unable to add new clients and retain existing clients.

We need to continue to expand our sales force and support team members in order to grow our client base and increase our revenues. Identifying and recruiting qualified personnel and training them in the use of our solution requires significant time, expense and attention and it can take a substantial amount of time before our sales representatives and support team members are fully-trained and productive. We may be unable to hire or retain sufficient numbers of qualified individuals in the markets where we currently, or intend in the future to do business, and our recent hires and planned hires may not achieve desired productivity levels in a reasonable period of time or become as productive as we expect. If these expansion efforts are unsuccessful or do not generate a corresponding increase in revenues, our business, operating results or financial condition could be adversely affected.

If we are not able to develop enhancements and new applications, keep pace with technological developments or respond to future disruptive technologies, we might not remain competitive and our business could be adversely affected.

Our future success will depend on our ability to adapt and innovate. To attract new clients and increase revenue from existing clients, we need to enhance, add new features and improve our existing applications and introduce new applications. The success of any enhancements or new features and applications depends on several factors, including timely completion, introduction and market acceptance. We may expend significant time and resources developing and pursuing sales of a particular application that may not result in revenues in the anticipated time frame or at all, or may not result in revenue growth sufficient to offset increased expenses. If we are unable to successfully develop enhancements, new features or new applications to meet client needs, our business and operating results could be adversely affected.

In addition, because our applications are designed to operate on a variety of network, hardware and software platforms using Internet tools and protocols, we will need to continuously modify and enhance our applications to keep pace with changes in Internet-related hardware, software, communication, browser and database technologies. If we are unable to respond in a timely and cost-effective manner to these rapid technological developments, our current and future applications may become less marketable and less competitive or even obsolete.

Our success is subject to the risk of future disruptive technologies. If new technologies emerge that are able to deliver HCM solutions at lower prices, more efficiently or more conveniently, such technologies could adversely impact our ability to compete.

The market for our solution among large companies may be limited if these companies demand customized features and functions that we do not offer.

Prospective clients, especially larger companies, may require customized features and functions unique to their business processes that we do not offer. In order to ensure we meet these requirements, we may devote a significant amount of support and services resources to larger prospective clients, increasing the cost and time required to complete sales with no guarantee that these clients will continue to use our solution. We may not be successful in implementing any customized features or functions. If prospective clients require customized features or functions that we do not offer, or that would be difficult for them to deploy themselves, then the market for our solution will be more limited and our business could be adversely affected.

16

Table of Contents

Our business and operations are experiencing rapid growth and organizational change. If we fail to manage such growth and change effectively, we may be unable to execute our business plan, maintain high levels of service or adequately address competitive challenges.

We have experienced, and may continue to experience, rapid growth in our headcount and operations, which has placed, and may continue to place, significant demands on our management, operational and financial resources. For example, our headcount has grown from 523 employees as of December 31, 2011 to 840 employees as of December 31, 2013 and we have expanded from 18 offices as of December 31, 2011 to 24 offices as of December 31, 2013. We have also experienced significant growth in the number of clients, transactions and client and employee data that our infrastructure supports. Finally, our organizational structure and recording systems and procedures are becoming more complex as we improve our operational, financial and management controls. Our success will depend in part on our ability to manage this growth and organizational change effectively. To manage the expected growth of our headcount and operations, we will need to continue to improve our operational, financial and management controls and our reporting systems and procedures. Our ability to add additional offices may be constrained by the willingness and availability of qualified personnel to help staff and manage any new offices. The failure to effectively manage growth could result in difficulties or delays in obtaining clients, selling additional applications to our clients, declines in quality or client satisfaction of our applications, increases in costs, and difficulties in introducing new applications or other operational difficulties, any of which could adversely affect our ability to retain and attract clients or sell additional applications to our existing clients.

Our business, operating results or financial condition could be adversely affected if our clients are not satisfied with our deployment or technical support services.

Our business depends on our ability to satisfy our clients, both with respect to our applications and the technical support provided to help clients use the applications that address the needs of their businesses. We use our in-house deployment personnel to implement and configure our solution and provide support to our clients. If a client is not satisfied with the quality of our solution or the applications delivered or the support provided, we could be required to incur additional costs to address the situation, the profitability of our solution might be negatively affected, and the client’s dissatisfaction with our deployment service could damage our ability to sell additional applications to that client. In addition, our sales process is highly dependent on the reputation of our solution and applications and on positive recommendations from our existing clients. Any failure to maintain high-quality technical support, or a market perception that we do not maintain high-quality support, could adversely affect our reputation, our ability to sell our applications to existing and prospective clients, and our business, operating results or financial condition.

If we fail to retain key employees and recruit qualified technical and sales personnel, our business could be adversely affected.

We believe that our success depends on the continued services of our senior management and other key employees, including Chad Richison, Craig E. Boelte, Jeffrey D. York and William X. Kerber III. In addition, because our future success is dependent on our ability to continue to enhance and introduce new applications, we are heavily dependent on our ability to attract and retain qualified software developers and IT personnel with the requisite education, background and industry experience. To continue to execute our growth strategy, we must also attract and retain qualified sales, marketing and operational personnel capable of supporting a larger and more diverse client base. The loss of the services of a significant number of our developers or sales professionals could be disruptive to our development efforts or business relationships. In addition, if any of our key employees joins a competitor or decides to otherwise compete with us, we may experience a material disruption of our operations and development plans, which may cause us to lose clients or increase operating expenses or divert management’s attention to recruit replacements for the departed key employees.

17

Table of Contents

Our financial results may fluctuate due to many factors, some of which may be beyond our control.

Our results of operations, including the levels of our revenues, costs of revenues, administrative expenses, operating income, cash flow and deferred revenue, may vary significantly in the future and the results of any one period should not be relied upon as an indication of future performance. Our financial results may fluctuate as a result of a variety of factors, many of which are outside of our control, and as a result, may not fully reflect the underlying performance of our business. Fluctuation in our financial results may negatively impact the value of our common stock. Factors that may cause our financial results to fluctuate from period to period include, without limitation:

| • | our ability to attract new clients or sell additional applications to our existing clients; |

| • | the number of new clients and their employees, as compared to the number of existing clients and their employees in a particular period; |

| • | the mix of clients between small, mid-sized and large organizations; |

| • | the extent to which we retain existing clients and the expansion or contraction of our relationship with them; |

| • | the mix of applications sold during a period; |

| • | changes in our pricing policies or those of our competitors; |

| • | seasonal factors affecting payroll processing, demand for our applications or potential clients’ purchasing decisions; |

| • | the amount and timing of operating expenses, including those related to the maintenance and expansion of our business, operations and infrastructure; |

| • | the timing and success of new applications introduced by us and the timing of expenses related to the development of new applications and technologies; |

| • | the timing and success of current and new competitive products and services by our competitors; |

| • | economic conditions affecting our clients, including their ability to outsource HCM solutions and hire employees; |

| • | other changes in the competitive dynamics of our industry, including consolidation among competitors or clients; |

| • | our ability to manage our existing business and future growth, including expenses related to our data centers and the expansion of such data centers and the addition of new offices; |

| • | the effects and expenses of acquisition of third-party technologies or businesses and any potential future charges for impairment of goodwill resulting from those acquisitions; |

| • | network outages or security breaches; and |

| • | general economic, industry and market conditions. |

Certain of our operating results and financial metrics are difficult to predict as a result of seasonality.

We have historically experienced seasonality in our revenues because a significant portion of our recurring revenues relate to the annual processing of payroll forms such as Form W-2 and Form 1099. Because these forms are typically processed in the first quarter of the year, first quarter revenues are generally higher than subsequent quarters. We expect this seasonality to continue in the future, which may cause fluctuations in certain of our operating results and financial metrics, and thus make such results and metrics difficult to predict.

18

Table of Contents

If we fail to adequately protect our proprietary rights, our competitive advantage could be impaired and we may lose valuable assets, generate reduced revenue or incur costly litigation to protect our rights.

Our success is dependent in part upon our intellectual property. We rely on a combination of copyrights, trademarks, service marks, trade secret laws and contractual restrictions to establish and to protect our intellectual property rights. However, the steps we take to protect our intellectual property may be inadequate. We will not be able to protect our intellectual property if we are unable to enforce our rights or if we do not detect unauthorized use of our intellectual property. Despite our precautions, it may be possible for unauthorized third parties to copy our applications and use information that we regard as proprietary to create products or services that compete with ours.