Attached files

| file | filename |

|---|---|

| EX-10.40 - EX-10.40 - SIRVA INC | d693356dex1040.htm |

| EX-10.46 - EX-10.46 - SIRVA INC | d693356dex1046.htm |

| EX-21.1 - EX-21.1 - SIRVA INC | d693356dex211.htm |

| EX-4.1 - EX-4.1 - SIRVA INC | d693356dex41.htm |

| EX-23.1 - EX-23.1 - SIRVA INC | d693356dex231.htm |

| EX-10.44 - EX-10.44 - SIRVA INC | d693356dex1044.htm |

| EX-10.38 - EX-10.38 - SIRVA INC | d693356dex1038.htm |

| EX-10.42 - EX-10.42 - SIRVA INC | d693356dex1042.htm |

| EX-10.39 - EX-10.39 - SIRVA INC | d693356dex1039.htm |

| EX-4.2 - EX-4.2 - SIRVA INC | d693356dex42.htm |

| EX-10.43 - EX-10.43 - SIRVA INC | d693356dex1043.htm |

| EX-10.45 - EX-10.45 - SIRVA INC | d693356dex1045.htm |

| EX-10.41 - EX-10.41 - SIRVA INC | d693356dex1041.htm |

Table of Contents

As filed with the Securities and Exchange Commission on March 28, 2014

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

SIRVA, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 4700 | 52-2070058 | ||

| (State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

One Parkview Plaza

Oakbrook Terrace, IL 60181

(630) 570-3050

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Thomas Oberdorf

Chief Financial Officer

One Parkview Plaza

Oakbrook Terrace, IL 60181

(630) 570-3050 (Phone)

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

Copies to:

| Alexander D. Lynch, Esq. Weil, Gotshal & Manges LLP 767 Fifth Avenue New York, New York 10153 (212) 310-8000 (Phone) (212) 310-8007 (Fax) |

Rachel W. Sheridan, Esq. Latham & Watkins LLP 555 Eleventh Street, NW, Suite 1000 Washington, DC 20004 (202) 637-2200 (Phone) (202) 637-2201 (Fax) |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer x Smaller reporting company ¨

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price (1)(2) |

Amount of Registration Fee | ||

| Common Stock, $0.01 par value per share |

$175,000,000 | $22,540 | ||

|

| ||||

|

| ||||

| (1) | Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(o) promulgated under the Securities Act. |

| (2) | Includes shares of common stock that may be issuable upon exercise of an option to purchase additional shares granted to the underwriters. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. Neither we nor the selling stockholders may sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and neither we nor the selling stockholders are soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

PROSPECTUS (Subject to Completion)

Dated March 28, 2014

Shares

SIRVA, Inc.

Common Stock

SIRVA, Inc. is offering shares of common stock and the selling stockholders are offering shares of common stock. We will not receive any proceeds from the sale of shares by the selling stockholders. This is our initial public offering and no public market currently exists for our shares of common stock. We expect the public offering price to be between $ and $ per share.

We intend to apply to list our common stock on the New York Stock Exchange (the “NYSE”) or NASDAQ Global Market (“Nasdaq”) under the symbol “ .”

Investing in our common stock involves risks. See ‘‘Risk Factors’’ beginning on page 21.

Price $ A SHARE

| Price to Public |

Underwriting and |

Proceeds to |

Proceeds to |

|||||||||||||

| Per share |

$ | $ | $ | $ | ||||||||||||

| Total |

$ | $ | $ | $ | ||||||||||||

We have granted the underwriters the right to purchase an additional shares of common stock, and the selling stockholders have granted the underwriters the right to purchase an additional shares of common stock.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of common stock to purchasers on or about , 2014.

| MORGAN STANLEY | GOLDMAN, SACHS & CO. | J.P. MORGAN |

| BAIRD | WILLIAM BLAIR |

, 2014.

Table of Contents

You should rely only on the information contained in this prospectus or in any free-writing prospectus we may authorize to be delivered or made available to you. Neither we, the selling stockholders nor the underwriters (or any of our or their respective affiliates) have authorized anyone to provide any information other than that contained in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. Neither we, the selling stockholders nor the underwriters (or any of our or their respective affiliates) take any responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We, the selling stockholders and the underwriters (or any of our or their respective affiliates) are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. The information contained in this prospectus is only accurate as of the date on the front cover of this prospectus. Our business, financial condition, results of operations and prospectus may have changed since that date.

Trademarks and Trade Names

We own or have the rights to use various trademarks, service marks and trade names referred to in this prospectus, including, among others, SIRVA, SIRVA Relocation, Allied, northAmerican, iMove.com and their respective logos. Solely for convenience, we refer to trademarks, service marks and trade names in this prospectus without the ™, SM and ® symbols. Such references are not intended to indicate, in any way, that we will not assert, to the fullest extent permitted by law, our rights to our trademarks, service marks and trade names. Other trademarks, trade names or service marks appearing in this prospectus are the property of their respective owners.

Market and Industry Information

Market data and industry information used throughout this prospectus is based on management’s knowledge of the industry and the good faith estimates of management. We also relied, to the extent available, upon management’s review of independent industry surveys and publications and other publicly available information prepared by a number of sources, including IBISWorld Inc., Information Week, PwC Talent Mobility 2020, Workforce Management, Worldwide ERC and the American Moving and Storage Association. All of the market data and industry information used in this prospectus involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates. Although we believe that these sources are reliable, we cannot guarantee the accuracy or completeness of this information and we have not independently verified this information. While we believe the estimated market position, market opportunity and market size information included in this prospectus is generally reliable, such information, which in part is derived from management’s estimates and beliefs, is inherently uncertain and imprecise. Projections, assumptions and estimates of our future performance and the future performance of the industry in which we operate are necessarily subject to a high

Table of Contents

degree of uncertainty and risk due to a variety of factors, including those described in “Risk Factors,” “Forward-Looking Statements” and elsewhere in this prospectus. These and other factors could cause results to differ materially from those expressed in our estimates and beliefs and in the estimates prepared by independent parties.

Until , 2014 (25 days after the date of this prospectus), all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

ii

Table of Contents

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information that you should consider before investing in our common stock. You should read this entire prospectus, including the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes thereto before making an investment decision. Unless otherwise stated in this prospectus, references to “we,” “our,” “us,” “SIRVA” and the “Company” and similar terms refer to SIRVA, Inc. and its consolidated subsidiaries.

Our Company

We are a leading provider of mobility services for multi-national corporations and government institutions. Our customers, typically corporate human resources departments, use SIRVA’s solutions to optimize the deployment of their professional talent on a global basis—ensuring that their best people are leading their most important initiatives, regardless of where in the world they are located. We serve a blue-chip customer base of more than 1,800 customers, including approximately 28% of the Fortune 500 and two-thirds of the Dow Jones 30.

We play a valuable role as the outsource partner for corporations and government institutions, providing an integrated solution that offers an overall enhanced mobility experience, program control and security for our customers, the relocating employee (the “transferee”) and the transferee’s family. We provide a suite of over 50 distinct mobility services, including relocation assistance and moving services. We enable our corporate and institutional customers to outsource their mobility needs, allowing them to focus on executing their strategies and enhancing their productivity. In 2013, we executed over 280,000 mobility events for our corporate, government and consumer customers. Our approximately 2,700 employees, located both within our offices and on-site within our customers’ human resources departments, provide a customized solution for each transferee.

Consistent with our marketing slogan “Everything you need, everywhere you need it,” we provide our customers with what we believe to be the most global and complete mobility solution. This has enabled us to maintain long-term relationships with our customers, as reflected by our high customer retention rates. For example, from 2011 to 2013, we achieved a 98% retention rate for our corporate customers in our Mobility Solutions segment.

A transfer to a new location is a challenging time for the transferee, their spouse/partner and their entire family, and can be even more difficult if the job is located in a new country with a different language and culture. We assist the corporation and the transferee with each aspect of the mobility process to ensure a smooth relocation and we generate revenue from each of the mobility services that we provide. Our relocation services, or mobility solutions, are provided by us and our network of third-party providers, and our moving services, or mobility networks, are provided through our agent/franchise network.

1

Table of Contents

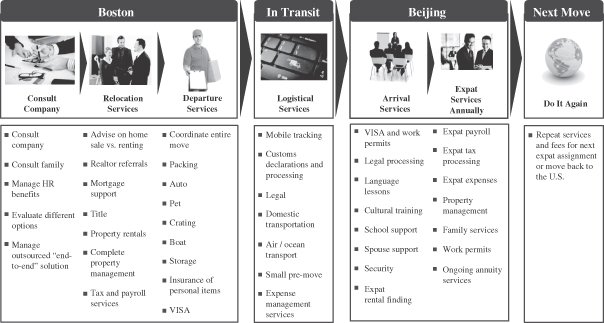

The following is an example of the transfer of an executive and his family from Boston to Beijing and illustrates the mobility services that we provide:

Our expertise in providing mobility services lies in our proprietary processes, our technological capabilities and our knowledge of the complex technical and logistical components of mobilizing talent on a global basis. For example, our technical knowledge of relocation requirements in the key areas of employment law, governance, expatriate taxes, compensation, customs, immigration, cultural integration, logistics and global supply chain optimization help ensure successful mobility events worldwide.

Our technological capabilities are core to our business model and customer value proposition. Our technology team has 140 employees and a dedicated research and development budget. We utilize leading technology to provide everyone involved in a mobility event—from the human resources department, the transferee and the transferee’s family to our agents/franchises and third-party providers—with a secure connection to our flexible technology network. Our technological capabilities have been acknowledged by our customers and their technology experts. In 2013, we were named on the Information Week 500 list of Top Technology Innovators, an annual listing of the most innovative corporate users of business technology in the United States across all industries, for the 11th consecutive year, earning the #126 position.

We operate an asset-light agent/franchise network, which has attributes similar to a traditional franchise model. We provide our mobility services through 1,224 locations, including 66 company-operated locations and 1,158 agent/franchise locations, in approximately 170 countries. We deliver our relocation services, or mobility solutions, directly and through contracted third-party providers. Our network of third-party providers allows us to deliver specialized, local expertise in a wide range of countries and manage such services without incurring the costs of establishing them on an in-house basis. Our agents and franchises operate in the United States and Canada under our nationally recognized moving brands Allied and northAmerican, and in the rest of the world under our Allied brands. Our mobility networks, established over many decades, allow us to deliver a quality customer experience and manage the move, while the agents and franchises provide the capital and labor-intensive aspects of the operations, including moving vehicles, warehouses and packaging and transportation support teams.

2

Table of Contents

Over the period from 2008 to 2013, we completed a series of business initiatives designed to improve our financial performance. These initiatives included implementing new policies intended to improve our risk management, focusing on an asset-light strategy, hiring a new management team, divesting non-core businesses that were not directly related to providing mobility services, and lowering our indebtedness.

Approximately 71% of our 2013 total revenue was derived from contracts with our corporate customers, which generally have durations ranging from one to four years. Approximately 29% of our 2013 total revenue was not from contracts, but was largely funded by corporations that provide “lump sum” payments to their transferring employees. We have a diversified customer base, with no single customer accounting for more than 2.4% of our total revenue in 2013 and our top ten customers accounting for approximately 12% of our total revenue in 2013.

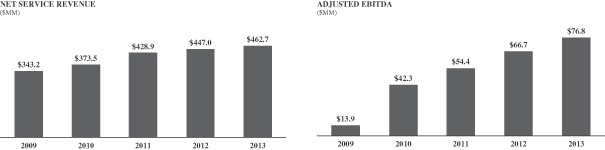

Between 2009 and 2013, we increased our total revenue from $1,676.4 million to $1,994.2 million, Net Service Revenue from $343.2 million to $462.7 million, Adjusted EBITDA from $13.9 million to $76.8 million and net income (loss) from $(78.0) million to $9.7 million. For fiscal years 2011, 2012 and 2013, our total revenue was $1,932.4 million, $1,950.8 million and $1,994.2 million, respectively, Net Service Revenue was $428.9 million, $447.0 million and $462.7 million, respectively, Adjusted EBITDA was $54.4 million, $66.7 million and $76.8 million, respectively, and net income (loss) was $(52.9) million, $(1.4) million and $9.7 million, respectively. For information on how we define Adjusted EBITDA and Net Service Revenue and reconciliations of net income (loss) to Adjusted EBITDA and total revenue to Net Service Revenue, see “—Summary Historical Financial and Other Data.”

Our Market Opportunity

Mobility Services are Critical for Talent Management

The talent needs of multi-national corporations are becoming increasingly global and complex. Strategic business decisions normally depend upon the deployment of employees to the most important projects with speed and agility, which drives demand for mobility services. Mobility services consist of managing numerous, distinct mobility events involving the relocation of the transferee, the transferee’s family and the transferee’s household goods from their originating location to a destination location, while also managing the related legal requirements, visa and immigration requirements, human resources policies and transferee-specific needs.

Trend Toward Outsourcing Mobility Services

In 2012, 90% of U.S.-based corporations surveyed by Worldwide ERC outsourced mobility services. Although large corporations often have a mobility function or capability within their human resources departments, they do not typically possess the expertise or local resources across diverse geographies to manage the numerous processes involved in a mobility event. Accordingly, most corporations outsource these functions to mobility services providers to leverage the provider’s scale, expertise and technology. When seeking a provider of outsourced mobility services, human resources departments seek consistent quality of experience for their transferees, global capabilities with local service delivery, regulatory compliance and security, robust technology capabilities and program management and control.

Large and Growing Global Market

Global mobility services is a large and growing market, consisting of a range of highly diversified services that enable corporations and government institutions to deploy executives and key personnel to locations throughout the world. Globalization, GDP performance, corporate spending and employment levels are key growth drivers in this market. Several trends, including corporate expansion into emerging markets and increased regulatory complexity, are also driving the shift to outsourced mobility services.

3

Table of Contents

U.S. Market

The U.S. mobility services market is well developed and is the largest mobility services market in the world. Third-party research describes U.S. mobility services as consisting of different sub-components, with relocation services and moving services as the largest.

| • | Relocation Services. IBISWorld Inc. (“IBISWorld”) estimates that the market for U.S. relocation services was $11.7 billion for 2013 and is forecasted to grow at an annualized rate of 6.9% from 2013 to 2018 to a total of $16.3 billion. Relocation services include expatriate services, temporary housing, property management, realtor advice, home sale and purchasing assistance and other value-added services. According to IBISWorld, we were a market leader in U.S. relocation services with an 18% U.S. market share in 2012. |

| • | Moving Services. IBISWorld estimates that the market for U.S. moving services was $15.5 billion market for 2014 and is forecasted to grow at an annualized rate of 2.0% from 2014 to 2019 to a total of $17.1 billion. Moving services include moving, valuables protection, records management and storage, integrated logistics and information services and other value-added services. According to the American Moving and Storage Association (“AMSA”), we had a 29% U.S. market share for interstate moves in 2013 among companies that self-report to AMSA. |

International Markets

The international mobility services market has also experienced growth. In 2013, international mobility managers reported that companies moving employees to or from international regions grew an estimated 12% in Central and South America, 10% in the Middle East and 9% in Australia, New Zealand, India and Northeast Asia. According to PricewaterhouseCoopers’ Talent Mobility 2020, the average number of mobile employees from global organizations has grown 25% over the past decade and is estimated to grow an additional 50% by 2020.

| • | Europe. We believe Europe is the second largest location for headquarters of large corporations. 151 of the Global Fortune 500 corporations are headquartered in Europe and account for a significant amount of global mobility volume. |

| • | Asia and Emerging Markets. We believe China, Brazil and India are growing markets for mobility services. As more corporations in these countries develop into global leaders, we believe their mobility needs will increase. Additionally, countries in the Middle East, including the United Arab Emirates, Qatar and Saudi Arabia, are becoming increasingly important to global corporations, driven partially by the energy industry, but also by technology, industrial, retail and business services sectors. |

| • | Australia. Australia is a relatively mature market, which is primarily impacted by the mining sector. Our revenue growth in this region has been predominantly driven by the addition of new services, new customer wins and the strength of our Allied and SIRVA Relocation brands. According to IBISWorld, we had the #1 position in Australia’s moving services market in 2013. |

Competitive Landscape

The mobility services industry is characterized by several well-established competitors. The substantial start-up costs associated with establishing the required infrastructure, establishing a global reach, building an extensive agent network and developing a credible reputation with multi-national corporations could deter new competitors from entering the market. Additionally, global mobility events often require local service delivery capabilities in a wide range of foreign markets and mobility-related local domain expertise, thereby limiting the risk that the industry will be subject to the introduction of disruptive technologies or that existing providers can be replaced by low-cost, off-shoring business models.

4

Table of Contents

Corporate Lump Sum

In addition to relocation benefits programs provided to key executives, corporations also provide mid and low-level employees with lump sum payments to purchase mobility services directly. We believe there is an opportunity to help these transferees acquire mobility services and to enable human resources departments to manage their lump sum programs and provide additional benefits to these transferees. Individual consumers may also seek similar assistance with mobility services in connection with their moves, which we believe is another market opportunity. To take advantage of this, in October 2013 we launched our LumpSum Xpress Marketplace. This program provides an online marketplace for mobility services, enabling transferees to manage their lump sum benefits online and enabling human resources departments to administer and track their lump sum programs.

Do-It-Yourself, Self-Storage and Containerization

There is also a Do-It-Yourself (“DIY”) moving and storage market. In contrast to a full-service corporate solution, DIY relocations are typically completed directly by the transferee or consumer and are normally provided at a lower price point. The DIY market is generally comprised of lower level employees who receive few benefits and consumers that need a more economical service to relocate to their new job and provides an additional market opportunity for mobility solutions providers. In March 2014, we acquired SMARTBOX Portable Self Storage (“SMARTBOX”), a DIY moving and storage company, to address this market opportunity.

Differentiated Delivery Model

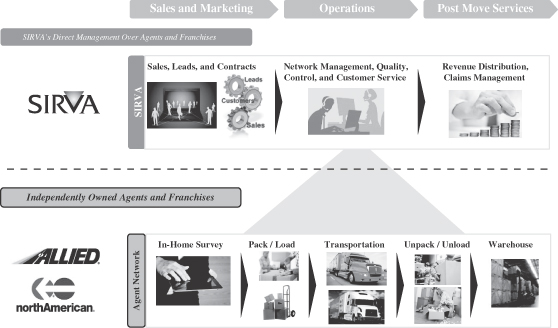

We place great value in offering an integrated end-to-end mobility solution to our customers. Both domestically and internationally, we strategically apply our core competencies to directly deliver select mobility services through our own staff and to deliver other services either through our agents and franchises or through partnerships with third-party mobility service providers. This approach enables us to relocate transferees across the globe, while delivering these specialized services with consistent quality on a local basis. Our domain experts work closely with our agent/franchise network and local third-party providers in order to maintain control over the services supply chain and provide our customers and their transferees with a secure experience.

Our independently owned agent network performs the moving and related services that we offer to our customers located in the United States and Canada. The agent network supports the physical transportation of a transferee’s household goods under our two nationally recognized moving brands—Allied and northAmerican. Our network in the United States and Canada, which is similar to a franchise model, includes 419 third-party agents serving customers in 712 locations. We do not own the assets required to move our customers in these locations. In contrast, our agents own and manage these assets required to execute and deliver moving services. They maintain their own fleet of transportation vehicles and real estate portfolio of warehouses and have packing/unpacking crews on their payroll. We believe our agent network positions us to maintain a low fixed-cost structure and provides us with significant operating leverage. We recently renewed the majority of the contracts with our agent network through January 2018.

5

Table of Contents

The following graphic illustrates examples of the services we provide to our agent network and the activities that are performed by our agent network:

Competitive Strengths

The following is a description of the competitive strengths that have helped establish us as a leading global mobility service provider:

Our Broad and Integrated Suite of Service Offerings

We provide an integrated end-to-end mobility solution for our customers. We take ownership of the key aspects of our customers’ global mobility programs and deliver over 50 distinct service offerings through our in-house domain experts, our network of exclusive agents and franchises and our third-party providers. Our broad, integrated suite of services enables us to provide a customized solution for each mobility event, including transferee-specific services at origin, moving of household goods and destination services, and in the case of an international relocation, on-going expatriate services during the foreign assignment.

Our Global Scale

We provide services across six continents and in over 170 countries. We serve more than 1,800 corporate customers globally, including 28% of the Fortune 500 and two-thirds of the Dow Jones 30. We operate two of the four largest nationally recognized moving network brands in the United States—Allied and northAmerican—which are leveraged across a network of 419 third-party agents in the United States and Canada. Internationally, we provide moving services under our Allied brands.

Our Local Delivery and Execution

We have built a worldwide local delivery capability in over 170 countries through our 66 company-operated locations, our 1,158 agent and franchise locations and our third-party provider network. These local agent,

6

Table of Contents

franchises and third-party provider relationships enable us to serve the complex needs of large multi-national corporations even in challenging or undeveloped markets while maintaining an asset-light structure. We actively manage our agent, franchise and third-party provider network, enabling us to deliver a consistent quality of service. We also maintain the ability to provide select services directly through our in-house domain experts to control sensitive aspects of a relocation. For example, our employees provide increased safety for the transferee’s family and protection over their personal information by directly delivering services in many challenging or developing countries, which we believe provides us with a competitive advantage.

Our Deep Domain Expertise

Our deep domain expertise in mobility services and our extensive global experience servicing the corporate human resources departments of Global Fortune 500, mid-size companies and small businesses enables us to accurately anticipate the complexities inherent in any mobility event. We typically review and update our customers’ mobility policy as a key aspect of on-boarding a new customer. We apply our domain expertise to establish our proprietary mobility processes and robust technological capabilities, and combine them with our employees’ knowledge of, and experience in, the complex technical, logistical and technological components in mobilizing talent around the world. Our employees are highly trained and we have certified relocation and moving experts on our teams to serve customers. In addition to providing an enhanced transferee experience and better control, we believe our expertise reduces the risk of non-compliance with laws in different geographies. This helps prevent some of the most critical and costly errors for our customers, such as the deportation of a transferred executive due to an unforeseen visa issue or tax compliance problems in the United States or a foreign country due to inaccurate reporting.

A Leading Technology Capability

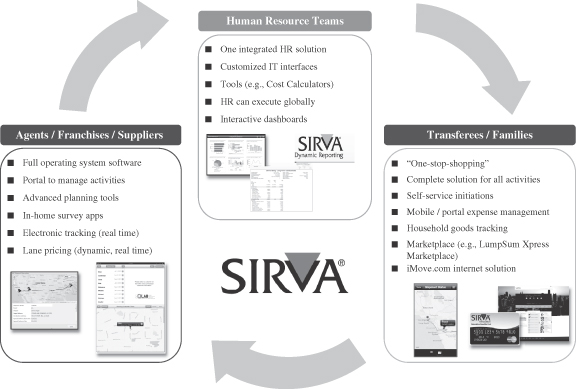

Our technology platform is integrated with our customers’ human resources departments, our agent/franchise network and our third-party providers. As of December 31, 2013, we employed 140 full-time technology professionals to develop, maintain and support our technology platforms and services. We have developed an extensive knowledge of the technologies deployed for mobility solutions, which has enabled us to design and build our technology and deploy it to our customers. Our proprietary global assignment platform, SIRVA Connect, provides us with the ability to estimate costs for a move, initiate a transaction, measure and track progress and manage key aspects of a mobility event, as well as collaborate with human resources departments. Transferees are also able to manage their transfer, allowing them to track the movement of their household goods and view and request additional mobility services directly via our platform, which is accessible on the transferee’s laptop, tablet or mobile device. We have the ability to update our technology independently of the corporate IT departments with which we integrate, giving us the freedom to update and innovate our platform on our own schedule.

Our Trusted, Well-Recognized Global Brands

|

|

|

We market the SIRVA brand to human resource professionals globally. We also own two of the top brands in moving services in the United States and Canada—Allied and northAmerican. According to the 2013 Workforce Management Relocation Hotlist, SIRVA held a 19% share globally in relocation services in 2013. In 2013, we were a market leader in U.S. relocation services according to IBISWorld.

7

Table of Contents

Management Team

The core values of our leadership team are integrity, collaboration, customer service and capital efficiency. Our leadership team has a diverse set of management experiences from companies including General Electric, McKinsey & Company, AlliedSignal, Getty Images, Prudential Financial, Xerox, Ricoh, Motorola and Dell Inc. Both our CEO, Wes Lucas, and our CFO, Tom Oberdorf, have over 14 years of experience in their respective roles. Since Mr. Lucas joined us in 2008, Net Service Revenue has grown from $343.2 million to $462.7 million over the period from 2009 to 2013, which represents a compound annual growth rate (“CAGR”) of 8%, and Adjusted EBITDA has grown from $13.9 million to $76.8 million over the period from 2009 to 2013, which represents a CAGR of 53%.

Growth Strategies

We intend to capitalize on our leading position in mobility services and our global scale to increase revenue, enhance our profitability and maximize the return on investment for our stockholders. We seek to achieve these objectives by executing on the following key strategies:

Grow Market Share and Win New Customers

We intend to leverage our leading market position, global presence, well-recognized brands, integrated service offering and commitment to delivering a high-quality of service to grow our market share and win new customers. Our recently implemented sales and marketing initiatives, including an expanded sales team, a new global sales strategy, targeted marketing efforts and new agent/franchise sales process will be integral in our efforts to win new customers. We believe that our differentiated technology solutions will also be a key factor in our ability to increase our market share. In 2013, we won four out of the five largest requests for proposal (“RFPs”) that we competed for and signed 41 new U.S. and Canadian corporate relocation customers. We believe that the addition of these new customers will provide incremental revenue and reinforce our leading position in the mobility services market. We are focused on offering customizable solutions, which enable us to win business and develop long-standing relationships with our customers, leading to a 98% customer retention rate for the period from 2011 to 2013 for our corporate customers in our Mobility Solutions segment.

Expand Globally

We believe there are growth opportunities in Asia, the Middle East, South America and Africa as corporations in these markets continue to expand their global reach, increasing their need for global mobility services, and as U.S. and European multinational corporations continue to focus on growing in these regions. We have an extensive agent/franchise network in these regions, including 85 locations in Asia Pacific, 113 locations in Africa and the Middle East and 63 locations in Central America and South America. In addition, we have 51 company-operated locations in Asia Pacific, three locations in Africa and the Middle East and two locations in Central and South America. In 2012, we hired a team of mobility professionals to lead our growth efforts in Asia, and we have been focused on strengthening our market position in underserved countries in that region, including China, Singapore and Malaysia. Additionally, in 2011 and 2012, we acquired relocation services businesses with locations in India and Brazil and invested in these regions to further strengthen our ability to serve these markets. We are also planning to expand our service offerings in key markets, including offering new immigration services in Malaysia, new destination services in the United Arab Emirates and new relocation services in Qatar.

We are also targeting expansion of our business in Europe. We believe that we can leverage our existing European mobility infrastructure, consisting of 171 agent/franchise locations and two company-operated offices in 42 countries, which we have developed to serve our U.S.-based customers, to market to these European-headquartered companies. We are also investing in sales and marketing capabilities in the region to expand our

8

Table of Contents

customer base. For example, in 2012, we hired a mobility professional with over 20 years of experience in the global mobility industry to lead our European operations. During 2012 and 2013, we had success winning business with three large European-headquartered customers. In addition, in March 2014, we acquired InHouse Relocation GmbH (“InHouse”), a niche German mobility company, to grow our position in Germany.

Increase “Share of Wallet” with Current Customers

Our broad service offerings provide an opportunity to cross-sell our diverse suite of services. Our team of dedicated domain experts works closely with our customers and their transferees to understand their individual needs at every stage of the relocation process and to identify areas where we can increase the quantity and depth of services that we provide to our customers and their transferees. We believe we are positioned to leverage the breadth of our mobility services to expand the scope of our work with a particular customer in a variety of ways. For example, once we have established a relationship with our customers, our account managers seek to add services to the contract, such as our visa services. Our moving counselors also offer transferees additional services during the relocation and at their destination location.

Continue New Product Development

We intend to continue to develop and market new technologies and tools that are designed to solidify our market position, expand our customer base, convert internet leads into revenue generating opportunities and be more responsive to our customers’ needs. We have several projects in various stages of development that we believe can be commercialized into attractive organic growth opportunities. Certain projects in development involve combining our industry expertise, global reach and proprietary technology platform to provide our customers with highly customized solutions. For example, we have recently developed a corporate human resources portal to enable human resources departments to access our mobility services directly, commercialized a global cost estimator and implemented a new reporting tool. We have also developed a portal for transferees so that they can shop directly for services, receive support and track the movement of their household goods. This portal is accessible on the transferee’s mobile phone and tablet. Additionally, we are working on expanding our service offerings to increase customer usage of higher margin services, such as expatriate taxes and compensation services.

Expand Into Adjacent Markets

We are continuously looking for opportunities to enter adjacent markets and capture new business. In October 2013, we launched the LumpSum Xpress Marketplace, targeting individual transferees who receive a lump sum payment to relocate and are obtaining mobility services on their own. These transferees are often a majority of a corporation’s relocating employees and tend to be mid or low-level employees and new hires. We believe this represents an under-served market. Our product provides a portal to our global network of agents, franchises and third-party providers along with our local delivery capability, enabling the transferees to better facilitate their mobility experience and stretch their lump sum allowance by using discounts they earn through our supply chain. The human resources department is now able to offer these transferees a service never before available. The human resources department also benefits from visibility of the relocation services utilized and monies spent, which allows them to better manage this group of transferees.

We are also targeting the estimated $7.0 billion self-storage market and the multi-billion dollar self-moving market and believe that our March 2014 acquisition of SMARTBOX Portable Self Storage (“SMARTBOX”), a DIY moving and storage company, provides a platform for the expansion of our mobility solution into these DIY markets. We believe the SMARTBOX acquisition will allow us to expand our mobility service offering to our corporate customers that want to provide a DIY option to their employees and to consumers looking for a more economical moving and storage option.

9

Table of Contents

Improve Productivity and Operations to Increase Margins

We continually seek to improve our financial and operating performance through productivity improvement initiatives. We utilize Six Sigma, LEAN and other leading operational excellence tools to enhance our productivity. Over the last five years, we have focused on productivity improvements that we believe have positioned us to improve our operating efficiency. We are upgrading our IT systems and modernizing our operating system, installing GPS tracking devices on our agent’s trucks to enable network optimization and automating sales systems to enhance pricing capabilities and invoice processing. We have made significant progress to provide transferees with technology that improves their experience with us and streamlines the implementation of the mobility process. From 2009 to 2013, we reduced selling, general and administrative expense as a percent of Net Service Revenue from 53% to 39%, and Adjusted EBITDA as a percent of Net Service Revenue grew from 4% to 17% over this same period. We believe that there is potential to further increase our productivity.

Revenue Model

The primary driver of our revenue is initiations, which represent the volume of transferees and families engaging in a mobility event with us. A mobility event can last anywhere from a month to several years. The average revenue per initiation varies depending on the complexity of the mobility event and the number and mix of services utilized. The revenue per initiation includes fees paid by the transferee, fees paid by the corporation and referral fees we receive for services provided by contracted third-party providers.

In our Mobility Solutions segment, our initiations vary from multiple premium services for home owners (initiations with home ownerships) to single services, and cover both domestic and global initiations under contracts signed in the United States. The average revenue per initiation involving home owners is typically the highest because of the need for complex mobility services, higher benefit packages provided to employees and higher value of personal possessions. We earn fees for both the relocation of the transferee and their family from one location to another and also for the destination services we provide, which include visa, corporate housing, cultural training, language lessons, school and spousal/partner support, and additional fees from ongoing services including expatriate payroll, expatriate expenses, property management and other services. As part of our broad suite of service offerings, we also provide home purchase and home sale assistance. Home purchase and sale assistance contributes significant revenue overall by enabling us to capture other complex mobility services as part of the bundled offering, partially offset by the corresponding cost of assisting in these home purchase and sale transactions.

In our Mobility Networks segment, initiations are domestic or international in nature. The average revenue per initiation is a function of the mix of services required by the transferee. International initiations are typically the highest revenue per initiation due to more services needed by the transferee. We recognize revenue invoiced to the transferee and incur costs (purchased transportation expense, or “PTE”) for services provided by our agent/franchise network.

We are the sole contractor used for the program management of relocation services to most of our corporate customers in our Mobility Solutions segment. Our periodic conversations with human resource teams regarding

10

Table of Contents

their budgets for mobility events provide an indication of our future revenue, as corporate expenditure on relocation generally follows budget allocations and the corporate programs for employee benefits are difficult to change. These characteristics of our business model, combined with our high customer retention rate, provide us with visibility into our future business performance.

Our Principal Stockholders

Following the consummation of this offering, affiliates of Aurora Capital Group (“Aurora”) and Equity Group Investments (“EGI”) are expected to own approximately % and % of our outstanding common stock, respectively, or % and %, respectively, if the underwriters exercise their option to purchase additional shares in full. As a result, Aurora and EGI will be able to exert significant voting influence over fundamental and significant corporate matters and transactions. See “Risk Factors—Risks Related to this Offering” and “Principal and Selling Stockholders.”

Aurora and EGI may acquire or hold interests that compete directly with us, or may pursue acquisition opportunities that are complementary to our business, making such an acquisition unavailable to us. Our amended and restated certificate of incorporation will contain provisions renouncing any interest or expectancy held by our directors affiliated with Aurora and EGI in certain corporate opportunities. For further information, see “Risk Factors—Risks Related to Our Company and Our Organizational Structure—Each of Aurora and EGI independently has substantial control over us and will be able to influence corporate matters with respect to us. Aurora and EGI may have interests that differ from each other and from those of our other stockholders.”

Aurora Capital Group

Aurora Capital Group, founded in 1991, is a Los Angeles-based private investment firm. Aurora’s Resurgence Funds focus on investing in equity and debt securities of middle-market companies. Aurora acts as a constructive partner with management teams and other stakeholders to help drive financial growth and operational improvements. Its broad investment mandate allows Aurora to be a flexible source of capital in creating tailored solutions for companies across a variety of industries.

Equity Group Investments

Equity Group Investments is a Chicago-based private investment firm founded by Sam Zell over 40 years ago. The firm’s current investment portfolio has equity interests in real estate, energy, logistics, transportation, media and healthcare. EGI’s current holdings also include fixed-income investments in public and private companies.

Risks Affecting Our Business

Investing in our common stock involves a high degree of risk. You should consider carefully the risks described in “Risk Factors” before making a decision to invest in our common stock. If any of these risks actually occur, our business, financial condition and results of operations would likely be materially adversely affected. In such case, the trading price of our common stock would likely decline, and you may lose all or part of your investment. Below is a summary of some of the principal risks that we face.

| • | We face intense competition in each of our operating segments; |

| • | We may be affected by adverse conditions in the global economy or in global financial markets; |

11

Table of Contents

| • | Our customer contracts do not provide for any minimum purchase amounts, and if our customers are not successful, they could decrease the number of initiations or mobility benefits for their employees, and our customers have the ability to terminate their contract with us on short notice; |

| • | Our growth depends, in large part, on continued growth in outsourcing of mobility services; |

| • | We have a history of operating losses and may not maintain profitability in the future; |

| • | We are exposed to risks related to the purchase, ownership, financing and resale of transferred employees’ homes at a loss; |

| • | We contract to provide our premium home sale product on a fixed percentage basis and inaccurate estimates could materially impact the profitability of these services; |

| • | We often face a long selling cycle to secure a new contract with our corporate customers, as well as long implementation periods that require significant resource commitments; |

| • | Our international operations subject us to risks of doing business in foreign countries, including exposure to, and potential fines and other penalties from, anti-corruption laws and export-control regulations, including those promulgated by the Office of Foreign Assets Control (“OFAC”); |

| • | We are dependent on third-party providers and service instability from these providers could increase our operating costs, expose us to liability and reduce our ability to offer services; |

| • | Several of our business activities are highly regulated; and |

| • | Each of Aurora and EGI independently has substantial control over us and will be able to influence corporate matters with respect to us. |

Corporate Information

We are a Delaware corporation. SIRVA, Inc. was incorporated on March 29, 1998. Our principal executive offices are located at One Parkview Plaza, Oakbrook Terrace, IL 60181. Our telephone number at our principal executive offices is (630) 570-3050. Our corporate website is www.sirva.com. The information that appears on our website is not part of, and is not incorporated into, this prospectus.

12

Table of Contents

THE OFFERING

| Common stock offered by us |

shares ( shares if the underwriters exercise their option to purchase additional shares in full). | |

| Common stock offered by the selling stockholders |

shares ( shares if the underwriters exercise their option to purchase additional shares in full). | |

| Common stock to be outstanding after this offering |

shares ( shares if the underwriters exercise their option to purchase additional shares in full). | |

| Option to purchase additional shares of common stock |

The underwriters also have the option to purchase up to an additional shares of common stock from us and an additional shares of common stock from the selling stockholders identified in this prospectus. The underwriters can exercise this option at any time within 30 days from the date of this prospectus. | |

| Use of proceeds |

We estimate that the net proceeds to us from this offering will be approximately $ million, after deducting underwriting discounts and commissions and estimated expenses payable by us in connection with this offering. This assumes a public offering price of $ per share, which is the midpoint of the range set forth on the cover of this prospectus. We intend to use approximately $ of the net proceeds from this offering to redeem all of our outstanding Series A Preferred Stock, including accumulated dividends, and to use the remainder for general corporate purposes. We will not receive any of the proceeds from the sale of common stock by the selling stockholders. See “Use of Proceeds.” | |

| Dividend policy |

We do not anticipate paying any dividends on our common stock in the foreseeable future; however, we may change this policy in the future. See “Dividend Policy.” | |

| Voting rights |

Each share of our common stock will entitle its holder to one vote on all matters to be voted on by stockholders generally. See “Description of Capital Stock.” | |

| Risk factors |

Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 21 of this prospectus for a discussion of factors you should carefully consider before investing in our common stock. | |

| Proposed NYSE or Nasdaq symbol |

“ .” | |

13

Table of Contents

Unless otherwise indicated, the number of shares of common stock to be outstanding after this offering excludes:

| • | shares of common stock reserved for future grant under our compensation plans; |

| • | shares of our common stock issuable upon the exercise of options to purchase shares of our common stock outstanding as of , 2014, with a weighted average exercise price of $ per share; |

Unless otherwise indicated, all information in this prospectus:

| • | assumes an initial public offering price of $ per share, the midpoint of the range set forth on the cover of this prospectus. |

| • | assumes no exercise of the underwriters’ option to purchase up to additional shares of common stock from us and an additional shares of common stock from the selling stockholders; |

| • | gives effect to our amended and restated certificate of incorporation and our amended and restated bylaws, which will be in effect prior to the consummation of this offering; and |

| • | gives effect to a -for-1 stock split of our common stock prior to the consummation of this offering. |

14

Table of Contents

SUMMARY HISTORICAL FINANCIAL AND OTHER DATA

The following table sets forth our summary historical financial and other data for the periods and as of the dates indicated. We derived our summary consolidated statement of operations data for the years ended December 31, 2013, 2012 and 2011 and our balance sheet data as of December 31, 2013 from our audited consolidated financial statements included elsewhere in this prospectus. We derived our summary consolidated statement of operations data for the fiscal years ended December 31, 2010 and 2009 from our unaudited consolidated financial statements which are not included in this prospectus. The unaudited consolidated financial statements have been prepared on the same basis as the audited consolidated financial statements and, in our opinion, reflect all adjustments necessary for the fair presentation of the financial information set forth in those statements.

The summary unaudited as adjusted balance sheet data as of December 31, 2013 has been prepared to give effect to the issuance of shares of our common stock in this offering at an assumed initial public offering price of $ , which is the midpoint of the range set forth on the cover of this prospectus. The following unaudited summary as adjusted financial information is presented for illustrative purposes only and is not necessarily indicative of the financial position that would have occurred if the relevant transactions had been consummated on the date indicated.

Our historical results are not necessarily indicative of future operating results. You should read the information set forth below in conjunction with “Selected Historical Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and the related notes thereto included elsewhere in this prospectus.

| Year Ended December 31, | ||||||||||||||||||||

| 2013 | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||

| (in millions, except share and per share data) | ||||||||||||||||||||

| (unaudited) | ||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||

| Revenue: |

||||||||||||||||||||

| Mobility Solutions |

$ | 148.8 | $ | 138.7 | $ | 143.7 | $ | 135.0 | $ | 129.6 | ||||||||||

| Mobility Networks |

1,088.9 | 1,080.9 | 1,017.0 | 901.2 | 839.1 | |||||||||||||||

| Europe, Asia and Emerging Markets |

72.2 | 63.1 | 58.9 | 51.3 | 45.8 | |||||||||||||||

| Australia |

160.5 | 173.7 | 167.1 | 131.0 | 112.8 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total service revenue |

1,470.4 | 1,456.4 | 1,386.7 | 1,218.5 | 1,127.3 | |||||||||||||||

| Home revenue |

523.8 | 494.4 | 545.7 | 491.1 | 549.1 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total revenue |

1,994.2 | 1,950.8 | 1,932.4 | 1,709.6 | 1,676.4 | |||||||||||||||

| Direct expenses: |

||||||||||||||||||||

| Purchased transportation expense |

1,004.6 | 1,006.5 | 953.8 | 839.7 | 781.2 | |||||||||||||||

| Home cost |

526.9 | 497.3 | 549.7 | 496.4 | 552.0 | |||||||||||||||

| Other direct expense |

232.7 | 225.5 | 220.5 | 186.1 | 172.3 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Gross profit |

$ | 230.0 | $ | 221.5 | $ | 208.4 | $ | 187.4 | $ | 170.9 | ||||||||||

| Operating expenses: |

||||||||||||||||||||

| Selling, general and administrative expense |

$ | 180.8 | $ | 184.0 | $ | 192.3 | $ | 173.7 | $ | 180.7 | ||||||||||

| Intangibles amortization |

7.3 | 9.3 | 10.4 | 10.4 | 8.6 | |||||||||||||||

| Restructuring and impairment expense |

2.3 | 2.3 | 3.7 | 0.6 | 7.0 | |||||||||||||||

15

Table of Contents

| Year Ended December 31, | ||||||||||||||||||||

| 2013 | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||

| (in millions, except share and per share data) | ||||||||||||||||||||

| (unaudited) | ||||||||||||||||||||

| Operating income (loss) from continuing operations: |

||||||||||||||||||||

| Mobility Solutions |

$ | 25.5 | $ | 17.9 | $ | 13.1 | $ | 8.5 | $ | 0.2 | ||||||||||

| Mobility Networks |

24.2 | 17.1 | 11.7 | 11.4 | (3.5 | ) | ||||||||||||||

| Europe, Asia and Emerging Markets |

4.6 | 1.3 | 4.8 | 5.3 | 4.9 | |||||||||||||||

| Australia |

2.7 | 1.5 | 1.3 | 0.4 | (0.5 | ) | ||||||||||||||

| Corporate |

(17.4 | ) | (11.9 | ) | (28.9 | ) | (22.9 | ) | (26.5 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total operating income (loss) from continuing operations |

$ | 39.6 | $ | 25.9 | $ | 2.0 | $ | 2.7 | $ | (25.4 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Interest expense, net |

$ | 26.2 | $ | 25.1 | $ | 32.2 | $ | 49.9 | $ | 46.5 | ||||||||||

| Debt extinguishment loss (gain) |

8.0 | (0.3 | ) | 16.8 | — | — | ||||||||||||||

| Other expense, net |

0.5 | — | 1.3 | 0.8 | (0.1 | ) | ||||||||||||||

| Income tax expense |

0.2 | 2.2 | 5.0 | 5.1 | 3.8 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) from continuing operations |

4.7 | (1.1 | ) | (53.3 | ) | (53.1 | ) | (75.6 | ) | |||||||||||

| Income (loss) from discontinued operations, net of tax |

5.0 | (0.3 | ) | 0.4 | 0.3 | (2.4 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) |

9.7 | (1.4 | ) | (52.9 | ) | (52.8 | ) | (78.0 | ) | |||||||||||

| Less: preferred stock dividends |

(20.4 | ) | (27.4 | ) | (18.4 | ) | — | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net loss available to common stockholders |

$ | (10.7 | ) | $ | (28.8 | ) | $ | (71.3 | ) | $ | (52.8 | ) | $ | (78.0 | ) | |||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Per Share Data: |

||||||||||||||||||||

| Basic and diluted loss per common share from continuing operations(1) |

$ | (14.97 | ) | $ | (27.60 | ) | $ | (70.32 | ) | $ | (53.02 | ) | $ | (77.51 | ) | |||||

| Basic and diluted earnings (loss) per common share from discontinued operations(1) |

4.78 | (0.21 | ) | 0.42 | 0.27 | (2.48 | ) | |||||||||||||

| Basic and diluted net loss per common share(1) |

(10.19 | ) | (27.81 | ) | (69.90 | ) | (52.75 | ) | (79.99 | ) | ||||||||||

| Weighted-average basic and diluted common shares outstanding |

1,048,465 | 1,033,450 | 1,019,736 | 1,001,641 | 975,364 | |||||||||||||||

| Other Data: |

||||||||||||||||||||

| Net Service Revenue(2) |

$ | 462.7 | $ | 447.0 | $ | 428.9 | $ | 373.5 | $ | 343.2 | ||||||||||

| Adjusted EBITDA(3) |

76.8 | 66.7 | 54.4 | 42.3 | 13.9 | |||||||||||||||

| Adjusted EBITDA as a percent of Net Service Revenue |

16.6 | % | 14.9 | % | 12.7 | % | 11.3 | % | 4.1 | % | ||||||||||

| As of December 31, 2013 | ||||||||

| Actual | As Adjusted(4) | |||||||

| (unaudited) | ||||||||

| Consolidated balance sheet data: |

||||||||

| Total assets |

$ | 427.3 | $ | |||||

| Short-term debt |

51.6 | |||||||

| Long-term debt (including current portions) |

294.0 | |||||||

| Preferred stock (involuntary liquidation value) |

141.9 | |||||||

| (1) | Basic and diluted earnings (loss) per common share is computed by dividing the net income (loss) available to common shareholders by the weighted-average number of shares of common stock outstanding during the period. Share-based compensation awards were not considered in the determination of diluted earnings (loss) per common share because the impact would be anti-dilutive. |

16

Table of Contents

| (2) | Net Service Revenue and the related ratios presented in this prospectus are supplemental measures of our performance that are not required by, or presented in accordance with, the generally accepted accounting principles in the United States (“GAAP”). Net Service Revenue is not a measurement of our financial performance under GAAP and should not be considered as an alternative to service revenue or total revenue or any other performance measures derived in accordance with GAAP. |

Net Service Revenue is defined as total revenue less purchased transportation expense and home cost.

Management uses Net Service Revenue:

| • | as a measurement used in evaluating our consolidated and segment-level operating performance on a consistent basis; |

| • | as a measurement to assess the amount of service revenue remaining after paying purchased transportation expense, which is the primary cost of providing household goods moving services by our agent/franchise network; |

| • | for planning purposes, including the preparation of our internal annual operating budget; and |

| • | to evaluate the performance and effectiveness of our operational strategies. |

By providing Net Service Revenue, together with a reconciliation to GAAP results, we believe we are enhancing investors’ understanding of our business and our results of operations.

Net Service Revenue has limitations as an analytical tool and you should not consider it in isolation, or as a substitute for, analysis of our results as reported under GAAP. Some of the limitations are:

| • | purchased transportation expense is more directly related to some service revenue types than others, thus the mix of service revenue types will effect gross profits; and |

| • | the mix effect on gross profit will effect gross margin metrics. |

We compensate for these limitations by relying primarily on our GAAP results and use Net Service Revenue as a supplemental metric.

To address these limitations, we reconcile Net Service Revenue to the most directly comparable GAAP measure, total revenue. Further, we also review GAAP measures and evaluate individual measures that are not included in Net Service Revenue.

The following table reconciles total revenue to Net Service Revenue:

| Year Ended December 31, | ||||||||||||||||||||

| 2013 | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||

| (in millions) | ||||||||||||||||||||

| Total revenue |

$ | 1,994.2 | $ | 1,950.8 | $ | 1,932.4 | $ | 1,709.6 | $ | 1,676.4 | ||||||||||

| Purchased transportation expense |

(1,004.6 | ) | (1,006.5 | ) | (953.8 | ) | (839.7 | ) | (781.2 | ) | ||||||||||

| Home cost |

(526.9 | ) | (497.3 | ) | (549.7 | ) | (496.4 | ) | (552.0 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net Service Revenue |

$ | 462.7 | $ | 447.0 | $ | 428.9 | $ | 373.5 | $ | 343.2 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (3) | Adjusted EBITDA and the related ratios presented in this prospectus are supplemental measures of our performance that are not required by, or presented in accordance with, GAAP. EBITDA and Adjusted EBITDA are not measurements of our financial performance under GAAP and should not be considered as alternatives to net income, operating income or any other performance measures derived in accordance with GAAP or as alternatives to cash flow from operating activities as measures of our liquidity. |

EBITDA represents income from continuing operations before interest, taxes, depreciation and amortization. We have included Adjusted EBITDA because we believe it provides management and

17

Table of Contents

investors with additional information to measure our performance and liquidity, estimate our value and evaluate our ability to service debt. Adjusted EBITDA eliminates the effects of items that we do not consider indicative of our core operating performance.

Management uses EBITDA and Adjusted EBITDA or comparable metrics:

| • | as a measurement used in evaluating our consolidated and segment-level operating performance on a consistent basis; |

| • | to calculate incentive compensation for our employees; |

| • | for planning purposes, including the preparation of our internal annual operating budget; |

| • | to evaluate the performance and effectiveness of our operational strategies; and |

| • | to assess compliance with various metrics associated with our debt agreements. |

Management believes the inclusion of the adjustments to EBITDA are appropriate to provide additional information to investors about certain material items that we do not expect to continue at the same level in the future. By providing EBITDA and Adjusted EBITDA, together with a reconciliation to GAAP results, we believe we are enhancing investors’ understanding of our business and our results of operations, as well as assisting investors in evaluating how well we are executing strategic initiatives. We believe EBITDA and Adjusted EBITDA are used by investors as a supplemental measure to evaluate the overall operating performance of companies in our industry.

In evaluating EBITDA and Adjusted EBITDA, you should be aware that in the future we will incur expenses such as those used in calculating EBITDA and Adjusted EBITDA. Our presentation of EBITDA and Adjusted EBITDA should not be construed as an inference that our future results will be unaffected by usual or nonrecurring items.

EBITDA and Adjusted EBITDA have limitations as analytical tools and you should not consider them in isolation, or as substitutes for, analysis of our results as reported under GAAP. Some of the limitations are:

| • | they do not reflect interest expense, or the cash requirements necessary to service interest or principal payments, on our debt; |

| • | they do not reflect our cash expenditures, or future requirements for capital expenditures or contractual commitments; |

| • | they do not reflect changes in, or cash requirements for, our working capital needs; |

| • | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and EBITDA and Adjusted EBITDA do not reflect the cash requirements for such replacements; |

| • | they do not reflect our tax expense or the cash requirements to pay our taxes; |

| • | Adjusted EBITDA does not reflect the non-cash component of employee compensation; |

| • | Adjusted EBITDA does not reflect the impact of earnings or charges resulting from matters we consider not to be indicative of our ongoing operations, as discussed in our presentation of Adjusted EBITDA and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this prospectus; and |

| • | other companies in our industry may calculate these measures differently than we do, limiting their usefulness as comparative measures. |

Because of these limitations, EBITDA and Adjusted EBITDA should not be considered as a measure of discretionary cash available to us to invest in the growth of our business. We compensate for these limitations by relying primarily on our GAAP results and using EBITDA and Adjusted EBITDA only supplementally.

18

Table of Contents

To address these limitations, we reconcile Adjusted EBITDA to the most directly comparable GAAP measure, (loss) income from continuing operations. Further, we also review GAAP measures and evaluate individual measures that are not included in Adjusted EBITDA.

The following table reconciles income (loss) from continuing operations to EBITDA and EBITDA to Adjusted EBITDA:

| Year Ended December 31, | ||||||||||||||||||||

| 2013 | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||

| (in millions) | ||||||||||||||||||||

| Income (loss) from continuing operations |

$ | 4.7 | $ | (1.1 | ) | $ | (53.3 | ) | $ | (53.1 | ) | $ | (75.6 | ) | ||||||

| Interest expense, net |

26.2 | 25.1 | 32.2 | 49.9 | 46.5 | |||||||||||||||

| Income tax expense |

0.2 | 2.2 | 5.0 | 5.2 | 3.7 | |||||||||||||||

| Depreciation and amortization |

25.5 | 28.1 | 27.7 | 27.0 | 28.5 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| EBITDA |

56.6 | 54.3 | 11.6 | 29.0 | 3.1 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Debt extinguishment loss (gain)(a) |

8.0 | (0.3 | ) | 16.8 | — | — | ||||||||||||||

| Restructuring and impairment expense(b) |

2.3 | 2.3 | 3.7 | 0.6 | 7.6 | |||||||||||||||

| Severance and other cost-savings initiative expenses(c) |

1.0 | 2.5 | 5.4 | 2.2 | 0.3 | |||||||||||||||

| Supplier contract termination costs(d) |

— | 0.1 | 5.2 | 6.0 | — | |||||||||||||||

| Pension expense(e) |

2.8 | 3.0 | 2.1 | 2.5 | 2.7 | |||||||||||||||

| Non-recurring professional fees and settlements(f) |

0.5 | 0.1 | 2.7 | 0.6 | — | |||||||||||||||

| Mortgage repurchases and reinsurance losses(g) |

— | 3.9 | 4.2 | — | — | |||||||||||||||

| Acquisitions and new location related costs(h) |

1.0 | 0.3 | 0.8 | — | — | |||||||||||||||

| New customer related costs(i) |

3.0 | — | — | — | — | |||||||||||||||

| Foreign exchange losses(j) |

0.9 | — | 1.4 | 1.3 | 0.1 | |||||||||||||||

| Board of director fees(k) |

— | 0.5 | 0.5 | — | — | |||||||||||||||

| Stock compensation(l) |

0.7 | — | — | 0.1 | 0.1 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Subtotal adjustments |

20.2 | 12.4 | 42.8 | 13.3 | 10.8 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted EBITDA |

$ | 76.8 | $ | 66.7 | $ | 54.4 | $ | 42.3 | $ | 13.9 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (a) | Charges recognized related to debt refinancing activities in the applicable periods as discussed further in Note 7 “Long-term Debt” to the Company’s Audited Financial Statements included elsewhere in this prospectus. |

| (b) | Costs incurred or accrued for various restructuring plans implemented throughout the business, including severance and employee benefits and facility exit costs as discussed further in Note 14 “Restructuring and Impairments” to the Company’s audited financial statements included elsewhere in this prospectus. |

| (c) | Costs incurred in connection with various cost savings initiatives implemented throughout the business including severance and employee benefits, hiring costs and compensation and other costs associated with completion of the debt refinancings. |

| (d) | Costs incurred to cancel certain information technology contracts associated with our decision to insource the functions previously provided by those suppliers. |

| (e) | Expenses associated with our frozen U.S. defined benefit pension plans. See Note 11 “Pension Plans and Other Benefits” to the Company’s audited financial statements included elsewhere in this prospectus. |

19

Table of Contents

| (f) | Legal, consulting and other professional fees and settlements, including tax consulting related to an Australian Tax Authority examination, costs related to our project to migrate applications from a mainframe platform to a server-based platform, and Australia franchise settlements and bad-debt write-offs. |

| (g) | Costs related to mortgage loan sale indemnification liabilities and mortgage reinsurance losses for years prior to us exiting the reinsurance business in 2009. See “Reinsurance Reserves” included within Note 2 “Summary of Significant Accounting Policies” as well as Note 17 “Contingencies” to the Company’s audited financial statements included elsewhere in this prospectus. |

| (h) | Costs incurred to acquire a business in Brazil and expand a business in India, consolidate warehouses in Australia and open new locations in Asia, including legal and professional fees, travel expenses and labor costs to move equipment and customer’s household goods stored by us. |

| (i) | Upfront costs incurred to implement major new customer service capabilities, including compensation and benefits for added staffing and associated hiring and training expenses. |

| (j) | Net losses associated with translation of foreign denominated assets and liabilities. See “Foreign Currency Translation” included within Note 2 “Summary of Significant Accounting Policies” to the Company’s Audited Financial Statements included elsewhere in this prospectus. |

| (k) | Expenses paid for board of director services and reimbursement of board member travel and related expenses. |

| (l) | Non-cash stock-based compensation expense for our board of directors and management. See Note 12 “Capital Stock and Incentive Plans” to the Company’s audited financial statements included elsewhere in this prospectus. |

| (4) | As adjusted information gives effect to this offering and the application of the net proceeds therefrom. |

20

Table of Contents

An investment in our common stock involves a high degree of risk. You should consider carefully the following risks and all of the other information contained in this prospectus, including our consolidated financial statements and related notes to such statements, before investing in our common stock. If any of the following risks actually occur, it could have a material adverse effect on our business, financial condition and results of operations. As a result, the trading price of our common stock could decline and you could lose part or all of your investment.

Risks Related to Our Business and Industry

We face intense competition in each of our operating segments and, if we are unable to compete successfully, it could have a material adverse effect on our business, financial condition and results of operations.