Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Sabra Health Care REIT, Inc. | a8-kgenesis2013auditedfina.htm |

| EX-23.1 - KPMG CONSENT - Sabra Health Care REIT, Inc. | ex231-kpmgconsent2013.htm |

Genesis HealthCare LLC and Subsidiaries

Consolidated Financial Statements

December 31, 2013

Index to Consolidated Financial Statements

In 2011, one of Genesis HealthCare LLC and subsidiaries’ (the Company) indirect members obtained a controlling interest of the Company in a business combination accounted for using the acquisition method. The term “Successor” refers to the Company after giving effect to the consummation of the business combination. The term “Predecessor” refers to the Company prior to giving effect to the consummation of the business combination. See note 3 – “Significant Transactions and Events – April 1, 2011 Transactions.”

Page | |

Independent Auditors’ Report…………………………….………………………………..……………...…. | 2 |

Consolidated Balance Sheets as of December 31, 2013 and 2012 (Successor)……………….…..………… | 3 |

Consolidated Statements of Operations for the years ended December 31, 2013 and 2012 (Successor periods) and 2011 (Predecessor period).....……………………………..…………………….………...…. | 4 |

Consolidated Statements of Comprehensive Income (Loss) for the years ended December 31, 2013 and 2012 (Successor periods) and 2011 (Predecessor period)....……………………………………………… | 5 |

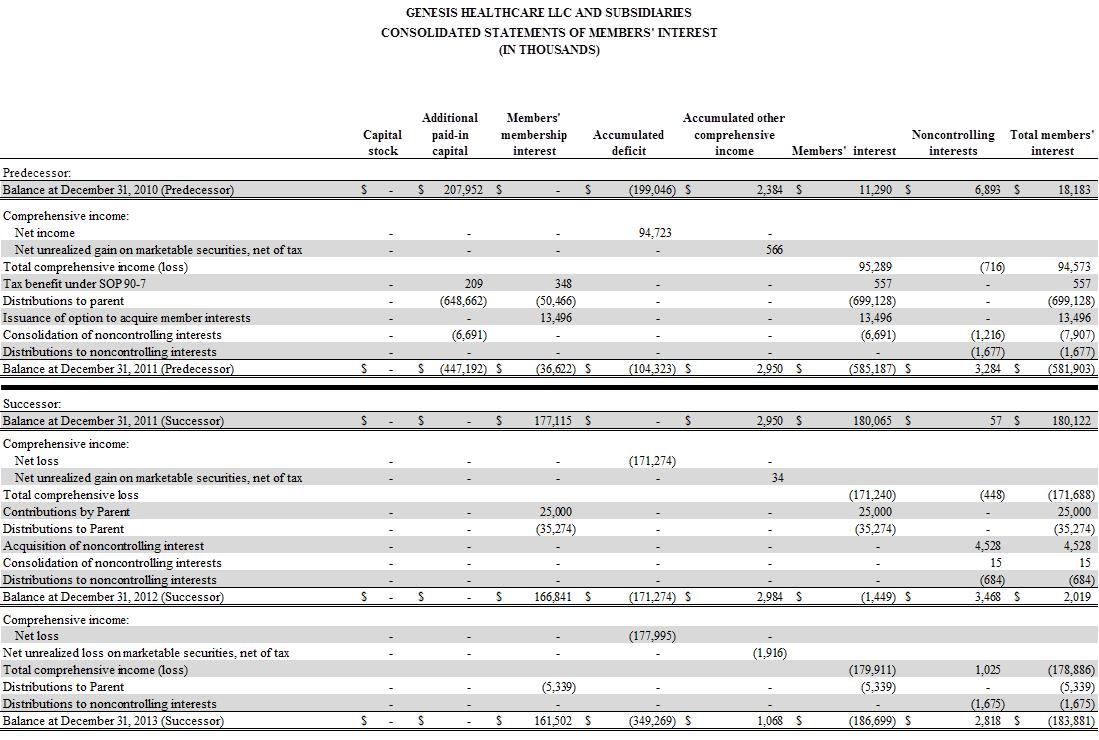

Consolidated Statements of Members’ Interest for the years ended December 31, 2013, 2012 and 2011 (Successor)……….…………………………………….…………….………………………...…....…...... | 6 |

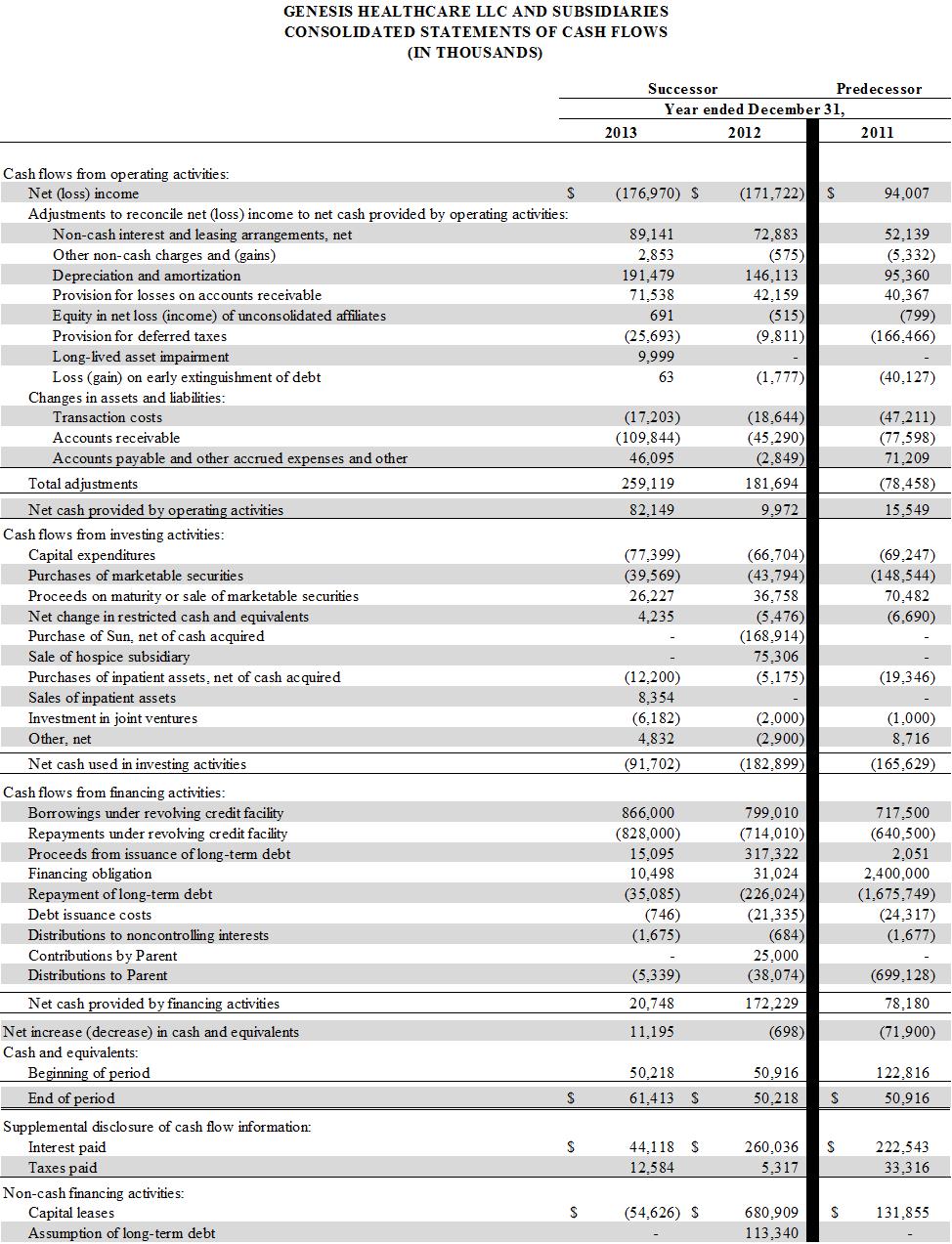

Consolidated Statements of Cash Flows for the years ended December 31, 2013 and 2012 (Successor periods), and 2011 (Predecessor period)………………………………………………………………….... | 7 |

Notes to Consolidated Financial Statements………..…………………………….…………………………. | 8 |

1

Independent Auditors’ Report

The Board of Managers

Genesis HealthCare LLC:

Report on the Financial Statements

We have audited the accompanying consolidated financial statements of Genesis HealthCare LLC and its subsidiaries (the Company), which comprise the consolidated balance sheets as of December 31, 2013 and 2012 (Successor), and the related consolidated statements of operations, comprehensive income (loss), members’ interest and cash flows for the two years ended December 31, 2013 and 2012, (Successor periods) and the year ended December 31, 2011(Predecessor period) and the related notes to the consolidated financial statements.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with U.S. generally accepted accounting principles; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the Successor consolidated financial statements referred to above present fairly, in all material respects, the financial position of Genesis HealthCare LLC and its subsidiaries as of December 31, 2013 and 2012, and the results of their operations and their cash flows for the years ended December 31, 2013 and 2012 (Successor periods) in accordance with U.S. generally accepted accounting principles. Further, in our opinion, the aforementioned Predecessor consolidated financial statements present fairly, in all material respects, the results of Genesis HealthCare LLC and subsidiaries’ operations and their cash flows for the year ended December 31, 2011 in accordance with U.S. generally accepted accounting principles.

As discussed in note 1 to the consolidated financial statements, one of the Company’s indirect members obtained a controlling interest of the Company in a business combination accounted for using the acquisition method. As a result of the business combination, the consolidated financial information for the period after the business combination is presented on a different cost basis than that for the periods before the business combination and, therefore, is not comparable.

/s/ KPMG LLP

Philadelphia, Pennsylvania

February 28, 201

2

See accompanying notes to the consolidated financial statements.

3

See accompanying notes to the consolidated financial statements.

4

See accompanying notes to the consolidated financial statements.

5

See accompanying notes to the consolidated financial statements.

6

See accompanying notes to the consolidated financial statements.

7

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

(1) General Information

Description of Business

The Company provides inpatient services through 411 skilled nursing, assisted living and behavioral health centers located in 28 states. Revenues of the Company’s owned, leased and otherwise consolidated centers constitute approximately 84% of its revenues.

The Company provides a range of rehabilitation therapy services, including speech pathology, physical therapy and occupational therapy. These services are provided by rehabilitation therapists and assistants employed or contracted at substantially all of the centers operated by the Company, as well as by contract to healthcare facilities operated by others. After the elimination of intercompany revenues, the rehabilitation therapy services business constitutes approximately 13% of the Company’s revenues.

The Company provides an array of other specialty medical services, including respiratory health services, management services, physician services, staffing services and other healthcare related services, which comprise the balance of the Company’s revenues.

Sun Healthcare Group Acquisition

Effective December 1, 2012, the Company completed the acquisition of Sun Healthcare Group, Inc. and its subsidiaries (Sun) (the Sun Merger). Upon consummation of the Sun Merger, each issued and outstanding share of Sun common stock and common stock equivalent was tendered for $8.50 in cash (the Merger Consideration). The purchase price totaled $228.4 million before considering cash acquired in the Sun Merger. The Company also assumed $88.8 million of long-term debt in the Sun Merger, of which $87.5 million was refinanced on December 3, 2012. The operating results of Sun have been included in the accompanying consolidated financial statements of the Company since December 1, 2012. See note 3 – “Significant Transactions and Events –Sun Merger”.

Basis of Presentation

The Company’s consolidated financial position at December 31, 2013 includes the impact of the Sun Merger, which has been accounted for as a business combination using the acquisition method effective December 1, 2012. The Company’s financial position at December 31, 2011 includes the impact of the JER Redemption, which has also been accounted for as a business combination using the acquisition method. The consolidated financial statements after giving effect to the JER Redemption are designated as “Successor” financial statements. The consolidated financial statements reflecting the results of operations and cash flows of the Company prior to giving effect to the JER Redemption are designated “Predecessor” financial statements. See note 3 – “Significant Transactions and Events – April 1, 2011 Transactions” for a description of the JER Redemption.

The accompanying consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting principles. In the opinion of management, the consolidated financial statements include all necessary adjustments for a fair presentation of the financial position and results of operations for the periods presented.

Principles of Consolidation and Variable Interest Entities

The accompanying consolidated financial statements include the accounts of the Company, its wholly owned subsidiaries, its consolidated variable interest entities (VIEs) and certain other partnerships. All significant intercompany accounts and transactions have been eliminated in consolidation for all periods presented.

The Company’s investments in VIEs in which it is the primary beneficiary are consolidated, while the investment in other VIEs in which it is not the primary beneficiary are accounted for under other accounting principles. Investments in and the operating results of 20% to 50% owned companies, which are not VIEs, are included in the consolidated financial statements using the equity method of accounting.

Consolidated VIEs and Other Consolidated Partnerships

At December 31, 2013 and 2012, the Company consolidated three VIEs. The total assets of the VIEs principally consist of property and equipment that serves as collateral for the VIEs’ non-recourse debt and is not available to satisfy any of the Company’s other obligations. Creditors of the VIEs, including senior lenders, have no recourse against the general credit of the Company. The consolidated VIEs at December 31, 2013 own and operate skilled nursing and assisted living facilities. The Company’s ownership interests in the consolidated VIEs range from 0% to 50% and the Company manages the day-to-day

8

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

operations of the consolidated VIEs under management agreements. The Company’s involvement with the VIEs began in years prior to 2000.

The Company consolidates one partnership as it is the general partner in the entity and may exercise considerable control over the business without substantive kick out rights afforded to the limited partners. The partnership is a jointly owned and managed skilled nursing facility. The total assets of this consolidated partnership consist of property and equipment that serves as collateral for the partnership’s non-recourse debt and is not available to satisfy any of the Company’s other obligations. Creditors of this consolidated partnership, including senior lenders, have no recourse against the general credit of the Company.

At December 31, 2013, total assets and non-recourse debt of the consolidated VIEs and the consolidated partnership were $55.1 million and $40.5 million, respectively. At December 31, 2012, total assets and non-recourse debt of the consolidated VIEs and the consolidated partnership were $68.8 million and $38.3 million, respectively.

(2) Summary of Significant Accounting Policies

Net Revenues and Accounts Receivable

The Company receives payments through reimbursement from Medicaid and Medicare programs and directly from individual residents (private pay), third-party insurers and long-term care facilities. The Company assesses collectibility on all accounts prior to providing services.

The Company records revenue for inpatient services and the related receivables in the accounting records at the Company’s established billing rates in the period the related services are rendered. The provision for contractual adjustments, which represents the differences between the established billing rates and predetermined reimbursement rates, is deducted from gross revenue to determine net revenue. Retroactive adjustments that are likely to result from future examinations by third party payors are accrued on an estimated basis in the period the related services are rendered and adjusted as necessary in future periods based upon new information or final settlements.

The Company records revenue for rehabilitation therapy services and other ancillary services and the related receivables at the time services or products are provided or delivered to the customer. Upon delivery of products or services, the Company has no additional performance obligation to the customer.

Use of Estimates

The preparation of consolidated financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from these estimates. Significant items subject to such estimates and assumptions include the useful lives of fixed assets; allowances for doubtful accounts and provisions for contractual adjustments; deferred tax assets, fixed assets, goodwill, identifiable intangible assets, investments, as well as reserves for employee benefit obligations, self-insurance liabilities, income tax uncertainties, asset retirement obligations and other contingencies. These estimates and assumptions are based on management’s best estimates and judgment. Management evaluates its estimates and assumptions on an ongoing basis using historical experience and other factors, including the current economic environment. Management believes its estimates to be reasonable under the circumstances. The current economic environment has increased the degree of uncertainty inherent in these estimates and assumptions. As future events and their effects cannot be determined with precision, actual results could differ significantly from these estimates.

Cash and Equivalents

Short-term investments that have a maturity of ninety days or less at acquisition are considered cash equivalents. Investments in cash equivalents are carried at cost, which approximates fair value.

Restricted Cash and Investments in Marketable Securities

Restricted cash includes cash and money market funds principally held by the Company’s wholly owned captive insurance subsidiary, which is substantially restricted to securing outstanding claims losses. The restricted cash and investments in marketable securities balances at December 31, 2013 and 2012 were $123.0 million and $117.1 million, respectively.

Restricted investments in marketable securities, comprised of fixed interest rate securities, are considered to be available-for-sale and accordingly are reported at fair value with unrealized gains and losses, net of related tax effects, included within accumulated other comprehensive income (loss), a separate component of members’ interest. Fair values for fixed interest rate

9

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

securities are based on quoted market prices. Premiums and discounts on fixed interest rate securities are amortized or accreted over the life of the related security as an adjustment to yield.

A decline in the market value of any security below cost that is deemed other-than-temporary is charged to income, resulting in the establishment of a new cost basis for the security. Realized gains and losses for securities classified as available for sale are derived using the specific identification method for determining the cost of securities sold.

Allowance for Doubtful Accounts

The Company evaluates the adequacy of its allowance for doubtful accounts by estimating allowance requirement percentages for each accounts receivable aging category for each type of payor. The Company has developed estimated allowance requirement percentages by utilizing historical collection trends and its understanding of the nature and collectibility of receivables in the various aging categories and the various lines of the Company’s business. The allowance percentages are developed by payor type as the accounts receivable from each payor type have unique characteristics. The allowance for doubtful accounts also considers accounts specifically identified as uncollectible. Accounts receivable that Company management specifically estimates to be uncollectible, based upon the age of the receivables, the results of collection efforts, or other circumstances, are reserved in the allowance for doubtful accounts until written-off.

Prepaid Expenses and Other Current Assets

Prepaid expenses and other current assets principally consist of expenses paid in advance of the provision of services, inventories of nursing center food and supplies, non-trade receivables and $9.3 million and $15.0 million of escrowed funds held by third parties at December 31, 2013 and 2012, respectively, in accordance with loan and other contractual agreements.

Property and Equipment

Property and equipment are recorded at cost. Depreciation is calculated using the straight-line method over estimated useful lives of 20-35 years for building improvements, land improvements, buildings and financing obligations building improvements, and 3-15 years for equipment, furniture and fixtures and information systems. Depreciation expense on leasehold improvements and assets held under capital leases is calculated using the straight-line method over the lesser of the lease term or the estimated useful life of the asset. Expenditures for maintenance and repairs necessary to maintain property and equipment in efficient operating condition are charged to operations as incurred. Costs of additions and betterments are capitalized.

Total depreciation expense from continuing operations for the years ended December 31, 2013, 2012 and 2011 was $180.3 million, $138.9 million, and $94.1 million, respectively.

Long-Lived Assets

The Company’s long-lived assets are reviewed for impairment whenever events or changes in circumstances indicate the carrying amount of an asset may not be recoverable. Recoverability of assets to be held and used is measured by comparison of the carrying amount of an asset to the future cash flows expected to be generated by the asset. If the carrying amount of an asset exceeds its estimated future cash flows, an impairment charge is recognized to the extent the carrying amount of the asset exceeds the fair value of the asset. Assets to be disposed of are reported at the lower of the carrying amount or the fair value less costs to sell.

The Company performs an assessment of qualitative factors prior to the use of the two step quantitative method to determine if goodwill had been impaired. If such qualitative assessment does not indicate that it is more likely than not the fair value of the reporting is less than its carrying value, no further analysis is required. The Company performs its annual impairment assessment as of September 30, of each year or more frequently if adverse events or changes in circumstances indicate that the asset may be impaired. See note 17 – “Asset Impairment Charges.”

Self-Insurance Risks

The Company provides for self-insurance risks for both general and professional liability and workers’ compensation claims based on estimates of the ultimate costs for both reported claims and claims incurred but not reported. Estimated losses from asserted and incurred but not reported claims are accrued based on the Company’s estimates of the ultimate costs of the claims, which includes costs associated with litigating or settling claims, and the relationship of past reported incidents to eventual claims payments. All relevant information, including the Company’s own historical experience, the nature and extent of existing asserted claims and reported incidents, and independent actuarial analyses of this information is used in estimating the expected amount of claims. The Company also considers amounts that may be recovered from excess insurance carriers in estimating the ultimate net liability for such risks.

10

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

Income Taxes

Effective April 1, 2011, there was a change in tax status which resulted in the Company being treated as a partnership for federal and state income tax purposes. Therefore, the consolidated financial statements do not include any provision for federal or state income taxes subsequent to April 1, 2011, except for the subsidiaries that continued to be treated as corporations for federal and state income tax purposes and for the few jurisdictions that tax partnership income. The Company’s financial results are allocated to the Company’s members. The Company’s members include these results on their separate tax returns. Prior to April 1, 2011, the Company was treated as a corporation for federal and state income tax purposes.

For the Company’s subsidiaries treated as corporations for federal and state income tax purposes, deferred income taxes arise from the recognition of the tax consequences of temporary differences between the tax basis of assets and liabilities and their reported amounts in the consolidated financial statements. These temporary differences will result in taxable or deductible amounts in future years when the reported amounts of the assets are recovered or liabilities are settled. The Company also recognizes as deferred tax assets the future tax benefits from net operating loss (NOL) carryforwards. A valuation allowance is provided for these and other deferred tax assets if it is more likely than not that some portion or all of the net deferred tax assets will not be realized.

Leases

Leasing transactions are a material part of the Company’s business. The following discussion summarizes various aspects of the Company’s accounting for leasing transactions and the related balances.

Capital Leases

Lease arrangements are capitalized when such leases convey substantially all the risks and benefits incidental to ownership. Capital leases are amortized over either the lease term or the life of the related assets, depending upon available purchase options and lease renewal features. Amortization related to capital leases is included in the consolidated statements of operations within depreciation and amortization expense.

Operating Leases

For operating leases, minimum lease payments, including minimum scheduled rent increases, are recognized as lease expense on a straight-line basis over the applicable lease terms and any periods during which the Company has use of the property but is not charged rent by a landlord. Lease terms, in most cases, provide for rent escalations and renewal options.

When the Company purchases businesses that have operating lease agreements, it recognizes the fair value of the lease arrangements as either favorable or unfavorable and records as other identifiable intangible assets or other long-term liabilities, respectively. Favorable and unfavorable leases are amortized to lease expense on a straight-line basis over the remaining term of the leases.

Sale/Leaseback Financing Obligation

Prior to recognition as a sale, or profit/loss thereon, sale/leaseback transactions are evaluated to determine if their terms transfer all of the risks and rewards of ownership as demonstrated by the absence of any other continuing involvement by the seller-lessee. A sale/leaseback transaction that does not qualify for sale/leaseback accounting because of any form of continuing involvement by the seller-lessee is accounted for as a financing transaction. Under the financing method: (1) the assets and accumulated depreciation remain on the consolidated balance sheet and continue to be depreciated over the remaining useful lives; (2) no gain is recognized; and (3) proceeds received by the Company from these transactions are recorded as a financing obligation.

Reimbursement of Managed Property Labor Costs

The Company manages the operations of 24 independently and jointly owned eldercare centers, including consolidated VIEs, and one transitional care unit as of December 31, 2013. Under most of these arrangements, the Company employs the operational staff of the managed center for ease of benefit administration and bills the related wage and benefit costs on a dollar-for-dollar basis to the owner of the managed property. In this capacity, the Company operates as an agent on behalf of the managed property owner and is not the primary obligor in the context of a traditional employee/employer relationship. Historically, the Company has treated these transactions on a “net basis,” thereby not reflecting the billed labor and benefit costs as a component of its net revenue or expenses. For the Successor years ended December 31, 2013 and 2012, the Company billed its managed clients $72.7 million and $81.1 million, respectively, for labor costs. For the Predecessor year ended December 31, 2011, the Company billed its managed clients $93.2 million for such labor related costs.

11

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

Asset Retirement Obligations

The fair value of a liability for an asset retirement obligation is recognized in the period when the asset is placed in service. The fair value of the liability is estimated using discounted cash flows. In subsequent periods, the retirement obligation is accreted to its future value or the estimate of the obligation at the asset retirement date. The accretion charge is reflected separately on the consolidated statement of operations. A corresponding retirement asset equal to the fair value of the retirement obligation is also recorded as part of the carrying amount of the related long-lived asset and depreciated over the asset’s useful life.

Recent Accounting Pronouncements

In February 2013, the FASB issued ASU No. 2013-02, Comprehensive Income (Topic 220): Reporting of Amounts Reclassified Out of Accumulated Other Comprehensive Income. ASU 2013-02 requires an entity to provide information about the amounts reclassified out of accumulated other comprehensive income by component. In addition, an entity is required to present, either on the face of the statement where net income is presented or in the notes, significant amounts reclassified out of accumulated comprehensive income by the respective line items of net income but only if the amount reclassified is required under U.S. GAAP to be reclassified to net income in its entirety in the same reporting period. For other amounts that are not required under U.S. GAAP to be reclassified in their entirety to net income, an entity is required to cross-reference to other disclosures required under U.S. GAAP that provide additional detail about those amounts. ASU 2013-02 does not change the requirements for reporting net income or other comprehensive income in financial statements. The new standard is effective for reporting periods beginning after December 15, 2013. The Company will implement the provisions of ASU 2013-02 as of January 1, 2014.

In July 2013, the FASB issued ASU 2013-11, Income Taxes (Topic 740): Presentation of an Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists. ASU 2013-11 requires an unrecognized tax benefit, or a portion of an unrecognized tax benefit, to be presented in the financial statements as a reduction to a deferred tax asset for a net operating loss carryforward, a similar tax loss, or a tax credit carryforward. ASU 2013-11 is effective for fiscal years, and interim periods within those years, beginning after December 15, 2014. The new standard is to be applied prospectively but retrospective application is permitted. The Company will implement the provisions of ASU 2013-11 as of January 1, 2015.

(3) | Significant Transactions and Events |

Sun Merger

Effective December 1, 2012, the Company completed the Sun Merger. Upon consummation of the Sun Merger, each issued and outstanding share of Sun common stock and common stock equivalent was tendered for $8.50 in cash. The purchase price totaled $228.4 million before considering cash acquired in connection with the Sun Merger. The Company also assumed $88.8 million of long-term debt in the Sun Merger, of which $87.5 million was refinanced on December 3, 2012. The operating results of Sun have been included in the accompanying consolidated financial statements of the Company since December 1, 2012.

In connection with the Sun Merger, the Company entered into two amended senior secured asset-based revolving credit facilities having aggregate borrowing capacity of $375 million (the Revolving Credit Facilities) and a new $325 million senior secured term loan facility (the Term Loan Facility) (collectively, the New Credit Facilities). The Company used proceeds from the New Credit Facilities to pay the Merger Consideration, repay all amounts outstanding under Sun’s previous credit facilities and to pay transaction costs. The amounts outstanding of $87.5 million under Sun’s former credit facilities was repaid with proceeds from the New Credit Facilities.

At the Sun Merger date, Sun and its subsidiaries operated 199 facilities in 25 states consisting of 179 skilled nursing facilities, 12 assisted or independent living facilities and 8 behavioral health facilities. Sun also operated a contract rehabilitation business serving over 500 sites of service in 36 states, a medical staffing business and a hospice business. The Sun Merger expanded the Company’s service offerings to new markets and provided opportunities for significant operating synergies.

Simultaneous with the Sun Merger, Sun’s hospice segment was sold to Life Choice Hospice, a provider of in-home hospice care, for approximately $85 million. Net cash sale proceeds of $75 million were used to repay the Term Loan Facility. The Company retained an approximate one-third interest in the sold hospice segment since it owned an approximate one-third interest in Life Choice Hospice’s parent company.

In connection with the Sun Merger, the Company amended leases with several landlords. See “– Lease Transactions”.

12

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

Operating results for 2013 and 2012 included Transaction costs totaling $2.0 million and $14.4 million, respectively. Deferred financing fees totaling $19.6 million related to the Sun Merger were initially recorded in other long-term assets and are amortized over the term of the related debt through interest expense.

Purchase Price Allocation

The total Sun purchase price of $228.4 million was allocated to the Company’s net tangible and identifiable intangible assets based upon the estimated fair values at December 1, 2012. The excess of the purchase price over the net tangible and identifiable intangible assets was recorded as goodwill. The allocation of the purchase price to property, plant and equipment, identifiable intangible assets and deferred income taxes was based upon valuation data and estimates. The aggregate goodwill arising from the Sun Merger is based upon the expected future cash flows of the Sun operations. Goodwill recognized from the Sun Merger is the result of (i) the expected savings to be realized from achieving certain economies of scale, (ii) cost savings from the elimination of compliance costs associated with Sun being a publicly held company and (iii) anticipated long-term improvements in Sun’s core businesses. The Company has estimated $38.2 million of pre-existing Sun goodwill that is deductible for income tax purposes related to the Sun Merger.

The purchase price and related allocation are summarized as follows (in thousands):

April 1, 2011 Transactions

FC-GEN Acquisition Holding, LLC (Holding Company) was formed in 2007. Private equity funds managed by affiliates of Formation Capital, LLC (FC Sponsors) and JER Partners (JER Sponsors) wholly own FC-GEN Investment, LLC (Former Parent), which owned 100% of the Holding Company. The Holding Company’s sponsors formed FC-GEN Operations Investment, LLC (Parent) in 2010. On April 1, 2011, the Holding Company (a) contributed the assets, liabilities and equity interests relating to (i) the business of operating and managing skilled nursing and assisted living facilities, (ii) joint venture entities and (iii) other ancillary businesses to Parent, and then (b) distributed all of the equity interests of the Holding Company to the members of the Former Parent in a taxable spin-off (the Distribution Transaction). See “– Distribution Transaction and JER Redemption” below. Unless the context otherwise requires, references to the “Company” refers to the operations of FC-GEN Acquisition Holding, LLC prior to April 1, 2011 and Genesis HealthCare LLC subsequent to April 1, 2011.

On April 1, 2011, the Parent entered into a sale/leaseback transaction of 140 skilled nursing and assisted living facilities with Health Care REIT, Inc., a publicly held Real Estate Investment Trust (HCN). In connection with this transaction, HCN holds a fixed purchase option to acquire 9.9% of Parent. See “– Transactions with HCN ” below.

On April 1, 2011, Parent redeemed the membership interest owned by JER Sponsors in exchange for a payment at that time plus certain contingent consideration (the JER Redemption). In 2011, FC Sponsors obtained a controlling interest in the Company as a result of the JER Redemption. Accordingly, the transaction was accounted for as a business combination using

13

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

the acquisition method. Parent has elected push-down accounting to reflect the Parent’s basis of accounting. See “– JER Redemption Purchase Accounting”.

Distribution Transaction and JER Redemption

On April 1, 2011, the Company was constituted from contributed assets, liabilities and equity interests of Holding Company relating expressly to (i) the business of operating and managing its skilled nursing and assisted living facilities, (ii) joint venture entities and (iii) other ancillary businesses. Simultaneously, the FC Sponsors and JER Sponsors entered into a membership interest purchase agreement whereby the FC Sponsors would acquire 100% of the JER Sponsors interests in the Company.

Pursuant to the terms of the JER Redemption, JER received $75 million in exchange for the JER interests in the Parent. The purchase price was financed 50% in cash and 50% in a note payable having a 12% rate of interest. At December 31, 2011, $37.5 million of the note payable remained outstanding. The note payable was fully satisfied in 2012.

Transactions with HCN

The Former Parent entered into a definitive purchase agreement with HCN pursuant to which the Former Parent, after the contribution of the operations to the Parent, sold 100% of the equity interests of the Holding Company to HCN for a purchase price of $2.4 billion (the Sale Transaction). Of the skilled nursing and assisted living centers operated by the Holding Company, it indirectly owned (1) 140 skilled nursing and assisted living facilities and (2) the leasehold interests in and option to purchase seven facilities, which represented substantially all of the Holding Company’s net property, plant and equipment. The Sale Transaction closed on April 1, 2011. Proceeds from the Sale Transaction were used to repay the $1.3 billion senior secured term loan, $375.0 million mezzanine term loan and $72.2 million of transaction costs. In connection with this transaction, HCN also received a fixed purchase option to acquire 9.9% of the Parent.

Contemporaneously with the closing of the Sale Transaction, an indirect subsidiary of the Company (Tenant) entered into a master lease (the HCN Master Lease) with a subsidiary of HCN. Tenant operates the 140 facilities under the HCN Master Lease and an affiliate of Tenant entered into a pass through master sub-sublease under which such affiliate will operate the seven leased facilities. The HCN Master Lease is supported by a guaranty from the Parent. Initial annual cash base rent of the Master Lease is $198.0 million with an annual rent escalator equal to the lesser of a consumer price index factor or 3.5% for years two through six of the lease term and not more than 3.0% thereafter. The initial lease term is for 15 years with a renewal option that can extend the lease term through December 31, 2040.

The senior secured term loan of $1.3 billion, mezzanine term loan of $375.0 million and related interest of $9.6 million and termination fees, which are mandatory interest payments that accrued over the term of the mezzanine term loan, of $20.8 million were repaid on April 1, 2011 and the agreements were terminated. The Company wrote off unamortized deferred financing fees of $5.7 million related to the senior secured credit facility and mezzanine term loan agreements, which were extinguished. In connection with the repayment, the Company received $10.7 million of proceeds from escrow balances that were required to be held under the terms of the senior secured term loan and mezzanine term loan agreements.

On June 30, 2012, the Company acquired the real property and operations of one facility. Upon acquisition, the real property of this facility was immediately conveyed to the HCN, and the facility was added to the HCN Master Lease. After being added to the HCN Master Lease, the facility is accounted for as a financing obligation. Initial annual rent on the facility is $0.8 million with escalators and terms identical to those described above. The acquisition and subsequent conveyance added $8.5 million of property and equipment and $8.9 million of financing obligation for the facility.

JER Redemption Purchase Accounting

The JER Redemption resulted in a change in ownership which is accounted for as a business combination. Under the acquisition method, the Company established opening fair values of assets acquired and liabilities assumed. The Company elected push-down accounting to reflect the basis of the Parent.

14

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

The accounting for the fair value of the assets acquired and liabilities assumed was as follows (in thousands):

Net identifiable assets acquired exceeded the fair value of the equity interests in the JER Redemption. Accordingly, there was no goodwill recognized in the transaction.

Transaction Costs

The Company expensed $15.4 million and $72.2 million of costs incurred related to the Sale Transaction in the twelve months ended December 31, 2012 and 2011, respectively. The Company expensed these costs in the period incurred. This balance includes legal, accounting, tax, stay-pay incentives and other consulting costs.

Lease Transactions

Effective May 1, 2013, the lease and purchase option of seven facilities between HCN and an unrelated third party was amended. Subject to the HCN Master Lease, the Company subleases these facilities. The term of the lease and option date is extended until April 30, 2023. Annual rent is reduced from $7.0 million to $4.2 million. The lease amendment resulted in a reduction of financing obligation buildings and improvements of $55.4 million with a corresponding reduction in financing obligation. The facilities are classified under the financing method.

Effective December 1, 2012 and in connection with the Sun Merger, the HCN Master Lease was amended to add the 18 Sun facilities. Following the amendment, the Company operates 174 facilities under the HCN Master Lease. The HCN Master Lease is supported by a guaranty from the Parent. The annual rent escalator was amended to equal 3.35% for the first five years of the original lease term and 2.9% thereafter. The amended lease term has an initial expiration date of January 31, 2029 with a renewal option that can extend the lease term through December 31, 2040.

The amended HCN Master Lease contains two options to purchase certain of the Sun facilities. The first option covers two facilities and the second option covers sixteen facilities. The purchase options are exercisable at a predetermined minimum price and subject to adjustment for the then fair value of the underlying facilities fair value at the time of exercise. The 18 Sun facilities were evaluated for lease accounting classification in purchase accounting and are being accounted for as capital leases resulting in $196.6 million of additional capital lease asset and $223.8 million of capital lease obligation. On March 15, 2013, the Company exercised the first option to acquire the two facilities for $12.2 million. The two facilities were immediately sold to an unrelated third party for a purchase price of $11.3 million. The acquisition was financed with cash and a note payable, which was settled within the fiscal year. The Company received cash of $8.0 million for the sale and has a receivable of $3.3 million recorded on the balance sheet as prepaid expenses and other current assets.

The amended HCN Master Lease requires the Company or its affiliate to acquire from the landlord a minimum of $50.0 million of currently leased facilities per year from fiscal years 2014 through 2018 for a total acquisition value of $250.0 million. Failure to acquire any portion of the minimum acquisition amount results in a two percent increase in rent applied to the amount not acquired below the contract minimum. On May 1, 2013, the HCN Master Lease was amended increasing the minimum acquisition requirement amount to $64.0 million per year from fiscal years 2014 through 2018 for an amended total acquisition value of $320 million. There have been no acquisitions through December 31, 2013.

15

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

Sabra Amendments

Effective December 1, 2012 and in connection with the Sun Merger, 20 Sun leases covering 86 facilities with Sabra Health Care REIT, Inc. (Sabra) were amended. The Sabra leases are supported by a guaranty from the Company. The annual rent escalator was amended to equal 2.5%. The amended initial lease terms for the Sabra leases range from eight to thirteen years with two five- year renewal options that can extend the various lease terms through 2030 to 2035. The Sabra facilities were evaluated for lease accounting classification and are being accounted for as operating leases.

Other Amendments

Effective July 24, 2013, a master lease with a portfolio of six facilities was amended. The Company paid $5.0 million to reduce the future annual rent by $0.4 million and acquire the real property of one of the facilities, removing it from the master lease. The master lease is classified as a capital lease.

Effective December 1, 2012 and in connection with the Sun Merger, a master lease was amended to add 40 Sun facilities. Following the amendment, the Company operates 53 facilities under the master lease. The master lease is supported by a guaranty from the Company. The amended lease term is for 13 years with two 10-year renewal options that can extend the lease term through December 31, 2045. The 53 facilities were evaluated for lease accounting classification and are accounted for as capital leases resulting in $512.8 million of additional capital lease asset and $570.8 million of capital lease obligation.

Effective December 1, 2012 and in connection with the Sun Merger, a master lease was amended to add five Sun facilities. Following the amendment, the Company operates 20 facilities under the master lease. The master lease is supported by a guaranty from the Company. The amended lease term is for nine years with two five-year renewal options that can extend the lease term through October 31, 2031. The facilities were evaluated for lease accounting classification with 14 classified as operating leases and six classified under the financing method.

Asset Purchases

In December 2012, the Company exercised its option to purchase the real estate of a leased skilled nursing facility for $3.8 million.

On January 1, 2012, the Company finalized a transaction to acquire the operations of 10 skilled nursing facilities located in Rhode Island, New Hampshire, Massachusetts and West Virginia. On September 1, 2012, the Company finalized a transaction to acquire the operations of two skilled nursing facilities located in Vermont. The total purchase price for these 12 facilities was $3.5 million. See note 13 – “Related Party Transactions”. The Company paid the landlord $14.5 million of advanced rents in 2012. The Company entered into a master lease agreement to lease the facilities for a term of 12 years with two 10-year renewal options. Following a 9-month rent-free period, the annual lease payment shall be $8.0 million. Annual rent will increase by 2% every year thereafter.

(4) Certain Significant Risks and Uncertainties

Revenue Sources

The Company receives revenues from Medicare, Medicaid, private insurance, self-pay residents, other third-party payors and long-term care facilities that utilize its rehabilitation therapy and other services. The Company’s inpatient services derives approximately 80% of its revenue from the Medicare and various state Medicaid programs.

The sources and amounts of the Company’s revenues are determined by a number of factors, including licensed bed capacity and occupancy rates of its inpatient facilities, the mix of patients and the rates of reimbursement among payors. Likewise, payment for ancillary medical services, including services provided by the Company’s rehabilitation therapy services business, vary based upon the type of payor and payment methodologies. Changes in the case mix of the patients as well as payor mix among Medicare, Medicaid and private pay can significantly affect the Company’s profitability.

It is not possible to quantify fully the effect of legislative changes, the interpretation or administration of such legislation or other governmental initiatives on the Company’s business and the business of the customers served by the Company’s rehabilitation therapy business. The potential impact of healthcare reform, which would initiate significant reforms to the United States healthcare system, including potential material changes to the delivery of healthcare services and the reimbursement paid for such services by the government or other third party payors, is uncertain at this time. Accordingly, there can be no assurance that the impact of any future healthcare legislation or regulation will not adversely affect the Company’s business. There can be no assurance that payments under governmental and private third-party payor programs will be timely, will remain at levels similar to present levels or will, in the future, be sufficient to cover the costs allocable to patients eligible for reimbursement pursuant to such programs. The Company’s financial condition and results of operations will be

16

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

affected by the reimbursement process, which in the healthcare industry is complex and can involve lengthy delays between the time that revenue is recognized and the time that reimbursement amounts are settled.

Laws and regulations governing the Medicare and Medicaid programs are complex and subject to interpretation. The Company believes that it is in material compliance with all applicable laws and regulations and is not aware of any pending or threatened investigations involving material allegations of potential wrongdoing. While no such regulatory inquiries have been made, noncompliance with such laws and regulations can be subject to regulatory actions including fines, penalties, and exclusion from the Medicare and Medicaid programs.

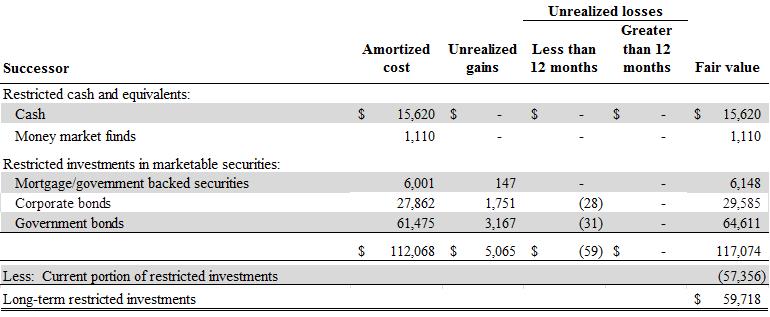

(5) Restricted Cash and Investments in Marketable Securities

The current portion of restricted cash and investments in marketable securities principally represents an estimate of the level of outstanding self-insured losses the Company expects to pay in the succeeding year through its wholly owned captive insurance company. See note 15 – “Commitments and Contingencies – Loss Reserves For Certain Self-Insured Programs.”

Restricted cash and equivalents and investments in marketable securities at December 31, 2013 consist of the following (in thousands):

Restricted cash and equivalents and investments in marketable securities at December 31, 2012 consist of the following (in thousands):

Maturities of restricted investments yielded proceeds of $23.5 million and $10.3 million for the Successor years ended December 31, 2013 and 2012, respectively, and $34.1 million for the Predecessor year ended December 31, 2011.

17

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

Sales of investments yielded proceeds of $2.7 million and $26.5 million for the Successor years ended December 31, 2013 and 2012, respectively and $36.4 million for the Predecessor year ended December 31, 2011. Associated gross realized gain and (loss) for the Successor year ended December 31, 2013 were $1.7 million and $(0.4) million, respectively. Associated gross realized gain and (loss) for the Successor year ended December 31, 2012 were $1.1 million and $(0.1) million, respectively. Associated gross realized gain and (loss) for the Predecessor year ended December 31, 2011 were $0.2 million and less than $(0.1) million, respectively.

The majority of the Company’s investments are investment grade government and corporate debt securities that have maturities of five years or less, and the Company has both the ability and intent to hold the investments until maturity.

Restricted investments in marketable securities held at December 31, 2013 mature as follows (in thousands):

Actual maturities may differ from stated maturities because borrowers may have the right to call or prepay certain obligations and may exercise that right with or without prepayment penalties.

The Company has issued letters of credit totaling $103.6 million at December 31, 2013 to its third party administrators and the Company’s excess insurance carriers. Restricted cash of $8.3 million and restricted investments with an amortized cost of $105.7 million and a market value of $107.5 million are pledged as security for these letters of credit as of December 31, 2013.

(6) Property and Equipment

Property and equipment at December 31, 2013 and 2012 consist of the following (in thousands):

The financing obligation buildings and improvements reflect the fair value of assets sold in the sale/leaseback transaction with HCN and the December 1, 2012 lease amendment of six facilities previously classified as capital leases. Both the HCN transaction and lease amendment are accounted for under the financing method. Those assets associated with the HCN transaction were all wholly owned by the Company prior to the sale/leaseback.

Construction in progress includes significant renovation projects at various locations. The Company undergoes such projects to enhance the value of the properties and improve earning potential of those operations. In addition, the Company is constructing four new skilled nursing facilities. Because the Company is the primary tenant and integrally involved in the construction phase of these projects, the Company is capitalizing the cost of the construction and the associated obligation to the landlord funding the project. The carrying value of the new facilities at December 31, 2013 is $59.3 million with a

18

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

corresponding long-term obligation of $59.0 million. The carrying value of the new facilities at December 31, 2012 is $45.1 million with a corresponding long-term obligation of $44.1 million.

(7) Other Long-Term Assets

Other long-term assets at December 31, 2013 and 2012 consist of the following (in thousands):

Deferred financing fees are recorded net of accumulated amortization of $12.9 million and $8.2 million at December 31, 2013 and 2012, respectively.

(8) Goodwill and Identifiable Intangible Assets

The changes in the carrying value of goodwill are as follows (in thousands):

The Company has no accumulated amortization of goodwill.

Goodwill is an asset representing the future economic benefits arising from other assets acquired in a business combination that are not individually identified and separately recognized. Through the acquisition accounting, for the JER Redemption in 2011 the fair value of assets acquired and liabilities assumed exceeded the fair value of members’ interest resulting in no goodwill.

The goodwill additions in 2012 of $134.7 million include $128.6 million of goodwill arising from the Sun Merger and the remainder arising from other acquisitions.

The goodwill additions in 2013 of $35.0 million are related to adjustments in finalizing the purchase accounting associated with the Sun Merger.

19

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

Identifiable intangible assets consist of the following at December 31, 2013 and 2012 (in thousands):

Acquisition-related identified intangible assets consist of customer relationship assets, favorable lease contracts and trade names.

• | Customer relationship assets exist in the Company’s rehabilitation services, respiratory services, management services and medical staffing businesses. These assets are amortized on a straight-line basis over the expected period of benefit. |

• | Favorable lease contracts represent the estimated value of future cash outflows of operating lease contracts compared to lease rates that could be negotiated in an arms-length transaction at the time of measurement. Favorable lease contracts are amortized on a straight-line basis over the lease terms. |

• | The Company’s trade names have value, in particular in the rehabilitation business which markets its services to other providers of skilled nursing and assisted living services. The trade name asset has an indefinite life and is measured no less than annually or if indicators of potential impairment become apparent. |

Amortization expense related to identifiable intangible assets for the Successor years ended December 31, 2013 and 2012 was $18.8 million and $7.2 million, respectively, and for the Predecessor year ended December 31, 2011 was $5.4 million.

Based upon amounts recorded at December 31, 2013, total estimated Successor amortization expense of identifiable intangible assets will be $18.4 million in 2014, $16.5 million in 2015, $16.4 million in 2016, $16.0 million in 2017, and $15.5 million in 2018 and $61.2 million, thereafter.

20

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

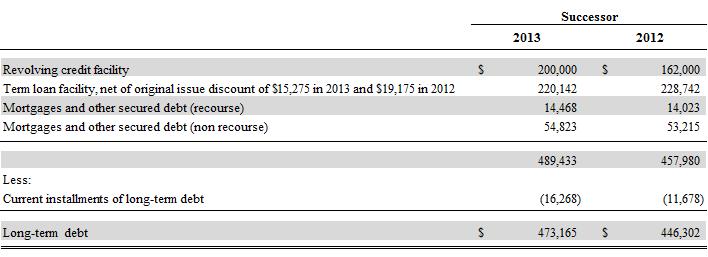

(9) Long-Term Debt

Long-term debt at December 31, 2013 and 2012 consists of the following (in thousands):

New Credit Facilities

In connection with the Sun Merger, the Company entered into the New Credit Facilities. The Company used proceeds from the New Credit Facilities to pay the Merger Consideration, repay all amounts outstanding under Sun’s previous credit facilities and to pay transaction costs. The amounts outstanding under Sun’s former credit facilities was $162.5 million, of which $87.5 million was repaid with proceeds from the New Credit Facilities and $75 million was repaid with the balance of a restricted cash escrow held by Sun. In connection with the New Credit Facilities, the Company paid $19.6 million of lender fees related to the debt issuance that were capitalized as deferred financing costs.

The New Credit Facilities, contain a number of restrictive covenants that, among other things, impose operating and financial restrictions on the Company and its subsidiaries. The New Credit Facilities also require the Company to meet defined financial covenants, including a minimum level of consolidated liquidity, a maximum consolidated net leverage ratio and a minimum consolidated fixed charge coverage ratio. The New Credit Facilities also contain other customary covenants and events of default. At December 31, 2013, the Company is in compliance with its covenants. On January 21, 2014, the Company amended the New Credit Facilities redefining certain restrictive covenants in exchange for fees of $4.3 million.

In 2013, pursuant to the New Credit Facilities, the Company entered into an interest rate cap agreement for a notional amount of $250 million limiting the Company’s exposure to LIBOR interest rate fluctuations at 1.5%. The interest rate cap agreement expires on December 31, 2014.

Revolving Credit Facilities

The Revolving Credit Facilities had a combined maximum borrowing capacity of $375 million in 2012 and five year terms. The larger of the two facilities is a $368 million facility and the smaller is a $7 million facility. The $7 million facility was established by certain wholly owned subsidiaries of the Company through which the Company leases real estate. This separate revolving credit facility was required when the owner of the real estate refinanced the outstanding debt, which is secured through the U.S. Department of Housing and Urban Development.

The Revolving Credit Facilities were amended in 2013 increasing the maximum borrowing capacity to $425 million. The larger of the two facilities is a $415 million facility and the smaller is a $10 million facility.

The Revolving Credit Facilities were established to provide the Company a source of financing to fund general working capital requirements. The Revolving Credit Facilities are secured by a first priority lien on eligible accounts receivable, cash, deposit accounts and certain other assets and property (the Revolving Credit Facility First Priority Collateral). The Revolving Credit Facilities have a second priority lien on the membership interests in the Company and substantially all of the Company’s assets.

Borrowings under the Revolving Credit Facilities may be in the form of revolving loans or swing line loans. Aggregate outstanding swing line loans have a sub-limit of $20 million. The Revolving Credit Facilities also provide a sub-limit of $125 million for letters of credit. Borrowing levels under the Revolving Credit Facilities are limited to a borrowing base that is computed based upon the level of Company eligible accounts receivable, as defined. In addition to paying interest on the outstanding principal borrowed under the revolving credit facilities, the Company is required to pay a commitment fee to the

21

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

lenders for any unutilized commitments. The commitment fee rate is 0.375% per annum when the unused commitment is greater than $200 million and 0.50% per annum when the unused commitment is less than $200 million.

As of December 31, 2013, the Company had outstanding borrowings under the Revolving Credit Facilities of $200 million and had $99.2 million of drawn letters of credit securing insurance and lease obligations, leaving the Company with approximately $105.0 million of available borrowing capacity under the revolving credit facilities.

Borrowings under the revolving credit facility, as amended, bear interest at a rate equal to, at the Company’s option, either a base rate plus an applicable margin or at LIBOR plus an applicable margin. The base rate is determined by reference to the highest of (i) a lender-defined prime rate, (ii) the federal funds rate plus 3.0%, and (iii) the sum of LIBOR plus an applicable margin. The applicable margin with respect to base rate borrowings is 3.0% at December 31, 2013. The applicable margin with respect to LIBOR borrowings is 3.0% at December 31, 2013. Base rate borrowings under the revolving credit facility bore interest of approximately 6.3% at December 31, 2013. One-month LIBOR borrowings under the revolving credit facility bore interest of approximately 3.4% at December 31, 2013.

Prior to December 1, 2012, the Company’s revolving credit facility had a maximum commitment ranging from $200 million to $300 million. The terms and conditions of the revolving credit facility prior to December 1, 2012 were similar to those disclosed above for the current revolving credit facility.

Term Loan Facility

The Term Loan Facility has a five-year term and is secured by a first priority lien on the membership interests in the Company, substantially all of the Company’s assets other than the Revolving Credit Facility First Priority Collateral and a second priority lien on the Revolving Credit Facility First Priority Collateral. The Term Loan Facility proceeds totaled $305.5 million, net of a $19.5 million original issue discount that will be amortized over the term of the Term Loan Facility.

Simultaneous with the Sun Merger, the Company used net cash proceeds of $75 million from the sale of the Sun hospice segment to repay the Term Loan Facility. Also in December 2012, the Company made a $2.1 million scheduled principal payment on the Term Loan Facility. In future periods, the Term Loan Facility amortizes quarterly at a rate of five percent per annum.

Borrowings under the Term Loan Facility bear interest at a rate per annum equal to the applicable margin plus, at the Company’s option, either (1) LIBOR determined by reference to the costs of funds for Eurodollar deposits for the interest period relevant to such borrowings, or (2) a base rate determined by reference to the highest of (a) the lender defined prime rate, (b) the federal funds rate effective plus one half of one percent and (c) LIBOR described in sub clause (1) plus 1.0%. LIBOR based loans are subject to an interest rate floor of 1.5% and base rate loans are subject to a floor of 2.5%. Base rate borrowings under the Term Loan Facility bore interest of approximately 10.8% at December 31, 2013. One-month LIBOR borrowings under the Term Loan Facility bore interest of approximately 10.0% at December 31, 2013.

Other Debt

Mortgages and other secured debt (recourse). The Company carries two mortgage loans on two of its corporate office buildings. The loans are secured by the underlying real property and have fixed or variable rates of interest ranging from 1.9% to 8.5% at December 31, 2013, with maturity dates ranging from 2014 to 2018. The Company is a named co-borrower on a loan with a fixed interest rate of 5.5% and a maturity date in 2014. The loan is offset with a receivable recorded on the consolidated balance sheet in prepaid expenses and other current assets.

Mortgages and other secured debt (non-recourse). Loans are carried by certain of the Company’s consolidated joint ventures. The loans consist principally of revenue bonds and secured bank loans. Loans are secured by the underlying real and personal property of individual facilities and have fixed or variable rates of interest ranging from 2.5% to 20.2% at December 31, 2013, with maturity dates ranging from 2014 to 2036. Loans are labeled “non-recourse” because neither the Company nor a wholly owned subsidiary is obligated to perform under the respective loan agreements.

The maturity of total debt of $489.4 million at December 31, 2013 is as follows: $16.2 million in fiscal 2014, $10.7 million in fiscal 2015, $10.8 million in fiscal 2016, $196.6 million in fiscal 2017, $223.2 million in fiscal 2018 and $31.9 million thereafter.

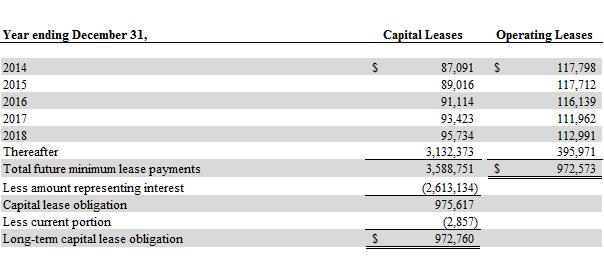

(10) Leases and Lease Commitments

The Company leases certain facilities under capital and operating leases. Future minimum payments for the next five years and thereafter under such leases at December 31, 2013 are as follows (in thousands):

22

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

Capital Lease Obligations

The capital lease obligations represent the present value of minimum lease payments under such capital lease arrangements and bear imputed interest at rates ranging from 8.5% to 12.8% at December 31, 2013, and mature at dates ranging primarily from 2014 to 2045.

The Company holds fixed price purchase options to acquire the land and buildings of 11 facilities for $55.6 million with expirations in 2025.

Deferred Lease Balances

At December 31, 2013 and 2012, the Company had $60.1 million and $71.5 million, respectively, of favorable leases net of accumulated amortization, included in other identifiable intangible assets and $36.7 million and $54.0 million, respectively, of unfavorable leases net of accumulated amortization included in other long-term liabilities on the consolidated balance sheet. The favorable leases will be amortized as an increase to lease expense over the remaining lease terms, which have a weighted average term of 10 years. The unfavorable leases will be amortized as a decrease to lease expense over the remaining lease terms, which have a weighted average term of 8 years.

(11) Financing Obligation

On April 1, 2011, the Company entered into the Sales Transaction and the HCN Master Lease. See note 1 – “General Information - Transactions with HCN”. Proceeds from the Sales Transaction were $2.4 billion. Due to certain forms of continuing involvement, the transaction was recorded under the financing method. Accordingly, the value of the land, buildings and improvements remained on the Company's consolidated financial statements at carrying value and continued to be depreciated over their remaining useful lives. The $2.4 billion of net proceeds received has been recorded as a financing obligation. A portion of the monthly cash lease payments is recorded to the financing obligation and a portion is recognized as interest expense.

The financing obligation represents the proceeds from the Sale Transaction that amortizes based on the present value of minimum lease payments under the HCN Master Lease and bears imputed interest at 8.8% at December 31, 2013, and matures in 2040.

On December 1, 2012, the Company amended a lease agreement. Prior to this amendment, six of the facilities under this lease arrangement were classified as capital leases. The facilities were reassessed for lease classification. Due to certain forms of continuing involvement, the amendment qualifies as a sale/leaseback transaction to be accounted for under the financing method. The Company reclassified the capital lease obligation of $78.6 million as a financing obligation.

The HCN Master Lease contains a number of restrictive covenants that, among other things and subject to certain exceptions, impose operating and financial restrictions on the Company and its subsidiaries. The HCN Master Lease also requires the Company to meet defined financial covenants, including a minimum level of consolidated liquidity, a maximum consolidated net leverage ratio, a minimum consolidated fixed charge coverage and a minimum level of tangible net worth. At December 31, 2013, the Company is in compliance with its covenants.

23

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

On January 21, 2014, the HCN Master Lease was amended redefining how certain restrictive covenants are calculated in exchange for additional collateral in the form of an increased letter of credit.

Future minimum payments for the next five years and thereafter under such leases at December 31, 2013 are as follows (in thousands):

(12) Income Taxes

The provision for income taxes was based upon management’s estimate of taxable income or loss for each respective accounting period. The Company recognizes an asset or liability for the deferred tax consequences of temporary differences between the tax bases of assets including net operating loss and credit carryforwards and liabilities and the amounts reported in the financial statements. These temporary differences would result in taxable or deductible amounts in future years when the assets are recovered or liabilities are relieved.

Effective April 1, 2011, there was a change in tax status which resulted in the Company being treated as a partnership for federal and state income tax purposes. Pursuant to accounting standards, pre-existing deferred tax assets and liabilities of the Company, excluding corporate subsidiaries, were included in income tax expense in the year the Company became a non-taxable enterprise. The Company, excluding corporate subsidiaries, no longer is subject to corporate level US federal, state and local income taxes except in the District of Columbia, New Hampshire, Tennessee, Texas, New York City and Philadelphia. The Company maintains deferred taxes for these jurisdictions as does its corporate subsidiaries for US federal, state, foreign and local jurisdictions.

The Sun Merger was treated as a purchase for accounting and tax purposes. Sun files a consolidated corporate federal income tax return and state and local income tax returns. The Company did not elect under IRC Sec. 338(g) to treat the Sun Merger as a purchase of assets. As a result, the tax bases of its assets and attributes such as net operating losses and tax credit carryforwards were carried over and subject to the provisions of IRC Sec. 382.

After the Sun Merger, the Company owns two separate corporate consolidated taxable groups: GHC Ancillary group and Sun group.

Income Tax Provision (Benefit)

Total income tax expense (benefit) was as follows (in thousands):

24

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

The components of the provision for income taxes on income (loss) from continuing operations for the periods presented were as follows (in thousands):

At December 31, 2013, the Company has established a valuation allowance in the amount of $32.0 million. This represents a decrease of $7.9 million from December 31, 2012, due to expiration of the state NOL carry-forward at December 31, 2013. The deferred tax assets that are subject to a valuation allowance are the deferred tax assets of a dual consolidated company (which relate to an entity that elected to be treated as a member of the GHC Ancillary group but whose deferred tax assets are subject to separate return limitations), the deferred tax assets of the Company (this partnership is subject to entity level state taxes and has incurred cumulative losses in the current and prior period) and state deferred tax assets including net operating loss carryforwards which are not expected to be realized.

In assessing the requirement for, and amount of, a valuation allowance in accordance with the more likely than not standard for all periods, the Company gives appropriate consideration to all positive and negative evidence related to the realization of the deferred tax assets. The assessment considers the nature, frequency and severity of current and cumulative losses, forecasts of future profitability, the duration of statutory carryforward periods and the Company’s experience with operating loss and tax credit expirations. A history of cumulative losses is a significant piece of negative evidence used in the assessment. If a history of cumulative losses is incurred for a tax jurisdiction, forecasts of future profitability are not used as positive evidence related to the realization of the deferred tax asset in the assessment.

The Company expects it will have sufficient taxable income in future periods from the reversal of existing taxable temporary differences and expected profitability to utilize the remaining deferred tax assets, net of valuation allowance, within the carryforward period. In arriving at this conclusion, the Company considered the profit generated before tax for years 2011 through 2013 adjusted for impairments of goodwill, as well as future reversals of existing temporary differences and projections of future profits before tax.

The Company has $22.3 million in deferred tax benefits from federal net operating loss (“NOL”) carryforwards with expirations between 2020 and 2032 and $21.7 million from state NOL carryforwards with expirations between 2014 and 2032. In addition, the Company has $7.0 million of federal credit carryforwards which expire between 2018 and 2032, $0.7 million of state credit carryforwards which expire between 2015 and 2017 and $4.8 million of federal alternative minimum tax credit carryforwards with no expiration date.

The Internal Revenue Code imposes limitations on a corporation’s ability to utilize federal and state tax attributes (such as net unrealized built-in-deductions), including federal income tax credits, in the event of an “ownership change”. States may impose similar limitations. In general terms, an ownership change may result from transactions increasing the ownership of certain shareholders in the stock of a corporation by more than 50 percentage points over a three year period. On April 1, 2011, there was an ownership change of the GHC Ancillary group. On December 1, 2012, there was an ownership change of the Sun group.

25

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

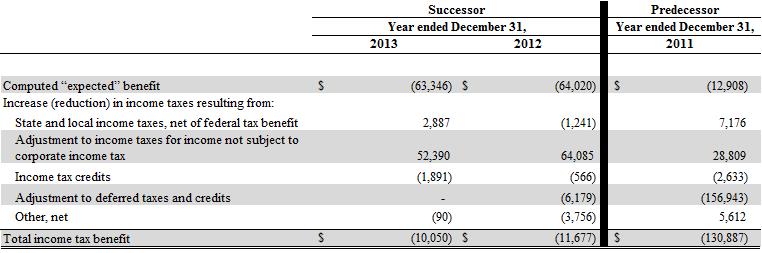

Total income tax expense (benefit) for the periods presented differed from the amounts computed by applying the federal income tax rate of 35% to income (loss) before income taxes as illustrated below (in thousands):

A significant portion of the Company’s 2013, 2012 and 2011 income (loss) before taxes is not subject to corporate income tax. However, in many jurisdictions in which the Company operates, it is obligated to remit income taxes on behalf of its members. The Company recorded these payments as distributions to its members.

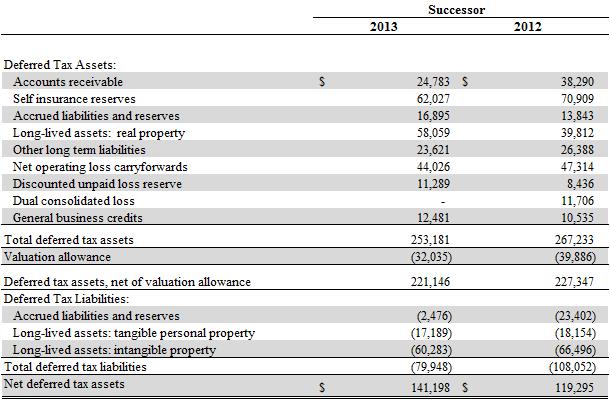

The tax effects of temporary differences that give rise to significant portions of the deferred tax assets and deferred tax liabilities at December 31, 2013 and 2012 are presented below (in thousands):

26

Genesis HealthCare LLC and Subsidiaries

Notes to Consolidated Financial Statements

Uncertain Tax Positions

The Company, excluding its two corporate groups, is only subject to state and local income tax in certain jurisdictions. The Company’s two corporate groups are subject to federal, state and local income taxes. Significant judgment is required in evaluating its uncertain tax positions and determining its provision for income taxes. Under GAAP, the Company utilizes a two-step approach to recognizing and measuring uncertain tax positions. The first step is to evaluate the tax position for recognition by determining if the weight of available evidence indicates that it is more likely than not that the position will be sustained on audit, including resolution of related appeals or litigation processes. The second step is to measure the tax benefit as the largest amount that is more than 50% likely of being realized upon settlement.

Although the Company believes it has adequately reserved for its uncertain tax positions, no assurance can be given that the final tax outcome of these matters will not be different. The Company adjusts these reserves in light of changing facts and circumstances, such as the closing of a tax audit or the expiration of the statute of limitations. To the extent that the final tax outcome of these matters is different than the amounts recorded, such differences will impact the provision for income taxes in the period in which such determination is made. The provision for income taxes includes the impact of reserve provisions and changes to reserves that are considered appropriate, as well as the related net interest.

The Company has recorded a $25.6 million reserve for uncertain tax positions primarily relating to certain tax exposure items acquired as a result of the Sun Merger. As such, the liability related to these amounts was accounted for as part of the purchase price and was not charged to income tax expense.

All of the gross unrecognized tax benefits would affect the effective tax rate if recognized. Unrecognized tax benefits are adjusted in the period in which new information about a tax position becomes available or the final outcome differs from the amount recorded. Unrecognized tax benefits are not expected to change significantly over the next twelve months. The Company recognizes potential accrued interest related to unrecognized tax benefits in income tax expense. Penalties, if incurred, would also be recognized as a component of income tax expense. The amount of accrued interest related to unrecognized tax benefits as of December 31, 2013, 2012, and 2011 was $0.4 million, $0.3 million, and $1.6 million, respectively. Generally, the Company has open tax years for state purposes subject to tax audit on average of between three years to six years. The Company’s U.S. income tax returns from 2009 through 2012 are open and could be subject to examination.

(13) Related Party Transactions

The Parent is wholly owned by private investors sponsored by affiliates of Formation Capital, LLC and was also previously partially owned by JER Partners.

The Company made an investment of $1.0 million and received an approximate 6.7% interest in National Home Care Holdings, LLC, an unconsolidated joint venture affiliated with one of the Company’s Sponsors.