Attached files

| file | filename |

|---|---|

| 8-K - 8-K - CMS ENERGY CORP | d673635d8k.htm |

Cross

Winds Energy Park

Jackson Gas Plant

Consumers Smart Energy Program

2014 Credit Suisse Energy Summit

February 11, 2014

Exhibit 99.1 |

This

presentation

is

made

as

of

the

date

hereof

and

contains

“forward-looking

statements”

as

defined

in

Rule

3b-6

of

the

Securities Exchange Act of 1934, Rule 175 of the Securities Act of 1933, and relevant

legal decisions. The forward-looking

statements are subject to risks and uncertainties.

All forward-looking statements should be considered in the context of the

risk and

other

factors

detailed

from

time

to

time

in

CMS

Energy’s

and

Consumers

Energy’s

Securities

and

Exchange

Commission

filings. Forward-looking statements should be read in conjunction with

“FORWARD-LOOKING STATEMENTS AND INFORMATION”

and “RISK FACTORS”

sections of CMS Energy’s and Consumers Energy’s Form 10-K for the year

ended December

31,

2013.

CMS

Energy’s

and

Consumers

Energy’s

“FORWARD-LOOKING

STATEMENTS

AND

INFORMATION”

and

“RISK FACTORS”

sections are incorporated herein by reference and discuss important factors that could

cause CMS Energy’s and

Consumers

Energy’s

results

to

differ

materially

from

those

anticipated

in

such

statements.

CMS

Energy

and

Consumers

Energy undertake no obligation to update any of the information presented herein to

reflect facts, events or circumstances after the date hereof.

The presentation also includes non-GAAP measures when describing CMS Energy’s

results of operations and financial performance. A reconciliation of each

of these measures to the most directly comparable GAAP measure is included in the

appendix

and

posted

on

our

website

at

www.cmsenergy.com. CMS

Energy provides historical financial results on both a reported (Generally Accepted Accounting Principles) and adjusted

(non-GAAP)

basis

and

provides

forward-looking

guidance

on

an

adjusted

basis.

Management

views

adjusted

earnings

as

a

key

measure of the company’s present operating financial performance, unaffected by

discontinued operations, asset sales, impairments, regulatory items from prior

years, or other items. These items have the potential to impact, favorably or unfavorably,

the company's reported earnings in future periods.

Because the company is not able to estimate the impact of these

matters, the

company is not providing a reconciliation to the comparable future period reported

earnings. 1 |

2

.

.

.

.

at

the

very

high

end

of

all

peers.

.

.

.

.

at

the

very

high

end

of

all

peers.

_ _ _ _ _

Source: Bloomberg, periods ending 12/31/2013. Consensus used for companies

that haven’t reported. One

Year

Three

Year

Five

Year

Ten

Year

Future

Annual

Growth

CMS

Energy

7%

22%

37%

105%

5%-7%

Note:

Dividend

Growth

6

29

116

na

5-7

Peer Group

3

9

15

45

?

CMS EPS Cumulative Growth . . . . |

Purchase

of Jackson Gas Plant .

.

.

.

Asset:

540 MW gas plant located in

Jackson, Michigan

Price:

$155 million ($286/kW)

Technology:

Combined cycle

Heat rate –

8,800 Btu/kWh

3

.

.

.

.

provides

substantial

savings

to

customers.

.

.

.

.

provides

substantial

savings

to

customers.

The Transaction

The Transaction

Connecting The “Dots”

Connecting The “Dots”

•

Retire small coal plants

•

Recover through

securitization; lower rates

•

Replace with cleaner,

inexpensive gas plant

purchase

•

Suspend CON; Thetford on

hold

•

Close late 2015 when

needed

•

Creates headroom for other

needed investments |

New Gas

Plant .

.

.

.

4

.

.

.

.

adds

capacity

and

makes

room

for

more

investment.

.

.

.

.

adds

capacity

and

makes

room

for

more

investment.

•

Customers benefit:

•

Lower rates

•

Better timing

•

Investors benefit:

•

Lower risk

•

Investment backfill

•

EPS & OCF growth

more certain

•

No block equity

Electric Reliability

$200 Million

Accelerate Smart Energy &

Other

$180 Million

Gas Infrastructure

$165 Million

Other Needed Investments -

Other Needed Investments -

$545 Million

$545 Million |

Regulatory

Update .

.

.

.

5

Amount

(mils)

•Savings

from purchase of Jackson Plant; $545

replacing build

•Securitize

Classic 7 $390

•

MPSC Order complete

•

No appeals

•Avoid

rate cases until 2015 test year $150

•New

investment self-funded

.

.

.

.

new

investment

self-funded,

improving

rates.

.

.

.

.

new

investment

self-funded,

improving

rates. |

6

.

.

.

.

good

for

customers

(prices)

and

investors

(no

ROE

risk).

.

.

.

.

good

for

customers

(prices)

and

investors

(no

ROE

risk).

Electric Rate Case Avoided

Gas Rate Case Avoided

Rate Cases Eliminated! .

. . . |

CMS Energy

MODEL .

.

.

.

Investment

•

Ten year -

$15 billion

•

Small, bite size projects

•

None “Bet The Company”

Upside Catalysts

A. Capex >$15 billion

B. PPA’s expire = 2,000 MW

C. Credit rating

D. Sales

E. Capacity price increases

F. ROA elimination

G.

Continuous cost reductions

Self-Imposed Limits

•

Sustainable base rates < 2% inflation

•

Investment “Needed Not Wanted”

RESULTS

Consistent

Predictable

.

.

.

.

benefits

customers

AND

shareowners.

.

.

.

.

benefits

customers

AND

shareowners.

7 |

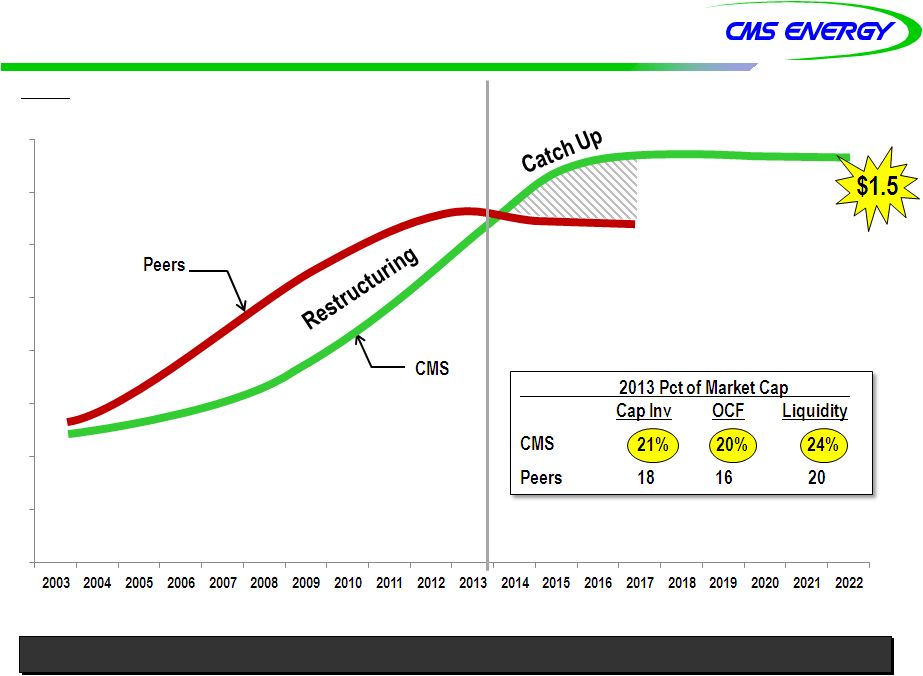

.

.

.

.

reflects

catch-up

needed

to

reduce

cost

and

improve

reliability.

.

.

.

.

reflects

catch-up

needed

to

reduce

cost

and

improve

reliability.

2013-2022

2013-2022

10-Year Plan

10-Year Plan

Opportunity Level

Opportunity Level

8

A. Visible, 10 - Year I NVESTMENT Plan . . . . |

Capital

Investment Visibility .

.

.

.

9

Amount

(bils)

$

.

.

.

.

clear

for

next

ten

years

–

needed,

not

just

wanted.

.

.

.

.

clear

for

next

ten

years

–

needed,

not

just

wanted. |

10

.

.

.

.

creates

unique

opportunity;

lagging

for

peers.

.

.

.

.

creates

unique

opportunity;

lagging

for

peers.

Amount

(bils)

$1.8

_ _ _ _ _

Source: 10K; actual amounts through 2012 smoothed for illustration

Catch

Investment

-Up .

.

.

. |

. .

. . will provide investment headroom. . . . . will provide investment

headroom. 11

•

Replace PPA

contracts with

owned

generation

•

Provides

incremental

rate base (and

earnings

potential) with

no impact to

customer rates

Opportunities

Opportunities

Capacity Need

Capacity Need

B. Expiring PPA’S . . . . |

C.

Credit RATINGS .

.

.

.

.

.

.

.

just

upgraded.

.

.

.

.

just

upgraded.

12

•

Consistent

Performance

•

Less Risk

•

Customer Focus

•

Constructive

Regulation

•

Good Energy

Policy

Reflects

Reflects

Present

Prior

2002

Scale

S&P /

Fitch

Moody’s

S&P

Moody’s

Fitch

A+

A1

A

A2

Consumers

Secured

A-

A3

BBB+

Baa1

BBB

Baa2

BBB-

Baa3

BB+

Ba1

CMS

Unsecured

BBB

Baa2

BBB-

Baa3

BB+

Ba1

BB

Ba2

BB-

Ba3

B+

B1

B

B2

B-

B3

Outlook

Stable

Stable

Positive |

D. SALES Growth

.

.

.

.

13

.

.

.

.

best

in

Midwest.

.

.

.

.

best

in

Midwest.

Economic Indicators

Economic Indicators

Grand

Rapids

Michigan

U.S

Unemployment

December 2013

5.6%

8.4%

6.7%

GDP

(real)

2010

thru

2012

14

11

7

Population

2010

Census

thru July 2012

2

0

2 |

E.

CAPACITY

Price

Market

Increases

.

.

.

.

14

.

.

.

.

could

add

value

to

the

700

MW

“DIG”

plant.

.

.

.

.

could

add

value

to

the

700

MW

“DIG”

plant.

Capacity price <

($ kW per month)

Today

(mils)

Future Scenarios

(mils)

$5

+$30

$55

$35

+$50 |

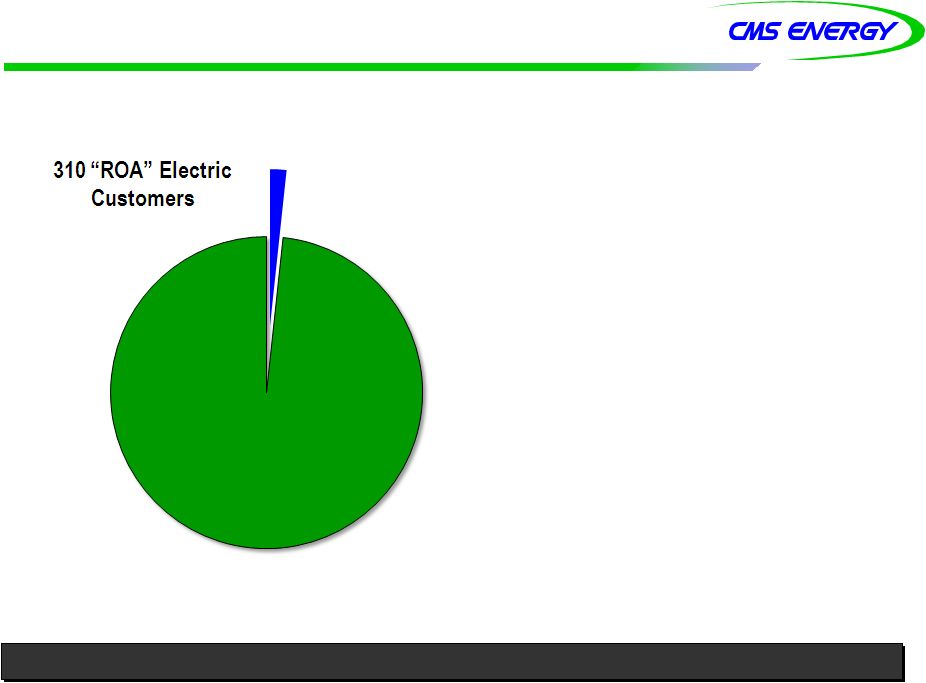

F.

Retail

Open

Access

Policy

(ROA)

.

.

.

.

15

.

.

.

.

change

could

allow

for

lower

industrial

rates.

.

.

.

.

change

could

allow

for

lower

industrial

rates.

1.8 Million Consumers Energy

1.8 Million Consumers Energy

Customers = 99.98%

Customers = 99.98%

0.02%

•

Governor wants affordable

residential bills and

competitive industrial rates

•

Eliminating ROA could:

•

Lower industrial rates by 10%

or all customers by 4%

•

Policy has big impact on

competitiveness

•

$150 million cost opportunity |

Michigan's Energy Future

.

.

.

.

Governor’s 2025 Energy Goals

Governor’s 2025 Energy Goals

•

Adaptability

•

Eliminate energy waste

•

Reduce coal, replace with renewables

and gas

•

Reliability

•

Top quartile performance (SAIFI)

•

Top half performance (SAIDI)

•

Affordability

•

Residential bills below U.S. average

•

Competitive industrial rates

•

Environmental Protection

•

Reduce mercury, acid rain, particulates

•

Increase renewables

16

.

.

.

.

will

continue

to

strengthen

with

sound

policy

and

strong

leadership.

.

.

.

.

will

continue

to

strengthen

with

sound

policy

and

strong

leadership.

Regulatory Support

Regulatory Support

(from the right)

Michigan Governor Rick Snyder

MPSC Chairman John Quackenbush

Michigan Energy Office Director Steve Bakkal |

“Choice creates a lot of challenges and problems so I wouldn’t jump to

say increasing choice is the answer. I’m concerned about people

bouncing back and forth depending on what’s going on with rates,

essentially trying to arbitrage markets.”

Governor Rick Snyder

17

Question:

“You

seem

to

agree

with

utilities’

argument on choice. Does that mean you will

eliminate shopping altogether or keep the 10% cap in

place?”

.

.

.

.

choice

is

not

the

solution

to

industrial

competitiveness.

.

.

.

.

choice

is

not

the

solution

to

industrial

competitiveness.

The Jackson City Council voted unanimously to pass a resolution opposing

House Bill 5184.

The Governor on Retail Open Access . . . . |

.

.

.

.

.

holds

down

rates

and

allows

better

system

reliability.

.

.

.

.

.

holds

down

rates

and

allows

better

system

reliability.

18

Average Annual O&M Change

+6%

Peers

2013

Reinvestment

-8%

-2%

Major

Storms

-6%

-3%

Major 2013

Storms

CMS Flat

-2%

G.

Self-Initiated Control . . . .

COST |

G.

Continuous COST Reduction

.

.

.

.

. . . . . a way of life at CMS.

. . . . . a way of life at CMS.

Past Progress

Past Progress

19

Future Examples

Future Examples

Fuel Mix

Benefits

MW

Employees

2016

Retire Coal

-

900

-

300

2016

Add GCC

+ 540

+ 20

Total

-360

-

280

Future Savings (mils)

$25

Future Annual

Savings

(mils)

2002-2012

Actions completed

$25

2013

EGWP, OPEB & other

50

Future savings

$75 |

CMS

Mindset .

.

.

.

20

.

.

.

.

deliver

for

customers

AND

investors.

.

.

.

.

deliver

for

customers

AND

investors.

2013 Cold

2013 Cold

Winter &

Winter &

Cost Savings

Cost Savings

$1.66

+7%

Guidance

2012

Warm

Winter

2012

Cost

Saving

2012 Hot

Summer

Reinvested

earlier

2014 Cold

Winter

2013 Mild

Summer

Icy Late December

O&M

B/(W)

Than

Forecast

(mils)

•

$(37)

•

16

•

9

•

12

$

0

Reinvestment (January-October)

Amount (mils)

Improve

gas

reliability

$16

Improve

electric

reliability

14

Accelerate

generation

maintenance

7

Prefund

pension

&

storm

response

21

Total

$58

Storm(total

$50

M)

Insurance

Lower

contributions

Sales-weather

Total |

Operating

Cash Flow Growth .

.

.

.

Amount

(bils)

$

Investment

Cash flow before dividend

NOLs & Credits

$0.7

$0.6

$0.4

$0.5

$0.4

$0.2

$0.1

Gross operating cash flow

a

up $0.1 billion per year

.

.

.

.

self-funds

investment

and

strategy.

.

.

.

.

self-funds

investment

and

strategy.

Up $0.5

Billion

21

Working capital

and taxes |

Mindset

.

.

.

.

22

.

.

.

.

drives

consistent

“real”

growth.

.

.

.

.

drives

consistent

“real”

growth.

_ _ _ _ _

Adjusted EPS (non-GAAP) excluding MTM in 2004-2006

a

$1.25 excluding discontinued Exeter operations and accounting changes related to

convertible debt and restricted stock $1.66 |

Growth

Growth

•

•

5%-7% EPS growth

5%-7% EPS growth

•

•

Dividend growth premium (like earnings)

Dividend growth premium (like earnings)

Transparent

Transparent

•

•

Ten-year, $15 billion investment plan

Ten-year, $15 billion investment plan

•

•

Constructive regulatory climate

Constructive regulatory climate

•

•

Continuous cost reductions

Continuous cost reductions

Predictable

Predictable

On

On

track

track

for

for

12

consecutive

consecutive

year

year

of

of

consistent,

consistent,

sector-leading

sector-leading

Catalysts not in plan!

Catalysts not in plan!

.

.

.

.

attractive

future

total

shareowner

return.

.

.

.

.

attractive

future

total

shareowner

return.

Key Takeaways . . . . th

financial performance

financial performance |

| Appendix

Appendix

*

*

*

*

*

*

*

*

*

*

*

*************************************** |

2014

Adjusted EPS (non-GAAP)

.

.

.

.

Enterprises and Parent

Enterprises and Parent

.

.

.

.

growth

up

5%

to

7%

over

2013.

.

.

.

.

.

.

.

.

growth

growth

up

up

5%

5%

to

to

7%

7%

over

over

2013.

2013.

Utility

Utility

25 |

CMS

Energy Parent CMS Energy Parent

Cash at year end 2013

116

$

Sources

Consumers Energy dividend and tax sharing

670

$

Enterprises

25

Sources

695

$

Uses

Interest and preferred dividend

(135)

$

Overhead and Federal tax payments

(10)

Equity infusion

(350)

Pension contribution

0

Uses

a

(495)

$

Cash flow

200

$

Financing and Dividend

New issues

250

$

Retirements

(250)

DRP, continuous equity

45

Net short-term financing & other

(10)

Common dividend

(290)

Financing

(255)

$

Cash at year end 2014

61

$

Bank Facility ($550) available

548

$

Amount

(mils)

Consumers Energy

Consumers Energy

_ _ _ _ _

a

Includes other

_ _ _ _ _

b

Includes

cost

of

removal

and

capital

leases

Cash at year end 2013

18

$

Sources

Operating (depreciation & amortization $679)

1,800

$

Other working capital

(125)

Sources

1,675

$

Uses

Interest and preferred dividend

(225)

$

Capital expenditures

b

(1,645)

Dividend and tax sharing $(225) to CMS

(670)

Pension contribution

0

Uses

(2,540)

$

Cash flow

(865)

$

Financing

Equity

350

$

New issues (includes securitization bonds)

850

Retirements

(200)

Net short-term financing & other

(128)

Financing

872

$

Cash at year end 2014

25

$

Bank Facility ($650) available

650

$

AR Facility ($250) available

180

$

Amount

(mils)

26

2014 Cash Flow Forecast (non

-

GAAP) |

| GAAP Reconciliation

GAAP Reconciliation

*

*

*

*

*

*

*

*

*

*

*

*

*

*

*

*

*

*

*

*

*

*

********************************* |

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Reported earnings (loss) per share - GAAP

($0.30)

$0.64

($0.44)

($0.41)

($1.02)

$1.20

$0.91

$1.28

$1.58

$1.42

$1.66

After-tax items:

Electric and gas utility

0.21

(0.39)

-

-

(0.07)

0.05

0.33

0.03

-

0.17

-

Enterprises

0.74

0.62

0.04

(0.02)

1.25

(0.02)

0.09

(0.03)

(0.11)

(0.01)

*

Corporate interest and other

0.16

(0.03)

0.04

0.27

(0.32)

(0.02)

0.01

*

(0.01)

*

*

Discontinued operations (income) loss

(0.16)

0.02

(0.07)

(0.03)

0.40

(*)

(0.08)

0.08

(0.01)

(0.03)

*

Asset impairment charges, net

-

-

1.82

0.76

0.60

-

-

-

-

-

-

Cumulative accounting changes

0.16

0.01

-

-

-

-

-

-

-

-

-

Adjusted earnings per share, including MTM -

non-GAAP $0.81

$0.87

$1.39

$0.57

$0.84

$1.21

(a)

$1.26

$1.36

$1.45

$1.55

$1.66

Mark-to-market impacts

0.03

(0.43)

0.51

Adjusted earnings per share, excluding MTM - non-GAAP

NA

$0.90

$0.96

$1.08

NA

NA

NA

NA

NA

NA

NA

*

Less than $500 thousand or $0.01 per share.

(a)

$1.25 excluding discontinued Exeter operations and accounting changes

related to convertible debt and restricted stock. Earnings Per Share

By Year GAAP Reconciliation (Unaudited)

28 |

2012

2013

2014

2015

2016

2017

2018

Consumers Operating Income + Depreciation & Amortization

1,635

$

(a)

1,740

$

1,800

$

1,876

$

1,952

$

2,054

$

2,162

$

Enterprises Project Cash Flows

17

16

25

30

28

35

36

Gross Operating Cash Flow

1,652

$

1,756

$

1,825

$

1,906

$

1,980

$

2,089

$

2,198

$

(411)

(335)

(375)

(356)

(730)

(739)

(748)

Net cash provided by operating activities

1,241

$

1,421

$

1,450

$

1,550

$

1,250

$

1,350

$

1,450

$

(a) excludes $(59) million 2012 disallowance related to electric decoupling

CMS Energy

Reconciliation of Gross Operating Cash Flow to GAAP Operating Activities

(unaudited)

(mils)

Other operating activities including taxes, interest payments and

working capital

29 |

30

Consumers Energy

2014

Forecasted

Cash

Flow

GAAP

Reconciliation

(in

millions)

(unaudited) |

31

CMS Energy Parent

2014 Forecasted Cash Flow GAAP Reconciliation (in millions) (unaudited)

|

32

Other

Consumers

Equity

Consumers

CMS Parent

Consolidated

Common Dividend

Infusions to

Consolidated Statements of Cash Flows

Description

Amount

Amount

Entities

as Financing

Consumers

Amount

Description

Cash at year end 2013

18

$

-

$

154

$

-

$

-

$

172

$

Cash at year end 2013

Net cash provided by

1,328

$

527

$

40

$

(445)

$

-

$

1,450

$

Net cash provided by

operating activities

operating activities

Net cash provided by

(1,684)

(350)

(114)

-

350

(1,798)

Net cash used in

investing activities

investing activities

Cash flow from

(356)

$

177

$

(74)

$

(445)

$

350

$

(348)

$

Cash flow from

operating and

operating and

investing activities

investing activities

Net cash provided by

363

$

(177)

$

18

$

445

$

(350)

$

299

$

Net cash provided by

financing activities

financing activities

Net change in cash

7

$

-

$

(56)

$

-

$

-

$

(49)

$

Net change in cash

Cash at year end 2014

25

$

-

$

98

$

-

$

-

$

123

$

Cash at year end 2014

Consolidated CMS Energy

2014 Forecasted Consolidation of Consumers Energy and CMS Energy Parent Statements of Cash Flow (in

millions) (unaudited) Eliminations/Reclassifications/Consolidation to

Arrive at the Consolidated Statement of Cash Flows

Statements of Cash Flows |