Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - CINCINNATI FINANCIAL CORP | v367808_8k.htm |

Cincinnati Financial Corporation February 2014

Nasdaq : CINF • This presentation contains forward - looking statements that involve risks and uncertainties. Please refer to our various filings with the U.S. Securities and Exchange Commission for factors that could cause results to materially differ from those discussed. • The forward - looking information in this presentation has been publicly disclosed, most recently on February 5, 2014, and should be considered to be effective only as of that date. Its inclusion in this document is not intended to be an update or reaffirmation of the forward - looking information as of any later date. • Reconciliations of non - GAAP measures are in our most recent quarterly earnings news release, which is available on the Investors page of our website cinfin.com .

Strategy Overview • Competitive advantages: • Relationships leading to agents’ best accounts • Financial strength for stability and confidence • Local decision making and claims excellence • Other distinguishing factors: • 53 years of shareholder dividend increases • Common stocks for roughly 30% of investments • 25 years of favorable reserve development

Performance Targets & Trends • 16.1% value creation ratio for 2013 exceeded 10% to 13% target • Related performance drivers were on track at year - end: – 12% premium growth more than doubled industry average – 93.8% combined ratio was below 95% target – Investment income grew the last two quarters, equity portfolio 2013 total return within 0.7 percentage - points of S&P 500 I ndex • Ranked #1 or #2 in ~75% of agencies appointed 5+ years • Improving through strategic profit and growth initiatives

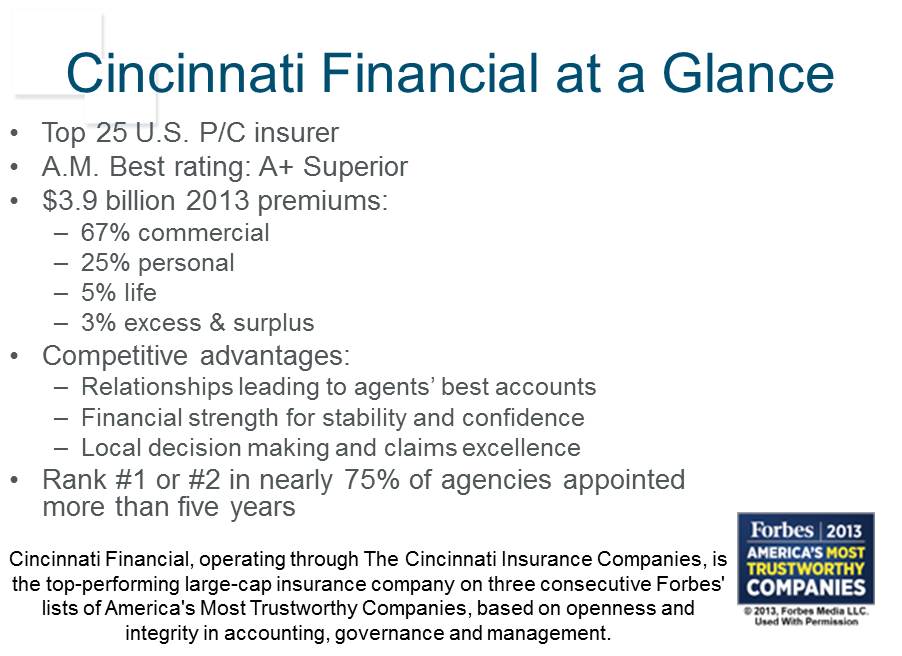

Cincinnati Financial at a Glance • Top 25 U.S. P/C insurer • A.M. Best rating: A+ Superior • $3.9 billion 2013 premiums: – 67% commercial – 25% personal – 5% life – 3% excess & surplus • Competitive advantages: – Relationships leading to agents’ best accounts – Financial strength for stability and confidence – Local decision making and claims excellence • Rank #1 or #2 in nearly 75% of agencies appointed more than five years Cincinnati Financial, operating through The Cincinnati Insurance Companies, is the top - performing large - cap insurance company on three consecutive Forbes' lists of America's Most Trustworthy Companies, based on openness and integrity in accounting, governance and management.

Full - year 2013 Highlights • EPS of $3.12 vs. 2012 of $2.57 per share, up 21% – Operating earnings of $2.80 per share, up 17% from 2012 • Property casualty net written premiums grew 12% – Higher average renewal pricing: commercial lines and personal lines rose mid - single - digits, excess and surplus lines rose high - single - digits • Combined ratio of 93.8%, 89.2% before catastrophes – 2.3 percentage - point combined ratio improvement from 2012 • Increased shareholder dividend for 53 rd consecutive year in August 2013, and another 4.8% January 2014 increase – Only nine U.S. public companies can match that record – Yield is attractive, over 3.5% in early February 2014 • Excellent financial flexibility – Over $1.5 billion cash and securities at parent company – Low debt leverage at 12.8%

Long - Term Value Creation • Targeting annual rate of growth in book value plus the rate of dividend contribution to average 10% to 13% from 2013 through 2017 – Value creation ratio (VCR) for 2009 through 2013 averaged 13.1% – 16.1% VCR for 2013 was up 3.5 points from 2012 • Realized plus unrealized capital gain component was 0.9 points higher • Operating earnings netted with other components was 2.6 points higher • Three performance drivers: – Premium growth above industry average – Combined ratio consistently within the range of 95% to 100% – Investment contribution • Investment income growth • Compound annual total return for equity portfolio over five - year period exceeding return for S&P 500 Index

Increase Value for Shareholders Measured by Value Creation Ratio (VCR) -10% -5% 0% 5% 10% 15% 20% 25% 30% 35% 40% 2009 2010 2011 2012 2013 VCR - Investment Income & Other VCR - P&C Underwriting VCR - Bond Portfolio Gains VCR - Equity Portfolio Gains Total Shareholder Return (TSR) 19.7% 16.1% Target for the period 2013 - 2017: Annual VCR averaging 10% to 13% 11.1% 6.0 % 12.6%

• 2011 ratios exclude the effects of $42 million reinsurance reinstatement premium Combined Ratio Reflects Improving Underwriting Profitability Trends 94.7% 86.1% 89.2% 103.9% 96.8% 92.5% 70% 75% 80% 85% 90% 95% 100% 105% Year 2011 Year 2012 Year 2013 AY 2011 at 12 mos AY 2012 at 12 mos AY 2013 at 12 mos Calendar Year basis - excl. cat. losses Accident Year basis - excl. cat. losses All combined ratios in the graph above exclude the effects of catastrophe losses

Strategies for Long - Term Success • Financial strength for consistent support to agencies – Diversified fixed - maturity portfolio, laddered maturity structure • No corporate exposure exceeded 0.7% of total bond portfolio at 12 - 31 - 13, no municipal exposure exceeded 0.3% – 31.2% of investment portfolio in common stocks to grow book value • No single security exceeded 3.2% of publicly traded common stock portfolio – Portfolio composition helps mitigate anticipated effects of inflation and a rise in interest rates – Low reliance on debt, with debt - to - total - capital target < 20% • Nonconvertible, noncallable debentures due in 2028 and 2034 – Capacity for growth with premiums - to - surplus at 0.9 - to - 1 • Operating structure reflects agency - centered model – Field focus – staffed for local decision - making, agency support – Superior claims service and broad insurance product offerings • Profit improvement and premium growth initiatives

Improve Profitability • Enhancing underwriting expertise and knowledge – Property loss mitigation efforts supplement rate increases and gradual geographic diversification: • Increasing specialized expertise of our claims and loss control staff • Revising underwriting guidelines and increasing property inspections • Implementing higher wind and hail deductibles in selected areas • Covering older roofs at actual cash value instead of replacement cost – Ongoing enhancement initiatives for predictive modeling tools and analytics to improve pricing precision – Data management for better underwriting and pricing decisions; long - term data warehouse project continues to be developed over time • Technology is improving efficiencies and streamlining processing for agencies and the company • Ongoing efforts for greater efficiency and effectiveness – A dditional field positions staffed for better risk selection and specialized claims service without adding to overall staffing levels – Seven full - time - equivalent decrease in total staff at year - end 2013 versus 2009 • 9 % increase in field staff and 4% decrease in headquarters staff

Drive Premium Growth • New agency appointments bring potential for growth over time – Target for 2014: appoint approximately 100 agencies • 96 appointed in 2013, $2.0B aggregate premiums from all carriers • 140 appointed in 2012, $2.7B aggregate premiums from all carriers • Expanding marketing and service capabilities – Ongoing development of target market programs and cross - selling – C ustomer care center pilot for small commercial policies – Growth includes gradual geographic diversification • Personal lines 2013 earned premium growth rate in 26 smallest states nearly tripled the rate for our four largest personal lines states of operation • Double - digit growth in 2013 property casualty net written premiums – Commercial up 12%, Personal up 9 %, E&S up 22% – Total P&C up 12%, Term life insurance earned premiums up 6% – Recent - year growth reflects strategic targeting ; almost half of the growth since mid - 2012 was from higher pricing

Premium Growth Potential • Historically, we earn approximately 10% market share in new agencies within 10 years after appointment – demonstrated by: – 2% share earned in 2012 for all agencies appointed in 2011, 5 % for appointments during 2008 - 11, 8 % for appointments during 2003 - 07 – $52 million of $543 million total 2013 new business written premiums produced by agencies appointed since early 2012 • Our agencies currently write significant amounts of business with other carriers, representing potential for us – Agencies appointed during 2009 - 13 place $10 billion in annual premiums for standard lines business with all carriers they represent – Excess and surplus lines for all of our agents – approximately $2 billion • We help our agencies grow their businesses by attracting more clients in their communities through our unique service

Select Group of Agencies in 39 States P&C Market Share: 1% and higher Less than 1% Inactive states Headquarters (no branches) 1,450 agency relationships with 1,823 locations Our Commercial Top Five = 41% Ohio, Illinois, Pennsylvania, Indiana, North Carolina Our Personal Top Five = 57% Ohio, Georgia, Indiana, Illinois, Michigan (as of December 31, 2013) Market Share Top Three Ohio at 4.8% Indiana at 2.8% Illinois at 1.4% Based on 2012 data excluding A&H

Appendix Income, Dividend & Cash Flow Trends Underwriting & Premium Growth Trends Business Mix & Premium Growth Potential Reserve Adequacy & Development Trends Investment Portfolio Management & Performance Reinsurance, Ratings & Valuation Comparison to Peers

Income and Shareholder Dividends $0.00 $0.50 $1.00 $1.50 $2.00 $2.50 $3.00 2009 2010 2011 2012 2013 Operating Income Net Income Dividends Per share basis

0% 20% 40% 60% 80% 100% 120% 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011* 2012 2013 Dividend Payout Ratio – Net Income Dividend Payout Ratio – Operating Income 58% average for years 2004 through 2013 (net income basis) Cash Dividend Payout Ratio Strong Capital and Cash Flow Support Recent - Year Payout Level * 2011 payout ratios (159% net income basis, 211% operating income basis) not fully shown on graph due to record - high catastrop he losses

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Dividend as a Percentage of Net Cash Flow From Operations

Operating Cash Flow Generally Trending Favorably, Aligned with Rising Profits $0 $100 $200 $300 $400 $500 $600 $700 $800 2008 2009 2010 2011 2012 2013 (In millions) Record - high catastrophe losses in 2011

Cincinnati Typically Outperforms the Industry 65% 70% 75% 80% 85% 90% 95% 100% 105% 2009 2010 2011 2012 2013 Cincinnati – excl. cat. losses Est. Industry (A.M. Best) – excl. cat. Losses Cincinnati – incl. cat. losses Est. Industry (A.M. Best) – incl. cat. Losses Statutory combined ratio Industry data excludes mortgage and financial guaranty Cincinnati’s historical catastrophe loss annual averages as of 12 - 31 - 13: 5 - year = 7.7%, 10 - year = 6.1%

Greater Pricing Precision Is Improving Profit Margins Commercial package p olicy mid - 2013 renewal price increase averages by modeled pricing segments illustrates pricing precision effects Most adequate refers to policies that need less price increase based on pricing adequacy of expiring premium per pricing mode ls 0% 15% Most adequately priced Near (+ or -) price adequacy Least adequately priced

Premium Growth Versus Industry Our Growth Rate Outpaced the Industry as the Market Firmed -4.0% -2.0% 0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 2009 2010 2011 2012 2013 Cincinnati Estimated Industry excluding mortgage and financial guaranty (A.M. Best) Property casualty net written premium growth

Market for 75% of Agency’s Typical Risks 2013 Net Earned Premiums Commercial Property 17% Machinery and Equipment 1% Commercial Casualty 23% Specialty Packages 4% Commercial Auto 13% Workers' Compensation 10% Management liability and surety 3% Excess & Surplus 3% Homeowner 11% Personal Auto 12% Other Personal 3% E&S Lines 3% Commercial Lines 67% Personal Lines 25% Life 5% Consolidated $ 3.902 Billion Property Casualty $3.713 Billion

Premium Growth Potential Steadily Increase Our Share Within Cincinnati - Appointed Agencies 1.8% 5.4% 8.0% 16.1% 1 year or less 2-5 years 6-10 years 10 years or more • Cincinnati share of estimated $33 billion total property casualty premiums produced by currently appointed agencies is approximately 12% Market share per agency reporting location by year appointed Based on 2012 standard market P&C agency written premiums (Excludes excess and surplus lines) New appointments also drive premium growth opportunity. The net amount of agency relationships has increased by 23% since the end of 2009.

Property Casualty Reserves Favorable Development for 25 Consecutive Years $3,661 $3,811 $3,905 $3,813 $ 3,942 2009 2010 2011 2012 2013 Reserve range at 12 - 31 - 13 Low end $ 3,727 High end $4,078 Carried at 61 st percentile Values shown are carried loss and loss expense reserves net of reinsurance Vertical bar represents reasonably likely range Calendar year development (Favorable) ($188) ($304) ($285) ($396) ($147) In millions Ex - cat development: (ratio to earned premiums) 9.3% 10.7% 3.3%

Accident Year Combined Ratios Effect of Reserve Development From Re - estimation Is Significant 94.5% 94.7% 96.3% 97.1% 93.8% 10.0% 10.3% 10.1% 6.3% 3.0% 80% 85% 90% 95% 100% 105% 110% 115% 120% 125% AY 2008 AY 2009 AY 2010 AY 2011 AY 2012 Accident yr as of Dec 31, 2013 Reserve development to date Catastrophe losses - current AY Reinstatement premium effect* Consolidated Property Casualty * $42M 2011 Cat treaty reinstatement premium Duration of loss & loss expense reserves is approximately 4.3 years, reflecting timing for majority of development.

Investment Income 0.7% Growth for 2H13, 0.7% CAGR since 2011 (pretax ) $400 $425 $450 $475 $500 $525 $550 2009 2010 2011 2012 2013 After - tax yield: (Bonds at amortized cost, stocks at fair value) 3.45% 3.39% 3.12% Pretax yield to book as of 12 - 31 - 13 for bonds maturing in 2014=4.8%, 2015=4.5%, 2016=4.5 % Portion of bond portfolio maturing: 6.1% in 2014, 7.6% in 2015, 7.9% in 2016, 22.6% in 2017 - 18

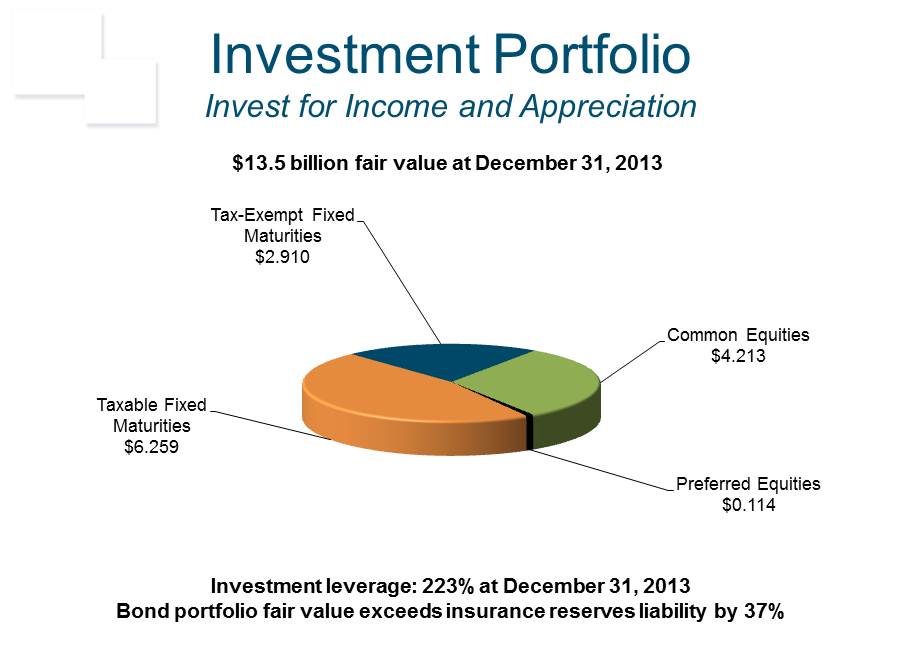

Investment Portfolio Invest for Income and Appreciation Taxable Fixed Maturities $6.259 Tax - Exempt Fixed Maturities $2.910 Common Equities $4.213 Preferred Equities $0.114 $ 13.5 billion fair value at December 31, 2013 Investment leverage: 223% at December 31, 2013 Bond portfolio fair value exceeds insurance reserves liability by 37%

Diversified Equity Portfolio * Balances Income Stability & Capital Appreciation Potential December 31, 2013 Sector CFC S&P 500 Weighting s Information technology 18.7% 18.6% Industrials 14.0 10.9 Financial 12.0 16.2 Healthcare 11.5 13.0 Energy 10.5 10.3 Consumer staples 10.5 9.8 Consumer discretionary 9.8 12.5 Materials 5.7 3.5 Utilities 4.2 2.9 Telecom services 3.1 2.3 * Publicly traded common stock core portfolio, approximately 50 holdings (excludes energy MLP’s, one private equity) Portfolio Highlights at 12 - 31 - 13 • BlackRock Inc. - largest holding • 3.2% of publicly traded common stock portfolio • 1.0% of total investment portfolio • 6 % increase in full - year 2013 dividend income • 47 of 48 companies in core portfolio improved their annual regular dividend over the past 12 months • Unrealized gains totaled $1.9 billion (pretax) • Exxon Mobil, P&G and Chevron combined represent 15% • Annual portfolio returns in 2013 & 2012: 31.7% & 10.9% ( S&P 500: 32.4% & 16.0%)

Bond Portfolio Risk Profile $9.169 Billion at December 31, 2013 • Credit risk – A2/A average rating – 60% rated >=A, 35% rated BBB, 3% rated <=BB, 2% unrated – No European sovereign debt – Euro - based securities are 5% of bond portfolio (mostly corporate bonds) • Interest rate risk – 4.6 years effective duration, 6.2 years weighted average maturity – Generally laddered maturity structure • 22% of year - end 2013 portfolio matures by the end of 2016, 44% by 2018, 85% by 2023 – With 31.2% of the investment portfolio invested in common stocks at 12 - 31 - 13, we estimated shareholders’ equity would decline 4.5% if interest rates were to rise by 100 basis points • Bond portfolio is well - diversified – Largest issuer (corporate bond) = 0.7% of total bond portfolio – Municipal bond portfolio (approximately 1,000 issuers) • Almost 60% insured at 12 - 31 - 13, 97% with underlying rating >=A3/A - • Texas issuers = 16%, Michigan = 9 %, 13 other states each 1% to 8% • 68% locally issued general obligations, 32% special revenue bonds

Solid Reinsurance Program Balances Costs With Shareholders’ Equity Protection Major Treaties (Estimated 2013 ceded premiums) Coverage and Retention Summary at 01 - 01 - 14 Property catastrophe ($60 million) • Treaty has one reinstatement provision • $100 million additional coverage collateralized by catastrophe bond for severe convective storm or earthquake losses in certain geographic regions For a single event: • Retain 100% of first $75 million in losses • Retain 60.8% for losses at $75 - 100 million • Retain 5.0% at $100 - 600 million • Max exposure for $600M event = $115 million Property per risk & $10 million property excess treaty ($42 million) For a single loss: • Retain 100% of first $8 million in losses • Retain 0% of losses $8 - 35 million • Facultative reinsurance for >$35 million Casualty per occurrence ($29 million) For a single loss: • Retain 100% of first $8 million in losses • Retain 0% of losses $8 - 25 million • Facultative reinsurance for >$25 million Casualty excess treaties ($3 million for two treaties combined) Workers’ comp, extra - contractual & clash coverage • $25 million excess of $25 million (first excess treaty) • $20 million excess of $50 million (second treaty) Primary reinsurers are Swiss Re, Munich Re, Hannover Re, Partner Re and Lloyds of London

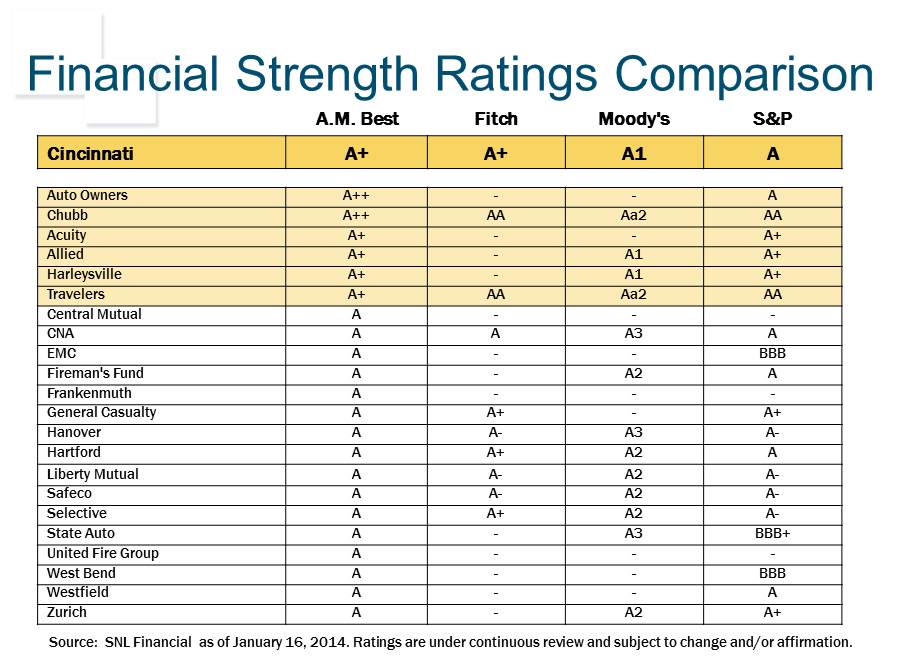

Source: SNL Financial as of January 16, 2014. Ratings are under continuous review and subject to change and/or affirmation. A.M. Best Fitch Moody's S&P Cincinnati A+ A+ A1 A Auto Owners A++ - - A Chubb A++ AA Aa2 AA Acuity A+ - - A+ Allied A+ - A1 A+ Harleysville A+ - A1 A+ Travelers A+ AA Aa2 AA Central Mutual A - - - CNA A A A3 A EMC A - - BBB Fireman's Fund A - A2 A Frankenmuth A - - - General Casualty A A+ - A+ Hanover A A - A3 A - Hartford A A+ A2 A Liberty Mutual A A - A2 A - Safeco A A - A2 A - Selective A A+ A2 A - State Auto A - A3 BBB+ United Fire Group A - - - West Bend A - - BBB Westfield A - - A Zurich A - A2 A+ Financial Strength Ratings Comparison

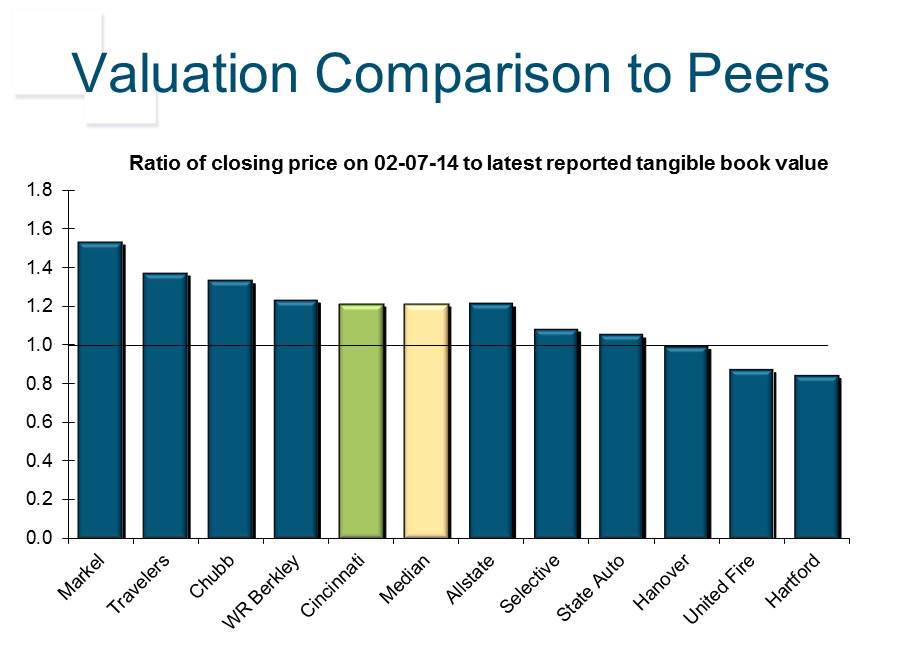

Valuation Comparison to Peers 0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 Ratio of closing price on 02 - 07 - 14 to latest reported tangible book value