Attached files

| file | filename |

|---|---|

| 8-K - 8-K - SUSQUEHANNA BANCSHARES INC | d672514d8k.htm |

Susquehanna Bancshares, Inc.

Investor Presentation

1

st

Quarter 2014

Exhibit 99.1 |

Forward-Looking Statements

During the course of this presentation, we may make forward-looking statements

regarding priorities and strategic objectives of

Susquehanna Bancshares, Inc., as well as capital ratios, efficiency ratios, net

income and earnings. Investors should understand that these

forward-looking statements are strategic objectives rather than projections of future performance. We

wish to caution you that actual results and trends could differ materially from

those set forth in such statements due to various risks, uncertainties and

other factors. The risks, uncertainties and other factors that could cause

actual results and experience to differ from those projected include, but

are not limited to, the following: ineffectiveness of Susquehanna’s business strategy

due to changes in current or future market conditions; the effects of competition,

including industry consolidation and development of competing financial

products and services; the costs and effects of legal and regulatory developments

including the resolution of legal proceedings or regulatory or other governmental

inquiries and the results of regulatory examinations or reviews; interest

rate movements; changes in credit quality; deteriorating economic conditions; other risks and

uncertainties; and our success at managing the risks involved in

the foregoing items. For a more detailed description of the

factors that may affect Susquehanna’s operating results, we refer you to our

filings with the Securities & Exchange Commission, including our annual

report on Form 10-K for the year ended December 31, 2012 and Form 10-Q for the quarter

ended September 30, 2013. Susquehanna assumes no obligation to update the

forward-looking statements made during this presentation.

For more information, please visit our Website at:

www.susquehanna.net

2 |

Why

Susquehanna? 3

Business Strategy

Regional bank with a customer-focused “community bank”

delivery model

Grow deposits –

attractive markets with rich deposit base and favorable demographics

Commercial loan focus –

ample small business opportunities within footprint

Enhance fee income activities –

capital markets, cash management, mortgage and wealth

Invest to enhance customer experience , employee engagement and risk

management Management Team

Executive management team with 200+ years of combined banking experience

Deep knowledge of the markets Susquehanna serves

Interests aligned with stockholders through short-term incentives tied to

strategic goals and long- term incentives tied to relative total

shareholder return and return on tangible common equity (“ROTCE”)

Valuation

Trade at a discount to peers on an earnings and book value basis

Very attractive dividend yield at 3.0%

1

Long-Term Upside

Execution of strategy builds attractive deposit franchise and enhances the

long-term earnings power of Susquehanna

Potential P/E expansion due to higher earnings growth and lower cost of

equity Stronger balance sheet and fee income activities while

improving liquidity and interest rate

risk profile

1

Based on current annualized dividend of $0.32 per share and closing price on January

31, 2014. |

Table

of Contents 4

Susquehanna Overview

5

Financial Review: Fourth Quarter and Full Year 2013

10

Business Strategy: Regional Bank With a Customer-Focused

“Community Bank”

Delivery Model

15

Valuation and Long-Term Upside

28

Quarterly Financial Supplement

31 |

Susquehanna Overview

5 |

Susquehanna Overview

6

Corporate Overview

Regional bank headquartered in Lititz, PA

245 banking offices concentrated in Central PA,

Western MD, and Philadelphia and Baltimore

MSAs

38

th

largest U.S. commercial bank by assets

and 2

nd

largest headquartered in PA

Experienced management team with extensive

market knowledge

Franchise is a diversified mix of consumer and

business customers, products and revenue

sources

Non-bank affiliates offering products and

services in:

–

Wealth management

–

Insurance brokerage and

employee benefits

–

Commercial finance

–

Vehicle leasing

Assets:

$18.5 billion

Deposits:

$12.9 billion

Loans & Leases:

$13.6 billion

Assets under management

$7.6 billion

and administration:

Market cap

1

:

$2.0 billion

Average daily volume

2

:

>1 million shares

Institutional ownership:

>70%

Dividend yield

3

:

3.0%

NASDAQ:

SUSQ

1

Based on closing price on January 31, 2014.

2

Over the last 52 weeks.

3

Based on current annualized dividend of $0.32 per share and closing price on

January 31, 2014. Selected Data as of 12/31/2013

|

Uniquely Positioned

7

Source: SNL Financial.

Note: Regulatory branch and deposit data as of June 30, 2013; banks and thrifts with

deposits in counties SUSQ operates in PA/NJ/MD/WV; traditional and

in-store branches only, as defined by SNL. Counties

of

operation

are

listed

in

the

“Quarterly

Financial

Supplement”

slides

at

the

conclusion

of

this

presentation.

Proven ability to grow share and

rank in key markets of operation:

–

Top 3 market share in 11 of 40

counties

–

10%+ market share in

13 counties

–

Top 5 market share in half the

MSAs where we do business

Largest locally based community

bank in our market

Ample opportunity to grow

deposits with small market share

gains:

–

Increasing market share 30 bps to

4.9% would bring loan to deposit

ratio just below 100%, in-line with

our 2014 target

Deposit Market Share: Counties of Operation

Rank

Institution

Branch

Count

Total Deposits in

Market ($000)

Total Market

Share (%)

1

Wells Fargo

377

41,514,008

14.9%

2

PNC

393

28,419,912

10.2%

3

Bank of America

217

25,180,194

9.1%

4

M&T Bank

324

24,420,075

8.8%

5

Toronto-Dominion Bank

167

20,925,057

7.5%

6

Royal Bank of Scotland

217

18,654,030

6.7%

7

Susquehanna

245

12,790,628

4.6%

8

Fulton

191

9,513,532

3.4%

9

Banco Santander

178

9,222,815

3.3%

10

National Penn

120

5,945,401

2.1%

11

BB&T

68

4,327,798

1.6%

12

Beneficial

60

3,777,354

1.4%

13

Citi

13

2,811,745

1.0%

14

First Niagara

61

2,481,487

0.9%

15

Customers

12

2,270,071

0.8%

Total

(1-15)

2,665

212,254,107

76.4%

Total

(1-239)

4,146

277,747,024

100.0% |

Leading Competitive Position

8

Better positioned with a stronger market concentration than peers

Markets of operation are wealthier and faster growing than peers

Market presence in 14 of the 20 most affluent counties in PA by median household

income –

Maryland market includes Baltimore and three of the nation’s 40

most-affluent counties including no. 3, Howard County Source:

SNL

Financial,

U.S.

Census.

Peer

data

reflects

median

of

peer

companies.

Identification

of

peer

companies

is

included

in

the

“Quarterly

Financial

Supplement”

at

the

conclusion

of

this

presentation.

Deposit

data

as

of

June

30,

2013

1

Reflects

weighted

average

by

deposits

at

the

county

level.

Household

income

as

of

2012.

2

Reflects

2012-2017

projected

population

growth.

SUSQ

Peers

% of Deposits in Counties

with #1 Rank

31%

21%

% of Deposits in Counties

with 25% Market Share

32%

15%

SUSQ

Peers

Median Household

Income

1

$56,915

$49,829

% of Deposits in Counties

with HHI Over $60,000

28%

12%

% of Deposits in Counties

with Population Growth

Over 2.5%

2

53%

36%

Attractive Market Demographics and Leading Competitive Position

|

Positioned for Further Growth

9

Pennsylvania Market

Delaware Valley Market

Maryland Market

115 branches

Foundation for growth with stable commercial

and retail banking base providing ample deposits

Home to distribution hubs for global retailers,

manufacturers and distributors serving Northeast

and Mid-Atlantic markets

69 branches

Growth opportunities fueled by world-leading

education, health care and research institutions

61 branches

Growth opportunities fueled by world-leading

education, health care and research institutions,

as well as major federal agencies and

contractors

Small Business Density Complements Branch Footprint

Source:

Bank

Intelligence.

“Small

Business”

defined

as

businesses

with

less

than

$10

million

in

annual

sales.

The

16

counties

comprising

the

company’s

Pennsylvania

Market,

the

10

counties

comprising

the

company’s

Delaware

Valley

Market

and

the

14

counties

comprising

the

company’s

Maryland

Market

are

listed

in

the

“Quarterly

Financial

Supplement”

slides

at

the

conclusion

of

this

presentation. |

Financial Review: Fourth Quarter and Full Year 2013

10 |

Fourth Quarter 2013 Highlights

11

GAAP EPS of $0.22

Modestly lower than $0.24 in 3Q13 and $0.23 in 4Q12

Fee

Income

Activities

Showing

Strength

Capital

markets

revenue

up

$2.1

million

in

4Q13

Wealth management revenue grew to $13.0 million, up 3.5% linked quarter

Mortgage banking revenue rebounded from 3Q13, up 11.0%

Strong

Commercial

Loan

Growth

Commercial loans grew 5.3% linked quarter

Continued strength in loan originations, up 16.6% from 4Q12

Continued

Focus

on

Deposit Growth

Non-CD deposits increased by 1.7% linked quarter

Non interest bearing demand deposits grew 2.2% linked quarter

Focused

on

Returns

ROAA of 0.89% compared to 0.96% and 0.95% in 3Q13 and 4Q12, respectively

ROATE

1

of 12.49% compared to 13.67% and 14.01% in 3Q13 and 4Q12, respectively

Branch

Initiatives

Completed

Sale leaseback transaction resulted in $5.0 million pre-tax gain and $4.0

million income tax benefit

Consolidation of 14 branches resulted in one-time costs totaling $6.6 million,

pre-tax and ongoing expected annual cost savings of $5.0 million

Solid

Credit

Quality

Metrics

and

Capital

Ratios

NPAs improved to 0.86% of loans, leases and foreclosed real estate

Strong coverage ratio with allowance representing 156% of nonaccrual loans and

leases Tangible common ratio

1

of 8.44%; regulatory ratios exceed “well capitalized”

1

Non-GAAP

based

financial

measures;

please

refer

to

the

“Quarterly

Financial

Supplement”

slides

at

the

conclusion

of

this

presentation

for

calculations. |

Fourth Quarter Purchase

Accounting Impact

12

Tower’s purchased credit impaired fair value marks are

amortized by pooling like asset classes while Abington’s marks

are amortized at the loan level

Non-purchased credit impaired fair value marks are amortized

at the loan level

Predicting future amortization is challenging due to

prepayment/refinancing, customer behavior and the overall

health of the economy

Total purchase accounting benefit was 15bps in 4Q13

compared to 18bps in 3Q13

Loan amortization was 11bps in 4Q13 compared to 13bps in

3Q13

Deposit and borrowing amortization was 4bps in 4Q13

compared to 5ps in 3Q13

Net interest margin, excluding purchase accounting,

1

declined

9bps from 3.54% in 3Q13 to 3.45% in 4Q13

Non purchase accounting roll forward

Note:

Additional

information

on

purchase

accounting

impact

is

included

in

the

“Quarterly

Financial

Supplement”

slides

at

the

conclusion

of

this

presentation.

1

Non-GAAP

based

financial

measures;

please

refer

to

the

“Quarterly

Financial

Supplement”

slides

at

the

conclusion

of

this

presentation

for

calculations

. |

Full

Year 2013 Highlights 13

1

Non-GAAP

based

financial

measures;

please

refer

to

the

“Quarterly

Financial

Supplement”

slides

at

the

conclusion

of

this

presentation

for

calculations.

Record Earnings

Record net income of $173.7 million, up 23% over 2012

Double-Digit Growth in Non-

Interest Income

Initiatives

to

grow

non-interest

income

delivered

solid

revenues

in

2013

–

up

10%

over

2012

–

Wealth management revenue up 8% to $51.3 million

–

Cash management revenue grew 15% to ~$10.0 million

–

Capital markets revenue up 66% to $5.0 million

Successful Lending Strategies

Commercial loans up 5.3% YOY, including planned exits from non-strategic

participations Successful originate-to-sell strategy in residential

mortgage: sold 56% of production and retained servicing on 68% of

loans Total originations up 33% from 2012

Deposit Growth

Non-CD deposits up 2.4% YOY

Growth muted by strategic exits from certain higher-priced

non-relationship customers Net Interest Margin

Net interest margin excluding purchase accounting of 3.53%

1

Improved Profitability

ROAA of 0.95% compared to 0.81% in 2012

ROATE

1

of 13.57% compared to 12.03% in 2012

Branch Initiatives Completed

Sale leaseback transaction resulted in $5.0 million pre-tax gain and $4.0

million tax benefit Branch consolidations resulted in one-time costs

totaling $6.6 million, pre-tax, and ongoing expected annual cost

savings of $5.0 million Solid Credit Quality Metrics

and Capital Ratios

NPAs declined 5.4% to $117.4 million, or 0.86% of loans, leases and foreclosed

real estate NCOs / average loans and leases decreased 11 bps to 0.44%

Tangible common ratio

1

of 8.44% increased 50 bps from 2012 |

2013

Performance vs. Peers 14

Susquehanna

Peer Median

5

ROAA

0.95%

0.86%

ROATE

1

13.57%

10.99%

Net Interest Margin

3.79%

3.41%

Loans % of Deposits

105%

85%

Loan Growth

5.3%

6.0%

Deposit Growth

2.3%

2.2%

Deposit Cost

0.47%

0.28%

C&I % of Total Loans

2

13.8%

24.9%

Checking Deposits %

of Total Deposits

2,3

22.2%

33.4%

Efficiency Ratio

1

62.55%

64.57%

Fee Income % of Operating Revenue

4

23.2%

29.2%

NPAs % of Loans and Leases and

Foreclosed Real Estate

0.86%

1.08%

NCOs % of Average Loans and Leases

0.44%

0.25%

Tier 1 Common Ratio

10.59%

10.55%

Source: SNL Financial and company filings

1

Non-GAAP

based

financial

measures;

please

refer

to

the

“Quarterly

Financial

Supplement”

slides

at

the

conclusion

of

this

presentation

for

calculations.

2

Per

9/30/13

regulatory

filings.

3

Interest-bearing

and

non-interest

bearing

transaction

deposits

per

regulatory

filings.

4

As

reported

by

SNL.

Excludes

securities

gains

and

losses

and

other

non-recurring

items.

5

Please

refer

to

the

“Quarterly

Financial

Supplement”

slides

at

the

conclusion

of

this

presentation

for

the

listing

of

the

peer

companies.

Solid profitability

Focus on improving loan to deposit ratio

Fee income activities in place to deepen

relationships and close the gap to peers

NCOs/Avg. loans and leases trending

towards peers while the Tier 1 common

ratio is in-line

Working to close the gap to peers by

growing checking deposits and commercial

loans in attractive markets

Comments |

Business Strategy: Regional Bank With a

Customer-Focused “Community Bank”

Delivery Model

15 |

Strategic Focus: Multi-Year Plan

16

OBJECTIVE: Transition to a Robust Relationship-Based Customer Model

1.

Shift in Model and

Focus

New investments

focused on:

–

Technology

–

Risk management

–

Employee engagement

–

Customer experience

–

Service delivery

–

Marketing

–

Pricing

–

Products

Evaluating new and existing relationships for relationship profitability

Piloting universal banker model in selective markets

2.

Hiring and Talent

Recruiting experienced leaders across the bank

Hiring individuals and teams

Employee engagement at all levels

Building capabilities to foster existing employee development

3.

Redesigned Incentive

Structure

New profitability model to drive bankers’

incentives

Incentives promote cross selling, risk management and total portfolio

management |

Investing for Tomorrow

17

Investments Focused on What We Can Control

Aligning Infrastructure With Our

Growth into Top 50 Bank Rankings

Ensuring systems, processes and capabilities can accommodate growth

beyond the $18 billion institution Susquehanna is today

Focus on Scalable Investments

Software and technology

Fee income activities

Risk management

Customer experience

Service delivery

Investments for Business Demand

4 of the top 5 budgeted capital expenditures for 2014 are for business

demand: –

ATMs

–

Branch relocation

–

Product software

–

Commercial Banking online upgrades

Investments today position Susquehanna for future growth and performance

Business demand drives

84% of budgeted spend

for top 5 capital

expenditures in 2014

Higher expenses in the

near-term |

Investing in Talent

18

Approximately 45% of Susquehanna’s top 60 leaders have joined within the last

two years, bringing new ideas and best

practices to bear

Aligning corporate and individual objectives with strategic plan

and stockholders’

interests

–

Short-term incentives tied to strategic goals

–

Long-term incentive plan tied to relative total shareholder return and

ROTCE WILLIAM REUTER

Chairman and CEO

39 years banking experience,

including 23 years with Susquehanna

ANDREW SAMUEL

Bank President and CEO

29 years banking experience

2 years with Susquehanna

MIKE HARRINGTON

Chief Financial Officer

27 years banking experience

2 years with Susquehanna

MICHAEL QUICK

Chief Corporate

Credit Officer

42 years banking experience

23 years with Susquehanna

GREGORY DUNCAN

Chief Operating Officer

30 years banking experience

23 years with Susquehanna

CARL LUNDBLAD

Chief Legal &

Administrative Officer

16 years banking / legal

experience

2 years with Susquehanna

BEV WISE

Chief Human

Resources Officer

25 years banking experience

2 years with Susquehanna

KEVIN BURNS

Chief Risk Officer

15 years banking experience

<1 year with Susquehanna |

Business Strategy

19

Strategic Priorities for 2014

Focus on

Deposits

Helps achieve 2014 target loan to deposit ratio of <100%; longer

term below mid-90’s

Significant opportunity in existing client base

Take share from larger competitors with “community bank”

delivery model

Complements strategy to grow commercial loans and success of Stellar Checking

retail campaign Optimize

Balance Sheet

Focus on growing commercial loans while limiting indirect auto and selling more

mortgage production –

Dense population of small businesses in-market

–

Product offerings position us to compete with small and large banks

Small business relationships provide opportunities in wealth, capital markets and

cash management –

Growing fee income reduces spread-reliance and promotes stable revenue

stream Customer

Experience

and Employee

Engagement

Delivering a differentiated customer experience with premier service and

simplified processes Fueling customer-centric culture through

investments in talent, technology, products and delivery Aligning

compensation around drivers of sustainable and profitable relationships

–

Incentives tied to full customer relationships, measured through

new profitability model

Enterprise

Risk

Management

Investments in people and processes to effectively manage risk commensurate with

our size, complexity, strategy and growth

More efficient pricing and capital allocation decisions

Enhanced governance and controls |

Focus: Deposits

20

Loan to Deposit Ratio %

Rationale

Ample opportunity to capture greater wallet share and profitability from existing

customers while improving liquidity and interest risk profile

–

Approximately 80% of small business loan customers have a deposit relationship

with Susquehanna, but aggregate small business deposits represent less than

40% of small business loan balances

Strategic

Initiatives

Enhanced profitability models to inform pricing and investment decisions

Focus on deposit-rich markets with ample small business opportunities

Investing in people and technology to streamline loan approval and closing and

deposit account opening process

Piloting universal banker model in selective markets

Sales training and development, emphasizing cross-sell

Increasing marketing spend

Trade-Off

Desire to lower loan to deposit ratio is a constraint on loan growth and earnings

in the short-term. Long-term benefits will be realized when

interest rates rise Source:

SNL

Financial.

Please

refer

to

the

“Quarterly

Financial

Supplement”

slides

at

the

conclusion

of

this

presentation

for

the

listing

of

the

peer

companies. |

Strong Deposit Growth

21

Organic Non-CD

Deposit CAGR:

7.1%

Strong Deposit Growth Momentum

Positive

results

in

mobile

deposit

services

and

Stellar

Checking

account

Non-CD

deposits

now

account

for

70%

of

total

deposits

Non-CD

growth

of

2.4%

since

4Q12,

including

strategic

exit

from

certain

relationships

Cost

of

deposits

decreased

from

2.86%

in

4Q07

to

0.43%

in

4Q13

Total Deposits 12/31/2007

$8.9 Billion

Total Deposits 12/31/2013

$12.9 Billion

Demand deposits

Interest-bearing demand

Savings

Time of $100K or more

Time < $100K |

Deposit Initiatives

22

Innovative Deposit Strategies Driving Growth

Strategic

Building on 2.3% deposit growth in 2013 to drive loan to deposit

ratio below 100% in 2014

Exiting non-strategic relationships and limiting exception pricing

Lowered deposit cost by 10 bps in 2013

Streamlined

Focused on cross-sell opportunities and commercial deposits

Three retail checking accounts today vs. 10+ at the start of 2013

Customer-Centric

Stellar Checking launched in 2013

–

57,000 accounts in first 10 months

–

Half from new customers, with higher average balances

than converted accounts

–

Driving new fee income through increased debit

card usage

Digital channel in 2013

–

Mobile Deposit launched

–

Mobile banking users up 120%

–

E-statements up 107%

–

Total online banking users up 27% |

Disciplined Asset Allocation:

Focus on Commercial Loans

23

Organic Loan

CAGR: 3.8%

Slowing Loan Growth Momentum, Focus on Mix

Rotating assets to achieve more valuable mix

Commercial loan growth of 5.3% since 4Q12, including strategic exit from certain

relationships Limit indirect portfolio growth while selling more

residential production in secondary market Average commercial loan yield in

4Q13 was 4.81%, compared to 3.39% for indirect auto leases 12/31/2007

$8.8 Billion

12/31/2013

$13.6 Billion

Real estate –

construction

Real estate secured –

commercial

Real estate secured –

residential

Consumer

Leases

Commercial, financial and agricultural |

Net

Interest Margin 24

Net interest margin of 3.60% in the quarter versus 3.72% in the prior quarter

Net interest margin, excluding purchase accounting, was down 9 bps, consistent with

expectations and most recent guidance, but remains in-line with peer

reported net interest margin The net interest margin decline is a function of

existing loans repricing at lower rates, a change in the mix of loans and

less benefit from the repricing of higher rate CDs

Deposit growth and strategic shift toward commercial lending expected to provide

more stability to the net interest margin going forward

Source:

SNL

Financial.

Please

refer

to

the

“Quarterly

Financial

Supplement”

slides

at

the

conclusion

of

this

presentation

for

the

listing

of

the

peer

companies.

1

Non-GAAP

based

financial

measure;

please

refer

to

the

“Quarterly

Financial

Supplement”

slides

at

the

conclusion

of

this

presentation

for

calculation.

Net Interest Margin

1 |

Focus on cross-sell as commercial loan and deposit relationships grow

–

Closing the gap to peers on fee income/operating revenue

Diversifying revenue and becoming less reliant on spread revenue

–

Momentum in wealth management, capital markets and cash management

Wealth management continues to expand

–

New wealth management business increased ~$400 million in 2013

Capital markets growing

–

Revenue up 66% in 2013

Cash management driving deposit growth and income

–

$90 million in new demand deposits in 2013

–

Revenue up 15% in 2013

Non-Interest Income

25

Non-interest

Income

($000)

-

Quarter

Ending

Dec.31, 2012

Sept. 30, 2013

Dec. 31, 2013

Service Charges on Deposit Accounts

$ 9,158

$ 9,514

$ 9,456

Vehicle Origination and Servicing Fees

3,746

2,907

3,057

Wealth Management Commissions and Fees

11,882

12,606

13,048

Commissions on Property and Casualty

Insurance Sales

3,749

3,872

4,023

Other Commissions and Fees

6,680

5,276

7,577

Mortgage Banking Revenue

4,835

2,237

2,483

Fee

Income

%

of

Operating

Revenue

1

1

As

reported

by

SNL

Financial.

Excludes

securities

gains

and

losses

and

other

non-recurring

items.

Please

refer

to

the

“Quarterly

Financial

Supplement”

slides

at

the

conclusion

of

this

presentation

for

the

listing

of

the

peer

companies. |

Expense Management

26

Successfully lowered efficiency ratio from 66.83% for 2011 to 62.55% for 2013

–

Recent elevation in efficiency ratio reflects expenses associated with incentive

compensation, branch consolidation costs and investments to build out ERM,

compliance and other strategic initiatives –

Targeted long-term efficiency ratio of 60%

–

Efficiency is a part of our culture; always looking for ways to improve expense

management Note:

Efficiency

ratio

excludes

net

realized

gain

on

acquisition,

merger

related

expenses

and

loss

on

extinguishment

of

debt

and

is

a

non-GAAP

based

financial

measure;

please

refer

to

the

“Quarterly

Financial

Supplement”

slides

at

the

conclusion

of

this

presentation

for

calculations. |

1Q14

Outlook & Current Trends 27

Strategic Priorities Reflected in First Quarter 2014 Outlook

Net Interest Margin

More stability in the net interest margin expected

Change in mix consistent with our strategic plan to grow commercial loans

Existing loans repricing at lower rates appears to have stabilized

Average Earning

Assets

Growth will be limited given strategy to lower the loan to deposit ratio

Commercial loan growth is priority

Focus on rotating the balance sheet mix rather than on total loan growth

Securities portfolio expected to remain relatively flat

Credit

Recent strength in asset quality expected to continue, but may be volatile

quarter-over-quarter Provision is expected to trend in line with

recent annual amounts Expenses

Excluding 4Q13 branch optimization costs, expenses expected to decline linked

quarter as year-end incentive expenses are normalized

Measured investments in the franchise continue

Fee Income

Expected to increase slightly compared to 4Q13, excluding gain on sale of branch

properties Seasonal factors and continued success of fee income activities

should drive modest growth |

Valuation and Long Term Upside

28 |

Price / Tangible Book Value

Price

/

Forward

Earnings

(2014)

2

Dividend

Yield

1

Price / Book Value

Valuation

29

Execution of strategy could result in P/E expansion due to higher earnings growth

and lower cost of equity –

Close the P/E discount to peers

Attractive dividend yield provides meaningful return in the near-term

Source:

SNL

Financial.

As

of

January

31,

2014.

Please

refer

to

the

“Quarterly

Financial

Supplement”

slides

at

the

conclusion

of

this

presentation

for

the

listing

of

the

peer

companies.

1

Based

on

current

annualized

dividend

of

$0.32

per

share

and

closing

price

on

January

31,

2014.

2

Reflects

mean

IBES

estimate

for

2014.

1

2 |

At

December 31, 2013 Tangible

Common

Equity

1

Tier 1

Common /

RWA

Tier 1

Leverage

Tier 1

Risk-Based

Total

Risk-Based

Susquehanna

8.44%

10.59%

9.54%

11.70%

13.03%

Management Minimum

Target

7.50%

8.00%

6.00%

9.50%

11.50%

Solid Capital Generation

30

1

The

tangible

common

equity

ratio

is

a

non-GAAP

based

financial

measure;

please

refer

to

the

“Quarterly

Financial

Supplement”

slides

at

the

conclusion

of

this

presentation

for

calculation.

Do not expect Basel III to have a material impact to our risk-weighted

assets –

We believe we would be fully compliant with revised capital requirements, including

the capital conservation buffer Capital generation has benefited from strong

profitability and approximately 35% dividend payout ratio Status quo until

stress test results are submitted and we receive feedback from regulators

–

If deemed to have capital beyond what is required by regulators and internal

capital targets, Susquehanna may look to distribute a portion of its excess

capital –

All capital distribution strategies will be evaluated

|

Quarterly Financial Supplement

31 |

Susquehanna Bank Markets

Pennsylvania Market

Maryland Market

Delaware Valley Market

Adams, PA

Berks, PA

Centre, PA

Cumberland, PA

Dauphin, PA

Lancaster, PA

Lebanon, PA

Lehigh, PA

Luzerne, PA

Lycoming, PA

Northampton, PA

Northumberland, PA

Schuylkill, PA

Snyder, PA

Union, PA

York, PA

Allegany, MD

Anne Arundel, MD

Baltimore, MD

Baltimore City, MD

Bedford, PA

Berkley, WV

Carroll, MD

Franklin, PA

Fulton, PA

Garrett, MD

Harford, MD

Howard, MD

Washington, MD

Worcester, MD

Atlantic, NJ

Bucks, PA

Burlington, NJ

Camden, NJ

Chester, PA

Cumberland, NJ

Delaware, PA

Gloucester, NJ

Montgomery, PA

Philadelphia, PA

32 |

Peer

Companies Associated Banc-Corp

IBERIABANK Corp.

BancorpSouth Inc.

MB Financial Inc.

City National Corp.

People's United Financial

Commerce Bancshares

Prosperity Bancshares Inc.

Cullen/Frost Bankers Inc.

TCF Financial Corp.

F.N.B. Corp.

UMB Financial Corp.

First Horizon Nat’l Corp.

Valley National Bancorp

FirstMerit Corp.

Webster Financial Corp.

Fulton Financial Corp.

Wintrust Financial Corp.

Hancock Holding Co.

33 |

Loan

and Lease Originations Average Balance*

4Q12

1Q13

2Q13

3Q13

4Q13

($ in Millions)

Balance

Origina-

tions

Balance

Origina-

tions

Balance

Origina-

tions

Balance

Origina-

tions

Balance

Origina-

tions

Commercial

$ 1,898

$ 226

$ 1,996

$ 224

$ 2,005

$ 221

$ 1,997

$ 166

$ 1,997

$ 189

Real Estate –

Const & Land

859

92

797

137

777

148

752

196

736

184

Real Estate –

1-4 Family Res

2,274

72

2,266

57

2,262

67

2,258

90

2,276

66

Real Estate –

Commercial

4,276

136

4,295

206

4,356

263

4,440

267

4,406

180

Real Estate –

HELOC

1,209

89

1,235

113

1,285

154

1,358

160

1,450

130

Tax-Free

430

4

427

3

420

2

402

42

418

34

Consumer Loans

810

104

820

114

853

149

887

128

908

125

Commercial Leases

289

85

287

78

300

124

319

101

320

89

Consumer Leases

512

167

644

138

698

87

756

122

837

142

VIE

168

-

162

-

156

-

122

-

74

-

Total Loans

$ 12,725

$ 975

$ 12,929

$ 1,070

$ 13,112

$ 1,215

$ 13,291

$ 1,272

$13,422

$ 1,137

34

*By collateral type. |

Loan

Mix & Yield 35

*By collateral type.

Average Balance*

($ in Millions)

4Q12

1Q13

2Q13

3Q13

4Q13

INT % QTR

Commercial

$ 1,898

5.35%

$ 1,996

5.28%

$ 2,005

5.03%

$ 1,997

5.00%

$ 1,997

4.81%

Real Estate –

Const & Land

859

5.90%

797

6.05%

777

6.69%

752

5.21%

736

5.37%

Real Estate –

1-4 Family Res

2,274

4.97%

2,266

4.91%

2,262

4.82%

2,258

4.60%

2,276

4.69%

Real Estate –

Commercial

4,276

5.51%

4,295

5.43%

4,356

5.22%

4,440

4.99%

4,406

4.65%

Real Estate –

HELOC

1,209

3.74%

1,235

3.68%

1,285

3.64%

1,358

3.59%

1,450

3.53%

Tax-Free

430

5.47%

427

5.10%

420

5.09%

402

5.07%

418

5.02%

Consumer Loans

810

4.95%

820

4.77%

853

4.52%

887

4.33%

908

4.25%

Commercial Leases

289

7.50%

287

7.56%

300

7.15%

319

6.64%

320

6.46%

Consumer Leases

512

4.11%

644

3.88%

698

3.68%

756

3.51%

837

3.39%

VIE

168

4.39%

162

4.36%

156

4.34%

122

4.92%

74

4.88%

Total Loans

$ 12,725

5.18%

$ 12,929

5.03%

$ 13,112

4.95%

$ 13,291

4.70%

$ 13,422

4.55% |

CRE

and Construction Composition 36

4Q13 |

Asset

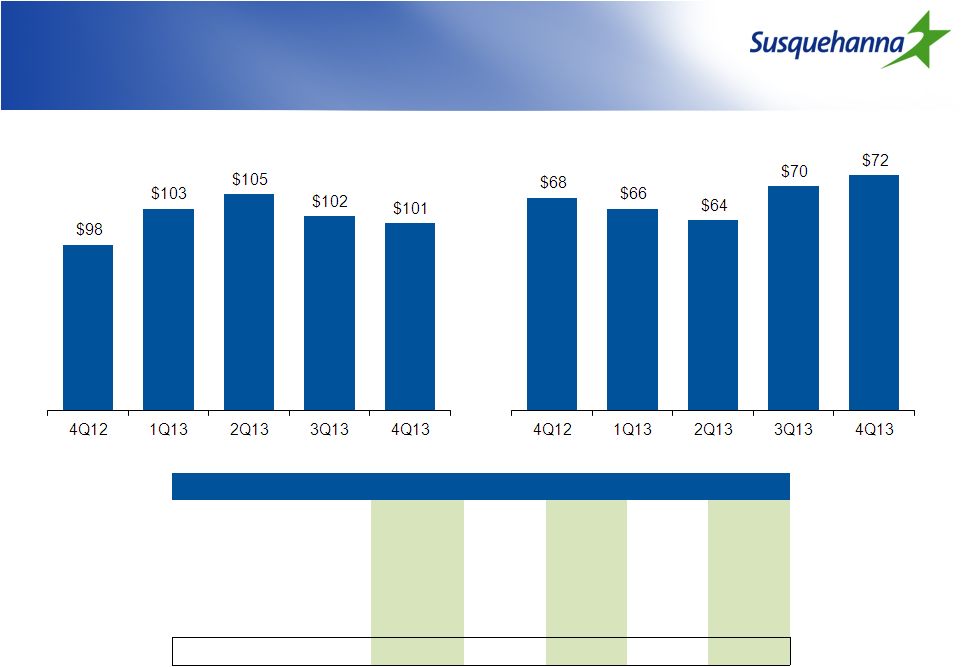

Quality 37

NPAs / Loans & leases +

Foreclosed Real Estate

Net Charge-Offs /

Average Loans & Leases

ALLL / Nonaccrual Loans and Leases

Source: SNL Financial |

TDRs

Asset Quality

($ in Millions)

38

Non Accruals

4Q12

1Q13

2Q13

3Q13

4Q13

NPL's Beginning of Period

$ 118.4

$ 97.8

$ 103.4

$ 105.1

$ 102.0

New Non Accruals

19.0

23.1

23.6

23.1

29.4

Cure/Exits/Other

(21.5)

0.4

(13.4)

(12.6)

(21.7)

Gross Charge-Offs

(15.4)

(15.5)

(5.0)

(8.9)

(5.3)

Transfer to OREO

(2.7)

(2.4)

(3.5)

(4.7)

(3.6)

NPL's End of Period

$ 97.8

$ 103.4

$ 105.1

$ 102.0

$ 100.8 |

Asset

Quality ($ in Millions)

39

Substandard

OAEM

Past Due 90 Days or More

Past Due 30-89 Days |

Investment Securities

40

EOP Balance

4Q12

1Q13

2Q13

3Q13

4Q13

($ in Millions)

QTR Yield

Total Investment Securities

$2,730

$2,553

$2,494

$2,644

$2,533

Duration (years)

3.6

3.6

4.3

4.1

3.5

Yield

2.59%

2.64%

2.61%

2.67%

2.65%

Unrealized Gain/(Loss)

$57.1

$50.6

($2.7)

$1.3

($12.0) |

Deposit Mix & Cost

41

Average Balance

4Q12

1Q13

2Q13

3Q13

4Q13

($ in Millions)

INT % QTR

Demand

$ 1,946

0.00%

$ 1,918

0.00%

$ 1,912

0.00%

$ 1,911

0.00%

$ 1,881

0.00%

Interest Bearing Demand

5,803

0.33%

5,895

0.32%

5,984

0.28%

5,937

0.26%

6,058

0.26%

Savings

1,019

0.11%

1,049

0.11%

1,080

0.11%

1,076

0.11%

1,076

0.11%

Certificates of Deposits

3,835

1.21%

3,778

1.21%

3,892

1.20%

3,871

1.05%

3,792

1.00%

Total Interest-Bearing Deposits

$ 10,657

0.62%

$ 10,722

0.61%

$ 10,956

0.59%

$ 10,884

0.53%

$ 10,926

0.50%

Non-CD Deposits/Total

69.6%

70.1%

69.8%

69.7%

70.4%

Loans(excluding VIE)/Deposits

99.6%

101.0%

100.7%

102.9%

104.2% |

Borrowing Mix & Cost

42

Average Balance

4Q12

1Q13

2Q13

3Q13

4Q13

($ in Millions)

INT % QTR

Short-Term Borrowings

$ 811

0.26%

$ 817

0.25%

$ 728

0.26%

$ 758

0.27%

$ 672

0.25%

FHLB Advances

1,167

0.36%

1,155

0.33%

1,042

0.36%

1,285

0.33%

1,502

0.32%

Long Term Debt

561

1.19%

509

3.28%

496

3.32%

476

3.45%

456

3.51%

Total Borrowings

$ 2,539

0.51%

$ 2,481

0.91%

$ 2,266

0.98%

$ 2,519

0.90%

$ 2,630

0.86%

Off Balance Sheet Swap Impact

675

0.71%

927

0.73%

927

0.82%

927

0.78%

1,100

0.80%

Total Borrowing Cost

1.22%

1.64%

1.80%

1.68%

1.66%

Total Borrowings / Total Assets

14.1%

13.8%

12.5%

13.8%

14.3% |

Non-GAAP Reconciliation

($ in thousands)

43

4Q13

3Q13

2Q13

1Q13

4Q12

2013

2012

Efficiency Ratio

Other expense

135,672

$

117,701

$

119,738

$

117,729

$

125,277

$

490,840

$

490,017

$

Less: Merger related expenses

0

0

0

0

(1,054)

0

(17,351)

Loss on extinguishment of debt

0

0

0

0

(409)

0

(5,860)

Noninterest operating expense (numerator)

135,672

$

117,701

$

119,738

$

117,729

$

123,814

$

490,840

$

466,806

$

Taxable-equivalent net interest income

146,430

$

149,683

$

151,916

$

153,021

$

159,332

$

600,945

606,530

$

Other income

50,666

41,343

49,076

42,644

43,772

183,729

166,759

Noninterest operating income (deminator)

197,096

$

191,026

$

200,992

$

195,665

$

203,104

$

784,674

$

773,289

$

Efficiency ratio

68.84%

61.62%

59.57%

60.17%

60.96%

62.55%

60.37%

Tangible

Common

Ratio

End of period balance sheet data

Shareholders' equity

2,717,587

$

2,679,348

$

2,644,940

$

2,639,489

$

2,595,909

$

2,717,587

$

2,595,909

$

Goodwill and other intangible assets

(1)

(1,264,839)

(1,263,928)

(1,265,016)

(1,266,610)

(1,263,563)

(1,264,839)

(1,263,563)

Tangible common equity (numerator)

1,452,748

$

1,415,420

$

1,379,924

$

1,372,879

$

1,332,346

$

1,452,748

$

1,332,346

$

Assets

18,473,489

$

18,481,150

$

18,083,039

$

17,967,174

$

18,037,667

$

18,473,489

$

18,037,667

$

Goodwill and other intangible assets

(1)

(1,264,839)

(1,263,928)

(1,265,016)

(1,266,610)

(1,263,563)

(1,264,839)

(1,263,563)

Tangible assets (denominator)

17,208,650

$

17,217,222

$

16,818,023

$

16,700,564

$

16,774,104

$

17,208,650

$

16,774,104

$

Tangible common ratio

8.44%

8.22%

8.21%

8.22%

7.94%

8.44%

7.94%

(1)

Net of applicable deferred income taxes

12 Months Ended

December 31,

The efficiency ratio is a non-GAAP based financial measure. Management

excludes merger-related expenses and certain other selected items when

calculating this ratio, which is used to measure the relationship of operating expenses to revenues.

The tangible common ratio is a non-GAAP based financial measure using

non-GAAP based amounts. The most directly comparable GAAP-based

measure

is

the

ratio

of

common

shareholders’

equity

to

total

assets.

In

order

to

calculate

tangible

common

shareholders

equity

and

assets,

our

Management

subtracts

the

intangible

assets

from

both

the

common

shareholders’

equity

and

total

assts.

Tangible

common

equity

is

then

divided

by

the

tangible

assets

to

arrive

at

the

ratio.

Management

uses

the

ratio

to

assess

the

strength

of

our

capital

position. |

Non-GAAP Reconciliation

($ in thousands)

44

4Q13

3Q13

2Q13

1Q13

4Q12

2013

2012

Return on Average Tangible Equity

Income statement data

Net income

41,341

$

44,291

$

45,648

$

42,399

$

43,174

$

173,679

$

141,172

$

Amortization of intangibles, net of taxes at 35%

1,822

1,626

1,984

2,124

2,127

7,557

8,141

Net tangible income (numerator)

43,163

$

45,917

$

47,632

$

44,523

$

45,301

$

181,236

$

149,313

$

Average balance sheet data

Shareholders' equity

2,679,242

$

2,642,806

$

2,648,314

$

2,614,319

$

2,597,254

$

2,646,339

$

2,511,604

$

Goodwill and other intangible assets

(1,308,690)

(1,310,155)

(1,312,257)

(1,312,662)

(1,311,192)

(1,310,928)

(1,270,053)

Tangible common equity (denominator)

1,370,552

$

1,332,651

$

1,336,057

$

1,301,657

$

1,286,062

$

1,335,411

$

1,241,551

$

Return on equity (GAAP basis)

6.12%

6.65%

6.91%

6.58%

6.61%

6.56%

5.62%

Effect of goodwill and other intangibles

6.37%

7.02%

7.39%

7.29%

7.40%

7.01%

6.41%

Return on average tangible equity

12.49%

13.67%

14.30%

13.87%

14.01%

13.57%

12.03%

Tangible Book Value per Common Share

End of period balance sheet data

Shareholders' equity

2,717,587

$

2,679,348

$

2,644,940

$

2,639,489

$

2,595,909

$

2,717,587

$

2,595,909

$

Goodwill and other intangible assets

(1,307,701)

(1,309,105)

(1,311,176)

(1,313,648)

(1,311,691)

(1,307,701)

(1,311,691)

Tangible common equity (numerator)

1,409,886

$

1,370,243

$

1,333,764

$

1,325,841

$

1,284,218

$

1,409,886

$

1,284,218

$

Common shares outstanding (denominator)

187,363

187,225

187,023

186,800

186,554

187,363

186,554

Tangible book value per common share

7.52

$

7.32

$

7.13

$

7.10

$

6.88

$

7.52

$

6.88

$

Tangible book value per share is a non-GAAP based financial measure calculated

using non-GAAP based amounts. The most directly comparable GAAP

based measure is book value per share. In order to calculate tangible book value per share, we divide tangible common equity, which is a

non-GAAP based measure calculated as common shareholders’

equity less intangible assets, by the number of shares of common stock

outstanding. In contrast, book value per share is calculated by

dividing total common shareholders’

equity by the number of shares of common

stock outstanding. Management uses tangible book value per share to assess our

capital position and ratios. 12 Months Ended

December 31,

Return on average tangible equity is a non-GAAP based financial measure

calculated using non-GAAP based amounts. The most directly

comparable GAAP-based measure is return on average equity. We calculate

return on average tangible equity by excluding the balance of intangible

assets and their related amortization expense from our calculation of return on average equity. Management uses the return on average

tangible equity in order to review our core operating results. Management

believes that this is a better measure of our performance. In addition, this

is consistent with the treatment by bank regulatory agencies, which excludes

goodwill and other intangible assets from the calculation of risk-based

capital ratios. |

Non-GAAP Reconciliation

45

4Q13

3Q13

2Q13

1Q13

4Q12

2013

2012

Net Interest Margin (excluding purchase

accounting)

Reported net interest margin (GAAP basis)

3.60%

3.72%

3.88%

3.97%

4.06%

3.79%

4.01%

Adjustments for purchase accounting:

Loans and leases

-0.11%

-0.13%

-0.27%

-0.27%

-0.23%

-0.20%

-0.17%

Deposits

-0.03%

-0.04%

-0.06%

-0.07%

-0.08%

-0.05%

-0.11%

Borrowings

-0.01%

-0.01%

-0.01%

-0.01%

-0.09%

-0.01%

-0.04%

Net Interest Margin (excluding

purchase accounting)

3.45%

3.54%

3.54%

3.62%

3.66%

3.53%

3.69%

Twelve Months Ended

December 31,

Net interest margin (excluding purchase accounting) is a non-GAAP based

financial measure using non-GAAP based amounts. The most directly

comparable GAAP based measure is net interest margin. In order to calculate net interest margin (excluding purchase

accounting) we subtract the effects of amortizing/accreting purchase accounting

valuation amounts from net interest income, and divide the remainder by

average earning assets. Our management uses net interest margin (excluding purchase accounting) to measure and

monitor the impact of the current economic environment on our net interest income

and believes that this measure is more representative of our ongoing

earnings power because it excludes the effect of valuation variables used to arrive at the acquisition fair value

recorded on

the acquisition date. We believe this non-GAAP measure, when taken

together with the corresponding GAAP measure, provides meaningful

supplemental information to investors regarding our performance. However, this non-GAAP measure should be considered in

addition to, and not as a substitute for or preferable to, net interest margin

prepared in accordance with GAAP. |