Attached files

| file | filename |

|---|---|

| 8-K - 8-K - POPULAR, INC. | d659952d8k.htm |

Financial Results

Financial Results

Fourth Quarter 2013

Fourth Quarter 2013

Exhibit 99.1 |

The

information

contained

in

this

presentation

includes

forward-looking

statements

within

the

meaning

of

the

Private

Securities

Litigation

Reform

Act

of

1995.

These

forward-looking

statements

are

based

on

management’s

current

expectations

and

involve

risks

and

uncertainties

that

may

cause

the

Company's

actual

results

to

differ

materially

from

any

future

results

expressed

or

implied

by

such

forward-looking

statements.

Factors

that

may

cause

such

a

difference

include,

but

are

not

limited

to

(i)

the

rate

of

growth

in

the

economy

and

employment

levels,

as

well

as

general

business

and

economic

conditions;

(ii)

changes

in

interest

rates,

as

well

as

the

magnitude

of

such

changes;

(iii)

the

fiscal

and

monetary

policies

of

the

federal

government

and

its

agencies;

(iv)

changes

in

federal

bank

regulatory

and

supervisory

policies,

including

required

levels

of

capital;

(v)

the

relative

strength

or

weakness

of

the

consumer

and

commercial

credit

sectors

and

of

the

real

estate

markets

in

Puerto

Rico

and

the

other

markets

in

which

borrowers

are

located;

(vi)

the

performance

of

the

stock

and

bond

markets;

(vii)

competition

in

the

financial

services

industry;

(viii)

possible

legislative,

tax

or

regulatory

changes;

(ix)

the

impact

of

the

Dodd-Frank

Act

on

our

businesses,

business

practice

and

cost

of

operations;

and

(x)

additional

Federal

Deposit

Insurance

Corporation

assessments.

Other

than

to

the

extent

required

by

applicable

law,

the

Company

undertakes

no

obligation

to

publicly

update

or

revise

any

forward-looking

statement.

Please

refer

to

our

Annual

Report

on

Form

10-K

for

the

year

ended

December

31,

2012

and

other

SEC

reports

for

a

discussion

of

those

factors

that

could

impact

our

future

results.

The

financial

information

included

in

this

presentation

for

the

quarter

ended

December

31,

2013

is

based

on

preliminary

unaudited

data

and

is

subject

to

change.

1

Forward Looking Statements |

2013

Full Year Highlights 2

Credit

EVTC

•

Current stake of 14.9% with a market value of approximately $300

million (January 2014) and book value of $19.9 million as of

December 31, 2013

•

Popular recognized an after tax gain of $424 million during 2013

which generated approximately $585 million in cash to the holding

company

•

$1.1 billion in NPAs sold in 2013

•

Continued improvement across key metrics, reaching new lows in the

cycle and returning to pre-crisis levels

NPAs/Total Assets declined to 2.6% from a peak of 7.2% in Q1 2010

NPL inflows down $492 million or 42% YoY; down 85% from peak levels in

Q2 2009

NCO ratio was 1.19% compared to 1.97% last year

Earnings

•

Reported annual net income of $599.3 million

•

Adjusted net income of $256.2 million*

* See appendix for non-GAAP to GAAP reconciliation |

Total

Deposits (Net of Brokered) 1

39%

Total Loans

1

35%

Commercial & Construction Loans

1

38%

Credit Cards

1

51%

Mortgage Loan Production

1

32%

Personal Loans

1

30%

Auto Loans/Leases

3

26%

Assets Under Management

3

14%

Category

Market Position

as of Q3 2013

Market Share

as of Q3 2013

Market Leadership in Puerto Rico

Popular’s Market Share Trend

Puerto Rico Market Share by Category

Source:

Puerto

Rico

Office

of

the

Commissioner

of

Financial

Institutions

&

10K

reports;

Mortgage

origination

data

is

not

publicly

available;

Figures

presented

for

BPPR

and

competitors

were

provided

internally;

Personal

Loans:

As

a

group,

Credit

Unions

represent

the

largest

competitor

with

52%

market

share

(115

Credit

Unions

were

in

business

as

of

December

31,

2012

guaranteed

by

COSSEC)

3 |

Q4

2013 Highlights 4

Credit

EVTC

•

Popular recognized an after tax gain of $99 million during the

quarter which generated approximately $118 million in cash to the

holding company

•

NPAs declined by $21.7 million

QoQ improvement was driven by commercial, legacy and construction

NPLs, in part offset by higher mortgage NPLs in the PR segment

•

Total NPL inflows decreased by $20.5 million, or 12.6% QoQ

•

NCOs for Q4 2013 are down by $22.5 million or 38.9% QoQ

NCO ratio stands at 0.66%, lowest level since Q2 2006

Earnings

•

Reported net income of $163 million

•

Adjusted net income of $74.6 million*

•

Strong margins: Popular, Inc. 4.74%, BPPR 5.59%

*See appendix for non-GAAP to GAAP reconciliation |

TARP

& Capital 5

•

Submitted an application to repay TARP in full; subject to regulatory

approval •

Robust capital (Tier1 Common Equity ratio of 15.0%), $2.3 billion in excess of 5%

CCAR target

Common Tier 1 Capital

5.0%

15.0%

13.2%

Tier 1 Capital

6.0%

19.4%

15.3%

Total Capital

10.0%

20.7%

16.6%

Leverage

5.0%

12.9%

10.1%

Minimum

Well

Capitalized

Ratio

12/31/2013

Pro-forma

12/31/2013

Excl. TARP |

Q4

2013 Q3 2013

See appendix for Non-GAAP to GAAP reconciliation

Non GAAP

Non GAAP

In thousands

Adjusted

Adjusted

Net interest income

$376,342

$354,206

$22,136

Non Interest Income

135,996

130,958

5,038

Total revenues before FDIC loss share impact

512,338

485,164

27,174

FDIC loss-share income (expense)

(37,164)

(14,866)

(22,298)

Gross revenues

475,174

470,298

4,876

Provision for loan losses (excluding covered loans)

47,729

55,230

(7,501)

Provision for loan losses (covered loans)

8,907

17,433

(8,526)

Total provision for loan losses

56,636

72,663

(16,027)

Net revenues

418,538

397,635

20,903

Personnel costs

114,360

116,839

(2,479)

Other real estate owned (OREO) expenses

10,558

17,175

(6,617)

Other operating expenses

197,785

192,335

5,450

Total operating expenses

322,703

326,349

(3,646)

Income before tax

95,835

71,286

24,549

Income tax expense

21,217

9,979

11,238

Net income

$74,618

$61,307

$13,311

Adjusted

Variance

Financial Summary (unaudited)

6 |

Capital

7

Capital Ratios %

Excess Capital ($ in billions)

**Excess

capital

over

“well

capitalized”

Basel

I

threshold

*Averages

for

30

bank

holding

Companies

with

$50

billion

or

more

of

total

consolidated

assets,

consisting

of

19

firms

included

in

Comprehensive

Capital

Analysis

and

Review

(CCAR)

and

11

firms

included

in

Capital

Plan

Review

(CapPR).

•

Tier 1 Common Equity capital ratio of 15.0% exceeds current CCAR

5% target by $2.3

billion

•

We

expect

to

remain

“well-capitalized”

under

Basel

III

rules

issued

by

the

Federal

Reserve |

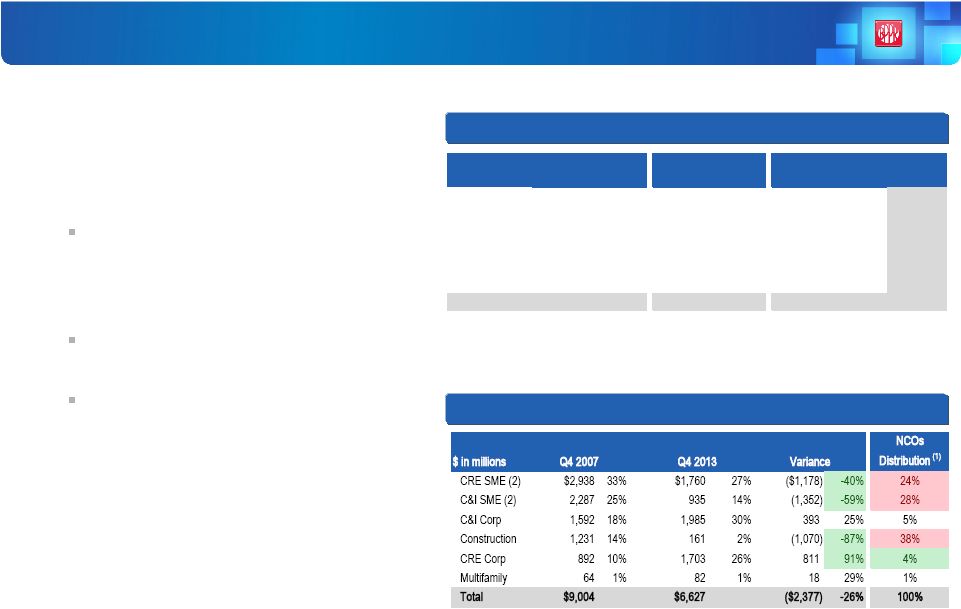

De-risked Loan Portfolios

•

PR has derisked its commercial loan

portfolio by reducing its exposure in

asset classes with historically high loss

content

Commercial portfolio, including

construction, has decreased from

55% of total loans held-in-portfolio

to 42%

Construction portfolio is down by

87% since Q4 2007

SME

(2)

lending is down by 48% from

Q4 2007

•

Collateralized exposure now represents

a larger portion of consumer loan

portfolio

•

Unsecured loans credit quality has

improved as overall FICO scores have

increased

Loan Composition (Held-in Portfolio)

PR Commercial and Construction Portfolio Distribution

8

(1) NCOs distribution represents the percentage allocation of NCOs from

Q1 2008 through Q3 2013 per each loan category. (2) Small and Medium

Enterprise Legacy portfolio is comprised of certain commercial, construction

and lease financings lending products exited by the US. $ in

millions Q4 2007

Q4 2013

Q4 2007

Q4 2013

Q4 2007

Q4 2013

Variance

Commercial

$7,774

$6,465

$4,515

$3,571

$12,288

$10,036

($2,252)

Consumer

3,552

3,317

1,698

1,281

5,249

4,598

(651)

Mortgage

2,933

5,401

3,139

616

6,071

6,017

(54)

Construction

1,231

161

237

45

1,468

206

(1,262)

Leases

814

544

-

-

814

544

(270)

Legacy

-

2,130

211

2,130

211

(1,919)

Total

$16,304

$15,888

$11,718

$5,724

$28,021

$21,612

($6,409)

Puerto Rico

US

Total |

$618

$770

$858

$1,008

$771

$781

$923

$1,028

$1,203

$1,404

$1,978

$2,116

$2,276

$2,313

$2,330

$2,344

$1,572

$1,614

$1,625

$1,732

$1,738

$1,682

$1,563

$1,550

$1,425

$1,051

$614

$618

$598

2.4%

2.7%

3.1%

2.8%

2.9%

3.5%

3.9%

4.7%

5.6%

8.0%

8.7%

9.6%

10.0%

10.4%

10.6%

7.6%

7.9%

7.9%

8.4%

8.4%

8.2%

7.6%

7.5%

6.8%

4.9%

2.9%

2.9%

2.8%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0

12.0

14.0

1Q 07

2Q 07

3Q 07

4Q 07

1Q 08

2Q 08

3Q 08

4Q 08

1Q 09

2Q 09

3Q 09

4Q 09

1Q 10

2Q 10

3Q 10

4Q 10

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

Q4 12

Q1 13

Q2 13

Q3 13

Q4 13

Mortgage

Commercial & Construction

Other

NPL/Loans (HIP)

$944

$859

$971

$1,142

$852

$866

$1,026

$1,101

$1,293

$1,500

$2,084

$2,245

$2,402

$2,448

$2,539

$2,623

$2,489

$2,314

$2,277

$2,254

$2,365

$2,311

$2,178

$2,120

$2,002

$1,419

$992

$944

$922

1.8%

2.1%

2.4%

1.9%

2.1%

2.5%

2.7%

3.3%

4.0%

5.7%

6.3%

6.9%

7.2%

6.0%

6.4%

6.4%

6.0%

5.8%

5.9%

6.3%

6.2%

5.9%

5.8%

5.5%

3.8%

2.7%

2.6%

2.6%

1Q 07

2Q 07

3Q 07

4Q 07

1Q 08

2Q 08

3Q 08

4Q 08

1Q 09

2Q 09

3Q 09

4Q 09

1Q 10

2Q 10

3Q 10

4Q 10

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

Q4 12

Q1 13

Q2 13

Q3 13

Q4 13

NPLs

OREO

NPL HFS

NPAs/Total Assets

Steady Improvements in Non Performing Assets

•

Non-performing loans held-in-portfolio declined by

$19.6 million, or 3.2%, QoQ and by $827 million, or

58% YoY

•

NPL to loans stands at 2.8% compared to 2.9% in Q3

2013, and at the same level in Q4 2007

•

QoQ improvement was driven by commercial, legacy

and construction NPLs, in part offset by higher

mortgage NPLs in the PR segment

Non-Performing Loans HIP ($MM)

9

Non-Performing Assets ($MM)

Metrics exclude covered loans

•

Non-performing assets declined by $21.7 million,

or 2.3%, QoQ and $1.1 billion, or 54%, YoY

•

Steady improvements following NPA bulk sales

completed

during the first half of 2013 |

Total NPL Inflows ($MM)

NPL Inflows Continued Trending Down

•

Total NPL inflows decreased by $21 million, or

13% QoQ, and $492 million or 42% YoY; down

85% from peak levels in Q2 2009

•

Commercial, construction and legacy NPL inflows

reached new record low, decreasing by $22

million or 34% QoQ

•

Mortgage NPLs remained flat in both regions QoQ

Mortgage NPL Inflows ($MM)

Commercial, Construction & Legacy NPL Inflows ($MM)

10

Excludes consumer loans

Metrics exclude covered loans

$67

$92

$87

$84

$55

$51

$52

$34

$26

$29

$27

$16

$271

$273

$397

$333

$279

$231

$257

$210

$158

$158

$136

$126

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

Q4 12

Q1 13

Q2 13

Q3 13

Q4 13

US Inflows

PR Inflows

$9

$13

$10

$8

$6

$6

$10

$8

$5

$7

$5

$6

$140

$154

$175

$232

$187

$166

$157

$167

$110

$99

$94

$94

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

Q4 12

Q1 13

Q2 13

Q3 13

Q4 13

US Inflows

PR Inflows

$58

$79

$77

$76

$48

$45

$42

$26

$22

$22

$22

$10

$131

$119

$222

$101

$93

$65

$100

$43

$48

$59

$42

$32

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

Q4 12

Q1 13

Q2 13

Q3 13

Q4 13

US Inflows

PR Inflows |

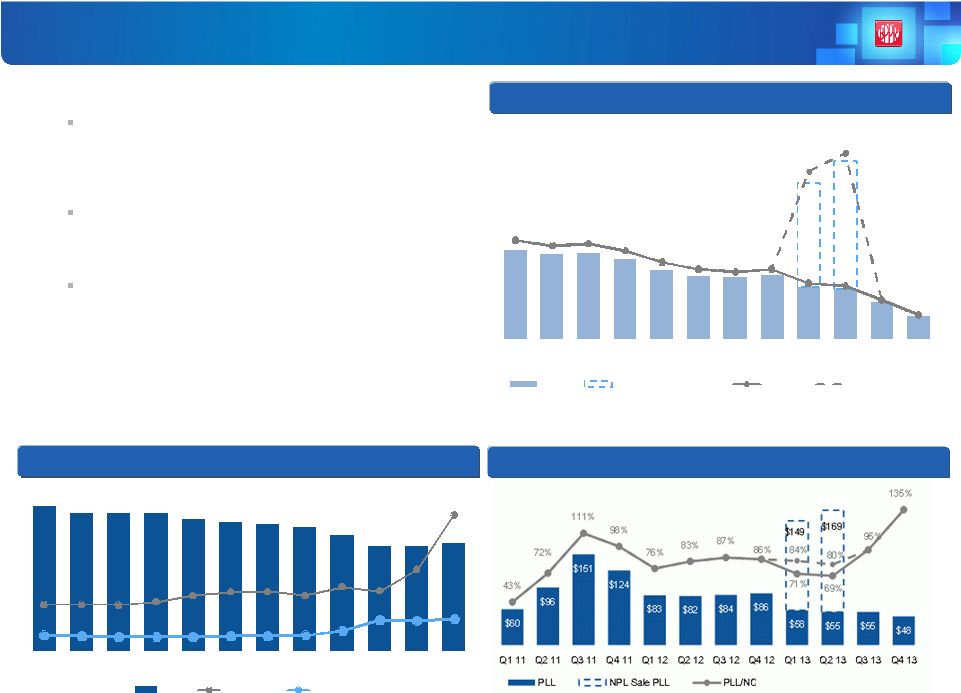

Continued Progress in Asset Quality

•

NCOs for Q4 2013 are down by $23 million or 39% QoQ

Recoveries up by $17 million driven by:

–

$9 million recovery related to the sale of previously

charged-off PR credit cards and personal loans

–

Higher commercial recoveries of $6 million

NCO ratio of 0.66%, lowest level since Q2 2006

Provision to NCO of 135%, compared to 95% in Q3

2013

•

ALLL to loans stands at 2.49% compared to 2.46% on Q3

2013

•

ALLL to NPL coverage ratio continued improving, standing

at 90% compared to 44% in Q4 2012, primarily driven by

the bulk sales in the first half of the year

ALLL ($MM), ALLL-to-NCO and ALLL-to-NPL Ratios

NCO ($MM) and NCO-to-HIP Loan Ratio

Provision ($MM) and Provision-to-NCO Ratio

11

Metrics exclude covered loans

$139

$133

$135

$126

$108

$98

$96

$101

$81

$79

$58

$35

$163

$200

2.74%

2.59%

2.64%

2.46%

2.13%

1.93%

1.87%

1.94%

1.55%

1.47%

1.08%

0.66%

4.66%

5.16%

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

Q4 12

Q1 13

Q2 13

Q3 13

Q4 13

NCO

NPL Sale Charge-offs

NCO%

NPL Sale NCO%

$727

$690

$693

$690

$665

$649

$636

$622

$584

$529

$526

$538

130%

129%

128%

137%

154%

165%

166%

154%

179%

167%

227%

381%

44%

42%

40%

40%

40%

41%

41%

44%

56%

86%

85%

90%

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

Q4 12

Q1 13

Q2 13

Q3 13

Q4 13

ALLL

ALLL/NCO

ALLL/NPL

•

Provision totaled $48 million, down by $8 million or 14%

vs. Q3 2013; |

PR

Public Sector Exposure •

Loans to the Government of Puerto Rico and Public Corporations

are either collateralized loans or obligations that have a specific

source of income or revenues identified for their repayment

12

•

Loans to various municipalities backed by unlimited taxing power

or

real and personal property taxes collected within such municipalities

•

Includes $274 million residential mortgage loans to individual

borrowers with a government guarantee

•

$52 million in PR pass-through housing bonds backed by FNMA,

GNMA or residential loan CMOs

•

$34 million of industrial development notes payable primarily by

non government tenants

•

Our

current

direct

exposure

to

the

PR

government, instrumentalities

and municipalities

is

$1.2

billion,

of which

approximately $950 million

is

outstanding

•

Of

the

amount

outstanding,

$789 million

consists

of

loans

and

$161

million

are

securities

PR

Government

$527 million

outstanding

Indirect

Exposure

$360 million

outstanding

Municipalities

$423 million

outstanding

•

Additional $360 million in indirect exposure of loans or instruments that are

payable by non-governmental entities and have a government guarantee to

cover any shortfall in collateral in the event of borrower default

|

Driving Shareholder Value

13

Capital

Earnings

Additional

Value

•

Robust

capital

with

excess

Tier

1

Common

Equity

of

$2.3

billion

and

significantly

improved

asset

quality

move

us

closer

to

TARP

exit

in

the

most

shareholder-friendly

fashion

•

Application for TARP repayment was submitted

•

Unique franchise in PR provides strong, stable revenue-generating

capacity

•

Popular’s credit metrics are now close to historical low levels

•

EVTC ownership, BHD stake and continued improvement in US

operations |

APPENDIX

APPENDIX |

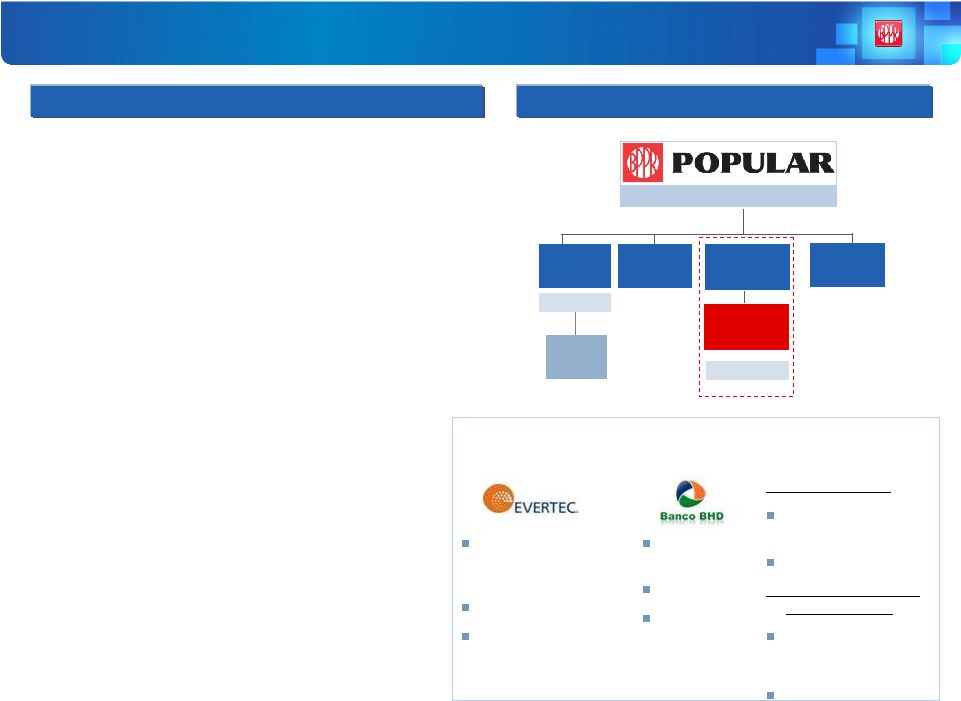

Who

We Are – Popular, Inc.

Franchise

•

Financial services company

•

Headquartered in San Juan, Puerto Rico

•

$36 billion in assets (top 50 bank holding

company in the U.S.)

•

$25 billion in total loans

•

$27 billion in total deposits

•

276 branches serving customers in Puerto

Rico, New York, California, Florida, Illinois,

U.S. Virgin Islands, and New Jersey

•

NASDAQ ticker symbol: BPOP

•

Market Cap: $2.97 billion

1

1

As of December 31, 2013

*Doing business as Popular Community Bank.

Summary Corporate Structure

Assets = $35.8 bn

Popular Auto,

Inc.

Banco Popular

de Puerto Rico

Popular

Securities, Inc.

Assets = $27 bn

Assets = $8.7bn

Banco Popular

North America*

Puerto Rico operations

Selected equity investments

(first two under “corporate”

segment and third and fourth under PR):

Popular

Insurance, Inc.

Popular North

America, Inc.

U.S. banking operations

Transaction processing,

business processes

outsourcing

14.9% stake

Adjusted EBITDA of $180.7

million for the 12-months

ended September 30, 2013;

$43.4 million for Q3 2013.

Dominican

Republic bank

19.99% stake

2012

approximate net

income $114

million

PRLP 2011 Holdings

Construction and

commercial loans vehicle

24.9% stake

PR Asset Portfolio 2013-1

International, LLC

Construction, commercial

loans and OREOs

vehicle

24.9% stake

15 |

[1] Covered loans represent loans acquired in the Westernbank FDIC-assisted

transaction that are covered under FDIC loss sharing agreements. 16

GAAP Reconciliation Q4 2013

Q4 2013

US GAAP

Non GAAP

In thousands, except per share amount

Actual

EVERTEC's

SPO

Adjusted

Net interest income

$376,342

$376,342

Non interest income

228,354

92,358

$135,996

Total revenues before FDIC loss-share impact

604,696

92,358

512,338

FDIC loss-share income (expense)

(37,164)

(37,164)

Gross revenues

567,532

92,358

475,174

Provision for loan losses (excluding covered loans)

47,729

47,729

Provision for loan losses (covered loans)

(1)

8,907

8,907

Total provision for loan losses

56,636

56,636

Net revenues

510,896

92,358

418,538

Personnel costs

114,360

114,360

OREO expenses

10,558

10,558

Other operating expenses

197,785

-

197,785

Total operating expenses

322,703

-

322,703

Income before tax

188,193

92,358

95,835

Income tax expense

25,162

3,945

21,217

Net income

$163,031

$88,413

$74,618

EPS -

Basic

$1.58

EPS -

Diluted

$1.57

NIM

4.74%

Tangible book value per share (quarter end)

$37.56

Market price (quarter end)

$28.73 |

GAAP

Reconciliation Q3 2013 17

[1] Covered loans represent loans acquired in the Westernbank FDIC-assisted

transaction that are covered under FDIC loss sharing agreements. Q3 2013

US GAAP

Non GAAP

In thousands, except per share amount

Actual

EVERTEC's

SPO

Adjusted

Net interest income

$354,206

$354,206

Non interest income

306,825

175,867

$130,958

Total revenues before FDIC loss-share impact

661,031

175,867

485,164

FDIC loss-share income (expense)

(14,866)

(14,866)

Gross revenues

646,165

175,867

470,298

Provision for loan losses (excluding covered loans)

55,230

55,230

Provision for loan losses (covered loans)

(1)

17,433

17,433

Total provision for loan losses

72,663

72,663

Net revenues

573,502

175,867

397,635

Personnel costs

116,839

116,839

OREO expenses

17,175

17,175

Other operating expenses

192,585

250

192,335

Total operating expenses

326,599

250

326,349

Income before tax

246,903

175,617

71,286

Income tax expense

17,768

7,789

9,979

Net income

$229,135

$167,828

$61,307

EPS -

Basic

$2.22

EPS -

Diluted

$2.22

NIM

4.49%

Tangible book value per share (quarter end)

$35.32

Market price (quarter end)

$26.25 |

GAAP

Reconciliation FY 2013 18

[1] Covered

loans

represent

loans

acquired

in

the

Westernbank

FDIC-assisted

transaction

that

are

covered

under

FDIC

loss

sharing

agreements.

[2]

Net

(loss)

gain

on

sale

of

loans

for

the

first

quarter

includes

$8.8

million

of

negative

valuation

adjustments

on

loans

held

for

sale

which

were

transferred

to

held-in-portfolio

subsequent

to

the

sale.

[3]

Represents

the

net

benefit

of

$215.6

million

for

the

increase

on

the

net

deferred

tax

asset

from

the

change

of

the

corporate

tax

rate

from

30%

to

39%,

$7.9

million

resulting

from

the

adjustment

in

tax

rate

for

distributions

from

EVERTEC

from

15%

to

4% |

19

Consolidated Credit Summary (Excluding Covered Loans)

1

Excluding provision for loan losses and net write-downs related to the asset

sale $ in millions

Q4 13

Q3 13

Q2 13

Q1 13

Q4 12

Loans Held in Portfolio (HIP)

$21,612

$21,427

$21,522

$21,634

$20,984

Performing HFS

109

123

180

183

258

NPL HFS

1

2

11

18

96

Total Non Covered Loans

21,722

21,552

21,713

21,835

21,338

Non-performing loans (NPLs)

$598

$618

$614

$1,051

$1,425

Commercial

$282

$320

$328

$321

$665

Construction

$24

$29

$45

$51

$43

Legacy

$15

$24

$28

$36

$41

Mortgage

$233

$203

$172

$601

$630

Consumer

$44

$42

$41

$42

$46

NPLs HIP to loans HIP

2.77%

2.88%

2.85%

4.86%

6.79%

Net charge-offs (NCOs)

$35

$58

$79

$81

$101

Commercial

$16

$21

$41

$32

$49

Construction

($2)

($5)

($2)

$0

($2)

Legacy

($5)

$2

($1)

$2

$3

Mortgage

$8

$13

$16

$20

$20

Consumer

$18

$27

$26

$27

$31

Write-downs bulk sale

$0

$0

$200

$163

$0

NCOs to average loans HIP

0.66%

1.08%

1

1.47%

1

1.55%

1.94%

Provision for loan losses (PLL)

$48

$55

1

$55

1

$58

$86

PLL to average loans HIP

0.89%

1.03%

1

1.02%

1

1.10%

1.66%

PLL to NCOs

1.35x

0.95x

1

0.69x

1

0.71x

0.86x

Allowance for loan losses (ALL)

$538

$526

$529

$584

$622

ALL to loans HIP

2.49%

2.46%

2.46%

2.70%

2.96%

ALL to NPLs HIP

90.05%

85.19%

86.14%

55.54%

43.62% |

PR

& US Business 20

1

Excludes covered loans

$ in millions (unaudited)

Q4 13

Q3 13

Variance

Q4 13

Q3 13

Variance

Net Interest Income

$331

$310

$21

$71

$73

($2)

Non Interest Income

72

91

(19)

16

17

(1)

Gross Revenues

403

401

2

87

90

(3)

Provision (non-covered)

63

51

12

(15)

5

(20)

Provision (covered)

9

17

(8)

-

-

- Provision for loan losses

72

68

4

(15)

5

(20)

Expenses

246

244

2

59

59

0

Tax Expense

25

26

(1)

0

1

(1)

Net Income

$60

$63

($3)

$43

$25

$18

NPLs (HIP) ¹

$447

$441

$6

$151

$176

($25)

NPLs (HIP + HFS) ¹

447

442

5

152

178

(26)

Loan loss reserve ¹

427

399

28

112

127

(15)

Assets

$26,883

$27,090

($207)

$8,725

$8,782

($57)

Loans (HIP)

18,871

18,739

132

5,724

5,763

(39)

Loans (HIP + HFS)

18,979

18,860

119

5,726

5,766

(40)

Deposits

20,753

20,401

352

6,027

6,042

(15)

NIM

5.59%

5.26%

0.33%

3.55%

3.66%

-0.11%

PR

US |

Popular, Inc. Credit Ratings

•

Our

senior

unsecured

ratings

have

been

gradually

improving

since

2010:

•

Moody’s:

B1

Negative Outlook (Revised October 2013)

•

Fitch:

BB-

Stable Outlook (Reaffirmed December 2013)

•

S&P:

B+

Stable Outlook (Revised December 2011)

•

October 2013: Moody’s revised outlook to negative

•

January

2013:

Fitch

raised

to

BB-

from

B+;

outlook

revised

to

stable

•

December 2012: Moody’s downgraded BPOP to B1; stable outlook assigned

•

April 2012: Moody’s placing most of the PR banks under review with the

possibility of downgrades, due to the state of the Puerto Rico economy

•

January 2012: Fitch raised BPOP’s outlook to positive

•

December

2011:

S&P

raised

its

ratings

on

BPPR

to

BB

from

BB-

and

changed

outlook

to

stable

given

revised

bank

criteria

to

regional

banks

•

July 2011: S&P raised our senior unsecured rating by one notch to B+

21 |

Financial Results

Financial Results

Fourth Quarter 2013

Fourth Quarter 2013 |