Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - FIFTH THIRD BANCORP | d660158d8k.htm |

| EX-99.1 - EX-99.1 - FIFTH THIRD BANCORP | d660158dex991.htm |

| EX-99.3 - EX-99.3 - FIFTH THIRD BANCORP | d660158dex993.htm |

| EX-99.4 - EX-99.4 - FIFTH THIRD BANCORP | d660158dex994.htm |

©

Fifth Third Bank | All Rights Reserved

4Q13 Earnings Conference Call

January 23, 2014

Please refer to earnings release dated January 23, 2014 for further

information. Exhibit 99.2 |

2

©

Fifth Third Bank | All Rights Reserved

Cautionary statement

This

report

contains

statements

that

we

believe

are

“forward-looking

statements”

within

the

meaning

of

Section

27A

of

the

Securities

Act

of

1933,

as

amended,

and

Rule

175

promulgated

thereunder,

and

Section

21E

of

the

Securities

Exchange

Act

of

1934,

as

amended,

and

Rule

3b-6

promulgated

thereunder.

These

statements

relate

to

our

financial

condition,

results

of

operations,

plans,

objectives,

future

performance

or

business.

They

usually

can

be

identified

by

the

use

of

forward-looking

language

such

as

“will

likely

result,”

“may,”

“are

expected

to,”

“is

anticipated,”

“estimate,”

“forecast,”

“projected,”

“intends

to,”

or

may

include

other

similar

words

or

phrases

such

as

“believes,”

“plans,”

“trend,”

“objective,”

“continue,”

“remain,”

or

similar

expressions,

or

future

or

conditional

verbs

such

as

“will,”

“would,”

“should,”

“could,”

“might,”

“can,”

or

similar

verbs.

You

should

not

place

undue

reliance

on

these

statements,

as

they

are

subject

to

risks

and

uncertainties,

including

but

not

limited

to

the

risk

factors

set

forth

in

our

most

recent

Annual

Report

on

Form

10-K.

When

considering

these

forward-looking

statements,

you

should

keep

in

mind

these

risks

and

uncertainties,

as

well

as

any

cautionary

statements

we

may

make.

Moreover,

you

should

treat

these

statements

as

speaking

only

as

of

the

date

they

are

made

and

based

only

on

information

then

actually

known

to

us.

There

are

a

number

of

important

factors

that

could

cause

future

results

to

differ

materially

from

historical

performance

and

these

forward-

looking

statements.

Factors

that

might

cause

such

a

difference

include,

but

are

not

limited

to:

(1)

general

economic

conditions

and

weakening

in

the

economy,

specifically

the

real

estate

market,

either

nationally

or

in

the

states

in

which

Fifth

Third,

one

or

more

acquired

entities

and/or

the

combined

company

do

business,

are

less

favorable

than

expected;

(2)

deteriorating

credit

quality;

(3)

political

developments,

wars

or

other

hostilities

may

disrupt

or

increase

volatility

in

securities

markets

or

other

economic

conditions;

(4)

changes

in

the

interest

rate

environment

reduce

interest

margins;

(5)

prepayment

speeds,

loan

origination

and

sale

volumes,

charge-offs

and

loan

loss

provisions;

(6)

Fifth

Third’s

ability

to

maintain

required

capital

levels

and

adequate

sources

of

funding

and

liquidity;

(7)

maintaining

capital

requirements

may

limit

Fifth

Third’s

operations

and

potential

growth;

(8)

changes

and

trends

in

capital

markets;

(9)

problems

encountered

by

larger

or

similar

financial

institutions

may

adversely

affect

the

banking

industry

and/or

Fifth

Third;

(10)

competitive

pressures

among

depository

institutions

increase

significantly;

(11)

effects

of

critical

accounting

policies

and

judgments;

(12)

changes

in

accounting

policies

or

procedures

as

may

be

required

by

the

Financial

Accounting

Standards

Board

(FASB)

or

other

regulatory

agencies;

(13)

legislative

or

regulatory

changes

or

actions,

or

significant

litigation,

adversely

affect

Fifth

Third,

one

or

more

acquired

entities

and/or

the

combined

company

or

the

businesses

in

which

Fifth

Third,

one

or

more

acquired

entities

and/or

the

combined

company

are

engaged,

including

the

Dodd-Frank

Wall

Street

Reform

and

Consumer

Protection

Act;

(14)

ability

to

maintain

favorable

ratings

from

rating

agencies;

(15)

fluctuation

of

Fifth

Third’s

stock

price;

(16)

ability

to

attract

and

retain

key

personnel;

(17)

ability

to

receive

dividends

from

its

subsidiaries;

(18)

potentially

dilutive

effect

of

future

acquisitions

on

current

shareholders’

ownership

of

Fifth

Third;

(19)

effects

of

accounting

or

financial

results

of

one

or

more

acquired

entities;

(20)

difficulties

from

the

separation

of

or

the

results

of

operations

of

Vantiv,

LLC;

(21)

loss

of

income

from

any

sale

or

potential

sale

of

businesses

that

could

have

an

adverse

effect

on

Fifth

Third’s

earnings

and

future

growth;

(22)

ability

to

secure

confidential

information

and

deliver

products

and

services

through

the

use

of

computer

systems

and

telecommunications

networks;

and

(23)

the

impact

of

reputational

risk

created

by

these

developments

on

such

matters

as

business

generation

and

retention,

funding

and

liquidity.

You

should

refer

to

our

periodic

and

current

reports

filed

with

the

Securities

and

Exchange

Commission,

or

“SEC,”

for

further

information

on

other

factors,

which

could

cause

actual

results

to

be

significantly

different

from

those

expressed

or

implied

by

these

forward-looking

statements. |

3

©

Fifth Third Bank | All Rights Reserved

2013: A record year

Return on avg. assets

Net charge-off ratio

Net income to common ($MM)

Generated highest level of net

income in Company’s history.

Improving profitability approaching

target for normalized environment.

Problem assets are at the lowest

levels in five years.

Tier 1 common ratio

1

Total payout ratio

ALLL / NPLs

Coverage levels more than adequate

to protect against potential losses.

Capital ratios strong and above

regulatory well-capitalized levels.

Net

payouts

to

shareholders

of

$1.3B

2

in

2013.

1

Non-GAAP measure; see Reg. G reconciliation in appendix; capital ratios

estimated; presented under current U.S. capital regulations. 2

2013 is net of the issuance of shares valued at $398MM related to the Series G

preferred stock conversion on July 1, 2013. 3

Repurchases of shares in the amount of after-tax gains on the sale of Vantiv

shares. |

4

©

Fifth Third Bank | All Rights Reserved

Net

income

available

to

common

shareholders

of

$383MM

($0.43

per

diluted

share),

vs.

$421MM

($0.47

per

share)

in

3Q13

and

$390MM

($0.43

per

share)

in

4Q12

Overall credit trends remain favorable

—

Net charge-offs of $148MM (0.67% of loans and leases)

–

Includes $43MM of charge-offs on a C&I loan restructured during the quarter

and $6MM of home equity charge-offs due to a change in policy (22 bps

combined impact) –

Excluding these items, net charge-offs declined $10MM or 4 bps from 3Q13

—

Total nonperforming assets (NPA) of $986MM including loans held-for-sale,

down $39MM, or 4%, from 3Q13; NPA ratio of 1.10% down 6 bps from 3Q13,

nonperforming loans ratio of 0.84% down 4 bps from 3Q13

–

Includes $46MM of additions due to a change in policy on home equity nonaccruals (5

bps impact to NPA ratio) Strong capital ratios

2

; sequentially reduced due to 4Q13 repurchases

—

Repurchased 32MM common shares in 4Q13; reduced average diluted share count by

12MM —

Tier 1 common ratio 9.38%

3

vs. 9.88% in 3Q13; Basel III pro forma estimate of ~9.0%

3

—

Tier 1 risk-based capital ratio 10.35%, Total risk-based capital ratio

14.07%, Leverage ratio 9.64% —

Tangible common equity ratio

3

of 8.63% excluding unrealized gains/losses; 8.69% including them

—

Book value per share of $15.85; tangible book value per share

1

of $13.00, up 5% from 4Q12

4Q13 in review

1

Assumes 35% marginal tax rate

2

Capital

ratios

estimated;

presented

under

current

U.S.

capital

regulations.

The

pro

forma

Basel

III

Tier

I

common

equity

ratio

is

management’s

estimate

based

upon

its

current

interpretation

of

recent

prospective

regulatory

capital

requirements

approved

in

July

2013.

3

Non-GAAP measure; see Reg. G reconciliation in appendix.

Significant items in 4Q13 results

$ in MM, except per share data

Net income impact

After tax EPS

impact

Pre-tax

After tax

1

Valuation adjustment on Vantiv warrant

$91

$59

Mortgage repurchase provision benefit

$28

$18

Vantiv tax receivable agreement

$9

$6

Contribution to Fifth Third Foundation

($8)

($5)

Severance expense

($8)

($5)

TruPS debt extinguishment

($8)

($5)

Valuation adjustment on Visa total return swap

($18)

($12)

Expense to increase litigation reserves

($69)

($45)

Total

$17

$11

~$0.01 |

5

©

Fifth Third Bank | All Rights Reserved

Financial summary

•

Strong returns, with sequential growth in NII and certain fee income categories as

well as ongoing disciplined expense management

•

4Q13 included $19MM, or $0.02 per diluted share, of dividends on

preferred stock

Actual

Seq.

YOY

($ in millions)

4Q12

3Q13

4Q13

$

%

$

%

Average Balances

Total loans & leases1

$83,943

$87,272

$87,895

$623

1%

$3,952

5%

Core deposits

$84,289

$86,921

$89,269

$2,348

3%

$4,980

6%

Income Statement Data

Net interest income (taxable equivalent) (NII)

$903

$898

$905

$7

1%

$2

-

Provision for loan and lease losses

76

51

53

2

5%

(23)

(30%)

Noninterest income

880

721

703

(18)

(2%)

(177)

(20%)

Noninterest expense

1,163

959

989

30

3%

(174)

(15%)

Net income attributable to Bancorp

$399

$421

$402

($19)

(4%)

3

1%

Net income available to common shareholders

$390

$421

$383

($38)

(9%)

($7)

(2%)

Financial Ratios

Earnings per share, diluted

0.43

0.47

0.43

($0.04)

(9%)

-

-

Net interest margin

3.49%

3.31%

3.21%

(10bps)

(3%)

(28bps)

(8%)

Efficiency ratio

65.2%

59.2%

61.5%

230bps

4%

(370bps)

(6%)

Return on average assets

1.33%

1.35%

1.24%

(11bps)

(8%)

(9bps)

(7%)

Return on average common equity

11.5%

12.1%

10.8%

(130bps)

(10%)

(70bps)

(6%)

Return on average tangible common equity2

14.1%

14.7%

13.1%

(160bps)

(11%)

(100bps)

(7%)

Note: Numbers may not sum due to rounding and percentages in all of the tables in

this presentation are calculated on actual dollar amounts not the rounded dollar amounts.

1

Excludes loans held-for-sale

2

Non-GAAP measure; see Reg. G reconciliation in appendix.

|

6

©

Fifth Third Bank | All Rights Reserved

Net interest income

NII and NIM (FTE)

•

Net interest income up $7MM from 3Q13 and $2MM from 4Q12

–

Sequential increase due to higher balances and yields in investment securities,

higher portfolio loan balances, and the benefit from high-priced CD

maturities partially offset by the effects of loan repricing, lower held-for-

sale loan balances, and higher interest expense.

–

Year-over-year increase due to lower asset yields partially offset by higher

average loan balances, lower long- term debt expense, and run-off in

higher-priced CDs. •

NIM declined 10 bps sequentially largely due to higher cash balances driven by strong

deposit growth as well as the impact of the debt issuances during the quarter.

Otherwise, the benefit from the maturity of high-priced CDs and higher

securities yields offset the impact of lower loan yields. Yield Analysis

4Q12

3Q13

4Q13

Seq.

(bps)

YoY

(bps)

Commercial and industrial loans

4.01%

3.49%

3.46%

(3)

(55)

Commercial mortgage loans

3.69%

3.60%

3.53%

(7)

(16)

Commercial construction loans

3.01%

3.71%

3.46%

(25)

45

Commercial leases

3.42%

3.22%

3.10%

(12)

(32)

Residential mortgage loans

3.94%

3.87%

3.88%

1

(6)

Home equity

3.72%

3.74%

3.62%

(12)

(10)

Automobile loans

3.46%

3.02%

2.96%

(6)

(50)

Credit card

9.96%

9.93%

9.90%

(3)

(6)

Other consumer loans and leases

50.06%

42.84%

43.19%

35

(687)

Total loans and leases

4.13%

3.83%

3.79%

(4)

(34)

Taxable securities

3.23%

3.20%

3.32%

12

9

Tax exempt securities

2.91%

5.08%

5.65%

57

274

Other short-term investments

0.28%

0.26%

0.26%

-

(2)

Total interest-earning assets

3.94%

3.68%

3.57%

(11)

(37)

Total interest-bearing liabilities

0.65%

0.54%

0.52%

(2)

(13)

Net interest spread

3.29%

3.14%

3.05%

(9)

(24) |

7

©

Fifth Third Bank | All Rights Reserved

Balance sheet

•

Average C&I loans up 2% sequentially and 13% from 4Q12

•

Period end CRE loans up 2% sequentially;

first quarter of sequential CRE growth since 2Q08

•

End of period commercial line utilization 29%;

potential source of future growth

•

Average consumer loans flat sequentially and

up 1% year-over-year

•

Lower production reduced average warehoused

residential mortgage loans held-for-sale to $934MM in

4Q13 versus $1.8B in 3Q13

•

Core deposit to loan ratio of 102%

–

DDAs flat sequentially and up 5% from 4Q12

–

Consumer average transaction deposits up 1%

sequentially and up 4% year-over-year

–

Commercial average transaction deposits up 6%

sequentially and up 10% year-over-year

•

Short-term wholesale borrowings represent <3% of total

funding

Note: Numbers may not sum due to rounding.

1

Excludes loans held-for-sale

Average loan growth ($B)

1

Average core deposit growth ($B) |

8

©

Fifth Third Bank | All Rights Reserved

Noninterest income

Noninterest income

Note: Numbers may not sum due to rounding.

1

Net

credit-related

costs

recognized

in

other

noninterest

income

were

$5MM

in

4Q13,

reflecting

$6MM

of

losses

on

OREO,

$2MM

of

fair

value

charges

on

commercial

loans

HFS,

and

$2MM

of

mortgage

repurchase

benefits.

This

compares

with

net

credit-related

costs

of

$5MM

in

3Q13

and

$13MM

in

4Q12.

•

4Q13 fee income included sequential growth in mortgage banking net revenue, card and

processing revenue, service charges on deposits, and investment advisory

revenue, partially offset by lower other noninterest income and corporate

banking revenue. •

4Q13 other noninterest income included a $91MM positive valuation adjustment on the

Vantiv warrant, $9MM in payments received pursuant to Fifth Third’s tax

receivable agreement with Vantiv, and an $18MM negative valuation on the Visa

total return swap. –

3Q13 other noninterest income included $89MM of net gains on significant items,

listed on page 10. •

Growth in service charges on deposits due to deeper customer relationships across

consumer and commercial platforms

Actual

Seq.

YOY

4Q12

3Q13

4Q13

$

%

$

%

($ in millions)

Service charges on deposits

$134

$140

$142

$2

1%

$8

6%

Corporate banking revenue

114

102

94

(8)

(8%)

(20)

(18%)

Mortgage banking net revenue

258

121

126

5

4%

(132)

(51%)

Investment advisory revenue

93

97

98

1

2%

5

6%

Card and processing revenue

66

69

71

2

3%

5

8%

Other noninterest income

1

215

185

170

(15)

(7%)

(45)

(21%)

Securities gains, net

2

2

2

-

(36%)

-

(23%)

Securities gains (losses), net -

(2)

5

-

(5)

(100%)

2

100%

non-qualifying hedges on MSRs

Total noninterest income

$880

$721

$703

($18)

(2%)

($177)

(20%)

|

9

©

Fifth Third Bank | All Rights Reserved

Noninterest expense

Noninterest expense

•

4Q13 results included $69MM in charges to increase litigation reserves, $8MM of debt

extinguishment costs related to TruPS,

$8MM

contribution

to

the

Fifth

Third

Foundation,

and

$8MM

in

severance

expense.

Results

also

included

a

$26MM

benefit

to

the

mortgage

repurchase

provision.

•

3Q13 results included $30MM in charges to increase litigation reserves, $5MM in

severance expense, $5MM in large bank assessment fees, and a $4MM seasonal

pension settlement charge. Results also included a $4MM benefit to the

mortgage repurchase provision.

•

Credit costs recorded in noninterest expense:

Note: Numbers may not sum due to rounding.

Actual

($ in millions)

4Q12

3Q13

4Q13

Mortgage repurchase expense

$44

($4)

($26)

Provision for unfunded commitments

3

1

(5)

Derivative valuation adjustments

(2)

-

(2)

OREO expense

5

5

4

Other problem asset related expenses

19

14

17

Total credit-related operating expenses

$68

$16

($12)

Actual

Seq.

YOY

4Q12

3Q13

4Q13

$

%

$

%

($ in millions)

Salaries, wages and incentives

$416

$389

$388

($1)

-

($28)

(7%)

Employee benefits

96

83

78

(5)

(6%)

(18)

(19%)

Net occupancy expense

76

75

77

2

2%

1

1%

Technology and communications

52

52

53

1

2%

1

2%

Equipment expense

27

29

29

-

-

2

8%

Card and processing expense

31

33

37

4

13%

6

18%

Other noninterest expense

465

298

327

29

10%

(138)

(30%)

Total noninterest expense

$1,163

$959

$989

$30

3%

($174)

(15%)

|

10

©

Fifth Third Bank | All Rights Reserved

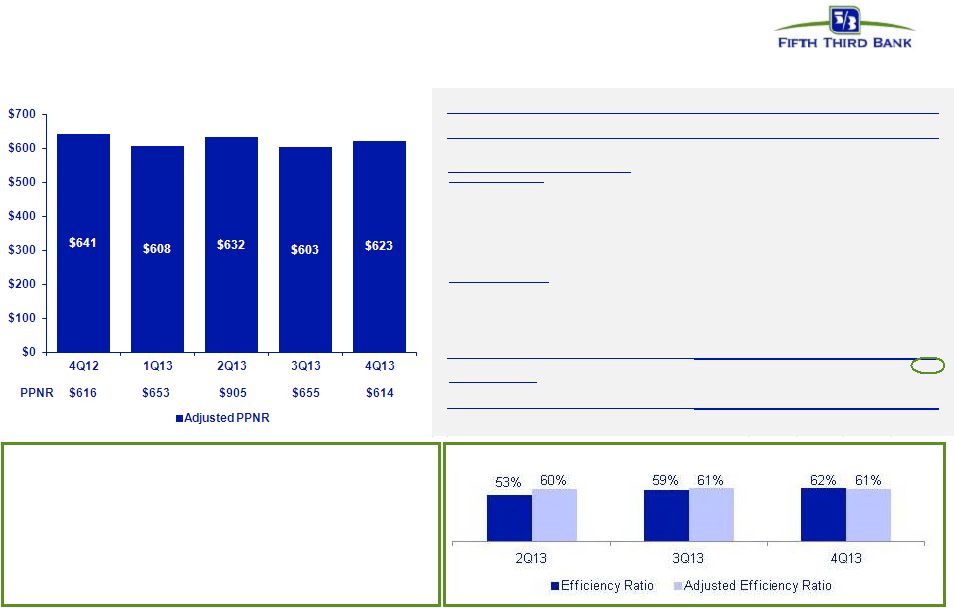

Pre-tax pre-provision earnings

1

PPNR trend

1

Non-GAAP measure; see Reg. G reconciliation in appendix.

2

Prior quarters include similar adjustments.

3

There

are

limitations

on

the

usefulness

of

credit-adjusted

PPNR,

including

the

significant

degree

to

which

changes

in

credit

and

fair

value

are

integral,

recurring

components

of

the

Bancorp’s

core

operations

as

a

financial

institution.

This

measure

has

been

included

herein

to

facilitate

a

greater

understanding

of

the

Bancorp’s

financial

condition.

Note:

4Q13

and

3Q13

also

included benefits to the mortgage repurchase provision of $28MM and $4MM,

respectively. 2Q13 also included the impact of $47MM in mortgage repurchase

provision.

These

impacts

are

reflected

in

“Credit-related

items”

and

“Adjusted

Efficiency

Ratio”

listed

above.

•

PPNR of $614MM down 6% from 3Q13 levels and

flat to prior year

•

Adjusted PPNR of $623MM, up 3% sequentially and

down 3% from prior year

PPNR reconciliation

Efficiency ratio

($ in millions)

4Q12

1Q13

2Q13

3Q13

4Q13

Income before income taxes (U.S. GAAP) (a)

$540

$591

$841

$604

$561

Add: Provision expense (U.S. GAAP) (b)

76

62

64

51

53

PPNR (a) + (b)

$616

$653

$905

$655

$614

2

In noninterest income:

Gain from sales of Vantiv shares

(157)

-

(242)

(85)

-

Vantiv warrant & puts

19

(34)

(76)

(6)

(91)

Other Vantiv-related income

-

-

-

-

(9)

Valuation of 2009 Visa total return swap

15

7

5

2

18

Sale of certain Fifth Third funds

-

(7)

-

-

-

BOLI settlement

-

-

(10)

-

-

Securities (gains) / losses

(2)

(17)

-

(2)

(2)

In noninterest expense:

Debt extinguishment (gains) / losses

134

-

-

-

8

Severance expense

3

3

1

5

8

Large bank assessment fees

-

-

-

5

-

Gain on sale of affordable housing investments

-

(9)

(2)

(1)

-

Donation to Fifth Third Foundation

-

3

-

-

8

Additions to litigation reserves

13

9

51

30

69

Adjusted PPNR

$641

$608

$632

$603

$623

Credit-related items

:

In noninterest income

13

10

6

5

5

In noninterest expense

68

24

35

16

(12)

Credit-adjusted PPNR

3

$722

$642

$673

$624

$616

:

Adjustments to remove (benefit) / detriment |

11

©

Fifth Third Bank | All Rights Reserved

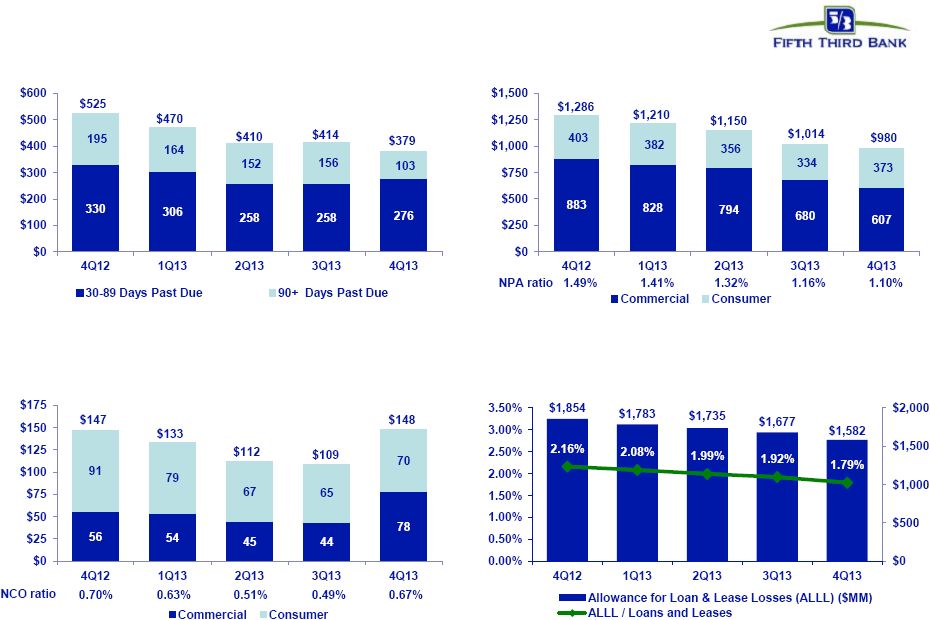

Improving Credit Quality

Net charge-offs ($MM)

4Q13 incl. a $43MM charge-off on a C&I loan restructured during the

quarter and $6MM of home equity charge-offs due to an accounting

policy change.

HFI Nonperforming assets ($MM)

NPAs down 24% from 4Q12;

lowest level since 2007

Reserve Coverage

Accruing Past Due ($MM)

Includes 4Q13 provision expense of $53MM;

Total delinquencies declined 28% from 4Q12;

remain at very low levels

reserve coverage levels remain among best-in-class

|

12

©

Fifth Third Bank | All Rights Reserved

NPL Rollforward

1

Increase in NPL inflow due to $43 million in inflows related to a portion of a

large credit restructured in 4Q13. This portion was charged off in 4Q13, therefore resulting in no net impact to ending

NPL balances.

2

Increase in NPL inflow primarily due to $46 million inflow resulting from change in

home equity nonaccrual policy. Note: Numbers may not sum due to

rounding. NPL HFI Rollforward

Commercial

4Q12

1Q13

2Q13

3Q13

4Q13

806

697

639

623

521

Transfers to nonperforming

68

80

151

71

107

Transfers to performing

(4)

(1)

(6)

(1)

(1)

Transfers to performing (restructured)

(5)

(4)

(7)

(2)

(2)

Transfers to held-for-sale

0

(1)

(2)

-

-

Loans sold from portfolio

(6)

(3)

(2)

(14)

(19)

Loan paydowns/payoffs

(89)

(53)

(80)

(101)

(61)

Transfers to other real estate owned

(22)

(27)

(28)

(14)

(12)

Charge-offs

(55)

(54)

(45)

(44)

(78)

Draws/other extensions of credit

4

5

3

3

3

697

639

623

521

458

Consumer

4Q12

1Q13

2Q13

3Q13

4Q13

347

332

314

286

248

Transfers to nonperforming

146

124

116

95

165

Transfers to performing

(28)

(26)

(31)

(30)

(25)

Transfers to performing (restructured)

(34)

(29)

(28)

(24)

(22)

Transfers to held-for-sale

-

-

-

-

-

Loans sold from portfolio

-

-

-

-

-

Loan paydowns/payoffs

(36)

(27)

(33)

(39)

(24)

Transfers to OREO/other repossessed property

(18)

(17)

(21)

(28)

(20)

Charge-offs

(47)

(46)

(30)

(13)

(30)

Draws/other extensions of credit

1

1

(1)

1

1

332

312

286

248

293

Total NPL

1,029

951

909

769

751

Total new nonaccrual loans -

HFI

214

204

267

166

272

Beginning NPL amount

Ending Commercial NPL

Beginning NPL amount

Ending Consumer NPL

1

1

2 |

13

©

Fifth Third Bank | All Rights Reserved

Mortgage repurchase overview

4Q13 balances of outstanding claims decreased 6% from 3Q13

Virtually all sold loans and the majority of new claims relate to

agencies

—

99% of outstanding balance of loans sold

—

89% of current quarter outstanding claims

Approximately 89% of outstanding balances of the serviced for

others portfolio relates to origination activity in 2009 and later

Private claims and exposure relate to whole loan sales (no

outstanding first mortgage securitizations)

—

Preponderance of private sales prior to 2006

2004-2008 vintages account for ~84% of total life to date losses

of $449MM from sold portfolio

$60MM decrease in repurchase reserves resulting from

previously announced settlement with Freddie Mac as well as

the corresponding expectations for future repurchase requests

and file claims.

Repurchase Reserves

1

($ in millions)

Outstanding Counterparty Claims ($ in millions)

4Q12

1Q13

2Q13

3Q13

4Q13

Beginning balance

$99

$131

$133

$139

$121

Net reserve additions

47

22

20

(4)

(27)

Repurchase losses

(15)

(20)

(14)

(13)

(33)

Ending balance

$131

$133

$139

$121

$61

1

Includes representation and warranty reserve ($44MM) and reserve for loans sold

with recourse ($16MM) Note: Numbers may not sum due to rounding.

Outstanding Balance of Sold Loans ($ in millions)

Fannie

Freddie

GNMA

Private

Total

2003 and Prior

$366

$1,590

$115

$122

$2,193

2004

151

586

22

92

851

2005

137

691

29

93

950

2006

182

537

25

150

895

8%

2007

269

888

33

126

1,316

2008

329

654

245

1,228

2009

858

4,174

2,179

1

7,211

2010

2,084

4,753

2,113

8,950

2011

2,744

5,101

1,721

9,566

2012

5,042

9,630

4,173

33

18,879

2013

3,932

7,376

5,553

259

17,120

Grand Total

16,095

35,979

16,208

877

69,159

1.3% |

14

©

Fifth Third Bank | All Rights Reserved

Strong capital position

1

Non-GAAP measure; See Reg. G reconciliation in appendix.

2

Capital

ratios

estimated;

presented

under

current

U.S.

capital

regulations.

The

pro

forma

Basel

III

Tier

I

common

equity

ratio

is

management’s

estimate

based

upon

its

current

interpretation

of

recent

prospective

regulatory

capital

requirements

approved

in

July

2013.

Significant payouts to shareholders

$710MM common

stock repurchases

(net of $398MM

shares issued

related to Series G

conversion)

$407MM common

dividends declared

$212MM common

stock repurchases

utilizing AT Vantiv

gains

•

Continue to execute on capital plans in 4Q13

–

Issued $450MM of preferred stock, Series I

–

Redeemed $750MM of Fifth Third Capital Trust

IV TruPS

Tier 1 common equity

1

Common Shares Outstanding (MM)

and Tangible Book Value per share |

15

©

Fifth Third Bank | All Rights Reserved

Balance Sheet:

Average loans & leases (excl. HFS)

Average transaction deposits

Income Statement:

Net interest income

2

Net interest margin

2

Noninterest income

1

Noninterest expense

Pre-provision net revenue

1,2

ROA

1

Effective tax rate

1

Asset Quality:

Net charge-offs

Loan loss allowance

4

Nonperforming assets

4

Tier 1 common equity

3,6

Category

Fifth Third: Outlook

2014 Outlook

1

$87.0B

$82.9B

1

2013 results exclude a net $534MM benefit from gains on Vantiv share issuance and

Vantiv warrants. 2014 outlook does not include potential but currently unforecasted items, such as any

potential additional Vantiv gains or losses, future capital actions, or changes in

regulatory or accounting guidance. 2

Presented on a fully-taxable equivalent basis.

3

Non-GAAP measure; see Reg. G reconciliation in appendix.

4

Ratio as a percent of loans excluding held-for-sale; allowance expectation

assumes current expectation for credit and economic trends and is subject to review in each period.

5

As a percentage of loans and leases

6

Current period capital ratios estimated. Tier 1 common equity ratio outlook assumes

generally stable common equity levels managed through asset growth and share repurchases.

Repurchases subject to ongoing evaluation under the Federal Reserve’s CCAR

process. 2013-Adjusted

1

Outlook as of January 23, 2014;

please see cautionary statement on slide 2 for risk factors related to

forward-looking statements Mid single digit growth

Mid single digit growth

Down ~$100MM (~0.40-0.45%

5

)

Lower vs. 4Q13

Down ~20%

vs. 4Q13

$3.58B

3.32% (3.21% 4Q13)

$2.70B

$3.95B

$2.31B

~1.2%

~28.4%

9.38%

$501MM (0.58%

5

)

$1.6B (1.79%)

$980MM (1.10%)

Consistent with 4Q13 |

16

©

Fifth Third Bank | All Rights Reserved

Appendix |

17

©

Fifth Third Bank | All Rights Reserved

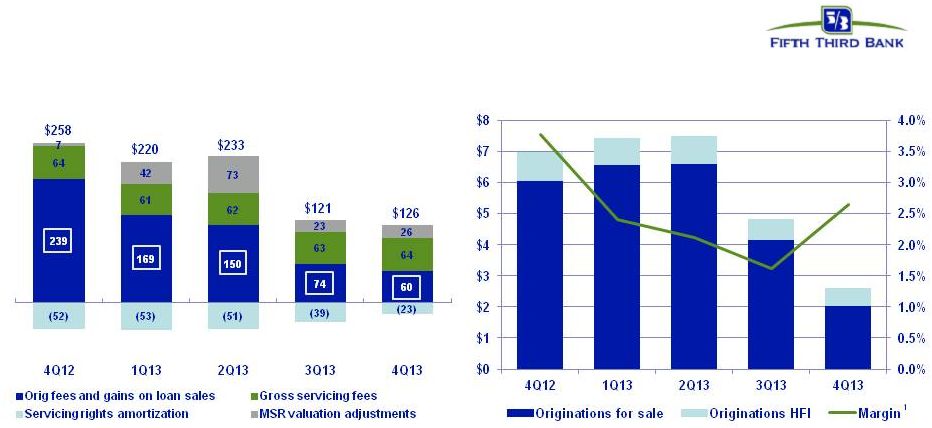

Mortgage banking results

•

4Q13 mortgage components:

–

MSR valuation adjustments of positive $26 million partially offset by lower gains on

sale –

Gain on sale margins improved

•

Expect stronger mortgage servicing results as rates rise

•

Emphasis on purchase business continues to shift volumes

–

51% purchase volume in 4Q13 vs. 43% 3Q13

Mortgage originations ($B) and gain-on-sale

margin1 Mortgage Banking Net Revenue ($MM)

Note: Numbers may not sum due to rounding.

1

Gain-on-sale margin represents gains on all loans originated for

sale. |

18

©

Fifth Third Bank | All Rights Reserved

Total

Funded

Total

Funded

Total

Funded

Total

Funded

(amounts in $MMs)

exposure

exposure

exposure

exposure

exposure

exposure

exposure

exposure

Peripheral Europe

-

-

10

-

202

103

212

103

Other Eurozone

-

-

56

14

2,031

1,161

2,087

1,175

Total Eurozone

-

-

66

14

2,233

1,264

2,299

1,278

Other Europe

-

-

83

23

889

500

972

523

Total Europe

-

-

149

37

3,122

1,764

3,271

1,801

Sovereigns

Financial Institutions

Non-Financial Entities

Total

European Exposure

Total exposure includes funded and unfunded commitments, net of collateral; funded

exposure excludes unfunded exposure Peripheral Europe includes Greece,

Ireland, Italy, Portugal and Spain Eurozone includes countries participating

in the European common currency (Euro)

Other Europe includes European countries not part of the Euro (primarily the United

Kingdom and Switzerland) Data above includes exposure to U.S. subsidiaries of

Europe-domiciled companies •

International exposure primarily related to trade finance and financing activities of

U.S. companies with foreign parent or overseas activities of U.S.

customers •

No European sovereign exposure (total international sovereign exposure $7MM)

•

Total exposure to European financial institutions <$150MM

•

Total exposure to five peripheral Europe countries ~$200MM

•

~$1.3B in funded exposure to Eurozone-related companies (~1% of total loan

portfolio) |

19

©

Fifth Third Bank | All Rights Reserved

Available and contingent borrowing capacity

(4Q13):

–

FHLB ~$12B available, ~$13B total

–

Federal Reserve ~$28B

Holding Company cash at 12/31/13: $2.1B

Cash currently sufficient to satisfy all fixed

obligations in a stressed environment for over

2 years (debt maturities, common and

preferred dividends, interest and other

expenses) without accessing capital markets;

relying on dividends from subsidiaries or any

other discretionary actions

Holding company unsecured debt maturities ($MM)

Bank unsecured debt maturities ($MM –

excl. Brokered CDs)

Heavily core funded

Strong liquidity profile

Demand

25%

Interest

checking

20%

Savings/

MMDA

22%

Consumer

time

3%

Foreign

Office

2%

Non-Core

Deposits

5%

S-T

borrowings

1%

Other

liabilities

4%

Equity

11%

L-T debt

7%

S-T

wholesale

6%

$1,250

$500

$500

$2,312

2014

2015

2016

2017

2018

2019

2020 on

Fifth Third Bancorp

Fifth Third Capital Trust (Bancorp) |

20

©

Fifth Third Bank | All Rights Reserved

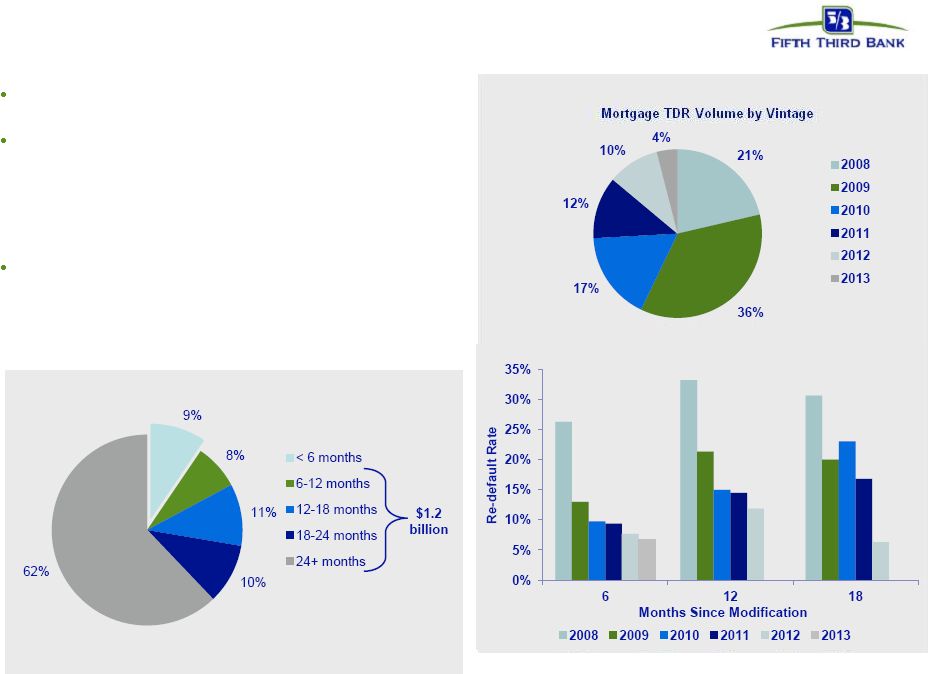

Troubled debt restructurings overview

Successive improvement in vintage performance during

2008 and 2009 as volume of modification increased

Of $1.8B in consumer TDRs, $1.7B were on accrual

status and $136MM were nonaccruals

—

$1.2B of TDRs are current and have been on the

books 6 or more months; within that, ~$1.1B of

TDRs are current and have been on the books for

more than a year

As current TDRs season, their default propensity

declines significantly

—

We see much lower defaults on current loans after

a vintage approaches 12 months since

modification

Source: Fifth Third and OCC/OTS data through 2Q13

$1.3B current consumer TDRs (%)

1

Fifth

Third

data

includes

changes

made

to

align

with

OCC/OTS

methodology

(i.e.

excludes

government

loans,

closed

loans

and

OREO

from

calculations)

TDR performance has improved in newer vintages

Mortgage TDRs that are past due 60 days or more trend by vintage

1 |

21

©

Fifth Third Bank | All Rights Reserved

Commercial & industrial

Loans by geography

Credit trends

Loans by industry

Comments

•

Commercial & industrial loans represented 44% of total loans and

45% of net charge-offs

–

4Q13 NCOs included a $43 million charge-off on a single

restructured credit

* Excludes loans held-for-sale.

($ in millions)

4Q12

1Q13

2Q13

3Q13

4Q13

EOP Balance*

$36,038

$36,757

$37,856

$38,253

$39,316

Avg Loans*

$34,301

$36,395

$37,630

$38,133

$38,835

90+ days delinquent

$1

$1

-

$3

-

as % of loans

NM

NM

NM

0.01%

NM

NPAs*

$352

$332

$361

$321

$290

as % of loans

0.98%

0.90%

0.95%

0.84%

0.74%

Net charge-offs

$36

$25

$33

$44

$66

as % of loans

0.42%

0.28%

0.35%

0.46%

0.67%

C&I |

22

©

Fifth Third Bank | All Rights Reserved

Commercial mortgage

Loans by geography

Credit trends

Loans by industry

Comments

•

Commercial mortgage loans represented 9% of total loans and

5% of net charge-offs

•

Owner occupied 4Q13 NCO ratio of 0.4%, non-owner occupied

4Q13 NCO ratio of 0.3%

•

Loans from FL/MI represented 36% of portfolio loans, 93% of

portfolio losses in 4Q13

* Excludes loans held-for-sale.

($ in millions)

4Q12

1Q13

2Q13

3Q13

4Q13

EOP Balance*

$9,103

$8,766

$8,443

$8,052

$8,066

Avg Loans*

$9,193

$8,965

$8,618

$8,273

$8,047

90+ days delinquent

$22

-

-

-

-

as % of loans

0.24%

NM

NM

NM

NM

NPAs*

$434

$409

$355

$296

$252

as % of loans

4.69%

4.59%

4.15%

3.62%

3.09%

Net charge-offs

$17

$26

$10

$2

$8

as % of loans

0.70%

1.18%

0.50%

0.14%

0.40%

Commercial mortgage |

23

©

Fifth Third Bank | All Rights Reserved

Commercial construction

Loans by geography

Credit trends

Loans by industry

Comments

•

Commercial construction loans represented 1% of total loans

and 3% of net charge-offs

•

Loans from FL/MI represented 17% of portfolio loans

* Excludes loans held-for-sale.

($ in millions)

4Q12

1Q13

2Q13

3Q13

4Q13

EOP Balance*

$698

$694

$754

$875

$1,039

Avg Loans*

$686

$695

$713

$793

$952

90+ days delinquent

$1

-

-

-

-

as % of loans

0.14%

NM

NM

NM

NM

NPAs*

$88

$78

$69

$62

$59

as % of loans

12.37%

11.12%

8.88%

6.86%

5.53%

Net charge-offs

$4

$3

-

($2)

$4

as % of loans

1.91%

1.44%

(0.04%)

(1.16%)

1.65%

Commercial construction |

24

©

Fifth Third Bank | All Rights Reserved

Homebuilders/developers

(included in previous slides)

Loans by geography

Credit trends

Loans by industry

Comments

•

Originations of builder/developer loans suspended in 2007

•

Remaining portfolio balance of $194MM, down 94% from peak of

$3.3B in 2Q08; represents <1% of total loans and <1% of commercial

loans

•

$47MM of NPAs (71% commercial mortgage, 16% commercial

construction, 13% C&I)

* Excludes loans held-for-sale.

($ in millions)

4Q12

1Q13

2Q13

3Q13

4Q13

EOP Balance*

$318

$309

$285

$226

$194

90+ days delinquent

-

-

-

-

-

as % of loans

NM

NM

NM

NM

NM

NPAs*

$88

$79

$63

$53

$47

as % of loans

24.19%

22.44%

22.00%

20.85%

20.72%

Net charge-offs

-

$1

($1)

($1)

$4

as % of loans

0.28%

1.57%

(0.84%)

(0.96%)

7.40%

Homebuilders/developers |

25

©

Fifth Third Bank | All Rights Reserved

Residential mortgage

1

st

liens: 100%; weighted average LTV: 72.7%

Weighted average origination FICO: 753

Origination FICO distribution: <660 6%; 660-689 5%; 690-719 9%;

720-749 14%; 750+ 57%; Other^ 9%

(note: loans <660 includes CRA loans and FHA/VA loans)

Origination LTV distribution: <=70 39%; 70.1-80 36%; 80.1-90 7%;

90.1-95 4%; >95 14%

Vintage distribution: 2013: 22%; 2012 24%; 2011 15%; 2010 8%;

2009 4%; 2008 4%; 2007 4%; 2006 4%; 2005 7%; 2004 and prior

8%

15% originated through 3rd

party; performance similar to direct

Loans by geography

Credit trends

Portfolio details

Comments

^ Includes acquired loans where FICO at origination is not available

* Excludes loans held-for-sale

•

Residential mortgage loans represented 14% of total loans and 8%

of

net charge-offs

•

FL portfolio 13% of residential mortgage loans and 16% of portfolio

losses; MI portfolio 15% of residential mortgage loans and 18% of

portfolio losses

($ in millions)

4Q12

1Q13

2Q13

3Q13

4Q13

EOP Balance*

$12,017

$12,091

$12,400

$12,534

$12,680

Avg Loans*

$11,846

$12,096

$12,260

$12,486

$12,609

90+ days delinquent

$75

$74

$71

$73

$66

as % of loans

0.62%

0.61%

0.57%

0.58%

0.52%

NPAs*

$290

$275

$255

$229

$222

as % of loans

2.41%

2.27%

2.06%

1.83%

1.75%

Net charge-offs

$23

$20

$15

$12

$13

as % of loans

0.77%

0.69%

0.48%

0.39%

0.39%

Residential mortgage |

26

©

Fifth Third Bank | All Rights Reserved

Home equity loans represented 10% of total loans and 17% of net

charge-offs

–

4Q13 included $6 million of additional charge-offs and $46 million

of additional NPAs due to a change in policy on home equity

nonaccruals

Approximately 13% of portfolio in broker product generated 31% total

loss

Approximately one third of Fifth Third 2

nd

liens are behind Fifth Third

1

st

liens

2005/2006 vintages represent approximately 25% of portfolio; account

for 45% of losses

Home equity

1

st

liens: 34%; 2nd liens: 66%

Weighted average origination FICO: 751

Origination FICO distribution^: <660 3%; 660-689 7%; 690-719 12%;

720-749 16%; 750+ 53%; Other 9%

Average CLTV: 73%; Origination CLTV distribution: <=70 40%; 70.1-

80 23%; 80.1-90 19%; 90.1-95 6%; >95 12%

Vintage distribution: 2013: 7%; 2012 5%; 2011 3%; 2010 3%; 2009

3%; 2008 9%; 2007 10%; 2006 13%; 2005 12%; 2004 and prior 35%

% through broker channels: 13% WA FICO: 734 brokered, 754 direct;

WA CLTV: 88% brokered; 71% direct

Portfolio details

Comments

Brokered loans by geography

Direct loans by geography

Credit trends

Note: Brokered and direct home equity net charge-off ratios are calculated

based on end of period loan balances ^ Includes acquired loans where FICO at

origination is not available * Excludes loans held-for-sale

($ in millions)

4Q12

1Q13

2Q13

3Q13

4Q13

EOP Balance*

$1,366

$1,321

$1,275

$1,231

$1,190

90+ days delinquent

$14

$13

$11

$11

-

as % of loans

1.05%

1.02%

0.89%

0.88%

NM

Net charge-offs

$12

$10

$7

$6

$8

as % of loans

3.48%

3.08%

2.30%

1.91%

2.75%

Home equity - brokered

($ in millions)

4Q12

1Q13

2Q13

3Q13

4Q13

EOP Balance*

$8,652

$8,406

$8,256

$8,125

$8,056

90+ days delinquent

$44

$40

$37

$35

-

as % of loans

0.50%

0.47%

0.44%

0.43%

NM

Net charge-offs

$22

$20

$16

$13

$18

as % of loans

1.01%

0.93%

0.76%

0.64%

0.87%

Home equity - direct |

27

©

Fifth Third Bank | All Rights Reserved

Regulation G Non-GAAP reconciliation

Fifth Third Bancorp and Subsidiaries

Regulation G Non-GAAP Reconcilation

$ and shares in millions

(unaudited)

December

September

June

March

December

2013

2013

2013

2013

2012

Income before income taxes (U.S. GAAP)

$561

$604

$841

$591

$540

Add:

Provision expense (U.S. GAAP)

53

51

64

62

76

Pre-provision net revenue (a)

614

655

905

653

616

Net income available to common shareholders (U.S. GAAP)

383

421

582

413

390

Add:

Intangible amortization, net of tax

1

1

1

1

2

Tangible net

income available to common shareholders 384

422

583

414

392

Tangible net income available to common

shareholders (annualized) (b) 1,523

1,674

2,338

1,679

1,559

Average Bancorp shareholders' equity (U.S. GAAP)

14,757

14,440

14,221

13,779

13,855

Less:

Average preferred stock

(703)

(593)

(717)

(398)

(398)

Average goodwill

(2,416)

(2,416)

(2,416)

(2,416)

(2,417)

Average intangible assets

(20)

(22)

(24)

(26)

(28)

Average tangible common equity

(c) 11,618

11,409

11,064

10,939

11,012

Total Bancorp shareholders' equity (U.S. GAAP)

14,589

14,641

14,239

13,882

13,716

Less:

Preferred stock

(1,034)

(593)

(991)

(398)

(398)

Goodwill

(2,416)

(2,416)

(2,416)

(2,416)

(2,416)

Intangible assets

(19)

(21)

(23)

(25)

(27)

Tangible common equity, including

unrealized gains / losses (d) 11,120

11,611

10,809

11,043

10,875

Less: Accumulated other comprehensive income

(82)

(218)

(149)

(333)

(375)

Tangible common equity, excluding unrealized gains /

losses (e) 11,038

11,393

10,660

10,710

10,500

Total assets (U.S. GAAP)

130,443

125,673

123,360

121,382

121,894

Less:

Goodwill

(2,416)

(2,416)

(2,416)

(2,416)

(2,416)

Intangible assets

(19)

(21)

(23)

(25)

(27)

Tangible assets, including

unrealized gains / losses (f) 128,008

123,236

120,921

118,941

119,451

Less: Accumulated other comprehensive income / loss, before tax

(126)

(335)

(229)

(512)

(577)

Tangible assets, excluding unrealized gains / losses

(g) 127,882

122,901

120,692

118,429

118,874

Common shares outstanding (h)

855

887

851

875

882

Ratios:

Return on average tangible common equity (b) / (c)

13.1%

14.7%

21.1%

15.4%

14.1%

Tangible common equity (excluding unrealized gains/losses) (e) / (g)

8.63%

9.27%

8.83%

9.03%

8.83%

Tangible common equity (including unrealized gains/losses) (d) / (f)

8.69%

9.42%

8.94%

9.28%

9.10%

Tangible book value per share (d) / (h)

13.00

13.09

12.69

12.62

12.33

For the Three Months Ended |

28

©

Fifth Third Bank | All Rights Reserved

Regulation G Non-GAAP reconciliation

Fifth Third Bancorp and Subsidiaries

Regulation G Non-GAAP Reconcilation

$ and shares in millions

(unaudited)

December

September

June

March

December

2013

2013

2013

2013

2012

Total Bancorp shareholders' equity (U.S. GAAP)

$14,589

$14,641

$14,239

$13,882

$13,716

Goodwill and certain other intangibles

(2,492)

(2,492)

(2,496)

(2,504)

(2,499)

Unrealized gains

(82)

(218)

(149)

(333)

(375)

Qualifying trust preferred securities

60

810

810

810

810

Other

19

21

22

23

33

Tier I capital

12,094

12,762

12,426

11,878

11,685

Less:

Preferred stock

(1,034)

(593)

(991)

(398)

(398)

Qualifying trust preferred securities

(60)

(810)

(810)

(810)

(810)

Qualifying noncontrolling interest in consolidated

subsidiaries (37)

(39)

(38)

(38)

(48)

Tier I common equity (a)

10,963

11,320

10,587

10,632

10,429

Risk-weighted assets, determined in accordance with

prescribed regulatory requirements (b)

116,836

114,544

112,285

109,626

109,699

Ratio:

Tier I common equity (a) / (b)

9.38%

9.88%

9.43%

9.70%

9.51%

Basel III - Estimated Tier 1 common equity ratio

December

September

2013

2013

Tier 1 common equity (Basel I)

$10,963

$11,320

Add:

Adjustment related to capital components

$82

$88

Estimated Tier 1 common equity under final Basel III rules without AOCI (opt out)(c)

$11,045

$11,408

Add:

Adjustment related to AOCI

$82

$218

Estimated Tier 1 common equity under final Basel III rules with AOCI (non opt out)(d)

$11,127

$11,626

Estimated risk-weighted assets under final Basel III rules (e)

122,602

120,447

Estimated Tier 1 common equity ratio under final Basel III rules (opt out) (c) /

(e) 9.01%

9.47%

Estimated Tier 1 common equity ratio under final Basel III rules (non opt out) (d) / (e)

9.08%

9.65%

(c), (d)

(e)

Under the final Basel III rules, non-advanced approach banks are permitted to make a one-time

election to opt out of the requirement to include AOCI in Tier 1 common equity. Other adjustments

include mortgage servicing rights and deferred tax assets subject to threshold limitations and

deferred tax liabilities related to intangible assets. Key differences under Basel III in the

calculation of risk-weighted assets compared to Basel I include: (1) Risk weighting for commitments under 1 year; (2) Higher risk weighting for exposures to

securitizations, past due loans, foreign banks and certain commercial real estate; (3) Higher risk

weighting for mortgage servicing rights and deferred tax assets that are under certain thresholds as

a percent of Tier 1 capial; and (4) Derivatives are differentiated between exchange clearing and

over-the-counter and the 50% risk-weight cap is removed. For the Three Months

Ended |

29

©

Fifth Third Bank | All Rights Reserved

Regulation G Non-GAAP reconciliation

Fifth Third Bancorp and Subsidiaries

Regulation G Non-GAAP Reconcilation

$ and shares in millions

(unaudited)

2013

2012

2011

2010

2009

Total Bancorp shareholders' equity (U.S. GAAP)

$14,589

$13,716

$13,201

$14,051

$13,497

Goodwill and certain other intangibles

(2,492)

(2,499)

(2,514)

(2,546)

(2,565)

Unrealized gains

(82)

(375)

(470)

(314)

(241)

Qualifying trust preferred securities

60

810

2,248

2,763

2,763

Other

19

33

38

11

(26)

Tier I capital

12,094

11,685

12,503

13,965

13,428

Less:

Preferred stock

(1,034)

(398)

(398)

(3,654)

(3,609)

Qualifying trust preferred securities

(60)

(810)

(2,248)

(2,763)

(2,763)

Qualifying noncontrolling interest in consolidated subsidiaries

(37)

(48)

(50)

(30)

-

Tier I common equity (a)

10,963

10,429

9,807

7,518

7,056

Risk-weighted assets, determined in accordance with

prescribed regulatory requirements (b)

116,836

109,699

104,945

100,561

100,933

Ratio:

Tier I common equity (a) / (b)

9.38%

9.51%

9.35%

7.48%

6.99%

For the Year Ended |