Attached files

| file | filename |

|---|---|

| 8-K - 8-K - BANCORPSOUTH INC | d660100d8k.htm |

| EX-99.1 - EX-99.1 - BANCORPSOUTH INC | d660100dex991.htm |

BancorpSouth, Inc.

Financial Information

As of December 31, 2013

Exhibit 99.2 |

Forward Looking Information

2

Certain statements contained in this presentation and the accompanying slides may not be based on

historical facts and are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933,

as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These

forward-looking statements may be identified by reference to a future period or by the use of forward-looking terminology,

such as “anticipate,” “believe,” “estimate,” “expect,”

“foresee,” “may,” “might,” “will,” “intend,” “could,” “would” or “plan,” or future or conditional verb tenses, and variations or negatives of such terms. These

forward- looking statements include, without limitation,, statements relating to revenue

estimates for the Company’s operations in Houston, Texas following the closing of the transaction with GEM Insurance Agencies, LP and

the potential for expansion of the Company’s business in Houston, the terms and closing of the

proposed transactions with Ouachita Bancshares Corp. and Central Community Corp., acceptance by customers of

Ouachita Bancshares Corp. and Central Community Corp. of the Company’s products and services, the

opportunities to enhance market share in certain markets and market acceptance of the Company generally in

new markets, the impact of cost-saving initiatives, our ability to improve efficiency, and our use

of non-GAAP financial measures. We caution you not to place undue reliance on the forward-looking statements

contained in this news release in that actual results could differ materially from those indicated in

such forward-looking statements because of a variety of factors. These factors may include, but are not limited to, the

ability to obtain required shareholder and regulatory approvals of the mergers, the ability of the

Company, Ouachita Bancshares Corp. and Central Community Corp. to close the mergers, the ability of the Company to

expand its insurance operations in Houston, conditions in the financial markets and economic conditions

generally, the adequacy of the Company’s provision and allowance for credit losses to cover actual credit losses,

the credit risk associated with real estate construction, acquisition and development loans, losses

resulting from the significant amount of the Company’s other real estate owned, limitations on the Company’s ability to

declare and pay dividends, the impact of legal or administrative proceedings, the availability of

capital on favorable terms if and when needed, liquidity risk, governmental regulation, including the Dodd Frank Act, and

supervision of the Company’s operations, the short-term and long-term impact of changes to

banking capital standards on the Company’s regulatory capital and liquidity, the impact of regulations on service charges on

the Company’s core deposit accounts, the susceptibility of the Company’s business to local

economic or environmental conditions, the soundness of other financial institutions, changes in interest rates, the impact of

monetary policies and economic factors on the Company’s ability to attract deposits or make loans,

volatility in capital and credit markets, reputational risk, the impact of hurricanes or other adverse weather events, any

requirement that the Company write down goodwill or other intangible assets, diversification in the

types of financial services the Company offers, the Company’s ability to adapt its products and services to evolving

industry standards and consumer preferences, competition with other financial services companies, risks

in connection with completed or potential acquisitions, the Company’s growth strategy, interruptions or breaches

in the Company’s information system security, the failure of certain third party vendors to

perform, unfavorable ratings by rating agencies, dilution caused by the Company’s issuance of any additional shares of its

common stock to raise capital or acquire other banks, bank holding companies, financial holding

companies and insurance agencies, other factors generally understood to affect the financial results of financial services

companies and other factors detailed from time to time in the Company’s press releases and filings

with the Securities and Exchange Commission. Forward-looking statements speak only as of the date they were

made, and, except as required by law, we do not undertake any obligation to update or revise

forward-looking statements to reflect events or circumstances after the date of this presentation. Certain tabular

presentations may not reconcile because of rounding. Unless otherwise noted, any quotes in this

presentation can be attributed to company management. In connection with the proposed merger of Central Community Corporation with and into BancopSouth,

BancorpSouth will file a registration statement on Form S-4 with the Securities and Exchange

Commission. Shareholders of BancorpSouth and Central Community Corporation are encouraged to read

the registration statement, including the proxy statement/prospectus that will be a part of the

registration statement, because it will contain important information about the merger, BancorpSouth and

Central Community Corporation After the registration statement is filed with the SEC, the proxy

statement/prospectus and other relevant documents will be available for free on the SEC’s web site

(www.sec.gov), and the proxy statement/prospectus will also be made available for free from the

Corporate Secretary of each of BancorpSouth and Central Community Corporation

In connection with the proposed merger of Ouachita Bancshares Corp. with and into BancorpSouth,

BancorpSouth will file a registration statement on Form S-4 with the Securities and Exchange

Commission. Shareholders of BancorpSouth and Ouachita Bancshares Corp. are encouraged to read the

registration statement, including the proxy statement/prospectus that will be a part of the

registration statement, because it will contain important information about the merger, BancorpSouth and

Ouachita Bancshares Corp. After the registration statement is filed with the SEC, the proxy

statement/prospectus and other relevant documents will be available for free on the SEC’s web site

(www.sec.gov), and the proxy statement/prospectus will also be made available for free from the

Corporate Secretary of each of BancorpSouth and Ouachita Bancshares Corp.

|

Q4

Highlights At and for the three months ended December 31, 2013

*Expected to close during the second quarter of 2014.

Net income of $27.7 million, or $0.29 per diluted share

Acquisition of Gem Insurance Agencies, LP (“GEM”)

Expected to produce annual insurance commission revenues of approximately $9

million Generated net loan growth of $184.9 million, or 8.4% annualized

Net interest margin increased to 3.52% from 3.45% for the third quarter

Expense control focus and efficiency initiatives continue to improve

performance Continued improving credit quality

Subsequent announcements*

Acquisition of Ouachita Bancshares Corp. (Ouachita Independent Bank)

Acquisition of Central Community Corporation (First State Bank Central

Texas) 3 |

Recent

Quarterly Results Dollars in millions, except per share data

4

12/31/13

9/30/13

12/31/12

vs 9/30/13

Net interest revenue

102.4

$

100.2

$

100.9

$

2.2

%

1.5

%

Provision for credit losses

0.0

0.5

6.0

(100.0)

(100.0)

Noninterest revenue

65.1

62.5

70.9

4.2

(8.1)

Noninterest expense

127.8

129.4

143.2

(1.2)

(10.7)

Income before income taxes

39.7

32.9

22.5

20.9

76.2

Income tax provision

12.0

8.0

5.6

50.2

116.0

Net income

27.7

$

24.9

$

17.0

$

11.4

%

63.1

%

Net income per share: diluted

0.29

$

0.26

$

0.18

$

11.5

%

61.1

%

Three Months Ended

% Change

vs 12/31/12 |

Noninterest Revenue

Dollars in thousands

NM –

Not Meaningful

5

12/31/13

9/30/13

12/31/12

vs 9/30/13

Mortgage lending revenue

9,605

5,134

17,188

87.1

(44.1)

Credit card, debit card and merchant fees

8,324

8,834

8,125

(5.8)

2.4

Deposit service charges

13,570

13,679

13,875

(0.8)

(2.2)

Trust income

3,717

3,332

3,391

11.6

9.6

Security gains, net

29

(5)

152

NM

NM

Insurance commissions

21,397

23,800

20,502

(10.1)

4.4

Other

8,483

7,740

7,668

9.6

10.6

Total noninterest revenue

65,125

$

62,514

$

70,901

$

4.2

%

(8.1)

%

% of total revenue

38.9%

38.4%

41.3%

Three Months Ended

% Change

vs 12/31/12 |

Mortgage and Insurance Revenue

Dollars in thousands

6

Mortgage Lending Revenue

12/31/13

9/30/13

6/30/13

3/31/13

12/31/12

Origination revenue

3,590

$

2,862

$

10,471

$

9,187

$

15,131

$

Servicing revenue

4,361

4,072

3,908

3,827

3,879

MSR payoffs/paydowns

(1,240)

(1,560)

(1,739)

(1,705)

(2,005)

MSR valuation adjustment

2,894

(240)

5,252

1,037

183

Total mortgage lending revenue

9,605

$

5,134

$

17,892

$

12,346

$

17,188

$

Production volume

222,282

$

341,854

$

434,966

$

425,882

$

549,392

$

Purchase money production

160,043

$

229,042

$

226,182

$

161,835

$

175,805

$

Margin on total production

1.62%

0.84%

2.41%

2.16%

2.75%

Insurance Commission Revenue

Property and casualty commissions

15,588

$

18,372

$

18,762

$

16,878

$

14,968

$

Life and health commissions

4,525

4,061

5,093

4,688

4,376

Risk management income

648

628

573

650

581

Other

636

739

1,434

4,425

577

Total insurance commissions

21,397

$

23,800

$

25,862

$

26,641

$

20,502

$

Three Months Ended |

Loan

Portfolio Dollars in millions

Net loans and leases

7

As of

12/31/13

9/30/13

12/31/12

Commercial and industrial

1,529

$

1,504

$

1,477

$

6.7

%

3.6

%

Real estate:

Consumer mortgages

1,976

1,931

1,874

9.2

5.5

Home equity

494

490

486

3.2

1.7

Agricultural

235

235

256

0.0

(8.4)

Commercial and industrial-owner occupied

1,473

1,422

1,333

14.3

10.5

Construction, acquisition and development

741

724

736

9.8

0.8

Commercial

1,846

1,795

1,749

11.2

5.6

Credit Cards

111

105

105

23.5

6.1

Other

552

567

622

(10.8)

(11.2)

Total

8,958

$

8,773

$

8,637

$

8.4

%

3.7

%

vs 12/31/12

% Change

vs 9/30/13

Annualized |

No

provision for credit losses recorded, which represents a decline from $0.5

million for the third quarter of 2013 and $6.0 million for the

fourth quarter of 2012

NPLs decreased $23.9 million, or 16.6%, and NPAs declined $31.4

million, or 14.2%

OREO decreased $7.5 million, or 9.8%

52% of non-accrual loans were paying as agreed

Near-term delinquencies modestly increased to $33.8 million

Net charge-offs declined to $0.7 million from $7.6 million for the third

quarter

Credit Quality Highlights

8

At and for the three months ended December 31, 2013

“Paying as agreed” includes loans < 30 days past due with payments occurring at least

quarterly |

Non-Performing Loans

Dollars in millions

Net loans and leases

9

As of

12/31/13

9/30/13

12/31/12

Commercial and industrial

4.2

$

6.6

$

10.2

$

(37.0)

%

(59.2)

%

Real estate:

Consumer mortgages

29.1

34.2

40.7

(14.8)

(28.5)

Home equity

3.7

3.3

3.5

12.4

5.7

Agricultural

1.9

4.5

8.0

(58.3)

(76.6)

Commercial and industrial-owner occupied

23.6

23.1

28.3

2.1

(16.7)

Construction, acquisition and development

24.3

32.7

72.0

(25.7)

(66.2)

Commercial

29.4

34.8

62.2

(15.6)

(52.8)

Credit Cards

1.8

2.0

2.5

(13.2)

(30.0)

Other

2.6

3.1

6.1

(18.4)

(58.1)

Total

120.4

$

144.3

$

233.6

$

(16.6)

%

(48.4)

%

NPL's to net loans and leases

1.34%

1.65%

2.70%

% Change

vs 9/30/13

vs 12/31/12 |

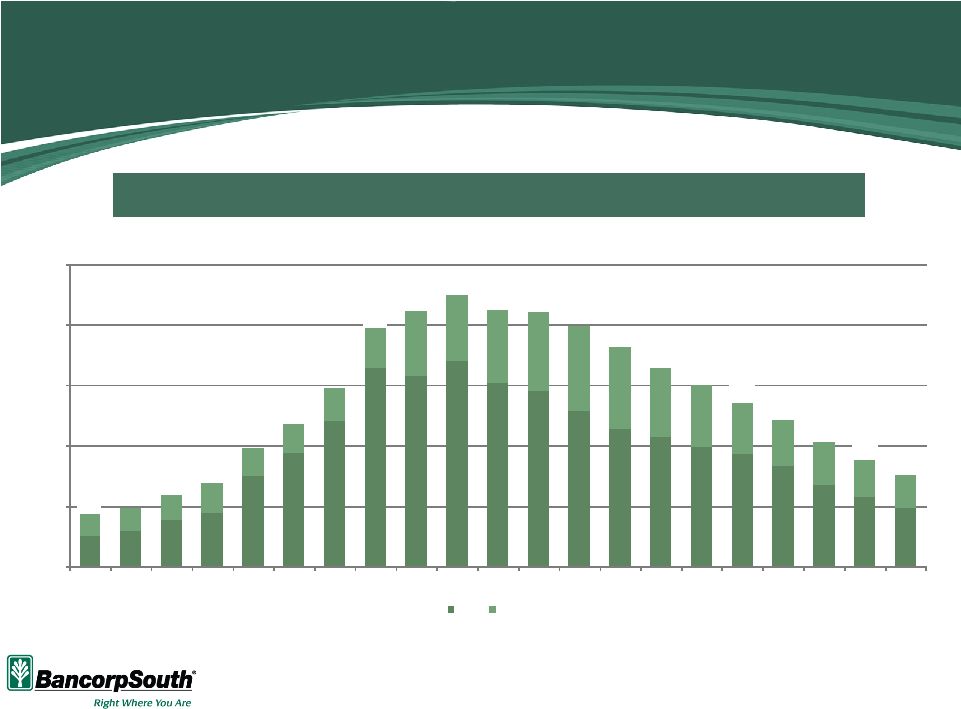

NPA

Improvement 10

Total NPAs Have Declined Over 40% in the Last 12 Months

$64

$74

$98

$112

$186

$236

$302

$409

$394

$425

$380

$363

$322

$285

$267

$247

$234

$207

$168

$144

$120

$46

$47

$51

$62

$59

$59

$68

$83

$133

$136

$151

$163

$174

$168

$144

$128

$103

$96

$88

$77

$69

$110

$121

$149

$174

$246

$295

$370

$528

$561

$531

$525

$496

$453

$411

$376

$337

$303

$256

$221

$190

$0

$125

$250

$375

$500

$625

4Q 08

1Q 09

2Q 09

3Q 09

4Q 09

1Q 10

2Q 10

3Q 10

4Q 10

1Q 11

2Q 11

3Q 11

4Q 11

1Q 12

2Q 12

3Q 12

4Q 12

1Q 13

2Q 13

3Q 13

4Q 13

NPLs

OREO

Dollars in millions

NPLs consist of nonaccrual loans, loans 90+ days past due and restructured

loans NPAs consist of NPLs and other real estate owned

$492 |

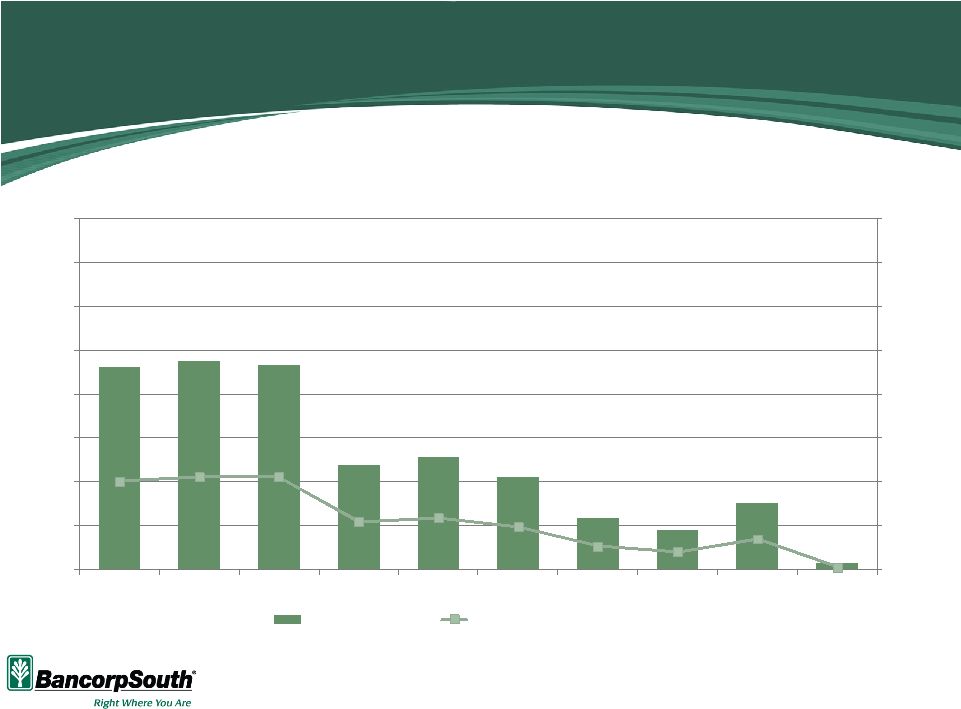

Net

Charge-offs % Avg. Loans

11

$23

$24

$23

$12

$13

$11

$6

$5

$8

$1

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

$0

$5

$10

$15

$20

$25

$30

$35

$40

9/30/11

12/31/11

3/31/12

6/30/12

9/30/12

12/31/12

3/31/13

6/30/13

9/30/13

12/31/13

Net charge-offs

Net charge-offs / average loans

Dollars in millions

Net charge-offs for the quarters ended as of the dates shown |

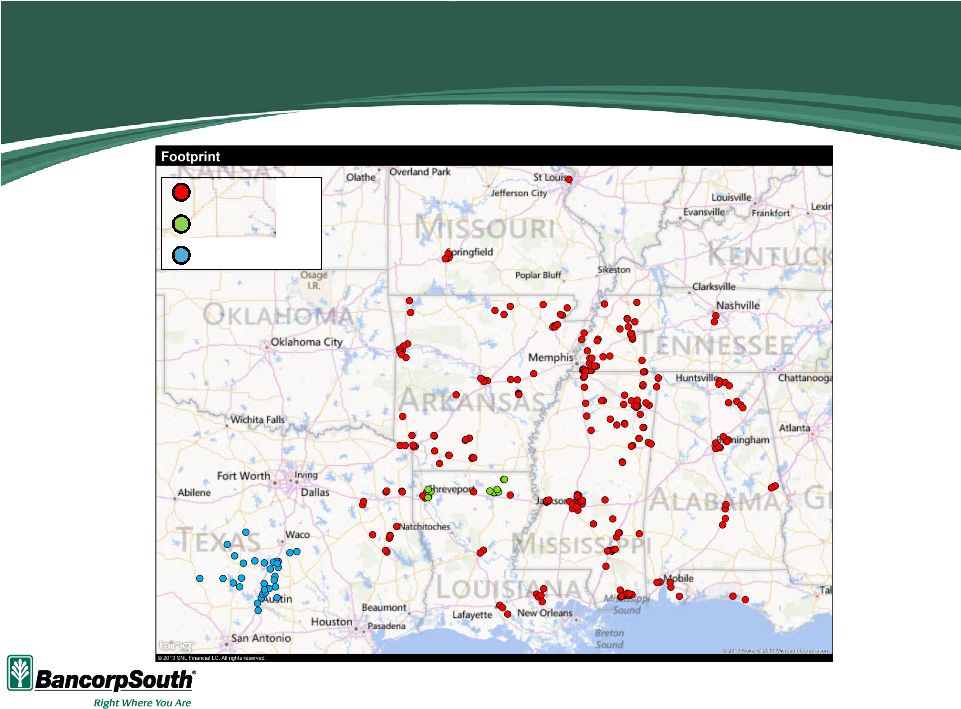

Footprint Expansion

12

Source:

SNL

Financial

BancorpSouth (256)

Ouachita* (12)

First State Bank* (31)

*Transactions

expected

to

close

during

the

second

quarter

of

2014 |

Recent Transaction Announcements

Ouachita Bancshares Corp. (Ouachita Independent Bank)

Assets

-

$650

million;

Loans

-

$475

million;

Deposits

-

$550

million

In-market

expansion

–

enhance

presence

along

I-20

corridor

•

Footprint overlap in Shreveport and Monroe

•

Meaningful cost save opportunities

Low-risk opportunity

•

Similar cultures and operating styles

•

Clean credit quality

Accretive to earnings per share

Central Community Corporation (First State Bank Central Texas)

Assets

-

$1.3

billion;

Loans

-

$550

million;

Deposits

-

$1.1

billion

Footprint

expansion

–

high

growth

Austin,

TX

market

and

other

markets

along

I-35

corridor

•

Austin, TX ranked No. 1 economy in the U.S. based on the economic rankings of The

Business Journals’

On Numbers report

•

Foundation for growth in Texas, both organically and future consolidation

opportunities Similar business models with community and customer

focus Accretive to earnings per share

13

Financial

data

as

of

12/31/13

Ouachita

Bancshares

Corp.

and

Central

Community

Corporation

transactions

expected

to

close

during

the

second

quarter

of

2014 |

14

Deposit Market Share

Source:

SNL

Financial

Market

BXS Market

Share Rank

6/30/13

Total BXS

Deposits

6/30/13

Percentage

of Total

Company

Deposits

BXS Market

Share 2013

(%)

Ouachita

Bancshares

Corp.

Deposits

6/30/13

Central

Community

Corp.

Deposits

6/30/13

Pro Forma

Deposits

6/30/13

Pro Forma

Percentage of

Total

Company

Deposits

Pro Forma

Market Share

Rank 6/30/13

Pro Forma

Market Share

2013 (%)

Market YoY

Deposit

Growth

2013 (%)

Mississippi

3

5,069,157

$

46.4%

10.6%

-

$

-

$

5,069,157

$

40.7%

3

10.6%

2.6%

Texas

65

826,576

7.6%

0.1%

-

977,625

1,804,201

14.5%

29

0.3%

8.9%

Arkansas

7

1,733,083

15.9%

3.3%

-

-

1,733,083

13.9%

7

3.3%

-0.5%

Louisiana

11

955,359

8.7%

1.0%

533,685

-

1,489,044

12.0%

7

1.6%

5.3%

Tennessee

15

1,184,566

10.8%

1.0%

-

-

1,184,566

9.5%

15

1.0%

0.1%

Alabama

13

824,116

7.5%

1.0%

-

-

824,116

6.6%

13

1.0%

1.8%

Missouri

66

317,286

2.9%

0.2%

-

-

317,286

2.6%

66

0.2%

6.2%

Florida

246

19,351

0.2%

0.0%

-

-

19,351

0.2%

246

0.0%

4.1%

Total

10,929,494

$

100.0%

533,685

$

977,625

$

12,440,804

$

100.0%

6/30/13 Deposit Market Share ($ in thousands)

Note:

Deposit

data

as

of

6/30/13

Ouachita

Bancshares

Corp.

and

Central

Community

Corporation

transactions

expected

to

close

during

the

second

quarter

of

2014 |

Summary

Meaningful progress during 2013

Profitability improvement

Loan growth following three years of contraction

Progress towards improving efficiency

Credit quality continues to improve

Current team focus

Lenders continue to bring quality deals into the loan pipeline

Insurance is growing, both through winning new business and the GEM

acquisition Mortgage group attracting and retaining key producers

Other lines of business continue to grow and improve performance

Operations

and

support

areas

preparing

for

integration

of

recent

bank

deals

Goals for 2014

More

of

the

same

–

growth

and

efficiency

Q&A

15 |