Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - BBX CAPITAL CORP | d661895d8k.htm |

Bluegreen Corporation

January 2014

Exhibit 99.1 |

1

Statements

in

this

presentation

may

constitute

forward-looking

statements

and

are

made

pursuant

to

the

Safe

Harbor

Provision

of

the

Private

Securities

Litigation

Reform

Act

of

1995.

Forward

looking

statements

are

based

largely

on

expectations

and

are

subject

to

a

number

of

risks

and

uncertainties

including,

but

not

limited

to,

the

risks

and

uncertainties

associated

with

economic,

credit

market,

competitive

and

other

factors

affecting

the

Company

and

its

operations,

markets,

products

and

services;

risks

relating

to

the

merger

with

BFC

Financial

Corporation

(“BFC”);

the

Company’s

efforts

to

improve

its

liquidity

through

cash

sales

and

larger

down

payments

on

financed

sales

may

not

be

successful;

the

performance

of

the

Company’s

VOI

notes

receivable

may

deteriorate,

and

the

FICO

®

score-

based

credit

underwriting

standards

may

not

have

the

expected

effects

on

the

performance

of

the

receivables;

the

Company

may

not

be

in

a

position

to

draw

down

on

its

existing

credit

lines

or

may

be

unable

to

renew,

extend,

or

replace

such

lines

of

credit;

the

Company

may

require

new

credit

lines

to

provide

liquidity

for

its

operations,

including

facilities

to

sell

or

finance

its

notes

receivable;

the

Company

may

not

be

able

to

successfully

securitize

additional

timeshare

loans

and/or

obtain

adequate

receivable

credit

facilities

in

the

future;

risks

relating

to

pending

or

future

litigation,

regulatory

proceedings,

claims

and

assessments;

sales

and

marketing

strategies

may

not

be

successful;

marketing

costs

may

increase

and

not

result

in

increased

sales;

system-wide

sales,

including

sales

on

behalf

of

third

parties

and

sales

to

existing

owners,

may

not

continue

at

current

levels

or

they

may decrease;

fee-

based

service

initiatives

may

not

be

successful

and

may

not

grow

or

generate

profits

as

anticipated;

it

may

be

necessary

or

desirable

to

increase

capital

expenditures,

thereby

decreasing

free

cash

flow;

risks

related

to

other

financial

trends

discussed

in

this

presentation

including

that

the

Company

may

be

required

to

further

increase

its

allowance

for

loan

losses

in

the

future

and

record

additional

impairment

charges

as

a

result

of

any

such

increase;

selling

and

marketing

expenses

as

a

percentage

of

system-wide

sales

of

VOIs,

net

may

not

remain

at

current

levels

or

they

may

increase;

and

the

Company’s

indebtedness

may

increase

in

the

future;

and

the

risks

and

other

factors

detailed

in

the

Company’s

previous

SEC

filings

and

BFC’s

SEC

filings,

including

those

contained

in

the

“Risk

Factors”

sections

of

such

filings.

NOTE:

Bluegreen

Corporation’s

(“Bluegreen’s”)

financial

statements

and

all

amounts

derived

from

such

included

in

this

presentation

are

presented

on

Bluegreen’s

historical

basis

accounting.

Bluegreen’s

financial

statements

are

also

included

in

BFC

Financial

Corporation’s

(“BFC’s”)

filings

with

the

Securities

and

Exchange

Commission,

and

certain

amounts

disclosed

therein

will

differ

from

those

included

in

this

presentation

due

to

the

impact

of

certain

“purchase

accounting”

adjustments

recorded

by

BFC

in

connection

with

its

November

2009

indirect

acquisition

of

approximately

7.4

million

additional

shares

of

Bluegreen’s

Common

Stock,

which

resulted

in

BFC,

indirectly,

holding

a

controlling

interest

in

Bluegreen. |

2

Table of Contents

Company Profile

Highlights

Our Industry

Our Business

Liquidity

Appendices

A –

Other Information |

3

A leading leisure/hospitality management & marketing company with

desirable vertical integration, focused on the timeshare industry.

Founded in 1966 and entered the timeshare space in 1994, today Bluegreen

is one of the largest timeshare companies.

Bluegreen was publicly-traded from 1985

–

2013

In April 2013,

BFC Financial Corporation (OTC: BFCF) ("BFC")

completed its previously announced acquisition of Bluegreen Corporation (the

“Merger").

BFC

had

been

a

significant

Bluegreen

shareholder

since

2002

and the majority shareholder since 2009. As a result of the Merger,

Bluegreen became an indirect, wholly-owned subsidiary of BFC and BBX

Capital Corporation (NYSE: BBX), and ceased to be an SEC registrant.

Core product is the flexible, points-based Bluegreen Vacation Club.

Strong emphasis on customer experience; attractive demographic profile.

This platform supports three source of revenues:

Traditional timeshare business

Growing fee-based services business

Finance business

Company Profile |

4

Highlights

Operating model features improvements from historical, capital-intensive

timeshare model: “Capital light”

business model that is generating cash from multiple streams:

Growing sales while focusing on marketing efficiencies

Improving debt profile

Minimizing capital spending

Established FICO®

score –

based credit underwriting program in December 2008

Completed sale of non-core real estate business (Bluegreen Communities) in May

2012 Traditional

timeshare

sales

operations

generate

significant

cash

sales

and

currently

have

historically low

capital

requirements

Fee-based Services Business:

Fee-Based services sales & marketing commissions

Property management, title, mortgage servicing & other Fee-Based services

Finance business income |

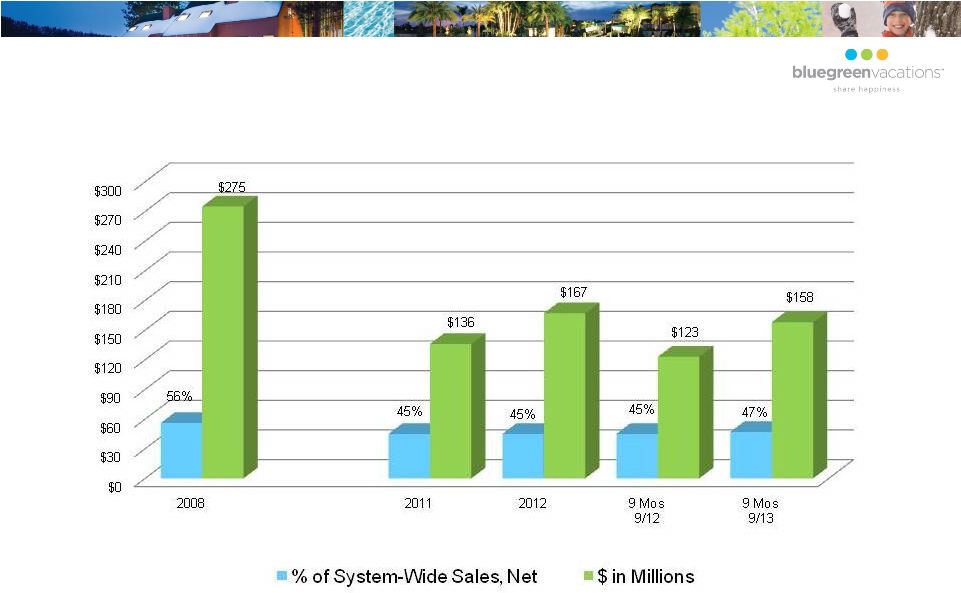

5

Highlights (cont.)

Generated

free

(1)

cash

flow

of

$71

million

during

YTD

September

2013.

Increased

cash

realized

within

30

days

of

sale

from

24%

of

sales

in

2008,

to

54%

in

YTD

September

2013.

The

“capital-light”

fee-based

service

business

model

generated

$46

million

in

pre-tax

profits

(2)

in

YTD

September

2013.

Receivable-backed

debt

decreased

41%

to

$442

million

at

September

30,

2013

from

$748

million

at

December

31,

2008.

Lines-of-credit

and

notes

payable

declined

61%

to

$88

million

as

of

September

30,

2013

from

$223

million

as

of

December

31,

2008.

Capital

expenditures

(3)

decreased

from

$188

million

in

2008

to

$23

million

in

YTD

September

2013.

(1)

Cash flow from operating and investing activities

(2)

Before corporate overhead and finance profits

(3)

Excludes

spending

for

inventory

obtained

under

“just-in-time”

fee-based

service

arrangements. |

6

Highlights (cont.)

Associate

headcount

decreased

26%

from

6,396

as

of

9/30/08

to

4,747

as

of

9/30/13.

Revolving

credit

facilities

of

$240

million

with

availability

of

$134

million

as

of

December

31,

2013.

Recent

transactions

in

credit

and

securitization

markets

(including

Merger

financing

of

$75

million

and

$110.6

million

securitization).

Unrestricted

cash

and

equivalents

of

$135

million

as

of

September

30,

2013.

Sales

to

Bluegreen

Vacation

Club

owners

represented

56%

of

total

Resort

sales

in

YTD

September

2013,

indicating

a

high

level

of

customer

satisfaction

and

providing

a

lower

cost

marketing

channel. |

7

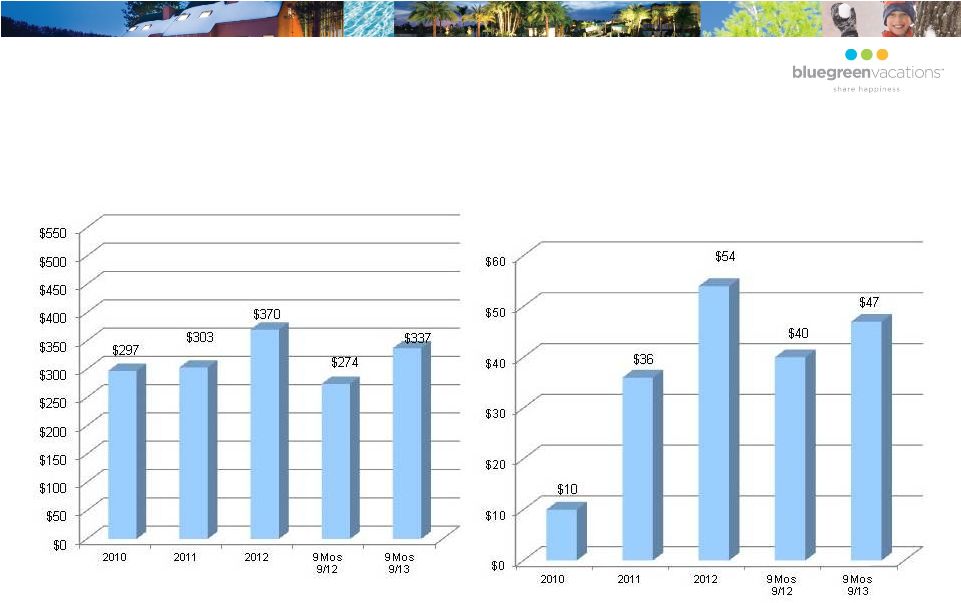

System Wide VOI Sales, Net (a)

(a) Excludes estimated uncollectible VOI notes receivable. Includes sales made

on behalf of fee-based service clients. Income from Continuing Operations

(b) ($ in millions)

($ in millions)

(b) Net of income taxes.

Results of Operations |

8

Timeshare Industry

2012

U.S.

Timeshare

sales

of

approximately

$6.9

billion

(up

6%).

Highest

one-year

sales

growth

since

2006.

Other

participants

include:

Wyndham,

Marriott,

Starwood,

Hilton,

Hyatt,

Disney,

Diamond,

Orange

Lake

and

Silverleaf.

Increased

activity

in

the

industry

in

corporate

transactions,

consolidation

and

ongoing

affiliation

through

Fee-Based

Service

arrangements. |

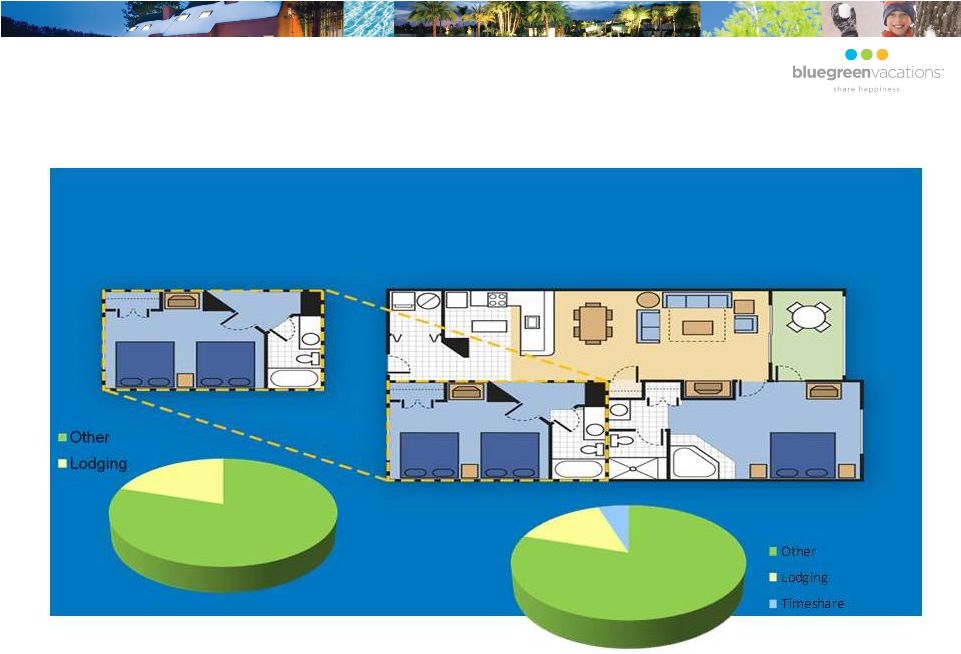

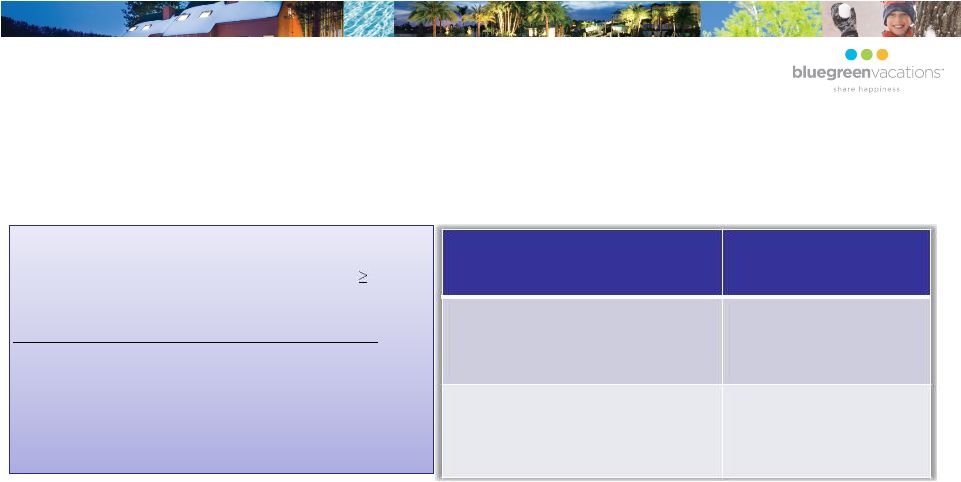

9

Why not just rent?

Hotel Room vs. Timeshare Vacation Home

Typical Hotel Room

Typical Bluegreen Vacation Villa

Lifetime Budget

Lifetime Budget |

10

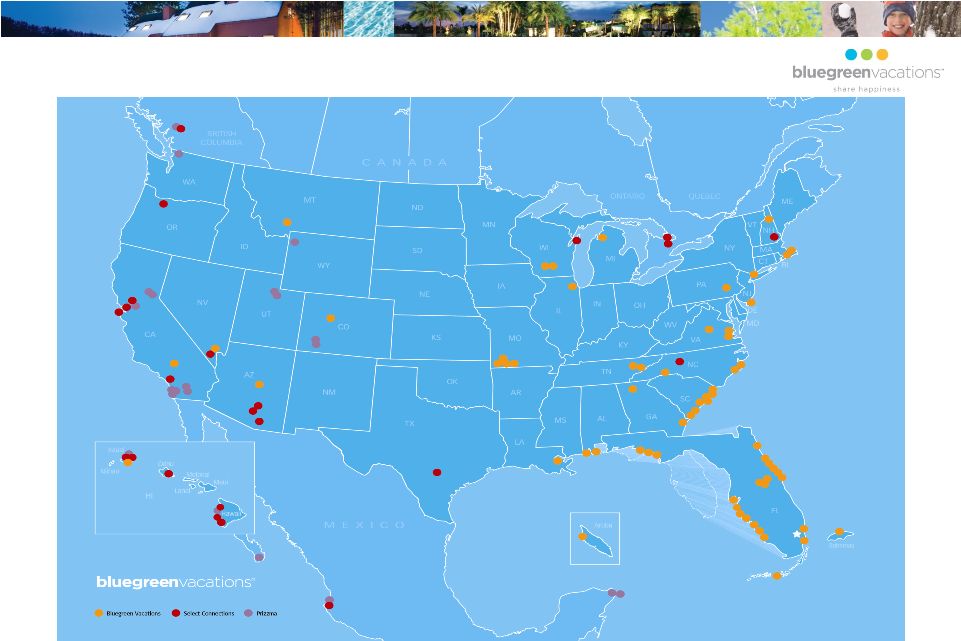

Bluegreen Vacations

Vacation Ownership Interests (real estate) sold

through points-based Bluegreen Vacation Club®.

More than 176,000 owners in the Bluegreen

Vacation Club and over 237,000 owners under

management as of September 30, 2013.

64 in-network resorts.

Access to 23 Shell Vacation Club Resorts through

“Select Connections”

partnership.

Access to 21 Raintree Vacation Club Resorts

through Prizzma.

In January 2013, Bluegreen Vacations was

named the “Official Vacation Ownership Provider

of Choice Hotels”. |

11

Bluegreen Vacation Club

Vacation Ownership with Flexibility, Quality and Value

Since 1994

Owners get the flexibility

of a points-based reservation system, not an internal exchange.

Note: All subject to terms and conditions of the Bluegreen Vacation Club.

|

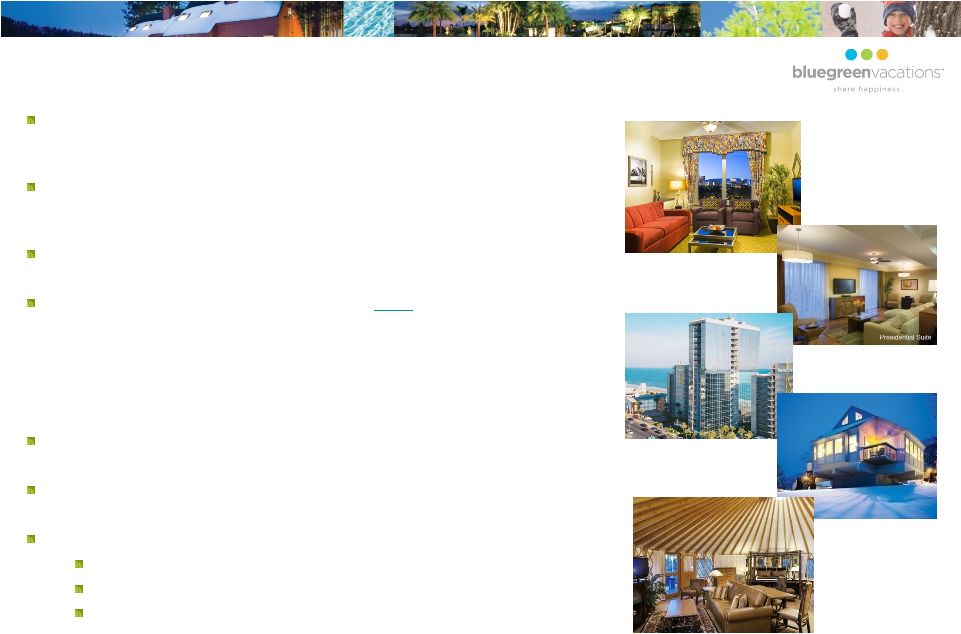

12

Bluegreen Vacation Club Resorts |

13

Mountain Run at Boyne, Boyne Falls Michigan

Club 36, Las Vegas, Nevada

Grande Villas at World Golf Village, St. Augustine,

Florida The Fountains, Orlando, Florida

Bluegreen Vacation Club Resorts |

14

La Cabana , Oranjestad, Aruba

The Club at Big Bear, Big Bear lake, California

Wilderness Club at Big Cedar, Ridgedale, Missouri

Shenandoah Crossing, Gordonsville, Virgina

Bluegreen Vacation Club Resorts |

15

•

Average income: $75,000 -

$80,000

•

Age: 44-55

•

Marital Status: Married

•

Number of persons per vacation ownership trip: 2.8

•

Number of nights per stay: 4.3

Typical Bluegreen Owner |

16

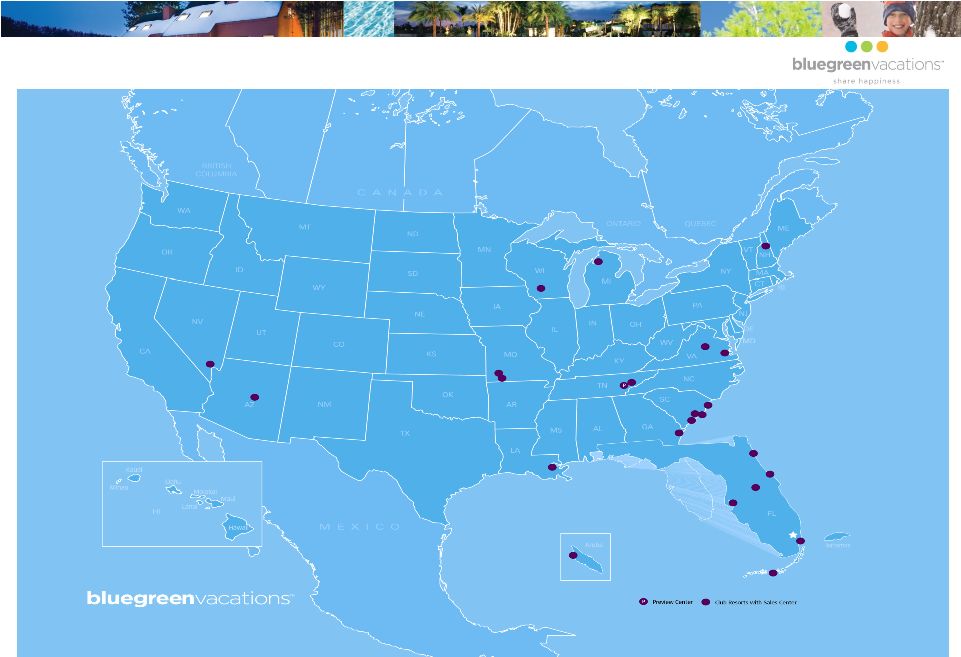

Bluegreen Sales Centers |

17

Experienced Direct Marketer

Over 161,000

Sales Tours

In YTD September 2013

Approximately 28,500

Sales

In YTD September 2013

17.7%

Conversion |

18

Selling and Marketing Expenses |

19

Fee-Based Services

•

We provide various timeshare services and product offerings for third-party

property owners/developers, lenders and investors.

•

Services are based on Bluegreen’s core competencies in:

–

Sales & Marketing

–

Property Management

–

Risk Management

–

Title & Escrow

–

Design & Development

–

Mortgage Servicing

•

Allows third-party property owners/developers to benefit from the Bluegreen

Vacation Club product and sales distribution platform.

•

Two types of Sales & Marketing Arrangements:

–

Commission-Based

–

Just-in-Time

•

Cash business, which requires little, if any, capital expenditure/debt by

Bluegreen. •

Expands the offerings of the Bluegreen Vacation Club. |

20

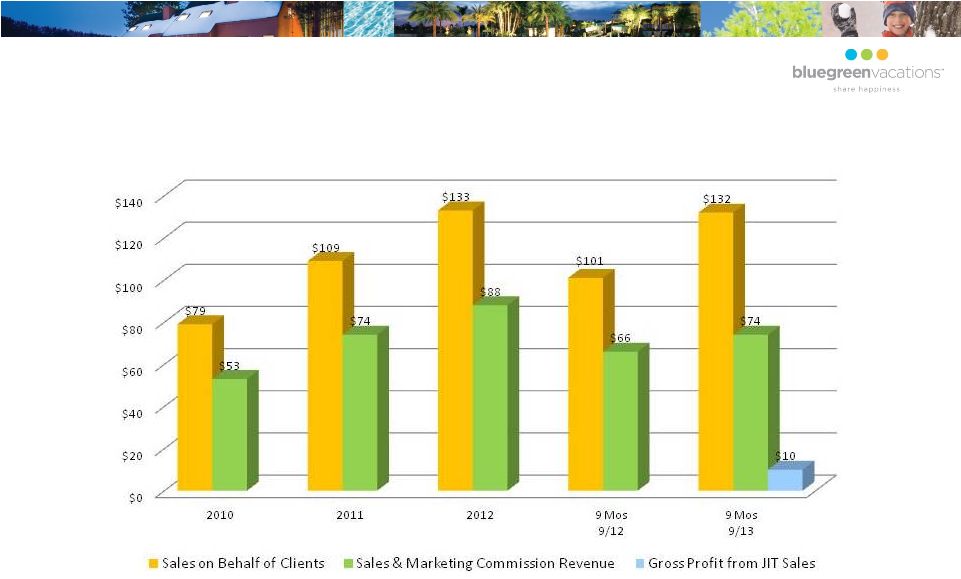

Fee-Based Services-Sales

($ in millions) |

21

Other Fee-Based Services

($ in millions) |

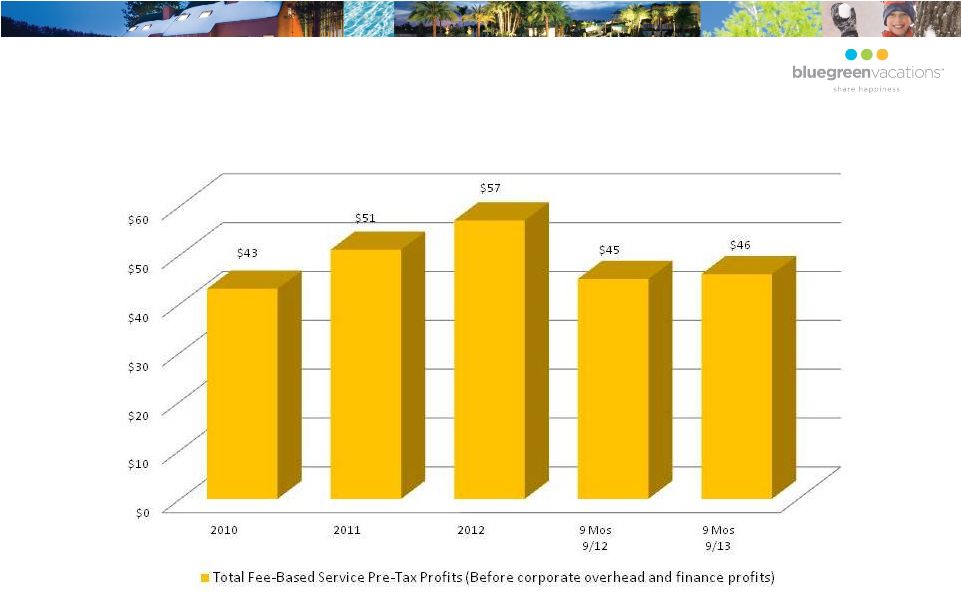

22

Fee-Based Services-Profits

($ in millions) |

23

Provides seller-financing to

FICO®

score credit qualified

Bluegreen timeshare customers to

facilitate sales and earn net interest

profits.

In-house servicing of all

Bluegreen receivables and certain

fee-based service clients; centralized

at our Boca Raton, FL headquarters.

Bluegreen has been servicing

loans for over 20 years. Our

Mortgage management team has a

combined 159 years of servicing

experience, with an average tenure

of 15 years with Bluegreen.

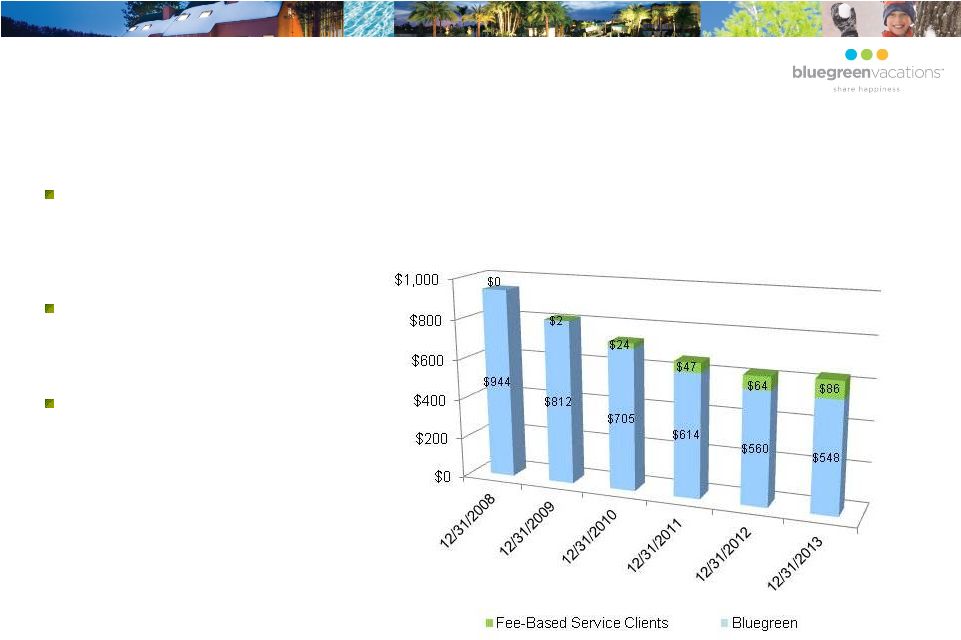

Resorts Notes Receivable Outstanding (update)

($ in millions)

Finance Business |

24

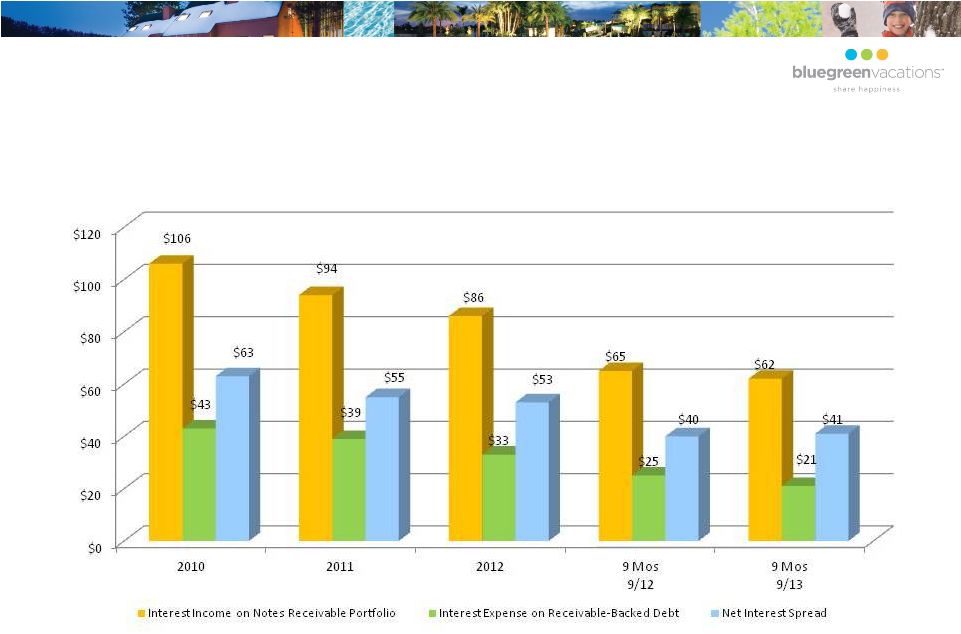

($ in millions)

Finance Operations –

Net Interest Spread |

25

Bluegreen Resorts

Credit Underwriting Standards

(FICO® Scores at time of

Origination) 300-499

300-574

500-599

575-599

300-850

600-850

600-850

300

350

400

450

500

550

600

650

700

750

800

850

1994 -

12/14/08

12/15/08 -

12/31/09

1/1/10 +

10% Down Payment

20% Down Payment

100% Cash Only

Minimum Down Payments*:

* Excludes individuals with no FICO®

score, for which there are separate down payment criteria.

|

26

Bluegreen Resorts

FICO®

Profile (a)

(a) Percentage of portfolio outstanding at 12/31/10 originated in the

2008-2010 periods by FICO® strata (12/31/11 for 2011 originated

loans,12/31/12 for 2012 originated loans and 09/30/13 for YTD

September 2013 originated loans), excluding foreign obligors and other

“No FICO®”

loans in 2009 –

September 2013, which were less than 1.5% in 2009 and 2010, and

3% in 2011, 2012 and YTD September

2013. 2008 assumes strata for 10% of loans outstanding at 12/31/10, for

which no FICO® score was obtained. Based on most recent

FICO®

score in Bluegreen’s files for each obligor. |

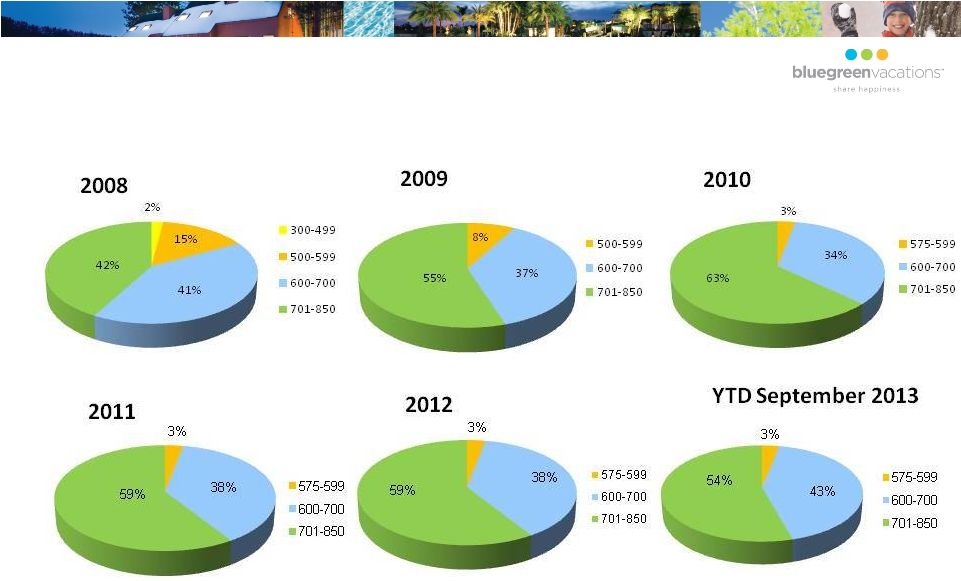

27

Original Portfolio Statistics

(1)

Loans without a FICO®

score are removed. FICO®

is at the time of sale. Excluding loans paid in full within 6 months from

origination.

VOI RATES & TERMS

NEW OBLIGORS with a FICO®

SCORE of

600

EFFECTIVE 11/01/08

Int. Rate

w/o

Down

Payment Int. Rate Auto-Debit Max Term

10%

16.99%*

17.99% 10 years

20%

15.99%* 16.99% 10 years

10%

15.99%*

16.99% 3/5/7 years 50%

9.99%

9.99% 1 year Interest

Rates *In the event a borrower goes off of pre-authorized checking, the

interest rate will increase by 1%. VOI Loans

YTD 9/30/13

Weighted Average FICO®

(Highest Obligor)

705

(1)

Weighted Average

Interest Rate

16.5% |

28

Typical Collection Process -

VOI

10 Days –

Telephone contact generally initiated on delinquent accounts when an

account is as few as 10 days past due

30

Days

–

Letter

mailed

advising

the

borrower

(if

a

U.S.

resident)

that

if

the

loan

is

not

brought

current,

the

delinquency

will

be

reported

to

the

credit

reporting

agencies

(telephone

contact

continues)

60 Days –

“Lock-out”

letter mailed, return receipt requested and regular mail,

advising that the borrower cannot use any accommodations until the delinquency is

cured (telephone contact continues)

90

Days

–

“Notice

of

Intent

to

Cancel

Membership”

mailed,

return

receipt

requested

and

regular

mail,

which

informs

the

borrower

that

unless

the

delinquency

is

cured

within

30

days,

the

borrower

will

forfeit

ownership

(telephone

contact

continues)

Approximately 120 Days –

Termination letter mailed, return receipt requested and

regular mail, advising the borrower that the owner’s beneficial rights in the

Bluegreen Vacation Club have been terminated and loan is defaulted

The VOI is placed back into inventory for resale to a new purchaser

|

29

VOI Portfolio Dynamics

*

In the event a borrower goes off of pre-authorized checking, the interest rate

will increase by 1%. Unlike floating rate residential mortgage loans (many of

which have “teaser”

rates), the monthly payment for Bluegreen’s borrowers does not

change over the life of the loan.*

The average monthly payment (approximately $200) for Bluegreen’s

borrowers is much less than a typical mortgage payment.

Geographical diversity of obligors, few foreign obligors.

Bluegreen’s VOI collections team has an average of 16 years of

collections experience. Our collectors are incentivized through a

performance-based compensation program.

Bluegreen implemented FICO®

score-based credit requirements on

12/15/08 and further raised such guidelines on 1/1/10.

|

30

Each sale facility/securitization/hypothecation has a separate, dedicated

lockbox.

There is a daily automated, repetitive wire to the paying agent/lender for each

sale facility/securitization/hypothecation.

Banking Partners in current

securitizations: Lock Box –

Bank of America

Paying Agent & Indenture Trustee –

U.S. Bank

Bluegreen VOI Loan Payment Methods

As of December 2013

PAC/ACH/Automated

90.4%

Coupon Book

9.6%

Total

100.0% |

31

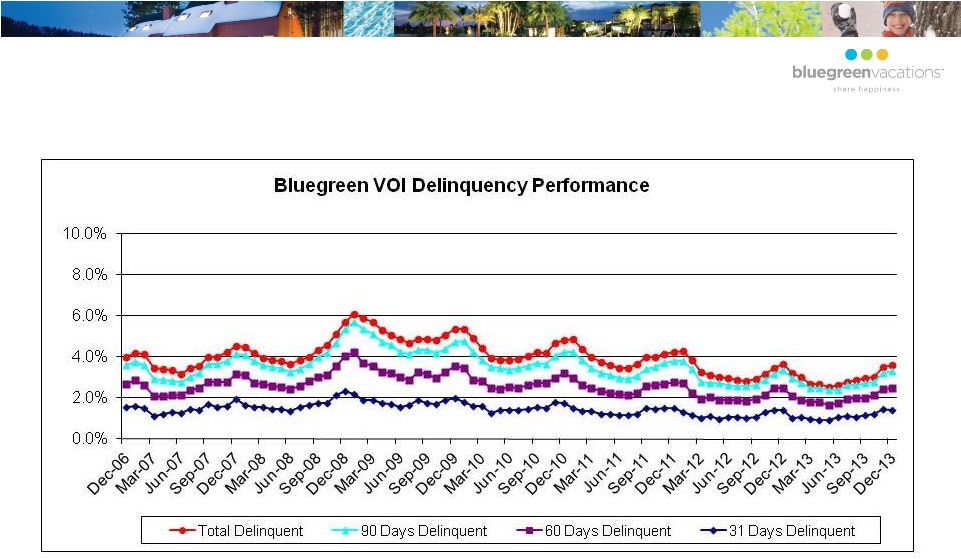

Bluegreen VOI Delinquency Performance

(1)

Excludes introductory products

Note: Loans are generally defaulted, and therefore no longer included in

delinquency, after 120 days. (1) |

32

Portfolio Performance

(1)

(1)

Excludes introductory products

(2)

Compares

cumulative

defaults

through

the

end

of

the

period

which

is

48

months

after

the

beginning

of

each

origination

year

listed.

Comparison

is

made

between

origination

year

2008

(which

was

the

last

year

that

loans

were

originated

with

no

FICO®-based

credit

underwriting

standards)

to

origination

year

2010

(the

first

year

of

the

current

FICO®-based

credit

underwriting

standards).

Percentage of

outstanding loans

Percentage of outstanding

principal balance over 30 days past due

Originations Pre-12/15/08

(loans not credit scored at origination)

37.6%

4.20%

Originations

12/15/08

–

12/31/2013

(loans

must

meet

minimum

FICO®

requirement

of

500

from

12/15/2008

–

12/31/2009;

575

thereafter)

62.4%

3.22%

Total

100%

3.59%

Non-Scored vs. Credit Scored VOI Defaults at 48 months

(2)

Percentage defaulted

Loans originated 1/1/08

–

12/14/08

23.86% (as of 12/31/11)

Loans originated 1/1/10

–

12/31/10

13.27% (as of 12/31/13)

VOI Delinquency Breakdown: As of December 31, 2013

Note: Loans are generally defaulted, and therefore no longer included in

delinquency, after 120 days. |

33

Bluegreen’s Previous Receivables Purchase

Facilities and Term Securitizations

There has never been a principal or interest payment delinquency or default under

any of these facilities. Purchase Facility/Term Securitization

Note Amount

1998 GE Purchase Facility

$100.0 MM

2000 GE Purchase Facility

$ 90.0 MM

2001-A ING Purchase Facility

$125.0 MM

2002-A Term Securitization

$170.2 MM

2004-A GE Purchase Facility

$ 38.6 MM

2004-B Term Securitization

$156.6 MM

2004-C BB&T Purchase Facility

$140.0 MM

2005-A Term Securitization

$203.8 MM

2006-A GE Purchase Facility

$125.0 MM

2006-B Term Securitization

$139.2 MM

2007-A Term Securitization

$177.0 MM

2008-A Term Securitization

$ 60.0 MM

BXG Legacy 2010 Securitization

$ 27.0 MM

2010-A Term

Securitization

$107.6 MM

Quorum Federal Credit Union Purchase Facility

$ 30.0 MM

2012-A Term Securitization

$100.0 MM

2013-A Term Securitization

$110.6 MM

2013 BB&T/DZ Bank Purchase Facility

$ 80.0 MM

Total

$ 2.0 Billion |

34

Liquidity: Cash Flow Activities

($ in millions)

2010

2011

2012

9 Mos 9/2012

9 Mos 9/2013

Cash Flow provided by operating

activities

$164

$167

$168

$115

$80

Cash Flow provided by (used in)

investing activities

(6)

(4)

22

23

(9)

Cash Flow used in financing activities

(156)

(154)

(117)

(119)

(90)

Net increase (decrease) in cash and

cash equivalents

$2

$9

$73

$19

$(19)

Ending unrestricted cash balance

$72

$81

$154

$100

$135 |

35

Revolving Credit Facilities

($ in thousands)

December 31, 2013

A.

Non-recourse (except for representations and warranties).

B.

Amount outstanding includes $4.2 million from an associated inventory loan with

same lender. Lender

Type

Facility

Amount

Amount

Outstanding

Amount

Available

Revolving Advance

Period Expiration

Maturity

BB&T/DZ Bank

Receivables Purchase Facility

12/17/2014

12/17/2017

$80,000

-------

$80,000(A)

Quorum

Receivables Purchase Facility

3/31/2014

12/30/2030

30,000

23,775

6,225(A)

Liberty

Receivable Hypothecation Facility

11/30/2015

11/30/2018

50,000

19,756

30,244

CapitalSource

Receivable Hypothecation Facility

9/20/2016

9/20/2019

40,000

24,851

15,149(B)

NBA

Receivable Hypothecation Facility

10/10/2015

4/10/2021

30,000

28,505

1,495

NBA

Inventory Facility

12/13/2016

12/13/2018

10,000

9,544

456

$240,000

$133,569 |

36

Contractual Debt Maturities

As of September 30, 2013

($ in millions)

(A) Net of Legacy Discount

Less Than

1-3

4-5

After 5

Debt

1 Year

Years

Years

Years

Balance

Receivable Backed Notes (Recourse)

$-

$3

$18

$35

(A)

$56

Lines of Credit & Notes Payable

8

24

21

35

88

Jr Subordinated Debentures

-

-

-

111

111

Subtotal –

Recourse Debt

8

27

39

181

255

Non-

Recourse Receivable –

Backed Notes

-

5

-

381

386

Total

$8

$32

$39

$562

$641 |

37

Balance Sheet

($ in thousands)

September 30, 2013

December 31, 2012

Assets

(unaudited)

Cash and cash equivalents,

unrestricted

$ 134,681

$ 153,662

Cash and cash equivalents, restricted

84,698

54,335

Notes receivable, net

470,198

480,865

Inventory, net

266,346

274,006

Property and equipment, net

72,508

68,975

Prepaid Expenses and Other assets

62,662

47,799

Total assets

$1,091,093

$1,079,642 |

38

Balance Sheet (cont.)

($ in thousands)

(a)

Reflects

payments

to

public

shareholders

of

$89.2

million

in

connection

with

the

Merger

and

payment

of

$38

million

of

dividends.

September 30, 2013

December 31, 2012

Liabilities and Shareholder’s Equity

(unaudited) Accounts payable & accrued

liabilities

$ 81,990

$ 81,970

Deferred income

31,912

27,679 Deferred income taxes

66,303

42,663 Receivable - backed debt :

Non-recourse

385,752

356,015 Recourse

56,100

89,640 Lines-of-credit and notes payable

88,445

21,551 Junior subordinated debentures

110,827

110,827 Total liabilities

821,329

730,345 Non-controlling interest

48,060

37,919 Bluegreen shareholder’s equity

(a)

221,704

311,378 Total shareholders’ equity

269,764

349,297

Total liabilities and shareholder’s equity

$

1,091,093

$ 1,079,642

|

39

Income Statements

($ in millions)

(a)

Unaudited

(b)

Sales of Bluegreen's inventory only, net of estimated uncollectible VOI notes

receivable. Nine Months Ended

(a)

Year Ended

9/2013

9/2012

2012

201

Sales of VOIs

(b)

$197

$152

$208

$16

Fee-based sales commission revenue

74

66

88

7

Other fee-based services revenue

61

57

75

7

Interest income and other

63

66

87

9

396

341

458

40

Cost of VOIs sold

35

31

40

4

Cost of other resort fee-based services

38

35

46

5

Selling, general and administrative expenses

223

179

247

19

Interest expense

29

33

42

5

Other expense, net

-

-

-

324

278

375

34

Pre-tax income from continuing operations

71

62

83

5

Provision for income taxes

24

22

29

2

Income from continuing operations

$47

$40

$54

$3

|

40

Appendix A:

Other Information |

41

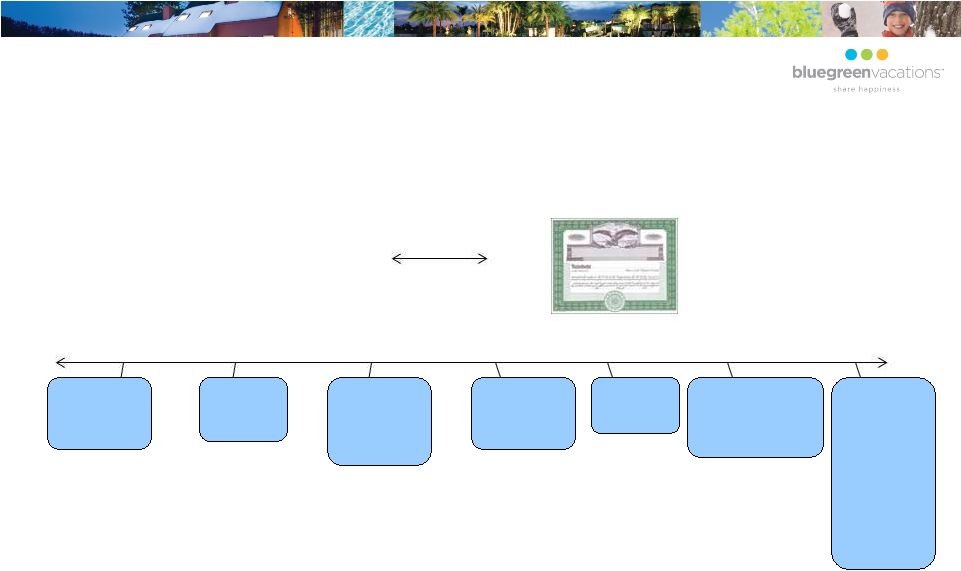

BFC and BBX’s Ownership History of Bluegreen

$10.00 per

share cash

1 Share

of Bluegreen

4/2002

38%

2002-2009

dilution to

28%

11/2009

52%

2012 seeking to

go to 100% for

$10.00 per

share cash

5/2002

Chairman

Vice

Chairman

<2002

0% -

4.9%

4/2013

Completed

merger

resulting in

BFC’s 54%

and BBX’s

46%

beneficial

interest in

BXG |

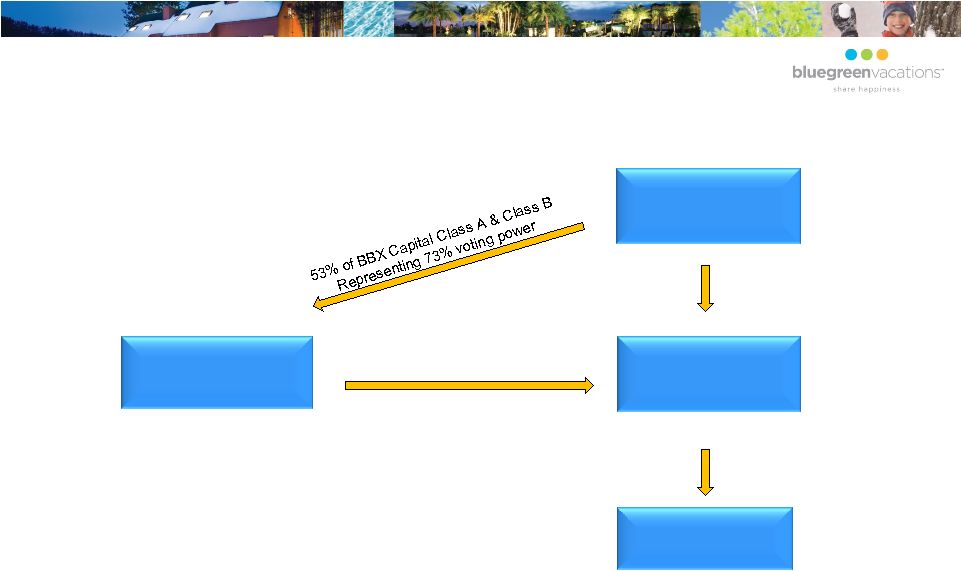

42

Bluegreen Corporation

Woodbridge Holdings,

LLC

BFC Financial

Corporation

(OTC: BFCF)

54%

46%

100%

BBX Capital Corporation

(NYSE: BBX)

Completed Merger with BFC |

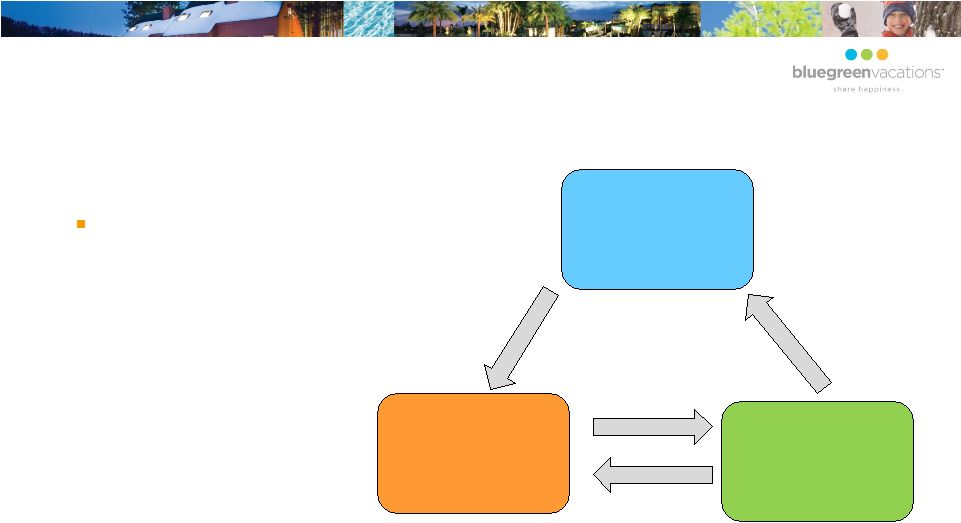

43

Unique Club Configuration

Bluegreen Vacation Club-

‘Trust’

architecture allows

for the retention of voting

rights once inventory is

sold, perpetual

management control, and

allows for recovery of the

underlying collateral for

non-performing consumer

loans or assessments

without necessity of

judicial process.

Purchaser

Bluegreen /

3

rd

Party

Developer

Vacation

Club Trust

1.

Promissory Note

2.

Deed To VOI

3.

Mortgage

4.

Owner Beneficiary Rights

1

2

3

4 |

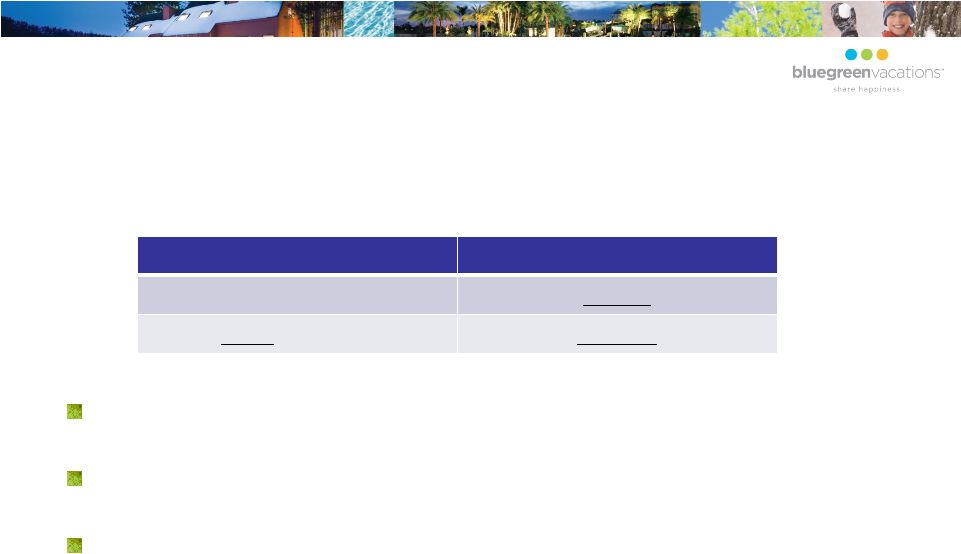

44

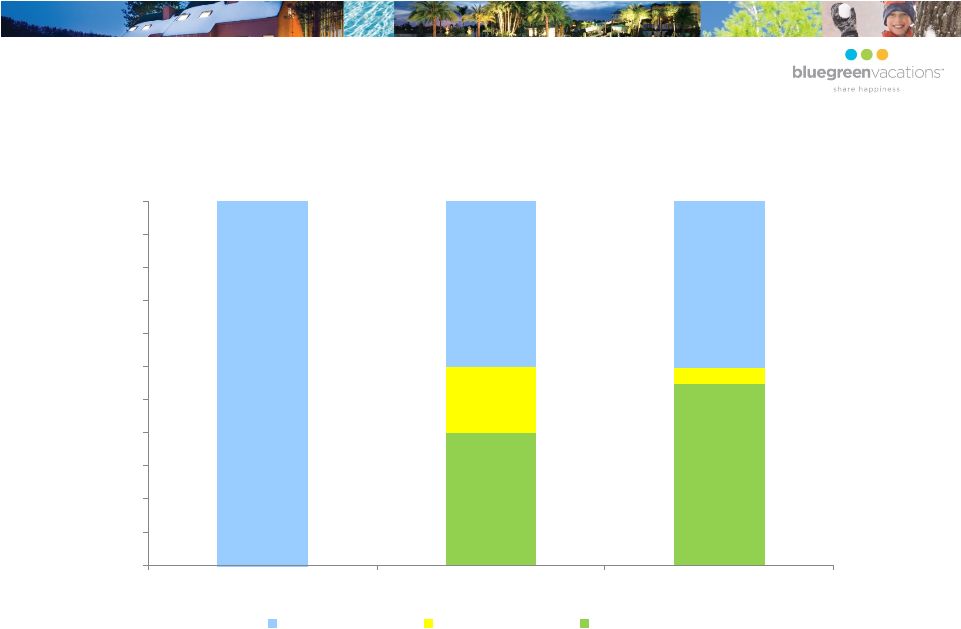

Realized Cash vs Receivables at

Point of Sale

(as a percentage of sales)

(1) Includes both 100% cash sales and down payments.

58%

42%

2011

Sales realized

in 30 days (1)

Sales that

become a

receivable

53%

47%

2012

Sales realized

in 30 days (1)

Sales that

become a

receivable

24%

76%

2008

Sales realized

in 30 days (1)

Sales that

become a

receivable

45%

55%

2009

Sales realized

in 30 days (1)

Sales that

become a

receivable

54%

46%

2010

Sales realized

in 30 days (1)

Sales that

become a

receivable

54%

46%

YTD Steptember 2013

Sales realized

in 30 days (1)

Sales that

become a

receivable |

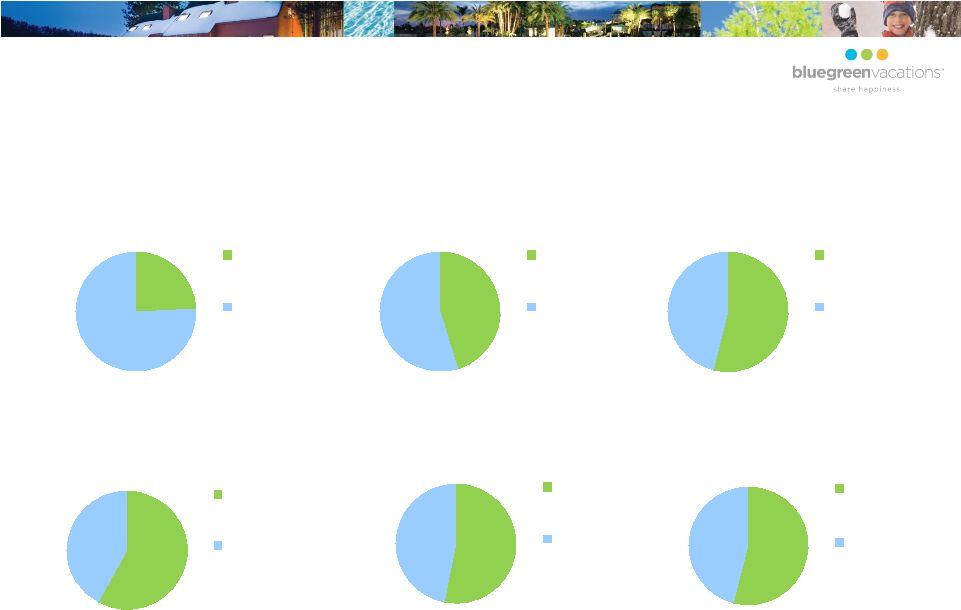

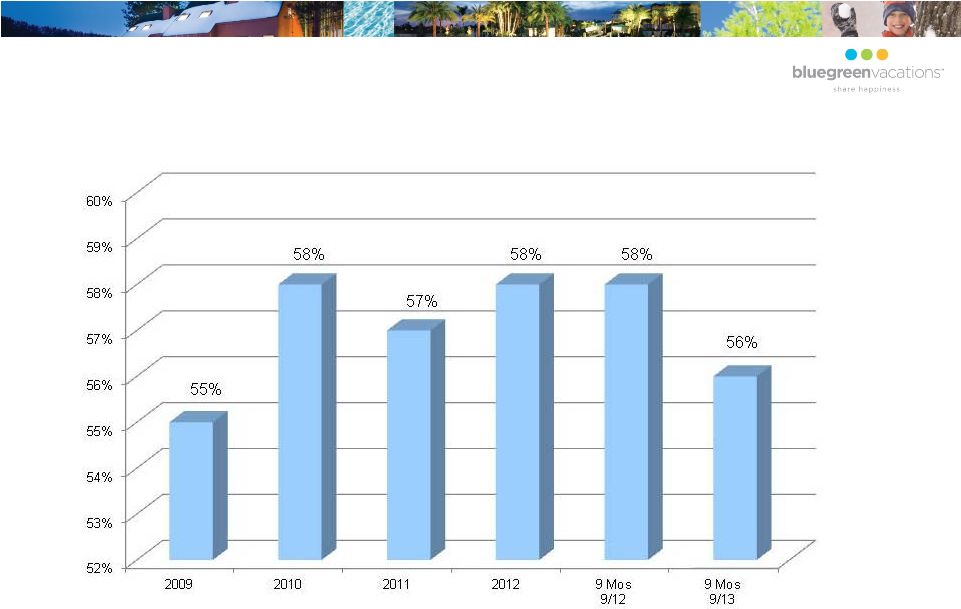

45

Sales to Existing Owner Base

( As a % of system-wide sales, which include sales on behalf of third

parties) |

46

How Bluegreen VOI Buyers Finance Their Purchase

*Dollar amount rounded to the nearest whole dollar.

**Note: Based on average household income of $80,000 for timeshare buyers.

Purchase Price of a Typical Vacation Ownership Interest:

$13,200 100%

Cash Down Payment:

($ 1,320) (10%)

Amount Financed:

$11,880 90%

Terms of Typical Financing:

Term / Amortization:

10 years

Fixed Interest Rate:

16.99%

Monthly Payment:

$ 206*

Approx. Annual Maintenance Fee/ Club Dues:

$ 809

Annual Cost During Financing Period:

$ 3,286* (4.1% of Income**)

Annual Cost After Financing Period:

$ 809 (1.0% of Income**)

|