Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Unum Group | d643202d8k.htm |

2014 Outlook Meeting

December 16, 2013 | New York

Exhibit 99.1 |

2

Safe Harbor Statement and Non-GAAP Financial Measures

Certain information in this presentation may be considered "forward-looking statements"

within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking

statements are those not based on historical information, but rather relate to our outlook, future

operations, strategies, financial results, or other developments. Forward-looking statements

speak only as of the date made. We undertake no obligation to update these statements, even if

made available on our website or otherwise. These forward-looking statements are subject to

numerous assumptions, risks, and uncertainties, many of which are beyond our control. We caution readers that the following factors, in addition to other factors mentioned from time to

time, may cause actual results to differ materially from those contemplated by the forward-looking

statements: (1) unfavorable economic or business conditions, both domestic and foreign; (2)

sustained periods of low interest rates; (3) fluctuation in insurance reserve liabilities and claim payments due to changes in claim incidence, recovery rates, mortality rates, and offsets

due to, among other factors, the rate of unemployment and consumer confidence, the emergence of new

diseases, epidemics, or pandemics, new trends and developments in medical treatments, the

effectiveness of claims management operations, and changes in government programs; (4) legislative, regulatory, or tax changes, both domestic and foreign, including the

effect of potential legislation and increased regulation in the current political environment; (5)

investment results, including, but not limited to, changes in interest rates, defaults, changes in

credit spreads, impairments, and the lack of appropriate investments in the market which can be

acquired to match our liabilities; (6) effects of business disruption or economic contraction

due to disasters such as terrorist attacks, cyber attacks, other hostilities, or natural catastrophes,

including any related impact on the value of our investment portfolio, our disaster recovery

systems, cyber or other information security systems, and business continuity planning; (7)

ineffectiveness of our derivatives hedging programs due to changes in the economic environment,

counterparty risk, ratings downgrades, capital market volatility, changes in interest rates, and/or regulation; (8) increased competition from other insurers and financial services

companies due to industry consolidation or other factors; (9) changes in our financial strength and

credit ratings; (10) damage to our reputation due to, among other factors, regulatory

investigations, legal proceedings, external events, and/or inadequate or failed internal controls and

procedures; (11) actual experience that deviates from our assumptions used in pricing,

underwriting, and reserving; (12) actual persistency and/or sales growth that is higher or lower than

projected; (13) changes in demand for our products due to, among other factors, changes in

societal attitudes, the rate of unemployment, consumer confidence, and/or legislative and regulatory changes, including healthcare reform; (14) effectiveness of our risk

management program; (15) the level and results of litigation; (16) changes in accounting standards,

practices, or policies; (17) fluctuation in foreign currency exchange rates; (18) ability to

generate sufficient internal liquidity and/or obtain external financing; (19) availability of

reinsurance in the market and the ability of our reinsurers to meet their obligations to us; (20)

recoverability and/or realization of the carrying value of our intangible assets, long-lived

assets, and deferred tax assets. For further discussion of risks and uncertainties which could cause

actual results to differ from those contained in the forward-looking statements, see Part 1, Item

1A of our annual report on Form 10-K for the year ended December 31, 2012. All

subsequent written and oral forward-looking statements attributable to us or any person acting on

our behalf are expressly qualified in their entirety by these cautionary statements.

In analyzing performance, Unum sometimes uses non-GAAP financial measures that differ from what is

reported under GAAP. This presentation contains non-GAAP financial measures,

including operating earnings per share, operating return on equity, book value per share (excluding

accumulated other comprehensive income, or AOCI), and before tax operating earnings

(BTOE). Please refer to the Appendix for a reconciliation of the non-GAAP financial measures

used in this presentation to the most directly comparable GAAP measures. |

3

Today’s Participants

Business Segment Presidents

Peter O’Donnell

President and Chief Executive Officer, Unum UK

President and Chief Executive Officer, Unum US

Mike Simonds

Jack McGarry

President and Chief Executive Officer, Closed Block

Randy Horn

President and Chief Executive Officer, Colonial Life

Rick McKenney

President and Chief Executive Officer

Tom Watjen

Kevin McCarthy

Executive Vice President and Chief Financial Officer

Executive Vice President and Chief Operating Officer

|

4

Introduction

State of the Business

Financial Performance

Unum US

Unum UK

Colonial Life

Closed Block

Investment Performance

2014 Outlook

Closing Comments

Agenda |

Introduction |

Introduction

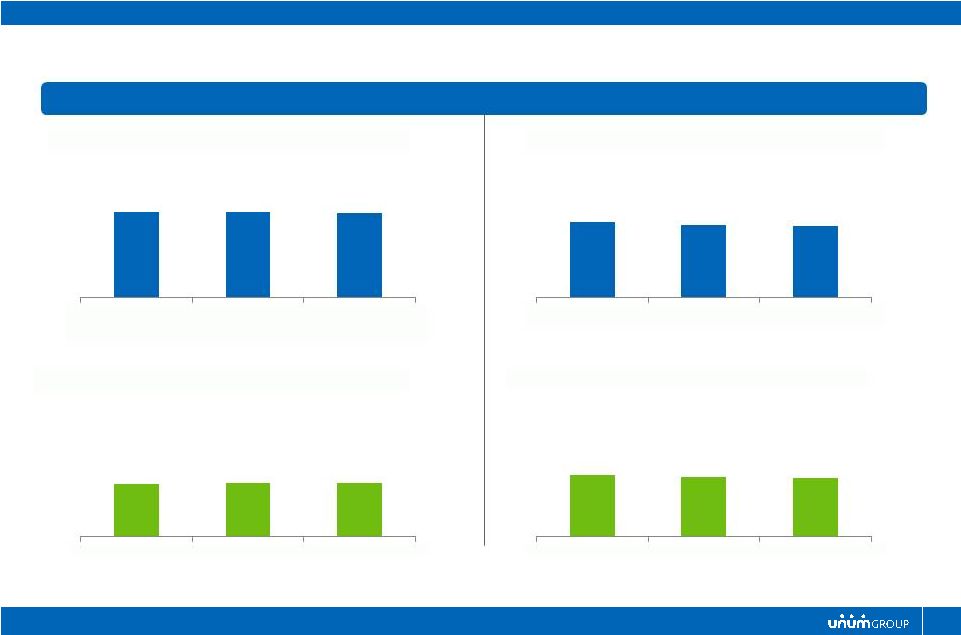

A TRACK RECORD OF DELIVERING RESULTS

$0.00

$1.00

$2.00

$3.00

$4.00

2004*

2005*

2006*

2007*

2008

2009

2010

2011

2012

2013

OPERATING EPS

7.4%

CAGR*

* Does not reflect impact of ASU 2010-26 and special items.

+3-6%

STOCK REPURCHASE HISTORY

($ millions)

$-

$200

$400

$600

$800

2004

2005

2006

2007

2008

2009

2010

2011

2012

9M13

DIVIDEND HISTORY

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

1.0%

CAGR

12.9%

CAGR

BOOK VALUE PER SHARE

(ex AOCI)

$19.37

$20.77

$20.74

$20.99

$20.84

$23.20

$25.69

$26.33

$29.55

$31.63

2004*

2005*

2006*

2007*

2008

2009

2010

2011

2012

3Q-13

9.1%

CAGR

* Does not reflect impact of ASU 2010-26 and special items.

2.7%

CAGR

6 |

7

SOLID “MACROS”

Tremendous need for basic financial protection

The workplace is the most efficient way to

educate consumers and provide simple solutions

For most consumers, if they don’t get financial

protection in the workplace, they generally don’t

get it at all

Introduction

(as of

9/30/13)

FURTHER OPPORTUNITIES FOR GROWTH

STRONG OPERATING RETURN ON EQUITY

13.1%

16.6%

12.3%

13.5%

16.8%

2.8%

Unum UK

Colonial Life

Closed Block

3Q13 YTD

Actual

Total

11.6%

Employer

Paid

46%

Employee

Paid

54%

Employer

Paid

31%

Employee

Paid

69%

WHY…

GOOD BUSINESSES

20%

12%

22%

10%

15%

34%

YTD % AVERAGE CONSOLIDATED GAAP EQUITY

A CHANGING MARKETPLACE

(% Sales* with Employee Contribution)

2003

YTD 2013

*US Sales excluding IDI-RI and LTC

Unum US

Group

Disability

Unum US

Group Life and

AD&D

Unum US

Supplemental

& Voluntary

7

Average equity excludes negative allocation of corporate deficit and will therefore not add to

100% |

8

Introduction

WHY…

A HISTORY OF TRANSPARENCY AND PROACTIVELY ADDRESSING ISSUES

8 |

Introduction

WHY…

EXPERIENCED MANAGEMENT TEAM AND HIGHLY ENGAGED EMPLOYEES

Company Leaders

*

Years

with

Unum

Years

In

Financial

Services

Tom Watjen, President & CEO

19 yrs

32 Yrs

Kevin McCarthy, Chief Operating Officer

34 Yrs

37 Yrs

Rick McKenney, Chief Financial Officer

4 Yrs

20 Yrs

Randy Horn, CEO, Colonial Life

10 Yrs

36 Yrs

Jack McGarry, CEO, Closed Block

27 Yrs

32 Yrs

Peter O’Donnell, CEO, Unum UK

3 Yrs

25 Yrs

Mike Simonds, CEO, Unum US

15 Yrs

17 Yrs

Joe Foley, SVP, Corp Marketing & PR

35 Yrs

35 Yrs

Roger Martin, CFO, US Finance

28 Yrs

28 Yrs

Tom White, SVP, Investor Relations

31 Yrs

31 Yrs

* Represents those leaders in attendance at Investor Meeting

9 |

Board Structure

•

Independence

•

Separate Chairman & CEO

•

Commitment to Diversity

92%

Yes

31%

Shareholder Rights

•

Staggered Board

•

Poison Pill

•

Say on Pay Frequency

Phasing Out

No

Annual

Compensation

•

Pay for Performance

•

Ownership Requirement

Significant alignment

SVP and above

Introduction

WHY…

SOUND CORPORATE GOVERNANCE

10 |

State of the Business |

Financial Performance |

13

Continue to expect our 2013 full year operating earnings per share growth to

be in upper half of 0% to 6% target range

Loss ratio trends continue to be generally stable

Premiums on track but sales growth slower than planned in a dynamic market

Solid capital generation and active capital management

$300+ million share repurchase

UPIL (Bermuda) re-domestication completed

12% dividend increase

Financial Performance

2013 OUTLOOK |

14

6.0%

+6%

$2.33

$2.47

9 mos -

2012

9 mos -

2013

Operating Earnings per Share

Financial Performance

PERFORMING AT HIGHER END OF OUR TARGET RANGE |

15

Financial Performance

CONSISTENTLY STRONG RETURNS

YTD 2013 Operating Return on Equity

13.1%

16.6%

12.3%

13.5%

16.8%

2.8%

Unum

US

Group Disability

Unum

US

Group Life and AD&D

Unum US

Supplemental &

Voluntary

Unum UK

Colonial Life

Closed Block

3Q13 YTD Actual

Total

11.6%

Average

equity

excludes

negative

allocation

of

corporate

deficit

and

will

therefore

not

add

to

100%

20%

12%

22%

10%

15%

34%

YTD % AVERAGE CONSOLIDATED GAAP EQUITY

(as of

9/30/13) |

16

Market Segmentation

Growth Trends in Premium Income

Financial Performance

MANAGED GROWTH IN OUR CORE BUSINESS SEGMENTS

2.6%

2.4%

5.0%

-2.4%

4Qtrs Ending 9/30/2013

Growth Markets

Unum

US

–

Core

Market

–

Employee

Benefits

Unum US –

Voluntary Benefits

Colonial Life

Unum UK –

Group LTD

Opportunistic Markets

Unum

US

–

Large

Case

–

Employee

Benefits

Unum US –

ID –

Recently Issued

Unum UK –

Group Life

Unum UK –

Supplemental and Voluntary

$4.1 billion

$2.2 billion

Opportunistic Markets

Growth Markets |

17

Benefit Ratios

Other Expense Ratios

Financial Performance

STRONG RISK EXPERIENCE AND EXPENSE DISCIPLINE

* Year to Date through September 30, 2013

72.5%

72.7%

71.6%

2011

2012

2013*

Unum US

23.2%

22.3%

22.0%

2011

2012

2013*

Unum US

51.9%

52.5%

52.5%

2011

2012

2013*

Colonial Life

18.9%

18.2%

18.0%

2011

2012

2013*

Colonial Life |

18

($ millions)

($ millions)

Financial Performance

CAPITAL GENERATION

* Statutory Net Income for traditional US Insurance Companies

†

Trailing twelve months

$574.0

$689.4

$850.3

$682.0

$741.2

$645.7

$664.0

$649.8

$740.6

-$8.2

-$64.1

-$58.3

-$141.2

-$102.0

-$16.9

-$21.1

-$25.3

-$35.6

2005

2006

2007

2008

2009

2010

2011

2012

3Q13†

After-tax Operating Income

Net Realized Investment Losses

Combined

Statutory

Net

Income

*

Capital Generation Model |

19

Re-domestication of UPIL to a U.S.-domiciled entity finalized

Off-shore Bermuda-based captive is now a U.S. regulated entity

$300 million capital contribution from holding company

Reserves in UPIL at U.S. Statutory levels consistent with Unum America

Capitalization

consistent

with

U.S.

insurance

companies

(375%

-

400%

RBC)

Financial Performance

UPIL RE-DOMESTICATION |

20

Financial Performance

ACTIVE CAPITAL DEPLOYMENT

•

YTD September 30, 2013

** Amounts in Millions

$ Amount

**

Share Repurchases (YTD)

*

$269

Dividend Payments (YTD)

*

109

Tailwind Debt Retirement (1Q-13)

63

Pension Funding (2Q-13)

53

SUBTOTAL

$494

UPIL Re-domestication

(4Q-13)

300

4Q Share Repurchases

TBD

4Q Dividends

38

TOTAL

$850-900 |

21

Financial Performance

STRONG CAPITAL POSITION

Risk Based

Capital

Holding Companies’

Cash and

Marketable Securities

Year-End 2012 Actual

396%

$805 million

9/30/13 Actual

397%

$678 million

2013 Range

375% -

400%

$500 -

$600 million |

22

(Excluding AOCI)

Financial Performance

BUILDING BOOK VALUE

9.1%

CAGR

10.4%

Book Value Per Share

Reported Book

Value per Share

$31.53

$33.20

$20.84

$23.20

$25.69

$26.33

$29.55

2008

2009

2010

2011

2012

$28.66

$31.63

9/30/2012

9/30/2013 |

23

No expected change in the overall business environment

Loss ratios are expected to remain stable

Investment environment is expected to be generally consistent

with 2

nd

half of 2013

Operating EPS growth from 5-10%

Strong capital generation and active capital deployment:

$300 to $600 million of share repurchases

Increase in dividend payout ratio

Financial Performance

2014 OUTLOOK |

Unum US |

25

Products –

Financial protection products,

including:

Long Term and Short Term Disability

Group Life and AD&D

Individual Disability and Voluntary Products

Distribution –

Broker-driven distribution

backed by robust network of field offices

and extensive home office support

Market Position

Top 3 market share position across all major

product lines

Unum US

BUSINESS SNAPSHOT

Unum US

*

Earned Premium

$4.5 billion

Before Tax Operating Income

$847 million

Operating Return on Equity

13.8%

46%

29%

25%

Premium Distribution

*

($m)

Group Disability

Group Life/AD&D

Voluntary

Supplemental &

* Information as of 12/31/2012 |

26

Our strategy is focused on expanding employee access to financial protection

benefits, broadening our employer client relationships, and building

collaborative marketplace partnerships.

We expect solid sales growth in 2014 as investments in new products and

capabilities offset marketplace headwinds.

Our business plan reflects continued investment in our strong value

proposition

while

maintaining

the

pricing

and

expense

discipline

that

has

yielded strong and predictable returns.

Unum US

2014 BUSINESS OUTLOOK |

27

Unum US

2014 KEY PRIORITIES

Consumers

Clients

Partnerships

Risk

Management

Client management strategy

Claims service and reporting

United Healthcare partnership expansion

Exchange and benefit administration connectivity

Continued new business and renewal discipline

Foundational technology investments

Voluntary product and bundling enhancements

Data-driven consumer enrollment support |

28

Sales Growth

7% to 10%

Premium Growth

0% to 2%

Op. Earnings Growth

1% to 3%

Operating ROE

12% to 14%

Unum US

2014 FINANCIAL OUTLOOK |

Unum UK |

30

Products –

Specializing in employer-paid

protection products, including:

Group Income Protection (GIP)

Group Life and Critical Illness

Sick Pay Insurance

Distribution –

Strong broker-driven

distribution backed by extensive home

office support

Recognized for many years by our

distribution partners as best provider in the

market

Market Position

#1 position in Group Income Protection

#4 position in Group Life

Unum UK

BUSINESS SNAPSHOT

Unum UK

*

Earned Premium

$695 million

Before Tax Operating Income

$131 million

Operating Return on Equity

12.2%

* Information as of 12/31/2012

59%

32%

9%

Premium Distribution

*

($m)

Group Disability

Group Life/AD&D

Supplemental &

Voluntary |

31

Focused on expanding the Group Income Protection market by partnering with

brokers to encourage employers to expand or commence providing protection

to their employees

Actions taken during 2013 will lead to higher margins in 2014, with plans

focused on:

Completing the re-pricing of the Group Life block, while expanding our Group

Income Protection proposition

Maintaining strong risk results through pricing discipline, operational

performance and the use of reinsurance where appropriate and

attractive Continuing to drive efficiencies and effectiveness through

process simplification and by leveraging group capabilities

Top line growth in 2014 constrained by market headwinds; longer term

opportunities for accelerated growth driven by the evolving political agenda

and changes in regulation

Unum UK

2014 BUSINESS OUTLOOK |

32

Unum UK

2014 KEY PRIORITIES

Distribution

Marketing

Operations

Risk

Management

Use analytics and targeted marketing to deliver awareness

campaigns to specific audiences

Enhance messages to HR and Finance Directors on the need

for financial protection

Strengthen analytical capability to maximise underwriting

competitive advantage in the marketplace

Drive process simplification to deliver enhanced broker and

customer proposition

Complete the re-pricing of the Group Life block and maintain

pricing discipline across all product lines

Maintain appropriate reinsurance arrangements where

appropriate and attractive

Maximise our relationship with existing distributors while

developing new distributors and channels

Invest in our sales organisation and solidify our position as

partner of choice for brokers |

33

Unum UK

2014 FINANCIAL OUTLOOK

Growth rates shown in GBP

Sales Growth

4% to 7%

Premium Growth

0% to 2%

Op. Earnings Growth

5% to 8%

Operating ROE

16% to 18% |

Colonial Life |

35

Products –

Exclusive focus on voluntary

benefits market, including:

Accident, Sickness & Disability

Life

Cancer & Critical Illness

Distribution –

Agency-driven distribution

that is national in scope and backed by

extensive home office support

Market Position

More than 80,000 businesses served

Over 3 million policies in force

Colonial Life

BUSINESS SNAPSHOT

61%

17%

22%

Accident, Sickness,

Disability

Voluntary Life

Cancer/Critical

Illness

Colonial

*

Earned Premium

$1.2

billion

Before

Tax Operating Income

$274 million

Operating Return on Equity

16.8%

Premium Distribution*

($m)

* Information as of 12/31/2012 |

36

Our business plan is centered on growth strategy execution, continuous

improvement, strong risk management practices, and talent development.

2014 sales growth will be primarily driven by distribution effectiveness and

opportunities in the core commercial and public sector segments.

We continue to invest in new products,

capabilities, and service offerings in

response

to

rapid

changes

in

the

market

environment

and

evolving

customer

expectations.

2014 operating earnings growth is expected to be in the 1-3% range, with

continued strong profit margins and operating ROE levels.

Colonial Life

2014 BUSINESS OUTLOOK |

37

Colonial Life

2014 KEY PRIORITIES

Distribution

Segmentation

Products &

Services

Operational

Excellence

Build out target segment capabilities

Focus on customers who value an integrated approach to

benefits counseling, enrollment, and voluntary products

Maintain a balanced product and service portfolio that

meets consumer needs and distribution requirements

Align products and services with distribution strategy

Continued emphasis on risk discipline, continuous

improvement and cross-business collaboration

Acquisition and development of talent

Continue to strengthen our sales organization

Enhance our marketing focus and delivery |

38

Colonial Life

2014 FINANCIAL OUTLOOK

Sales

Growth

4% to 7%

Premium

Growth

2% to 4%

Op. Earnings Growth

1% to 3%

Operating ROE

15% to 17% |

Closed Block |

40

Products –

Legacy block of discontinued

products, split primarily between:

Individual Disability

Long Term Care

Distribution

IDI sales discontinued in the mid-90s

ILTC sales discontinued in 2009

GLTC sales discontinued in 2011

Closed Block

BUSINESS SNAPSHOT

Closed Block

*

Earned Premium

$1.4 billion

Before Tax Operating Income

$95 million

Operating Return on Equity

2.8%

* Information as of 12/31/2012

Premium Distribution

*

($m)

Individual Disability

Long Term Care

54%

46% |

41

In 2014, we expect BTOE growth of 6-9% driven by LTC asset growth and a

slight improvement in loss ratios.

The financial performance of individual disability block is stable with

predictable run-off of premium and capital.

Investment yields will continue to be a concern for LTC as we invest at below

portfolio rates.

Our near-term expenses will increase in the closed block as we continue to

make strategic investments in our resources and infrastructure.

Continued focus on capital efficiency.

Closed Block

2014 BUSINESS OUTLOOK |

42

Closed Block

2014 KEY PRIORITIES

Operational

Effectiveness

Financial

Analysis

Rate Increases

Capital

Management

Improved analytics through new LTC actuarial platform

Use new experience analysis to drive deeper

Continue pursuit of justified rate increases

Stratify rate requests and enhance policyholder options

Implement structure changes to enhance flexibility

Keep abreast of developments in the capital markets

High quality claims management

Effective communication and implementation of approved

rate increases

understanding of underlying trends |

43

Closed Block

2014 FINANCIAL OUTLOOK

Sales Growth

NA

Premium Growth

-4% to -6%

Op. Earnings Growth

6% to 9%

Operating ROE

2% to 4% |

Investment Performance |

45

Overall credit quality remains very

strong

Minimal watch list of potential problem

credits

Immaterial losses from sales and

write-downs

3Q13 realized losses reflect active

portfolio optimization

Average credit quality remains stable

in the single-A range

Investment Performance

STRONG CREDIT QUALITY

SALES AND WRITE-DOWNS OF INVESTMENTS

SALES AND WRITE-DOWNS OF INVESTMENTS

$0

$100

$200

$300

$400

$500

$600

$700

$800

WATCH LIST

WATCH LIST

$ millions

-$300

-$200

-$100

$0

$100

2007

2008

2009

2010

2011

2012

9M13

$ millions |

46

2013 Results to Date

$3.1 billion invested

Overall portfolio yield down 15 bps to 6.32%

Interest Rate Headwinds

Investing new cash flows at lower rates

Adjustments to reserve discount rates as necessary

Mitigating Factors

Opportunistic deployment

Placement of premium rate increases

Measured reduction in interest reserve margins

Investment Performance

ENTERPRISE INTEREST RATE IMPACTS |

47

Management of Interest Margin

Pricing flexibility

Discount rate adjustments

Margin build-up during credit crisis

Manageable amount of new cash flow

to invest

Investment Performance

INTEREST

RATE

MANAGEMENT

–

UNUM

US

LTD

40

50

60

70

80

90

100

110

2004

2005

2006

2007

2008

2009

2010

2011

2012

3Q-

13

UNUM US LTD INTEREST MARGIN

TARGET RANGE

*

Interest margin is the spread between the portfolio yield and the

aggregate discount rate |

2014 Outlook |

49

Slightly more favorable sales environment

Improved premium growth; 1-3% growth for core operations

Persistency remains favorable, generally consistent with 2013

Maintaining strong margins and profitability through disciplined

pricing and risk selection

Operating EPS growth from 5-10%

We will continue to execute our capital deployment plans in 2014:

$300 to $600 million of share repurchases

Increase in dividend payout ratio

2014 Outlook

KEY MESSAGES |

50

2014 Outlook

CAPITAL OUTLOOK

Capital Management Criteria

3Q-2013

Actual

2013

Projection

2014

Projection

Risk-Based Capital Ratio for

Traditional U.S. Insurance Companies

397%

390% -

400%

375% -

400%

Holding Companies’

Cash and

Marketable

Securities

($

millions)

$678

$500 -

$600

>$500 |

51

2014 Outlook

BUSINESS SEGMENT OUTLOOK

* Consolidated After-Tax Operating Earnings including Corporate

Segment Closed Block

(4 –

6%)

6 –

9%

2 –

4%

Total Operations*

3 –

6%

10 –

12%

Capital Management

3 –

5%

0 –

1%

Total

5 –

10%

11 –

12%

Sales

Growth

Premium

Growth

Operating

Earnings

Growth

Operating

ROE

Unum US

7 –

10%

0 –

2%

1 –

3%

12 –

14%

Unum UK (£)

4 –

7%

0 –

2%

5 –

8%

16 –

18%

Colonial Life

4 –

7%

2 –

4%

1 –

3%

15 –

17%

Core Operations

5 –

9%

1 –

3%

2 –

4%

13 –

15% |

Closing Comments |

53

Good operating businesses with positive long-term trends

…and a commitment to disciplined growth

An intense focus on the management of our closed block

…consistent with our history with these types of issues

Solid financial foundation and predictable cash flow remain an asset

…leading to significant financial flexibility

We

are

confident

we

are

taking

the

actions

needed

to

continue

to

build

value

…just as we have done in the past

Closing Comments |

Closing Comments

DIVIDEND HISTORY

1.0%

CAGR

12.9%

CAGR

BOOK VALUE PER SHARE

(ex AOCI)

BOOK VALUE PER SHARE

(ex AOCI)

9.1%

CAGR

2.7%

CAGR

STOCK REPURCHASE HISTORY

($ millions)

STOCK REPURCHASE HISTORY

($ millions)

OPERATING EPS

7.4%

CAGR

*

+3-6%

$0.00

$1.00

$2.00

$3.00

$4.00

2004*

2005*

2006*

2007*

2008

2009

2010

2011

2012

2013

* Does not reflect impact of ASU 2010

-

26 and special items.

$-

$200

$400

$600

$800

2004

2005

2006

2007

2008

2009

2010

2011

2012

9M13

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

$19.37

$20.77

$20.74

$20.99

$20.84

$23.20

$25.69

$26.33

$29.55

$31.63

2004*

2005*

2006*

2007*

2008

2009

2010

2011

2012

3Q-13

* Does not reflect impact of ASU 2010-26 and special items.

A TRACK RECORD OF DELIVERING RESULTS

54 |

Questions & Answers |

Appendix

Reconciliation of Non-GAAP Financial Measures |

57

Appendix

RECONCILIATION OF NON-GAAP FINANCIAL MEASURES

2012

2011

2010

2009

2008

2007**

2006**

2005**

2004**

After-tax Operating Income

3.15

$

2.98

$

2.73

$

2.64

$

2.54

$

2.25

$

1.85

$

1.69

$

1.78

$

Net Realized Investment Gain (Loss), Net of Tax

0.13

(0.01)

0.05

-

(0.89)

(0.12)

0.01

(0.02)

0.06

Non-operating Retirement-related Loss, Net of Tax

(0.11)

(0.07)

(0.06)

(0.09)

(0.03)

(0.04)

(0.05)

(0.05)

(0.04)

Deferred Acquisition Costs and Reserve Charges for

Closed Block, Net of Tax

-

(2.04)

-

-

-

-

-

-

(2.37)

Regulatory Reassessment Charges, Net of Tax

-

-

-

-

-

(0.10)

(0.79)

(0.16)

(0.29)

Special Tax Items and Debt Extinguishment Costs

-

0.08

(0.03)

-

-

(0.10)

0.23

0.14

0.17

Other, Net of Tax

-

-

-

-

-

-

(0.04)

0.01

0.01

Income (Loss) from Continuing Operations

3.17

0.94

2.69

2.55

1.62

1.89

1.21

1.61

(0.68)

Income (Loss) from Discontinued Operations

-

-

-

-

-

0.02

0.02

0.03

(0.18)

Net Income (Loss)

3.17

$

0.94

$

2.69

$

2.55

$

1.62

$

1.91

$

1.23

$

1.64

$

(0.86)

$

* Amounts per diluted common share.

** Does not reflect the impact of ASU 2010-26.

2013

2012

2012

2011

2010

2009

2008

2007*

2006*

2005*

2004*

Total Stockholders' Equity (Book Value)

33.20

$

31.53

$

31.87

$

27.91

$

26.80

$

24.25

$

17.94

$

22.28

$

22.53

$

24.66

$

24.36

$

Net Unrealized Gain on Securities

1.64

3.24

3.23

2.11

1.31

1.16

(2.53)

0.99

1.56

3.49

4.41

Net Gain on Cash Flow Hedges

1.52

1.46

1.48

1.39

1.14

1.12

1.38

0.50

0.57

0.91

0.80

Subtotal

30.04

26.83

27.16

24.41

24.35

21.97

19.09

20.79

20.40

20.26

19.15

Foreign Currency Translation Adjustment

(0.28)

(0.29)

(0.26)

(0.41)

(0.34)

(0.23)

(0.52)

0.35

0.34

0.07

0.33

Subtotal

30.32

27.12

27.42

24.82

24.69

22.20

19.61

20.44

20.06

20.19

18.82

Unrecognized Pension and Postretirement Benefit Costs

(1.31)

(1.54)

(2.13)

(1.51)

(1.00)

(1.00)

(1.23)

(0.55)

(0.68)

(0.58)

(0.55)

Total Stockholders' Equity, Excluding Accumulated

Other Comprehensive Income

31.63

$

28.66

$

29.55

$

26.33

$

25.69

$

23.20

$

20.84

$

20.99

$

20.74

$

20.77

$

19.37

$

* Does not reflect impact of ASU 2010-26 and special items.

Year Ended December 31*

September 30

December 31

(per share) |

58

Appendix

RECONCILIATION OF NON-GAAP FINANCIAL MEASURES

After-Tax

Average

Annualized

Operating

Allocated

Operating

Income (Loss)

Equity

Return

On Equity

Nine Months Ended September 30, 2013

Unum US

Group Disability

151.0

$

1,534.9

$

13.1%

Group Life and Accidental Death and Dismemberment

113.2

907.2

16.6%

Supplemental and Voluntary

156.6

1,694.2

12.3%

Total Unum US

420.8

4,136.3

13.6%

Unum UK

74.8

737.5

13.5%

Colonial Life

140.1

1,112.5

16.8%

Closed Block

54.2

2,548.2

2.8%

Corporate

(31.2)

(943.1)

Total

658.7

$

7,591.4

$

11.6%

Twelve Months Ended December 31, 2012

Unum US

Group Disability

193.0

$

1,495.6

$

12.9%

Group Life and Accidental Death and Dismemberment

143.8

890.6

16.2%

Supplemental and Voluntary

218.5

1,637.9

13.3%

Total Unum US

555.3

4,024.1

13.8%

Unum UK

99.2

811.2

12.2%

Colonial Life

178.3

1,064.4

16.8%

Closed Block

62.3

2,234.2

2.8%

Corporate

(7.6)

(892.1)

Total

887.5

$

7,241.8

$

12.3%

(in millions) |

59

Appendix

RECONCILIATION OF NON-GAAP FINANCIAL MEASURES

December 31

2013

2012

(in millions)

per share *

(in millions)

per share *

(in millions)

After-tax Operating Income

658.7

$

2.47

$

662.5

$

2.33

$

887.5

$

Net Realized Investment Gain (Loss), Net of Tax

(1.9)

(0.01)

20.7

0.07

37.1

Non-operating Retirement-related Loss, Net of Tax

(19.9)

(0.08)

(22.7)

(0.08)

(30.2)

Net Income

636.9

$

2.38

$

660.5

$

2.32

$

894.4

$

* Amounts per diluted common share.

September 30

2013

2012

2011

Total Stockholders' Equity, As Reported

8,669.9

$

8,612.6

$

8,169.7

$

Net Unrealized Gain on Securities

427.4

873.5

614.8

Net Gain on Cash Flow Hedges

397.2

401.6

408.7

Total Stockholders' Equity, As Adjusted

7,845.3

$

7,337.5

$

7,146.2

$

Average Equity, As Adjusted

7,591.4

$

7,241.8

$

December 31

2012

(in millions)

Operating Income (Loss) by Segment

Unum US

847.1

$

Unum UK

131.3

Colonial Life

274.3

Closed Block

95.5

Corporate

(108.5)

Total Before Tax Operating Earnings

1,239.7

Net Realized Investment Gain

56.2

Non-operating Retirement-related Loss

(46.4)

Income Tax

(355.1)

Net Income

894.4

$

December 31

(in millions)

2012

Nine Months Ended September 30 |