Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Vantage Drilling CO | d644409d8k.htm |

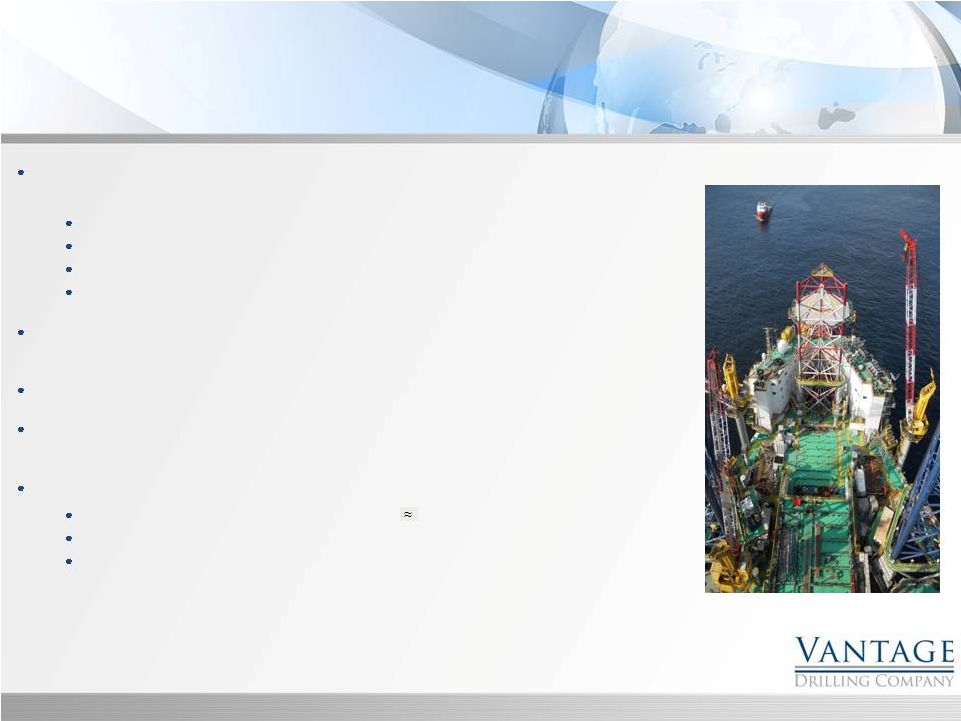

Vantage Drilling Company

Wells Fargo 2013 Energy Symposium

New York

December 11, 2013

Exhibit 99.1 |

Some of the statements in this presentation constitute

forward-looking statements. Forward-looking statements relate to

expectations,

beliefs,

projections,

future

plans

and

strategies,

anticipated

events

or

trends

and

similar

expressions

concerning

matters that are not historical facts. The forward looking

statements contained in this presentation involve risks and

uncertainties as well as statements as to:

•

our limited operating history;

•

availability of investment opportunities;

•

general volatility of the market price of our securities;

•

changes in our business strategy;

•

our ability to consummate an appropriate investment opportunity within

given time constraints; •

availability of qualified personnel;

•

changes in our industry, interest rates, the debt securities markets

or the general economy; •

changes in governmental, tax and environmental regulations and similar

matters; •

changes in generally accepted accounting principles by

standard-setting bodies; and •

the degree and nature of our competition.

The forward-looking statements are based on our beliefs,

assumptions and expectations of our future performance, taking

into account all information currently available to us. These

beliefs, assumptions and expectations can change as a result of

many possible events or factors, not all of which are known to us or

are within our control. If a change occurs, our business,

financial condition, liquidity and results of operations may vary

materially from those expressed in our forward-looking

statements.

Forward-Looking Statements

2 |

Symbol:

VTG (NYSE MKT)

Location:

Houston (Headquarters), Singapore, Dubai

Market

Cap:

$551

million

($1.82

per

share)

Enterprise

Value:

$3.5

billion

Employees:

> 1,100

Contract Backlog:

approximately $3.1 billion

Owned Fleet:

4 Ultra-Premium Jackups (operating in SE Asia & West

Africa) 3 Ultra-Deepwater Drillships (operating offshore

India, GOM & SE Asia) 1

Ultra-Deepwater

Drillship

(under

construction

–

Q3

2015

delivery)

Managed Fleet:

1 Ultra-Deepwater Drillship (under construction)

2 Ultra-Premium Jackups (one operating; one preparing for

commencement) 2 Ultra-Premium Jackups (under

construction) Corporate Overview

3 |

Took

delivery

of

UDW

drillship

Tungsten

Explorer

on

July

11,

2013.

Commenced

operations

on

first contract September 20, 2013.

Contracted 50 days in Myanmar

Contracted 120 days in Malaysia

Contracted 45 days in Gabon

Contracted 2 years (plus 4 x 6-month options) in Congo (Moho Nord

Development) Sapphire Driller

contracted for 18-month contract in West Africa plus

options. Commencement early November.

Ordered

Cobalt

Explorer

–

Ultra-deepwater

drillship;

August

2015

delivery

Vantage

hired

as

construction

manager

for

two

“V

Ships”

Ultra-Deepwater

Drillships

to

be

constructed at DSME shpyard.

Refinanced Balance Sheet

with –

Lowered

borrowing

costs

about

460

BPS

saving

$90

million/year

in

interest

Much longer and staggered maturities

$850

million

of

“prepayable”

debt

Recent Developments

4 |

Vantage Strategic Focus

5

To provide the long-term

value to our shareholders,

we

must

provide

the

right

people

and

the

right

assets.

The

right

customers

have

long-term business

opportunities that provide

sound cash flow necessary

to

achieve

the

right

financial structure.

Right

People

Right

Assets

Right

Customers

Right

Financial

Structure

Shareholder

Value |

•

Industry

leading

safety

record

–

in

2012,

we

completed

over

2.2

million man-hours with 0 lost time incidents,

•

Jack-up

fleet

has

achieved

approximately

99% productive

time

over the first 55 months of operations.

•

Enhanced

business

opportunities

as

Vantage

has

been

selected

to

manage complex 3

rd

party shipyard projects.

•

We

are

leveraging

our

technical

expertise

to

manage

operations

of two ultra-high specification jack-ups in Mexico without

making a financial investment.

•

We are investing in leading-edge training programs –

•

CARE –

Competency Assurance with Results and Effectiveness

•

GOLD –

Global Operations Leadership Development Program

Right People

6

Our senior management team averages over 29 years of

Industry experience. The cornerstones of our corporate culture

are safety and professionalism. |

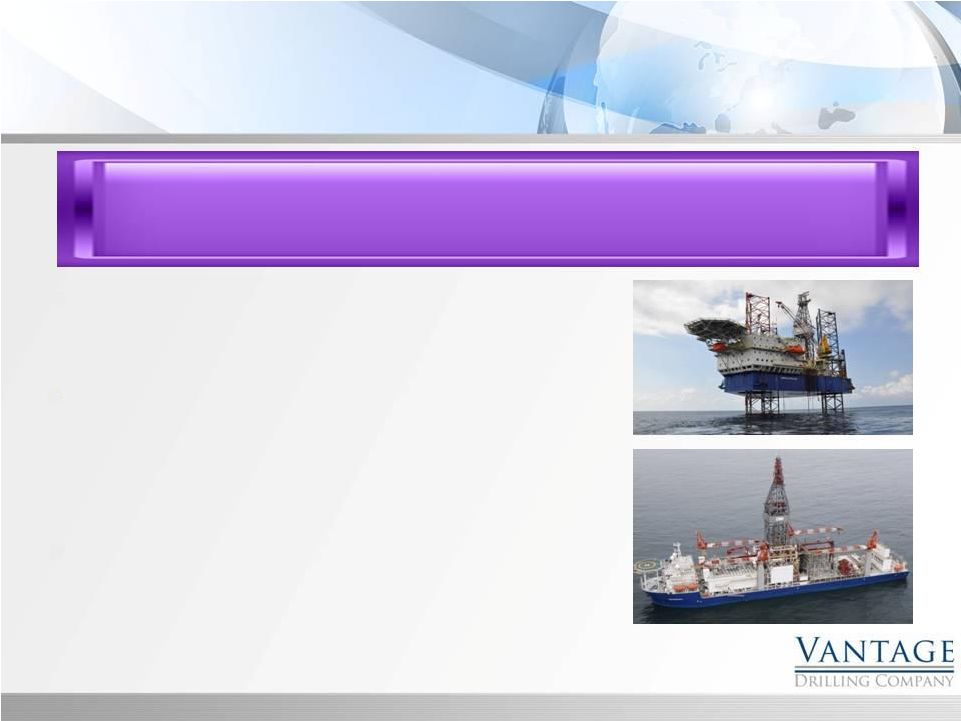

Right

Assets 7

Premium high-specification drilling units, including four

jackup rigs and three drillships. Total costs of owned fleet of

approximately $3.2 billion.

High-specification drillships, combined with deep technical

expertise, has allowed us to secure technically challenging

ultra-deepwater

projects;

Platinum

Explorer

and

Titanium

Explorer

have worked in 9,300+ and 8,800+ feet of water,

respectively.

Recently

ordered

Cobalt

Explorer,

7

th

generation,

dual-

activity UDW drillship equipped with (2) seven-ram

BOP’s. Also invested in joint venture to construct

similar drillshp, Palladium

Explorer

–

construction

subject

to

commercial

issues with builder.

•

•

•

We have built a fleet of new, premium assets that our customers

demand now and for the future. |

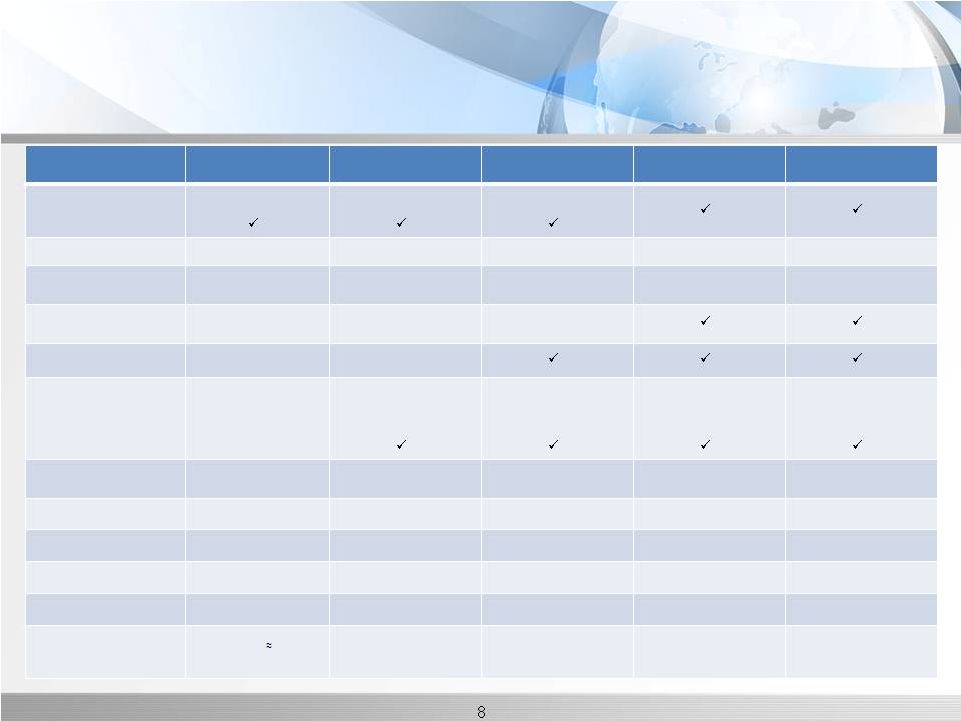

Ultra-Deepwater Bifurcation –

Vantage Has High-Spec Drillships

8

Platinum Explorer

Titanium Explorer

Tungsten Explorer

Cobalt Explorer

Palladium Explorer

Derrick Load Paths –

-

2x Activity

-

1.5x Activity

Draw Works (HP)

4,500

6,000

9,000

9,000 / 6,000

11,200 / 6,000

Hook Load (tons)

(net lifting capacity)

1,000

1,250

1,250

1,250 / 1,000

1,250 / 1,000

Heave Compensating Xmas

Tree Crane (165 t)

Tripsaver

BOPS’s

-

Onboard

-

RAM’s (*planned)

-

API SP53/GOM

Compliant

1

5 /6*

*planned for 2015

1

6

1

6

2

7

2

7

Water Depth

-

Capable/Outfitted

12,000 / 10,000

12,000 / 10,000

12,000 / 10,000

12,000 / 10,000

12,000 / 12,000

Payload

20,000 MT

20,000 MT

20,000 MT

25,000 MT

25,000 MT

Accommodation (beds)

180

180

200

200

212

Thrusters

6 x 5.5 Mw / DP3

6 x 5.5 Mw / DP3

6 x 5.5 Mw / DP3

6 x 5.5 Mw / DP3

6 x 5.5 Mw / DP3

Features

MPD Upgradeable

20K psi Ready

Notable accomplishments

-Drilling well in 8800 ft of

Water

-

>2 million lb casing load

Fastest shipyard delivery –

27 months from order

Drilled well in

9400 ft of

water |

Owned Assets

Delivered On-Time, On-

Budget -

December 2008

Premium Fleet with a Proven Track Record

Management Projects

Sonangol drillships

Newbuild Ultra-Premium Marine Pacific Class 375 Jackups

Emerald Driller

Sapphire Driller

Aquamarine Driller

Topaz Driller

Ultra-Deepwater 12,000 ft Drillships

Delivered On-Time, On-

Budget -

July 2009

Delivered On-Time, On-

Budget -

December 2009

Delivered On-Time, On-

Budget -

September 2009

3

newbuild project at DSME

Delivered July 2013

On Contract in SE Asia

Tungsten Explorer

Mexican Operator

Construction Management

Platinum Explorer

2

Successful newbuild at

DSME

Delivered April 2012

On Contract in GoM

Titanium Explorer

Palladium Explorer

Cobalt Explorer

th

th

rd

nd

th

Newbuild project pending

resolution of contractual issues

7

generation two x 7-ram

BOP’s, dual-derrick

4

newbuild project at DSME

Leverages shipyard experience

7 generation

two

x

7-ram

BOP’s, dual-derrick

Delivery Q3 2015

Delivered On-Time, On-

Budget -

November 2010

Hired by newly formed

drilling company to

manage initial assets

2 x “V ships”

UDW

drillships at DSME

9 |

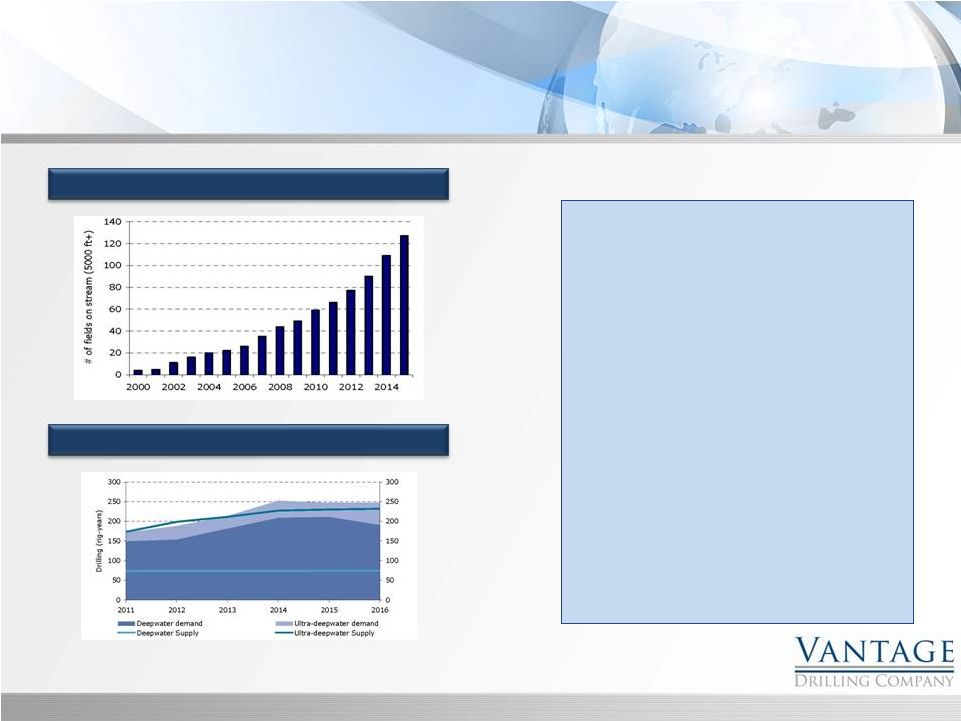

Strong Demand for Deepwater Assets

10

Source: ODS-Petrodata, DnB NOR

“Investments in global deepwater

exploration are predicted by Wood

Mackenzie to more than double from

last year’s level of $43 billion to as

much as $114 billion by 2022, driven

by the need to find the world’s

remaining hydrocarbons in greater

water depths…

As a result,

there will be a need for 95

additional deepwater rigs to be built

between 2016 and 2022…

Representing a change for the

deepwater sector from cyclical to

sustained growth.”

Continued Growth Cycle

Demand is Likely to Exceed Rig Supply |

Jackups

•

Modern, high-spec jackups have been, and continue to be

essentially fully contracted

•

Customers have strong preference for modern, high-spec

jackups •

We believe the market will easily absorb additional newbuilds for quite

some time.

11

“Enough said”

315

315

Jackups

>25 yrs old

115

115

Jackups

Under

Construction |

Spending Trends

12

Industry spending trends remain positive for continued

strong demand for offshore drilling.

Continued E&P Spending Growth

Over Half of E&P Spend is Offshore |

Right

Customers 13

We have focused our marketing efforts on customers with long-term drilling

requirements providing the opportunity for long-term contracts.

Three

of

our

jack-ups

are

currently

working

for

repeat

customers.

We

currently

have

over

$3.1

billion

of

backlog.

We have continuously improved our high satisfaction

ratings, based on direct customer surveys.

|

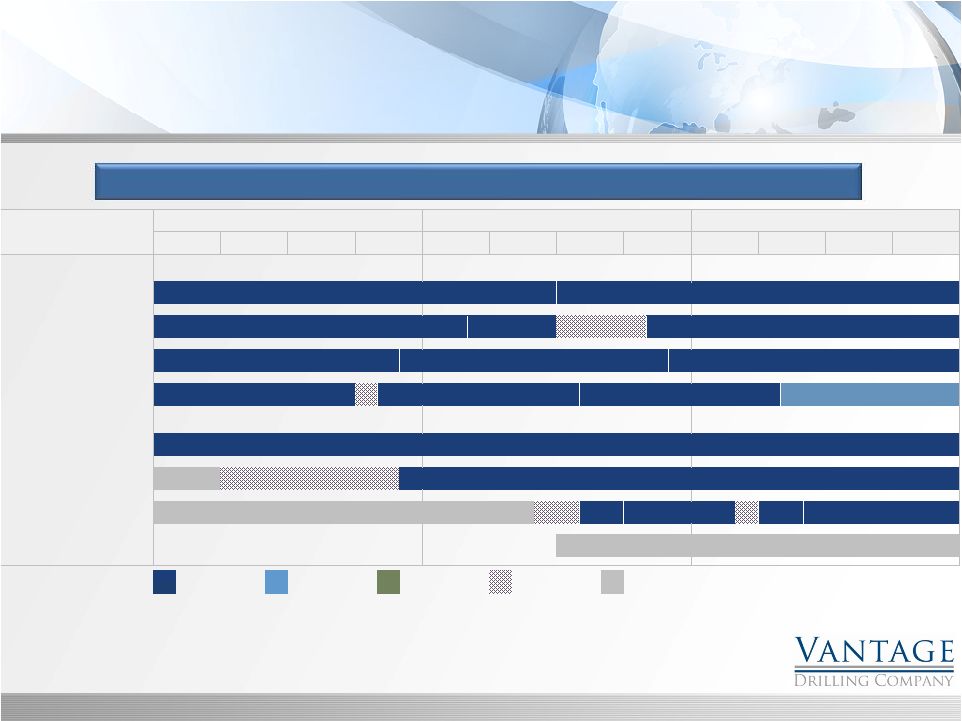

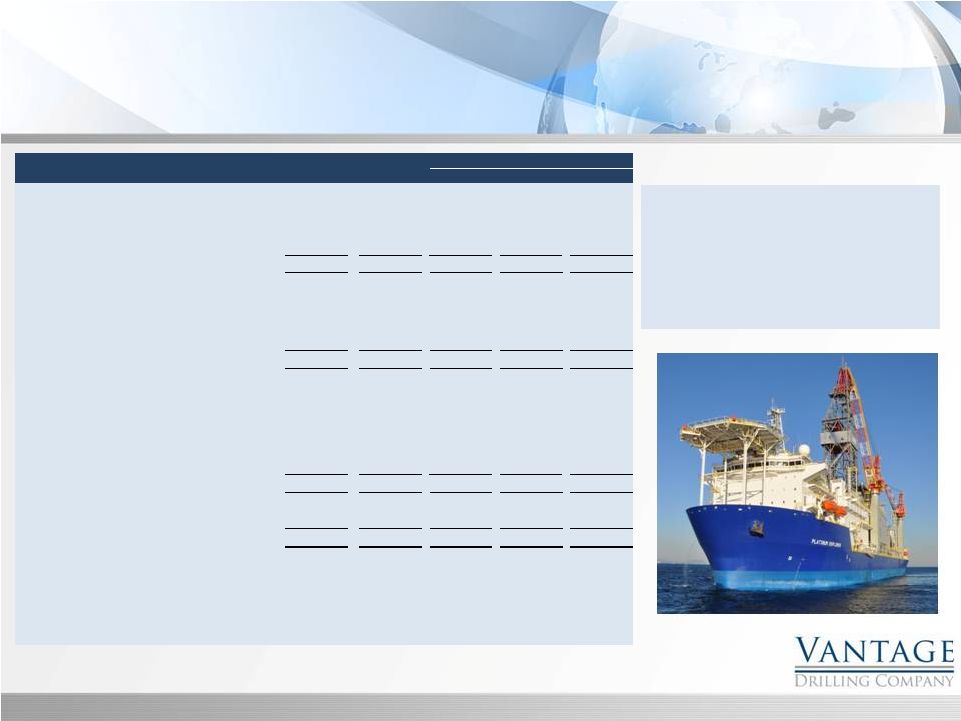

Customers Provide Strong Backlog

14

Customer

backlog

of

approximately

$3.1

Billion

provides

visibility

to

cash

flows

Ownership

2012

2013

2014

Rig

%

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Jackups

Emerald Driller

100%

$130,000

$156,000 (2 years)

Sapphire Driller

100%

$120,000 (net of taxes)

$165,000 (net)

18 months

Aquamarine Driller

100%

$132,000

$153,000

$155,000

Topaz Driller

100%

$187,000 (incl. upgrades and mobilization)

$155,000

$155,000

$155,000 (12 mos. - Indonesia)

Drillships

Platinum Explorer

100%

$590,000 (5 years)

Titanium Explorer

100%

$572,000 (8 years)

(2)

Tungsten Explorer

100%

(48 days)

4 wells (145 days)

60 days

$641,000 (2 years firm)

Cobalt Explorer

100%

Contracted

Option

Letter of Award;

Commisioning /

Construction

Contract

subject to conditions

Mobilization

(1)

Average drilling revenue per day is based on the total estimated revenue divided by the minimum number

of days committed in a contract. Unless otherwise noted, the total revenue includes any

mobilization and demobilization fees and other contractual revenues associated with the drilling

services. (2)

The drilling revenue per day includes the achievement of the 12.5% bonus opportunity, but excludes

mobilization revenues and revenue escalations included in the contract. |

We have refinanced our senior debt –

Staggered maturities through 2023,

Added flexibility to pre-pay debt without premiums,

Reduced

annual

cash

interest

costs

by

approximately

$90

million,

and

We have expanded our UDW fleet with limited equity exposure

– Cobalt

Explorer

(only

$59.5

million

down

payment;

tail-end

heavy

contract)

Palladium

Explorer

investment

(42%)

limits

pre-delivery

equity

exposure

to

$31 million. (Project pending resolution of contractual

issues.) Right Financial Structure

15

Our financial leverage is counter-balanced by a strong contract

backlog and long-term visibility of cash flows. |

Strong Growing Cash Flow to Service Debt

16

Long-term contracts provide visibility to cash flow to support existing

leverage. Investments made to-date generating favorable returns

for the future. Commencing

Q4 2013

Vantage has

seven out of

seven completed

rigs in service

(versus only five

in Q3)

$(200.0)

$-

$200.0

$400.0

$600.0

2011

2012

2013

2014

2015

Majority of Projected EBITDA is Contracted

Contracted

Uncontracted

Net Income

Projected

Actual |

Strategic Focus

Debt

Refinancing

–

DONE

Titanium

Explorer

back

to

full

day

rate

–

DONE

Tungsten

Explorer

contract

commencing

with shipyard delivery (“gap period”) –

DONE

Sapphire

Driller

Contract

–long-term

follow

on job –

DONE

Add

UDW

asset

–

Cobalt

Explorer

–

DONE

Deployment & startup of Tungsten Explorer

–

resulting in EBITDA run-rate > $500

million; dramatically increasing profitability

–

DONE

•

Deployment

of

Cobalt

Explorer

–

Aug.

2015

•

Deployment of Palladium Explorer (42% VTG)

•

Accelerating

reduction

of

debt

/

improved

debt

statistics and rating

•

Begin

to

return

capital

to

shareholders

17

Next Steps

Near Term |

HISTORICAL FINANCIAL

Appendix

18 |

Balance Sheet

The Debt to EBITDA leverage

ratio will continue to reduce as

Vantage reports a full year of

operations from the Titanium

Explorer

(December

2012)

and

the Tungsten Explorer

(September 2013)

19

($ in millions)

December 31,

December 31,

2011

2012

31-Mar-13

30-Jun-13

30-Sep-13

Cash and cash equivalents

117.0

$

506.2

$

460.5

$

443.8

$

71.1

$

Trade receivables

100.9

119.5

101.9

107.9

144.9

Inventory, prepaids & other

41.3

63.1

62.1

64.8

65.9

Total current assets

259.2

688.8

624.5

616.5

281.9

Property and Equipment

1,805.1

2,717.5

2,711.2

2,719.2

3,207.2

Other assets

58.2

123.9

119.9

125.4

128.7

Total assets

2,122.5

$

3,530.2

$

3,455.6

$

3,461.1

$

3,617.8

$

Accounts payable and accruals

150.2

$

174.4

127.5

133.1

176.8

Revolving Credit Agreement

-

-

-

-

10.0

Current maturities

-

31.2

41.0

47.3

53.5

Total current liabilities

150.2

205.6

168.5

180.4

240.3

Long-term debt

1,246.4

2,710.6

2,796.3

2,784.8

2,862.5

Other long-term liabilities

29.8

45.5

43.4

42.7

41.5

Shareholders equity

696.1

568.5

447.4

453.2

473.5

Total liabilities and shareholders' equity

2,122.5

$

3,530.2

$

3,455.6

$

3,461.1

$

3,617.8

$

Long-term Debt/LTM EBITDA

7.1

X

12.6

X

12.6

X

10.7

X

9.9

X

For the Quarter Ended |

Statement of Operations

20

Net income and cash flow from

operations is increasing

significantly for Vantage as the

Tungsten

Explorer

commenced

operations in September 2013.

($ in millions)

December 31,

December 31,

2011

2012

31-Mar-13

30-Jun-13

30-Sep-13

REVENUE

Contract Drilling Services

366.8

$

423.8

$

134.7

$

155.8

$

158.9

$

Management Fees

13.7

6.6

3.2

2.4

3.9

Reimbursables

105.3

41.0

9.1

12.4

13.1

Total revenues

485.8

471.4

147.0

170.6

175.9

OPERATING COSTS AND EXPNSES

Operating Costs

284.9

230.1

75.3

77.1

84.1

General and Administrative

26.3

26.0

7.4

7.0

8.9

Depreciation

64.5

68.7

24.9

25.0

24.9

Total operating expenses

375.7

324.8

107.6

109.1

117.9

INCOME FROM OPERATIONS

110.1

146.6

39.4

61.5

58.0

OTHER INCOME (EXPENSE)

Interest Income

0.1

0.1

0.1

0.1

-

Interest Expense and Financing

(154.9)

(149.1)

(59.7)

(51.3)

(47.4)

Loss on Debt Extinguishment

(25.2)

(124.6)

(98.3)

-

-

Other Income

1.3

0.6

0.9

1.0

0.3

Total other expenses

(178.7)

(273.0)

(157.0)

(50.2)

(47.1)

INCOME (LOSS) BEFORE TAX

(68.6)

(126.4)

(117.6)

11.3

10.9

INCOME TAX PROVISION

11.4

18.9

5.6

7.1

4.1

Net income (loss)

(80.0)

$

(145.3)

$

(123.2)

$

4.2

$

6.8

$

INCOME (LOSS) PER SHARE

(0.28)

$

(0.50)

$

(0.41)

$

0.01

$

0.02

$

PRO FORMA INCOME (LOSS) PER SHARE

(0.19)

$

(0.07)

$

(0.08)

$

0.01

$

0.02

$

EBITDA

174.7

$

215.3

$

64.3

$

86.5

$

83.0

$

LTM EBITDA

174.7

$

215.3

$

222.3

$

260.4

$

290.3

$

For the Quarter Ended |

EBITDA RECONCILIATION

21

($ in millions)

December 31,

December 31,

2011

2012

31-Mar-13

30-Jun-13

30-Sep-13

Net Income (Loss)

(80.0)

$

(145.3)

$

(123.2)

$

4.2

$

6.8

$

Interest Expense, Net

154.8

149.0

59.6

51.2

47.4

Income Tax Provision

11.4

18.9

5.6

7.1

4.1

Depreciation

64.5

68.7

24.9

25.0

24.9

Loss on Debt Extinguishment

25.2

124.6

98.3

-

-

Other

(1.2)

(0.6)

(0.9)

(1.0)

(0.2)

EBITDA

174.7

$

215.3

$

64.3

$

86.5

$

83.0

$

For the Quarter Ended |