Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - Ryerson Holding Corp | d618878dex231.htm |

Table of Contents

As filed with the Securities and Exchange Commission on December 4, 2013.

Registration No 333-164484

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 17

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

RYERSON HOLDING CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware | 5051 | 26-1251524 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

227 W. Monroe, 27th Floor

Chicago, Illinois 60606

(312) 292-5000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Mark S. Silver

Vice President and Managing Counsel

Ryerson Holding Corporation

227 W. Monroe, 27th Floor

Chicago, Illinois 60606

(312) 292-5000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Cristopher Greer, Esq. | James J. Clark, Esq. William J. Miller, Esq. | |

| Willkie Farr & Gallagher LLP 787 Seventh Avenue New York, New York 10019 (212) 728-8000 Facsimile: (212) 728-9214 |

Cahill Gordon & Reindel LLP 80 Pine Street New York, New York 10005 (212) 701-3000 Facsimile: (212) 269-5420 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ | |

| Non-accelerated filer x | Smaller reporting company ¨ | |

| (Do not check if a smaller reporting company) |

|

| ||||

| Title of Each Class of Securities To Be Registered | Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee(3) | ||

| Common Stock, par value $0.01 per share |

$300,000,000 | $34,380 | ||

|

| ||||

| (1) | Estimated solely for purposes of determining the registration fee in accordance with Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Includes shares of common stock that may be purchased by the underwriters to cover over-allotments, if any. See “Underwriting.” |

| (3) | Previously paid. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. Neither we nor the selling stockholders may sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus dated , 2013

PROSPECTUS

Shares

Ryerson Holding Corporation

Common Stock

We are selling shares of our common stock. The selling stockholders identified in this prospectus have granted the underwriters an option to purchase up to additional shares of common stock to cover over-allotments. We will not receive any proceeds from the sale of shares by the selling stockholders.

This is the initial public offering of our common stock. We currently expect the initial public offering price to be between $ and $ per share. We have applied to have our common stock listed on the New York Stock Exchange under the symbol “RYI.”

Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 18.

| Per Share | Total | |||||||

| Public Offering Price |

$ | $ | ||||||

| Underwriting Discount(1) |

$ | $ | ||||||

| Proceeds, before expenses, to us |

$ | $ | ||||||

| (1) | See “Underwriting” for a description of the compensation payable to the underwriters. |

The underwriters may also purchase up to an additional shares from the selling stockholders, at the public offering price, less the underwriting discount, within 30 days of the date of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares to purchasers on or about , 2014.

| BofA Merrill Lynch | Deutsche Bank Securities | BMO Capital Markets |

| J.P. Morgan | Jefferies | |

| Wells Fargo Securities | KeyBanc Capital Markets | Citigroup | ||||

| Macquarie Capital | ||||||

The date of this prospectus is , 2013

Table of Contents

Table of Contents

You should rely only on the information contained in this prospectus and any free writing prospectus we may specifically authorize to be delivered or made available to you. We have not, and the selling stockholders and the underwriters have not, authorized anyone to provide you with different information. We are not, and the selling stockholders and the underwriters are not, making an offer of these securities in any jurisdiction where the offer is not permitted. You should not assume that the information contained in this prospectus and any free writing prospectus we may specifically authorize to be delivered or made available to you is accurate as of any date other than the date on the front of this prospectus, regardless of its time of delivery or of any sale of shares of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

| Page | ||||

| 1 | ||||

| 18 | ||||

| 31 | ||||

| 33 | ||||

| 34 | ||||

| 36 | ||||

| 37 | ||||

| 38 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

40 | |||

| 62 | ||||

| 79 | ||||

| 84 | ||||

| 92 | ||||

| 96 | ||||

| 97 | ||||

| 99 | ||||

| 101 | ||||

| 105 | ||||

| 111 | ||||

| 113 | ||||

| 116 | ||||

| 124 | ||||

| 124 | ||||

| 124 | ||||

| F-1 | ||||

Table of Contents

INDUSTRY AND MARKET DATA

In this prospectus, we rely on and refer to information and statistics regarding the steel processing industry and our market share in the sectors in which we compete. We obtained this information and these statistics from sources other than us, which we have supplemented where necessary with information from publicly available sources, discussions with our customers and our own internal estimates. References in this prospectus to:

| • | American Iron and Steel Institute (“AISI”) refer to its SteelWorks website from March 2013, or its Steel Production Capacity Utilization index from November 2013; |

| • | The Institute for Supply Management refer to its October 2013 Manufacturing ISM Report on Business®; |

| • | United States Federal Reserve refer to its September 2013 “Summary of Economic Projections”; |

| • | The Metals Service Center Institute (“MSCI”) refer to its October 2013 edition of “MSCI Metal Activity Report”; |

| • | The Federal Reserve Bank of Philadelphia refer to its June 2013 issue of “The Livingston Survey”; |

| • | Euromonitor refer to its February 2013 “Consumer Appliances in the U.S.” report; |

| • | IBIS Worldwide refer to its January 2013 “Heating & Air Conditioning in the U.S.” report; |

| • | LMC Automotive refer to its Q3 2013 data; |

| • | MarketLine refer to its May 2013 “Machinery in the United States” report; |

| • | Wood Mackenzie refer to its October 2013 “Metals Market Service Monthly Update” reports; |

| • | Bureau of Economic Analysis refer to its November 2013 “Auto and Truck Seasonal Adjustment” data; and |

| • | Metal Center News refer to its September 2013 “Service Center Top 50” report. |

We use these sources and estimates and believe them to be reliable, but we cannot give you any assurance that any of the projected results will be achieved.

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information that you should consider before investing in our common stock. You should read the entire prospectus carefully together with our consolidated financial statements and the related notes appearing elsewhere in this prospectus before making an investment decision. This prospectus contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in such forward-looking statements as a result of certain factors, including those discussed in the “Risk Factors” and other sections of this prospectus.

Except as otherwise indicated herein or as the context otherwise requires, references in this prospectus to “Ryerson Holding,” “the Company,” “we,” “our,” and “us” refer to Ryerson Holding Corporation and its direct and indirect subsidiaries (including Ryerson Inc.). The term “Ryerson” refers to Ryerson Inc., a direct wholly owned subsidiary of Ryerson Holding, together with its subsidiaries on a consolidated basis. “Platinum” refers to Platinum Equity, LLC and its affiliated investment funds, certain of which are our principal stockholders, and “Platinum Advisors” refers to Platinum Equity Advisors, LLC. We refer to the issuance of our common stock being offered hereby as the “offering.”

Our Company

We believe we are one of the largest processors and distributors of metals in North America measured in terms of sales, with global operations in North America, China and a recently established presence in Brazil. Our industry is highly fragmented with the largest companies accounting for only a small percentage of total market share. Our customer base ranges from local, independently owned fabricators and machine shops to large, international original equipment manufacturers. We process and distribute a full line of over 75,000 products in stainless steel, aluminum, carbon steel and alloy steels and a limited line of nickel and red metals in various shapes and forms. More than one-half of the products we sell are processed to meet customer requirements. We use various processing and fabricating techniques to process materials to a specified thickness, length, width, shape and surface quality pursuant to customer orders. For the year ended December 31, 2012, we purchased 2.1 million tons of materials from suppliers throughout the world. For the nine months ended September 30, 2013, our Adjusted EBITDA, excluding LIFO expense was $128.1 million, revenue was $2,657.8 million and net income was $8.2 million. See note 4 in “Summary Historical Consolidated Financial and Other Data” for a reconciliation of Adjusted EBITDA to net income.

We operate over 90 facilities across North America, six facilities in China and one in Brazil. Our service centers are strategically located in close proximity to our customers, which allows us to quickly process and deliver our products and services, often within the next day of receiving an order. We own, lease or contract a fleet of tractors and trailers, allowing us to efficiently meet our customers’ delivery demands. In addition, our scale enables us to maintain low operating costs. Our operating expenses as a percentage of sales for the years ended December 31, 2011 and 2012 were 11.8% and 12.6%, respectively.

We serve more than 40,000 customers across a wide range of manufacturing end markets. We believe the diverse end markets we serve reduce the volatility of our business in the aggregate. Our geographic network and broad range of products and services allow us to serve large, international manufacturing companies across multiple locations.

Following this offering, because Platinum will control more than 50% of the voting power of our common stock, we will be considered a “controlled company” under the New York Stock Exchange rules. As such, we are permitted, and have elected, to opt out of compliance with certain NYSE corporate governance requirements. Accordingly, stockholders will not have the same protections afforded to stockholders of companies that are

1

Table of Contents

subject to all of the NYSE corporate governance requirements. See “Risk Factors” — We are exempt from certain corporate governance requirements because we are a controlled company within the meaning of the NYSE rules for a summary of the effects of a controlled company on investors.

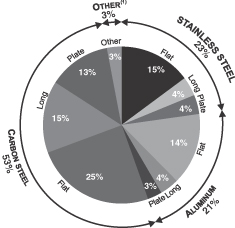

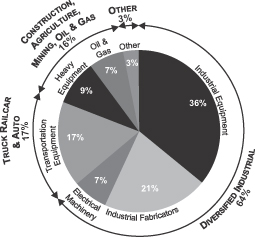

We are broadly diversified in our end markets and product lines in North America, as detailed below.

| 2012 Sales by End Market | 2012 Sales by Product | |

|

|

| |

| (1) “Other” includes copper, brass, nickel, pipe, valves and fittings. | ||

Industry and End Market Outlook

Ryerson participates in the metals service center industry providing steel, aluminum and other metals products across a wide range of industrial manufacturing end markets. Our business performance is therefore impacted by a number of factors tied to industrial activity, including economic growth, end market demand and metals pricing. With steel products accounting for 76% of our 2012 sales, it is the largest driver of our business. Aluminum products account for 21% of our business, with other metals accounting for the remainder.

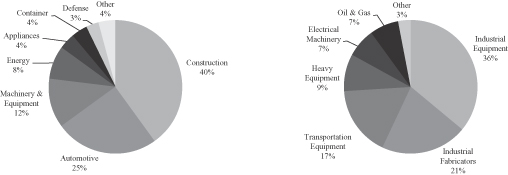

Macroeconomic Outlook. Steel is utilized in a diverse range of manufacturing and fabrication applications with a variety of end market demand drivers. The primary drivers of demand for the steel industry are the construction, automotive, machinery and equipment, and energy end markets, which, according to the American Iron and Steel Institute, account for approximately 85% of shipments collectively. As evidenced by our end market sales segmentation, we are not reliant on a single specific sector, but rather broader diversified industrial activity. Our primary end markets include industrial equipment and fabrication, transportation equipment, heavy equipment, electrical machinery and oil and gas. We believe that we are well positioned in these markets and that they are poised for growth as the broader industrial sectors continue to grow. The charts below, which reflect the most recently available data from AISI, show our end market exposure as well as the broader steel market.

2

Table of Contents

| 2012 Steel Shipments by Market Classification (AISI) | 2012 Ryerson Sales by End Market | |

| ||

| Source: American Iron and Steel Institute | Source: Company estimates | |

While some of the key end market drivers of steel industry demand do not directly overlap with our end markets, they do impact broader steel demand and pricing, which can impact our business. Recently, leading indicators in the key steel industry end markets referenced above have begun to show sustained growth and continue to build positive momentum. For example, housing starts have shown stable growth over the last 24 months, while non-residential construction, which typically lags housing, is starting to show signs of sustained improvement as well. Additionally, U.S. automotive sales continue to rise according to the Bureau of Economic Analysis, reaching 15.2 million vehicles on a seasonally adjusted annualized rate basis in October 2013 versus 14.3 million for October of 2012. Machinery and equipment, a key end market for us, includes a variety of industrial manufacturing end markets, many of which are showing signs of significant growth. This is evidenced by the Institute for Supply Management’s (“ISM”) Purchasing Managers’ Index (“PMI”), which reached 56.4 in October 2013. The United States Federal Reserve midpoint GDP growth estimates of 3.0% and 3.25% for 2014 and 2015, respectively. Finally, the oil and gas end market continues to be a long-term growth market in steel. Much of this growth is attributable to growth in North American drilling and refining, substantially impacted by activity in United States shale oil and gas and the Canadian oil sands. Additionally, investment in new petrochemical production capacity in the United States as a result of relatively low domestic natural gas prices may further bolster steel demand. The following chart shows the historical movements of the Purchasing Managers’ Index.

ISM Purchasing Managers’ Index

According to MSCI, total inventory levels of carbon steel, stainless steel and aluminum at U.S. service centers reached a trough in August 2009 and bottomed at the lowest levels since the data series began in 1977. Although industry demand recovered in 2010, 2011 and 2012, shipments and inventory are still well below pre-downturn averages, which we believe suggests long-term growth potential that may be realized if these metrics return to, or exceed, their historical averages.

3

Table of Contents

| North American Monthly Service Center Shipments | North American Monthly Service Center Inventory | |

|

|

Ryerson End Market Outlook. Although our revenue for the nine months ended September 30, 2013 decreased 16.3% compared to the nine months ended September 30, 2012 due to weaker economic conditions in the metals market, according to the latest Livingston Survey, published by the Federal Reserve Bank of Philadelphia, U.S. industrial production is expected to grow by 2.8% and 3.1% in 2013 and 2014, respectively. Two of our largest end markets, industrial equipment and fabrication, include numerous diversified industrial manufacturing markets which, along with the broader economy, are showing signs of sustained growth. For example, in the U.S. major appliances and Heating Ventilation and Air Conditioning (“HVAC”) equipment, both markets we serve, are projected to grow at even higher rates. Specifically, major appliances are expected to grow 6.5% and 6.1% in 2014 and 2015, respectively, according to Euromonitor. According to IBIS Worldwide, HVAC is expected to grow 2.2% and 3.7% over the same periods.

In addition, we also serve the transportation equipment, heavy equipment and electrical equipment markets which are expected to show significant growth in the coming years. Transportation equipment, including commercial vehicle production, represents 17% of our sales and is expected to grow 2.8% per year in the U.S. between 2013 and 2015 according to LMC Automotive. Machinery and heavy equipment, including construction and agricultural equipment, represents 9% of our end-market sales and is projected to grow 7.1% per year in the U.S. between 2012 and 2016 according to MarketLine.

Metals Pricing. Along with improvements in volume, as indicated by demand trends in the end markets, movements in the price of steel will also impact our business. Steel prices are driven by a number of factors, including input prices, capacity utilization and foreign imports. Currently, input costs are providing support for steel pricing, as they flow directly through the pricing of the mills’ steel output. Additionally, we believe that recent closings of mills, including the Sparrows Point steel mill, among others, that have been dismantled, combined with continued growth in the global economy and end market demand, should begin to absorb global capacity, resulting in increased utilization. The U.S. steel industry production capacity utilization rate increased to 77.5% by the end of November 2013 from a low of 34% in December 2008, according to AISI. North American production capacity utilization levels remain below the 85% average utilization level observed in the post- consolidation restructured steel industry from 2002 to 2008. Although our average selling price decreased 10.3% in the nine months ended September 30, 2013 compared to the nine months ended September 30, 2012 due to decreases in metals prices across all of our products, with some of the largest decreases in our carbon plate, stainless steel plate and stainless steel long product lines, we believe that the combination of higher input prices, increased global demand and increased capacity utilization will support steel price increases in the near future, positively impacting our business.

Aluminum pricing also remains well below pre-downturn levels but has stabilized recently. Global output of aluminum is projected to increase 6.6% in 2014 according to Wood Mackenzie, fueled by factors including the rebound in U.S. construction and increased demand from the transportation and infrastructure markets in China.

4

Table of Contents

Industry Consolidation. The United States service center industry is a highly fragmented market with the top 50 service centers controlling approximately 25% of industry sales, according to Metal Center News, only 12 of which have sales over $1 billion. Such fragmentation has historically resulted in the smaller service centers having less negotiating leverage with both the larger consolidated steel mills, as well as larger customers. In recent years, however, there has been increased consolidation among larger players resulting in fewer customers of size for the mills and greater purchasing power for service centers. A recent example is the acquisition of Metals USA Holding Corp. by Reliance Steel & Aluminum Co. We believe that there is significant opportunity for consolidation and we expect the trend will continue.

Our Competitive Strengths

Leading Market Position in North America.

We believe we are one of the largest service center companies for carbon and stainless steel as well as aluminum based on sales in the North American market where we have a broad geographic presence with over 90 locations.

Our service centers are located near our customer locations, enabling us to provide timely delivery to customers across numerous geographic markets. Additionally, our widespread network of locations in the United States, Canada and Mexico helps us to utilize our expertise to more efficiently serve customers with complex supply chain requirements across multiple manufacturing locations. We believe this is a key differentiator among customers who need a supplier that can reliably and consistently support them. Our ability to transfer inventory among our facilities better enables us to more timely and profitably source and process specialized items at regional locations throughout our network than if we were required to maintain inventory of all products and specialized equipment at each location.

We believe with our significant footprint in the North American market, combined with our significant scale and operating leverage, a cyclical recovery of the service center industry supported by long-term growth trends in Ryerson’s end-markets should allow us to experience higher growth rates relative to North American economic improvement, but there can be no guarantee that we will experience such higher growth rates.

Broad Geographic Reach across Attractive End Markets.

Our operations cover a diverse range of industries, including industrial equipment, industrial fabrication, electrical machinery, transportation equipment, heavy equipment and oil and gas. Manufacturing growth has accelerated since November 2012 as shown by the ISM index (as described in the Industry and End Market Outlook), and we believe industries we serve will provide strong demand for our products and services as the North American manufacturing economy continues to recover. We also believe that the continued trend of moving manufacturing to the United States from overseas should benefit us with our broad North American platform. In addition, we expect to benefit from continued growth in international markets that will help spur demand at domestic manufacturing facilities that sell into the global market. We believe that our ability to quickly adjust our offering based on regional and industry specific trends creates stability while also providing the opportunity to access specific growth markets.

Established Platform for Organic and Acquisition Growth.

Since 2011, we have opened seven new service centers in previously underserved North American regions. We have acquired another ten facilities to complement our existing locations and expanded the product offering in many locations based on customer demand. Over the last two years, a significant portion of our capital expenditures have been made to expand our long and plate processing capabilities at 15 existing locations. We believe that our expanded presence in select regions and products positions us well to capture further growth in these regions and products.

5

Table of Contents

Although there can be no guarantee of growth, we believe a number of our other strategies, such as improving our product mix, pricing our products and services based on the value we provide our customers, growing our large national network, and expanding our diverse operating capabilities, will provide us with growth opportunities.

In addition, we have utilized our leadership and experience in the North American markets to establish operations in China, the largest and one of the highest growth metals markets in the world, as well as in Brazil.

Given the highly fragmented nature of the service center industry, we believe there are numerous additional opportunities to acquire businesses and incorporate them into our existing infrastructure. Given our large scale and geographic reach, we believe we can add value to these businesses in a number of ways, including providing greater purchasing power, access to additional end markets and broadening product mix. Although the Company does not have any current plans to engage in any specific acquisitions, from time to time and in the ordinary course of business, the Company regularly evaluates potential acquisition opportunities.

Lean Operating Structure Providing Operating Leverage.

Since the acquisition by Platinum, we have transformed our operating model by decentralizing our operations and reducing our cost base. Decentralization has improved our customer service by moving key functions such as procurement, credit and operations support to our regional offices. From 2007 through the end of 2009, we engaged in a number of cost reduction initiatives that included a headcount reduction of approximately 1,700, representing 33% of our workforce, and the closure of 14 redundant or underperforming facilities in North America. Furthermore, in 2011, we also completed the decentralization of credit, operations, and procurement and reduced field staffing levels. In that overall period, we believe that we have generated annual fixed cost savings of approximately $200 million since 2007. We believe this reduction has improved our operating efficiency while also providing the flexibility for further growth in our targeted markets.

We have also focused on process improvements in inventory management. Despite an increase in average inventory days from 74 days in 2011 to 86 days in 2013, our average inventory days have improved on an overall basis from 100 days in 2006. This reduction has decreased our exposure to metals price movements as well as increased capacity in our facilities to devote to higher margin products. These organizational and operating changes have improved our operating structure, working capital management and efficiency.

As a result of our initiatives, we have increased our financial flexibility and believe we have a favorable cost structure compared to many of our peers. This will provide significant operating leverage.

Extensive Breadth of Products and Services for Diverse Customer Base.

We carry a full range of over 75,000 products, including aluminum, carbon, stainless and alloy steels and a limited line of nickel and red metals. In addition, we provide a broad range of processing and fabrication services to meet the needs of our 40,000 customers and fulfill more than 1,000,000 orders per year. We also provide supply chain solutions, including just-in-time delivery, and value-added components to many original equipment manufacturers.

We believe our broad product mix and marketing approach provides customers with a “one-stop shop” solution few other service center companies are able to offer.

For the year ended December 31, 2012, no single customer accounted for more than 2% of our sales, and our top 10 customers accounted for less than 10% of sales.

6

Table of Contents

Strong Relationships with Suppliers.

We are among the largest purchasers of metals in North America and have long-term relationships with many of our North American suppliers. We believe we are frequently one of the largest customers of our suppliers and that concentrating our orders among a core group of suppliers is an effective method for obtaining favorable pricing and service. We believe we have the opportunity to further leverage this strength through continued focus on price and volume using an analytics-driven approach to procurement. In addition, we view our strategic suppliers as supply chain partners. Our coordinated effort focused on logistics, lead times, rolling schedules, and scrap return programs ultimately results in value-based buying that is advantageous for us. Metals producers worldwide are consolidating, and large, geographically diversified customers, such as Ryerson, are desirable partners for these larger suppliers. Our relationships with suppliers often provides us with access to metals when supply is constrained. Through our knowledge of the global metals marketplace and capabilities of specific mills we believe we have developed a global purchasing strategy that allows us to secure favorable prices across our product lines.

Experienced Management Team with Deep Industry Knowledge.

Our senior management team has extensive industry and operational experience and has been instrumental in optimizing and implementing our strategy in the last two years. Our senior management has an average of more than 20 years of experience in the metals or service center industries. The senior executive team’s extensive experience in international markets and outside the service center industry provides perspective to drive profitable growth.

Our CEO, Mr. Michael Arnold, joined the Company in January 2011 and has 34 years of diversified industrial experience. Mr. Edward Lehner, who has been our CFO since August 2012, has 24 years of experience predominantly in the metals industry. Under their leadership, we have increased our focus on positioning the Company for growth and enhanced profitability.

Our Strategy

Expand Margins.

We are actively pursuing strategies to achieve increased gross margins. We believe this will allow our profitability to accelerate as volumes in our industry improve. Although the first nine months of net sales in 2013 decreased by 16.3% as compared to the first nine months of net sales in 2012, we have employed and continue to employ the initiatives below, which have resulted in an increase in our gross margins as a percentage of sales, excluding LIFO expense, by over 100 basis points, from 15.7% in Q3 2012 to 16.9% in Q3 2013. We have excluded LIFO expense from the gross margin as a percentage of sales metric in order to provide a means of comparison amongst our competitors who may not use the same basis of accounting for inventories.

Optimize Product Mix. We see significant opportunities to continue to improve our margins by increasing long and plate products supplied to our customers, as long and plate products typically generate higher margins than flat products. We have established regional long product inventory to provide a broad line of stainless, aluminum, carbon and alloy long products as well as the necessary processing equipment to meet demanding requirements of these customers. In addition, over the past two years, 45% of our capital expenditures have gone toward upgrading and adding plate and long processing capabilities throughout our operational footprint. We expect to continue to optimize product mix through these initiatives.

Optimize Customer Mix. We have increased our focus on serving a diversified group of industrial customers that value our customized processing services which we price on a transaction-by-transaction basis as opposed to larger volume program account customers who typically have fixed pricing arrangements over varying time periods. Our sales to customers using transactional pricing arrangements typically generate higher margins and require less working capital investment. We have re-evaluated and re-priced many of our lower margin program accounts which has resulted in an increase in our margins, as evidenced above.

7

Table of Contents

Expand Value-added Processing Services. We seek to continue to improve our margins by complementing our products with first stage manufacturing and other processing capabilities that add value for our customers. Additionally, for certain customers we have assumed the management and responsibility for complex supply chains involving numerous suppliers, fabricators and processors. We leverage our capabilities to deliver the highest value proposition to our customers by providing a wide breadth of competitive products and services, as well as superior customer service and product quality.

Improve Supply Chain and Procurement Management. As a large purchaser of metals we continue to use analytic-driven processes to develop supply chains which lower our procured costs, shorten our lead times, improve our working capital management and decrease our exposure to commodity price fluctuations.

Improve Operating Efficiency.

We are committed to improving our operating capabilities through continuous business improvements and cost reductions. We have made, and continue to make, improvements in a variety of areas, including operations, sales, delivery, administration and working capital management. Furthermore, we continue to focus on better customer service and the hiring, retention and promotion of high performing employees as well as place greater emphasis on working capital efficiencies. In particular with respect to inventory, our goal of maintaining approximately 75-80 days of sales on hand reduces our exposure to metals prices and increases capacity in facilities to devote to higher margin products. Our streamlined organizational structure combines local decision making with regional and national sourcing to improve efficiency.

Pursue Profitable Growth Through Expansion and Value-Accretive Acquisitions.

We are focused on increasing our sales to existing customers, as well as expanding our customer base globally, but there can be no guarantee we will be able to expand. We expect to continue increasing revenue through a variety of sales initiatives and by targeting attractive markets.

In North America, we have expanded and continue to expand in markets that we believe are underserved. We opened seven new facilities since 2011 in Texas, Georgia, Iowa, Illinois, Utah and Mexico, and have expanded higher-margin plate fabrication or long-product capabilities at many existing locations, where we have observed an opportunity to generate attractive returns. We are continuously monitoring opportunities for further expansion across the United States, Canada and Mexico. We expect to leverage our expertise in North America and selectively expand our business in China and Brazil as well as additional high growth emerging markets.

Since 2010, we have completed five strategic acquisitions: Texas Steel Processing Inc., SFI-Gray Steel Inc., Singer Steel Company, Turret Steel and Açofran Aços e Metais Ltda. These acquisitions have provided various opportunities for long-term value creation through the expansion of our product and service capabilities, geographic reach, operational distribution network, end markets diversification, cross-selling opportunities and the addition of transactional-based customers. Although the Company does not have any current plans to engage in any specific acquisitions, we regularly evaluate potential acquisitions of service center companies that complement our existing customer base and product offerings, and plan to continue pursuing our disciplined approach to such acquisitions.

Maintain Flexible Capital Structure and Strong Liquidity Position.

Our management team is focused on maintaining a strong level of liquidity that will facilitate our plans to execute our various growth strategies. Throughout the economic downturn, we maintained liquidity in excess of $300 million. Liquidity as of September 30, 2013 was approximately $423 million, comprised of $319 million of availability under Ryerson’s senior secured $1.35 billion asset-based revolving credit facility and foreign debt facilities, and $104 million of cash-on-hand and marketable securities. We have no financial maintenance covenants in our debt agreements unless availability under the Ryerson Credit Facility falls below $125 million.

8

Table of Contents

Substantially all of the proceeds from this offering will be used to further reduce our outstanding indebtedness. In addition, following the 2012 bond refinancing, there are no significant debt maturities until the maturity of the Ryerson Credit Facility, which occurs on the earlier of (a) April 3, 2018 or (b) August 16, 2017 (60 days prior to the scheduled maturity date of the 9% Senior Secured Notes due 2017 issued by Ryerson and its wholly owned subsidiary, Joseph T. Ryerson & Son Inc. (the “2017 Notes”)), if the 2017 Notes are then outstanding.

Risk Factors

An investment in our common stock is subject to substantial risks and uncertainties. Before investing in our common stock, you should carefully consider the following, as well as the more detailed discussion of risk factors and other information included in this prospectus:

| • | although the financial markets are in a state of recovery, the economic downturn reduced both demand for our products and metals prices; |

| • | the metals distribution business is very competitive and increased competition could reduce our gross margins and net income; |

| • | we may not be able to sustain the annual cost savings realized as part of our cost reduction initiatives; and |

| • | we may not be able to successfully consummate and complete the integration of future acquisitions, and if we are unable to do so, we may be unable to increase our growth rates. |

Recent Developments

Stock Split

On , 2013, our Board of Directors approved a for 1.00 stock split of the Company’s common stock to be effected prior to the closing of this offering. Our consolidated financial statements as of December 31, 2012 and 2011 and for the years ended December 31, 2012, 2011 and 2010 give retroactive effect to the stock split.

The Sponsor

Platinum Equity, LLC (together with its affiliates, “Platinum Equity”) is a global acquisition firm headquartered in Beverly Hills, California with principal offices in New York, Boston and London. Since its founding in 1995, Platinum Equity has completed more than 145 acquisitions in a broad range of market sectors including packaging, technology, industrials, logistics, distribution, maintenance and service. Platinum Equity’s current portfolio includes over 30 companies in a variety of different industries that serve customers around the world. Platinum Equity has a diversified capital base that includes the assets of its portfolio companies, which generated more than $15 billion in revenue in 2012, as well as capital commitments from institutional investors in private equity funds managed by the firm. Platinum Equity’s M&A&O® (Mergers & Acquisitions & Operations) approach to investing focuses on acquiring businesses that need operational support to realize their full potential and can benefit from Platinum Equity’s expertise in transition, integration and operations.

Joseph T. Ryerson & Son, Inc. (“JT Ryerson”), one of our subsidiaries, is party to a corporate advisory services agreement (the “Services Agreement”) with Platinum Advisors, an affiliate of Platinum. In connection with this offering, Platinum Advisors and JT Ryerson intend to terminate the Services Agreement, pursuant to which JT Ryerson will pay Platinum Advisors $ million as consideration for terminating the Services Agreement. We refer to this as the “Services Agreement Termination.” See “Certain Relationships and Related Party Transactions—Services Agreement.” Upon the consummation of this offering, the Company and Platinum

9

Table of Contents

will enter into an amended and restated investor rights agreement (the “Investor Rights Agreement”) which will provide, among other things, that for so long as Platinum collectively beneficially owns (i) at least 30% of the voting power of the outstanding capital stock of the Company, Platinum will have the right to nominate for election to the board of directors of the Company no fewer than that number of directors that would constitute a majority of the number of directors if there were no vacancies on the board, (ii) at least 15% but less than 30% of the voting power of the outstanding capital stock of the Company, Platinum will have the right to nominate two directors and (iii) at least 5% but less than 15% of the voting power of the outstanding capital stock of the Company, Platinum will have the right to nominate one director. For additional information with respect to Platinum’s rights pursuant to the Investor Rights Agreement, see “Certain Relationships and Related Party Transactions—Investor Rights Agreement.”

10

Table of Contents

Corporate Structure

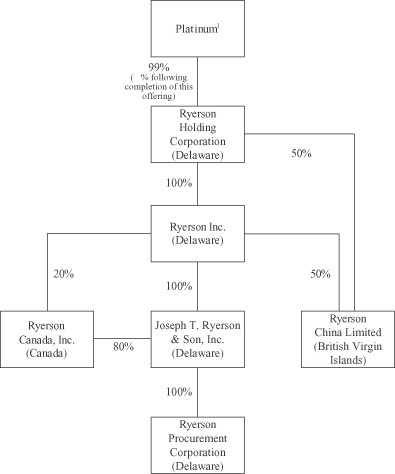

Our current corporate structure is made up as follows: Ryerson Holding, the issuer of the common stock offered hereby, owns all of the common stock of Ryerson Inc. and all of the membership interests of Rhombus JV Holdings, LLC. Ryerson Inc. owns, directly or indirectly, all of the common stock of the following entities: JT Ryerson; Ryerson Americas, Inc.; Ryerson International, Inc.; Ryerson Pan-Pacific LLC; J.M. Tull Metals Company, Inc.; RdM Holdings, Inc.; RCJV Holdings, Inc.; Ryerson Procurement Corporation; Ryerson International Material Management Services, Inc.; Ryerson International Trading, Inc.; Ryerson Canada, Inc.; Ryerson Metals de Mexico, S. de R.L. de C.V.; 862809 Ontario, Inc.; Leets Assurance, Ltd.; Integris Metals Mexicana, S.A. de C.V.; Servicios Empresariales Ryerson Tull, S.A. de C.V.; Servicios Corporativos RIM, S.A. de C.V.; Turret Holding Corporation; Turret Steel Industries, Inc.; Turret Steel Canada, ULC; Sunbelt-Turret Steel, Inc.; Ryerson Brasil Participacoes Ltda; Ryerson Holdings (Brazil), LLC; EPE LLC; Ryerson Canada Finance ULC; Imperial Trucking Company, LLC; Wilcox-Turret Cold Drawn, Inc.; and Ryerson Holdings (India) Pte Ltd. Platinum currently owns 99% of the capital stock of Ryerson Holding and will own approximately % of the capital stock following this offering. The chart below illustrates in summary form our material operating subsidiaries.

| 1 | Platinum refers to the following entities: Platinum Equity Capital Partners, L.P.; Platinum Equity Capital Partners-PF, L.P.; Platinum Equity Capital Partners-A, L.P.; Platinum Equity Capital Partners II, L.P.; Platinum Equity Capital Partners-PF II, L.P.; Platinum Equity Capital Partners-A II, L.P.; and Platinum Rhombus Principals, LLC. For additional detail regarding ownership by Platinum, see “Principal and Selling Stockholders.” |

11

Table of Contents

Corporate Information

Ryerson Holding and Ryerson Inc. are each incorporated under the laws of the State of Delaware. Ryerson Holding was formed in July 2007. Our principal executive offices are located at 227 W. Monroe, 27th Floor, Chicago, Illinois 60606. Our telephone number is (312) 292-5000.

On January 1, 2006, Ryerson Inc. changed its name from Ryerson Tull, Inc. to Ryerson Inc. On January 4, 2010, Ryerson Holding changed its name from Rhombus Holding Corporation to Ryerson Holding Corporation. Our website is located at www.ryerson.com. Our website and the information contained on the website or connected thereto will not be deemed to be incorporated into this prospectus and you should not rely on any such information in making your decision whether to purchase our securities.

12

Table of Contents

The Offering

| Issuer |

Ryerson Holding Corporation. |

| Common stock offered by us |

shares. |

| Underwriters’ over-allotment option to purchase additional common stock from the selling stockholders |

Up to shares. |

| Common stock outstanding before this offering |

5,000,000 shares. |

| Common stock to be outstanding immediately following this offering |

shares. |

| Use of proceeds |

We estimate that our net proceeds from this offering will be approximately $ million, assuming an initial public offering price of $ per share, the mid-point of the estimated initial public offering price range. |

We intend to use the net proceeds to us from this offering to (i) redeem $ in aggregate principal amount of the 11.25% Senior Notes due 2018 issued by Ryerson and its wholly owned subsidiary Joseph T. Ryerson & Son Inc. (the “2018 Notes”), (ii) repay approximately $ of the borrowings outstanding under our $1.35 billion revolving credit facility agreement that matures on the earlier of (a) April 3, 2018 or (b) August 16, 2017 (60 days prior to the scheduled maturity date of the 2017 Notes), if the 2017 Notes are then outstanding (as amended, the “Ryerson Credit Facility”), (iii) pay Platinum Advisors $ as consideration for terminating the Services Agreement, (iv) redeem up to $ in aggregate principal amount of the 9% Senior Secured Notes due 2017 issued by Ryerson and its wholly owned subsidiary Joseph T. Ryerson & Son Inc. (the “2017 Notes” and together with the 2018 Notes, the “2017 and 2018 Notes”) and (v) pay related transaction fees, expenses and premiums in connection with this offering, which we currently expect to equal approximately $22.0 million.

| If the over-allotment is exercised, we will not receive any proceeds from the sale of our common stock by the selling stockholders. |

| Risk factors |

See “Risk Factors” on page 17 of this prospectus for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

| Dividend policy |

We do not anticipate declaring or paying any regular cash dividends on our common stock in the foreseeable future. Any payment of cash dividends on our common stock in the future will be at the discretion of our Board of Directors and will depend upon our results of operations, earnings, capital requirements, financial condition, future prospects, contractual restrictions, including under the Ryerson Credit Facility and our outstanding notes, and other factors deemed relevant by our Board of Directors. |

13

Table of Contents

| Proposed New York Stock Exchange symbol |

“RYI.” |

| Directed share program |

At our request, the underwriters have reserved up to 5% of the shares of common stock for sale at the initial public offering price to persons who are employees, officers, directors and other parties associated with us through a directed share program. The number of shares of common stock available for sale to the general public will be reduced by the number of directed shares purchased by participants in the program. Any directed shares not purchased will be offered by the underwriters to the general public on the same basis as all other shares of common stock offered. We have agreed to indemnify the underwriters against certain liabilities and expenses, including liabilities under the Securities Act, in connection with the sales of the directed shares. Individuals who purchase shares in excess of $1,000,000 in the directed share program will be subject to a 25-day lock-up period, except that any of our executive officers or directors or any selling stockholders who purchase shares in the directed share program will remain subject to the 180-day lock-up period from the date of this prospectus, as described in “Underwriting—No Sales of Similar Securities.” |

The number of shares to be outstanding after this offering is based on 5,000,000 shares of common stock outstanding immediately before this offering and the shares of common stock being sold by us in this offering, and assumes no exercise by the underwriters of their option to purchase shares of our common stock in this offering to cover over-allotments, if any. The number of shares to be outstanding after this offering excludes shares of common stock reserved for future grants under our stock incentive plan assuming such plan is adopted in connection with this offering.

Unless we specifically state otherwise, the information in this prospectus assumes:

| • | an initial public offering price of $ per share, the mid-point of the offering range set forth on the cover page of this prospectus; |

| • | the underwriters do not exercise their over-allotment option; and |

| • | a for 1.00 stock split that will occur prior to the closing of this offering. |

14

Table of Contents

Summary Historical Consolidated Financial and Other Data

The following table presents our summary historical consolidated financial data, as of the dates and for the periods indicated. Our summary historical consolidated statements of operations data for the years ended December 31, 2010, 2011 and 2012 and the summary historical balance sheet data as of December 31, 2011 and 2012 have been derived from our audited consolidated financial statements included elsewhere in this prospectus.

Our selected historical consolidated financial data as of September 30, 2012 and 2013 and for the nine months ended September 30, 2012 and 2013 have been derived from our unaudited consolidated financial statements included elsewhere in this prospectus. The September 30, 2012 and 2013 unaudited financial statements have been prepared on a basis consistent with our audited consolidated financial statements and reflect all adjustments, consisting of normal recurring adjustments that are, in the opinion of management, necessary for a fair presentation of the financial position and results of operations for the periods presented. The results of any interim period are not necessarily indicative of the results that may be expected for any other interim period or for the full fiscal year, and the historical results set forth below do not necessarily indicate results expected for any future period.

You should read the summary financial and other data set forth below along with the sections in this prospectus entitled “Use of Proceeds,” “Selected Consolidated Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and related notes included elsewhere in this prospectus. The share and per share information presented below has been adjusted to give effect to the for 1.00 stock split that will occur immediately prior to the closing of this offering.

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||||

| 2010 | 2011 | 2012 | 2012 | 2013 | ||||||||||||||||

| ($ in millions) | ||||||||||||||||||||

| Statements of Operations Data: |

||||||||||||||||||||

| Net sales |

$ | 3,895.5 | $ | 4,729.8 | $ | 4,024.7 | $ | 3,174.4 | $ | 2,657.8 | ||||||||||

| Cost of materials sold |

3,355.7 | 4,071.0 | 3,315.1 | 2,619.1 | 2,188.4 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Gross profit |

539.8 | 658.8 | 709.6 | 555.3 | 469.4 | |||||||||||||||

| Warehousing, selling, general and administrative |

506.9 | 539.7 | 508.9 | 389.9 | 363.2 | |||||||||||||||

| Restructuring and other charges |

12.0 | 11.1 | 1.1 | — | 2.1 | |||||||||||||||

| Gain on insurance settlement |

(2.6 | ) | — | — | — | — | ||||||||||||||

| Impairment charges on fixed assets and goodwill |

1.4 | 9.3 | 1.0 | 0.9 | 8.8 | |||||||||||||||

| Pension and other postretirement benefits curtailment (gain) loss |

2.0 | — | (1.7 | ) | — | — | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating profit |

20.1 | 98.7 | 200.3 | 164.5 | 95.3 | |||||||||||||||

| Other income and (expense), net (1) |

(3.2 | ) | 4.6 | (33.5 | ) | (1.0 | ) | 2.1 | ||||||||||||

| Interest and other expense on debt (2) |

(107.5 | ) | (123.1 | ) | (126.5 | ) | (97.6 | ) | (83.3 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) before income taxes |

(90.6 | ) | (19.8 | ) | 40.3 | 65.9 | 14.1 | |||||||||||||

| Provision (benefit) for income taxes (3) |

13.1 | (11.0 | ) | (5.5 | ) | 9.6 | 5.9 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) |

(103.7 | ) | (8.8 | ) | 45.8 | 56.3 | 8.2 | |||||||||||||

| Less: Net income (loss) attributable to noncontrolling interest |

0.3 | (0.7 | ) | (1.3 | ) | (0.7 | ) | (0.9 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) attributable to Ryerson Holding Corporation |

$ | (104.0 | ) | $ | (8.1 | ) | $ | 47.1 | $ | 57.0 | $ | 9.1 | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

15

Table of Contents

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||||

| 2010 | 2011 | 2012 | 2012 | 2013 | ||||||||||||||||

| ($ in millions, except per share data) | ||||||||||||||||||||

| Earnings (loss) per share of common stock: |

||||||||||||||||||||

| Basic earnings (loss) per share |

$ | (20.80 | ) | $ | (1.62 | ) | $ | 9.41 | $ | 11.41 | $ | 1.82 | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Diluted earnings (loss) per share |

$ | (20.80 | ) | $ | (1.62 | ) | $ | 9.41 | $ | 11.41 | $ | 1.82 | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Weighted average shares outstanding — Basic |

5.0 | 5.0 | 5.0 | 5.0 | 5.0 | |||||||||||||||

| Weighted average shares outstanding — Diluted |

5.0 | 5.0 | 5.0 | 5.0 | 5.0 | |||||||||||||||

| Balance Sheet Data (at period end): |

||||||||||||||||||||

| Cash and cash equivalents |

$ | 62.6 | $ | 61.7 | $ | 71.2 | $ | 54.4 | $ | 81.1 | ||||||||||

| Restricted cash |

15.6 | 5.3 | 3.9 | 4.3 | 4.6 | |||||||||||||||

| Inventory |

783.4 | 732.4 | 741.5 | 779.8 | 702.8 | |||||||||||||||

| Working capital |

858.8 | 806.6 | 796.7 | 801.4 | 738.9 | |||||||||||||||

| Property, plant and equipment, net |

479.2 | 479.7 | 472.3 | 478.9 | 450.4 | |||||||||||||||

| Total assets |

2,053.5 | 2,058.4 | 1,954.1 | 2,056.4 | 1,922.5 | |||||||||||||||

| Long-term debt, including current maturities |

1,211.3 | 1,316.2 | 1,305.4 | 1,260.1 | 1,240.1 | |||||||||||||||

| Other Financial Data: |

||||||||||||||||||||

| Cash flows provided by (used in) operations |

$ | (198.7 | ) | $ | 54.5 | $ | 186.5 | $ | 86.1 | $ | 88.0 | |||||||||

| Cash flows used in investing activities |

(44.4 | ) | (115.0 | ) | (35.3 | ) | (29.5 | ) | (12.9 | ) | ||||||||||

| Cash flows provided by (used in) financing activities |

185.1 | 57.9 | (143.4 | ) | (65.5 | ) | (62.5 | ) | ||||||||||||

| Capital expenditures |

27.0 | 47.0 | 40.8 | 32.0 | 16.5 | |||||||||||||||

| Depreciation and amortization |

38.4 | 43.0 | 47.0 | 34.6 | 34.7 | |||||||||||||||

| EBITDA (4) |

55.0 | 147.0 | 215.1 | 198.8 | 133.0 | |||||||||||||||

| Adjusted EBITDA (4) |

81.1 | 174.5 | 264.7 | 212.7 | 154.7 | |||||||||||||||

| Adjusted EBITDA, excluding LIFO (4) |

133.5 | 223.1 | 201.6 | 166.3 | 128.1 | |||||||||||||||

| Ratio of Tangible Assets to Total Net Debt (5) |

1.5x | 1.4x | 1.3x | 1.4x | 1.4x | |||||||||||||||

| Volume and Per Ton Data: |

||||||||||||||||||||

| Tons shipped (000) |

2,252 | 2,433 | 2,149 | 1,671 | 1,559 | |||||||||||||||

| Average number of employees |

4,126 | 4,236 | 4,021 | 4,061 | 3,888 | |||||||||||||||

| Tons shipped per employee |

546 | 574 | 534 | 411 | 401 | |||||||||||||||

| Average selling price per ton |

$ | 1,730 | $ | 1,944 | $ | 1,873 | $ | 1,900 | $ | 1,705 | ||||||||||

| Gross profit per ton |

240 | 271 | 330 | 332 | 301 | |||||||||||||||

| Operating profit per ton |

9 | 41 | 93 | 98 | 61 | |||||||||||||||

| (1) | The year ended December 31, 2010 includes $2.6 million of foreign exchange losses related to the repayment of a long-term loan to our Canadian operations. The year ended December 31, 2011 includes a $5.8 million gain on bargain purchase related to our Singer acquisition. The year ended December 31, 2012 includes a $32.8 million loss on the redemption of the Ryerson Notes and Ryerson Holding Notes. |

| (2) | The year ended December 31, 2011 includes a $1.1 million write off of debt issuance costs associated with our prior credit facility upon entering into an amended revolving credit facility on March 14, 2011. |

| (3) | The year ended December 31, 2011 includes income tax benefits of $18.0 million relating to the purchase accounting impact of the Turret and Singer acquisitions. The year ended December 31, 2012 includes an income tax benefit of $15.2 million related to the release of valuation allowance associated with certain state deferred tax assets. |

| (4) | EBITDA, for the periods presented, represents net income before interest and other expense on debt, provision for income taxes, depreciation and amortization. Adjusted EBITDA gives further effect to, among other things, loss on retirement of debt, impairment charges on fixed assets and goodwill, reorganization expenses and the payment of management fees. We believe that the presentation of EBITDA, Adjusted EBITDA and Adjusted EBITDA, excluding LIFO expense (income) provides useful information to investors regarding our operational performance because they enhance an investor’s overall understanding of our core financial performance and provide a basis of comparison of results between current, past and future periods. We also disclose the metric Adjusted EBITDA, excluding LIFO expense (income), to provide a means of comparison amongst our competitors who may not use the same basis of accounting for inventories. EBITDA, Adjusted EBITDA and Adjusted EBITDA, excluding LIFO expense (income) are three of the primary metrics management uses for planning and forecasting in future periods, including trending and analyzing the core operating performance of our business without the effect of U.S. generally |

16

Table of Contents

| accepted accounting principles, or GAAP, expenses, revenues and gains (losses) that are unrelated to the day to day performance of our business. We also establish compensation programs for our executive management and regional employees that are based upon the achievement of pre-established EBITDA, Adjusted EBITDA and Adjusted EBITDA, excluding LIFO expense (income) targets. We also use EBITDA, Adjusted EBITDA and Adjusted EBITDA, excluding LIFO expense (income) to benchmark our operating performance to that of our competitors. EBITDA, Adjusted EBITDA and Adjusted EBITDA, excluding LIFO expense (income) do not represent, and should not be used as a substitute for, net income or cash flows from operations as determined in accordance with generally accepted accounting principles, and neither EBITDA, Adjusted EBITDA and Adjusted EBITDA, excluding LIFO expense (income) is necessarily an indication of whether cash flow will be sufficient to fund our cash requirements. Our definitions of EBITDA, Adjusted EBITDA and Adjusted EBITDA, excluding LIFO expense (income) may differ from that of other companies. Set forth below is the reconciliation of net income to EBITDA, as further adjusted to Adjusted EBITDA and Adjusted EBITDA, excluding LIFO expense (income). |

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||||

| 2010 | 2011 | 2012 | 2012 | 2013 | ||||||||||||||||

| ($ in millions) | ||||||||||||||||||||

| Net income (loss) attributable to Ryerson Holding |

$ | (104.0 | ) | $ | (8.1 | ) | $ | 47.1 | $ | 57.0 | $ | 9.1 | ||||||||

| Interest and other expense on debt |

107.5 | 123.1 | 126.5 | 97.6 | 83.3 | |||||||||||||||

| Provision (benefit) for income taxes |

13.1 | (11.0 | ) | (5.5 | ) | 9.6 | 5.9 | |||||||||||||

| Depreciation and amortization |

38.4 | 43.0 | 47.0 | 34.6 | 34.7 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| EBITDA |

55.0 | 147.0 | 215.1 | 198.8 | 133.0 | |||||||||||||||

| Reorganization |

19.1 | 17.8 | 5.8 | 4.7 | 8.5 | |||||||||||||||

| Advisory service fee |

5.0 | 5.0 | 5.0 | 3.8 | 3.8 | |||||||||||||||

| Loss on retirement of debt |

— | — | 32.8 | — | — | |||||||||||||||

| Foreign currency transaction (gains) losses |

2.7 | 0.8 | 1.5 | 1.6 | (1.6 | ) | ||||||||||||||

| Gain on insurance settlement |

(2.6 | ) | — | — | — | — | ||||||||||||||

| Impairment charges on fixed assets and goodwill |

1.4 | 9.3 | 1.0 | 0.9 | 8.8 | |||||||||||||||

| Gain on bargain purchase |

— | (5.8 | ) | — | — | — | ||||||||||||||

| Purchase consideration |

— | — | 4.3 | 3.5 | 2.7 | |||||||||||||||

| Other adjustments |

0.5 | 0.4 | (0.8 | ) | (0.6 | ) | (0.5 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted EBITDA |

81.1 | 174.5 | 264.7 | 212.7 | 154.7 | |||||||||||||||

| LIFO expense (income) |

52.4 | 48.6 | (63.1 | ) | (46.4 | ) | (26.6 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted EBITDA, excluding LIFO expense (income) |

$ | 133.5 | $ | 223.1 | $ | 201.6 | $ | 166.3 | $ | 128.1 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (5) | The table below sets forth the inputs used for the calculations of the ratio of tangible assets to total net debt for the years ended December 31, 2010, 2011 and 2012 and nine months ended September 30, 2012 and 2013. |

| Year ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||||

| 2010 | 2011 | 2012 | 2012 | 2013 | ||||||||||||||||

| ($ in millions) | ||||||||||||||||||||

| Receivables less provision for allowances, claims and doubtful accounts |

$ | 497.9 | $ | 513.9 | $ | 394.1 | $ | 484.4 | $ | 420.2 | ||||||||||

| Inventories |

783.4 | 732.4 | 741.5 | 779.8 | 702.8 | |||||||||||||||

| Assets held for sale |

14.3 | 10.0 | 3.6 | 3.7 | 4.5 | |||||||||||||||

| Property, plant and equipment, net of accumulated depreciation |

479.2 | 479.7 | 472.3 | 478.9 | 450.4 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Tangible Assets |

$ | 1,774.8 | $ | 1,736.0 | $ | 1,611.5 | $ | 1,746.8 | $ | 1,577.9 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Long-term debt, including current maturities |

$ | 1,211.3 | $ | 1,316.2 | $ | 1,305.4 | $ | 1,260.1 | $ | 1,240.1 | ||||||||||

| Less cash and cash equivalents |

(62.6 | ) | (61.7 | ) | (71.2 | ) | (54.4 | ) | (81.1 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Net Debt |

$ | 1,148.7 | $ | 1,254.5 | $ | 1,234.2 | $ | 1,205.7 | $ | 1,159.0 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Ratio of Tangible Assets to Total Net Debt |

1.5x | 1.4x | 1.3x | 1.4x | 1.4x | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

17

Table of Contents

Investing in our common stock involves a high degree of risk. You should carefully consider the risks described below, together with the other information contained in this prospectus, before making your decision to invest in shares of our common stock. We cannot assure you that any of the events discussed in the risk factors below will not occur. These risks could have a material and adverse impact on our business, results of operations, financial condition and cash flows. If that were to happen, the trading price of our common stock could decline, and you could lose all or part of your investment.

Risks Relating to Our Business

We service industries that are highly cyclical, and any downturn in our customers’ industries could reduce our sales and profitability. The economic downturn has reduced demand for our products and may continue to reduce demand until an economic recovery.

Many of our products are sold to industries that experience significant fluctuations in demand based on economic conditions, energy prices, seasonality, consumer demand and other factors beyond our control. These industries include manufacturing, electrical products and transportation. We do not expect the cyclical nature of our industry to change.

The U.S. economy entered an economic recession in December 2007, which spread to many global markets in 2008 and 2009 and affected Ryerson and other metals service centers. Beginning in late 2008 and continuing through 2013, the metals industry, including Ryerson and other service centers, felt additional effects of the global economic crisis and recovery thereto and the impact of the credit market disruption. These events contributed to a rapid decline in both demand for our products and pricing levels for those products. The Company has implemented a number of actions to conserve cash, reduce costs and strengthen its competitiveness, including curtailing non-critical capital expenditures, initiating headcount reductions and reductions of certain employee benefits, among other actions. However, there can be no assurance that these actions, or any others that the Company may take in response to further deterioration in economic and financial conditions, will be sufficient.

The volatility of the market could result in a material impairment of goodwill.

We evaluate goodwill annually on October 1 and whenever events or changes in circumstances indicate potential impairment. Events or changes in circumstances that could trigger an impairment review include significant underperformance relative to our historical or projected future operating results, significant changes in the manner or the use of our assets or the strategy for our overall business, and significant negative industry or economic trends. We test for impairment of goodwill by calculating the fair value of a reporting unit using an average of an income approach based on discounted future cash flows and a market approach at the date of valuation. Under the discounted cash flow method, the fair value of each reporting unit is estimated based on expected future economic benefits discounted to a present value at a rate of return commensurate with the risk associated with the investment. Projected cash flows are discounted to present value using an estimated weighted average cost of capital, which considers both returns to equity and debt investors. Significant changes in any one of the assumptions made as part of our analysis, which could occur as a result of actual events, or further declines in the market conditions for our products, could significantly impact our impairment analysis. An impairment charge, if incurred, could be material.

The metals distribution business is very competitive and increased competition could reduce our revenues and gross margins.

The principal markets that we serve are highly competitive. The metals distribution industry is fragmented and competitive, consisting of a large number of small companies and a few relatively large companies. Competition is based principally on price, service, quality, production capabilities, inventory availability and

18

Table of Contents

timely delivery. Competition in the various markets in which we participate comes from companies of various sizes, some of which have greater financial resources than we have and some of which have more established brand names in the local markets served by us. Increased competition could reduce our market share, force us to lower our prices or to offer increased services at a higher cost, which could reduce our profitability.

The economic downturn has reduced metals prices. Though prices have risen since the onset of the economic downturn, we cannot assure you that prices will continue to rise. Changing metals prices may have a significant impact on our liquidity, net sales, gross margins, operating income and net income.

The metals industry as a whole is cyclical and, at times, pricing and availability of metal can be volatile due to numerous factors beyond our control, including general domestic and international economic conditions, labor costs, sales levels, competition, levels of inventory held by other metals service centers, consolidation of metals producers, higher raw material costs for the producers of metals, import duties and tariffs and currency exchange rates. This volatility can significantly affect the availability and cost of materials for us.

We, like many other metals service centers, maintain substantial inventories of metal to accommodate the short lead times and just-in-time delivery requirements of our customers. Accordingly, we purchase metals in an effort to maintain our inventory at levels that we believe to be appropriate to satisfy the anticipated needs of our customers based upon historic buying practices, contracts with customers and market conditions. When metals prices decline, as they did in 2008 and 2009, customer demands for lower prices and our competitors’ responses to those demands could result in lower sale prices and, consequently, lower margins as we use existing metals inventory. Notwithstanding recent price increases, metals prices may decline, and declines in those prices or further reductions in sales volumes could adversely impact our ability to maintain our liquidity and to remain in compliance with certain financial covenants under the Ryerson Credit Facility, as well as result in us incurring inventory or goodwill impairment charges. Changing metals prices therefore could significantly impact our liquidity, net sales, gross margins, operating income and net income.

We have a substantial amount of indebtedness, which could adversely affect our financial position and prevent us from fulfilling our obligations.

We currently have a substantial amount of indebtedness, including, as of September 30, 2013, $600.0 million outstanding under our 2017 Notes and $300.0 million outstanding under our 2018 Notes, and may incur additional indebtedness in the future. As of September 30, 2013, after giving effect to this offering and the application of net proceeds from this offering our total indebtedness would have been approximately $ million and we would have had approximately $ million of unused capacity under the Ryerson Credit Facility. Our substantial indebtedness may:

| • | make it difficult for us to satisfy our financial obligations, including making scheduled principal and interest payments on our outstanding notes and our other indebtedness; |

| • | limit our ability to borrow additional funds for working capital, capital expenditures, acquisitions and general corporate and other purposes; |

| • | limit our ability to use our cash flow or obtain additional financing for future working capital, capital expenditures, acquisitions or other general corporate purposes; |

| • | require us to use a substantial portion of our cash flow from operations to make debt service payments; |

| • | limit our flexibility to plan for, or react to, changes in our business and industry; |

| • | place us at a competitive disadvantage compared to our less leveraged competitors; and |

| • | increase our vulnerability to the impact of adverse economic and industry conditions. |

We may also incur additional indebtedness in the future. The terms of the Ryerson Credit Facility and the indentures governing our outstanding notes restrict but do not prohibit us from doing so, and the indebtedness incurred in compliance with these restrictions could be substantial. If new indebtedness is added to our current debt levels, the related risks that we now face could intensify.

19

Table of Contents

The covenants in the Ryerson Credit Facility and the indentures governing our outstanding notes impose, and covenants contained in agreements governing indebtedness we incur in the future may impose, restrictions that may limit our operating and financial flexibility.

The Ryerson Credit Facility and the indentures governing our outstanding notes contain a number of significant restrictions and covenants that limit our ability and the ability of our restricted subsidiaries, including Ryerson Inc., to:

| • | incur additional debt; |

| • | pay dividends on our capital stock or repurchase our capital stock; |

| • | make certain investments or other restricted payments; |

| • | create liens or use assets as security in other transactions; |

| • | merge, consolidate or transfer or dispose of substantially all of our assets; and |

| • | engage in transactions with affiliates. |

The terms of the Ryerson Credit Facility require that, in the event availability under the facility declines to a certain level, we maintain a minimum fixed charge coverage ratio at the end of each fiscal quarter. Total credit availability is limited by the amount of eligible accounts receivable and inventory pledged as collateral under the agreement insofar as the Company is subject to a borrowing base comprised of the aggregate of these two amounts, less applicable reserves. As of September 30, 2013, total credit availability was $291 million based upon eligible accounts receivable and inventory pledged as collateral.