Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - United Financial Bancorp, Inc. | form8-k.htm |

| EX-99.1 - EXHIBIT 99.1 - United Financial Bancorp, Inc. | ex99-1.htm |

+ Creating A Premier New England Community Bank Through a Transformational Merger-of-Equals Strictly Private and Confidential November 15, 2013 NASDAQ: RCKB NASDAQ: UBNK

* This document contains forward looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 giving Rockville Financial, Inc.’s (“Rockville”) or United Financial Bancorp, Inc.’s (“United”) expectations or predictions of future financial or business performance or conditions. Forward-looking statements are typically identified by words such as “believe,” “expect,” “anticipate,” “intend,” “target,” “estimate,” “continue,” “positions,” “prospects” or “potential,” by future conditional verbs such as “will,” “would,” “should,” “could” or “may”, or by variations of such words or by similar expressions. Such forward-looking statements include, but are not limited to, statements about the benefits of the business combination transaction involving United and Rockville, including future financial and operating results, the combined company’s plans, objectives, expectations and intentions and other statements that are not historical facts. These forward-looking statements are subject to numerous assumptions, risks and uncertainties which change over time. Forward-looking statements speak only as of the date they are made and neither Rockville nor United assumes any duty to update forward-looking statements. In addition to factors previously disclosed in Rockville’s and United’s reports filed with the Securities and Exchange Commission, the following factors, among others, could cause actual results to differ materially from forward-looking statements: ability to obtain regulatory approvals and meet other closing conditions to the merger, including approval by Rockville and United shareholders, on the expected terms and schedule; delay in closing the merger; difficulties and delays in integrating the Rockville and United businesses or fully realizing cost savings and other benefits; business disruption following the proposed transaction; changes in asset quality and credit risk; the inability to sustain revenue and earnings growth; changes in interest rates and capital markets; inflation; customer borrowing, repayment, investment and deposit practices; customer disintermediation; the introduction, withdrawal, success and timing of business initiatives; competitive conditions; the inability to realize cost savings or revenues or to implement integration plans and other consequences associated with mergers, acquisitions and divestitures; economic conditions; changes in Rockville’s stock price before closing, including as a result of the financial performance of United prior to closing; the reaction to the transaction of the companies’ customers, employees and counterparties; and the impact, extent and timing of technological changes, capital management activities, and other actions of the Federal Reserve Board and legislative and regulatory actions and reforms. Annualized, pro forma, projected and estimated numbers are used for illustrative purpose only, are not forecasts and may not reflect actual results. Cautionary Statements Regarding Forward-Looking Information

* Additional Information for Stockholders In connection with the proposed merger, Rockville will file with the Securities and Exchange Commission (“SEC”) a Registration Statement on Form S-4 that will include a joint proxy statement of Rockville and United and a prospectus of Rockville, as well as other relevant documents concerning the proposed transaction. Rockville and United will mail the joint proxy statement/prospectus to their stockholders. SHAREHOLDERS OF ROCKVILLE AND UNITED ARE URGED TO READ THE REGISTRATION STATEMENT AND JOINT PROXY STATEMENT/PROSPECTUS REGARDING THE PROPOSED MERGER WHEN IT BECOMES AVAILABLE AND ANY OTHER RELEVANT DOCUMENTS FILED WITH THE SEC, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THOSE DOCUMENTS, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Investors and security holders may obtain a free copy of the proxy statement/prospectus (when available) and other filings containing information about Rockville and United at the SEC’s website at www.sec.gov. The joint proxy statement/prospectus (when available) and the other filings may also be obtained free of charge at Rockville’s website at www.Rockvillebank.com under the section “SEC Filings” or at United’s website at www.bankatUnited.com under the tab “About Us” and then “Investor Relations,” and then under the heading “SEC Filings.” Rockville, United and certain of their respective directors and executive officers, under the SEC’s rules, may be deemed to be participants in the solicitation of proxies of Rockville’s and United’s shareholders in connection with the proposed merger. Information about the directors and executive officers of Rockville and their ownership of Rockville common stock is set forth in the proxy statement for Rockville’s 2013 Annual Meeting of Shareholders, as filed with the SEC on Schedule 14A on April 4, 2013. Information about the directors and executive officers of United and their ownership of United common stock is set forth in the proxy statement for United’s 2013 Annual Meeting of Shareholders, as filed with the SEC on a Schedule 14A on March 13, 2013. Additional information regarding the interests of those participants and other persons who may be deemed participants in the transaction may be obtained by reading the joint proxy statement/prospectus regarding the proposed merger when it becomes available. Free copies of this document may be obtained as described in the preceding paragraph.

* Transaction Highlights Strategically Compelling Creates a leading New England bank with $4.8 billion in assets and over 50 branches in two states with the size, scale and product breadth to compete effectively #1 community bank in combined Hartford and Springfield market Fortifies both companies’ position within the “Knowledge Corridor” (20th largest metropolitan area if considered as a single MSA) Better positioned for future growth Complementary branch networks provide both greater market density, opportunities for consolidation and unique franchise scarcity value Enhanced management team, bringing strengths from both sides Highly compatible cultures with similar strategies, customer focus and strong service and community orientation 2015E EPS accretion of 35% Manageable tangible book dilution with earnback of less than 5 years High teens IRR Post integration ROAA > 1% and ROATCE approaching 10% Meaningful potential revenue synergies, indentified but not modeled, provide additional upside Strong pro forma capital position supports future growth and capital management Attractively valued with significant upside potential Financially Attractive True merger-of-equals creating the largest community bank headquartered in the Hartford - Springfield market, western New England's largest metro area.

* Transaction Overview Based on Rockville closing price of $13.62 on November 14, 2013. Consideration Exchange ratio of 1.3472x Rockville shares for each United share. 100% stock Implied Transaction value of $369 million / $18.35 per share(1) Pro Forma Ownership Approximately 49% Rockville / 51% United of fully diluted shares outstanding Legal and Accounting Acquirer Rockville Financial, Inc. Name and Executive Offices United Financial Bancorp, Inc. (holding company) and United Bank (bank) - Surviving Ticker: UBNK Executive offices in Glastonbury and West Springfield Management CEO: William H.W. Crawford IV (Rockville) President: J. Jeffrey Sullivan (United) Richard B. Collins to retire and have a one-year consulting agreement and two-year non-compete Other key executive positions filled from executive management of both organizations Board Composition Chairman of the Board: Robert A. Stewart Jr. (United), Vice Chairman: Raymond H. Lefurge Jr. (Rockville) 20 total – 10 Rockville / 10 United including William H.W. Crawford IV and J. Jeffrey Sullivan Five Board Committees, Committee Chairs divided between Rockville and United Board parity contractually guaranteed for three years Required Approvals Customary regulatory approvals and shareholder approvals of both Rockville and United Targeted Closing Mid 2014 Due Diligence Extensive due diligence, including 3rd party loan review

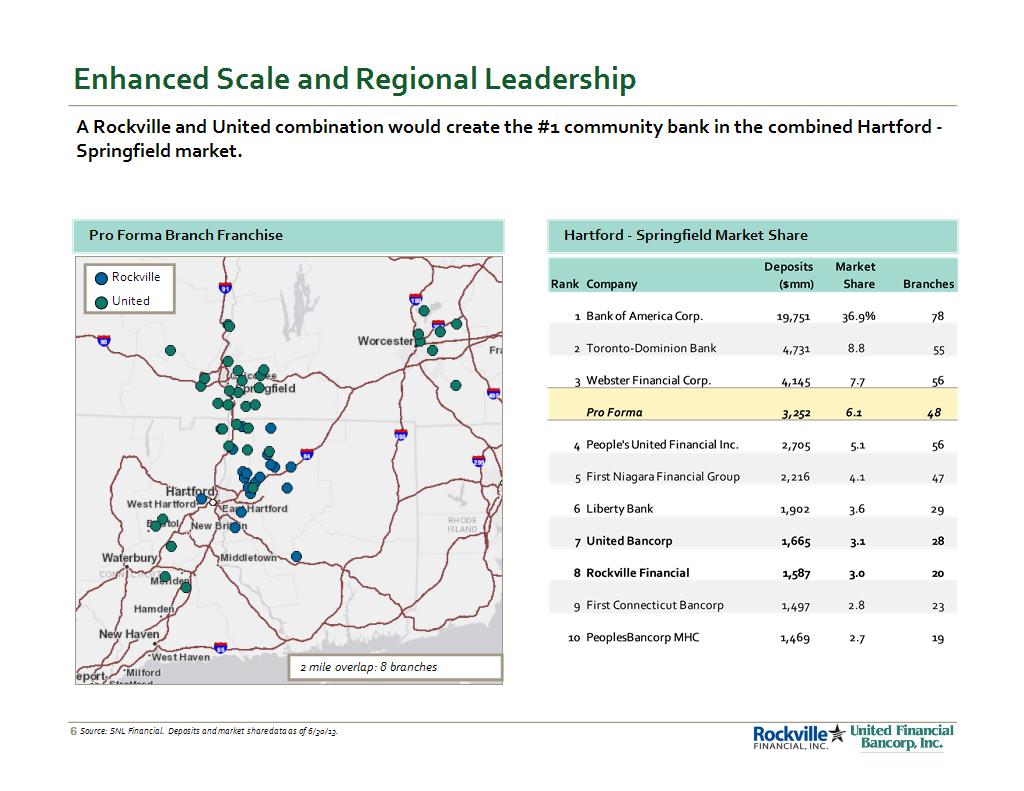

* Enhanced Scale and Regional Leadership A Rockville and United combination would create the #1 community bank in the combined Hartford - Springfield market. Pro Forma Branch Franchise Hartford – Springfield Market Share Source: SNL Financial. Deposits and market share data as of 6/30/13. Rockville United 2 mile overlap: 8 branches

* Hartford – Springfield is the largest metro area in western New England Total combined population of 2.8 million - would rank as 20th largest metro area if taken as a single MSA “Knowledge Corridor” is home to 41 colleges and universities with 215,000 students Region has a workforce of 1.25 million and over 64,000 businesses, is home to six Fortune 500 companies and has a combined GDP exceeding $100 billion a year, more than 16 U.S. states New Haven is the 2nd largest city in Connecticut and home to Yale University Worcester, an hour distance from Boston, Springfield, Providence and Hartford, is New England’s fastest growing metro market Favorable competitive dynamics as these markets are dominated by large out-of-market banks Large Markets with Significant Growth Potential Source: SNL Financial. Deposits and market share data as of 6/30/13. “New England’s Knowledge Corridor” State of the Region Annual Report, June 7, 2013. The combined franchise will serve an area with over 3.4 million people and have top 5 share in its core Hartford and Springfield markets while Worcester and New Haven offer additional avenues for growth.

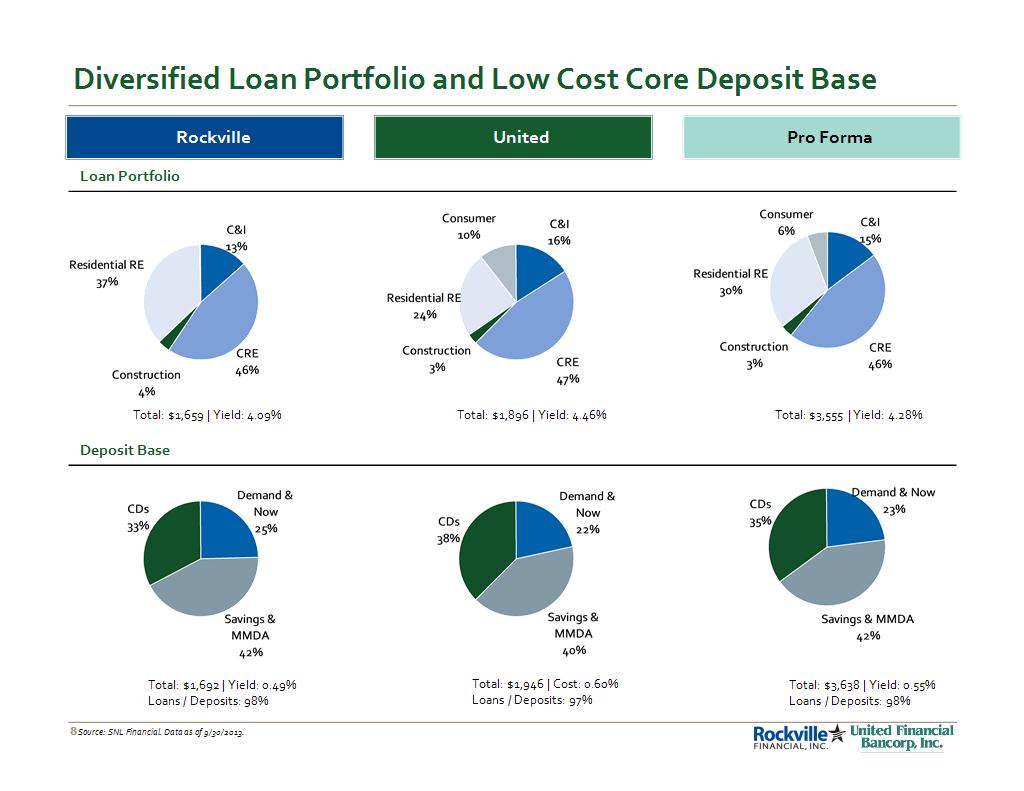

* Diversified Loan Portfolio and Low Cost Core Deposit Base Rockville United Pro Forma Loan Portfolio Deposit Base Total: $1,659 | Yield: 4.09% Total: $1,896 | Yield: 4.46% Total: $3,555 | Yield: 4.28% Total: $1,692 | Yield: 0.49% Loans / Deposits: 98% Total: $1,946 | Cost: 0.60% Loans / Deposits: 97% Total: $3,638 | Yield: 0.55% Loans / Deposits: 98% Source: SNL Financial. Data as of 9/30/2013.

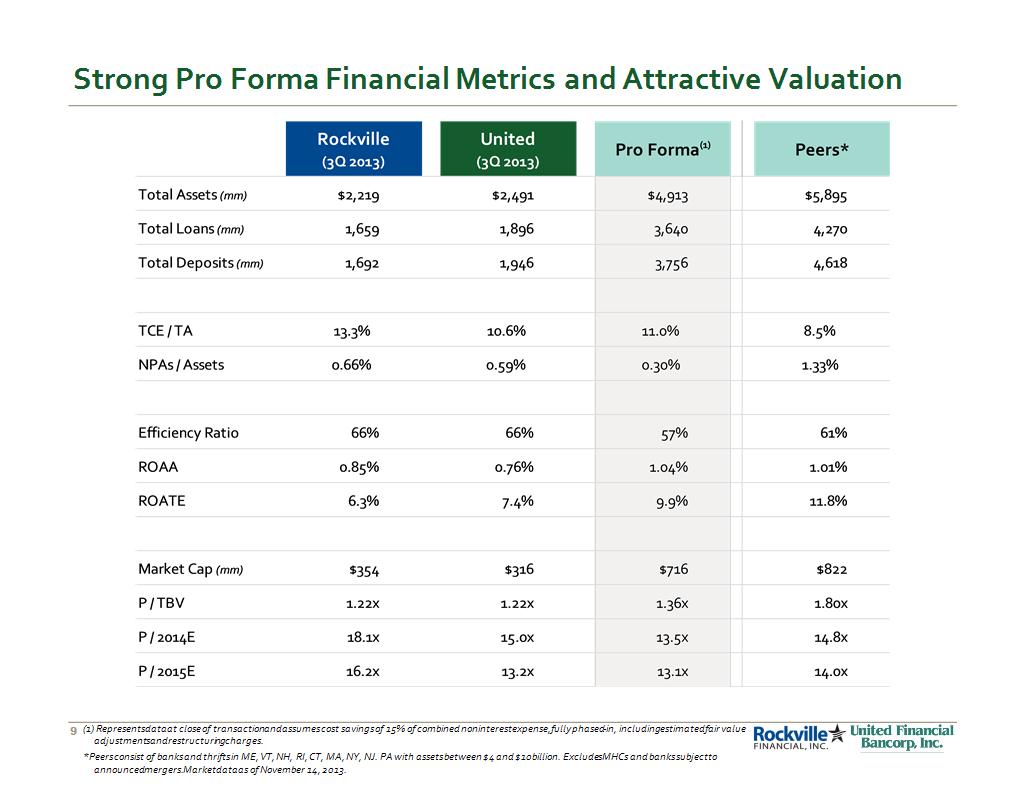

* Strong Pro Forma Financial Metrics and Attractive Valuation (1) Represents data at close of transaction and assumes cost savings of 15% of combined noninterest expense, fully phased-in, including estimated fair value adjustments and restructuring charges. *Peers consist of banks and thrifts in ME, VT, NH, RI, CT, MA, NY, NJ. PA with assets between $4 and $10 billion. Excludes MHCs and banks subject to announced mergers. Market data as of November 14, 2013.

* Potential Upside from Improved Return on Equity Rockville United Pro Forma Price to Tangible Book is highly correlated to ROATE. The pro forma company will have a significantly higher ROATE. Source: SNL Financial. Banks and thrifts in ME, VT, NH, RI, CT, MA, NY, NJ, PA with assets between $4 billion and $10 billion, that and excludes banks subject to announced mergers, MHCs or traded on OTCQB or Pink Sheets and have 2015 ROE estimates. Market data as of November 14, 2013.

* Donna Patel Virtual Channel Banking Strong Proposed Combined Team Focused on Execution William H.W. Crawford IV CEO Eric R. Newell CFO J. Jeffrey Sullivan President Dena M. Hall Marketing Miriam J. Siegel Human Resources Scott C. Bechtle CRO Marino J. Santarelli COO Marliese L. Shaw Corp Secretary / IR Select Management From United Select Management From Rockville Mark A. Kucia Head Commercial Banking Brandon C. Lorey Head Consumer Lending Board of Directors Charles R. Valade Commercial Regional Executive Nicholas Statalous Retail Operations S. Stephen Koniecki CTO Elizabeth K. Wynnick Internal Audit David Yaffee Financial Advisory Deborah M. Gebo Retail Administration Joan B. Klinakis Deposit Operations

* Comprehensive Integration Plan Integration Management Office (IMO) led by executive management of both Rockville and United Responsible for reporting to executive management, Board, and regulatory authorities An Integration Leader from IMO will be designated point person on all integration strategy IMO Work Groups established to focus on key areas including: Financial Reporting Human Resources Communication Technology IMO Action Teams formed for narrower, more specific projects Newly created Integration Management Office will facilitate successful execution of integration plan. Both Rockville and United senior executives have extensive merger and integration experience

* Significant Cost Savings Identified Cost savings estimated at $17.6 million, equal to 15% of combined overhead.

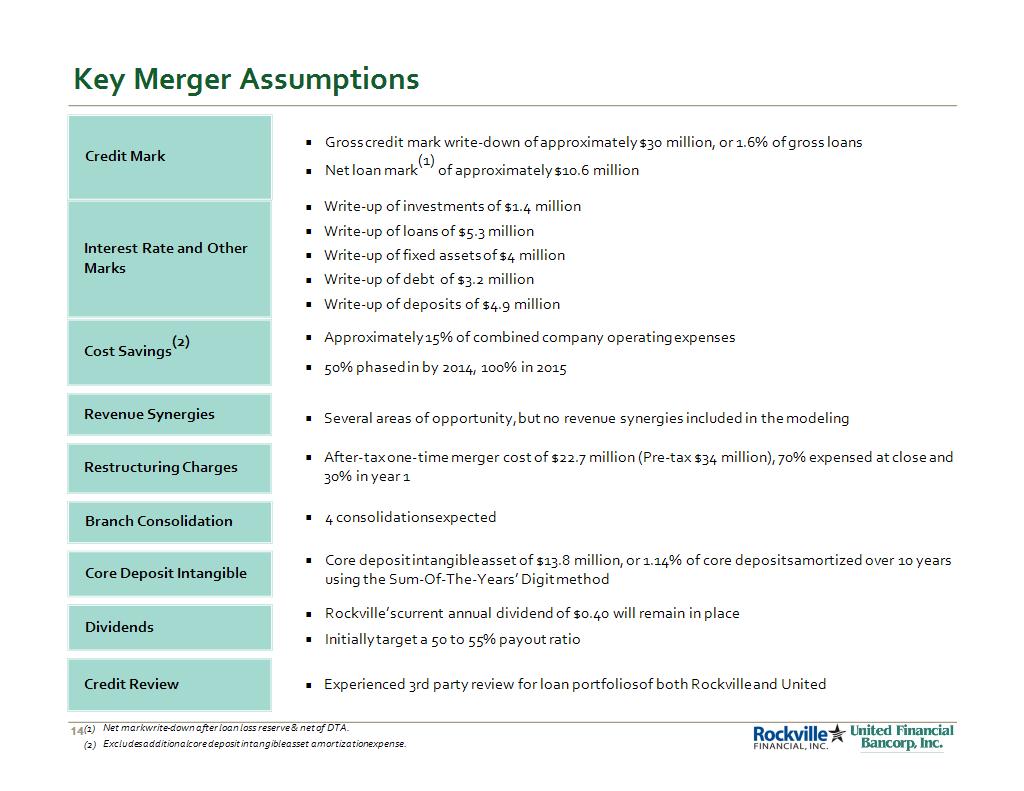

* Key Merger Assumptions Core Deposit Intangible Core deposit intangible asset of $13.8 million, or 1.14% of core deposits amortized over 10 years using the Sum-Of-The-Years’ Digit method Branch Consolidation 4 consolidations expected Revenue Synergies Several areas of opportunity, but no revenue synergies included in the modeling Interest Rate and Other Marks Write-up of investments of $1.4 million Write-up of loans of $5.3 million Write-up of fixed assets of $4 million Write-up of debt of $3.2 million Write-up of deposits of $4.9 million Restructuring Charges After-tax one-time merger cost of $22.7 million (Pre-tax $34 million), 70% expensed at close and 30% in year 1 Net mark write-down after loan loss reserve & net of DTA. Excludes additional core deposit intangible asset amortization expense. Credit Mark Gross credit mark write-down of approximately $30 million, or 1.6% of gross loans Net loan mark(1) of approximately $10.6 million Cost Savings(2) Approximately 15% of combined company operating expenses 50% phased in by 2014, 100% in 2015 Credit Review Experienced 3rd party review for loan portfolios of both Rockville and United Dividends Rockville’s current annual dividend of $0.40 will remain in place Initially target a 50 to 55% payout ratio

* Due Diligence Highlights Performed extensive, reciprocal due diligence, including 3rd party loan review. Rockville and United conducted a comprehensive reciprocal due diligence process including core systems, legal and credit Two tiered credit due diligence process completed by senior management and 3rd party loan review team for both banks Analyzed credit files, underwriting methodology and policy and portfolio management processes Rockville’s extensive credit reviews focused on the largest relationships, adversely classified assets and watch list loans Reviewed 100% of relationships with a balance greater than $1 million and sampled from $500 thousand and up Reviewed 73% of all total loans Reviewed 100% of adversely classified loans

* Favorable Pro Forma Impact EPS accretion of approximately 18% in 2014 EPS accretion of approximately 35% in 2015 EPS 11.1% dilution expected at closing Tangible Book value earnback of 4.7 years (using cross over method) Tangible Book Value IRR of 19% ROIC of 11% IRR and ROIC TCE / TA ~ 11% at close Capital

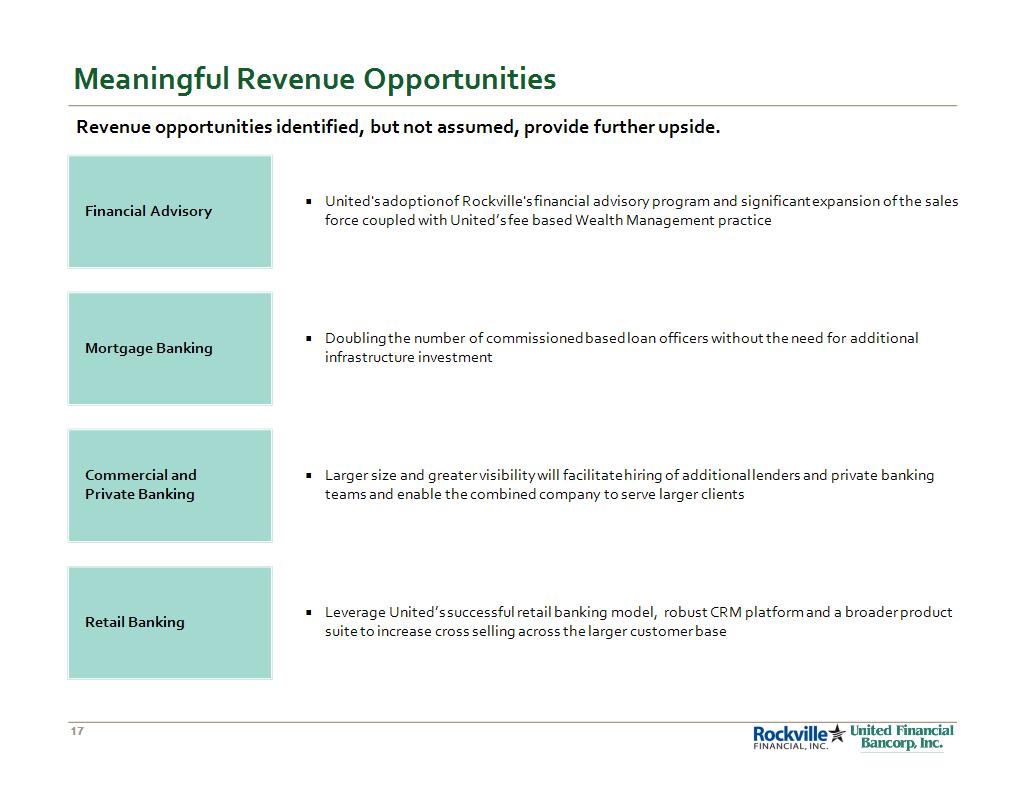

* Meaningful Revenue Opportunities Revenue opportunities identified, but not assumed, provide further upside. Retail Banking Leverage United’s successful retail banking model, robust CRM platform and a broader product suite to increase cross selling across the larger customer base Commercial and Private Banking Larger size and greater visibility will facilitate hiring of additional lenders and private banking teams and enable the combined company to serve larger clients Mortgage Banking Doubling the number of commissioned based loan officers without the need for additional infrastructure investment Financial Advisory United's adoption of Rockville's financial advisory program and significant expansion of the sales force coupled with United’s fee based Wealth Management practice

* Value Creating Transaction for Both Sets of Shareholders Rockville United Premium to Current Stock Price 25+% Earning Accretion 1%+ Return on Assets ROATCE Approaching 10% Better Positioned for Growth Greater Franchise Scarcity Value Significant Stock Upside 20%+ Cash Dividend Pickup Improved Stock Liquidity Retain Strong Capital Base

* Compelling Value Proposition Creates a leading New England community bank with the franchise scarcity value, profitability and growth to warrant higher valuation multiples Fortifies both companies’ position within the “Knowledge Corridor” Strong regional brand dedicated to outstanding customer service and giving back to the community Financially compelling – 35% EPS accretion in 2015 and 19% IRR with manageable TBV earnback Attractively valued with significant upside potential Robust capital base provides flexibility with respect to capital management, organic growth and acquisitions Creates a management team with notable integration experience and demonstrated ability to improve performance Tough decisions made by management, cost savings identified and integration plan agreed to

Strictly Private and Confidential Appendix

* Pro Forma Board Composition Pro Forma Board Pro Forma Board Committees Robert A. Stewart Jr. Board Chair & Member of Exec. Committee J. Jeffrey Sullivan President William H.W. Crawford IV CEO Former United Director Governance & Nominating Committee Chair Former United Director Audit Committee Chair 8 Additional Rockville Board Members 8 Additional United Board Members Former Rockville Director Risk Committee Chair Former Rockville Director Compensation Committee Chair Former United Director Executive Committee Chair United Rockville Raymond H. Lefurge Jr. Vice Chairman

* Tangible Book Value Dilution Detail (1) United’s projected TCE at closing equals 3Q 2013 tangible book value of $258mm plus $10mm (2 quarters of earnings), less $4mm (2 quarters of $0.11/share dividend). Reflective of projected marks, rate environment and pending transactions as of announcement Walk-forward to closing capital Calculation of intangibles created

* Key Management Bios Name / Position Experience William H. W. Crawford, IV President & CEO Age 47 Mr. Crawford has been the President and Chief Executive Officer since April 2011. Prior to joining Rockville, Mr. Crawford served in numerous executive roles with Wells Fargo Bank, Wachovia Bank, and SouthTrust Bank from 1997 to 2010 including: Executive Vice President, Commercial Banking, Eastern Virginia, Regional President/Executive Vice President in four different markets: Raleigh/Durham, Southeast Florida, Greensboro/ Winston Salem, and Norfolk/Virginia Beach. Mr. Crawford has 25 years of industry experience including leading regional banks exceeding $4 billion in deposits and 1,000+ employee organizations J. Jeffrey Sullivan President Age 48 Mr. Sullivan is the COO of United and also the former Head of Commercial Banking. Mr. Sullivan served as the EVP and Chief Lending Officer of the Bank until November 2012. He joined the Bank in 2003 after previously working at The Bank of Western Massachusetts and BayBank Eric R. Newell CFO Age 34 Mr. Newell was named CFO of Rockville on November 14, 2013 and previously served as Executive Vice President, Head of Treasury and Corporate Strategy. Mr. Newell joined Rockville Bank in May 2011 as Vice President, Treasury Officer and was promoted to Senior Vice President, Director of Treasury in March 2012. Mr. Newell holds a CFA designation and prior to joining the Bank he served as an analyst at AllianceBernstein, as an analyst for Fitch Ratings, and as a Bank Examiner with the Federal Deposit Insurance Corporation (“FDIC”), out of the Hartford, Connecticut office. Mr. Newell has 10 years of industry experience Dena M. Hall Marketing Age 40 Ms. Hall is the Senior Vice President of Marketing and Investor Relations at United Bank and the President of the United Bank Foundation. Prior to joining the bank in 2005; she was the Marketing Director of the former Woronoco Savings Bank in Westfield, MA and Executive Director of the Woronoco Savings Charitable Foundation. Ms. Hall has nearly 20 years of experience in bank marketing and charitable giving Marino J. Santarelli COO Age 61 Mr. Santarelli, Executive Vice President, Chief Operating Officer, joined Rockville Bank in July 2011. Prior to joining the Bank, Mr. Santarelli was with Wells Fargo and its predecessor banks for seventeen years, most recently he served as the Wells Fargo Market Executive and Business Banking Executive for Eastern Virginia. Mr. Santarelli has 40 years of industry experience Miriam J. Siegel Human Resources Age 46 Ms. Siegel is the Senior Vice President of Human Resources at United Bank. She is a Certified Compensation Professional (CCP) and Certified Benefits Professional (CBP). Ms. Siegel joined the bank in 1993 and has over 24 years of experience in the field

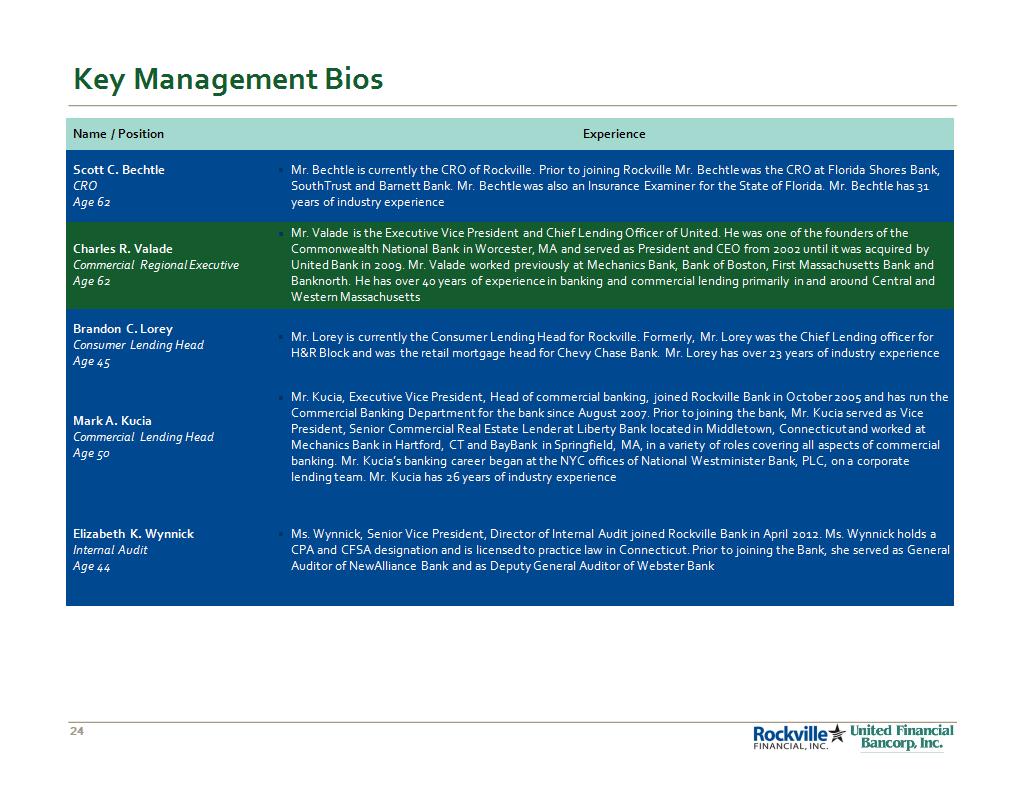

* Key Management Bios Name / Position Experience Scott C. Bechtle CRO Age 62 Mr. Bechtle is currently the CRO of Rockville. Prior to joining Rockville Mr. Bechtle was the CRO at Florida Shores Bank, SouthTrust and Barnett Bank. Mr. Bechtle was also an Insurance Examiner for the State of Florida. Mr. Bechtle has 31 years of industry experience Charles R. Valade Commercial Regional Executive Age 62 Mr. Valade is the Executive Vice President and Chief Lending Officer of United. He was one of the founders of the Commonwealth National Bank in Worcester, MA and served as President and CEO from 2002 until it was acquired by United Bank in 2009. Mr. Valade worked previously at Mechanics Bank, Bank of Boston, First Massachusetts Bank and Banknorth. He has over 40 years of experience in banking and commercial lending primarily in and around Central and Western Massachusetts Brandon C. Lorey Consumer Lending Head Age 45 Mr. Lorey is currently the Consumer Lending Head for Rockville. Formerly, Mr. Lorey was the Chief Lending officer for H&R Block and was the retail mortgage head for Chevy Chase Bank. Mr. Lorey has over 23 years of industry experience Mark A. Kucia Commercial Lending Head Age 50 Mr. Kucia, Executive Vice President, Head of commercial banking, joined Rockville Bank in October 2005 and has run the Commercial Banking Department for the bank since August 2007. Prior to joining the bank, Mr. Kucia served as Vice President, Senior Commercial Real Estate Lender at Liberty Bank located in Middletown, Connecticut and worked at Mechanics Bank in Hartford, CT and BayBank in Springfield, MA, in a variety of roles covering all aspects of commercial banking. Mr. Kucia’s banking career began at the NYC offices of National Westminister Bank, PLC, on a corporate lending team. Mr. Kucia has 26 years of industry experience Elizabeth K. Wynnick Internal Audit Age 44 Ms. Wynnick, Senior Vice President, Director of Internal Audit joined Rockville Bank in April 2012. Ms. Wynnick holds a CPA and CFSA designation and is licensed to practice law in Connecticut. Prior to joining the Bank, she served as General Auditor of NewAlliance Bank and as Deputy General Auditor of Webster Bank

* Large Affluent Markets Median Household Income (2012) Projected HH Income Growth (2012-2017) Source: SNL Financial. New England MSA - Population (2012) (thousands)