UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 OR 15(d) of

the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): November 8, 2013

ROYAL GOLD, INC.

(Exact name of registrant as specified in its charter)

|

Delaware |

|

001-13357 |

|

84-0835164 |

|

(State or other jurisdiction |

|

(Commission |

|

(IRS Employer |

|

of incorporation) |

|

File Number) |

|

Identification No.) |

|

1660 Wynkoop Street, Suite 1000, Denver, CO |

|

80202-1132 |

|

(Address of principal executive offices) |

|

(Zip Code) |

Registrant’s telephone number, including area code 303-573-1660

(Former name or former address, if changed since last report.)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

o Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

o Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

o Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

o Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Item 8.01 Other Events

ADDITIONAL INFORMATION REGARDING THE 2013 ANNUAL MEETING OF

STOCKHOLDERS

TO BE HELD ON WEDNESDAY, NOVEMBER 20, 2013

THIS INFORMATION SHOULD BE READ IN CONJUNCTION WITH THE PROXY STATEMENT.

November 8, 2013

RE: Royal Gold, Inc. Annual Meeting of Stockholders — November 20, 2013

Proposal 3, Advisory Vote on Executive Compensation (“Say on Pay”)

Dear Stockholder:

By now you should have received Royal Gold, Inc.’s Notice of the 2013 Annual Meeting and Proxy Statement. You can also view our Proxy Statement at www.royalgold.com.

We write to ask for your support at the Annual Meeting by voting in accordance with the recommendations of our Board of Directors on all proposals, including Proposal 3, Advisory Vote on Compensation of the Named Executive Officers (“Say on Pay”).

Institutional Shareholder Services (ISS) recommended a vote against this proposal. While ISS has indicated to us that it may revise its October 31, 2013 Proxy Report, we are compelled to express our strong disagreement with its recommendation. In its report, ISS based its recommendation largely on the size of our CEO’s equity awards measured against a group of comparator companies determined by ISS.

· We fundamentally disagree with the peer group selected by ISS to benchmark our CEO compensation and believe that it fails to recognize our unique royalty-based, precious metals business model. It also fails to recognize that Royal Gold is one of the 20 largest precious metals companies in the world by market capitalization. We understand that ISS internal policy requires it to take a standardized approach that identifies comparator companies based on companies in the MSCI metals and mining sector and based on magnitude of revenues, ignoring market capitalization. None of the 15 companies selected by ISS are in the precious metals royalty business, and only four of the 15 companies selected by ISS are in the precious metals mining business.

· If this was not misleading enough, ISS failed to use comparable trailing 12-month period results for its selected peer companies, which, given the decline in gold and silver prices in the first 6 months of 2013, completely distorted the comparability of results between the ISS-selected peer group and Royal Gold with its June 30 fiscal year-end.

· The ISS methodologies compare apples to oranges and in our opinion are substantially flawed and invalid.

ISS Measurement Periods are Inconsistent.

The summary financials for Royal Gold in the ISS report present results on our fiscal year basis (July 1 to June 30) while representing the financial results for the ISS peer companies for other annual periods, mostly calendar year end.

· The mismatch in measurement period results in a very misleading comparison to Royal Gold. Everyone who follows the industry knows that gold and silver prices declined significantly after December 31, 2012. The decline in gold and silver prices amounted to 29.6% and 38.9%, respectively, from January 2, 2013 to June 28, 2013 (trading days). Correspondingly, precious metal equities as measured by the Philadelphia Gold and Silver Index (XAU) declined 46.5% during the same period. This highlights the lack of precision in ISS’ analytical approach.

· We corrected this mismatch of financial reporting periods for the five companies highlighted in the ISS report. The rows in the table below show: (i) the ISS TSR calculations using different twelve month measurement periods; (ii) our calculation of TSR using consistent trailing twelve month periods ending June 30, 2013; and (iii) our calculation of TSR using consistent trailing twelve month periods ending December 31, 2012. Clearly, Royal Gold performed much better than suggested in the ISS report on a relative basis.

|

Royal Gold Historical Performance TSR (%) |

|

Compared to Peers TSR (%) |

| ||||||||||||||||||

|

Company |

|

2009 |

|

2010 |

|

2011 |

|

2012 |

|

2013 |

|

ANV |

|

HL |

|

GORO |

|

GSS |

|

HAYN |

|

|

ISS Report |

|

34.29 |

|

16.0 |

|

23.02 |

|

34.68 |

|

-45.79 |

|

-0.50 |

|

12.85 |

|

-25.05 |

|

11.52 |

|

21.95 |

|

|

Fiscal Year |

|

34.29 |

|

16.0 |

|

23.02 |

|

34.68 |

|

-45.79 |

|

-77.17 |

|

-37.26 |

|

-66.49 |

|

-63.79 |

|

-6.03 |

|

|

Calendar Year |

|

-4.31 |

|

16.01 |

|

23.43 |

|

20.66 |

|

N/A |

|

-0.50 |

|

12.85 |

|

-25.05 |

|

11.52 |

|

-5.00 |

|

ISS Excludes Relevant Companies from ISS Peer Group.

There are only about ten publicly traded companies worldwide that are involved in the precious metal royalty business. All of them maintain primary listings outside the United States except for Royal Gold. This means that all of the companies most directly comparable to Royal Gold are excluded from the United States industry classification used by ISS. ISS selected numerous broader “materials” industry companies for its peer group, in addition to four United States precious metals mining companies with far smaller market values than Royal Gold.

· Gold is often negatively correlated to the broader economy, so benchmarking Royal Gold’s total shareholder return against chemical, construction materials, base metals and forest products companies is simply not relevant in determining relative performance.

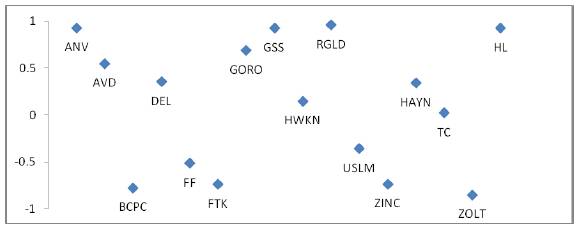

· To demonstrate the importance of this point, Royal Gold’s share price has a 95.8% correlation to the price of gold. The chart below illustrates that the bulk of the ISS peer group has no or significantly negative correlation to the price of gold.

Correlation of ISS Peer Companies to

LME Gold Price

July 1, 2012-June 30, 2013

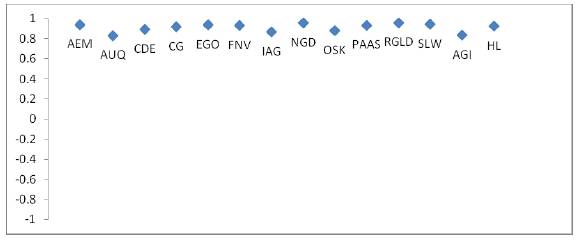

· Royal Gold thoughtfully constructed and disclosed its peer group on page 28 of the Proxy Statement. The group we selected includes our direct royalty competitors and precious metal mining companies of similar relative size as measured by market capitalization. This group consists of 13 publicly traded companies including IAMGOLD, Silver Wheaton, Franco-Nevada, Pan American Silver, Coeur Mining, Hecla Mining, Osisko Mining, Centerra Gold, New Gold, Alamos Gold, AuRico Gold, Eldorado Gold and Agnico Eagle.

· We note that ISS does not display a complete listing of our benchmark companies in its report. Many of these companies are not listed in the United States. However, gold mining is an international business, and the United States does not domicile a sufficient number of precious metals companies to make peer group selection statistically valid. Furthermore, this is the international peer group with whom we compete for executive talent and is therefore the relevant comparator group.

· The average correlation to gold for Royal Gold’s selected peer group companies is 90.1% as displayed on the following chart.

Correlation of Royal Gold Peer Companies to

LME Gold Price

July 1, 2012-June 30, 2013

· If ISS had used Royal Gold’s compensation peer group, rather than its internal policy-generated comparators, we believe we would have passed ISS’s CEO compensation tests.

ISS’ Peer Group Ignores Market Capitalization.

Our Board believes that market capitalization, rather than revenue, is the appropriate primary criterion for selecting companies for executive compensation decision-making for the following reasons (which are supported by the tables included in this letter):

· Market capitalization is directly correlated to stockholder benefit.

· Market capitalization, a key component of which is stock price, is the key driver of the value of equity awards, which comprise the single largest component of compensation for Royal Gold executives, including our CEO.

· Market capitalization as the primary selection criterion is more appropriate than revenues. For example, assume companies A and B have identical revenues of $300 million and both have 100 million shares outstanding, but company A’s market capitalization is $500 million as compared to company B’s $3 billion market capitalization. It is logical that company B would provide more compensation to its CEO. However, the ISS analysis suggests that they should be the same because both companies have the same revenues.

Royal Gold is Significantly Larger than the Companies in the ISS Comparator Group.

· As we pointed out on page 26 of our Proxy Statement, revenues are a poor indicator of Royal Gold’s value. Revenues of a typical business are significantly offset by the operating costs of that business. Royal Gold’s investors understand our business model, which provides very low operating costs and superior operating margins compared to both mining and industrial companies. Royal Gold believes market capitalization is a much better indication of relative size for purposes of external benchmarking. Based on market size, Royal Gold is significantly larger than any of the ISS-identified peers:

Comparison of Royal Gold’s Market Capitalization to the Market Capitalization of

ISS-Identified Peer Group Companies

· Because ISS uses mostly much smaller companies in its analysis, it is no surprise that our CEO’s compensation was viewed as being relatively higher.

ISS Disregards Our Performance Criteria and GAAP Accounting.

ISS’ analysis of our executive compensation ignores that our CEO’s compensation declined 14% in fiscal 2013 compared to fiscal 2012. Moreover, ISS assumed all performance-based awards will fully vest, despite challenging vesting criteria, and has modified the GAAP-based disclosure in Royal Gold’s Proxy Statement to disregard performance criteria.

· The August 2012 performance share grants to the Company’s CEO had a GAAP value of $828,520, a decline of over 40% from the value of the August 2011 grants, because of significant performance-based vesting criteria. From ISS’s perspective, the value of the August 2012 grants increased 12.5% from August 2011 to $1.7 million. This conclusion can only be achieved by ignoring performance criteria and GAAP accounting.

· In addition, ISS option vesting calculations are not consistent with GAAP accounting and those modifications further amplify the suggested value in the ISS report. GAAP accounting exists to provide a consistent approach to accounting, and we do not believe it is prudent to use a combination of accounting practices.

ISS Mischaracterized Our Performance Share Vesting Criteria.

ISS cited our failure to identify performance share vesting criteria as a concern. Our vesting criteria is a 10% compounded annual growth rate in adjusted free cash flow per share, as disclosed in our September 3, 2013, Form 8-K Report. We note that ISS incorrectly identifies the metric as growth in free cash flow overall, which would encourage dilutive growth and would be a much easier measure to achieve than our per share annual growth performance metric.

ISS also cited our failure to identify the specific Adjusted EBITDA threshold which must be achieved before restricted stock awards to our named executive officers, including our CEO, may vest. Beginning in August 2012, if the Company does not meet a minimum Adjusted EBITDA (earnings before interest, taxes, depreciation and amortization, and other non-cash charges) threshold for a fiscal year, then all of

the shares of stock underlying the restricted stock grant awarded for that fiscal year will be forfeited. For restricted stock awards made in August 2012 and 2013, the Adjusted EBITDA threshold was $175 million. Actual Adjusted EBITDA was $260.8 million for fiscal 2013, surpassing the threshold. We note that the same Adjusted EBITDA threshold must be met in order for the named executive officers, including our CEO, to receive a cash bonus for the relevant fiscal year.

Looking through all the ISS noise on misleading comparisons and marginal disclosure, Royal Gold delivered record results in fiscal 2013.

· Our fiscal 2013 results included year-over-year increases in revenues (10%) and operating cash flow (6%) despite significant headwinds in the precious metals industry in the second half of fiscal 2013.

· In fiscal 2013, we returned $43.9 million of capital to stockholders, representing a payout ratio of 25% of operating cash flow.

We have implemented a comprehensive program of compensation best practices.

· Seventy-five percent of our executive officers’ total direct compensation for fiscal 2013 was performance based. Cash bonuses, performance-based restricted stock and performance stock awards vest, for our named executive officers, only if specific financial performance measures are achieved.

· The Company applies a “double trigger” approach to vesting awards made under the Company’s 2004 Omnibus Long-Term Incentive Plan (“LTIP”) in the event of a change-in-control. This means that vesting of these awards is accelerated upon a change-in-control only if the executive is also terminated under certain circumstances.

· The Company believes perquisites for executives should be extremely limited in scope and value and, therefore, generally does not provide perquisites or other special benefits to the executive officers.

· The Company’s LTIP expressly prohibits the re-pricing of stock options.

· The Company’s executives may participate in a Salary Reduction/Simplified Employee Pension Plan on the same terms as other eligible employees. The Company does not maintain a defined pension benefit plan.

· The employment agreements between the Company and the named executive officers do not provide for excise tax gross-ups for change-in-control provisions.

· The Company’s executive stock ownership program requires the Company’s named executive officers to own a number of shares valued at a multiple of their salary to assure that their interests are aligned with those of our stockholders.

We invite you to read the Proxy Statement for more information regarding the reasons the Board is recommending a vote “FOR” Proposal 3, Advisory Vote on Executive Compensation.

We appreciate your time and consideration on these matters and ask for your support of the Board’s recommendation.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

|

|

Royal Gold, Inc. | |

|

|

(Registrant) | |

|

|

| |

|

|

| |

|

Dated: November 8, 2013 |

By: |

/s/ Bruce C. Kirchhoff |

|

|

Name: |

Bruce C. Kirchhoff |

|

|

Title: |

Vice President, General Counsel and |

|

|

|

Secretary |