Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - FIRST BUSINESS FINANCIAL SERVICES, INC. | ceoletter930138-k.htm |

Exhibit 99.1

First Business CEO Report Third Quarter 2013

Dear Shareholders and Friends of First Business:

I am pleased to share that by continuing to originate high quality loans, steadily improve asset quality and efficiently execute on the Company's initiative to increase full banking relationships with businesses, executives and high net worth individuals, First Business earned record profits again in the third quarter of 2013.

These strong third quarter 2013 results and positive year-to-date momentum include a jump in third quarter net income of 38% compared to the third quarter of 2012 and record nine-month net income of $10 million, up 56% compared to the prior-year period. We look to continue to build on this momentum and finish the year strong as we remain focused on exceeding client expectations, delivering strong financial performance and consistently creating value for our shareholders.

BUSINESS MODEL PROVIDES COMPETITIVE EDGE

Our unique business model continues to provide a competitive edge by allowing us to operate more efficiently than our peers. Not operating retail branches allows us to run our business with fewer employees and significantly lower overhead costs. Thus, we have avoided the challenges faced by many institutions that are now focused on scaling back branch networks to cut costs. A recent Financial Times article explored the trend, quoting Wayne Busch, managing director of Accenture’s North America banking practice, stating that, “branches are hugely expensive for banks to build and maintain.” In addition, as a business bank we have not relied on revenues from the residential mortgage business. Those organizations that have are now dealing with reduced revenue and, in many cases, the unenviable need to make staff reductions.

At First Business, we prefer to invest in key talent who can fully leverage our strategic initiatives, allowing us to generate more revenue per employee than peer banks who are operating branch networks. A clear indicator of that enhanced productivity is demonstrated through our consistently strong efficiency ratio, a measure of the cost to generate one dollar of revenue. Our efficiency ratio for the third quarter of 2013 was 56.1%, marking the fifth consecutive quarter below 60%. To put the value of that metric in context, consider that for the second quarter of 2013 the average efficiency ratio for banks with between $1 billion and $3 billion in assets was 67.1%, and for our peer group it was 65.2%. Bottom line: First Business consistently spends less to generate one dollar of revenue than the majority of our peers and the industry as a whole.

THRIVING IN A CHALLENGING ENVIRONMENT

Although we are certainly pleased with our trend line of positive results, we are not complacent. The banking industry continues to be challenged by a range of factors including continued low rates and competitive pricing pressures. While we are not immune to these factors, we believe our company remains well positioned as we continue to leverage the strengths of our efficient and focused business model. For example:

• | Decreased funding costs. We have benefited from lower funding costs, primarily due to increased in-market transaction accounts, lower rates paid on brokered certificates of deposit and the paydown of our subordinated debt, creating margin stability even as the industry trends down. |

Steadily improving asset quality metrics. The ratio of non-performing assets to total assets improved to 0.82% at September 30, 2013, representing

• | our company’s lowest level since prior to the financial crisis in March 2008. |

• | Improving deposit mix. In-market deposits grew $43.5 million, or 6.5%, to $714 million at quarter’s end, up from $670.5 million at the prior year quarter end. We believe that this growth can be attributed largely to existing and new clients responding positively to our high-touch, individualized service model. These in-market deposits include all transaction accounts, money-market accounts, and non-brokered certificates of deposit. In-market deposits, which now make up 63.3% of our total deposits, continue to be a desirable resource that strengthens our mix of core funding. While we are pleased with this ratio, we remain focused on maintaining and increasing the use of in-market deposits to fund loan growth. In fact, early in the fourth quarter of 2013 we invested in an additional treasury management officer in the Milwaukee market, as well as a private wealth management officer in the Madison market. |

SUPERIOR EXECUTION PROVIDES RECORD RESULTS

Due to consistent improvement realized throughout 2013, our team has pushed the Company’s third quarter performance to new heights with record results from top line revenue down through net income.

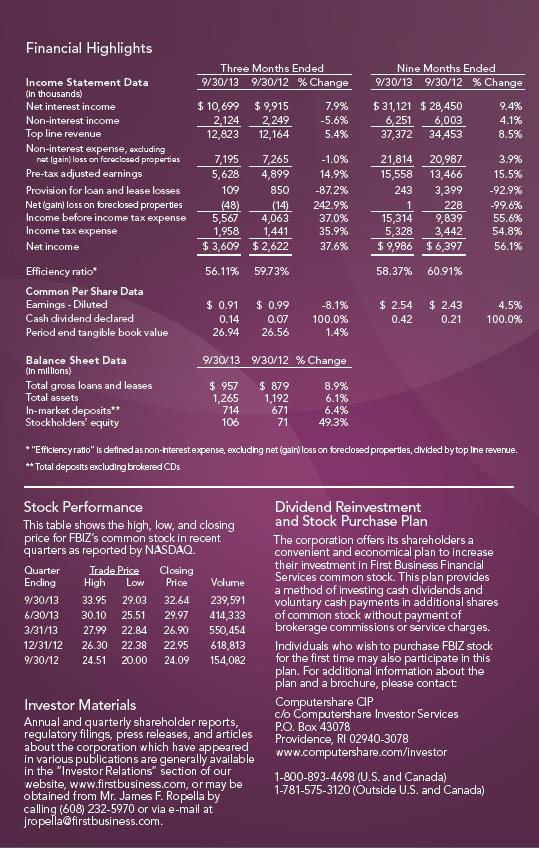

Top line revenue, consisting of net interest income and non-interest income, grew $659,000, or 5%, compared to the third quarter of 2012, to a record $12.8 million. Pre-tax adjusted earnings, defined as pre-tax income excluding the provision for loan and lease losses, other identifiable costs of credit and other discrete items unrelated to the Company’s primary business activities, grew 15% from the prior year quarter to a record $5.6 million. Third quarter net income grew by nearly $1 million compared to the third quarter of 2012, reaching a record level of $3.6 million.

These record operating results were a reflection of balance sheet growth, which continued in the third quarter of 2013. For the sixth consecutive quarter, average loans and leases increased to a record $939.1 million, growth of $53.2 million or an annualized 8% from the fourth quarter of 2012; and an increase of $60 million, or 7%, from the third quarter of 2012. In addition, for the third consecutive quarter our annualized return on average assets (ROAA) exceeded 1.0%, increasing by 26 basis points to a record 1.14%, compared to the third quarter of 2012.

WELL POSITIONED TO GROW

We have developed and honed a very attractive alternative to the traditional banking model that allows us to be lean, efficient and strategically positioned to continue on a course of measured growth in the current operating environment. Further, we are poised to accelerate that growth as the banking environment, and broader economy improves.

Our model allows us to be nimble and responsive as we deal with emerging trends and fast-changing client expectations. Yet the model also provides considerable stability in the face of challenging economic times and constantly changing industry trends. I believe our clients are benefiting from a relationship with our institution which is financially strong and highly invested in the markets we serve.

Moving forward, we continue to see real synergy in the strategic approach with which we serve our clients. The efficiency built into this approach directly impacts

the bottom-line, enabling our investors to more fully realize the benefits of our growth trends. This alignment has emerged as a key strength of our unique model, assuring that our daily focus on providing exceptional personalized service to clients will, in turn, fuel the creation of long-term shareholder value.

COMMITTED TO SHAREHOLDER VALUE

We are committed to continue earning our shareholders’ support through steadily improving performance and a disciplined approach to executing successfully on our strategy. As we continue to deliver profitable results, it is encouraging to see that strength translate to our stock’s increasing market valuation.

We are confident our strategy offers a path to building long-term shareholder value. And don’t just take my word for it. Third-party validation of that strategy came during the third quarter as First Business was selected to the prestigious Sandler O’Neill + Partners Sm-All Star List for 2013.

First Business is one of only 31 institutions, out of the initial 450 evaluated, to be recognized for “delivering bottom line results that are markedly better than the industry as a whole.” This recognition is based on analysis of growth, profitability, credit quality and capital strength - all areas in which we have placed considerable focus in our effort to consistently deliver strong results that benefit shareholders over the long haul.

It’s certainly rewarding to be considered an all-star institution and it provides well-deserved recognition for our talented team. A team whose commitment to providing superior service, in the most efficient way possible, is core to our strong performance. Yet, just like a high-performing all-star athlete needs to stay focused on continually upping his or her game, we see such recognition as a motivator and catalyst to continue to strengthen our capabilities, deepen our talent pool and execute with increasing efficiency and discipline.

We strive to increase shareholder value every day, and I am confident we have the right talent, strategy and business model in place to achieve that goal. As always, we thank you for your support of First Business. We believe we have a good story to tell and we appreciate your continued efforts to share it with potential investors.

Sincerely,

Corey Chambas, President and CEO

Note: First Business’ peer group, as defined by management, includes: Bank of Kentucky Financial Corporation (BKYF), Guaranty Bancorp (GBNK), Heritage Financial Corporation (HFWA), Mackinac Financial Corporation (MFNC), Mercantile Bank Corporation (MBWM), MetroCorp Bancshares, Inc. (MCBI), Mid Penn Bancorp, Inc. (MPB), MidSouth Bancorp, Inc. (MSL), Old Line Bancshares, Inc. (OLBK), Pacific Continental Corporation (PCBK), Peoples Financial Corporation (PFBX), QCR Holdings, Inc. (QCRH), Republic First Bancorp, Inc. (FRBK), S.Y. Bancorp, Inc. (SYBT), Southern National Bancorp of Virginia, Inc. (SONA), Southwest Bancorp, Inc. (OKSB), Univest Corporation of Pennsylvania (UVSP), Washington Banking Company (WBCO), WashingtonFirst Bankshares, Inc. (WFBI), West Bancorporation, Inc. (WTBA). All peer data sourced from SNL Financial.

This letter includes "forward-looking" statements related to First Business Financial Services, Inc. (the "Company") that can generally be identified as describing the Company's future plans, objectives or goals. Such forward-looking statements are subject to risks and uncertainties that could cause actual results or outcomes to differ materially from those currently anticipated. These forward-looking statements are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. For further information about the factors that could affect the Company's future results, please see the Company's annual report on Form 10-K, quarterly reports on Form 10-Q and other filings with the Securities and Exchange Commission.

Footprint