Attached files

| file | filename |

|---|---|

| 8-K - 8-K - AgEagle Aerial Systems Inc. | v356439_8k.htm |

| EX-99.2 - EXHIBIT 99.2 - AgEagle Aerial Systems Inc. | v356439_ex99-2.htm |

A Domestic Onshore Oil Company EnerJex Resources, Inc. (Stock Symbol: ENRJ) IPAA OGIS San Francisco – October 1, 2013

SUMMARY : The material presented is a presentation of general background information about EnerJex Resources, Inc . (“ENRJ”) as of the date of this document . This information is in summary form and does not purport to be complete . This document (and/or attachments to this document) is not intended to be relied upon as advice to existing or potential investors . FORWARD - LOOKING STATEMENTS : This document (including the financial projections and any subsequent questions and answers) contains statements that are forward - looking within the meaning of Section 27 A of the Securities Act of 1933 and Section 21 E of the Securities Exchange Act of 1934 . Such forward - looking statements are only predictions and are not guarantees of future performance . Investors are cautioned that any such forward - looking statements are and will be, as the case may be, subject to many risks, uncertainties, certain assumptions and factors relating to the operations and business environment of ENRJ that may cause the actual results of the companies to be materially different from any future results expressed or implied in such forward-looking statements . RESERVE AND RESOURCE DISCLOSURE : Securities and Exchange Commission (“SEC”) rules prohibit a publicly - reporting oil and gas company from including oil and gas resource estimates in its filings with the SEC, except proved, probable and possible reserves that meet the SEC’s definition of such terms . Estimates of non - proved and non - probable reserves included herein are not based on SEC definitions and guidelines and may not meet specific definitions of reserves or resource categories within the meaning of the SPE/SPEE/WPC Petroleum Resource Management System . NO REPRESENTATIONS : The information in this document (and/or attachments to this document) is current as of the date indicated . That information is not complete, and the performance projections included herein have not been audited . These presentation materials do not contain certain material information concerning ENRJ, including important disclosures and risk factors associated with making an investment in ENRJ, and are subject to revision at any time . ENRJ does not undertake any obligated to inform you of any changes in circumstances that may affect, in the future, the accuracy of the information set forth herein . Although ENRJ believes that the expectations and assumptions reflected in this document and the forward - looking statements are reasonable based upon information currently available to ENRJ, and their respective principals, employees, agents and authorized representatives, none of ENRJ, or their respective principals, employees, agents or authorized representatives makes any warranty or representation, whether express or implied, or assumes any legal liability for the accuracy, completeness or usefulness of any information disclosed . ENRJ nor any of its respective principals, employees, agents or authorized representatives accepts any responsibility or liability whatsoever caused by any action taken in reliance upon this document and/or its attachments . Disclaimer / Forward Looking Statements 2

▪ Merger Update ▪ Company Overview ▪ Summary of Oil Reserves COMPANY OVERVIEW

EnerJex Resources (“ENRJ”) merged with Black Raven Energy (“BRE”) on September 27, 2013. ▪ Transaction based on a negotiated value of $0.70 per share of ENRJ common stock. ▪ 73% of ENRJ shares outstanding voted of which 99.99% were in favor of the merger. ▪ BRE provides attractive entrance into the prolific Denver - Julesburg Basin. ▪ Sizeable acreage footprint approaching 100,000 net acres with large seismic database. ▪ Two scalable projects immediately increase ENRJ’s production and accelerate growth. ▪ Significant exposure to emerging oil resource plays being pursued by numerous competitors. ▪ ENRJ revenue increased to current annual run - rate of approximately $15 million. ▪ ENRJ 3P reserve exposure increased 5x to 16.7 million barrels of oil equivalent. ENRJ senior revolving credit facility expanded on September 30, 2013. ▪ Principal commitment increased from $50 million to $100 million. ▪ Borrowing base increased from $19.5 million to $38 million. ▪ Current interest rate decreased from 3.75% to 3.30%. ▪ Availability increased to $8 million and borrowing base is expected to continue growing. Merger Update 4 EnerJex is poised to significantly accelerate growth beginning immediately.

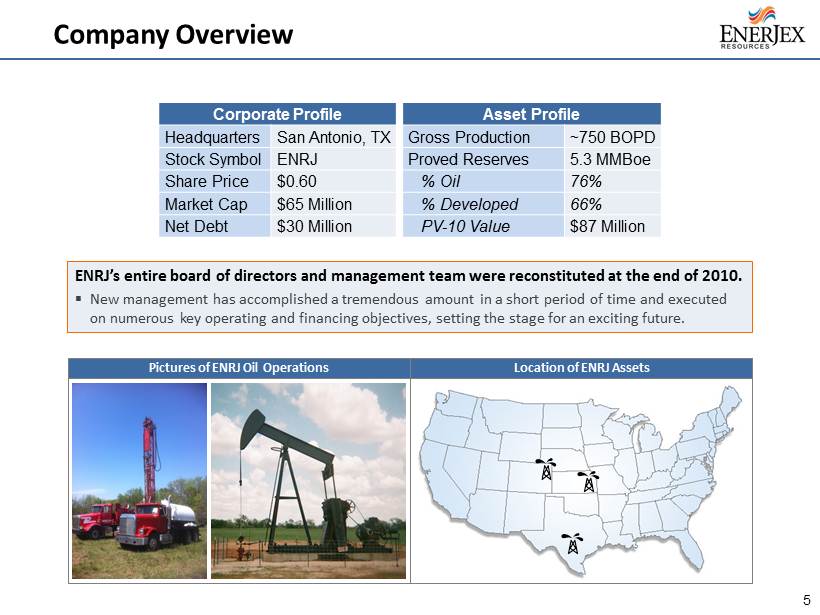

Company Overview Location of ENRJ Assets Pictures of ENRJ Oil Operations Corporate Profile Asset Profile Headquarters San Antonio, TX Gross Production ~750 BOPD Stock Symbol ENRJ Proved Reserves 5.3 MMBoe Share Price $0.60 % Oil 76% Market Cap $65 Million % Developed 66% Net Debt $30 Million PV - 10 Value $87 Million 5 ENRJ’s entire board of directors and management team were reconstituted at the end of 2010. ▪ New management has accomplished a tremendous amount in a short period of time and executed on numerous key operating and financing objectives, setting the stage for an exciting future.

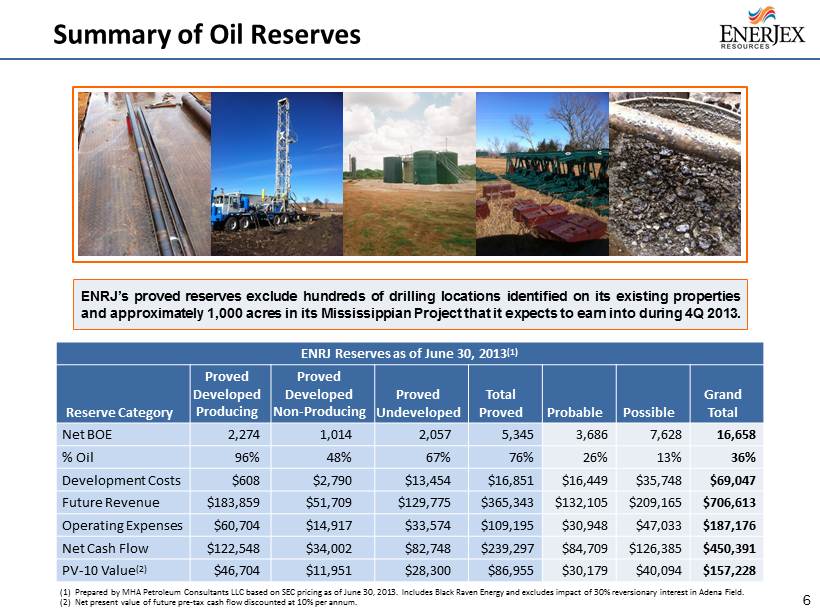

Summary of Oil Reserves ENRJ Reserves as of June 30, 2013 (1) Reserve Category Proved Developed Producing Proved Developed Non - Producing Proved Undeveloped Total Proved Probable Possible Grand Total Net BOE 2,274 1,014 2,057 5,345 3,686 7,628 16,658 % Oil 96% 48% 67% 76% 26% 13% 36% Development Costs $608 $2,790 $13,454 $16,851 $16,449 $35,748 $69,047 Future Revenue $183,859 $51,709 $129,775 $365,343 $132,105 $209,165 $706,613 Operating Expenses $60,704 $14,917 $33,574 $109,195 $30,948 $47,033 $187,176 Net Cash Flow $122,548 $34,002 $82,748 $239,297 $84,709 $126,385 $450,391 PV - 10 Value (2) $46,704 $11,951 $28,300 $86,955 $30,179 $40,094 $157,228 (1) Prepared by MHA Petroleum Consultants LLC based on SEC pricing as of June 30 , 2013 . Includes Black Raven Energy and excludes impact of 30 % reversionary interest in Adena Field . (2) Net present value of future pre - tax cash flow discounted at 10 % per annum . ENRJ’s proved reserves exclude hundreds of drilling locations identified on its existing properties and approximately 1 , 000 acres in its Mississippian Project that it expects to earn into during 4 Q 2013 . 6

▪ Project Locations ▪ Adena Field ▪ Niobrara Play ▪ Emerging Oil Resource Plays OVERVIEW OF ASSETS ACQUIRED IN MERGER

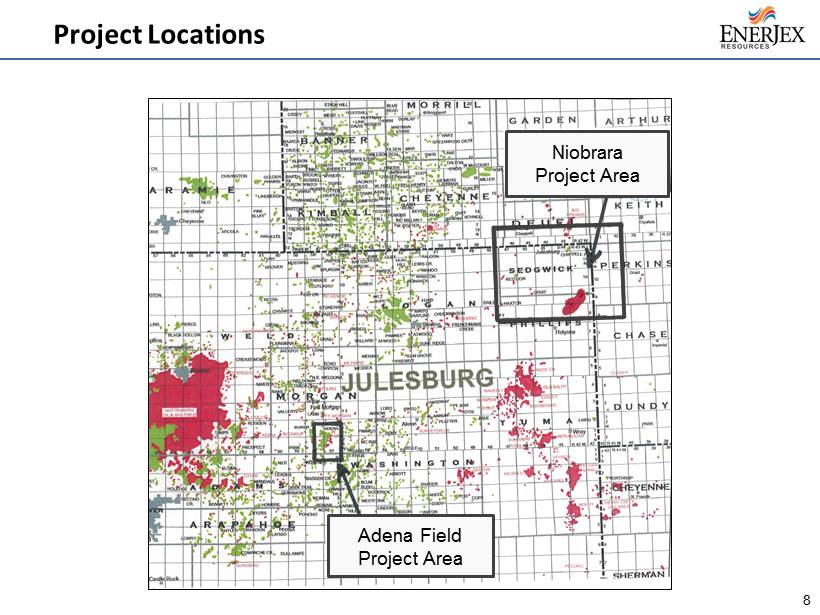

Project Locations 8 Niobrara Project Area Adena Field Project Area

▪ Adena is the third largest oil field in the history of Colorado based on cumulative production, behind Rangely and Wattenberg, having produced 75 million barrels of oil and 125 billion cubic feet of gas. ▪ Vast majority of the productive acreage (18,760 acres) was unitized in 1956 and developed by Union Oil Company of California (Unocal). ▪ Peak production reached 25,000 barrels of oil per day. ▪ Nearly all of the producing oil wells were temporarily abandoned during the secondary recovery phase in the mid 1980’s when oil prices collapsed. ▪ A small operator purchased the unit from Unocal in 1987 and produced a minimal number of wells during the subsequent 25 year period (enough to maintain the leasehold position). ▪ BRE acquired a 100% working interest in the unit through non - competitive transactions during 2011 . ▪ Subject to a 30% reversionary working interest after payout of all costs plus interest. ▪ BRE increased production from 100 barrels of oil equivalent per day ( Boe /d) to 250 Boe /d (75% oil) by reactivating 3 J - Sand wells and re - completing 4 wells in the D - Sand. ▪ Attractive opportunity to reactivate the J - Sand waterflood, exploit bypassed oil pay in the D - Sand, and implement secondary recovery in depleted D - Sand oil pools. Adena Field Background 9

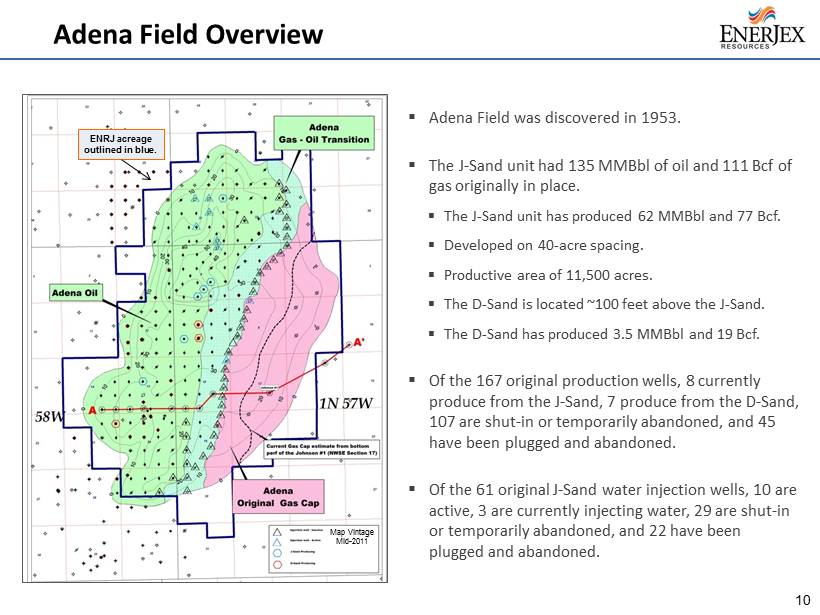

Adena Field Overview ▪ Adena Field was discovered in 1953. ▪ The J - Sand unit had 135 MMBbl of oil and 111 Bcf of gas originally in place. ▪ The J - Sand unit has produced 62 MMBbl and 77 Bcf . ▪ Developed on 40 - acre spacing. ▪ Productive area of 11,500 acres. ▪ The D - Sand is located ~100 feet above the J - Sand. ▪ The D - Sand has produced 3.5 MMBbl and 19 Bcf . ▪ Of the 167 original production wells, 8 currently produce from the J - Sand, 7 produce from the D - Sand, 107 are shut - in or temporarily abandoned, and 45 have been plugged and abandoned. ▪ Of the 61 original J - Sand water injection wells, 10 are active, 3 are currently injecting water, 29 are shut - in or temporarily abandoned, and 22 have been plugged and abandoned. 10 ENRJ acreage outlined in blue. Map Vintage Mid - 2011

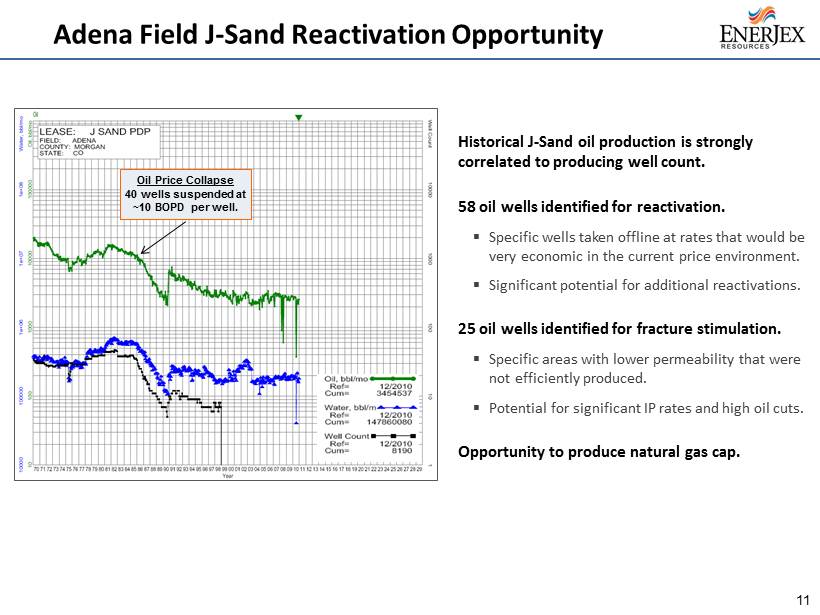

Adena Field J - Sand Reactivation Opportunity 11 Historical J - Sand oil production is strongly correlated to producing well count. 58 oil wells identified for reactivation. ▪ Specific wells taken offline at rates that would be very economic in the current price environment. ▪ Significant potential for additional reactivations. 25 oil wells identified for fracture stimulation. ▪ Specific areas with lower permeability that were not efficiently produced. ▪ Potential for significant IP rates and high oil cuts. Opportunity to produce natural gas cap. Oil Price Collapse 40 wells suspended at ~10 BOPD per well.

Adena Field D - Sand Opportunity 12 19 wells identified for re - completion in D - Sand. ▪ Bypassed oil pay up - hole in specific J - Sand wells. ▪ IP of 100 BOPD from most recent well which stabilized at approximately 30 BOPD. 3 New drilling locations identified in productive D - Sand oil pool. Multiple secondary recovery opportunities identified in depleted D - Sand oil pools. ▪ Utilize existing wellbores to implement water injection pattern at minimal cost. Southern Area Waterflood ▪ Phase I water injection initiated in March 2013. ▪ Currently injecting ~2,000 barrels of water per day from 5 wells. ▪ Production response of ~100 BOPD expected within approximately 6 months. ▪ ~500,000 barrels of recoverable oil expected. Opportunity to produce liquids - rich natural gas cap.

>55,000 net acres leased primarily in Phillips and Sedgwick Counties, Colorado and Perkins County, Nebraska. ▪ Acreage has been high - graded from original position of more than 330,000 net acres based on structural features. ▪ ~25,000 acres HBP and 15,000 acres expire after 2015. >150 high - ranked drilling locations identified on ENRJ acreage. ENRJ owns a 6% overriding royalty interest in ~200 wells. 114 miles of 2D and 165 square miles (105,000 acres) of 3D seismic data. Substantial infrastructure assets including a high pressure pipeline capable of transporting 10 MMcf /d. Immediate proximity to 1,679 - mile Rocky Mountain Express and 436 - mile Trailblazer natural gas pipelines. Niobrara Project Overview 13 - 3D Seismic Example -

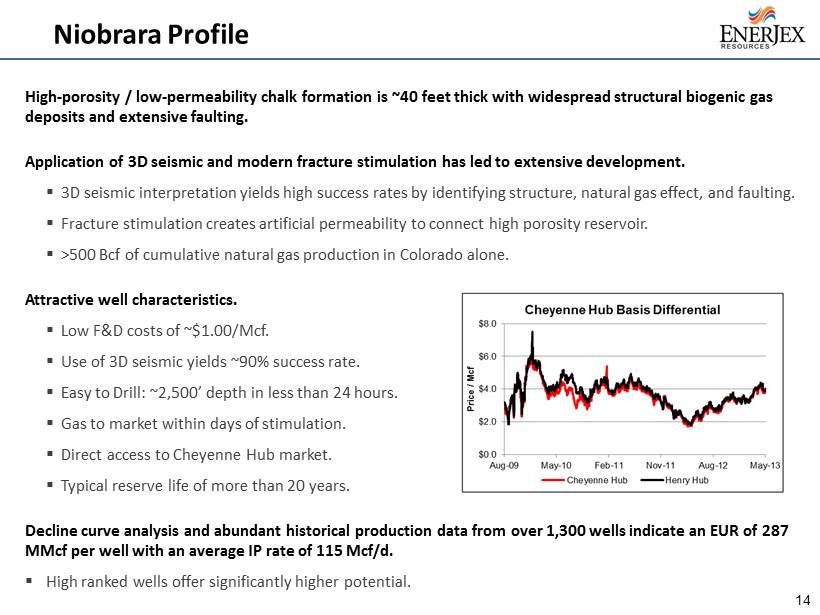

High - porosity / low - permeability chalk formation is ~40 feet thick with widespread structural biogenic gas deposits and extensive faulting. Application of 3D seismic and modern fracture stimulation has led to extensive development. ▪ 3D seismic interpretation yields high success rates by identifying structure, natural gas effect, and faulting. ▪ Fracture stimulation creates artificial permeability to connect high porosity reservoir. ▪ >500 Bcf of cumulative natural gas production in Colorado alone. Attractive well characteristics. ▪ Low F&D costs of ~$1.00/Mcf. ▪ Use of 3D seismic yields ~90% success rate. ▪ Easy to Drill: ~2,500’ depth in less than 24 hours. ▪ Gas to market within days of stimulation. ▪ Direct access to Cheyenne Hub market. ▪ Typical reserve life of more than 20 years. Decline curve analysis and abundant historical production data from over 1,300 wells indicate an EUR of 287 MMcf per well with an average IP rate of 115 Mcf/d. ▪ High ranked wells offer significantly higher potential. Niobrara Profile 14

Multiple unconventional oil resource plays are emerging on trend with ENRJ’s Niobrara and Adena projects. ▪ Numerous wells have recently been permitted, drilled, and tested on trend with ENRJ’s acreage targeting unconventional oil production from Paleozoic (Permian and Pennsylvanian) carbonates and shales . ▪ 1,500 foot gross interval with objective section ranging from 300 to 750 feet thick. ▪ Primary oil targets being pursued include the Marmaton, Cherokee, Atoka, Morrow, Virgil, and Admire formations. ▪ Key well discovered in 2009 achieved an IP rate of 1,500 BOPD and averaged 400 BOPD over the first 20 months . ▪ Unconventional oil production is also being targeted in the Cretaceous Greenhorn formation. ▪ Competitors reportedly include Southwestern Energy, Devon Energy, Apache Corp, Wiepking - Fullerton Energy, Cascade Petroleum, Nighthawk Energy, Synergy Resources, Vecta Oil & Gas, Omimex Petroleum, and Recovery Energy. ▪ These plays are in the early stages of exploration and widespread economic success has not yet been established. Emerging Oil Resource Plays 15

▪ Kansas – Mississippian ▪ Kansas – Cherokee ▪ Texas – El Toro ▪ Key Metrics OVERVIEW OF VINTAGE ASSETS

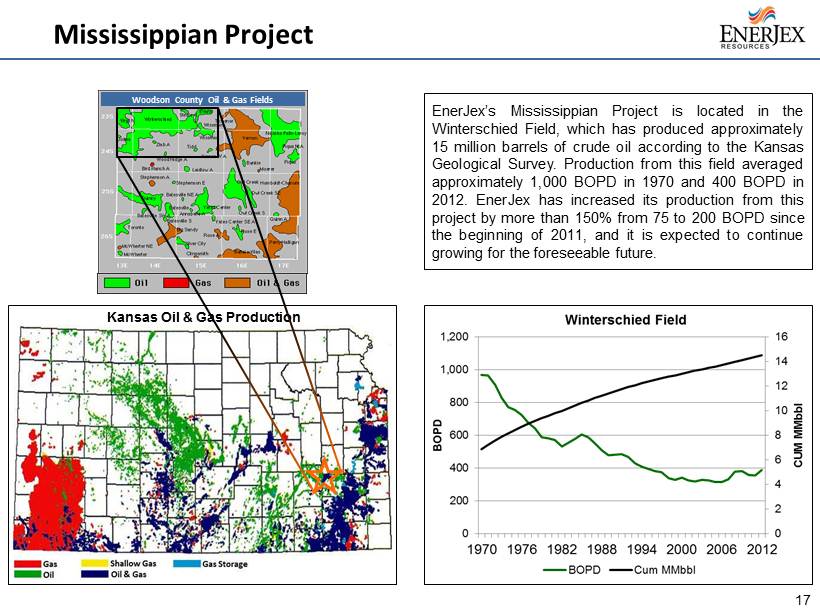

Kansas Oil & Gas Production EnerJex’s Mississippian Project is located in the Winterschied Field, which has produced approximately 15 million barrels of crude oil according to the Kansas Geological Survey . Production from this field averaged approximately 1 , 000 BOPD in 1970 and 400 BOPD in 2012 . EnerJex has increased its production from this project by more than 150 % from 75 to 200 BOPD since the beginning of 2011 , and it is expected to continue growing for the foreseeable future . Mississippian Project 17 Woodson County Oil & Gas Fields

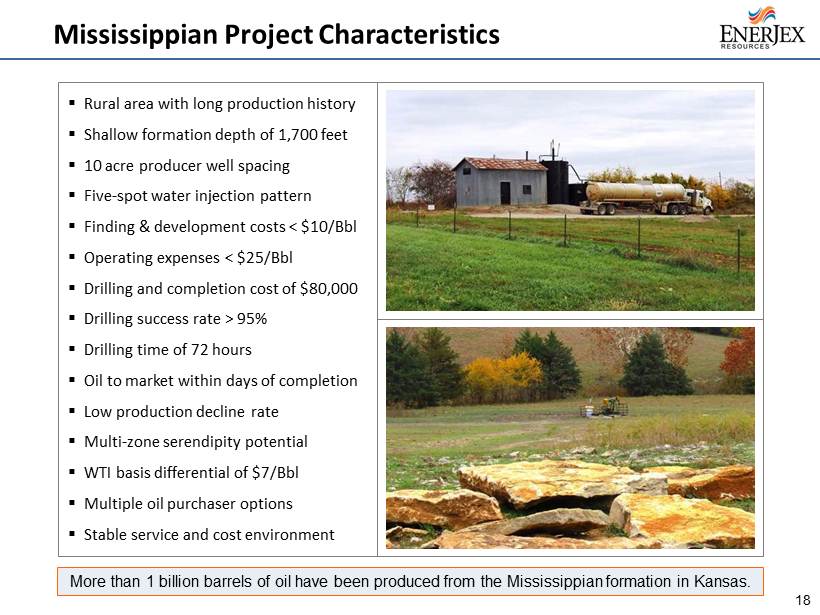

Mississippian Project Characteristics ▪ Rural area with long production history ▪ Shallow formation depth of 1,700 feet ▪ 10 acre producer well spacing ▪ Five - spot water injection pattern ▪ Finding & development costs < $10/Bbl ▪ Operating expenses < $25/Bbl ▪ Drilling and completion cost of $80,000 ▪ Drilling success rate > 95% ▪ Drilling time of 72 hours ▪ Oil to market within days of completion ▪ Low production decline rate ▪ Multi - zone serendipity potential ▪ WTI basis differential of $7/Bbl ▪ Multiple oil purchaser options ▪ Stable service and cost environment 18 More than 1 billion barrels of oil have been produced from the Mississippian formation in Kansas.

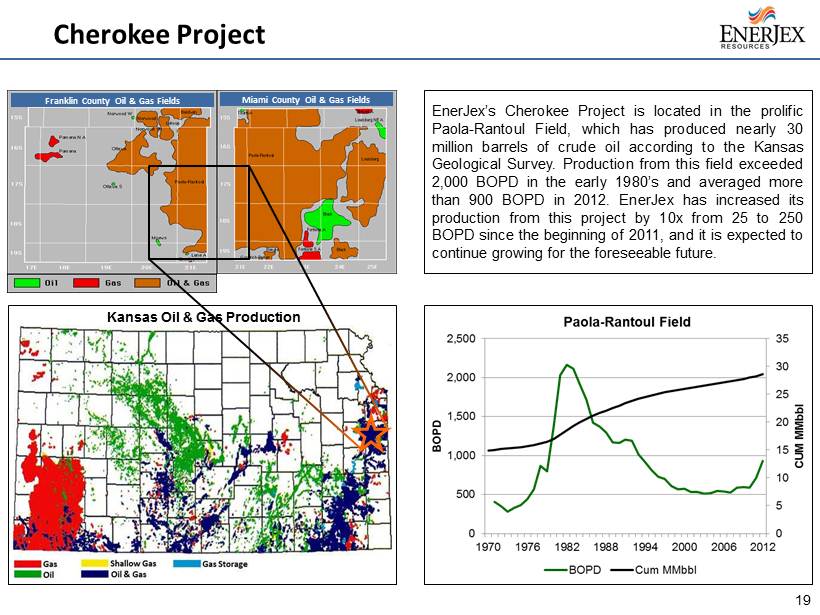

Franklin County Oil & Gas Fields Miami County Oil & Gas Fields Kansas Oil & Gas Production EnerJex’s Cherokee Project is located in the prolific Paola - Rantoul Field, which has produced nearly 30 million barrels of crude oil according to the Kansas Geological Survey . Production from this field exceeded 2 , 000 BOPD in the early 1980 ’s and averaged more than 900 BOPD in 2012 . EnerJex has increased its production from this project by 10 x from 25 to 250 BOPD since the beginning of 2011 , and it is expected to continue growing for the foreseeable future . Cherokee Project 19

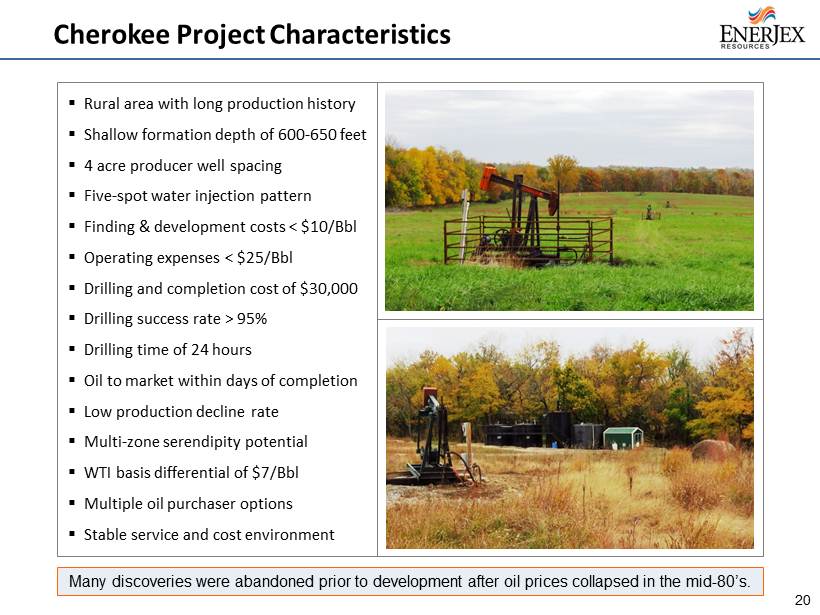

Cherokee Project Characteristics ▪ Rural area with long production history ▪ Shallow formation depth of 600 - 650 feet ▪ 4 acre producer well spacing ▪ Five - spot water injection pattern ▪ Finding & development costs < $10/Bbl ▪ Operating expenses < $25/Bbl ▪ Drilling and completion cost of $30,000 ▪ Drilling success rate > 95% ▪ Drilling time of 24 hours ▪ Oil to market within days of completion ▪ Low production decline rate ▪ Multi - zone serendipity potential ▪ WTI basis differential of $7/Bbl ▪ Multiple oil purchaser options ▪ Stable service and cost environment 20 Many discoveries were abandoned prior to development after oil prices collapsed in the mid - 80’s.

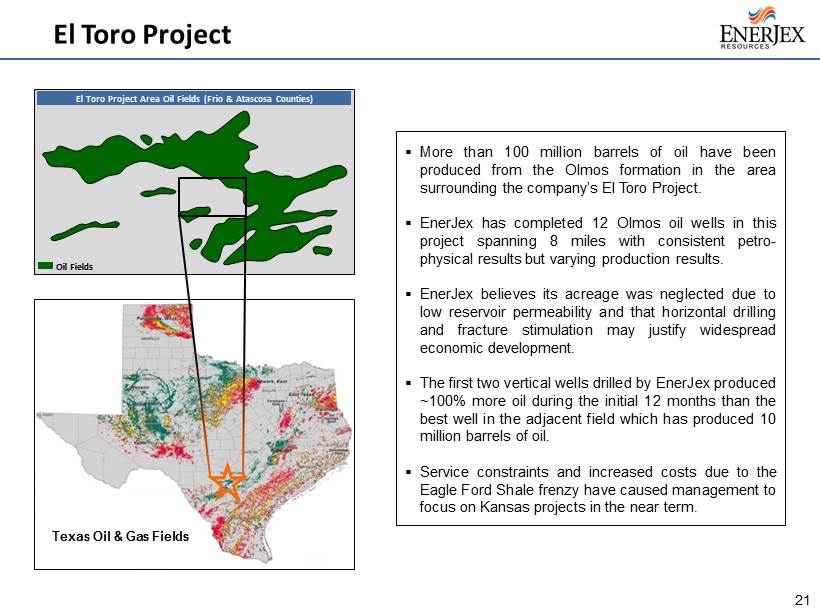

El Toro Project El Toro Project Area Oil Fields (Frio & Atascosa Counties) Oil Fields Texas Oil & Gas Fields ▪ More than 100 million barrels of oil have been produced from the Olmos formation in the area surrounding the company’s El Toro Project . ▪ EnerJex has completed 12 Olmos oil wells in this project spanning 8 miles with consistent petro - physical results but varying production results . ▪ EnerJex believes its acreage was neglected due to low reservoir permeability and that horizontal drilling and fracture stimulation may justify widespread economic development . ▪ The first two vertical wells drilled by EnerJex produced ~ 100 % more oil during the initial 12 months than the best well in the adjacent field which has produced 10 million barrels of oil . ▪ Service constraints and increased costs due to the Eagle Ford Shale frenzy have caused management to focus on Kansas projects in the near term . 21

▪ Key Executives ▪ Senior Credit Facility ▪ Corporate Objectives CORPORATE OVERVIEW

Robert Watson Jr. (Chief Executive Officer) ▪ Co - founder and former CEO of Black Sable Energy, a private oil exploration and production company focused on South Texas that was subsequently sold to ENRJ. ▪ Former President of Centerra Energy Partners, a private oil and gas partnership focused on South Texas. ▪ Senior Associate at American Capital, Ltd. (NASDAQ: ACAS), a publicly traded middle - market private equity firm and global asset manager with $68 billion in assets under management. » Executed 7 transactions in excess of $150 million in invested capital, and actively participated in the daily management of 12 portfolio companies. ▪ Member of Investment Banking Team in the Energy Group at CIBC World Markets. Douglas Wright (Chief Financial Officer) ▪ Former Corporate Controller and Chief Accounting Officer of Nations Petroleum Company, Ltd. » Privately held company grew production of its core U.S. asset from 300 BOPD to ~5,000 BOPD over a 5 - year period before selling to Occidental Petroleum. » Built accounting staff and developed the company’s financial accounting and reporting procedures while arranging $250 million of mezzanine financing. ▪ Oversight of Financial Reporting for subsidiary of Noble Energy, Inc. (NYSE: NBL) from 2005 to 2006. ▪ Responsible for SEC reporting relating to its $3.4 billion acquisition of Patina Oil & Gas Corp. ▪ Served in managerial roles from 1986 to 1996 at Oryx Energy, which was acquired by Kerr McGee Corp. for $3.1 billion. David Kunovic (EVP of Exploration) ▪ Over 30 years of experience as an exploration geologist focused on the Denver - Julesburg Basin. ▪ Held numerous exploration management positions at Kachina Energy, Canyon Energy, Petroleum Incorporated, Newport Exploration, Union Texas Petroleum, and Apache Corp. Key Executives 23

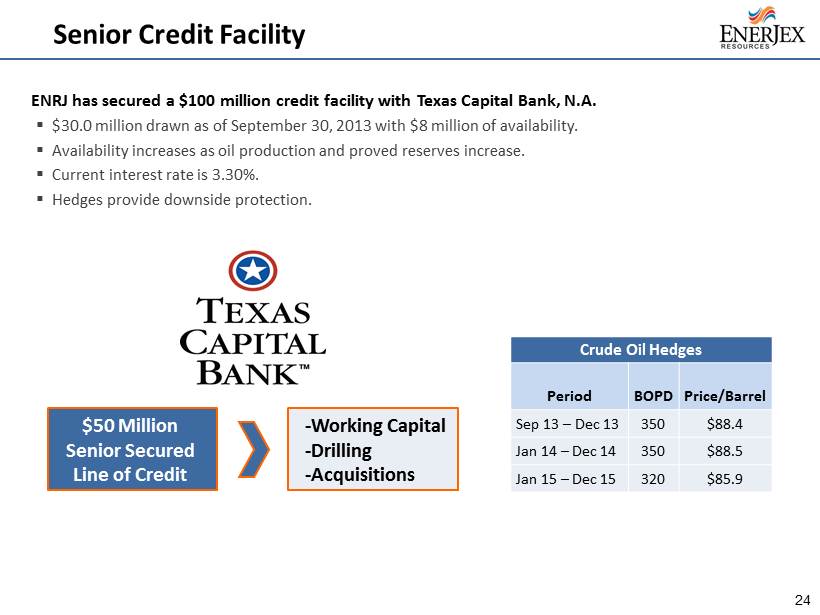

ENRJ has secured a $100 million credit facility with Texas Capital Bank, N.A. ▪ $30.0 million drawn as of September 30, 2013 with $8 million of availability. ▪ Availability increases as oil production and proved reserves increase. ▪ Current interest rate is 3.30%. ▪ Hedges provide downside protection. Senior Credit Facility $50 Million Senior Secured Line of Credit - Working Capital - Drilling - Acquisitions Crude Oil Hedges Period BOPD Price/Barrel Sep 13 – Dec 13 350 $88.4 Jan 14 – Dec 14 350 $88.5 Jan 15 – Dec 15 320 $85.9 24

Corporate Objectives ▪ Increase production to 1,000+ barrels of oil per day through development of existing drilling inventory. ▪ Significantly increase proved oil reserves attributed to existing properties. ▪ List stock on NASDAQ or NYSE MKT. MANAGEMENT IS 100% FOCUSED ON CREATING PER - SHARE VALUE FOR STOCKHOLDERS 25

Corporate Website: www.enerjex.com Corporate Headquarters: 4040 Broadway Street, Suite 508 San Antonio, TX 78209 Chief Executive Officer: Robert Watson, Jr. (210) 451-5545 Investor Relations: Daniel Vernon (405) 230 - 1124 A Domestic Onshore Oil Company