Attached files

| file | filename |

|---|---|

| 8-K - 8-K - CMS ENERGY CORP | d602085d8k.htm |

Exhibit 99.1

Wolfe Research Power & Gas Leaders Conference

Growing Ratebase & Managing Costs

September 25, 2013

Cross Winds Energy Park Consumers Smart Energy Program

Gas Combined Cycle Plant

This presentation is made as of the date hereof and contains “forward-looking statements” as defined in Rule 3b-6 of the

Securities Exchange Act of 1934, Rule 175 of the Securities Act of 1933, and relevant legal decisions. The forward-looking statements are subject to risks and uncertainties. All forward-looking statements should be considered in the context of the risk and other factors detailed from time to time in CMS Energy’s and Consumers Energy’s Securities and Exchange Commission filings. Forward-looking statements should be read in conjunction with “FORWARD-LOOKING STATEMENTS AND

INFORMATION” and “RISK FACTORS” sections of CMS Energy’s and Consumers Energy’s Form 10-K for the year ended

December 31, 2012 and as updated in subsequent 10-Qs. CMS Energy’s and Consumers Energy’s “FORWARD-LOOKING

STATEMENTS AND INFORMATION” and “RISK FACTORS” sections are incorporated herein by reference and discuss important factors that could cause CMS Energy’s and Consumers Energy’s results to differ materially from those anticipated in such statements. CMS Energy and Consumers Energy undertake no obligation to update any of the information presented herein to reflect facts, events or circumstances after the date hereof.

The presentation also includes non-GAAP measures when describing CMS Energy’s results of operations and financial performance. A reconciliation of each of these measures to the most directly comparable GAAP measure is included in the appendix and posted on our website at www.cmsenergy.com.

CMS Energy provides historical financial results on both a reported (Generally Accepted Accounting Principles) and adjusted (non-GAAP) basis and provides forward-looking guidance on an adjusted basis. Management views adjusted earnings as a key measure of the company’s present operating financial performance, unaffected by discontinued operations, asset sales, impairments, regulatory items from prior years, or other items. These items have the potential to impact, favorably or unfavorably, the company’s reported earnings in future periods. Because the company is not able to estimate the impact of these matters, the company is not providing a reconciliation to the comparable future period reported earnings.

2

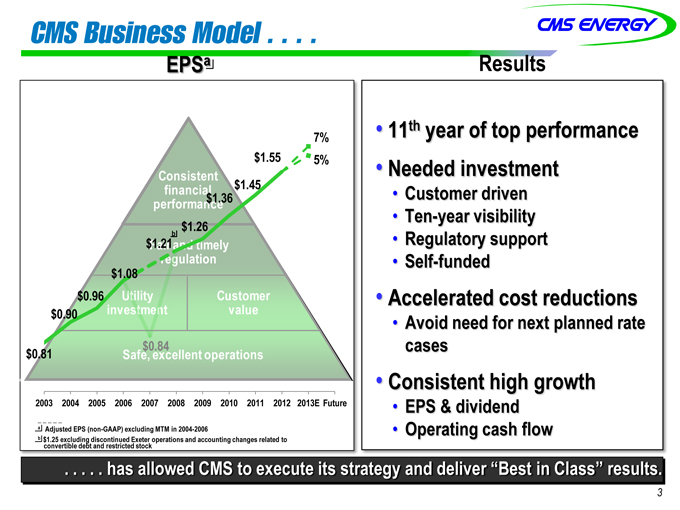

CMS Business Model

EPSa Results

7% 11th year of top performance

$1.55 5% Needed investment

Consistent $1.45

performance financial$1.36 Customer driven

$1.26 Ten-year visibility

$1.21b Regulatory support

Fair and timely

regulation Self-funded

$1.08

$0.96 Utility Customer Accelerated cost reductions

$0.90 investment value

Avoid need for next planned rate

$0.84 cases

$0.81 Safe, excellent operations

Consistent high growth

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E Future EPS & dividend

a Adjusted EPS (non-GAAP) excluding MTM in 2004-2006 Operating cash flow

. . . . . has allowed CMS to execute its strategy and deliver “Best in Class” results.

3

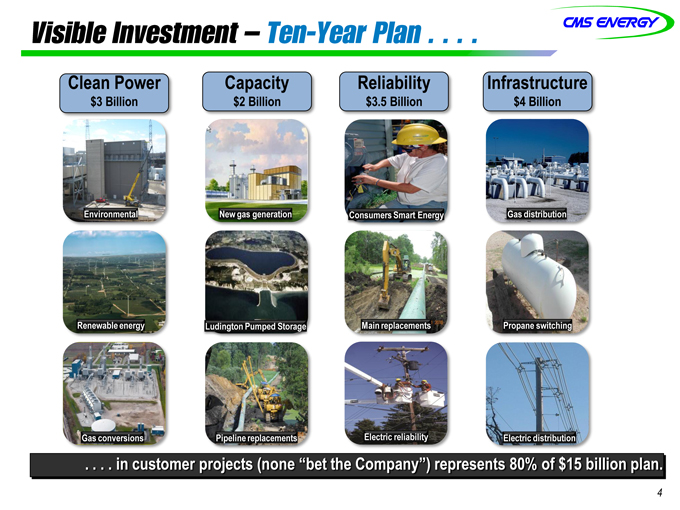

Visible Investment – Ten-Year Plan

Clean Power Capacity Reliability Infrastructure

$3 Billion $2 Billion $3.5 Billion $4 Billion

Environmental New gas generation Consumers Smart Energy Gas distribution

Renewable energy Ludington Pumped Storage Main replacements Propane switching

Gas conversions Pipeline replacements Electric reliability Electric distribution

. . . . in customer projects (none “bet the Company”) represents 80% of $15 billion plan.

4

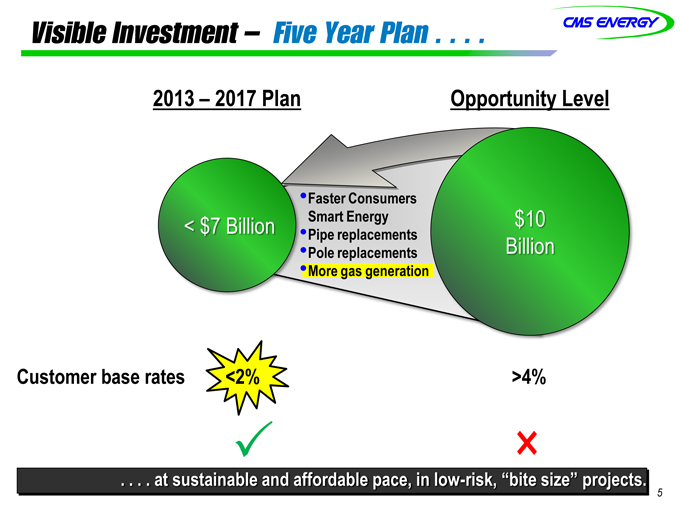

Visible Investment – Five Year Plan

2013 – 2017 Plan Opportunity Level

Faster Consumers

< $7 Billion Pipe Smart replacements Energy $10

Pole replacements Billion

More gas generation

Customer base rates <2% >4%

×

. . . . at sustainable and affordable pace, in low-risk, “bite size” projects.

5

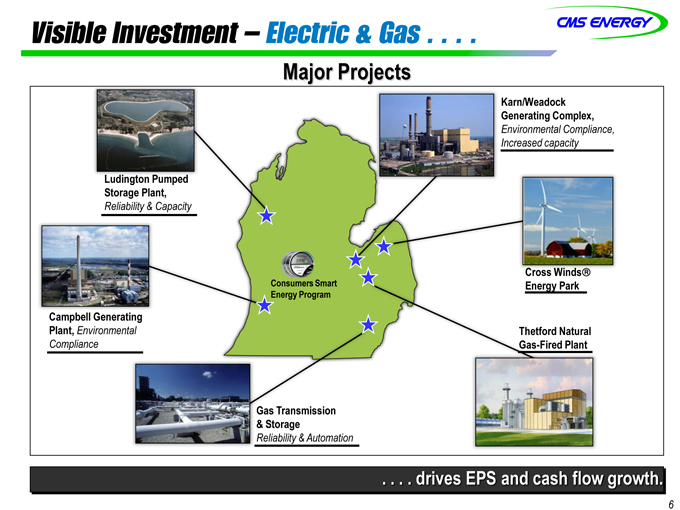

Visible Investment – Electric & Gas

Major Projects

Karn/Weadock

Generating Complex,

Environmental Compliance,

Increased capacity

Storage Plant,

Reliability & Capacit

Consumers Smart gy Park

Energy Program

Campbell Generating

Plant, Environmental ord Natural

Compliance Fired Plant

& Storage

Reliability & Automation

. . . . drives EPS and cash flow growth.

6

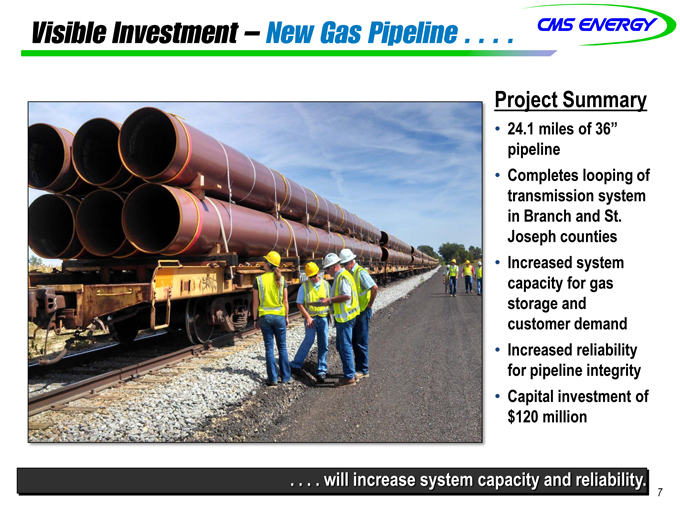

Visible Investment – New Gas Pipeline

Project Summary

24.1 miles of 36” pipeline

Completes looping of transmission system in Branch and St.

Joseph counties

Increased system capacity for gas storage and customer demand

Increased reliability for pipeline integrity

Capital investment of $120 million

. . . . will increase system capacity and reliability.

7

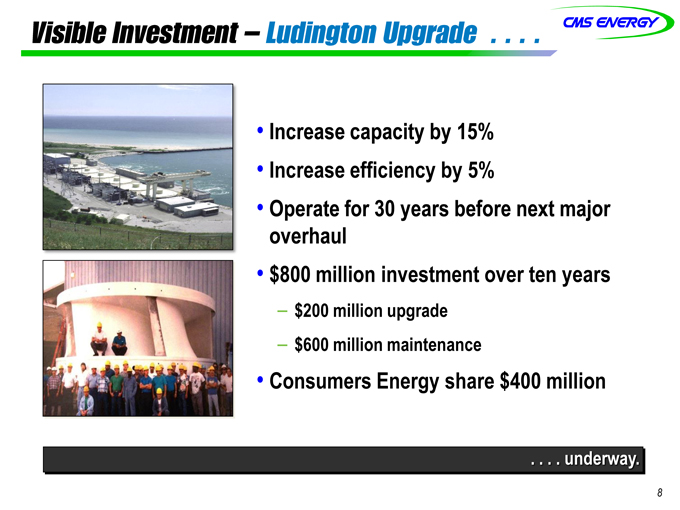

Visible Investment – Ludington Upgrade

Increase capacity by 15%

Increase efficiency by 5%

Operate for 30 years before next major overhaul

$800 million investment over ten years

$200 million upgrade

$600 million maintenance

Consumers Energy share $400 million

. . . . underway.

8

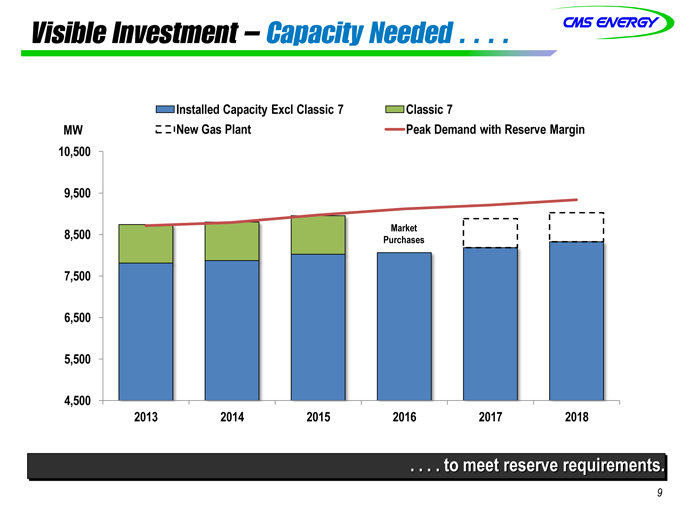

Visible Investment – Capacity Needed

Installed Capacity Excl Classic 7 Classic 7

MW New Gas Plant Peak Demand with Reserve Margin

10,500

9,500

Market

8,500 Purchases

7,500

6,500

5,500

4,500

2013 2014 2015 2016 2017 2018

. . . . to meet reserve requirements.

9

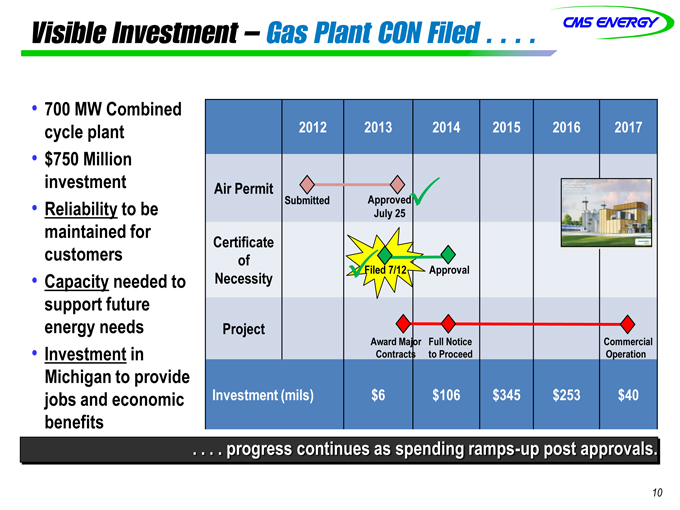

Visible Investment – Gas Plant CON Filed

700 MW Combined cycle plant

$750 Million investment

Reliability to be maintained for customers

Capacity needed to support future energy needs

Investment in Michigan to provide jobs and economic benefits

2012 2013 2014 2015 2016 2017

Air Permit

Submitted Approved

July 25

Certificate

of

Necessity Filed 7/12 Approval

Project

Award Major Full Notice Commercial

Contracts to Proceed Operation

Investment (mils) $6 $106 $345 $253 $40

. . . . progress continues as spending ramps-up post approvals.

10

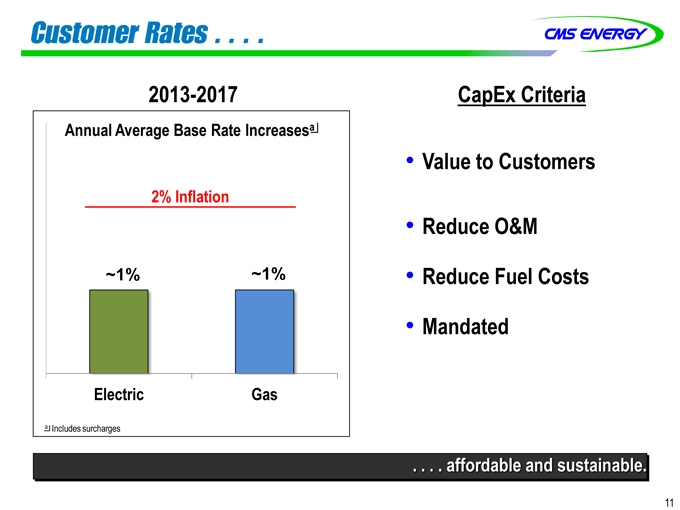

Customer Rates

2013-2017

Annual Average Base Rate Increasesa

2% Inflation

~1%

Electric

~1%

Gas

a Includes surcharges

CapEx

Criteria

Value to Customers

Reduce O&M

Reduce Fuel Costs

Mandated

. . . . affordable and sustainable.

11

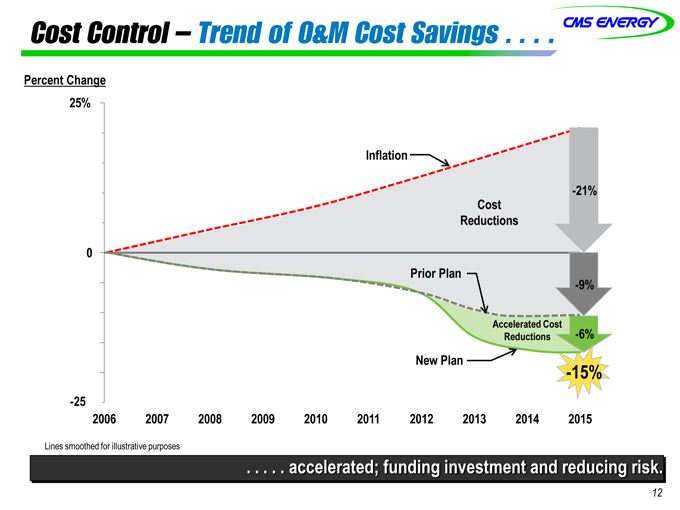

Cost Control – Trend of O&M Cost Savings

Percent Change

25%

Inflation

-21%

Cost

Reductions

0

Prior Plan

-9%

Accelerated Cost

Reductions

-6%

New Plan

-15%

-25%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Lines smoothed for illustrative purposes

. . . .

.

accelerated; funding investment and reducing

risk.

12

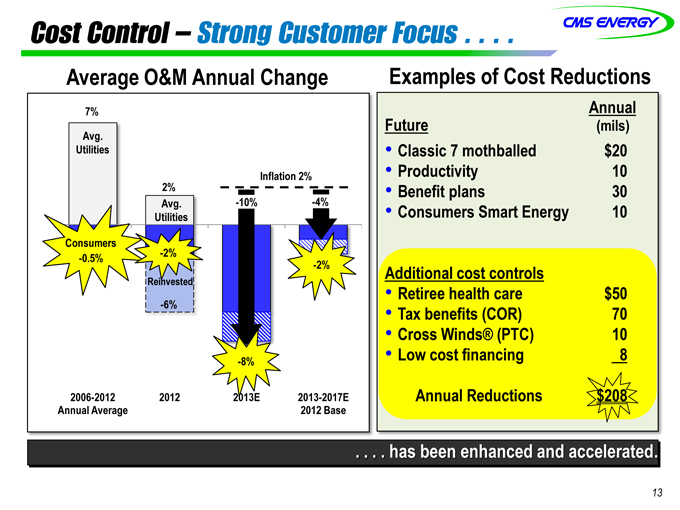

Cost Control – Strong Customer Focus

Average O&M Annual Change

7%

Avg.

Utilities

Inflation 2%

2%

Avg. -10% -4%

Utilities

Consumers

-0.5% -2%

-2%

Reinvested

-6%

-8%

2006-2012 2012 2013E 2013-2017E

Annual Average 2012 Base

Examples of Cost Reductions

Annual

Future(mils)

Classic 7 mothballed $20

Productivity 10

Benefit plans 30

Consumers Smart Energy 10

Additional cost controls

Retiree health care $50

Tax benefits (COR) 70

Cross Winds® (PTC) 10

Low cost financing 8

Annual Reductions $208

[Graphic Appears Here]

. . . . has been enhanced and accelerated.

13

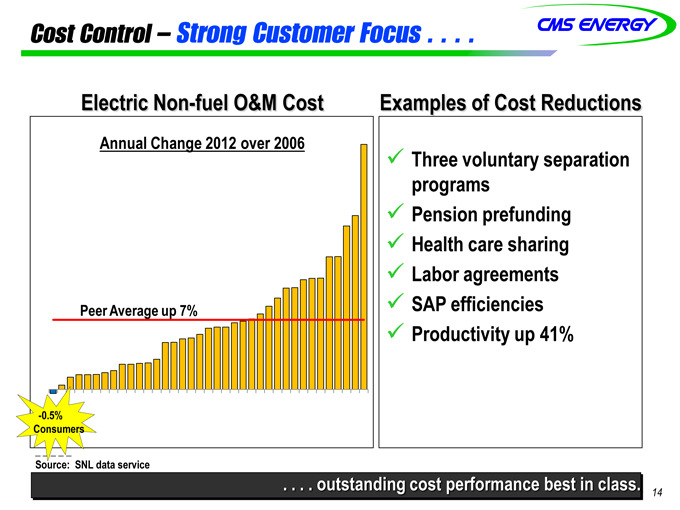

Cost Control – Strong Customer Focus

Electric Non-fuel O&M Cost Examples of Cost Reductions

Annual Change 2012 over 2006

Three voluntary separation

programs

Pension prefunding

Health care sharing

Labor agreements

Peer Average up 7% SAP efficiencies

Productivity up 41%

-0.5%

Consumers

Source: SNL data service

. . . . outstanding cost performance best in class.

14

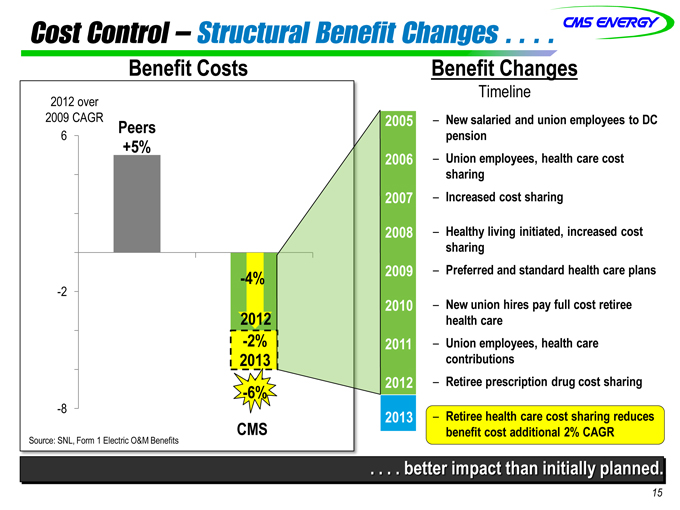

Cost Control – Structural Benefit Changes

Benefit Costs

2012 over

2009 CAGR Peers 2005

6

+5%

2006

2007

2008

-4% 2009

-2

2010

2012

-2% 2011

2013

-6% 2012

-6%

-8 2013

CMS

Source: SNL, Form 1 Electric O&M Benefits

Benefit Changes

Timeline

New salaried and union employees to DC pension

Union employees, health care cost sharing

Increased cost sharing

Healthy living initiated, increased cost sharing

Preferred and standard health care plans

New union hires pay full cost retiree health care

Union employees, health care contributions

Retiree prescription drug cost sharing

Retiree health care cost sharing reduces benefit cost additional 2% CAGR

. . . . better impact than initially planned.

15

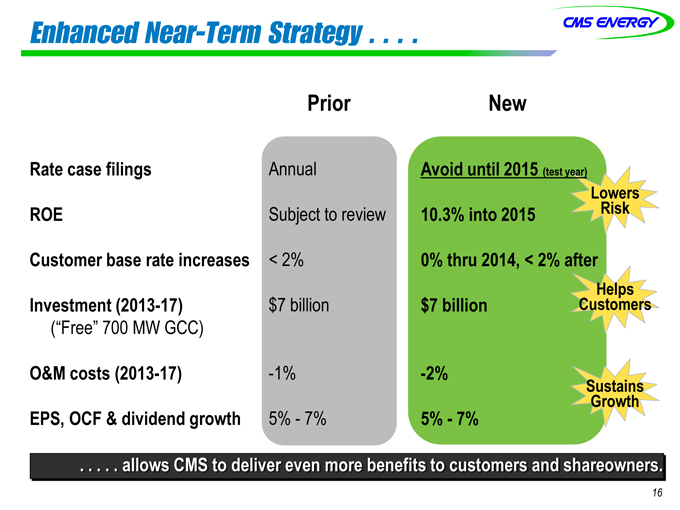

Enhanced Near-Term Strategy

Prior New

Rate case filings Annual Avoid until 2015 (test year)

Lowers

ROE Subject to review 10.3% into 2015 Risk

Customer base rate increases < 2% 0% thru 2014, < 2% after

Helps

Investment (2013-17) $7 billion $7 billion Customers

(“Free” 700 MW GCC)

O&M costs (2013-17) -1% -2%

Sustains

Growth

EPS, OCF & dividend growth 5%—7% 5%—7%

. . . . . allows CMS to deliver even more benefits to customers and shareowners.

16

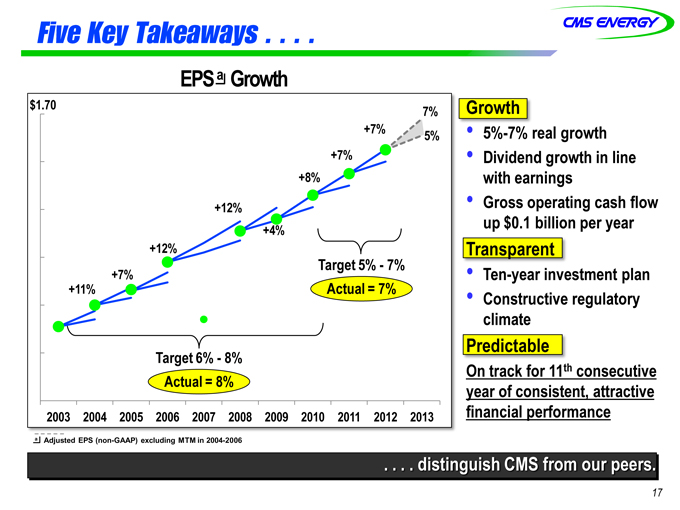

Five Key Takeaways

EPS a Growth

$1.70 7%

+7% 5%

+7%

+8%

+12%

+4%

+12%

+7% Target 5%—7%

+11% Actual = 7%

Target 6%—8%

Actual = 8%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Growth

5%-7% real growth

Dividend growth in line

with earnings

Gross operating cash flow

up $0.1 billion per year

Transparent

Ten-year investment plan

Constructive regulatory

climate

Predictable

On track for 11th consecutive

year of consistent, attractive

financial performance

a Adjusted EPS (non-GAAP) excluding MTM in 2004-2006

. . . . distinguish CMS from our peers.

17

Appendix

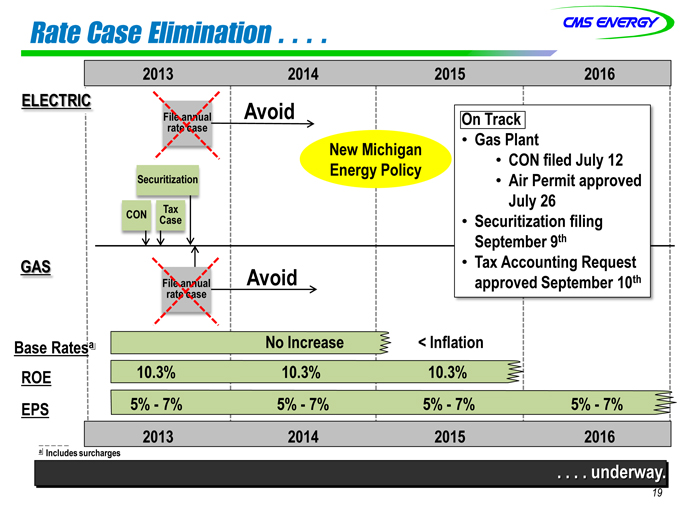

Rate Case Elimination

2013 2014 2015 2016

ELECTRIC Avoid

File annual On Track

rate case

New Michigan Gas Plant

Energy Policy CON filed July 12

Securitization Air Permit approved

July 26

CON Case Tax Securitization filing

September 9th

GAS Tax Accounting Request

File annual Avoid approved September 10th

rate case

Base Ratesa No Increase < Inflation

ROE 10.3% 10.3% 10.3%

EPS 5%—7% 5%—7% 5%—7% 5% -5%7%- 7%

2013 2014 2015 2016

a Includes surcharges

. . . . underway.

19

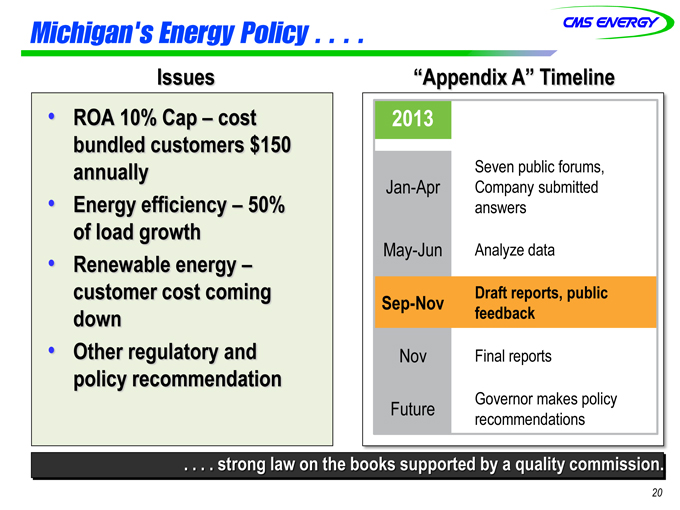

Michigan’s Energy Policy

Issues

ROA 10% Cap – cost bundled customers $150 annually

Energy efficiency – 50% of load growth

Renewable energy – customer cost coming down

Other regulatory and policy recommendation

“Appendix A” Timeline

2013

Seven public forums,

Jan-Apr Company submitted

answers

May-Jun Analyze data

Draft reports, public

Sep-Nov feedback

Nov Final reports

Future Governor makes policy

recommendations

. . . . strong law on the books supported by a quality commission.

20

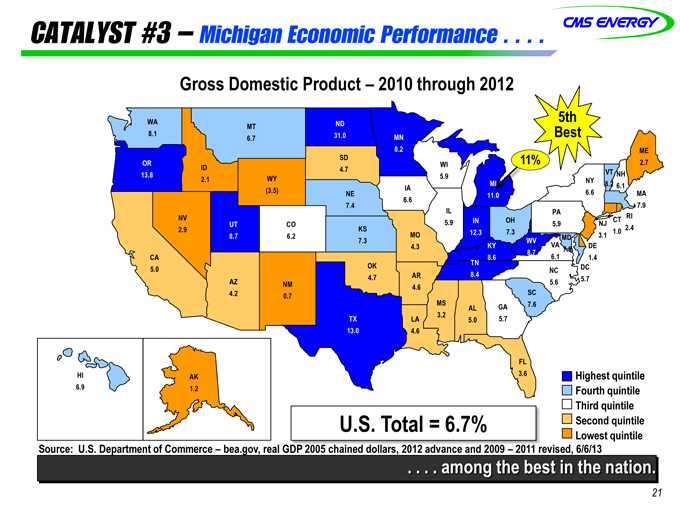

CATALYST#3 – Michigan Economic Performance

Gross Domestic Product – 2010 through 2012

WA ND 5th

MT

8.1 6.7 31.0 MN Best

8.2 ME

OR SD WI 11% 2.7

13.8 ID 4.7 5.9 VT NH

2.1 WY MI NY

IA 8.2 6.1

(3.5) NE 11.0 6.6 MA

6.6

7.4 7.9

IL PA

NV UT CO 5.9 IN OH 5.9 NJ CT RI

2.9 KS 12.3 7.3 1.0 2.4

8.7 6.2 7.3 MO WV MD 3.1

4.3 KY VA 7.5 DE

8.7

CA 8.6 6.1 1.4

OK TN

5.0 NC DC

AZ 4.7 AR 8.4 5.6 5.7

NM 4.6

4.2 0.7 SC

MS AL GA 7.6

3.2

TX LA 5.0 5.7

13.0 4.6

FL

HI AK 3.6 Highest quintile

6.9 1.2 Fourth quintile

Third quintile

U.S. Total = 6.7% Second quintile

Lowest quintile

Source: U.S. Department of Commerce – bea.gov, real GDP 2005 chained dollars, 2012 advance and 2009 – 2011 revised, 6/6/13

. . . . among the best in the nation.

21

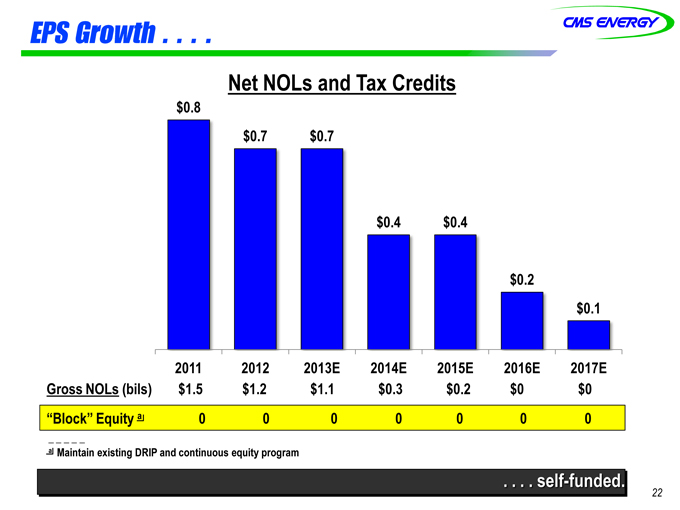

EPS Growth

Net NOLs and Tax Credits

$0.8

$0.7 $0.7

$0.4 $0.4

$0.2

$0.1

2011 2012 2013E 2014E 2015E 2016E 2017E

Gross NOLs (bils) $1.5 $1.2 $1.1 $0.3 $0.2 $0 $0

“Block” Equity a 0 0 0 0 0 0 0

a Maintain existing DRIP and continuous equity program

. . . . self-funded.

22

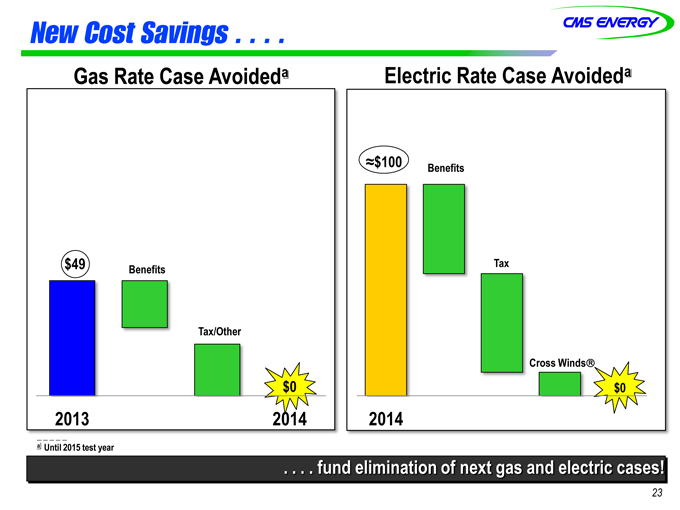

New Cost Savings

Gas Rate Case Avoideda Electric Rate Case Avoideda

$100 Benefits

$49 Benefits Tax

Tax/Other

Cross Winds

$0 $0

2013 2014 2014

a Until 2015 test year

. . . . fund elimination of next gas and electric cases!

23

GAAP Reconciliation

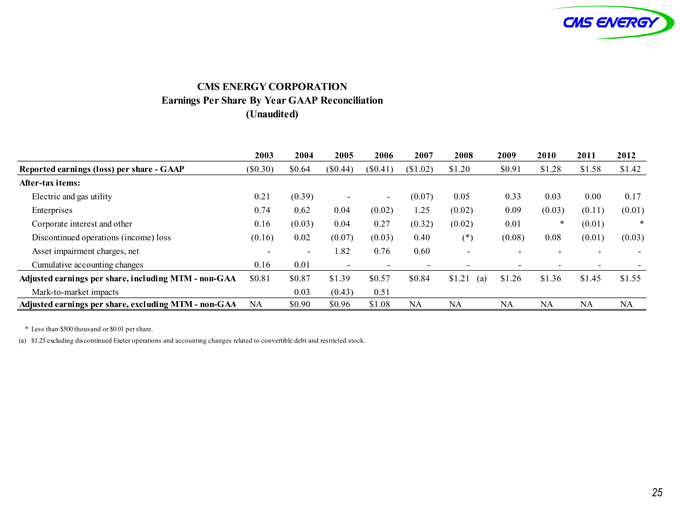

CMS ENERGY CORPORATION

Earnings Per Share By Year GAAP Reconciliation

(Unaudited)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Reported earnings (loss) per share—GAAP($0.30) $0.64($0.44)($0.41)($1.02) $1.20 $0.91 $1.28 $1.58 $1.42

After-tax items:

Electric and gas utility 0.21(0.39) —(0.07) 0.05 0.33 0.03 0.00 0.17

Enterprises 0.74 0.62 0.04(0.02) 1.25(0.02) 0.09(0.03)(0.11)(0.01)

Corporate interest and other 0.16(0.03) 0.04 0.27(0.32)(0.02) 0.01*(0.01)*

Discontinued operations (income) loss(0.16) 0.02(0.07)(0.03) 0.40(*)(0.08) 0.08(0.01)(0.03)

Asset impairment charges, net — 1.82 0.76 0.60 — — -

Cumulative accounting changes 0.16 0.01 — — — —

Adjusted earnings per share, including MTM—non-GAA $0.81 $0.87 $1.39 $0.57 $0.84 $1.21(a) $1.26 $1.36 $1.45 $1.55

Mark-to-market impacts 0.03(0.43) 0.51

Adjusted earnings per share, excluding MTM—non-GAA NA $0.90 $0.96 $1.08 NA NA NA NA NA NA

* Less than $500 thousand or $0.01 per share.

(a) $1.25 excluding discontinued Exeter operations and accounting changes related to convertible debt and restricted stock.

25