Attached files

| file | filename |

|---|---|

| 8-K - FORM 8K - PPL Corp | form8k.htm |

© PPL Corporation 2013

Barclays CEO Energy-Power

Conference

Conference

September 11, 2013

Exhibit 99.1

© PPL Corporation 2013

2

Cautionary Statements and Factors

That May Affect Future Results

That May Affect Future Results

Any statements made in this presentation about future operating

results or other future events are forward-looking statements

under the Safe Harbor Provisions of the Private Securities

Litigation Reform Act of 1995. Actual results may differ materially

from such forward-looking statements. A discussion of factors

that could cause actual results or events to vary is contained in

the Appendix to this presentation and in the Company’s SEC

filings.

results or other future events are forward-looking statements

under the Safe Harbor Provisions of the Private Securities

Litigation Reform Act of 1995. Actual results may differ materially

from such forward-looking statements. A discussion of factors

that could cause actual results or events to vary is contained in

the Appendix to this presentation and in the Company’s SEC

filings.

© PPL Corporation 2013

3

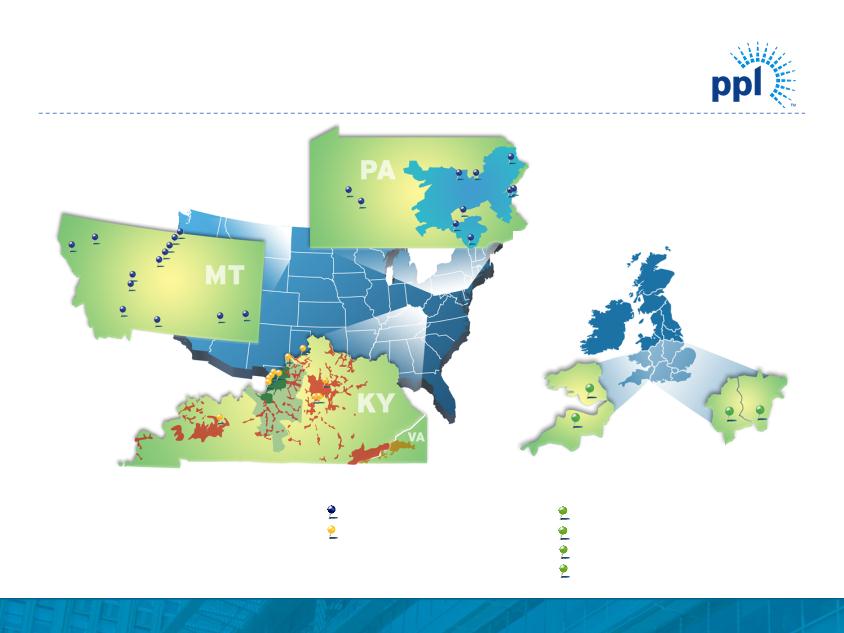

U.K. Delivery Territories:

WPD (South Wales)

WPD (South West)

WPD (West Midlands)

WPD (East Midlands)

U.S. Delivery Territories:

•

PPL Electric Utilities

•

Kentucky Utilities

•

Louisville Gas and Electric

•

•

•

•

•

•

Generation Assets:

Competitive power plants

Regulated power plants

PPL Delivery and Generation Assets

© PPL Corporation 2013

4

• Rate-regulated business provides earnings and dividend stability in weak

economic and market environment

economic and market environment

– 85% of projected 2013 EPS from regulated businesses

– Substantial projected growth in rate base: ~8% CAGR from 2013-2017

– Business Risk Profile rated “Excellent” by S&P

– Secure dividend with strong platform for continued growth

• Highly attractive competitive generation fleet with diverse fuel mix allows for

significant upside when power markets recover

significant upside when power markets recover

– Strong baseload footprint in PJM complemented by flexible gas-fired units

– No major exposure to currently proposed environmental regulations

• Strong management team with track record of execution

– U.K. team best-in-class among U.K. peers

– Awarded 10.25% ROE(1) in Kentucky for both base rates and ECR mechanism

– Awarded 10.4% ROE(1) in Pennsylvania for both base rates and DSIC mechanism

PPL Well-Positioned for Future Success

(1) Effective January 1, 2013.

© PPL Corporation 2013

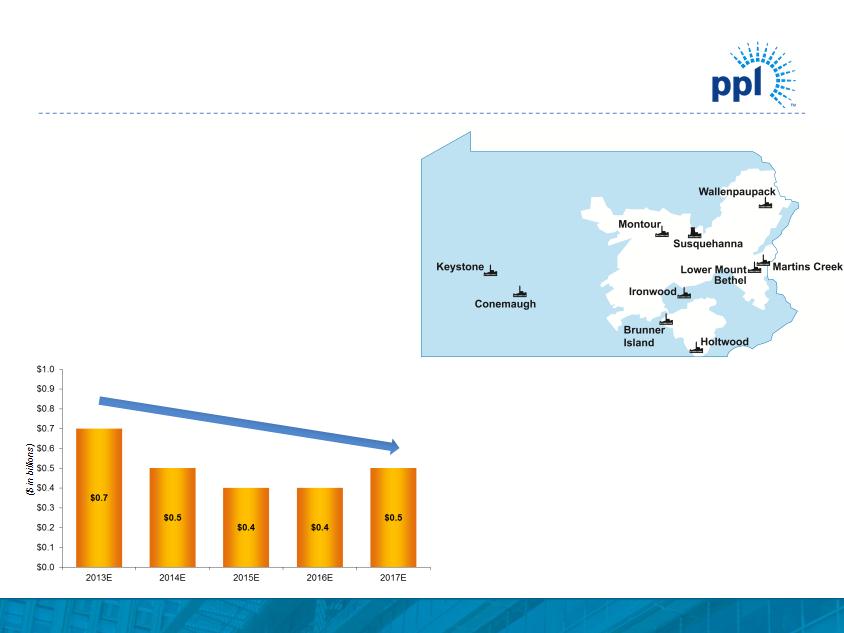

5

Approximately two-thirds of regulated capital expenditures

earn returns subject to minimal or no regulatory lag

earn returns subject to minimal or no regulatory lag

(1)

69%

$1.2

$0.6

$0.6

(1) Includes capex for WPD Midlands. Figures based on assumed exchange rate of $1.58 / GBP.

(2) Assumes 85% of total planned ECR spend as LKE expects between 80% and 90% to receive timely returns via ECR mechanism based on historical experience and future

projections.

projections.

Real-Time Recovery of Regulated

Capex Spending

Capex Spending

73%

$1.1

$0.6

$0.6

71%

$1.1

$0.4

$0.4

($ in billions)

$1.2

$0.3

$0.4

65%

$1.2

$0.3

61%

(2)

$0.1

$0.1

$0.1

$0.1

$0.2

$0.2

© PPL Corporation 2013

6

• Highly attractive rate-regulated business

– Regulator-approved multi-year forward-looking revenues based on future business plan, including capital

expenditures and O&M plus adjustments for inflation

expenditures and O&M plus adjustments for inflation

– Real-time return of and return on capital investment - no lag

– No volumetric risk

– Additional incentives for operational efficiency and high-quality service

• Best-in-class management team with track record of delivering results

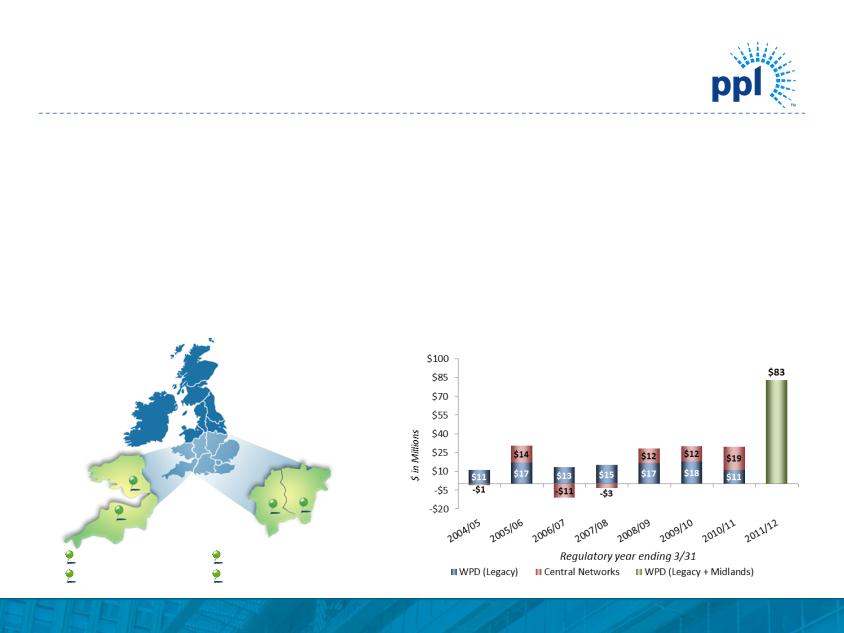

U.K. Regulated Segment

Investment Highlights

Investment Highlights

Top performing electricity distribution business in the U.K.

• WPD has earned over $185 million in annual performance awards

over the past 8 regulatory years

over the past 8 regulatory years

United Kingdom Delivery Territories:

WPD (South Wales)

WPD (South West)

WPD (West Midlands)

WPD (East Midlands)

(1) Central Networks was renamed WPD Midlands upon PPL acquisition in April 2011.

(1)

© PPL Corporation 2013

7

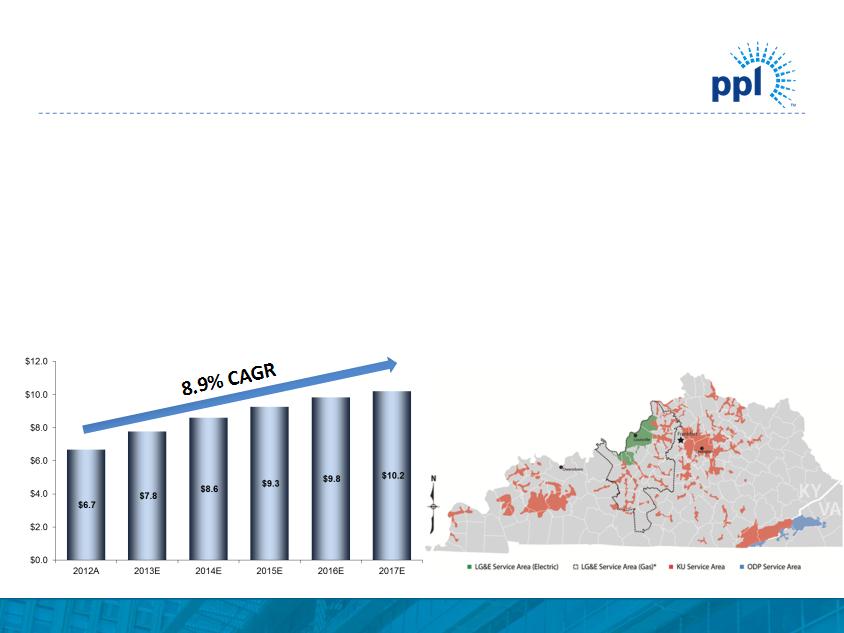

• Efficient, well-run utilities focused on safety, reliability and customer service

• Constructive regulatory environment that provides a timely return on a

substantial amount of planned capex over the next 5 years

substantial amount of planned capex over the next 5 years

– Environmental Cost Recovery (ECR): ~$2.3 billion estimated spend on projects approved by the KPSC with

a 10.25% ROE - virtually no regulatory lag

a 10.25% ROE - virtually no regulatory lag

– Other supportive recovery mechanisms include Construction Work In Progress, Fuel Adjustment Clause,

Gas Supply Clause Adjustment and Demand Side Management recovery

Gas Supply Clause Adjustment and Demand Side Management recovery

Kentucky Regulated Segment

Investment Highlights

Investment Highlights

Significant Rate Base Growth

Kentucky Delivery Territories

($ in billions)

© PPL Corporation 2013

8

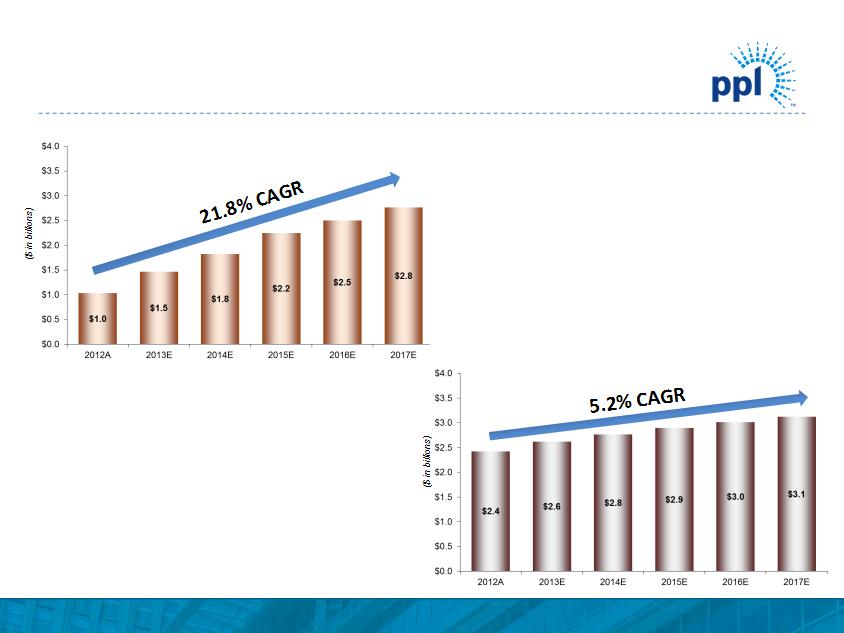

• Significant growth in transmission portion of

business which earns a favorable rate of

return on a near real-time basis

business which earns a favorable rate of

return on a near real-time basis

– CAGR of 21.8% in transmission rate base

through 2017 driven by initiatives to improve

aging infrastructure

through 2017 driven by initiatives to improve

aging infrastructure

– ROE of 11.68% earned through FERC Formula

Rate Mechanism

Rate Mechanism

– Return on CWIP for $310 million of

Northeast/Pocono Reliability project

Northeast/Pocono Reliability project

– ROE of 12.93% and return on CWIP for $630

million Susquehanna-Roseland project

million Susquehanna-Roseland project

Pennsylvania Regulated Segment

Investment Highlights

Investment Highlights

Projected Distribution Rate Base Growth

Projected Transmission Rate Base Growth

• Reliability initiatives drive distribution rate

base growth at a projected CAGR of over 5%

through 2017

base growth at a projected CAGR of over 5%

through 2017

• Act 11 - Alternative ratemaking legislation

provides for more timely recovery of about

$700 million in distribution plant costs that

improve and maintain safety and reliability

over 5 years

provides for more timely recovery of about

$700 million in distribution plant costs that

improve and maintain safety and reliability

over 5 years

© PPL Corporation 2013

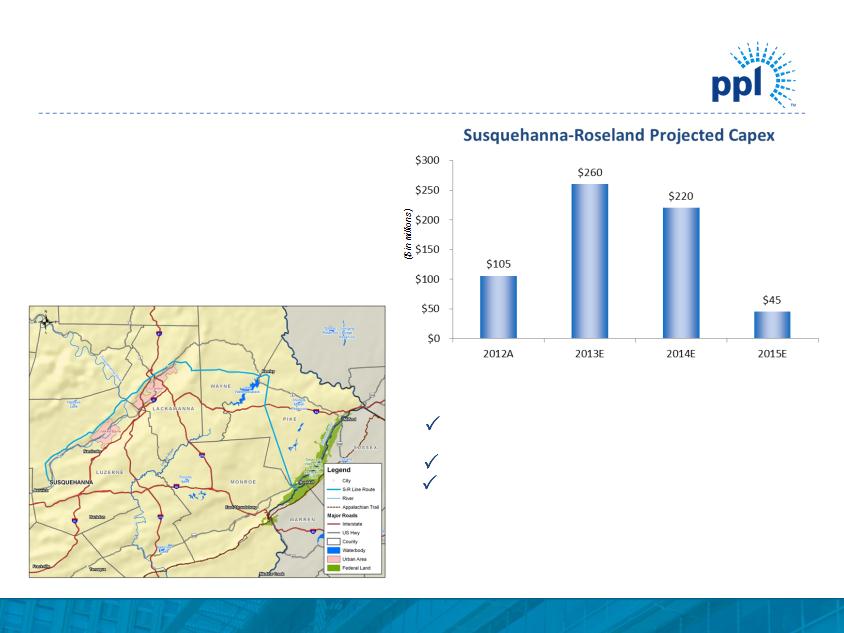

Pennsylvania Regulated: Transmission

Susquehanna-Roseland Project:

• PPL Electric to build Pennsylvania portion of

the 150-mile Susquehanna to Roseland, NJ

the 150-mile Susquehanna to Roseland, NJ

500 kV transmission line. New Jersey portion

of the line to be built by PSEG

of the line to be built by PSEG

• Already approved by both PA and NJ state

utility commissions

utility commissions

• ROE of 12.93% and return on CWIP

9

Key Milestones:

• Oct. 1, 2012 - Official Record of Decision

from the National Park Service

from the National Park Service

• Oct. 2012 - Begin overhead line construction

• March 2013 - Begin Lackawanna 500kV

substation construction

substation construction

• Nov. 2014 - Complete Lackawanna 500kV

substation

substation

• June 2015 - Energize the Susquehanna-

Roseland line

Roseland line

(1) Actual costs to date through December 31, 2012.

(1)

© PPL Corporation 2013

10

• Very well-positioned competitive generation

– PJM assets:

• Excellent mix of low marginal cost nuclear and hydro

facilities, efficient supercritical coal units and

attractive gas-fired assets that capture market

opportunity and back-stop base load unit availability

facilities, efficient supercritical coal units and

attractive gas-fired assets that capture market

opportunity and back-stop base load unit availability

– Montana assets:

• Low marginal cost coal and hydro units that are

critical to infrastructure

critical to infrastructure

Supply Segment

Investment Highlights

Investment Highlights

• Substantially in compliance with new

emissions standards without further major

investments

emissions standards without further major

investments

• Generation fleet will benefit from multiple

factors

factors

– Tightening reserve margins

– General firming of natural gas prices

PJM Generation Assets

Managing capital spend through low commodity cycle

• Cut over $1 billion in capital spending at Supply since 2010

© PPL Corporation 2013

11

A predominant rate-regulated business mix provides strong support for

current dividend and a platform for future growth

current dividend and a platform for future growth

(1) Based on midpoint of revised forecast. Annualized dividend based on 2nd quarter declaration. Actual dividends to be determined by Board of Directors.

(2) From only regulated segments.

(3) See Appendix for the reconciliation of earnings from ongoing operations to reported earnings.

$/Share

Annualized

(2)

(1)

Dividend Profile

(3)

© PPL Corporation 2013

12

Appendix

© PPL Corporation 2013

13

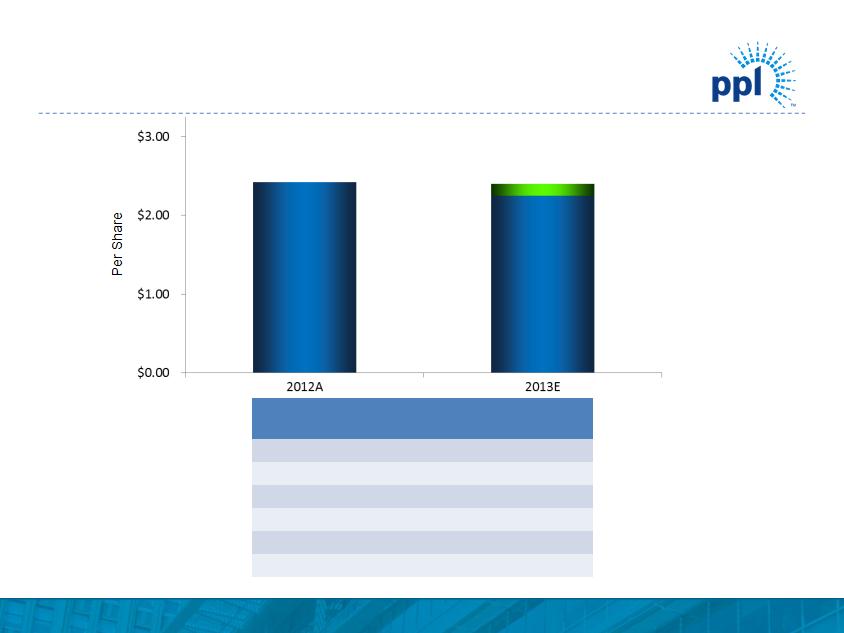

Note: See Appendix for the reconciliation of earnings from ongoing operations to reported earnings.

2013 Ongoing Earnings Forecast

|

Segment

|

2012A

|

2013E

Midpoint |

|

Kentucky Regulated

|

$0.33

|

$0.46

|

|

U.K. Regulated

|

1.19

|

1.28

|

|

PA Regulated

|

0.22

|

0.27

|

|

Supply

|

0.68

|

0.34

|

|

Corporate and Other

|

|

(0.03)

|

|

Total

|

$2.42

|

$2.32

|

$2.42

$2.40

$2.25

© PPL Corporation 2013

14

Weighted-Average Shares - Diluted EPS

(1) Original Forecast of average common shares outstanding included the issuance of common stock to satisfy the 2012 forward equity sale, the DRIP and the settlement of the

PPL Capital Funding equity units in 2013 and 2014.

(2) Revised Forecast reflects PPL’s projected average shares outstanding after adjusting for the removal of equity issuances under the DRIP, the dilutive impact of the 2012

forward equity sale, and the full expected impact of common shares under the 2010 and 2011 Equity Units including the accelerated recognition of equity unit shares

in the calculation of earnings per share effective January 1, 2013. The terms of the equity units have not changed, and the actual issuance of common stock under the

terms of the 2010 Equity Units occurred July 1, 2013 and is still scheduled to occur May 1, 2014 for the 2011 Equity Units.

Average Common Shares Outstanding

(in millions)

|

For the Year Ended

|

Original Forecast(1)

|

Revised Forecast(2)

|

|

December 31, 2013

|

615

|

665

|

|

December 31, 2014

|

670

|

670

|

|

December 31, 2015

|

680

|

670

|

© PPL Corporation 2013

15

P

U.K. Electricity Distribution Price Control

Review Schedule

Review Schedule

|

RIIO-ED1 Timetable

|

|

|

Provisional Timing

|

Milestone

|

|

September 2012

|

Publication of Strategy Consultation

|

|

March 2013

|

Strategy decision published

|

|

July 2013

|

DNOs submit and publish business plans

|

|

November 2013

|

Initial assessment and fast-track Draft Determination published

|

|

March 2014

|

Fast-track Final Determination published

|

|

March 2014

|

Non-fast-track DNOs resubmit & publish business plans

|

|

July 2014

|

Non-fast-track Draft Determination published

|

|

November 2014

|

Non-fast-track Final Determination published

|

|

December 2014

|

Statutory Consultation on license modifications

|

|

April 1, 2015

|

New price control period commences

|

Source: Ofgem, June 2013

Completed

P

P

P

© PPL Corporation 2013

16

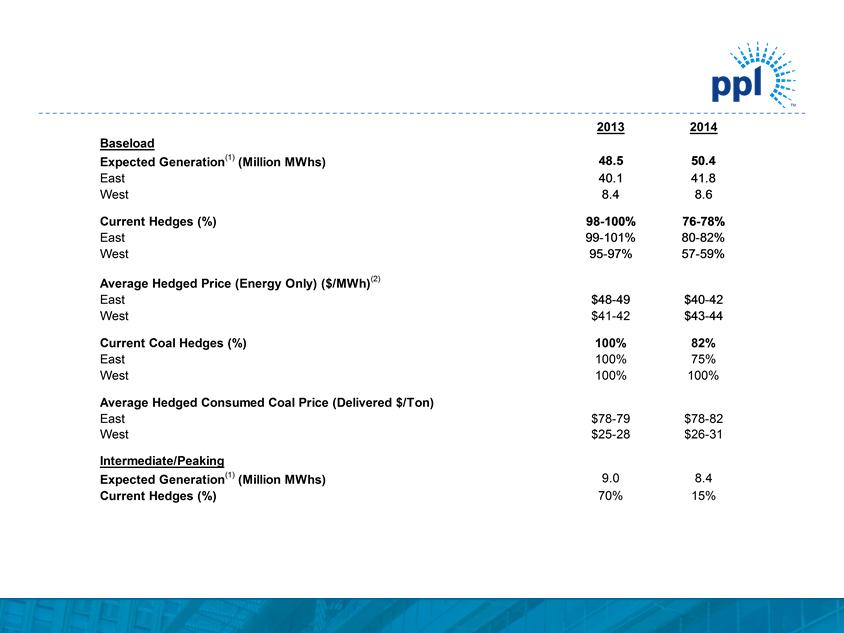

Enhancing Value Through Active Hedging

Capacity revenues are expected to be $590 million and $560 million for 2013 and 2014, respectively.

Note: As of June 30, 2013

(1) Represents expected sales of Supply segment based on current business plan assumptions.

(2) The 2014 ranges of average energy prices for existing hedges were estimated by determining the impact on the existing collars resulting from 2014 power prices at

the 5th and 95th percentile confidence levels.

EEI Bkg_inside2 © PPL Corporation 2013 Burst 16 Enhancing Value Through Active Hedging Capacity revenues are expected to be $590 million and $560 million for 2013 and 2014, respectively. Note: As of June 30, 2013 (1) Represents expected sales of Supply segment based on current business plan assumptions. (2) The 2014 ranges of average energy prices for existing hedges were estimated by determining the impact on the existing collars resulting from 2014 power prices at the 5th and 95th percentile confidence levels. 20132014 Baseload Expected Generation(1) (Million MWhs)48.550.4 .141.8 West 8.48.6 Current Hedges (%)98-100%76-78% East 99-101%80-82% West 95-97%57-59% Average Hedged Price (Energy Only) ($/MWh)(2) East $48-49$40-42 West $41-42$43-44 Current Coal Hedges (%)100%82% East 100%75% West 100 %100% Average Hedged Consumed Coal Price (Delivered $/Ton) East $78-79$78-8 2 West $25-28$26-31 Intermediate/Peaking Expected Generation(1) (Million MWhs)9.08.4 Current Hedges (%)70%15%

© PPL Corporation 2013

17

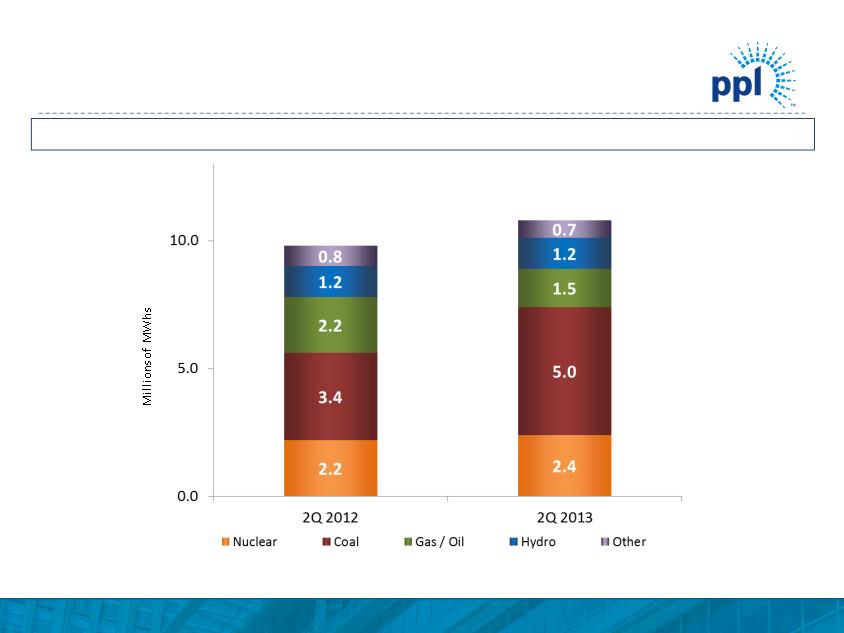

Competitive Generation Overview

Note: As of June 30, 2013

(1) Includes owned and contracted generation.

(2) Other includes PPAs, renewables and NUGS.

9.8

10.8

Total 2Q generation output(1) improved by more than 10% compared to 2Q

2012

2012

(2)

© PPL Corporation 2013

18

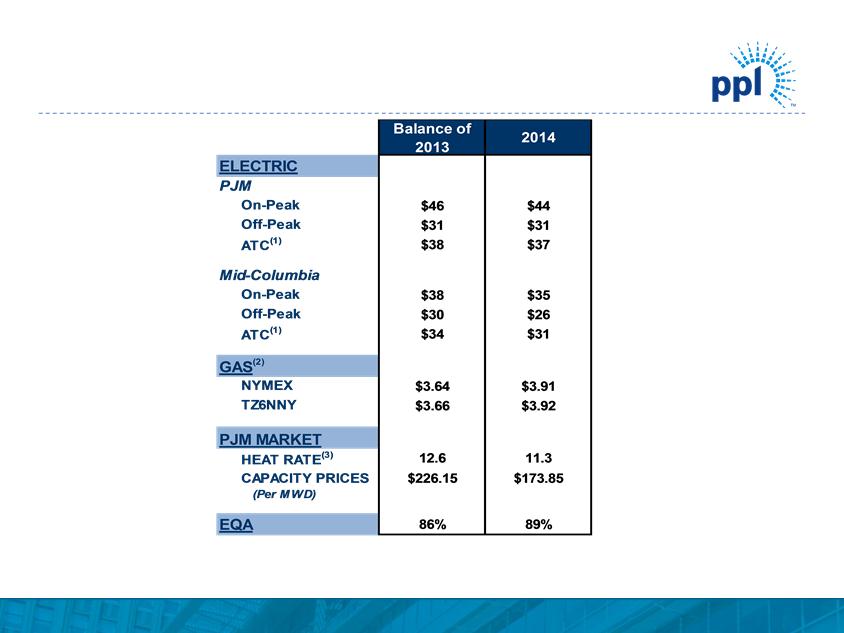

|

(1)

|

24-hour average.

|

|

(2)

|

NYMEX and TZ6NNY forward gas prices on 6/30/2013.

|

|

(3)

|

Market Heat Rate = PJM on-peak power price divided by TZ6NNY gas price.

|

Market Prices

EEI Bkg_inside2 © PPL Corporation 2013 Burst 18 (1) 24-hour average. (2) NYMEX and TZ6NNY forward gas prices on 6/30/2013. (3) Market Heat Rate = PJM on-peak power price divided by TZ6NNY gas price. Market Prices Balance of 20132014$46 $44 $31 $31 $38 $37 $38 $35 $30 $26 $34 $31 $3.64 $3.91 $3.66 $3.92 12.611.3$226.15 $173.85 86%89% ATC(1) NYMEXGAS(2) Mid-Columbia On-Peak Off-Peak ATC(1) ELECTRIC PJM On-Peak Off-Peak(Per MWD) EQAHEAT RATE(3) TZ6NNYPJM MARKETCAPACITY PRICES

© PPL Corporation 2013

19

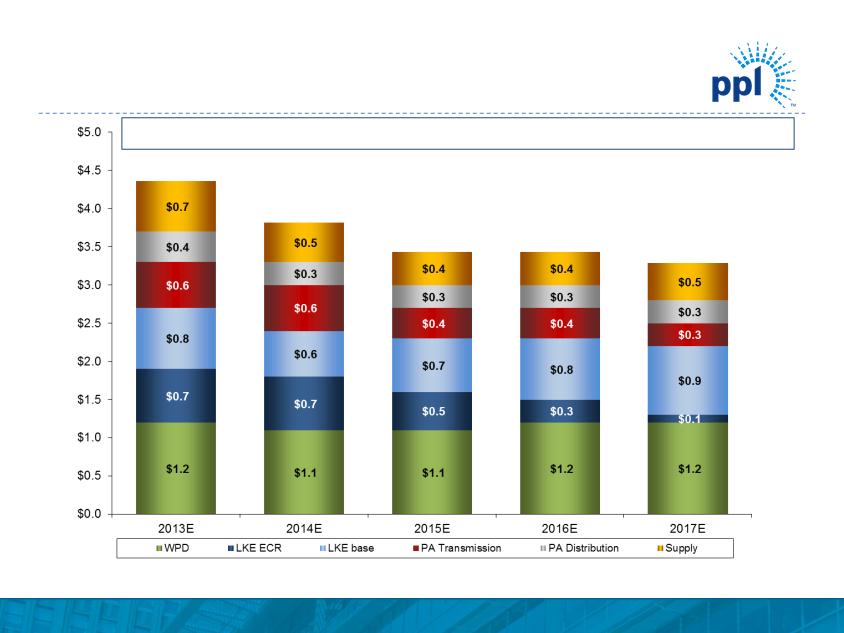

($ in billions)

Note: Corporate and Other capital expenditures average approximately $50 million per year.

(1) Figures based on assumed exchange rate of $1.58 / GBP.

(2) Expect between 80% and 90% to receive timely returns via ECR mechanism based on historical experience and future projections.

(1)

(2)

$4.4

$3.8

$3.4

$3.4

Operating Segment Capital Expenditures

Declining capital expenditures provide additional financial flexibility

$3.3

© PPL Corporation 2013

20

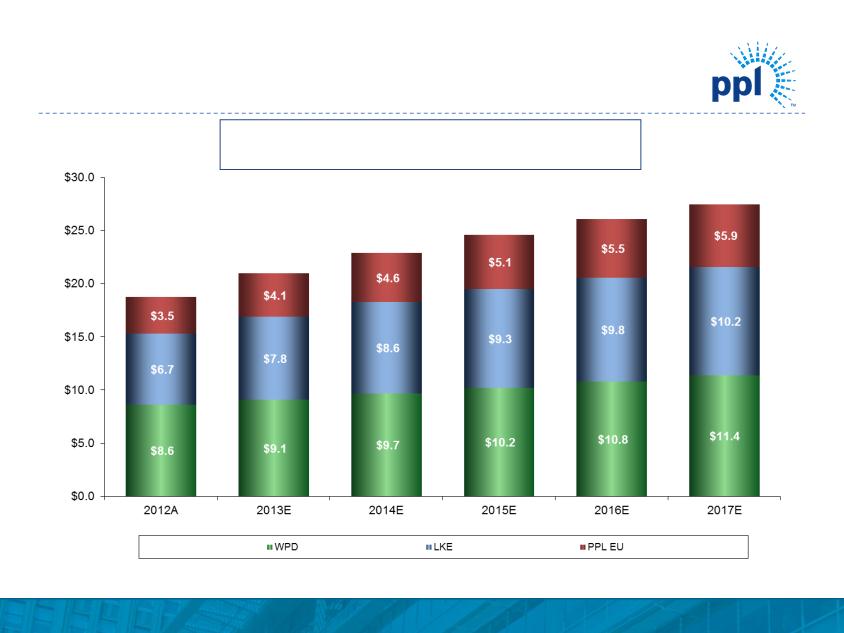

($ in billions)

(1) Represents capitalization for LKE, as LG&E and KU rate constructs are based on capitalization. Represents Regulatory Asset Value (RAV) for WPD.

(2) Figures based on assumed exchange rate of $1.58 / GBP and the RIIO-ED1 business plan as filed on July 1, 2013.

$18.8

$21.0

$22.9

$24.6

(2)

5-Year Regulatory Asset Base(1) CAGR: 7.9%

$26.1

Projected Regulated Rate Base Growth

$27.5

© PPL Corporation 2013

21

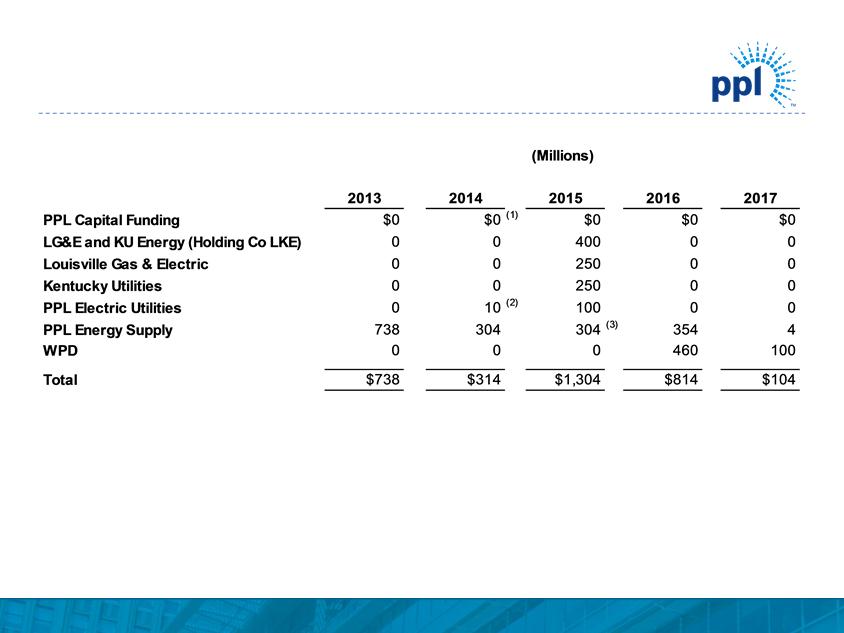

Note: As of June 30, 2013

(1) Excludes $978 million of junior subordinated notes due 2019 that are a component of PPL’s 2011 Equity Units and may be put back to PPL Capital

Funding if the remarketing in 2014 is not successful.

Funding if the remarketing in 2014 is not successful.

(2) Bonds defeased in substance in 2008 by depositing sufficient funds with the trustee.

(3) Includes $300 million of REset Put Securities due 2035 that are required to be put by the holders in October 2015 either for (a) purchase and

remarketing by a remarketing dealer or (b) repurchase by PPL Energy Supply.

remarketing by a remarketing dealer or (b) repurchase by PPL Energy Supply.

Debt Maturities

EEI Bkg_inside2 © PPL Corporation 2013 Burst 21 Note: As of June 30, 2013 (1) Excludes $978 million of junior subordinated notes due 2019 that are a component of PPL’s 2011 Equity Units and may be put back to PPL Capital Funding if the remarketing in 2014 is not successful. (2) Bonds defeased in substance in 2008 by depositing sufficient funds with the trustee. (3) Includes $300 million of REset Put Securities due 2035 that are required to be put by the holders in October 2015 either for (a) purchase and remarketing by a remarketing dealer or (b) repurchase by PPL Energy Supply. 20132014201520162017PPL Capital Funding $0$0 (1)$0$0$0LG&E and KU Energy (Holding Co LKE)0040000 Louisville Gas & Electric 0025000 Kentucky Utilities 0025000 PPL Electric Utilities 010(2)10000PPL Energy Supply738304304(3)3544WPD000460100Total$738$314$1,304$814$104(Millions) Debt Maturities

© PPL Corporation 2013

22

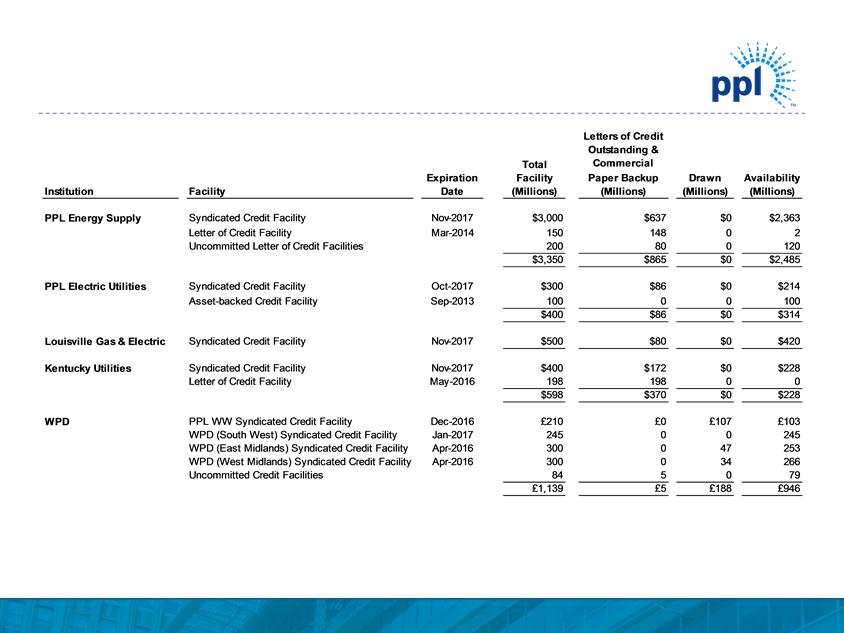

Liquidity Profile

Note: As of June 30, 2013

• Credit facilities consist of a diverse bank group, with no bank and its affiliates providing an aggregate commitment of more than 8% of the total committed

capacity for the domestic facilities and 13% of the total committed capacity for WPD’s facilities.

EEI Bkg_inside2 © PPL Corporation 2013 Burst Institution Facility Expiration Date Total Facility(Millions) Letters of Credit Outstanding & Commercial Paper Backup (Millions) Drawn (Millions) Availability (Millions) PPL Energy Supply Syndicated Credit Facility Nov-2017$3,000$637$0$2,363 Letter of Credit Facility Mar-201415014802 Uncommitted Letter of Credit Facilities 200800120$3,350$865$0$2,485PPL Electric Utilities Syndicated Credit Facility Oct-2017$300$86$0$214 Asset-backed Credit Facility Sep- 201310000100$400$86$0$314 Louisville Gas & Electric Syndicated Credit Facility Nov-2017$500$80$0$420 Kentucky Utilities Syndicated Credit Facility Nov-2017$400$172$0$228 Letter of Credit Facility May-201619819800$598$370$0$228WPDPPL WW Syndicated Credit Facility Dec-2016£210£0£107£103WPD (South West) Syndicated Credit Facility Jan-201724500245WPD (East Midlands) Syndicated Credit Facility Apr-2016300047253WPD (West Midlands) Syndicated Credit Facility Apr-2016300034266 Uncommitted Credit Facilities 845079£1,139£5£188£946 22 Liquidity Profile Note: As of June 30, 2013 • Credit facilities consist of a diverse bank group, with no bank and its affiliates providing an aggregate commitment of more than 8% of the total committed capacity for the domestic facilities and 13% of the total committed capacity for WPD’s facilities

© PPL Corporation 2013

23

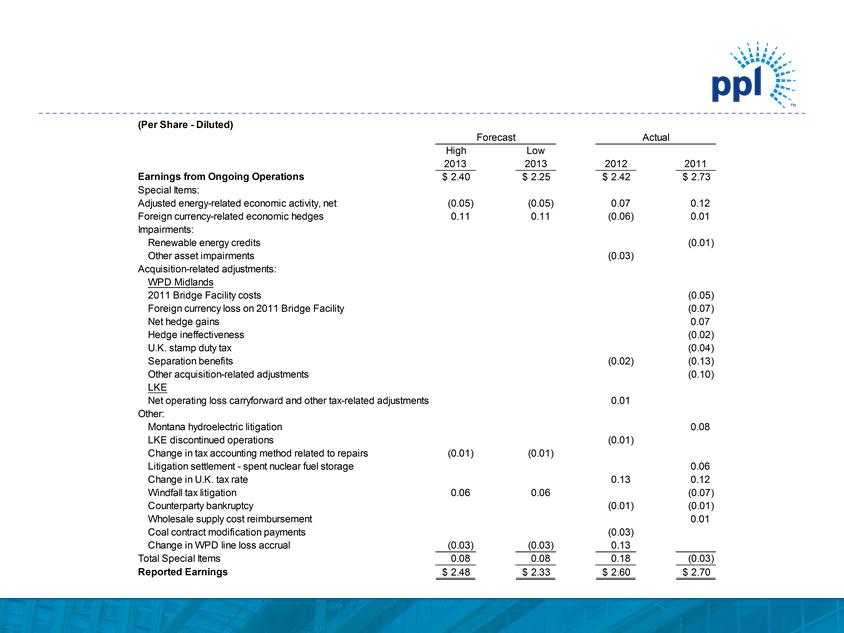

Reconciliation of PPL’s Earnings from

Ongoing Operations to Reported Earnings

Ongoing Operations to Reported Earnings

EEI Bkg_inside2 © PPL Corporation 2013 Burst 23 Reconciliation of PPL’s Earnings from Ongoing Operations to Reported Earnings High Low 20132013201220112.40$ 2.25$ 2.42$ 2.73$ (0.05) (0.05) 0.07 0.12 0.11 0.11 (0.06) 0.01 Renewable energy credits (0.01) Other asset impairments(0.03) WPD Midlands 2011 Bridge Facility costs (0.05) Foreign currency loss on 2011 Bridge Facility (0.07) Net hedge gains 0.07 Hedge ineffectiveness (0.02) U.K. stamp duty tax (0.04) Separation benefits(0.02) (0.13) Other acquisition-related adjustments (0.10) LKE Net operating loss carryforward and other tax-related adjustments 0.01 Montana hydroelectric litigation 0.08 LKE discontinued operations(0.01) Change in tax accounting method related to repairs(0.01) (0.01) Litigation settlement - spent nuclear fuel storage 0.06 Change in U.K. tax rate 0.13 0.12 Windfall tax litigation 0.06 0.06 (0.07) Counterparty bankruptcy(0.01) (0.01) Wholesale supply cost reimbursement 0.01 Coal contract modification payments(0.03) Change in WPD line loss accrual(0.03) (0.03) 0.13 0.08 0.08 0.18 (0.03) 2.48$ 2.33$ 2.60$ 2.70$ Special Items: (Per Share - Diluted) Forecast Actual Earnings from Ongoing Operations Reported Earnings Adjusted energy-related economic activity, net Foreign currency-related economic hedges Impairments: Acquisition-related adjustments: Other: Total Special Items

© PPL Corporation 2013

24

(a) The results of operations for 2012 are not comparable with 2011 due to the acquisition of WPD Midlands. WPD Midlands' results are consolidated on a one-month lag, and include eight months of results in 2011, as the date of

acquisition was April 1, 2011.

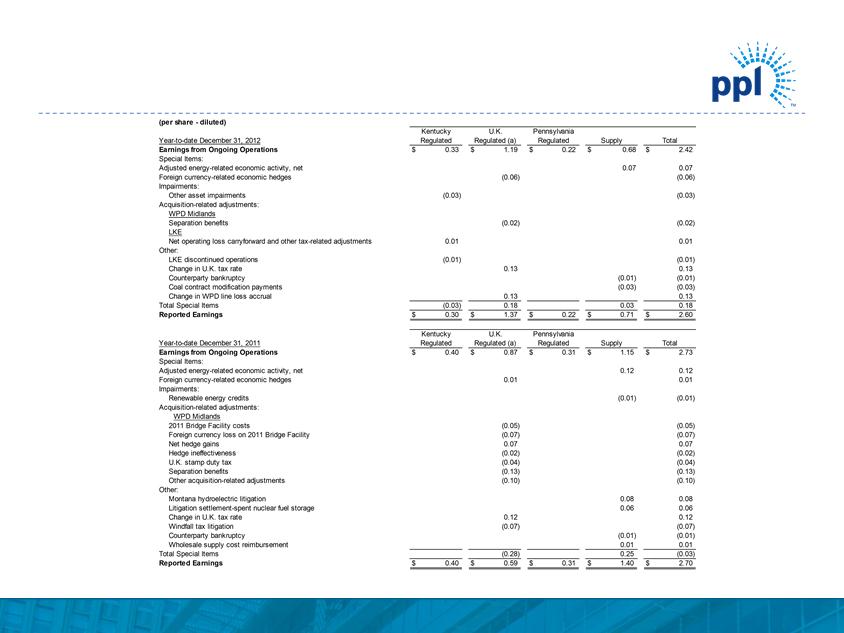

Reconciliation of PPL’s Earnings from

Ongoing Operations to Reported Earnings

Ongoing Operations to Reported Earnings

EEI Bkg_inside2 © PPL Corporation 2013 Burst 24 (a) The results of operations for 2012 are not comparable with 2011 due to the acquisition of WPD Midlands. WPD Midlands' results are consolidated on a one-month lag, and include eight months of results in 2011, as the date of acquisition was April 1, 2011. (per share - diluted) Year-to-date December 31, 2012 Earnings from Ongoing Operations $0.33 $1.19 $0.22 $0.68$2.42 Special Items: Adjusted energy-related economic activity, net 0.070.07 Foreign currency-related economic hedges(0.06) (0.06) Impairments: Other asset impairments(0.03) (0.03) Acquisition-related adjustments: WPD Midlands Separation benefits(0.02) (0.02) LKE Net operating loss carryforward and other tax-related adjustments 0.01 0.01 Other: LKE discontinued operations(0.01) (0.01) Change in U.K. tax rate 0.13 0.13 Counterparty bankruptcy(0.01) (0.01) Coal contract modification payments(0.03) (0.03) Change in WPD line loss accrual 0.13 0.13 Total Special Items(0.03) 0.18 0.03 0.18 Reported Earnings $0.30 $1.37 $0.22 $0.71 $2.60 Year-to-date December 31, 2011 Earnings from Ongoing Operations $0.40 $0.87 $0.31 $1.15 $2.73 Special Items: Adjusted energy-related economic activity, net 0.12 0.12 Foreign currency-related economic hedges 0.01 0.01 Impairments: Renewable energy credits(0.01) (0.01) Acquisition-related adjustments: WPD Midlands 2011 Bridge Facility costs(0.05) (0.05) Foreign currency loss on 2011 Bridge Facility(0.07) (0.07) Net hedge gains 0.07 0.07 Hedge ineffectiveness(0.02) (0.02) U.K. stamp duty tax(0.04) (0.04) Separation benefits(0.13) (0.13) Other acquisition-related adjustments(0.10) (0.10) Other: Montana hydroelectric litigation 0.08 0.08 Litigation settlement-spent nuclear fuel storage 0.06 0.06 Change in U.K. tax rate 0.12 0.12 Windfall tax litigation(0.07) (0.07) Counterparty bankruptcy(0.01) (0.01) Wholesale supply cost reimbursement 0.01 0.01 Total Special Items(0.28) 0.25 (0.03) Reported Earnings $0.40 $0.59 $0.31 $1.40 $2.70 Regulated Regulated (a)Regulated Kentucky U.K. Pennsylvania Supply Total Kentucky U.K. Pennsylvania Regulated Regulated (a)Regulated Supply Total Reconciliation of PPL’s Earnings from Ongoing Operations to Reported Earnings

© PPL Corporation 2013

25

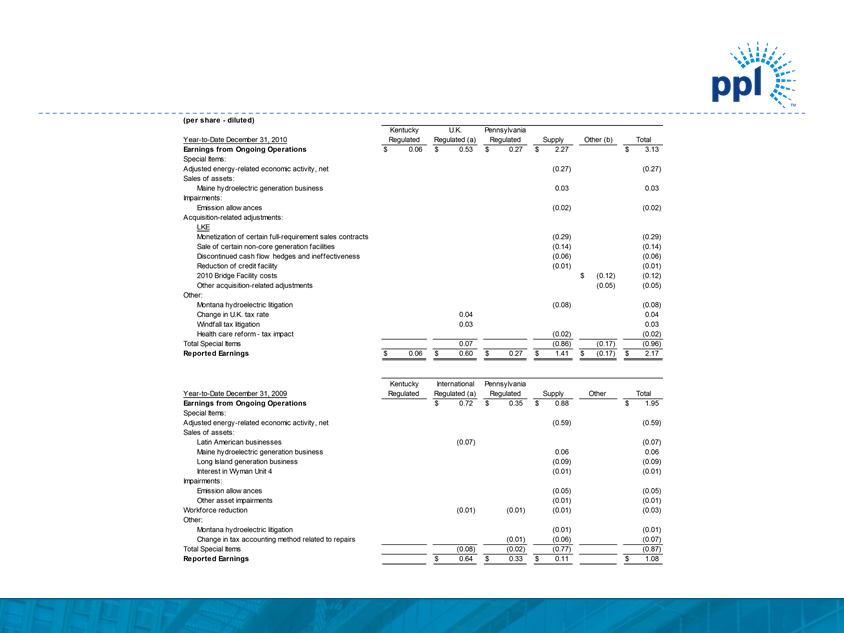

Reconciliation of PPL’s Earnings from

Ongoing Operations to Reported Earnings

Ongoing Operations to Reported Earnings

(a) Following the sale of PPL's Latin American Businesses, this segment was primarily engaged in regulated electricity delivery operations in the U.K. As a result, the "International Regulated" segment was renamed "U.K. Regulated."

(b) Includes certain costs incurred prior to the November 1, 2010 acquisition of LKE.

EEI Bkg_inside2 © PPL Corporation 2013 Burst 25 Reconciliation of PPL’s Earnings from Ongoing Operations to Reported Earnings (a) Following the sale of PPL's Latin American Businesses, this segment was primarily engaged in regulated electricity delivery operations in the U.K. As a result, the "International Regulated" segment was renamed "U.K. Regulated." (b) Includes certain costs incurred prior to the November 1, 2010 acquisition of LKE. Year-to-Date December 31, 2010$0.06 $0.53 $0.27 $2.27 $3.13 (0.27) (0.27) Maine hydroelectric generation business 0.03 0.03 Emission allowances(0.02) (0.02) LKE Monetization of certain full-requirement sales contracts(0.29) (0.29) Sale of certain non-core generation facilities(0.14) (0.14) Discontinued cash flow hedges and ineffectiveness(0.06) (0.06) Reduction of credit facility(0.01) (0.01) 2010 Bridge Facility costs$(0.12) (0.12) Other acquisition-related adjustments(0.05) (0.05) Montana hydroelectric litigation(0.08) (0.08) Change in U.K. tax rate 0.04 0.04 Windfall tax litigation n0.03 0.03 Health care reform - tax impact(0.02) (0.02) 0.07 (0.86) (0.17) (0.96) $0.06 $0.60 $0.27 $1.41 $(0.17) $2.17 Year-to-Date December 31, 2009$0.72 $0.35 $0.88 $1.95 (0.59) (0.59) Latin American businesses(0.07) (0.07) Maine hydroelectric generation business 0.06 0.06 Long Island generation business(0.09) (0.09) Interest in Wyman Unit 4(0.01) (0.01) Emission allowances(0.05) (0.05) Other asset impairments(0.01) (0.01) (0.01) (0.01) (0.01) (0.03) Montana hydroelectric litigation(0.01) (0.01) Change in tax accounting method related to repairs(0.01) (0.06) (0.07) (0.08) (0.02) (0.77) (0.87) $0.64 $0.33 $0.11 $1.08 Other International Regulated Regulated (a)Supply Pennsylvania Sales of assets: Other: Sales of assets: Impairments: Reported Earnings Acquisition-related adjustments: Adjusted energy-related economic activity, net Special Items: Earnings from Ongoing Operations Total Regulated Kentucky Kentucky U.K. Pennsylvania Special Items: Adjusted energy-related economic activity, net Regulated Supply Other (b) (per share - diluted) Total Regulated Regulated (a) Earnings from Ongoing Operations Total Special Items Impairments: Reported Earnings Total Special Items Other: Workforce reduction

© PPL Corporation 2013

26

Statements contained in this presentation, including statements with respect to future earnings, cash flows, financing, regulation and

corporate strategy are "forward-looking statements" within the meaning of the federal securities laws. Although PPL Corporation

believes that the expectations and assumptions reflected in these forward-looking statements are reasonable, these statements are

subject to a number of risks and uncertainties, and actual results may differ materially from the results discussed in the statements.

The following are among the important factors that could cause actual results to differ materially from the forward-looking statements:

market demand and prices for energy, capacity and fuel; weather conditions affecting customer energy usage and operating costs;

competition in power markets; the effect of any business or industry restructuring; the profitability and liquidity of PPL Corporation, its

subsidiaries and customers; new accounting requirements or new interpretations or applications of existing requirements; operating

performance of plants and other facilities; the length of scheduled and unscheduled outages at our generating plants; environmental

conditions and requirements and the related costs of compliance, including environmental capital expenditures and emission allowance

and other expenses; system conditions and operating costs; development of new projects, markets and technologies; performance of

new ventures; asset or business acquisitions and dispositions, and PPL Corporation's ability to realize the expected benefits from

acquired businesses, including the 2010 acquisition of Louisville Gas and Electric Company and Kentucky Utilities Company and the

2011 acquisition of the Central Networks electricity distribution businesses in the U.K.; any impact of hurricanes or other severe

weather on our business, including any impact on fuel prices; receipt of necessary government permits, approvals, rate relief and

regulatory cost recovery; capital market conditions and decisions regarding capital structure; the impact of state, federal or foreign

investigations applicable to PPL Corporation and its subsidiaries; the outcome of litigation against PPL Corporation and its

subsidiaries; stock price performance; the market prices of equity securities and the impact on pension income and resultant cash

funding requirements for defined benefit pension plans; the securities and credit ratings of PPL Corporation and its subsidiaries;

political, regulatory or economic conditions in states, regions or countries where PPL Corporation or its subsidiaries conduct business,

including any potential effects of threatened or actual terrorism or war or other hostilities; foreign exchange rates; new state, federal or

foreign legislation, including new tax legislation; and the commitments and liabilities of PPL Corporation and its subsidiaries. Any such

forward-looking statements should be considered in light of such important factors and in conjunction with PPL Corporation's Form 10-

K and other reports on file with the Securities and Exchange Commission.

corporate strategy are "forward-looking statements" within the meaning of the federal securities laws. Although PPL Corporation

believes that the expectations and assumptions reflected in these forward-looking statements are reasonable, these statements are

subject to a number of risks and uncertainties, and actual results may differ materially from the results discussed in the statements.

The following are among the important factors that could cause actual results to differ materially from the forward-looking statements:

market demand and prices for energy, capacity and fuel; weather conditions affecting customer energy usage and operating costs;

competition in power markets; the effect of any business or industry restructuring; the profitability and liquidity of PPL Corporation, its

subsidiaries and customers; new accounting requirements or new interpretations or applications of existing requirements; operating

performance of plants and other facilities; the length of scheduled and unscheduled outages at our generating plants; environmental

conditions and requirements and the related costs of compliance, including environmental capital expenditures and emission allowance

and other expenses; system conditions and operating costs; development of new projects, markets and technologies; performance of

new ventures; asset or business acquisitions and dispositions, and PPL Corporation's ability to realize the expected benefits from

acquired businesses, including the 2010 acquisition of Louisville Gas and Electric Company and Kentucky Utilities Company and the

2011 acquisition of the Central Networks electricity distribution businesses in the U.K.; any impact of hurricanes or other severe

weather on our business, including any impact on fuel prices; receipt of necessary government permits, approvals, rate relief and

regulatory cost recovery; capital market conditions and decisions regarding capital structure; the impact of state, federal or foreign

investigations applicable to PPL Corporation and its subsidiaries; the outcome of litigation against PPL Corporation and its

subsidiaries; stock price performance; the market prices of equity securities and the impact on pension income and resultant cash

funding requirements for defined benefit pension plans; the securities and credit ratings of PPL Corporation and its subsidiaries;

political, regulatory or economic conditions in states, regions or countries where PPL Corporation or its subsidiaries conduct business,

including any potential effects of threatened or actual terrorism or war or other hostilities; foreign exchange rates; new state, federal or

foreign legislation, including new tax legislation; and the commitments and liabilities of PPL Corporation and its subsidiaries. Any such

forward-looking statements should be considered in light of such important factors and in conjunction with PPL Corporation's Form 10-

K and other reports on file with the Securities and Exchange Commission.

Forward-Looking Information Statement

© PPL Corporation 2013

27

Definitions of Non-GAAP Financial Measures

"Earnings from ongoing operations," also referred to as "ongoing earnings," should not be considered as an alternative to reported earnings, or

net income attributable to PPL shareowners, which is an indicator of operating performance determined in accordance with U.S. generally

accepted accounting principles (GAAP). PPL believes that "earnings from ongoing operations," although a non-GAAP financial measure, is also

useful and meaningful to investors because it provides management's view of PPL's fundamental earnings performance as another criterion in

making investment decisions. PPL's management also uses "earnings from ongoing operations" in measuring certain corporate performance

goals. Other companies may use different measures to present financial performance.

net income attributable to PPL shareowners, which is an indicator of operating performance determined in accordance with U.S. generally

accepted accounting principles (GAAP). PPL believes that "earnings from ongoing operations," although a non-GAAP financial measure, is also

useful and meaningful to investors because it provides management's view of PPL's fundamental earnings performance as another criterion in

making investment decisions. PPL's management also uses "earnings from ongoing operations" in measuring certain corporate performance

goals. Other companies may use different measures to present financial performance.

"Earnings from ongoing operations" is adjusted for the impact of special items. Special items include:

• Adjusted energy-related economic activity (as discussed below).

• Foreign currency-related economic hedges.

• Gains and losses on sales of assets not in the ordinary course of business.

• Impairment charges (including impairments of securities in the company's nuclear decommissioning trust funds).

• Workforce reduction and other restructuring effects.

• Acquisition-related adjustments.

• Other charges or credits that are, in management's view, not reflective of the company's ongoing operations.

Adjusted energy-related economic activity includes the changes in fair value of positions used to economically hedge a portion of the economic

value of PPL's competitive generation assets, full-requirement sales contracts and retail activities. This economic value is subject to changes in

fair value due to market price volatility of the input and output commodities (e.g., fuel and power) prior to the delivery period that was hedged.

Also included in adjusted energy-related economic activity is the premium amortization associated with options and the ineffective portion of

qualifying cash flow hedges and realized economic activity associated with the monetization of certain full-requirement sales contracts in 2010.

This economic activity was deferred, with the exception of the full-requirement sales contracts that were monetized, and included in earnings

from ongoing operations over the delivery period of the item that was hedged or upon realization. Management believes that adjusting for such

amounts provides a better matching of earnings from ongoing operations to the actual amounts settled for PPL's underlying hedged assets.

Please refer to the Notes to the Consolidated Financial Statements and MD&A in PPL Corporation's periodic filings with the Securities and

Exchange Commission for additional information on adjusted energy-related economic activity.

value of PPL's competitive generation assets, full-requirement sales contracts and retail activities. This economic value is subject to changes in

fair value due to market price volatility of the input and output commodities (e.g., fuel and power) prior to the delivery period that was hedged.

Also included in adjusted energy-related economic activity is the premium amortization associated with options and the ineffective portion of

qualifying cash flow hedges and realized economic activity associated with the monetization of certain full-requirement sales contracts in 2010.

This economic activity was deferred, with the exception of the full-requirement sales contracts that were monetized, and included in earnings

from ongoing operations over the delivery period of the item that was hedged or upon realization. Management believes that adjusting for such

amounts provides a better matching of earnings from ongoing operations to the actual amounts settled for PPL's underlying hedged assets.

Please refer to the Notes to the Consolidated Financial Statements and MD&A in PPL Corporation's periodic filings with the Securities and

Exchange Commission for additional information on adjusted energy-related economic activity.

© PPL Corporation 2013

28

Definitions of Non-GAAP Financial Measures

PPL uses "Kentucky Gross Margins," "Pennsylvania Gross Delivery Margins" and "Unregulated Gross Energy Margins." These non-GAAP financial measures

are not intended to replace "Operating Income," which is determined in accordance with GAAP, as an indicator of overall operating performance. Other

companies may use different measures to analyze and to report on the results of their operations. PPL believes that these measures provide additional criteria

to make investment decisions. These performance measures are used, in conjunction with other information, internally by senior management and the Board of

Directors to manage the Kentucky Regulated, Pennsylvania Regulated and Supply segment operations, analyze each respective segment's actual results

compared with budget and, in certain cases, to measure certain corporate financial goals used in determining variable compensation.

are not intended to replace "Operating Income," which is determined in accordance with GAAP, as an indicator of overall operating performance. Other

companies may use different measures to analyze and to report on the results of their operations. PPL believes that these measures provide additional criteria

to make investment decisions. These performance measures are used, in conjunction with other information, internally by senior management and the Board of

Directors to manage the Kentucky Regulated, Pennsylvania Regulated and Supply segment operations, analyze each respective segment's actual results

compared with budget and, in certain cases, to measure certain corporate financial goals used in determining variable compensation.

"Kentucky Gross Margins" is a single financial performance measure of the Kentucky Regulated segment's electricity generation, transmission and distribution

operations as well as its distribution and sale of natural gas. In calculating this measure, fuel and energy purchases are deducted from revenues. In addition,

utility revenues and expenses associated with approved cost recovery mechanisms are offset. These mechanisms allow for recovery of certain expenses, return

on capital investments and performance incentives. Certain costs associated with these mechanisms, primarily ECR, DSM and GLT, are recorded as "Other

operation and maintenance" and "Depreciation." As a result, this measure represents the net revenues from the Kentucky Regulated segment's operations.

operations as well as its distribution and sale of natural gas. In calculating this measure, fuel and energy purchases are deducted from revenues. In addition,

utility revenues and expenses associated with approved cost recovery mechanisms are offset. These mechanisms allow for recovery of certain expenses, return

on capital investments and performance incentives. Certain costs associated with these mechanisms, primarily ECR, DSM and GLT, are recorded as "Other

operation and maintenance" and "Depreciation." As a result, this measure represents the net revenues from the Kentucky Regulated segment's operations.

"Pennsylvania Gross Delivery Margins" is a single financial performance measure of the Pennsylvania Regulated segment's electric delivery operations, which

includes transmission and distribution activities. In calculating this measure, utility revenues and expenses associated with approved recovery mechanisms,

including energy provided as a PLR, are offset with minimal impact on earnings. Costs associated with these mechanisms are recorded in "Energy purchases,"

"Other operation and maintenance," which is primarily Act 129 costs, and "Taxes, other than income," which is primarily gross receipts tax. This performance

measure includes PLR energy purchases by PPL Electric from PPL EnergyPlus, which are reflected in "PLR intersegment utility revenue (expense)." As a

result, this measure represents the net revenues from the Pennsylvania Regulated segment's electric delivery operations.

includes transmission and distribution activities. In calculating this measure, utility revenues and expenses associated with approved recovery mechanisms,

including energy provided as a PLR, are offset with minimal impact on earnings. Costs associated with these mechanisms are recorded in "Energy purchases,"

"Other operation and maintenance," which is primarily Act 129 costs, and "Taxes, other than income," which is primarily gross receipts tax. This performance

measure includes PLR energy purchases by PPL Electric from PPL EnergyPlus, which are reflected in "PLR intersegment utility revenue (expense)." As a

result, this measure represents the net revenues from the Pennsylvania Regulated segment's electric delivery operations.

"Unregulated Gross Energy Margins" is a single financial performance measure of the Supply segment's competitive energy non-trading and trading activities. In

calculating this measure, the Supply segment's energy revenues are offset by the cost of fuel, energy purchases, certain other operation and maintenance

expenses, primarily ancillary charges and gross receipts tax, which is recorded in "Taxes, other than income." This performance measure is relevant to PPL due

to the volatility in the individual revenue and expense lines on the Statements of Income that comprise "Unregulated Gross Energy Margins." This volatility

stems from a number of factors, including the required netting of certain transactions with ISOs and significant fluctuations in unrealized gains and losses. Such

factors could result in gains or losses being recorded in either "Wholesale energy marketing" or "Energy purchases" on the Statements of Income. This

performance measure includes PLR revenues from energy sales to PPL Electric by PPL EnergyPlus, which are recorded in "PLR intersegment utility revenue

(expense)." PPL excludes from "Unregulated Gross Energy Margins" the Supply segment's adjusted energy-related economic activity, which includes the

changes in fair value of positions used to economically hedge a portion of the economic value of PPL's competitive generation assets, full-requirement sales

contracts and retail activities. This economic value is subject to changes in fair value due to market price volatility of the input and output commodities (e.g., fuel

and power) prior to the delivery period that was hedged. Also included in adjusted energy-related economic activity is the premium amortization associated with

options, the ineffective portion of qualifying cash flow hedges and realized economic activity associated with the monetization of certain full-requirement sales

contracts in 2010. This economic activity was deferred, with the exception of the full-requirement sales contracts that were monetized, and included in

"Unregulated Gross Energy Margins" over the delivery period that was hedged or upon realization.

calculating this measure, the Supply segment's energy revenues are offset by the cost of fuel, energy purchases, certain other operation and maintenance

expenses, primarily ancillary charges and gross receipts tax, which is recorded in "Taxes, other than income." This performance measure is relevant to PPL due

to the volatility in the individual revenue and expense lines on the Statements of Income that comprise "Unregulated Gross Energy Margins." This volatility

stems from a number of factors, including the required netting of certain transactions with ISOs and significant fluctuations in unrealized gains and losses. Such

factors could result in gains or losses being recorded in either "Wholesale energy marketing" or "Energy purchases" on the Statements of Income. This

performance measure includes PLR revenues from energy sales to PPL Electric by PPL EnergyPlus, which are recorded in "PLR intersegment utility revenue

(expense)." PPL excludes from "Unregulated Gross Energy Margins" the Supply segment's adjusted energy-related economic activity, which includes the

changes in fair value of positions used to economically hedge a portion of the economic value of PPL's competitive generation assets, full-requirement sales

contracts and retail activities. This economic value is subject to changes in fair value due to market price volatility of the input and output commodities (e.g., fuel

and power) prior to the delivery period that was hedged. Also included in adjusted energy-related economic activity is the premium amortization associated with

options, the ineffective portion of qualifying cash flow hedges and realized economic activity associated with the monetization of certain full-requirement sales

contracts in 2010. This economic activity was deferred, with the exception of the full-requirement sales contracts that were monetized, and included in

"Unregulated Gross Energy Margins" over the delivery period that was hedged or upon realization.