Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - NTELOS HOLDINGS CORP. | d596657d8k.htm |

NASDAQ: NTLS

Investor Presentation

September 2013

Exhibit 99.1 |

Presentation of Financial and Other Important Information

2

NASDAQ: NTLS

USE OF NON-GAAP FINANCIAL MEASURES

Included in this presentation are certain non-GAAP financial measures that are not determined in

accordance with US generally accepted accounting principles (“GAAP”). These financial

performance measures are not indicative of cash provided or used by operating activities and exclude the effects of certain operating,

capital and financing costs and may differ from comparable information provided by other companies,

and they should not be considered in isolation, as an alternative to, or more meaningful than

measures of financial performance determined in accordance with US generally accepted accounting principles. These

financial performance measures are commonly used in the industry and are presented because NTELOS

believes they provide relevant and useful information to investors. NTELOS utilizes these

financial performance measures to assess its ability to meet future capital expenditure and working capital requirements, to

incur indebtedness if necessary, and to fund continued growth. NTELOS also uses these financial

performance measures to evaluate the performance of its business, for budget planning purposes

and as factors in its employee compensation programs. Adjusted EBITDA is defined as net income attributable to

NTELOS Holdings Corp. before interest, income taxes, depreciation and amortization, accretion of asset

retirement obligations, gain/loss on derivatives, net income attributable to

non-controlling interests, other expenses/income, equity based compensation charges, acquisition related charges, gain/loss on sale of

assets and net loss from discontinued operations and costs related to the separation of the wireless

and wireline companies. Please review the reconciliations and other definitions of non-GAAP

financial measures contained in the press releases filed by the Company with the SEC, including those filed on Form 8-K on

August 1, 2012, November 8, 2012, February 28, 2013, May 7, 2013 and July 30, 2013.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Any statements contained in this presentation that are not statements of historical fact, including

statements about our beliefs and expectations, are forward- looking statements and should be

evaluated as such. The words “anticipates,” “believes,” “expects,” “intends,” “plans,” “estimates,” “targets,” “projects,” “should

“may,” “will” and similar words and expressions are intended to identify

forward-looking statements. Such forward-looking statements reflect, among other

things, our current expectations, plans and strategies, and anticipated financial results, all of

which are subject to known and unknown risks, uncertainties and factors that may cause our

actual results to differ materially from those expressed or implied by these forward-looking statements. Many of these risks are

beyond our ability to control or predict. Because of these risks, uncertainties and assumptions, you

should not place undue reliance on these forward-looking statements. Furthermore,

forward-looking statements speak only as of the date they are made. We do not undertake any obligation to update or review any

forward-looking information, whether as a result of new information, future events or

otherwise. Important factors with respect to any such forward-looking statements,

including certain risks and uncertainties that could cause actual results to differ from those contained in the forward-looking statements, include,

but are not limited to: our ability to attract and retain retail subscribers to our services;

our dependence on our strategic relationship and the potential outcome of any disputes with

Sprint Nextel (“Sprint”); a potential increase in roaming rates and wireless handset subsidy costs; rapid development and intense

competition in the telecommunications industry; our ability to finance, design, construct and realize

the benefits of any planned network technology upgrade; our ability to acquire or gain access

to additional spectrum; the potential to experience a high rate of customer turnover; the potential for Sprint and others to

build networks in our markets; cash and capital requirements; operating and financial restrictions

imposed by our senior credit facility; adverse economic conditions; federal and state

regulatory fees, requirements and developments; loss of ability to use our current cell sites; our continued reliance on indirect

channels of retail distribution; our reliance on certain suppliers and vendors; and other unforeseen

difficulties that may occur. These risks and uncertainties are not intended to represent a

complete list of all risks and uncertainties inherent in our business, and should be read in conjunction with the more detailed

cautionary statements and risk factors included in our SEC filings, including our most recent Annual

Report filed on Form 10-K. |

Company Overview

3

Leading “pure-play”

wireless carrier in mid-Atlantic region

Headquartered in Waynesboro, VA

Exclusive CDMA Network provider for Sprint in WV and Western VA

NTELOS-branded retail postpay and prepay subscribers; robust wholesale

business NASDAQ: NTLS

NASDAQ:

NTLS

–

Market

Capitalization

approximately

$348

million¹

7.9 million licensed POPs; covered POPs of 6.0 million; 454,800 subscribers

¹

As of market close 9/9/13 |

Investment Considerations

Leading “pure-play”

regional wireless company

4

Strategic asset set

Strong free cash flow

Broad geographic and network technology footprint

Experienced management team

NASDAQ: NTLS

Competitive and diversified business model |

Key

Operating Strategies 5

Elevate brand & best value in wireless position to improve quality of

subscriber base and grow market share

Enhance customer experience at all touch points by focusing on core differentiators

of Savings, Simplicity and Service to improve customer satisfaction and

reduce subscriber

churn

Leverage disciplined network investments to expand revenues and margins

Drive Smartphone and data services penetration to increase ARPU

NASDAQ: NTLS

Manage cost structure to improve profitability |

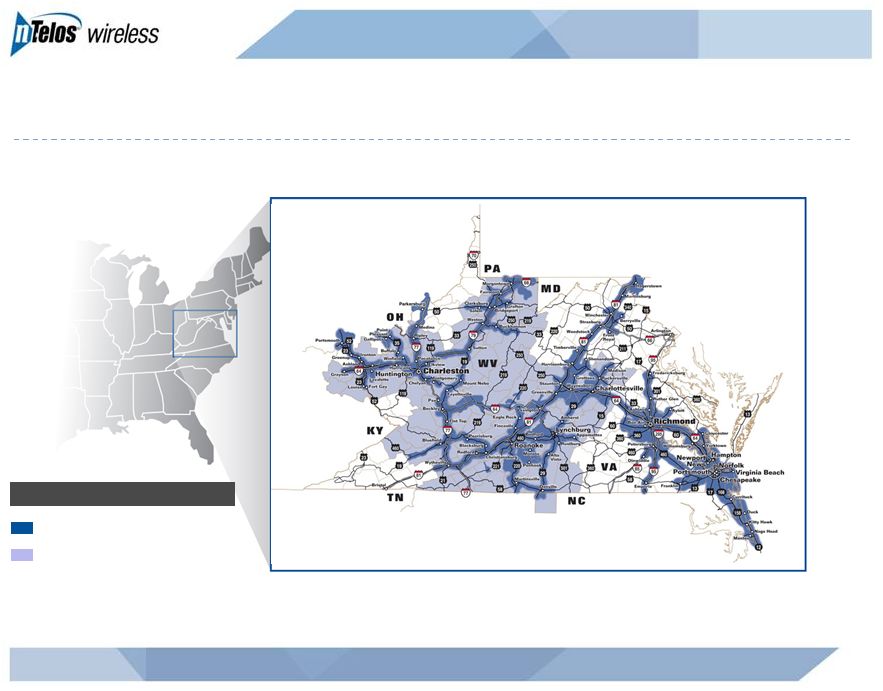

Regional Wireless Service Provider

NASDAQ: NTLS

6

Ntelos Covered Network

Sprint Wholesale Markets

STRATEGIC NETWORK ASSETS |

Carriers Without Network Assets in NTELOS’s Footprint

7

NASDAQ: NTLS

West Virginia / Virginia West

Leap³

Sprint¹

T-Mobile

US Cellular²

Virginia East

Leap³

US Cellular

¹Sprint’s retail business runs on NTELOS’s Network in West Virginia

and portions of Virginia ²US Cellular has network assets and retail

business within a portion of NTELOS’s footprint ³Pending

acquisition by AT&T |

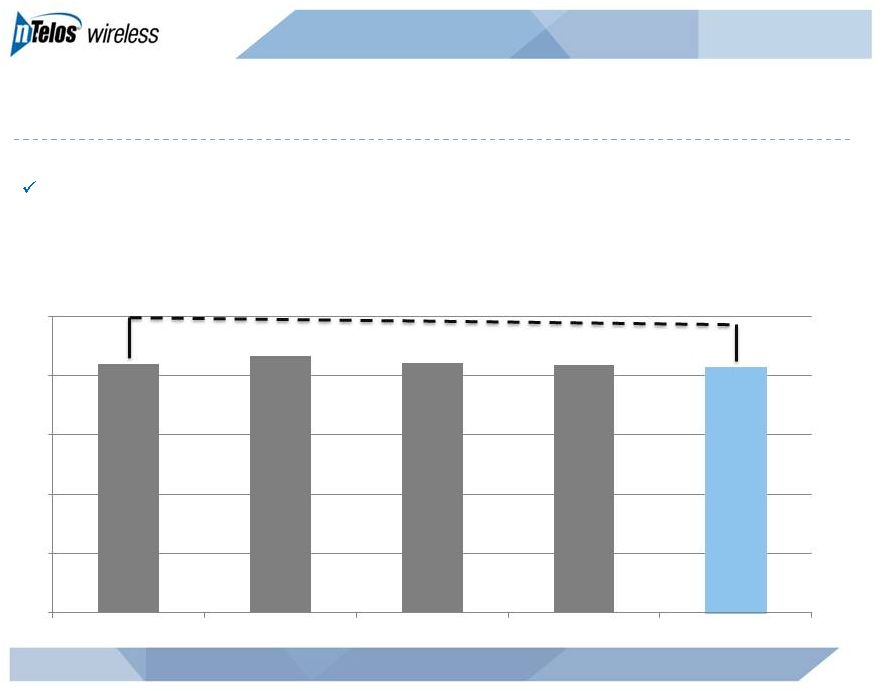

Attractive Spectrum Portfolio

8

NASDAQ: NTLS

Average Spectrum Depth in Key Markets

Source:

Map

Info:

Custom

Data,

Total

Population

–

Current

Year

and

Five

Year

USA

by

Block

Group:

United

States,

SO215245

Band

Commentary

PCS

Average depth of 23 MHz

Scarce strategic asset

AWS

Significant spectrum

holdings in contiguous

markets in western Virginia

Currently undeployed

MHZ

3,673

2,710

1,767

1,016

Licensed POPs

(000’s)

302

200

209

216

205

278

66 |

Competitively Differentiated Retail Model

SAVINGS

SIMPLICITY

SERVICE

Driving consideration for

“the best value in

wireless”

proposition

Making it “easy”

to switch

Creating “raving fans”

through superior

customer service

9

NASDAQ: NTLS

Note: Historical examples of campaigns; not to be considered current offers.

|

Closing the Device Gap on Competition

10

NASDAQ: NTLS

Q4 2009

Q4 2010

3Q 2013

LG Optimus

Plus

Motorola

Defy XT

Alcatel One

Touch Ultra

Motorola

Milestone 3

HTC One V

Samsung Galaxy S II

Samsung

Galaxy III

LG Optimus

Select

iPhone 4

iPhone 4S

iPhone 5

BlackBerry

Curve 8330

BlackBerry

Pearl Flip

8230

HTC Hero

Android

BlackBerry

Pearl

8130

HTC 6800

HTC Touch

Diamond

BlackBerry

Curve 8330

BlackBerry

Pearl Flip

8230

HTC Snap

HTC Hero

Android

BlackBerry

Tour 9630

Best

Better

Good |

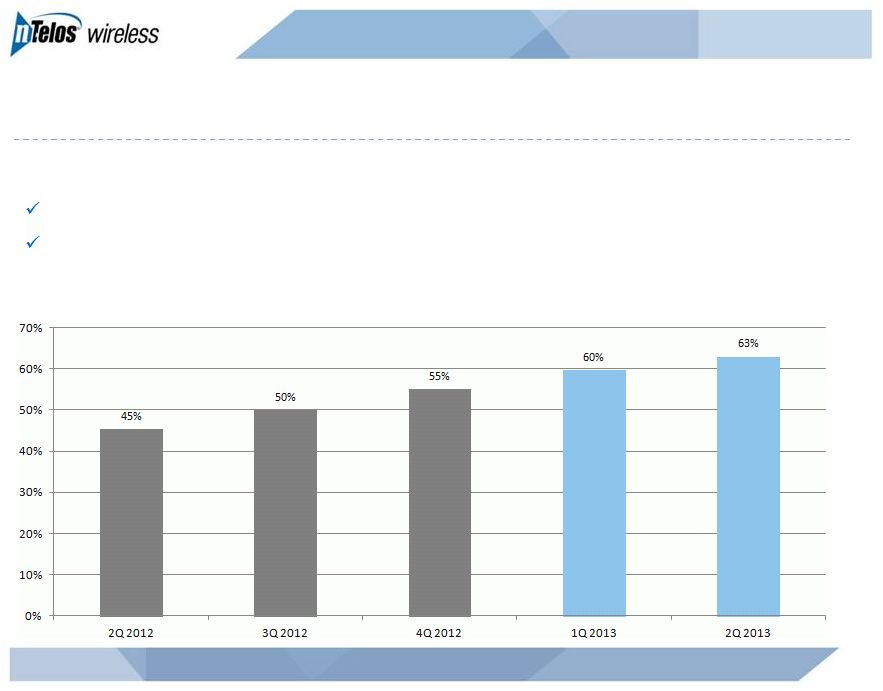

Smartphone Penetration

11

NASDAQ: NTLS

As of June 30, 2013:

66% of postpaid subscribers have a smartphone

56% of prepaid subscribers have a smartphone |

NTELOS Branding Resonating With Consumers

12

NASDAQ: NTLS

2Q11

2Q12

2Q13

Unaided

Awareness

22%

28%

26%

Unaided

Recall

18%

25%

26%

Purchase

Consideration

11%

14%

11%

Source: Independent third-party research studies.

Positive net ports

vs. all other carriers |

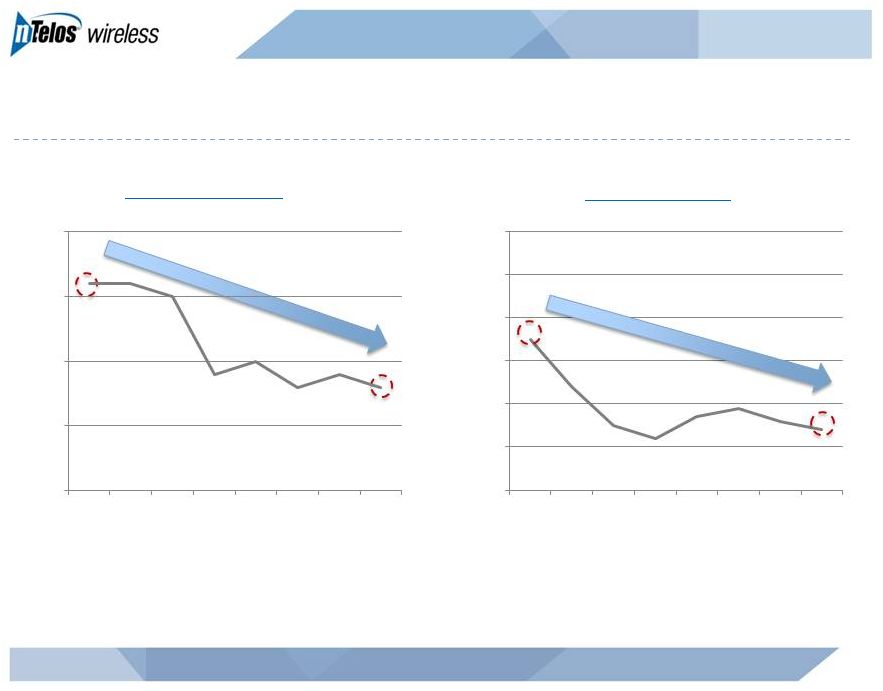

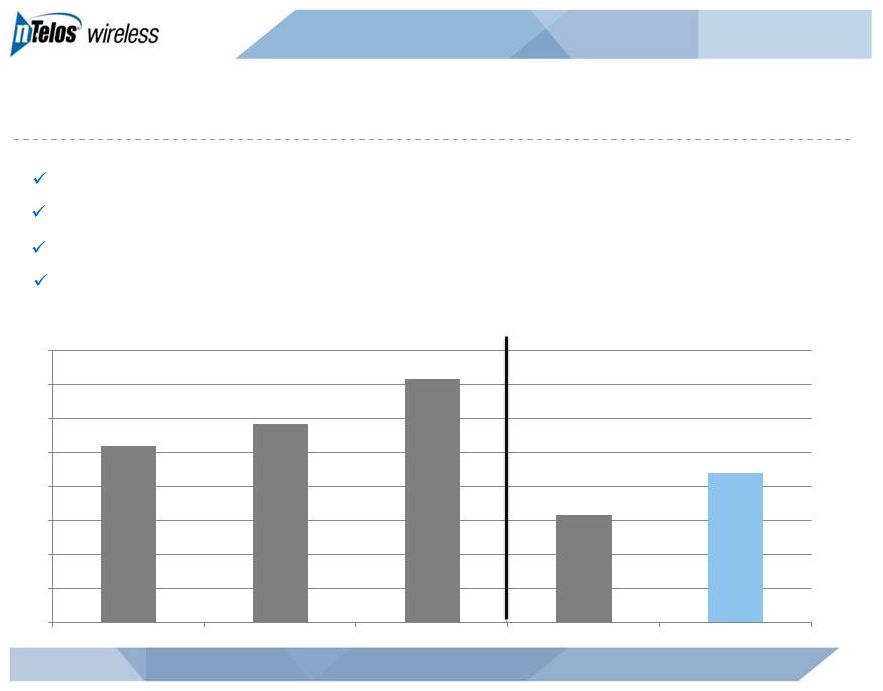

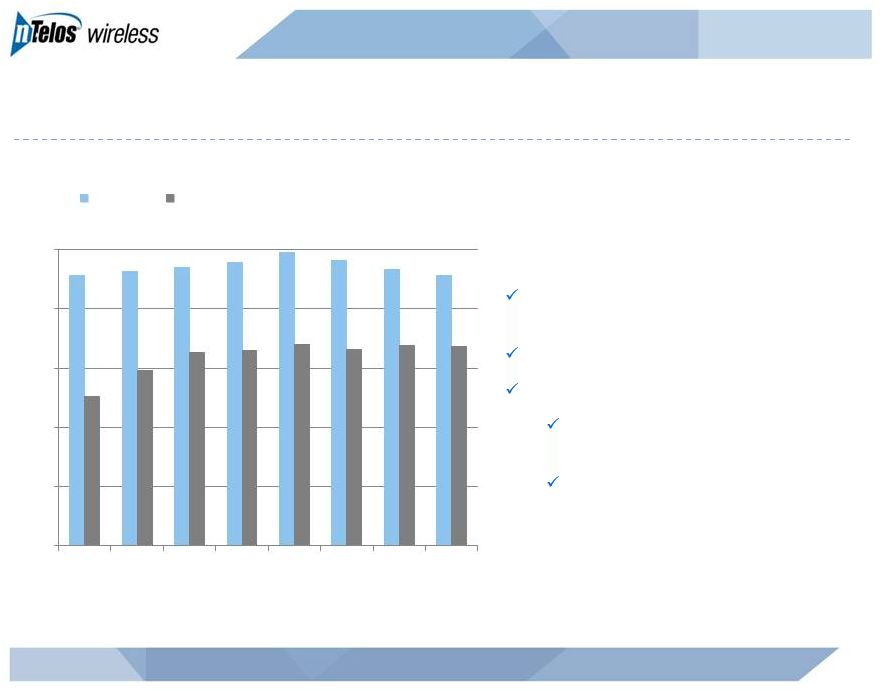

Managing Churn to Enhance Profitability

13

NASDAQ: NTLS

Prepaid Churn

Postpaid Churn

1.0%

1.5%

2.0%

2.5%

3.0%

3Q

2011

4Q

2011

1Q

2012

2Q

2012

3Q

2012

4Q

2012

1Q

2013

2Q

2013

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

3Q

2011

4Q

2011

1Q

2012

2Q

2012

3Q

2012

4Q

2012

1Q

2013

2Q

2013 |

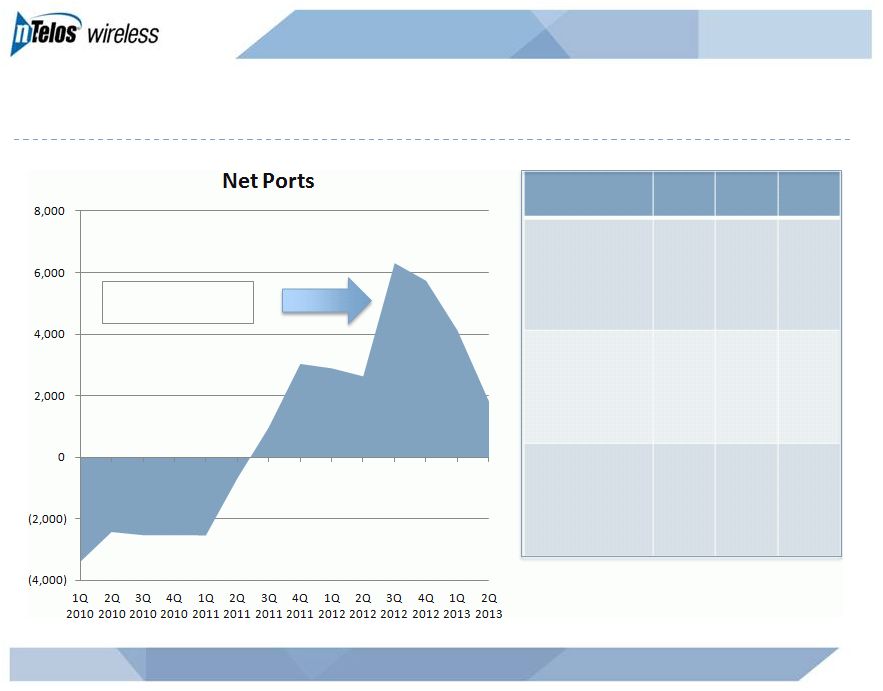

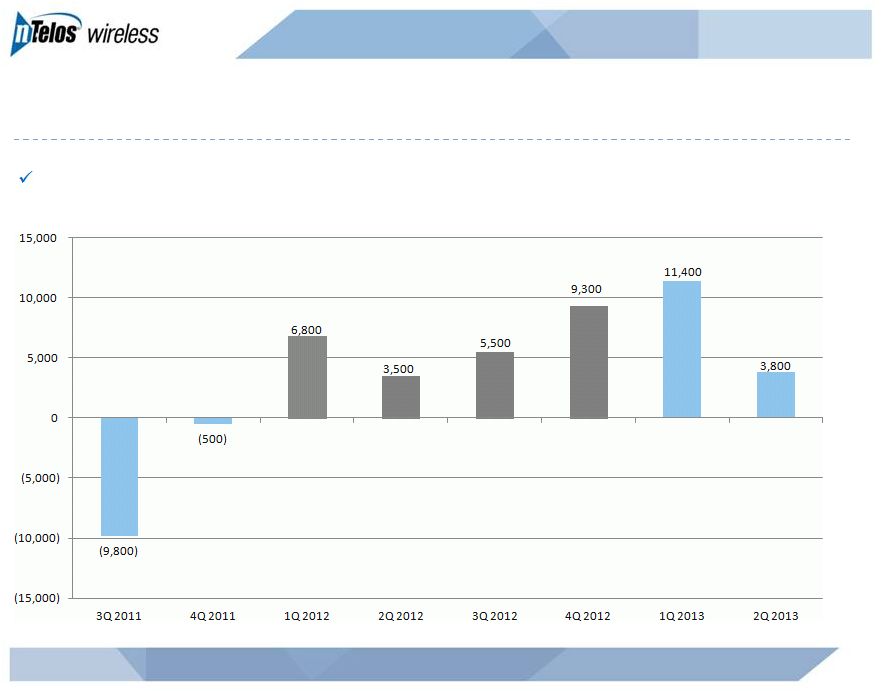

Subscribers

–

Net

Additions

Trend

14

NASDAQ: NTLS

Sixth consecutive quarter of positive net adds |

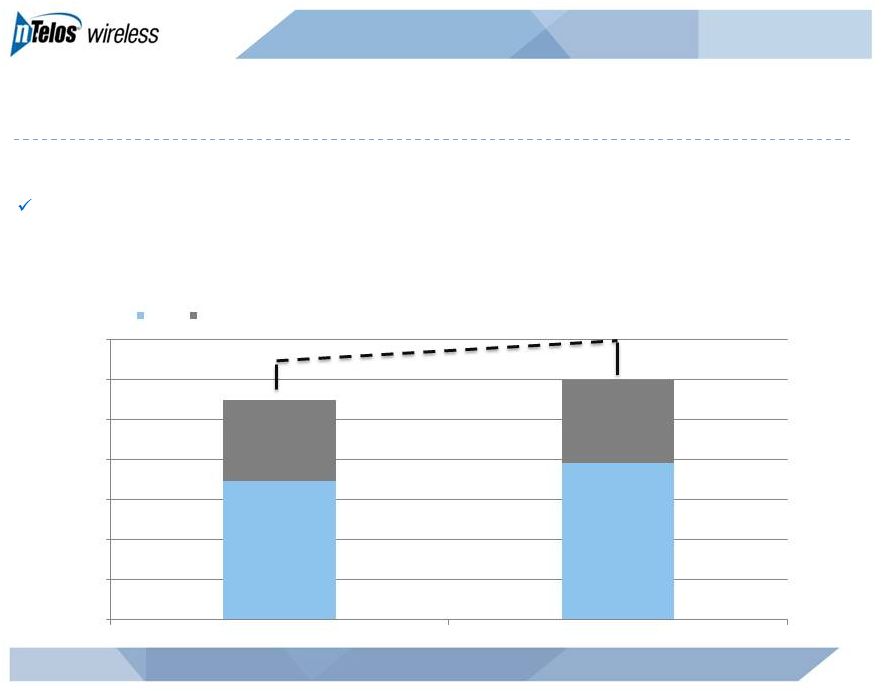

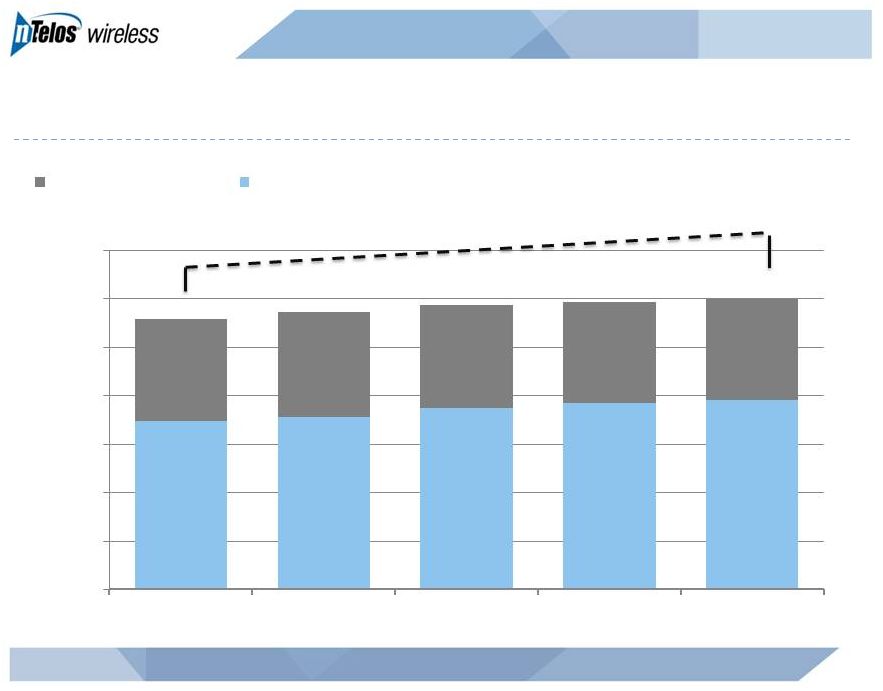

Continuing Growth in Operating Revenues

15

NASDAQ: NTLS

millions

+7%

2Q13 revenue increased 7% from 2Q12 to $119.9 million

$0.0

$20.0

$40.0

$60.0

$80.0

$100.0

$120.0

$140.0

2Q 2012

2Q 2013

Retail

Wholesale & Other |

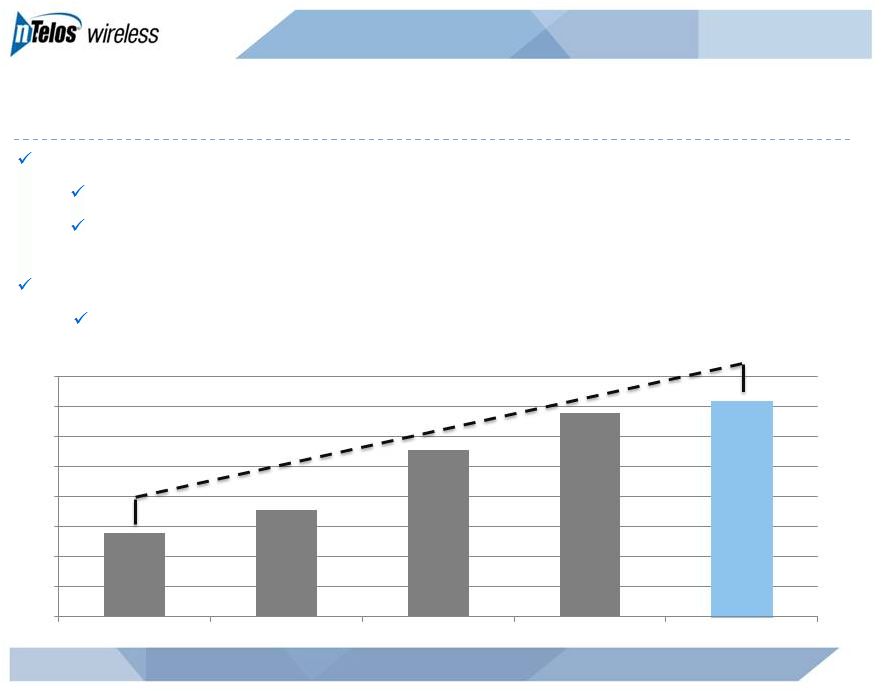

Retail Revenue Gains Continue

16

NASDAQ: NTLS

millions

Subscriber revenue growth driven by both:

ARPU growth

Subscriber growth

2Q13 retail revenue increased 1% sequentially and 13% from 2Q12 to $78.4

million Highest level in four years

+13%

$64.0

$66.0

$68.0

$70.0

$72.0

$74.0

$76.0

$78.0

$80.0

2Q 2012

3Q 2012

4Q 2012

1Q 2013

2Q 2013 |

Wholesale/Other Revenue Remains Strong

17

NASDAQ: NTLS

millions

-1%

2Q13 wholesale/other revenue decreased 1% from 2Q12 to $41.4 million

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

2Q 2012

3Q 2012

4Q 2012

1Q 2013

2Q 2013 |

Capital Investments Driving Operational Improvements

18

NASDAQ: NTLS

Expand wholesale coverage

Control roaming costs

Mitigate churn risk

1,432 3G EV-DO cell sites as of June 30, 2013

millions

$52

$58

$72

$32

$44

$0

$10

$20

$30

$40

$50

$60

$70

$80

FY 2010

FY 2011

FY 2012

1H 2012

1H 2013 |

Network Evolution

NASDAQ: NTLS

19

•

6.0mm covered POPs; 7.9 mm licensed

POPs

•

100% of covered POPs are served with 3G

EV-DO Rev. A

•

Primarily Alcatel Lucent equipment

•

1,432 cell sites deployed

•

Market level spectrum holdings ranging from

10 MHz to 50 MHz

•

PCS average depth of 23 MHz

•

AWS average depth of 20 MHz

•

Additional spectrum includes

•

Small amount of BRS

•

Opportunities for additional spectrum

and spectrum sharing being evaluated

•

Upgrade history

•

1xRTT launched in 2002

•

EV-DO Rev A launched in 2008

•

LTE Drivers

•

Serve the needs of our retail

subscribers

•

Maintain competitive position in

marketplace

•

Optimize long-term network

operating cost with new technology

•

Serve the needs of our largest

wholesale customer, Sprint

•

Deployment Plan

•

Launch first LTE markets in 2H 2013

•

Complete initial build-out by year-end

2014; 70% of covered POPs

•

Devices supporting Band Classes 2,

4 and 25

•

Estimated network CapEx of

approximately $65mm to $70mm

Current network

4G LTE upgrade plans |

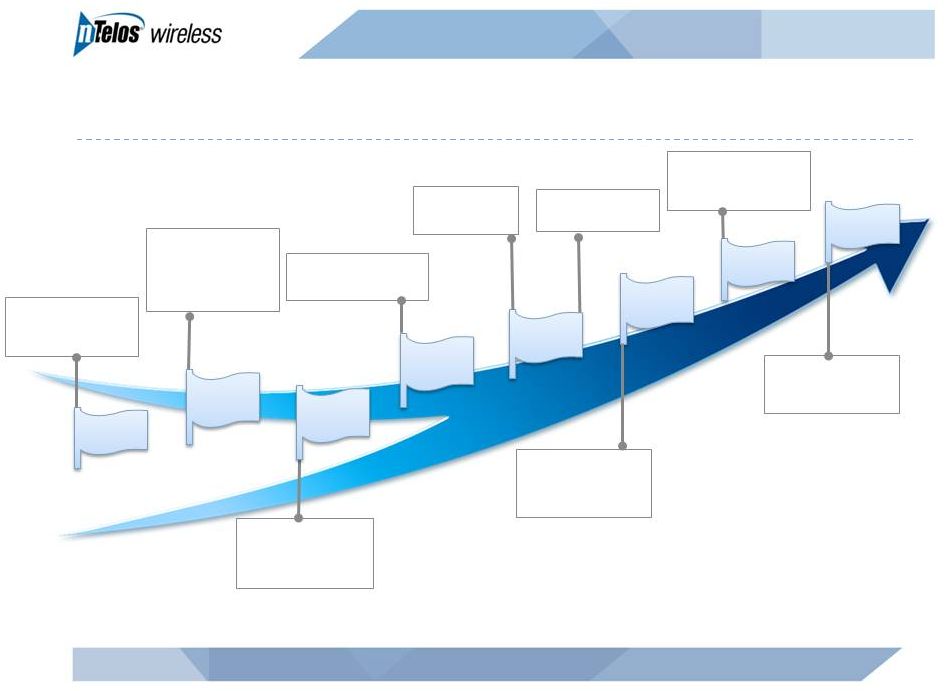

Sprint Strategic Network Alliance Evolution

20

NASDAQ: NTLS

1999

8/1999:

Agreement

with Horizon PCS

(Sprint affiliate)

10/2010:

Sprint

announces

Network Vision

2010

8/2004:

Horizon

bankruptcy; Sprint

agreement signed

8/2007:

Amends

agreement with Sprint

10/2006:

Sprint

launches EV-DO

Rev A in San Diego

2006

9/2012:

Sprint

has

19

metropolitan areas

with 4G LTE

2012

2008

3/2008:

Launch

of EV-DO

11/2008:

Completes

EV-DO build

2013

7/2013:

Sprint

has

151 metropolitan

areas with 4G LTE

2008

2004 |

Sprint Strategic Network Alliance Service

21

NASDAQ: NTLS

Exclusively provides 3G services to large number of Sprint home and travel

subscribers

Encompasses approximately

•

2.0mm covered POPs in WV and Western VA

•

823 cell sites

•

36,800 square miles

Provides ~$40mm in quarterly revenues

Sprint relationship update

•

Rate dispute previously outlined remains outstanding; ranges updated to:

•

Sprint’s favor: $12.0 million

•

nTelos’s favor: $19.0 million

•

$4.2 million unrelated dispute raised during 3Q 2012, isolated to historical

billing issues •

$18.3 million accrual recorded for the disputes, included in current

liabilities |

Sprint Strategic Network Alliance Leverages NTELOS’s Network

22

NASDAQ: NTLS

Strategic

Network

Alliance

revenues

(1)

(1)

Excludes roaming

Sprint Nextel Strategic Network Alliance

through at least July 2015

Attractive contribution to margin

Growing Usage

Significant growth in data usage

since EV-DO launched

Voice continues to grow

millions

$23

$23

$24

$24

$25

$24

$23

$23

$13

$15

$16

$17

$17

$17

$17

$17

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

3Q 2011

4Q 2011

1Q 2012

2Q 2012

3Q 2012

4Q 2012

1Q 2013

2Q 2013

Total Voice

Total Data |

Financial Summary |

Operating Revenues

24

NASDAQ: NTLS

millions

+7%

$70

$71

$75

$77

$78

$42

$43

$42

$42

$41

$112

$114

$117

$119

$120

$0

$20

$40

$60

$80

$100

$120

$140

2Q 2012

3Q 2012

4Q 2012

1Q 2013

2Q 2013

Sprint, Wholesale & Other

Retail |

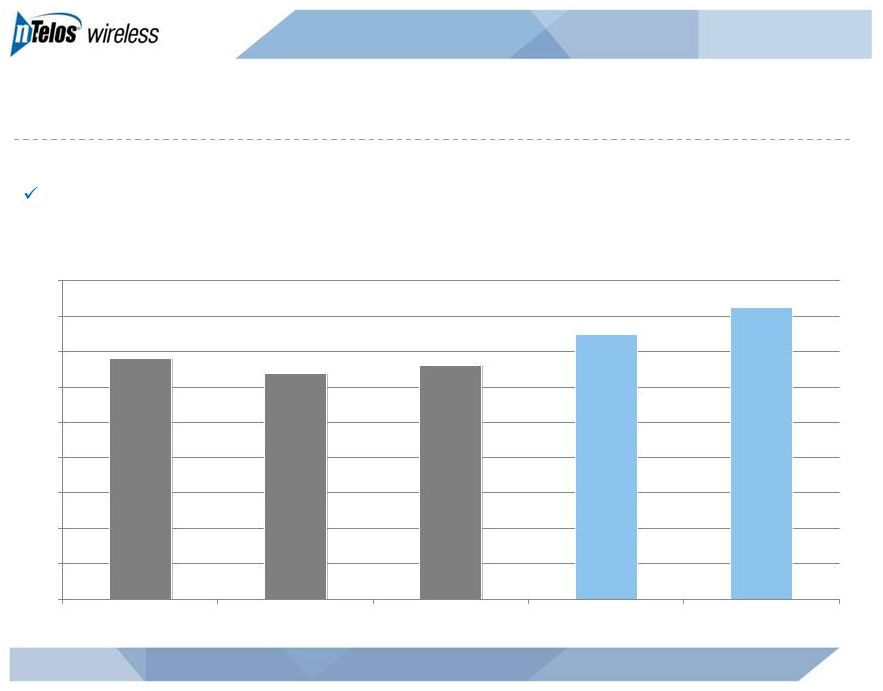

Adjusted EBITDA

25

NASDAQ: NTLS

millions

Continued investments in the business resulted in higher Adjusted EBITDA

$34

$32

$33

$37

$41

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

2Q 2012

3Q 2012

4Q 2012

1Q 2013

2Q 2013 |

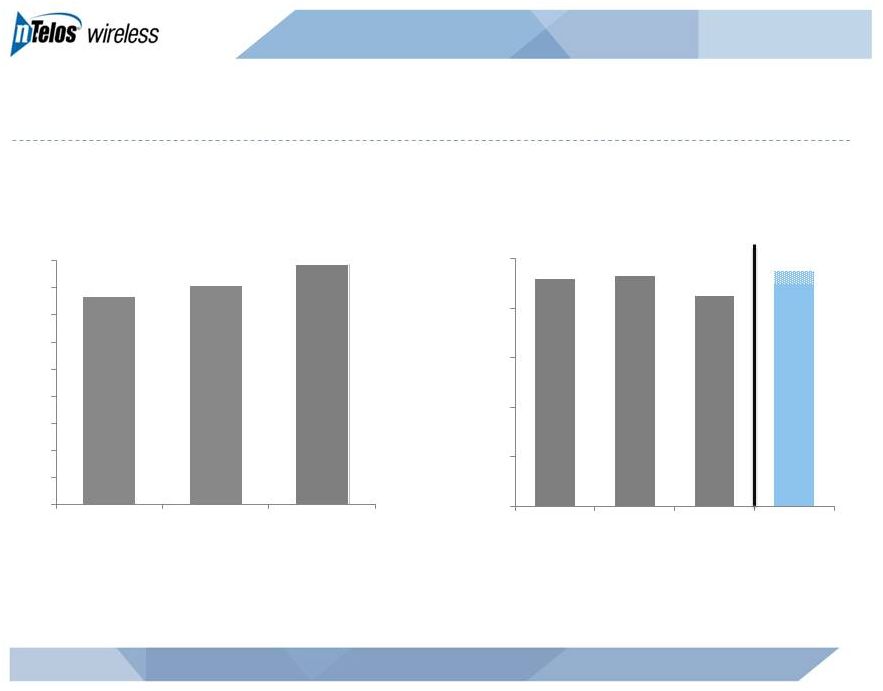

Historical Financial Performance

26

NASDAQ: NTLS

Revenue

Adjusted EBITDA

millions

millions

(1) As of July 30, 2013

$407

$423

$454

$100

$140

$180

$220

$260

$300

$340

$380

$420

$460

2010

2011

2012

$142

$143

$135

$140 -

$145

$50

$70

$90

$110

$130

$150

2010

2011

2012

2013 G (1) |

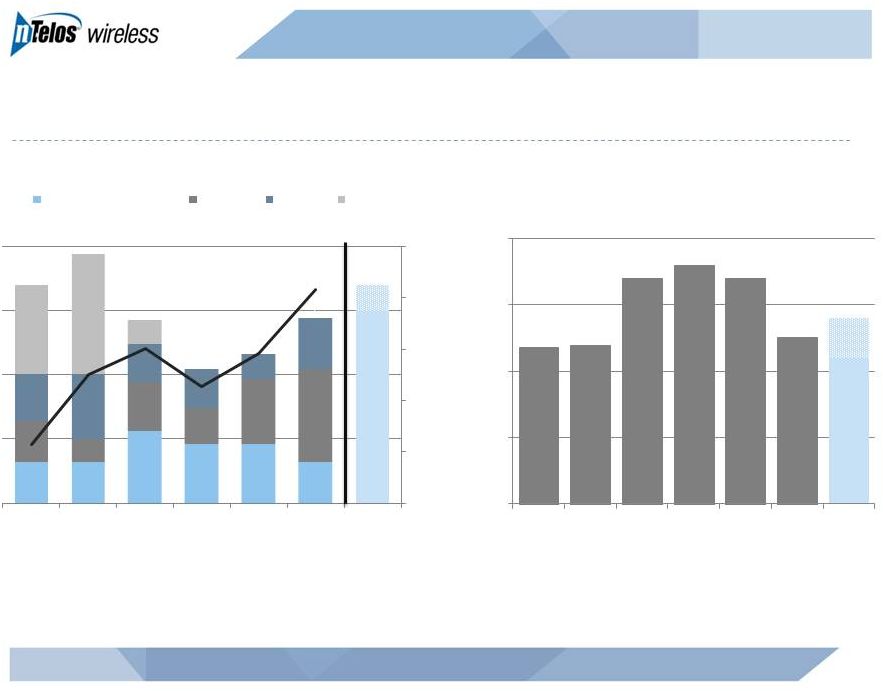

Managing Free Cash Flow with Disciplined Capital Investment

27

NASDAQ: NTLS

CapEx

millions

millions

CapEx

Free Cash Flow

(Adjusted EBITDA Less CapEx)

(1) As of July 30, 2013

Note: Excludes wireline and related capex incurred prior to business separation

Revenue

Revenue

millions

$85

$97

$71

$52

$58

$72

$75 -

$85

$350

$375

$400

$425

$450

$475

$0

$25

$50

$75

$100

2007

2008

2009

2010

2011

2012

2013 G (1)

Maintenance, IT & Other

Capacity

Growth

EV-DO

$55 -

$70

$59

$60

$85

$90

$85

$63

$0

$25

$50

$75

$100

2007

2008

2009

2010

2011

2012

2013 G (1) |

Capitalization Overview

($ in millions)

June 30, 2013

Cash

$98.2

Total Debt

$492.5

Net Debt

$394.3

LTM Adjusted EBITDA

$143.5

Secured Term Loan

$491.5

Net Debt Leverage

2.7x

NASDAQ: NTLS

28 |

Guidance (as of July 30, 2013)

NASDAQ: NTLS

29

FY

2013

Adjusted

EBITDA

of

$140

million

-

$145

million

FY

2013

CapEx

of

$75

million

-

$85

million

2013 net adds expected to be at or about 2012 net adds

|

Senior Executives—Wireless Veterans

JIM HYDE

CEO, President and Director

STEB CHANDOR

EVP, CFO and Treasurer

CONRAD HUNTER

EVP, COO

Former CEO, T-Mobile UK

Former T-Mobile USA /

Western Wireless /

VoiceStream Sr. Exec

18 years industry experience

Former CFO, iPCS Wireless

Former CFO, Metro One

Telecommunications

17 years industry experience

Former COO, iPCS Wireless

Former VP of Midwest

Operations, U.S. Cellular

Corporation

33 years industry experience

30

NASDAQ: NTLS

ROBERT McAVOY

EVP, CTO

Former Market General

Manager, PrimeCo

Began career at Bell Atlantic

25 years industry experience |

Summary

Leading “pure-play”

regional wireless company

31

Strategic asset set

Strong free cash flow

Broad geographic and network technology footprint

Experienced management team

NASDAQ: NTLS

Competitive and diversified business model |

Appendix |

33

NASDAQ: NTLS

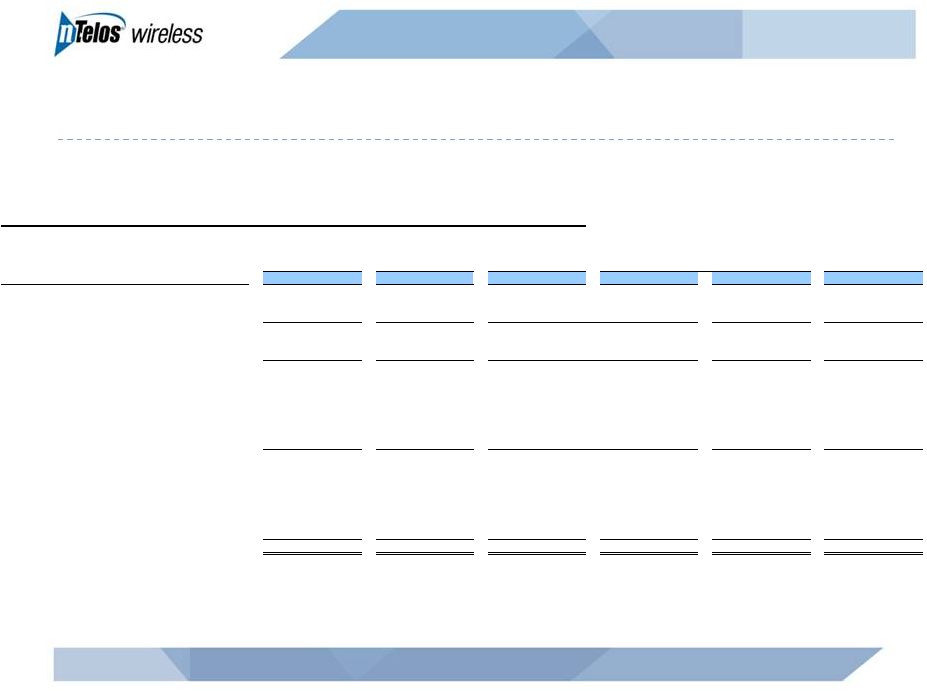

NTELOS Holdings Corp.

Reconciliation of Net Income Attributable to NTELOS Holdings Corp. to Adjusted EBITDA

Year Ended:

(In thousands)

2012

2011

2010

2009

2008

2007

Net Income Attributable to NTELOS Holdings Corp.

18,387

$

(23,715)

$

44,808

$

63,285

$

44,829

$

32,453

$

Net income attributable to noncontrolling interests

1,941

(1,769)

(1,417)

(851)

Net Income

20,328

(21,946)

46,225

64,136

44,829

32,453

Discontinued operations, net

-

(45,386)

16,882

18,054

16,002

12,638

Income from continuing operations

20,328

23,440

29,343

46,082

28,827

19,815

Interest expense

22,944

23,380

24,728

15,922

17,024

24,520

Loss (gain) on derivatives

-

264

147

(2,100)

9,531

3,527

Income taxes

12,676

16,363

20,251

26,526

20,787

17,161

Corporate financing fees

-

1,567

Other expense (income), net

7,194

1,240

413

971

1,402

2,953

Operating income

63,142

66,254

74,882

87,401

77,571

67,976

Depreciation and amortization

63,258

63,083

58,016

63,015

75,982

70,102

Accretion of asset retirement obligations

637

658

770

695

914

746

Equity-based compensation

6,029

6,072

5,270

3,227

2,729

4,328

Acquisition related charges

-

-

2,815

1,477

570

Business separation charges

1,660

6,997

352

Adjusted EBITDA

134,726

$

143,064

$

142,105

$

155,815

$

157,196

$

143,721

$

1

Charges

for

legal

and

consulting

services

costs

in

connection

with

the

separation

of

the

wireless

and

wireline

operations.

1 |

34

NASDAQ: NTLS

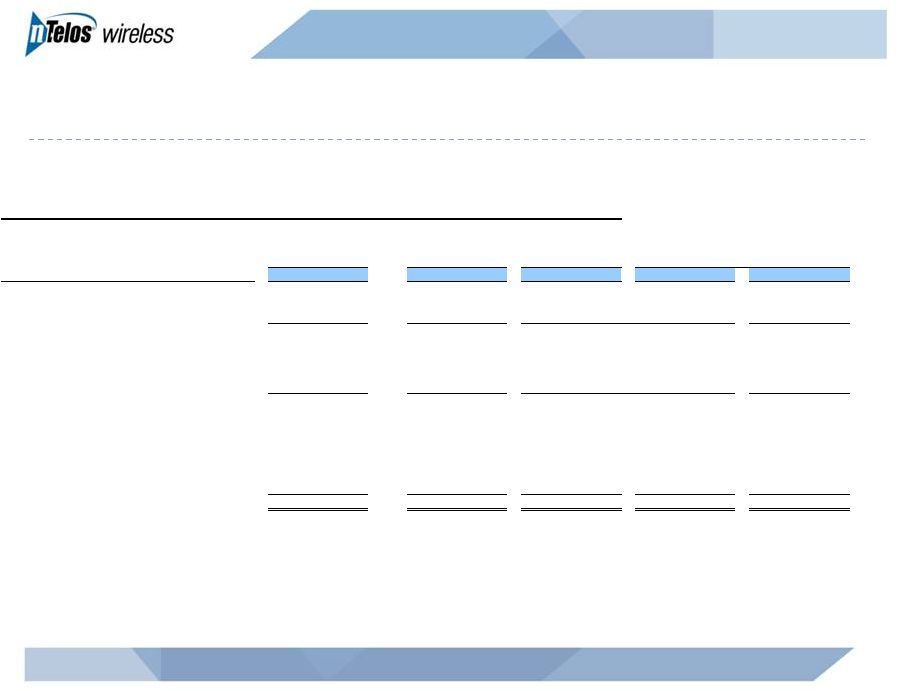

NTELOS Holdings Corp.

Reconciliation of Net Income Attributable to NTELOS Holdings Corp. to Adjusted EBITDA

(In thousands)

2Q13

1Q13

4Q12

3Q12

2Q12

Net Income Attributable to NTELOS Holdings Corp.

9,386

$

5,493

$

321

$

4,608

$

5,606

$

Net income attributable to noncontrolling interests

541

529

443

488

881

Net Income

9,927

6,022

764

5,096

6,487

Interest expense

7,398

7,361

6,651

5,432

5,433

Income taxes

6,380

3,744

(454)

3,141

4,609

Other expense (income), net

(151)

369

7,038

50

44

Operating income

23,554

17,496

13,999

13,719

16,573

Depreciation and amortization

20,443

18,456

17,440

15,810

15,101

Gain on sale of intangible assets

(4,442)

-

-

-

-

Accretion of asset retirement obligations

173

143

174

163

151

Equity-based compensation

1,460

1,321

1,346

1,478

1,536

Business separation charges

-

-

56

684

635

Adjusted EBITDA

41,188

$

37,416

$

33,015

$

31,854

$

33,996

$

1

Charges for legal and consulting services costs in connection with the separation

of the wireless and wireline operations. 1 |

35

NASDAQ: NTLS

NTELOS Holdings Corp.

ARPU Reconciliation

Average Monthly Revenue per User (ARPU)

1

2Q13

1Q13

4Q12

3Q12

2Q12

FY 2012

FY 2011

(In thousands, except for subscribers and ARPU)

Operating Revenues

119,859

$

119,345

$

117,398

$

114,466

$

111,585

$

453,989

$

422,629

$

Less: Equipment revenue from sales to new customers

(3,104)

(3,521)

(3,808)

(3,333)

(4,026)

(15,041)

(9,091)

Less: Equipment revenue from sales to existing customers

(2,395)

(3,117)

(3,315)

(3,416)

(3,903)

(15,037)

(17,793)

Less: Wholesale, other and adjustments

(41,179)

(40,918)

(41,488)

(42,380)

(41,061)

(165,765)

(143,477)

Gross subscriber revenue

73,181

71,789

68,787

65,337

62,595

258,146

252,268

Less: prepay subscriber revenue

(15,879)

(15,205)

(14,823)

(14,103)

(14,001)

(56,330)

(48,758)

Less: adjustments to prepay subscriber revenue

(303)

(479)

(237)

(434)

(382)

(1,706)

(1,175)

Gross postpay subscriber revenue

56,999

$

56,105

$

53,727

$

50,800

$

48,212

$

200,110

$

202,335

$

Prepay subscriber revenue

15,879

15,205

14,823

14,103

14,001

56,330

48,758

Plus: adjustments to prepay subscriber revenue

303

479

237

434

382

1,706

1,175

Gross prepay subscriber revenue

16,182

$

15,684

$

15,060

$

14,537

$

14,383

$

58,036

$

49,933

$

Average number of subscribers

453,262

444,244

434,457

427,610

422,247

425,377

422,256

Total ARPU

53.82

$

53.87

$

52.78

$

50.93

$

49.41

$

50.57

$

49.79

$

Average number of postpay subscribers

299,304

298,414

292,668

287,165

284,834

288,428

298,992

Postpay ARPU

63.48

$

62.67

$

61.19

$

58.97

$

56.42

$

57.82

$

56.39

$

Average number of prepay subscribers

153,958

145,831

141,789

140,446

137,413

136,949

123,264

Prepay ARPU

35.04

$

35.85

$

35.41

$

34.50

$

34.89

$

35.31

$

33.76

$

Gross subscriber revenue

73,181

71,789

68,787

65,337

62,595

258,146

252,268

Less: voice and other feature revenue

(43,078)

(42,658)

(41,379)

(39,366)

(37,708)

(156,032)

(171,882)

Data revenue

30,103

$

29,131

$

27,408

$

25,971

$

24,887

$

102,114

$

80,386

$

Average number of subscribers

453,262

444,244

434,457

427,610

422,247

425,377

422,256

Total Data ARPU

22.14

$

21.86

$

21.03

$

20.25

$

19.65

$

20.00

$

15.86

$

Gross postpay subscriber revenue

56,999

56,105

53,727

50,800

48,212

200,110

202,335

Less: postpay voice and other feature revenue

(36,170)

(35,952)

(34,651)

(33,028)

(31,490)

(130,601)

(144,114)

Postpay data revenue

20,829

$

20,153

$

19,076

$

17,772

$

16,722

$

69,509

$

58,221

$

Gross prepay subscriber revenue

16,182

15,684

15,060

14,537

14,383

58,036

49,933

Less: prepay voice and other feature revenue

(6,908)

(6,706)

(6,728)

(6,338)

(6,218)

(25,431)

(27,768)

Prepay data revenue

9,274

$

8,978

$

8,332

$

8,199

$

8,165

$

32,605

$

22,165

$

Average number of postpay subscribers

299,304

298,414

292,668

287,165

284,834

288,428

298,992

Postpay data ARPU

23.20

$

22.51

$

21.73

$

20.63

$

19.57

$

20.08

$

16.23

$

Average number of prepay subscribers

153,958

145,831

141,789

140,445

137,413

136,949

123,264

Prepay data ARPU

20.08

$

20.52

$

19.59

$

19.46

$

19.81

$

19.84

$

14.99

$

1

Average monthly revenue per user (ARPU) is computed by dividing service revenues per period by the

average number of subscribers during that period. ARPU as defined may not be similar to ARPU measures of other companies, is

not a measurement under GAAP and should be considered in addition to, but not as a substitute for, the

information contained in the Company’s consolidated statements of operations. The Company closely monitors the effects of new

rate plans and service offerings on ARPU in order to determine their effectiveness. ARPU provides

management useful information concerning the appeal of NTELOS rate plans and service offerings and the Company’s performance in

attracting and retaining high-value customers. |