Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - People's United Financial, Inc. | d595120d8k.htm |

Investor Contact:

Peter Goulding, CFA

203-338-6799

peter.goulding@peoples.com

Barclays Global Financial Services Conference

September 10, 2013

Exhibit 99.1 |

1

Forward-Looking Statement

Certain statements contained in this release are forward-looking in nature. These include all

statements about People's United Financial's plans, objectives, expectations and other

statements that are not historical facts, and usually use words such as "expect,"

"anticipate," "believe," "should" and similar expressions. Such

statements represent management's current beliefs, based upon information available at the time

the statements are made, with regard to the matters addressed. All forward-looking

statements are subject to risks and uncertainties that could cause People's United Financial's actual

results or financial condition to differ materially from those expressed in or implied by such

statements. Factors of particular importance to People’s United Financial include, but are

not limited to: (1) changes in general, national or regional economic conditions; (2) changes

in interest rates; (3) changes in loan default and charge-off rates; (4) changes in deposit

levels; (5) changes in levels of income and expense in non-interest income and expense

related activities; (6) residential mortgage and secondary market activity; (7) changes in

accounting and regulatory guidance applicable to banks; (8) price levels and conditions in the

public securities markets generally; (9) competition and its effect on pricing, spending,

third-party relationships and revenues; (10) the successful integration of acquisitions; and (11)

changes in regulation resulting from or relating to financial reform legislation. People's

United Financial does not undertake any obligation to update or revise any forward-looking

statements, whether as a result of new information, future events or otherwise.

|

2

Corporate Overview

Snapshot as of June 30, 2013

People’s United Financial, Inc.

NASDAQ (PBCT)

Headquarters:

Bridgeport, CT

Chief Executive Officer:

Jack Barnes

Chief Financial Officer:

Kirk Walters

Market Capitalization (9/6/13):

$4.6 billion

Assets:

$31.3 billion

Loans:

$22.9 billion

Deposits:

$22.0 billion

Branches:

418

ATMs:

638

Standalone ATMs:*

109

Founded:

1842

* Includes 25 ATMs in Stop & Shop locations where a branch is not

present |

3

Fortified Foundation for Growth

Our Relationship Based World |

Retail & Business

Banking Franchise Distribution

400+ branches over 6 states

•

~33% of branches are in-store

600+ ATMs

Online & mobile banking

Call center operations located in Bridgeport,

CT and Burlington, VT

Scale

5

th

in deposit market share in New England *

Customer base

Approximately 800,000 commercial, business

banking and consumer relationships

* Source: SNL Financial

4 |

5

Deepening Market Presence

Connecticut

Massachusetts

Vermont

New York

New Hampshire

Maine

Source: SNL Financial

Branches

$BN

%

1

B of A

151

24.4

24.0

2

Webster

123

12.0

11.8

3

People's United

165

10.9

10.8

4

Wells Fargo

76

7.3

7.2

5

TD Bank

81

5.9

5.8

6

First Niagara

85

4.6

4.5

7

JPM Chase

53

4.5

4.4

8

Citi

20

3.0

2.9

9

Liberty

48

2.9

2.8

10

RBS

47

2.5

2.5

Branches

$BN

%

1

B of A

255

54.3

20.0

2

RBS

253

30.9

11.4

3

Santander

229

18.9

7.0

4

TD Bank

157

10.6

3.9

5

Eastern Bank

98

6.7

2.5

6

Independent Bank

85

4.7

1.7

7

Middlesex

31

3.5

1.3

8

People's United

56

3.2

1.2

9

Boston Private

11

2.9

1.1

10

Brookline

29

2.4

0.9

Branches

$BN

%

1

People's United

42

2.6

22.4

2

TD Bank

34

2.6

22.0

3

Merchants

33

1.2

10.6

4

RBS

21

0.9

7.3

5

KeyCorp

13

0.8

6.7

6

Northfield

13

0.5

4.3

7

Community

14

0.4

3.7

8

Union

13

0.4

3.4

9

Berkshire Hills

7

0.3

2.9

10

Passumpsic

7

0.3

2.8

Branches

$BN

%

1

JPM Chase

802

392.9

37.1

2

Citi

269

69.6

6.6

3

B of A

352

60.1

5.7

4

HSBC

162

57.0

5.4

5

Capital One

274

38.8

3.7

6

M&T

298

33.3

3.1

7

TD Bank

228

22.4

2.1

8

KeyCorp

260

18.2

1.7

9

Wells Fargo

86

17.9

1.7

10

First Niagara

209

16.1

1.5

35

People's United

98

2.5

0.2

Branches

$BN

%

1

RBS

80

6.8

24.4

2

TD Bank

72

5.4

19.3

3

B of A

28

4.8

17.4

4

People's United

29

1.4

4.9

5

NH Mutual

18

1.0

3.7

6

BNH

23

0.9

3.2

7

Santander

20

0.8

2.9

8

NH Thrift

20

0.8

2.8

9

Northway

18

0.7

2.4

10

Centrix

6

0.7

2.3

Branches

$BN

%

1

TD Bank

56

14.4

43.3

2

KeyCorp

59

2.6

7.9

3

Bangor Bancorp

60

2.0

6.1

4

Camden National

44

1.8

5.3

5

B of A

19

1.4

4.1

6

First Bancorp

16

1.0

3.1

7

Machias

14

0.8

2.4

8

People's United

28

0.8

2.4

9

Bar Harbor

16

0.8

2.3

10

Norway

22

0.7

2.2

Leading market position in the best commercial banking market in the US

#1 in Fairfield County, CT, 65 branches, $6.1BN, 18.4% deposit market share |

6

Strategic Vision Outlined in mid-2010

Optimize the Existing Business

Continue to grow high quality, in-footprint, relationship-based C&I,

commercial real estate, home equity and select residential loans

Maintain conservative underwriting standards and focus on asset quality

Compete on service and relationships and maintain pricing discipline

Yield

enhancing

decisions

in

securities

portfolio

without

credit

risk

or

significant

duration risk

Further leverage our brand

Deepen our presence in metro New York and greater Boston markets

Continue to upgrade our products and services

Build out our small business lending capabilities

Continue to deepen wealth management and insurance relationships

Improved infrastructure facilitates future growth

Core systems conversion complete

Our objective is to reach 55% efficiency ratio and 1.25% ROAA over the longer

term |

7

Substantial Progress Since 1Q 2010

Continued to build on our premium brand

Significant

growth

runway

within

existing

markets

–

expanding

in

two

of

the

largest MSAs in the US (New York City, #1, Boston, #10)

Attracted senior level talent to augment an already strong leadership team

Significantly enhanced corporate governance and risk capabilities

Maintained

superior

asset

quality

with

NCOs

/

Average

Loans

of

26bps

Lowered

the

efficiency

ratio

from

76.1%

in

1Q

2010

to

62.7%

in

2Q

2013

Grew

operating

earnings

per

share

at

a

30%

compound

annual

growth

rate

Operating

ROAA

has

increased

35%

from

60bps

in

1Q

2010

to

81bps

in

2Q

2013

Operating

ROATE

has

increased

610bps

from

3.2%

in

1Q

2010

to

9.3%

in

2Q

2013

Returned

over

$1.7BN

of

capital

to

shareholders

through

dividends

and

share

repurchases –

over 35% of our current market capitalization |

8

Growing loans and deposits organically

Continue to grow in existing markets

We have an outstanding brand to leverage in under-represented large markets

Lower deposit costs

Improve DDA mix, commercial mix

Lower deposit costs on acquired deposits

Strengthen fee income

Continue to tightly managed expense levels

Operating Leverage

Grow Revenue While Reducing Expenses |

9

Consistent Loan Growth

Since the end of 2010, People’s United is one of only six banks within the top 50 by

assets that have grown loans in each quarter

Source:

SNL Financial. Excludes trust banks. Statements based on Total Gross Loans and Finance Leases, as

reported, net of unearned discounts and gross of loss reserves. Does not include accrued

interest on loans Notes:

Includes People’s United, First Niagara, First Republic, Signature, UMB and Prosperity

Reflects completion of Danvers Bancorp acquisition in 2Q 2011

Quarterly Loan Growth Since 1Q 2011

PBCT Median = 1.67%

Top 50 Median = 1.09%

¹

1

2 |

10

Revenue Opportunities

Continue to deepen our presence in heritage markets such as Connecticut and

Vermont

Substantial growth prospects in larger markets such as New York metro and greater

Boston

Total New York 1H 2013 loan originations run-rate ~$2.0BN

•

Increased New York commercial relationship managers to 18 from zero since 1Q

2010 •

Significant branch expansion in New York with 98 branches up from 5 in 1Q 2010; 58

branches, or 59%, are in- store locations

Total Massachusetts 1H 2013 loan originations run-rate ~$660MM

•

Increased Massachusetts commercial relationship managers to 33 from 14 since 1Q

2010 •

Solid branch foundation in Massachusetts with 56 branches up from 19 in 1Q

2010 •

Currently 3 de novo branches with over $40MM deposits: Prudential Center in Boston

(opened November 2010); Milk Street in Boston (opened December 2010);

Lexington, MA (opened July 2011) |

11

Under-represented asset classes ramping up

Recently hired senior professionals to lead large corporate and government banking

businesses New York Commercial

Real

Estate

gaining

traction

as

evidenced

by

strong

growth

Increased Private Banking activity with initial focus on CT, metro New York and

greater Boston Significant progress within asset-based and mortgage

warehouse lending teams Enhancing wealth management offering

Proprietary asset allocation and risk management strategies are implemented both

internally and with a suite of external managers who represent our "best

in class" recommendations •

UMA

technology

allows

us

to

“rent”

intellectual

capital

–

no

customer

funds

leave

the

bank

Increasing momentum in other fee income businesses with a focus on

cross-sell Commercial

insurance:

revamped

systems

and

combined

all

agencies

into

a

single

entity

Delivering interest rate swaps and foreign exchange products to existing corporate

customers Expanding international trade finance with the recent hire of a

senior executive Growing cash management, merchant and payroll services

Revenue Opportunities

Multiple Levers for Growth |

12

Average Deposits Per Branch ($MM)

Southern New York Branch Update

One Year Performance Review

Deposits as of 6/30/13 totaled $591 million, up $269 million or 84% since close

Branches provide significant support to our commercial and retail banking efforts

Strengthened brand awareness in the New York market is also accelerating the

expansion of fee income businesses

“Break-even”

Originally

Forecast to

Occur at

6/30/14

The acquired Southern New York branches have surpassed expectations

Acquired NY In-store

Branches at 6/25/12

Acquired NY In-store

Branches at 6/30/13

PBCT CT In-store

Branches at 6/30/13

Note: Represents an activity-based approach versus a branch of origination approach as reported

by the FDIC |

13

Connecticut In-store Versus Traditional Branch Business (Last Twelve Months

Through 6/30/13) In-store Versus Traditional Branches

Connecticut

On average, in-store locations are open 37% more hours per week than traditional

branches (56 hours vs. 41 hours) but are 30% less expensive to operate

Partnership allows us to leverage our brand with the ~1.8 million shoppers who

visit Connecticut Stop & Shop stores every week

In-store locations operate under the same business model as traditional branches

and sell all the Bank’s products and services

Mortgages, Home Equity Loans, Business Loans and Investments*

Connecticut in-store branches accounted for a significant portion of the new

branch business booked in the market

Consumer

Checking Accounts

Opened

Savings Accounts

Opened

Business Checking

Accounts Opened

Home Equity Loan

Originations

Mortgage Loan

Originations

Business Banking

Loan Originations

Investment Sales

In-store Branches

Traditional Branches

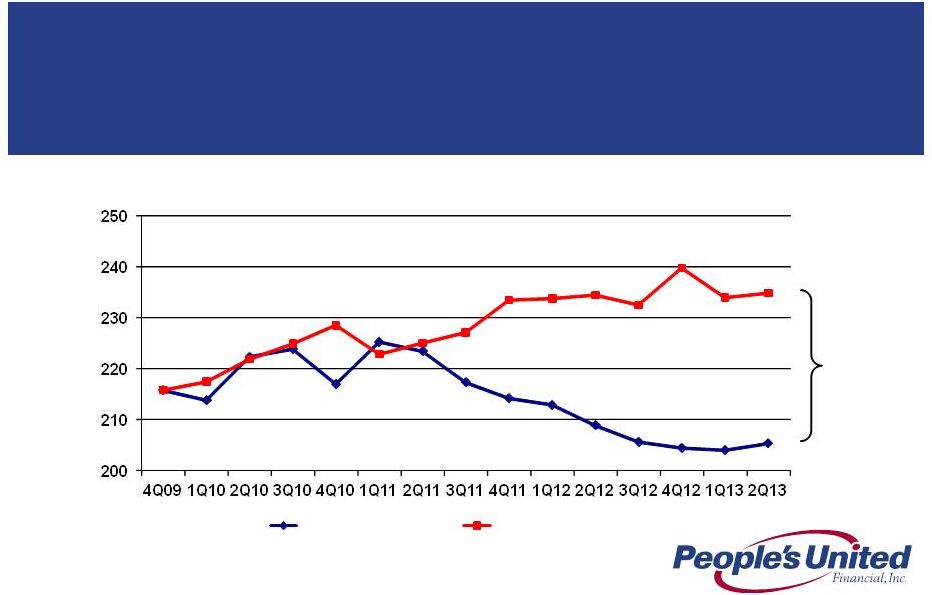

* Sold by employees who are also licensed representatives of our brokerage affiliate |

14

Expense Progress

Estimated Cost Savings Analysis

Source: SNL Financial

Note:

“Pro

Forma

/

Actual”

represents

PBCT

operating

noninterest

expense

and

the

actual

expenses

at

the

acquired

institutions.

Acquisition target costs fall away as the acquisitions are completed.

“Without

Expense

Initiatives”

represents

PBCT

operating

noninterest

expense

and

the

actual

expenses

at

the

acquired

institutions in 4Q09, and then applies the peer median expense growth rate in each subsequent

quarter Cost savings overlooked: the ~$30MM in additional annual expenses from the acquired

Southern New York branches has been partially offset by ~$16MM of annual cost

reduction initiatives on a year-over-year basis

As of 2Q 2013 we have eliminated ~$118MM of annual expenses, or 13% of the annual

cost base without expense initiatives

205

235

Operating Noninterest Expense ($MM)

Pro Forma / Actual

Without Expense Initiatives

.

$30MM

Cost

Savings |

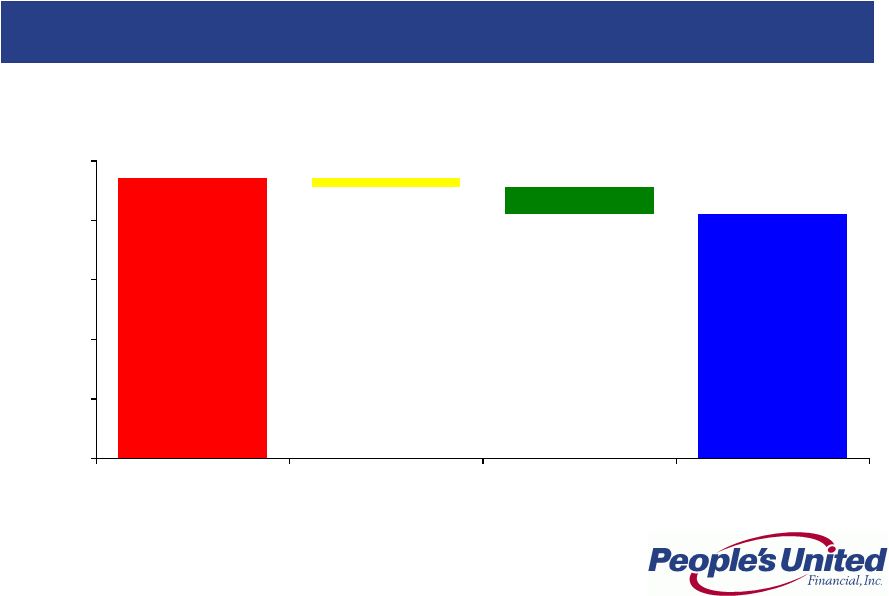

15

Expense Progress

Estimated Cost Savings Analysis

The $30MM in quarterly cost reductions is attributable to efforts related to

acquisition cost savings and other initiatives

Source: SNL Financial

Note:

“Pro

Forma

/

Actual”

represents

PBCT

operating

noninterest

expense

and

the

actual

expenses

at

the

acquired

institutions.

Acquisition target costs fall away as the acquisitions are completed.

“Without

Expense

Initiatives”

represents

PBCT

operating

noninterest

expense

and

the

actual

expenses

at

the

acquired

institutions in 4Q09, and then applies the peer median expense growth rate in each subsequent

quarter 235

205

7

23

$0

$50

$100

$150

$200

$250

Without Expense

Initiatives

Announced Acquisition

Savings

Other Initiatives

Pro Forma / Actual

Operating Noninterest Expense ($MM) |

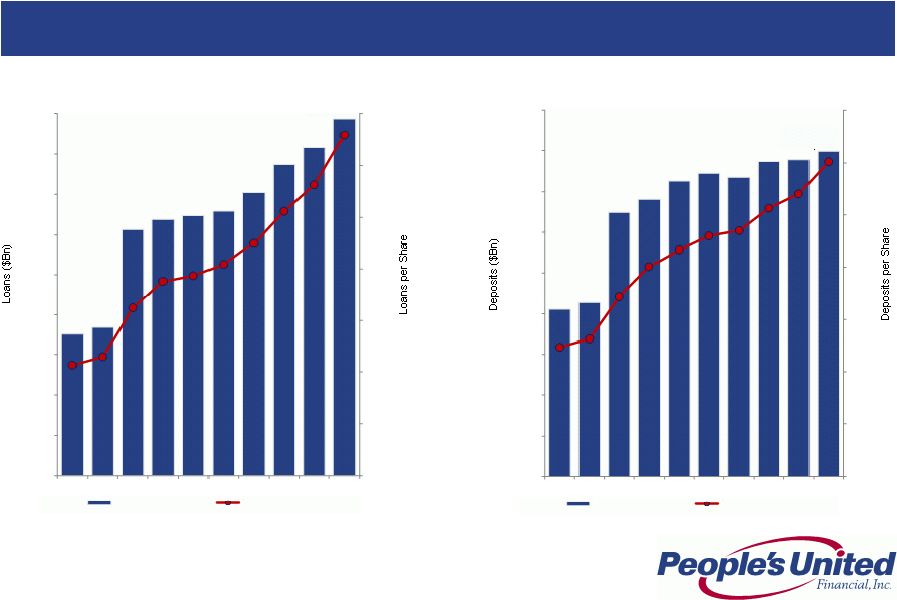

16

Growing Future Earnings Per Share

Loans and Deposits per Share

We have made substantial progress over the past two years, growing loans and deposits

at compound annual growth rates of 19% and 15%, respectively

$72.93

$40

$45

$50

$55

$60

$65

$70

$75

$14

$15

$16

$17

$18

$19

$20

$21

$22

$23

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

Gross Loans ($BN)

Loans per Share

$70.11

$40

$45

$50

$55

$60

$65

$70

$75

$14

$15

$16

$17

$18

$19

$20

$21

$22

$23

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

Deposits ($BN)

Deposits per Share |

17

Immediate Parallel Shock

Yield Curve Twist

Net

Interest

Income

(NII)

Sensitivity

1

Interest Rate Risk Profile

1, 2

Short End

Scenarios

Long End

Scenarios

1

Notes:

The simulation of net interest income requires many key assumptions such as: (i) future balance sheet

volume and mix assumptions that are management judgments based on estimates and historical

experience; (ii) prepayment projections for loans and securities that are projected under each

interest rate scenario using internal and external mortgage analytics; (iii) new business

loan rates that are based on recent new business origination experience; and (iv) deposit pricing

assumptions that are based on historical regression models and management judgment

Yield curve twist pivot point is 18 month point on yield curve. Short End defined as overnight

to 18 months. Long End defined as terms greater than 18 months

1.

2. |

18

Summary

Sustainable Competitive Advantage

Premium brand built over 170 years

High quality Northeast footprint characterized by wealth, density and

commercial activity

Strong leadership team

Solid net interest margin

Superior asset quality

Focus on relationship-based banking

Growing

loans

and

deposits

within

footprint

-

in

two

of

the

largest

MSAs

in

the country (New York City, #1 and Boston, #10)

Improving profitability

Returning capital to shareholders

Strong capital base

Naturally asset sensitive |

19

Appendix |

20

For 2Q 2013 we were more than twice as asset sensitive as the estimated median of our

peer group

Notes:

1.

Analysis is as of 06/30/13 filings

2.

Data as of 06/30/13 SEC filings; where exact +100bps shock up scenario data was

not provided, PBCT interpolated based on data disclosed 3.

Data as of 06/30/13 SEC filings; where exact +200bps shock up scenario data was

not provided, PBCT interpolated based on data disclosed Interest Rate Sensitivity

vs. Peers Net Interest Income at Risk

Analysis involves PBCT estimates, see notes below

Change in Net Interest Income

Scenario

Lowest

Amongst Peers

Highest

Amongst Peers

Peer Median

PBCT Multiple to

Peer Median

Shock Up

100bps

2

-3.4%

8.4%

1.9%

2.3x

Shock Up

200bps

3

-6.0%

16.8%

3.8%

2.9x

1 |

21

Peer Group

Firm

Ticker

City

State

1

Associated

ASBC

Green Bay

WI

2

BancorpSouth

BXS

Tupelo

MS

3

City National

CYN

Los Angeles

CA

4

Comerica

CMA

Dallas

TX

5

Commerce

CBSH

Kansas City

MO

6

Cullen/Frost

CFR

San Antonio

TX

7

East West

EWBC

Pasadena

CA

8

First Niagara

FNFG

Buffalo

NY

9

FirstMerit

FMER

Akron

OH

10

Fulton

FULT

Lancaster

PA

11

Huntington

HBAN

Columbus

OH

12

M&T

MTB

Buffalo

NY

13

New York Community

NYCB

Westbury

NY

14

Signature

SBNY

New York

NY

15

Susquehanna

SUSQ

Lititz

PA

16

Synovus

SNV

Columbus

GA

17

Valley National

VLY

Wayne

NJ

18

Webster

WBS

Waterbury

CT

19

Wintrust

WTFC

Lake Forest

IL

20

Zions

ZION

Salt Lake City

UT |

22

Non-GAAP Financial Measures and Reconciliation to GAAP

In addition to evaluating People’s United Financial’s results of operations in accordance

with U.S. generally accepted accounting principles (“GAAP”), management routinely

supplements this evaluation with an analysis of certain non-GAAP financial measures, such

as the efficiency and tangible equity ratios, tangible book value per share and operating

earnings metrics. Management believes these non- GAAP financial measures provide information

useful to investors in understanding People’s United Financial’s underlying operating

performance and trends, and facilitates comparisons with the performance of other banks and

thrifts. Further, the efficiency ratio and operating earnings metrics are used by management in

its assessment of financial performance, including non-interest expense control, while the

tangible equity ratio and tangible book value per share are used to analyze the relative

strength of People’s United Financial’s capital position.

The efficiency ratio, which represents an approximate measure of the cost required by People’s

United Financial to generate a dollar of revenue, is the ratio of (i) total non-interest

expense (excluding goodwill impairment charges, amortization of other acquisition-related

intangible assets, losses on real estate assets and non-recurring expenses) (the numerator)

to (ii) net interest income on a fully taxable equivalent ("FTE") basis plus total

non-interest income (including the FTE adjustment on bank-owned life insurance

("BOLI") income, and excluding gains and losses on sales of assets other than residential

mortgage loans and acquired loans, and non-recurring income) (the denominator). People’s

United Financial generally considers an item of income or expense to be non-recurring if it

is not similar to an item of income or expense of a type incurred within the last two years and

is not similar to an item of income or expense of a type reasonably expected to be incurred

within the following two years. |

23

Operating earnings exclude from net income those items that management considers to be of such a

non- recurring or infrequent nature that, by excluding such items (net of income taxes),

People’s United Financial’s results can be measured and assessed on a more consistent

basis from period to period. Items excluded from operating earnings, which include, but are not

limited to, merger-related expenses, charges related to executive-level management

separation costs, severance-related costs and writedowns of banking house assets, are

generally also excluded when calculating the efficiency ratio. Operating earnings per share is

derived by determining the per share impact of the respective adjustments to arrive at operating

earnings and adding (subtracting) such amounts to (from) GAAP earnings per share. Operating

return on average assets is calculated by dividing operating earnings (annualized) by average

assets. Operating return on average tangible stockholders' equity is calculated by dividing

operating earnings (annualized) by average tangible stockholders' equity. The operating

dividend payout ratio is calculated by dividing dividends paid by operating earnings for the

respective period. Operating net interest margin excludes from the net interest margin those

items that management considers to be of such a discrete nature that, by excluding such items,

People’s United Financial’s net interest margin can be measured and assessed on a

more consistent basis from period to period. Items excluded from operating net interest margin

include cost recovery income on acquired loans and changes in the accretable yield on acquired

loans stemming from periodic cash flow reassessments. Operating net interest margin is calculated

by dividing operating net interest income (annualized) by average earning assets.

Non-GAAP Financial Measures and Reconciliation to GAAP

|

24

Non-GAAP Financial Measures and Reconciliation to GAAP

The tangible equity ratio is the ratio of (i) tangible stockholders’ equity (total

stockholders’ equity less goodwill and other acquisition-related intangible assets)

(the numerator) to (ii) tangible assets (total assets less goodwill and other

acquisition-related intangible assets) (the denominator). Tangible book value per share is

calculated by dividing tangible stockholders’ equity by common shares (total common shares

issued, less common shares classified as treasury shares and unallocated Employee Stock

Ownership Plan ("ESOP") common shares).

In light of diversity in presentation among financial institutions, the methodologies used by

People’s United Financial for determining the non-GAAP financial measures discussed

above may differ from those used by other financial institutions. Please refer to People’s

United Financial’s latest Form 10-Q regulatory filing for detailed reconciliations to

GAAP figures. |

For

more information, investors may contact: Peter Goulding, CFA

203-338-6799

peter.goulding@peoples.com |