Attached files

| file | filename |

|---|---|

| 8-K - 8-K - RED ROBIN GOURMET BURGERS INC | a13-18589_18k.htm |

| EX-99.1 - EX-99.1 - RED ROBIN GOURMET BURGERS INC | a13-18589_1ex99d1.htm |

Exhibit 99.2

|

|

Fiscal Q213 Results August 15, 2013 |

|

|

Forward-Looking Statements 1 Forward-looking statements in this presentation regarding our expected earnings per share, restaurant sales, new restaurant growth, brand transformation initiative, future economic performance, costs and capital expenditures, certain statements under the headings “Brand Transformation” and “2013 Outlook -- Financials” and all other statements that are not historical facts, are made under the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These statements are based on assumptions believed by the Company to be reasonable and speak only as of the date on which such statements are made. Without limiting the generality of the foregoing, words such as “expect,” “believe,” “anticipate,” “intend,” “plan,” “continue,” “project,” or “estimate,” or the negative or other variations thereof or comparable terminology are intended to identify forward-looking statements. We undertake no obligation to update such statements to reflect events or circumstances arising after such date, and we caution investors not to place undue reliance on any such forward-looking statements. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those described in the statements based on a number of factors, including but not limited to the following: the effectiveness of the Company’s marketing strategies, loyalty program and guest count initiatives to achieve restaurant sales growth; the ability to fulfill planned expansion; the cost and availability of key food products, labor and energy; the ability to achieve anticipated revenue and cost savings from our anticipated new technology systems and other initiatives; availability of capital or credit facility borrowings; the adequacy of cash flows or available debt resources to fund operations and growth opportunities; federal, state and local regulation of our business; and other risk factors described from time to time in the Company’s Form 10-K, Form 10-Q and Form 8-K reports (including all amendments to those reports) filed with the U.S. Securities and Exchange Commission. This presentation may also contain non-GAAP financial information. Management uses this information in its internal analysis of results and believes that this information may be informative to investors in gauging the quality of our financial performance, identifying trends in our results and providing meaningful period-to-period comparisons. For a reconciliation of non-GAAP measures presented in this document, see the Appendix of this presentation. |

|

|

Comp sales up 4.3% -- 12th consecutive quarter of same store sales growth Total restaurant revenues increased 6.6% Restaurant-level operating profit margin increased 220 bps to 23.3% EPS $0.77 compared to $0.52 in Q212 Q213 Headlines 2 |

|

|

“24 Burgers. A Million Reasons” Campaign FPO 3 |

|

|

Menu Innovation 4 |

|

|

Summer Promo 5 |

|

|

Brand Transformation Launched most impactful changes system wide Elevated bar experience New plating, presentation and service model Favorable guest feedback on changes Continued testing; plans to transform additional 20 restaurants in 2013 6 |

|

|

Financial Update 7 |

|

|

Adjusted Earnings Per Diluted Share Note: Fiscal Q4 2012 contained 13 weeks compared to 12 weeks in 2011 8 See slide 21 for reconciliation of non-GAAP Adjusted Earnings Per Diluted Share to Earnings Per Diluted share +16% YTD 2013 |

|

|

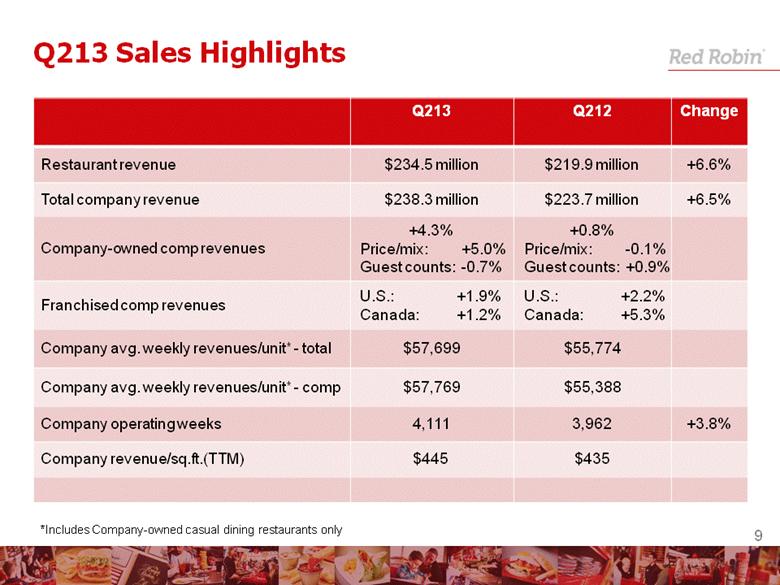

Q213 Q212 Change Restaurant revenue $234.5 million $219.9 million +6.6% Total company revenue $238.3 million $223.7 million +6.5% Company-owned comp revenues +4.3% Price/mix: +5.0% Guest counts: -0.7% +0.8% Price/mix: -0.1% Guest counts: +0.9% Franchised comp revenues U.S.: +1.9% Canada: +1.2% U.S.: +2.2% Canada: +5.3% Company avg. weekly revenues/unit* - total $57,699 $55,774 Company avg. weekly revenues/unit* - comp $57,769 $55,388 Company operating weeks 4,111 3,962 +3.8% Company revenue/sq.ft.(TTM) $445 $435 Q213 Sales Highlights *Includes Company-owned casual dining restaurants only 9 |

|

|

Comparable Sales Growth 10 |

|

|

Leading RLOP Margins 11 |

|

|

RLOP Margin Improvement Change over prior year, in bps 12 |

|

|

Line Item % of Restaurant Revenues Q213 % of Restaurant Revenues Q212 Favorable (Unfavorable) Cost of Sales 24.7% 25.4% 70 bps Labor 32.7% 33.2% 50 bps Other Operating 12.1% 13.1% 100 bps Occupancy 7.2% 7.2% No change Restaurant Level Operating Profit (Non-GAAP) 23.3% 21.1% 220 bps Q213 Restaurant Results 13 |

|

|

Adjusted EBITDA $ in millions 14 $62.2 million YTD 2013 |

|

|

2013 Outlook – Financials Capital investments approximately $70 million Open 20 new company-owned Red Robin® restaurants plus several Red Robin’s Burger Works® Comparable restaurant revenue growth of approximately 3.0% versus 2012 RLOP margins approximately 21.3% G&A costs between $89 million and $90 million 15 |

|

|

Appendix 16 |

|

|

Category % of Total COGS in Q2 2013 Market vs. Contract Hamburger 14.3% Market Steak Fries 10.8% 100% contract through 10/13 Poultry 10.8% 100% contract through 12/13 Produce 7.9% 100% contract through 9/13 Bread 6.5% 100% contract through 12/13 Cheese 5.5% Market Meat 4.6% 100% contract through 8/13 on bacon, 100% contract through 12/13 on prime rib Fry oil 2.6% 100% contract through 12/13 Q213 Commodity Update 17 |

|

|

Adjusted Net Income $ in millions 18 See slide 21 for reconciliation of non-GAAP Adjusted Net Income to Net Income |

|

|

Cash Flow from Operations $ in millions 19 |

|

|

Adjusted EBITDA Reconciliation to Net Income 2011 2012 2013 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Net income as reported $8,708 $6,895 $2,069 $2,905 $10,558 $7,748 $3,533 $6,492 $9,480 $11,139 Adjustments to net income: Income tax expense (benefit) 1,132 663 (369) 85 3,356 2,408 1,210 1,552 2,977 3,576 Interest expense, net 1,353 1,474 1,523 1,473 1,833 1,223 1,041 1,217 1,052 623 Depreciation and amortization 17,111 12,634 13,006 12,521 16,652 12,532 13,284 13,000 17,834 13,319 Non-cash stock-based compensation 858 623 696 1,142 1,202 1,068 894 644 1,192 1,050 Loss on debt refinancing - - - - - - - 2,919 - Executive transition & severance 785 902 541 - - - - - - Impairment and closure charges - - 1,919 2,418 - - - - - Initial gift card breakage (438) - - - - - - - - Adjusted EBITDA $29,509 $23,191 $19,385 $20,544 $33,601 $24,979 $19,962 $25,824 $32,535 $29,707 20 |

|

|

Reconciliation of Adjusted Net Income to Net Income and Adjusted Earnings Per Diluted Share to Earnings Per Diluted Share 2011 2012 2013 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Net income as reported $ 8,708 $ 6,895 $ 2,069 $ 2,905 $ 10,558 $ 7,748 $ 3,533 $ 6,492 $ 9,480 $ 11,139 Adjustments to net income: Loss on debt refinancing - - - - - - - 2,919 - - Executive transition & severance 785 902 541 - - - - - - - Impairment and closure charges - - 1,919 2,418 - - - - - - Initial gift card breakage (438) - - - - - - - - - Income tax expense of adjustments (34) (302) (846) (1,208) (1,020) - - Adjusted net income $ 9,021 $ 7,495 $ 3,683 $ 4,115 $ 10,558 $ 7,748 $ 3,533 $ 8,391 $ 9,480 $ 11,139 Diluted net income per share: Net income as reported $ 0.56 $ 0.44 $ 0.14 $ 0.20 $ 0.71 $ 0.52 $ 0.24 $ 0.45 $ 0.66 $ 0.77 Adjustments to net income: Loss on debt refinancing - - - - - - - 0.20 - - Executive transition & severance 0.05 0.06 0.04 - - - - - - - Impairment and closure charges - - 0.12 0.16 - - - - - - Initial gift card breakage (0.03) - - - - - - - - - Income tax expense of adjustments - (0.02) (0.06) (0.08) (0.06) - - Adjusted earnings per share - diluted $ 0.58 $ 0.48 $ 0.24 $ 0.28 $ 0.71 $ 0.52 $ 0.24 $ 0.59 $ 0.66 $0.77 21 |