Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - JONES LANG LASALLE INC | d579404d8k.htm |

Investor Presentation

August 2013

50,000 employees

200 offices

70 countries

1 global platform

1

Exhibit 99.1 |

Table of Contents

I.

Company Description

II.

Global Growth Strategy

III.

Financial Overview

IV.

Appendix

2 |

Company

Description 3 |

Creating real value for clients and our firm

4

Shareholder opportunity

•

Leading global market positions

•

Consolidator in a consolidating industry

•

Productivity and margin expansion

Premier global investment manager

•

LaSalle Investment Management provides outstanding

performance for global real estate investors

•

Investment expertise including core, value-add,

opportunistic investing across property types

•

More than 300 institutional clients worldwide

Global real estate services

•

Strategic, fully integrated services for real estate

owners, occupiers and investors

•

Productivity and cost solutions for corporate clients

•

Industry leader recognized for deep

market knowledge

and execution

Shareholder value

•

Strong cash-generating business model

•

Revenue growth

•

Investment-grade balance sheet

•

Effective tax and interest expense management |

Jones

Lang Wootton founded

1783

1968

1997

1999

LaSalle Partners

founded

LaSalle Partners initial

public offering

LaSalle Partners and Jones

Lang Wootton merge to create

Jones Lang LaSalle

Integrated global platform

(NYSE ticker “JLL”)

Strategic M&A establishes premier market position

2008

The Staubach Company and

Jones Lang LaSalle combine operations

Largest merger in JLL history transforms

U.S. local markets position

King Sturge (est. 1760) and Jones Lang LaSalle merge EMEA operations

Enhances strength and depth of service capabilities in the UK and EMEA

1760

2011

5

14% compound annual

revenue growth rate since

1999 merger |

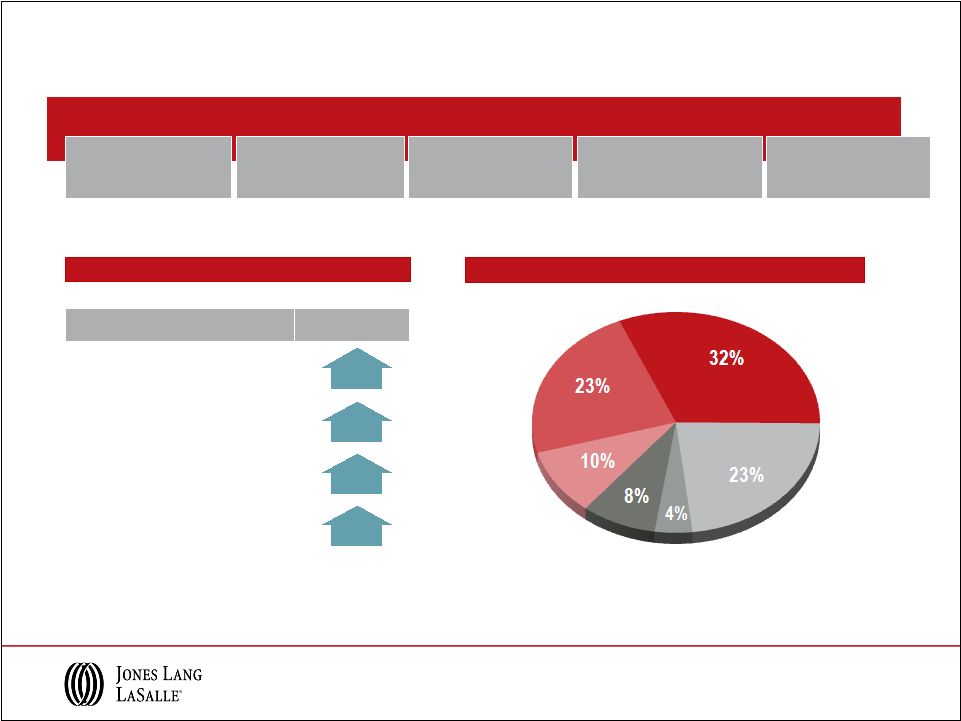

Delivering integrated services globally

2012 Fee Revenue = $3.6B

Global Distribution

Leasing

Advisory

& Other

LaSalle Inv. Mgmt.

Property & Facility

Mgmt.

Project &

Development

Services

Capital Markets

Other

United Kingdom

France

Germany

Other

Europe

Japan

Greater China

(incl. Hong Kong)

Australia

India

Singapore

EMEA

Asia Pacific

Americas

43%

5%

3%

4%

6%

7%

10%

13%

4%

3%

2%

United

States

6 |

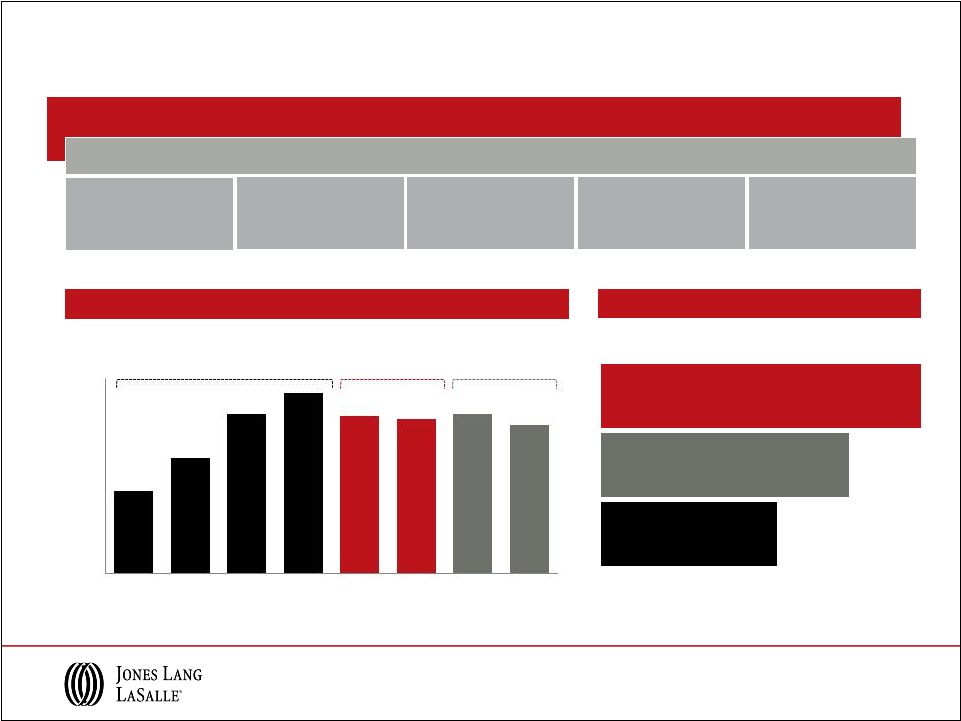

Repositioning Creates Opportunity: Trends from 2002 to 2012

Growth in a consolidating industry

Jones Lang LaSalle ($ in millions)

Fee Revenue

Adjusted Operating Income

Market Cap

1

~4x

$3,640

$860

2002

2012

~5x

$340

$67

2002

2012

~5x

$3,836

$786

2002

2012

(1) Based on peak share price in each year

Opportunity

Trend

Toward centralized decisions

Toward larger, global service providers

Toward cross-border investing

Toward market share growth for established brands

7

Complex corporate real estate portfolio decisions benefit from

JLL’s expertise

Few players possess JLL’s breadth of service

and reach

Global platform and deep research create opportunities for

cross-border investor clients

High-quality brand, reputation and platform attract

and retain top talent |

JLL

3-Year Performance Market Trends

Emerging markets to

lead global expansion

Demand for

local and global services

Outsourcing growth

continues

Top asset managers win

investor mandates

Industry

consolidation

(1)

Other Financing Activities include change in working capital, debt issue costs and

share activity related to taxes on stock awards Market share

expansion drives growth and cash generation 3-Year Cash from Earnings =

$962M New

Acquisitions

Deferred Acquisition

Obligations

Co-Investment

Other Financing

Activities¹

Dividends

CapEx

8

Metric

Growth

Revenue

34%

Adjusted Net Income

48%

Adjusted EBITDA

29%

Adjusted EPS

45% |

Global

Growth Strategy 9 |

G5

CONNECTIONS:

Differentiate and Sustain

G5 global growth strategy

G4

G2

G3

G1

Build our local and

regional leasing

and capital

markets business

Capture the leading

share of global

capital flows for

investment sales

Strengthen our winning

positions in Corporate

Solutions

Grow LaSalle Investment

Management’s leadership

position

10 |

Full-Year Capital Markets & Leasing Markets Volumes

Q2 2013 v. Q2 2012

FY 2013 v. FY 2012

Gross Absorption

Gross Absorption

Leasing

Americas (U.S. only)

-3%

0-5%

EMEA (Europe only)

-3%

Flat

Asia Pacific (select markets)

-25%

-10-15%

Total

-5%

Flat

Q2 2013 v. Q2 2012

FY 2013 v. FY 2012

Market Volumes

Market Volumes

Capital Markets

Americas

11%

10-15%

EMEA

2%

Flat

Asia Pacific

18%

10-15%

Total

10%

5-10%

2013 Leasing volumes predicted flat to 2012

Projected 2013 Capital Markets volumes: $450 -

$500 Billion

11 |

+15-20%

0

50

100

150

200

250

300

350

Americas

EMEA

Asia Pacific

2005

2006

2007

2008

2009

2010

2011

2012

2013 Projection

Flat

+10-15%

($ in billions)

Global capital flows for investment sales

* EMEA: In US$ terms, unchanged in Euro terms.

Source: Jones Lang LaSalle, July 2013

Direct Commercial Real Estate Investment, 2005-2013

2013 Capital Markets volumes projected up 5-10% on 2012

Projection updates as of Q2:

Americas: Previous forecast was up 15-20% EMEA:

Unchanged

Asia Pacific: Unchanged

Consolidated: Previous forecast was up 10-15%

12 |

Asia

Pacific EMEA

Americas

$593

$781

$753

$1,000

$1,188

$1,278

$557

$317

$203

$306

$460

*

$513

Leasing

Capital Markets

Scale and leadership in Leasing and Capital Markets

Market Outlook

Overall, Leasing volumes projected flat to 2012 levels

2013 Capital Markets volumes projected up

5%-10% on 2012

JLL Revenue

($ in millions)

**

*

* July 2008: Staubach Company acquired, annual revenue = $375 million

**May 2011: King Sturge acquired, annual revenue -

$260 million

13 |

Global outsourcing propels Corporate Solutions

Competitive Advantages

Global

Position

Transformational

outsourcing

Space

optimization

Portfolio transparency

Energy

management

Expertise across services & geographies to capitalize on market trends

JLL’s world-class capabilities

2012 JLL Client Wins

Scalable platform

Integrated Service

Wins

58

Wins

48

Expansions

39

Renewals

47

Large Corporations

Middle Market

14

Transaction

management

Energy &

sustainability

Single point of

accountability |

$228

$245

$238

$242

$278

$245

$178

$128

Competitive Advantages

Diversified global

platform

Core, Value Add,

Opportunistic,

Public Equity

300+

institutional clients

Consistent client

services delivery model

Financial backing

of well-capitalized

parent company

Proven performance history with long-standing client relationships

($ millions)

2005 to 2012 Advisory Fees

Assets Under Management

Q2 2013 AUM = $46B

Performance drives LaSalle Investment Management

Building Advisory Fees in

Healthy Markets

Global Financial

Crisis

Stabilized

Advisory Fees

($ billions)

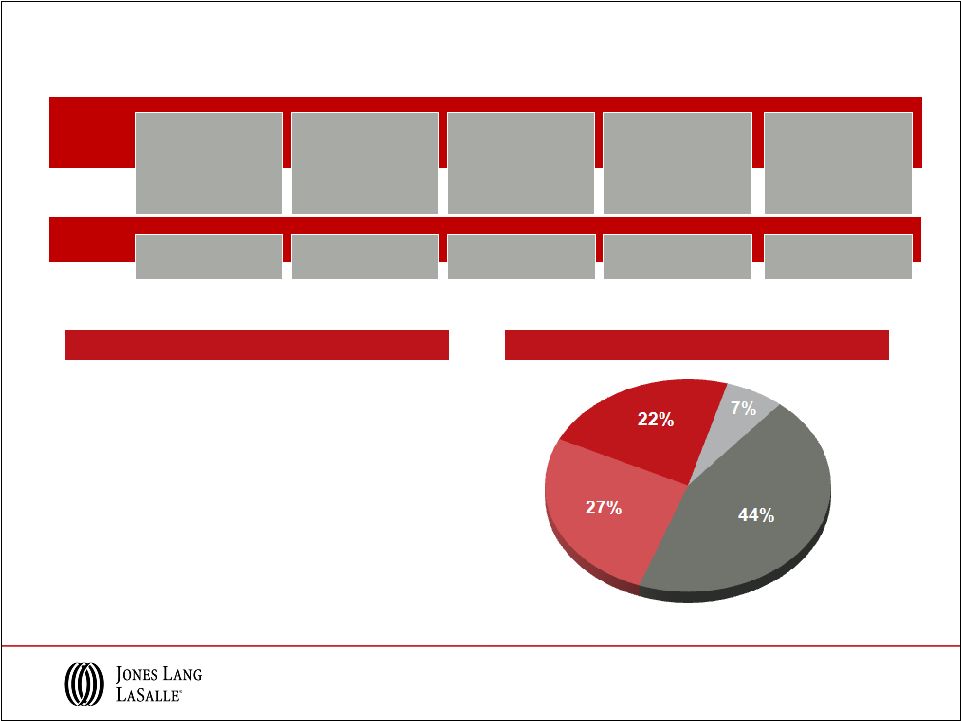

Fund Management $14.6

Public Securities $10.3

Separate Accounts $21.4

15

$0

$100

$200

$300

2005

2006

2007

2008

2009

2010

2011

2012 |

Consolidating industry leads to JLL opportunity

Transformative Results

The Staubach

Company

King Sturge

Meghraj

Trinity Funds

Management

Strategy

Establish leading U.S. local

market tenant rep position

Strengthen local market

scale, particularly in the UK

Augment India corporate business

with leading local presence

Gain scale and credibility

in Australia for LaSalle

Purchase Price

$613 million

£197 million

$60 million

A$9 million

Payment

Structure

36% upfront;

64% deferred over 5 years

50% upfront;

50% deferred over 5 years

50% upfront:

50% deferred over 5 years

100% upfront

EBITDA

multiple

8.0x notional,

7.0x on PV basis

7.5x notional,

7.0x on PV basis

7.5x

4.0x

Strategic

Align with

G5 strategy

Enhance service

delivery for clients

Cultural

alignment

Meet

financial goals

Financial

Profit growth to

shareholders

Neutral to accretive

EBITDA multiples

EPS accretive within

12-18 months

Maintain investment

grade strength

16 |

Financial Overview

17 |

Note:

2012 and 2011 adjusted for restructuring and intangible amortization. 2012

Fee

Revenue

Adjusted

Net Income

$245M

Adjusted

EPS

$5.48

Adjusted

EBITDA

$436M

Adjusted EBITDA

Margin

12.0%

Gross revenue : $3.9B

2011

$215M

$4.83

$395M

11.7%

$3.4B

US GAAP: $164M

US GAAP: $3.70

EBITDA: $339M

EBITDA margin: 9.5%

Gross Revenue: $3.6B

US GAAP: $208M

US GAAP: $4.63

EBITDA: $391M

EBITDA margin: 9.9%

Continued solid fee revenue growth with 7% increase

for the second quarter and YTD

Capital Markets & Hotels outperformed markets in all

regions

Healthy corporate outsourcing pipeline; transitioning

new clients from previous wins

Focus on market share growth and improved

productivity across the firm

$3.6B

Consolidated earnings scorecard

H1 2013 Performance & Priorities

2012 Revenue Contribution

Americas

LIM

Asia Pacific

EMEA

18

Margin is calculated on a fee revenue basis. |

YTD 2013 Real Estate Services Revenue

($ in millions; % change in USD

over YTD 2012)

Note: Segment and Consolidated Real Estate Services (“RES”) operating

revenue exclude Equity earnings (losses). Fee revenue presentation of

Property & Facility Management, Project & Development Services and Total RES Operating Revenue excludes

gross contract costs.

Leasing

$350.1

4%

$109.1

(4%)

$68.6

(13%)

$527.8

0%

Capital Markets & Hotels

$92.1

32%

$121.5

36%

$64.7

43%

$278.3

36%

Property & Facility

Management

$218.6

7%

$89.7

5%

$200.5

6%

$508.8

6%

Fee Revenue

$175.7

5%

$82.5

0%

$164.7

10%

$422.9

6%

Project & Development

Services

$80.7

(5%)

$112.1

9%

$41.2

13%

$234.0

4%

Fee Revenue

$80.1

(5%)

$51.6

3%

$31.6

2%

$163.3

(1%)

Advisory,

Consulting & Other

$51.5

4%

$80.7

0%

$43.3

7%

$175.5

2%

Total RES Operating

Revenue

$793.0

7%

$513.1

9%

$418.3

7%

$1,724.4

7%

Fee Revenue

$749.5

6%

$445.4

7%

$372.9

8%

$1,567.8

6%

Americas

EMEA

Asia Pacific

Total RES

19 |

2012

Fee

Revenue

Operating Income

$168M

Operating Income

Margin

10.1%

EBITDA

$210M

EBITDA Margin

12.7%

Gross revenue : $1.7B

2011

$163M

10.8%

$201M

13.4%

$1.5B

Leasing and Capital Markets both outpaced market

volumes; strong transaction pipelines for remainder

of 2013

Growing Property & Facility Management revenue

from new outsourcing assignments;

transitioning

new clients to generate revenue growth in second

half of 2013

Actively managing cost base to drive performance,

particularly in challenging economies such as

Brazil

$1.7B

Americas Real Estate Services

H1 2013 Performance & Priorities

2012 Revenue Contribution

Note:

Margin

is

calculated

on

a

fee

revenue

basis.

See

Appendix

for

calculation

of

fee

revenue.

EBITDA

margin

for

2012

and

2011

would

have

been

~13.0%

after

adjusting

2012

compensation

expense

for

the

Staubach

acquisition

payment

and

adjusting

2011

compensation expense for the elimination of SOP.

20

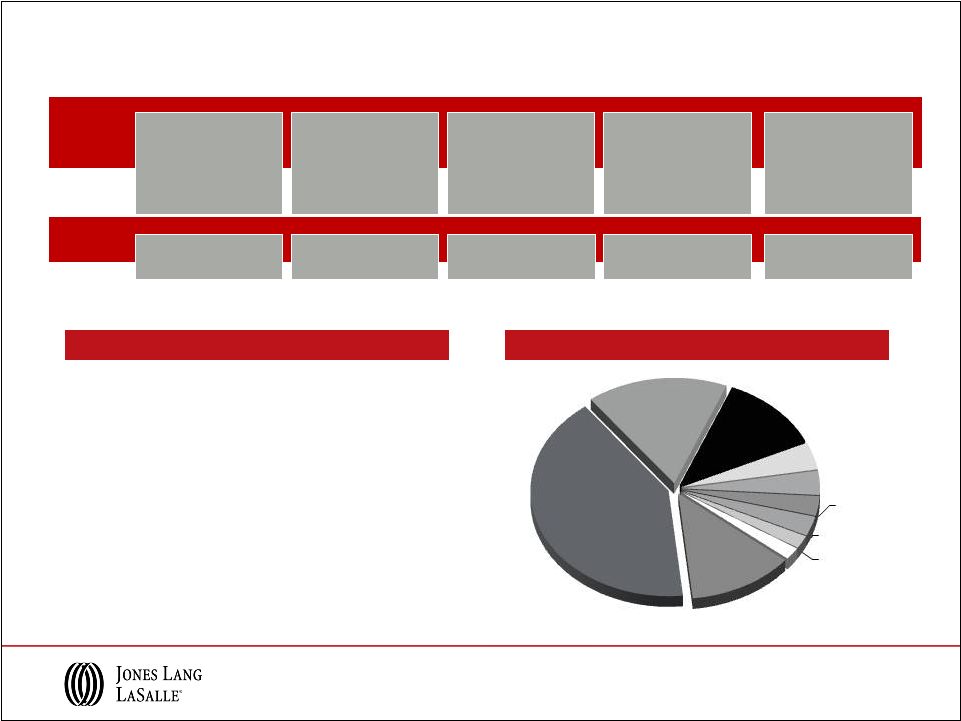

United

States

92%

Brazil 3%

Canada 2%

Mexico 1%

Other

Americas 2% |

2012

Fee

Revenue

Operating Income

$58M

Operating Income

Margin

6.2%

EBITDA

$75M

EBITDA Margin

8.0%

Gross revenue : $1.0B

2011

$39M

4.4%

$57M

6.5%

$888M

UK, France and Spain drove a 28% increase in

Capital Markets & Hotels revenue in the second

quarter, up 37% YTD 2013

Project & Development Services; Tetris fit-out

business continues to grow, expanding offer to

hotel and retail clients

EMEA operating margins up significantly for the

first half of 2013 versus 2012, reflecting strong

performance in flat overall markets

$936M

EMEA Real Estate Services

H1 2013 Performance & Priorities

2012 Revenue Contribution

Note: Operating income has been adjusted to exclude $5 million of King Sturge

intangibles amortization. Margin is calculated on a fee revenue

basis. See Appendix for calculation of fee revenue. 21

U.K. 41%

France 17%

Germany

12%

Russia 4%

Spain 4%

Netherlands

3%

Belgium 3%

Italy 2%

MENA 2%

Other EMEA

12% |

2012

Fee

Revenue

Operating Income

$65M

Operating Income

Margin

8.4%

EBITDA

$78M

EBITDA Margin

10.0%

Gross revenue : $876M

2011

$66M

9.3%

$78M

11.0%

$731M

Revenue growth of 11% in first half of 2013 led by 44%

transactional growth in Capital Markets & Hotels, well

above market volume increases

Leasing revenue down 12% in H1, but outperformed

market volumes that were down 21%, reflecting

hesitancy among corporate clients to make space

decisions

Winning Corporate Solutions business continues to

generate profitable, recurring revenue; Property & Facility

Management revenue up 14% YTD 2013

$781M

Asia Pacific Real Estate Services

H1 2013 Performance & Priorities

2012 Revenue Contribution

Note:

Margin

is

calculated

on

a

fee

revenue

basis.

See

Appendix

for

calculation

of

fee

revenue.

22 |

2012

Fee

Revenue

Operating Income

$72M

Operating Income

Margin

25.2%

EBITDA

$74M

EBITDA Margin

25.9%

2011

$57M

20.7%

$60M

21.7%

$275M

$1.8B of capital was raised during the quarter, $2.4

billion YTD 2013

Improved investment activity and capital raising will

generate growth in AUM and in advisory fees as

the capital is invested

Expect lower incentive fees for FY 2013 compared

with FY 2012

Equity earnings of $15 million YTD 2013 reflects

continued positive investment performance for our

clients

$285M

LaSalle Investment Management

H1 2013 Performance & Priorities

Q2 2013 Assets Under Management

($ in billions)

Note: AUM data reported on a one-quarter lag.

23 |

Strong balance sheet position

Investment

grade

balance

sheet;

Baa2

/

BBB-

(Stable)

–

–

–

Healthy

net

debt

position

entering

historically

strong

second

half

–

Net debt reduction of $37 million during Q2; consistent with previous

seasonal borrowing pattern

Semi-annual dividend increased by 10% to $0.22 per share from

$0.20 per share

–

Paid June 14, 2013

Q2 Capital Spending primarily on Deferred Acquisition Payments

and Earn Outs

Q2 2013

Q2 2012

–

Cap Ex

$ 18M

$ 13M

–

New M&A Payment

$ 2M

$ 0M

–

Deferred Acquisition Payments/ Earn Outs

$ 72M

$ 41M

–

Co-Investment

($10M)

($20M)

Q2 2013 Highlights

24

Balance Sheet

Q2

Q1

Q4

$ millions

2013

2013

2012

Cash

$ 122

$ 133

$ 152

51

38

32

Credit Facility

479

470

169

Net Bank Debt

$ 408

$ 375

$ 49

LT Senior Notes

275

275

275

Deferred Acquisition

Obligations

150

220

214

Total Net Debt

$ 833

$ 870

$ 538

Low debt cost: Q2 2013 net interest expense of $9.0M

Credit

facility

capacity

of

$1.1B

Diversified funding sources with $275M, 4.4% coupon Long Term

Senior Notes issued in Q4 2012

Short Term Borrowings |

Jones

Lang LaSalle Integrated global

services

Industry-leading

research and market

expertise

Superior client

relationship

management

Strong

brand

Investment-grade

balance sheet

Solid performance in growth opportunities

JLL actions for continued success

Optimism returning to global markets

Leverage global positions to grow market share and

continue client success in local markets

Increase productivity and manage costs to improve margin

Continue to invest strategically to capitalize

on market consolidation

Maintain financial strength and flexibility to respond to

opportunities and challenges

On-going industry consolidation

trends continue

Continuing growth in

corporate outsourcing

Steady institutional capital flows

into global real estate

25 |

Appendix

26 |

as of

Q2 2013 Leasing Values

Source: Jones Lang LaSalle

Asia Pacific

EMEA

Americas

as of Q2 2013

Capital Values

JLL Property Clocks

SM

Chicago

Hong

Kong

Singapore

Brussels

Dallas, Frankfurt

Houston

San Francisco

Toronto

Rental Value

growth slowing

Rental Value

growth

accelerating

Rental Values

bottoming out

Rental Values

falling

Los

Angeles, Seoul, Shanghai

Tokyo

Washington, DC

Mexico

City

Sao Paulo

Paris

Mumbai, Boston

Madrid

New York

Istanbul, Dubai

London

Berlin, Moscow

Stockholm

Amsterdam

Johannesburg

Milan

Capital Value

growth slowing

Capital Value

growth

accelerating

Capital Values

bottoming out

Capital Values

falling

Boston, Chicago

San Francisco, Houston, Berlin

Washington DC, Amsterdam

Toronto

Sao

Paulo, Paris

Mexico

City, Frankfurt

Dallas, Singapore

New York, Los Angeles, Stockholm

Beijing

Shanghai

Mumbai

Seoul, Tokyo

Sydney

Milan

Madrid

Brussels

London

Moscow

Hong Kong

Beijing

Sydney

27 |

Q2 2013 Real Estate Services Revenue

($ in millions; % change in USD

over Q2 2012)

Note: Segment and Consolidated Real Estate Services (“RES”) operating

revenue exclude Equity earnings (losses). Fee revenue presentation of

Property & Facility Management, Project & Development Services and Total RES Operating Revenue excludes

gross contract costs.

Leasing

$197.8

6%

$60.2

(9%)

$40.6

(11%)

$298.6

0%

Capital Markets & Hotels

$53.4

27%

$63.2

27%

$41.0

72%

$157.6

36%

Property & Facility

Management

$110.1

8%

$46.9

9%

$100.5

8%

$257.5

8%

Fee Revenue

$86.3

5%

$42.0

0%

$82.3

10%

$210.6

6%

Project & Development

Services

$42.7

(5%)

$56.2

7%

$21.4

11%

$120.3

3%

Fee Revenue

$42.3

(6%)

$27.6

7%

$16.2

(1%)

$86.1

(1%)

Advisory,

Consulting & Other

$27.5

3%

$41.6

(3%)

$25.0

10%

$94.1

2%

Total RES Operating

Revenue

$431.5

7%

$268.1

5%

$228.5

12%

$928.1

8%

Fee Revenue

$407.3

6%

$234.6

4%

$205.1

12%

$847.0

6%

Americas

EMEA

Asia Pacific

Total RES

28 |

FY 2012 Real Estate Services revenue

($

in

millions;

%

change

in

USD

over

FY

2011)

Note: Segment and Consolidated Real Estate Services (“RES”) operating

revenue exclude Equity earnings (losses). Fee revenue presentation of

Property & Facility Management, Project & Development Services and Total RES Operating Revenue excludes gross

contract costs.

Leasing

$829.6

9%

$250.0

6%

$198.2

3%

$1,277.8

7%

Capital Markets & Hotels

$168.5

24%

$235.1

3%

$109.3

15%

$512.9

12%

Property & Facility

Management

$458.7

31%

$155.2

5%

$398.4

9%

$1,012.3

17%

Fee Revenue

$375.0

14%

$155.2

5%

$319.9

12%

$850.1

12%

Project & Development

Services

$182.9

3%

$219.8

21%

$83.5

3%

$486.2

10%

Fee Revenue

$182.1

2%

$106.5

11%

$67.2

13%

$355.8

7%

Advisory,

Consulting & Other

$107.0

9%

$189.1

6%

$86.1

6%

$382.2

7%

Total RES Operating

Revenue

$1,746.7

15%

$1,049.2

8%

$875.5

7%

$3,671.4

11%

Fee Revenue

$1,662.2

11%

$935.9

5%

$780.7

10%

$3,378.8

8%

Americas

EMEA

Asia Pacific

Total RES

29 |

Fee revenue / expense reconciliation

•

Reimbursable vendor, subcontractor and out-of-pocket costs reported as revenue

and expense in JLL financial statements have been steadily increasing

•

Margins diluted as gross-accounting requirements increase revenue and costs without

corresponding profit •

Business managed on a “fee”

basis to focus on margin expansion in the base business

($ in millions)

2013

2012

2013

2012

Consolidated Revenue

989.4

$

921.3

$

1,845.4

$

1,734.7

$

Consolidated Operating Expenses

917.0

846.7

1,749.7

1,636.4

Adjusted Operating Income Margin

7.4%

8.3%

5.2%

5.9%

Gross Contract Costs:

Property & Facility Management

23.8

19.9

42.9

35.7

Project & Development Services

0.4

0.2

0.6

0.3

Total Gross Contract Costs

24.2

20.1

43.5

36.0

Property & Facility Management

4.9

1.4

7.2

2.7

Project & Development Services

28.6

26.6

60.5

53.0

Total Gross Contract Costs

33.5

28.0

67.7

55.7

Property & Facility Management

18.2

18.1

35.8

40.3

Project & Development Services

5.2

2.9

9.6

5.6

Total Gross Contract Costs

23.4

21.0

45.4

45.9

Consolidated Fee Revenue

908.3

$

852.2

$

1,688.8

$

1,597.1

$

Consolidated Fee-based Operating Expenses

835.9

$

777.6

$

1,593.1

$

1,498.8

$

Adjusted Operating Income Margin ("fee"-based)

8.0%

9.0%

5.7%

6.4%

Asia Pacific

Americas

EMEA

Q2

YTD

Note: Consolidated revenue and fee revenue exclude equity earnings (losses).

Restructuring and acquisition charges are excluded from operating

expenses. Restructuring and acquisition charges as well as intangible

amortization related to the King Sturge acquisition are excluded from operating

expenses when calculating adjusted operating income margin. 30

|

2013

2012

2013

2012

46.3

$

37.2

$

59.4

$

51.2

$

45,141

44,847

45,091

44,726

1.03

$

0.83

$

1.32

$

1.14

$

46.3

$

37.2

$

59.4

$

51.2

$

5.0

12.4

7.4

19.1

0.4

1.2

0.8

2.8

51.7

$

50.8

$

67.6

$

73.1

$

45,141

44,847

45,091

44,726

1.15

$

1.13

$

1.50

$

1.63

$

Adjusted earnings per share

Three Months Ended

June 30,

Six Months Ended

June 30,

($ in millions)

GAAP Net income attributable to common

shareholders

Shares (in 000s)

GAAP earnings per share

GAAP Net income attributable to common

shareholders

Restructuring and acquisition charges, net

Intangible amortization, net

Adjusted net income

Shares (in 000s)

Reconciliation of GAAP net income to adjusted net income and

calculations of earnings per share

31 |

Reconciliation of GAAP operating income to adjusted operating

income and net income to adjusted EBITDA

2013

2012

2013

2012

65.8

$

58.1

$

85.9

$

72.7

$

6.6

16.6

9.8

25.6

0.6

1.6

1.1

3.8

73.0

76.3

96.8

102.1

49.5

$

37.7

$

62.7

$

51.9

$

9.0

7.5

17.0

14.9

16.4

12.8

20.8

17.7

20.2

20.0

39.2

39.6

95.1

$

78.0

$

139.7

$

124.1

$

6.6

16.6

9.8

25.6

101.7

$

94.6

$

149.5

$

149.7

$

Adjusted EBITDA

Three Months

Ended June 30,

Six Months Ended

June 30,

($ in millions)

GAAP Net income

Interest expense, net of interest income

Provision for income taxes

Depreciation and amortization

EBITDA

Restructuring and acquisition charges

Operating Income

Restructuring and acquisition charges

Intangible amortization

Adjusted Operating Income

32 |

Forward-looking statements

Statements in this presentation regarding, among other things, future financial results

and performance, achievements, plans and objectives and dividend payments may be

considered forward-looking statements within the meaning of the Private

Securities Litigation Reform Act of 1995. Such statements involve known and

unknown risks, uncertainties and other factors which may cause actual results,

performance, achievements, plans and objectives of Jones Lang LaSalle to be

materially different from those expressed or implied by such forward-looking

statements. Factors that could cause actual results to differ materially include those discussed

under

“Business,”

“Risk

Factors,”

“Management’s

Discussion

and

Analysis

of

Financial

Condition

and

Results

of

Operations,”

“Quantitative

and

Qualitative

Disclosures

about

Market

Risk,”

“Cautionary

Note

Regarding

Forward-

Looking

Statements”

and

elsewhere

in

Jones

Lang

LaSalle’s

Annual

Report

on

Form

10-K

for

the

year

ended

December 31, 2012, in the Quarterly Report on Form 10-Q for the quarter ended June

30, 2013 and in other reports filed with the Securities and Exchange Commission.

There can be no assurance that future dividends will be declared since the actual

declaration of future dividends, and the establishment of record and payment dates,

remains

subject

to

final

determination

by

the

Company’s

Board

of

Directors.

Statements

speak

only

as

of

the

date of this presentation. Jones Lang LaSalle expressly disclaims any obligation or

undertaking to update or revise any forward-looking statements contained

herein to reflect any change in Jones Lang LaSalle’s expectations or results,

or any change in events. ©

Jones Lang LaSalle IP, Inc. 2013. All rights reserved. No part of this publication may be

reproduced by any means, whether graphically, electronically, mechanically or

otherwise howsoever, including without limitation photocopying and recording on

magnetic tape, or included in any information store and/or retrieval system

without prior written permission of Jones Lang LaSalle IP, Inc.

33 |