Attached files

| file | filename |

|---|---|

| 8-K - 8-K - MVB FINANCIAL CORP | form8k-132368_mvb.htm |

| EX-99.1 - EX-99.1 - MVB FINANCIAL CORP | ex99-1.htm |

1 KBW Community Bank Investor Conference July 31, 2013 MVB Financial Corp. Briefing

2 Forward Looking Statement Certain matters discussed in this presentation that are based on other than historical data are forward - looking within the mean ing of the Private Securities Litigation Reform Act of 1995. Forward - looking statements provide current expectations or forecasts of future events and include, among oth ers: statements with respect to the beliefs, plans, objectives, goals, guidelines, expectations, anticipations, and future financial condition, results of op era tions and performance of MVB Financial Corp. (“the Company”) and its subsidiaries (collectively “we,” “our,” or “us), including MVB Bank, Inc. (the “Bank”); and st ate ments preceded by, followed by or that include the words “may,” “could,” “should,” “would,” “believe,” “anticipate,” “estimate,” “expect,” “intend,” “plan,” “projec ts, ” or similar expressions. These forward - looking statements are not guarantees of future performance, nor should they be relied upon as representing the Company or the Bank management’s views as of any subsequent date. Forward - looking statements involve significant risks and uncertainties and actual results may differ materially from those presented, either expressed or implied, including, but not limited to, those presented in Management’s Discussion and A nal ysis. Factors that might cause such differences include, but are not limited to: the ability of the Company and the Bank to successfully execute its business pla ns, manage its risks, and achieve its objectives; changes in local, national and international political and economic conditions, including without limitation the pol itical and economic effects of the recent economic crisis, delay of recovery from that crisis, economic conditions and fiscal imbalances in the United States and other co untries, potential or actual downgrades in rating of sovereign debt issued by the United States and other countries, and other major developments, includi ng wars, military actions, and terrorist attacks; changes in financial market conditions, either internationally, nationally or locally in areas in which th e C ompany conducts its operations, including without limitation reduced rates of business formation and growth, commercial and residential real estate development and rea l e state prices; fluctuations in markets for equity, fixed - income, commercial paper and other securities, including availability, market liquidity levels, and pr icing; changes in interest rates, the quality and composition of the loan and securities portfolios, demand for loan products, deposit flows and competition; acqui sit ions and integration of acquired businesses; increases in the levels of losses, customer bankruptcies, bank failures, claims, and assessments; changes in fisc al, monetary, regulatory, trade and tax policies and laws, and regulatory assessments and fees, including policies of the U.S. Department of Treasury, the Board of G ove rnors of the Federal Reserve Board System, and the FDIC; the impact of executive compensation rules under the Dodd - Frank Act and banking regulations which may impa ct the ability of the Company, the Bank, and other American financial institutions to retain and recruit executives and other personnel necessary for their bus inesses and competitiveness; the impact of the Dodd - Frank Act and of new international standards known as Basel III, and rules and regulations thereunder, many o f which have not yet been promulgated, on our required regulatory capital and liquidity levels, governmental assessments on us, the scope of business a cti vities in which we may engage, the manner in which the Bank engages in such activities, the fees the Bank may charge for certain products and services, and othe r m atters affected by the Dodd - Frank Act and these international standards; continuing consolidation in the financial services industry; new legal claims against the Company, including litigation, arbitration and proceedings brought by governmental or self - regulatory agencies, or changes in existing legal matters; success i n gaining regulatory approvals, when required; changes in consumer spending and savings habits; increased competitive challenges and expanding product and pricing pr essures among financial institutions; inflation and deflation; technological changes and the Company’s implementation of new technologies; the Compan y’s ability to develop and maintain secure and reliable information technology systems; legislation or regulatory changes which adversely affect the Company’s op era tions or business; the Company’s ability to comply with applicable laws and regulations; changes in accounting policies or procedures as may be required by th e F inancial Accounting Standards Board or regulatory agencies; and, costs of deposit insurance and changes with respect to FDIC insurance coverage levels. Except to the extent required by law, the Company specifically disclaims any obligation to update any factors or to publicly announc e t he result of revisions to any of the forward - looking statements included herein to reflect future events or developments .

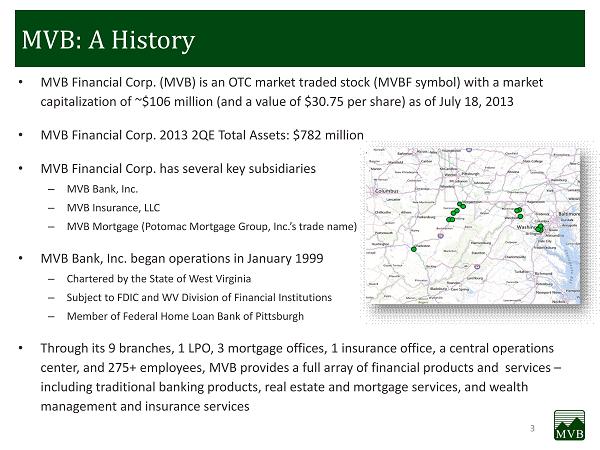

3 MVB: A History • MVB Financial Corp. (MVB) is an OTC market traded stock (MVBF symbol) with a market capitalization of ~$106 million (and a value of $30.75 per share) as of July 18, 2013 • MVB Financial Corp. 2013 2QE Total Assets: $ 782 million • MVB Financial Corp. has several key subsidiaries – MVB Bank, Inc. – MVB Insurance, LLC – MVB Mortgage (Potomac Mortgage Group, Inc.’s trade name) • MVB Bank, Inc. began operations in January 1999 – Chartered by the State of West Virginia – Subject to FDIC and WV Division of Financial Institutions – Member of Federal Home Loan Bank of Pittsburgh • T hrough its 9 branches, 1 LPO, 3 mortgage offices, 1 insurance office, a central operations center, and 275+ employees, MVB provides a full array of financial products and services – including traditional banking products, real estate and mortgage services, and wealth management and insurance services

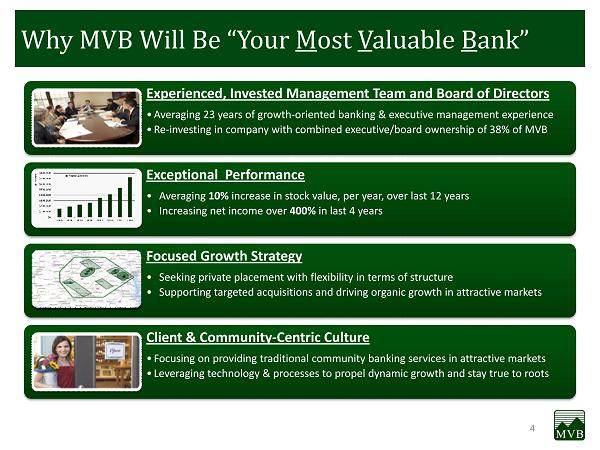

4 Why MVB W ill B e “Your M ost V aluable B ank” Experienced, Invested Management Team and Board of Directors • Averaging 23 years of growth - oriented banking & executive management experience • Re - investing in company with combined executive/board ownership of 38% of MVB Exceptional Performance • A veraging 10% increase in stock value, per year, over last 12 years • Increasing net income over 400% in last 4 years Focused Growth Strategy • Seeking private placement with flexibility in terms of structure • Supporting targeted acquisitions and driving organic growth in attractive markets Client & Community - Centric Culture • Focusing on providing traditional community banking services in attractive markets • Leveraging technology & processes to propel dynamic growth and stay true to roots

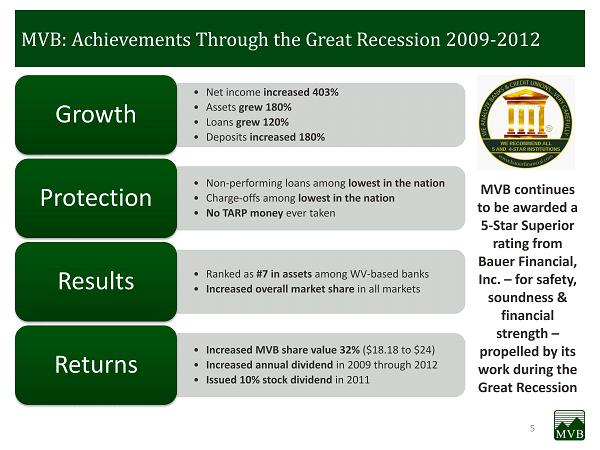

5 • Net income increased 403% • Assets grew 180% • Loans grew 120% • Deposits increased 180% Growth • Non - performing loans among lowest in the nation • Charge - offs among lowest in the nation • No TARP money ever taken Protection • Ranked as #7 in assets among WV - based banks • Increased overall market share in all markets Results • Increased MVB share value 32% ($18.18 to $24) • Increased annual dividend in 2009 through 2012 • Issued 10% stock dividend in 2011 Returns MVB continues to be awarded a 5 - Star Superior rating from Bauer Financial, Inc. – for safety, soundness & financial strength – propelled by its work during the Great Recession MVB: Achievements Through the Great Recession 2009 - 2012

6 MVB Capital Position: Demonstrating Strength Dividend Reinvestment Program (DRIP) showed 46% participation during most recent June 2013 cycle compared to standard USA market average of 10% Steadily Increasing Market Capitalization Demonstrating Strength with Robust Ratios $29 $29 $34 $48 $54 $ 97 $- $10 $20 $30 $40 $50 $60 $70 $80 $90 $100 $110 2008 2009 2010 2011 2012 Q2 2013 Millions End of Year / Quarter

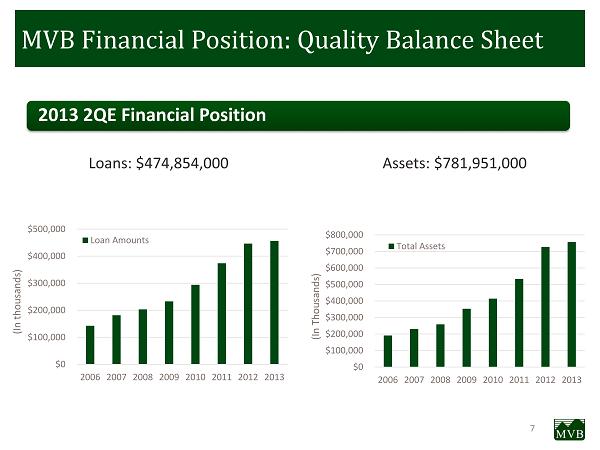

7 Loans : $474,854,000 Assets: $781,951,000 $0 $100,000 $200,000 $300,000 $400,000 $500,000 $600,000 $700,000 $800,000 2006 2007 2008 2009 2010 2011 2012 2013 (In Thousands) Total Assets MVB Financial Position: Quality Balance Sheet $0 $100,000 $200,000 $300,000 $400,000 $500,000 2006 2007 2008 2009 2010 2011 2012 2013 (In thousands) Loan Amounts 2013 2QE Financial Position

8 MVB: Capital Management Disciplined Capital Management Principles • Deploy the most efficient capital model • Focus on balance sheet and non - interest income growth • Target little to no capital dilution • Be ahead of the game by never waiting to raise capital Successful Investment Principles • Focus on near - term accretive acquisitions • Invest in financial services businesses to generate non - interest income • Add talent infusions to support current and future growth

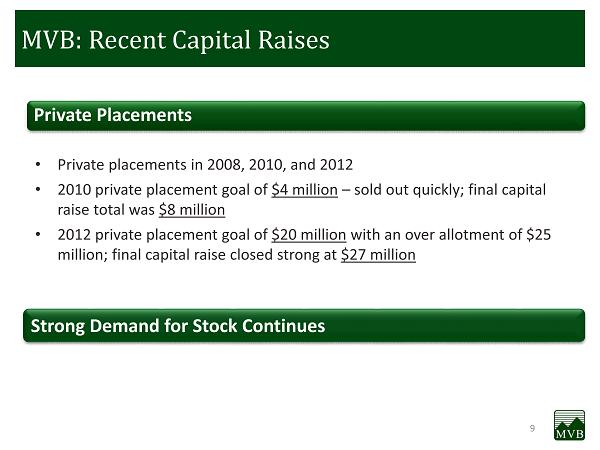

9 MVB: Recent Capital Raises Private Placements • Private placements in 2008, 2010, and 2012 • 2010 private placement goal of $4 million – sold out quickly; final capital raise total was $8 million • 2012 private placement goal of $20 million with an over allotment of $25 million; final capital raise closed strong at $27 million Strong Demand for Stock Continues

10 Performance: MVB / S&P 500 / KBW Bank Index MVB $30,179 10.1% KBW Bank Index $6,972 - 3.1% S&P 500 $13,699 2.8% $- $5,000 $10,000 $15,000 $20,000 $25,000 $30,000 $35,000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 Jun 2013 Value of $10,000 Invested in December 2001 MVB Stock Performance vs. S&P 500 & KBW Bank Index

11 MVB Profile: Strong Growth in Deposits $134,593 $157,448 $173,065 $264,531 $300,434 $390,545 $486,519 $531,338 $0 $100,000 $200,000 $300,000 $400,000 $500,000 $600,000 2006 2007 2008 2009 2010 2011 2012 2Q 2013 Thousands

12 MVB: Deposit Portfolio Profile Net Non - Core Funding is now 13%; down from a high of 19% Demand Deposits 11% Interest - Bearing Demand Deposits 46% Savings & Money Market 10% Time Deposits 20% Brokered Deposits 4% CDARS Deposits 9% 30 - JUNE - 13 Demand Deposits 11% Interest - Bearing Demand Deposits 46% Savings & Money Market 10% Time Deposits 14% Brokered Deposits 7% CDARS Deposits 12% 31 - DEC - 12 Demand Deposits 10% Interest - Bearing Demand Deposits 42% Savings & Money Market 13% Time Deposits 19% Brokered Deposits 7% CDARS Deposits 9% 30 - JUN - 12

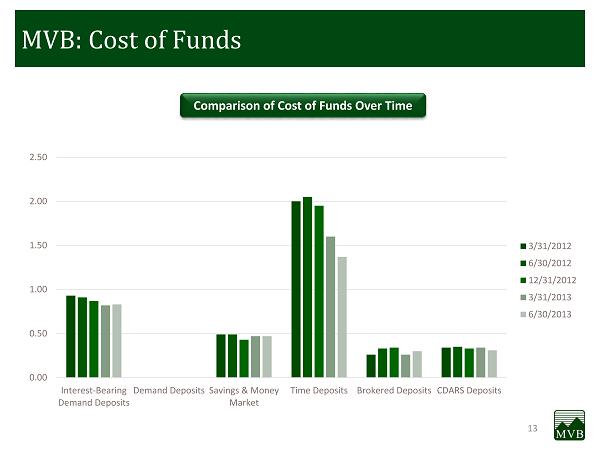

13 MVB: Cost of Funds Comparison of Cost of Funds Over Time 0.00 0.50 1.00 1.50 2.00 2.50 Interest-Bearing Demand Deposits Demand Deposits Savings & Money Market Time Deposits Brokered Deposits CDARS Deposits 3/31/2012 6/30/2012 12/31/2012 3/31/2013 6/30/2013

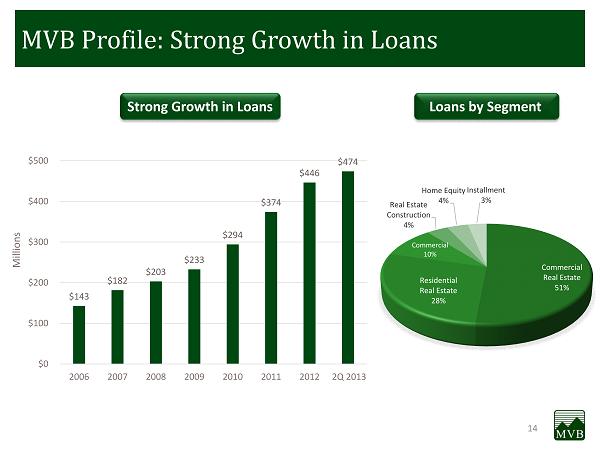

14 MVB Profile: Strong Growth in Loans Loans by Segment Strong Growth in Loans $143 $182 $203 $233 $294 $374 $446 $474 $0 $100 $200 $300 $400 $500 2006 2007 2008 2009 2010 2011 2012 2Q 2013 Millions Commercial Real Estate 51% Residential Real Estate 28% Commercial 10% Real Estate Construction 4% Home Equity 4% Installment 3%

15 $ In Thousands Year End 2010 Year End 2011 Year End 2012 2QE 2013 Loans Past Due 30 - 89 Days $ 2,619 $ 5,125 $ 3,289 $ 5,794 Nonperforming Loans (NPLs) $ 2,791 $ 2,758 $ 3,125 $ 1,358 Real Estate Owned $ 403 $ 176 $ 207 $ 183 Total Nonperforming Assets $ 3,194 $ 2,934 $ 3,332 $ 1,541 Net Charge Offs (Recovery) $ 863 $ 1,156 $ 1,769 $ 914 Loan Loss Reserve Period End $ 2,478 $ 3,045 $ 4,076 $ 4,828 Provision Expense In Period $ 1,100 $ 1,723 $ 2,800 $ 1,666 Reserve/NPLs 89 % 110 % 130% 356% NPA/Total Assets 0.77% 0.55% 0.46% 0.20% Credit Metrics Trends MVB Profile: Credit Metrics Trends

16 MVB Asset Quality: By Business Segment 88% 10% 2% Risk Code 1-4 [614 Loans] Risk Code 5-6 [75 Loans] Risk Code 7-8+ (Includes TDR & Impared) [14 Loans] Commercial Loans 91% 9% 0% Risk Code 1-4 [623 Loans] Risk Code 5-6 [79 Loans] Risk Code 7-8+ (Includes TDR & Impaired) [3 Loans] Mortgage Loans 94% 6% 0% Risk Code 1-4 [954 Loans] Risk Code 5-6 [49 Loans] Risk Code 7-8+ (Includes TDR & Impared) [6 Loans] Installment Loans

17 Larry Mazza, Chief Executive Officer • Brings 27 years of banking sector management – including service in a Big 8 accounting firm and executive management roles – and possesses CPA credentials • Named CEO of MVB Financial Corp. in 2009 (after shepherding growth for MVB Bank – Central and East – beginning in 2005) • Named President of Empire National Bank at age 29 and served as Regional President of One Valley Bank (acquired by BB&T) • Served as Retail Banking Manager for BB&T’s WV North Region (which included 33 financial centers and 300 employees, held $2 billion in assets, and was ranked #1 in regional performance) • Delivers public company corporate governance experience from service on board of directors of PDC Energy, Inc. (NASDAQ:PDCE) • Delivers 33 years experience in banking with specialty in commercial lending • Named President of MVB Financial Corp. in 2010 • Works as Senior Commercial Lending Officer overseeing the commercial lending division of MVB Bank • Served as marketing and leasing representative with General Electric Credit Corporation Roger Turner, President MVB Executives: Experienced Leadership Don Robinson, Chief Operating Officer • Brings 16 years of banking and financial institution experience – including service in a Big 8 accounting firm, management roles for public companies, and as an M&A advisor – and possesses CPA credentials • Named Chief Operating Officer of MVB Financial Corp. in 2012 • Named as Regional President for MVB North in 2011 • Served as Market President and Commercial Regional head with Huntington Bancshares, Inc. • Served as EVP and Chief Accounting Officer of Linn Energy, Inc. (NASDAQ:LINE), a publicly traded oil and gas company • Advised multiple companies on over 20 M&A transactions Ed Dean, CEO – MVB Mortgage • Brings 22 years of mortgage & banking experience • Leads subsidiary, MVB Mortgage, a DBA of Potomac Mortgage Group, Inc. (PMG), which he co - founded and led from 2005 to acquisition in 2012 • Helped lead George Mason Mortgage, which was acquired by United Bank and, subsequently, Cardinal Bank • Started career with Empire National Bank working for Empire’s CEO, Larry Mazza (who is now MVB’s CEO) over 20 years ago

18 John Schirripa, Regional President • Brings 26 years banking experience • Serves as Executive Vice President for President and CEO of MVB Bank Inc. - Central • Leads the MVB Central Commercial Lending Team • Served as Vice President and Relationship Manager with Chase • Served as Senior Vice President/Community President of Huntington National Bank MVB Executives: Strong Domain Expertise David Jones, Chief Credit Officer • Brings 25 years banking experience including commercial lending experience and an emphasis on credit analysis & quality performance of loans • Serves as Chief Credit Officer of MVB Bank, Inc. and coordinates its enterprise risk management program • Has background in accounting and bank auditing from Big 8 firm • Worked at other banking institutions including Huntington National Bank and BB&T Eric Tichenor, Chief Financial Officer • Brings 22 years of banking experience • Named as MVB Bank’s Chief Financial Officer in 2008 and also serves as Chief Financial Officer at MVB Financial Corp. • Was a founding member of the MVB Bank Team • Served in financial and accounting roles for CB&T and Huntington Bancshares, including being responsible for accounting functions of 42 branch offices in WV Patrick Esposito, Chief Risk Officer & General Counsel • Brings 13 years of executive & legal experience • Serves as Vice President, Corporate Development, Project Management, Vendor Management, Chief Risk Officer & General Counsel of MVB Financial Corp. & MVB Bank Inc. • Served as Chief Executive Officer of Augusta Systems, Inc., an Inc. 500 company, and led company to acquisition by Intergraph Corp. • Served as co - founder and board member responsible for M&A for Resilient Technologies, LLC, which was acquired by Polaris Industries (NYSE: PII) • Served as deputy general counsel in the Office of the West Virginia Governor

19 Executive Management Team Members MVB Position(s) Years Ownership Shares and (%) (includes all stock options granted) Banking/Finance/ Management MVB Team Larry Mazza, 52 * Chief Executive Officer, MVB Financial President & Chief Executive Officer, MVB Bank 27 8 186,637 Roger Turner, 61 * President, MVB Financial Executive VP, Sr. Commercial Loan Officer, MVB Bank 33 8 71,672 Don Robinson, 38 Executive Vice President & Chief Operating Officer , MVB Financial & MVB Bank 16 2 31,429 Ed Dean , 44 * President & Chief Executive Officer, MVB Mortgage 22 4 91,826 John Schirripa, 50 Executive VP, Regional President, MVB Bank 29 3 39,556 Eric Tichenor, 44 Senior VP, Chief Financial Officer, Bank Internal Operations & Treasurer, MVB Financial & MVB Bank 22 14 27,188 Patrick Esposito, 39 VP, Corporate Development, Chief Risk Officer & General Counsel, MVB Financial and MVB Bank 13 <1 13,000 David Jones, 50 Senior VP, Chief Credit Officer, MVB Bank 26 8 36,675 Total Executive Management: 188 years experience 497,983 (15%) Board Equity: 1,104,220 (34%) * Board of Directors Member Total Executive Management & Board Equity**: (**Some Executive Management Members are also Board Members; Total does not duplicate share counts) 1,212,512 (38%) Executives & Board: Invested in Success

20 Interest - based Growth: Organic • Increasing productivity with existing team • Expanding geographic footprint through new bank locations to increase loans & deposits Interest - based Growth: M&A • Acquiring full banks in existing and new markets • Acquiring select branches in existing and new markets Non - interest Income Growth: Organic and/or M&A • Adding insurance offerings and producers • Increasing wealth management offerings • Adding strong new producers to mortgage team MVB Strategy: Growth & Diversification

21 Organic Successes: Core Banking Growth Expanded into Morgantown, WV in Q2 2011 • First Morgantown branch profitable three quarters after opening • Second Morgantown branch opened in March 2013 • $60 million in deposits at Morgantown branches as of 7/15/13 Opened first Clarksburg, WV branch in Q4 2012 • $16 million in deposits in Clarksburg within first two quarters

22 Organic Success: MVB Insurance Initiated operations in 2007 with focus on title insurance Closed 2012 with 3 employees focused on title insurance and ~$200,000 in annual revenue Added 16 new employees in Q1 and Q2 2013, including new seasoned leadership and team members from Wells Fargo, Huntington & smaller regional firms Bolstered insurance offerings to add commercial property and casualty, employee benefits, professional liability, and personal lines Expanded carriers including Chubb, Hartford, SAFECO, Travelers, and Zurich, among others Signed new clients to increase revenue to ~$2.5M (with more to come)

23 Drives Shareholder Value Asset Quality Deposits Geographic Growth in Attractive Markets Addition Growth Potential Cultural Fit Talent & New Expertise MVB M&A Growth: Selective & Strategic • Conducting Disciplined Deal - making: M&A deals will be rooted in a reasonable transaction price – based upon asset quality and deposits – and must demonstrate a true value for MVB shareholders • Focusing on the Right T argets : Strategic opportunities in West Virginia and other key states – with a focus on Virginia and Pennsylvania – targeting attractive markets with growth opportunities to increase MVB value • Growing and Cultivating a Strong Team: M &A must ensure perpetuation of MVB culture, while also infusing complementary talent to the existing MVB team and, if possible, deliver new expertise to enhance growth opportunities M&A Assessment Model

24 • Potomac Mortgage Group ( PMG ), direct residential mortgage lender, was acquired by MVB in December 2012 • Based in Fairfax, VA with lending in VA, MD, WV, DE and DC with sales offices in Reston, Fairfax, and McLean, VA and a joint venture loan operations center in Alabama • Top 100 USA Mortgage Companies (2011) • Roughly $800 million in annual production • Annual net income of $4.5 million for nine months ended September 30, 2012 • 100 % of originations are sold with average mortgage loans at $390,000 and average FICO 756 and average LTV 80 % • Current markets have over 7 million people • Rebranded as MVB Mortgage on July 15, 2013 • Is immediately accretive to all shareholders • Increases net income and earnings per share • Increases non - interest income opportunity with declining NIM • Projects to potentially increase MVB year - over - year earnings by over 50% by YE 2013 • Supports entry into attractive Northern Virginia market and positions future opportunity to cross - sell MVB products and services in this market • Decreases MVB’s concentration risk • Enhances MVB mortgage practice through efficiency gains in mortgage underwriting and sales , increase in servicing income and escrow deposits, and improved pricing of existing mortgage portfolio M&A Success: MVB Mortgage (formerly PMG) Business Summary Benefits to MVB Shareholders

25 MVB Growth: Targeting Attractive Markets • Features West Virginia University, major health care centers, and growing private sector ( Mylan , etc.) • Serves as hub for Marcellus & Utica energy production plays • Offers US government facilities (DOE, FBI, DOD, etc.) North Region: Morgantown, Fairmont, Bridgeport & Clarksburg • Features high - growth economic region with leading US household income & lowest MSA unemployment • Offers large 5.7 million person market opportunity • Leverages, in Northern Virginia, presence of MVB subsidiary, Potomac Mortgage Group East Region: Martinsburg & Charles Town, WV + Northern Virginia locations • Features WV State Capitol, large health care center, and strong natural resource sector • Features largest deposit base in WV ($4.2B) • Limited community bank presence in market South Region: Charleston • Focuses on most attractive, high - growth markets in expanded Mid - Atlantic region • Key potential targets: Expanded Northern Virginia footprint, western Virginia, southwestern Pennsylvania, and other West Virginia markets New Markets: Virginia, Pennsylvania & Other Areas

26 MVB Markets: Today & Tomorrow Current & Pending Markets • North Region – Morgantown (2) – Fairmont (2 w/ 1 replacement pending) – Bridgeport – Clarksburg • East Region – Charles Town – Martinsburg (2) – MVB Mortgage (mortgage only) o Fairfax (currently mortgage only ) o McLean (currently mortgage only) o Reston ( currently mortgage only ) • South Region – Charleston (LPO only + 1 pending) Future Markets • Key Growth Markets • Expansion Markets • Strategic Market Focus

27 Summary: Why Invest in MVB? Experienced Management Team & Board of Directors • Delivers one of the most experienced leadership teams in our markets • Features team with significant holdings & interests that are aligned with shareholders Client & Community - Centric Culture • Focusing on providing traditional community banking services in attractive markets • Leveraging technology & processes to propel dynamic growth and stay true to roots Focused Growth Strategy • Propelling organic growth in existing, strong markets with team, approach & practices • Executing targeted acquisitions to drive growth in attractive markets – current & new Exceptional Performance • Features strong record of growth and stewardship approach to capital management • Net income set to increase 50% year - over - year in 2013 with accretive acquisitions

28 A Great Story Today… with excellent performance during the Great R ecession, the advent of Basel III, a slowly improving economy and the enforcement of Dodd - Frank, many financial holding companies, bank holding companies, and banks will fall victim to regulatory issues, which will be an opportunity for MVB . We are strong, profitable, growth - oriented & well capitalized with an outstanding team. With The Best Yet T o Come! Final Thoughts & Contact Information For more i nformation, please contact: Larry Mazza Don Robinson Patrick Esposito Chief Executive Officer Chief Operating Officer VP, Corp. Dev. & General Counsel lmazza@mvbbanking.com drobinson@mvbbanking.com pesposito@mvbbanking.com 304.657.0396 304.685.4933 304.282.8876

29 This Presentation has been prepared solely for information purposes and to assist prospective investors who receive this Pres ent ation (the “Recipients”) in deciding whether to proceed with a further investigation of MVB Financial Corp. Under no circumstances shall th is Presentation be deemed or construed to be an offer to sell or the solicitation of an offer to buy any securities, and it is n ot intended to be the basis of any invest investment decision or any decision to invest in MVB Financial Corp. The contents of this Presentation ar e c onfidential and proprietary to MVB Financial Corp. MVB Financial Corp does not make any representation or warranty, expressed or implied, as to the accuracy or completeness of thi s Presentation and shall not have liability for any omission from this Presentation or any other written or oral communications tr ansmitted to any Recipient heretofore or in the course of his or her evaluation of MVB Financial Corp. No liability is or will be accepted , b y MVB Financial Corp. or its officers, direct directors, employees, or agents as to, or in relation to, the accuracy or completeness of this Presen tat ion or any other written or oral information transmitted to any Recipient regarding MVB Financial Corp., and any liability therefore is hereby expressly disclaimed. Delivery of this Presentation shall not, under any circumstance, create any implication that the information cont ain ed herein is correct or complete. This presentation contains certain statements, estimates and projections made by MVB Financial Corp. with respect to the anticipated future performance of MVB Financial Corp. Such statements, estimates and projections reflect various assumptions concerning anticipa ted results, which assumptions may or may not prove to be correct. No representations or warranties are made as to the accuracy or such st ate ments, estimates or projections. The only information that will have any legal effect will be that specifically represented or warra nte d in a Confidential Offering Memorandum tailored to the proposed transaction and any Subscription Agreement relating to that transaction that may be entered into among potential invest investors in such transaction; in no event will either such Confidential Offering Memorandum or S ubs cription Agreement contain any representation or warranty as to projections. This Presentation is for distribution only to persons rea son ably believed to have sufficient expertise to understand the risks involved. For additional information, please contact: Larry Mazza, CEO, MVB Financial Corp. 301 Virginia Avenue, Fairmont, WV 26554 Disclaimer