Attached files

| file | filename |

|---|---|

| EX-4.1 - EX-4.1 - Lipocine Inc. | d562293dex41.htm |

| EX-3.2 - EX-3.2 - Lipocine Inc. | d562293dex32.htm |

| EX-2.1 - EX-2.1 - Lipocine Inc. | d562293dex21.htm |

| EX-3.1 - EX-3.1 - Lipocine Inc. | d562293dex31.htm |

| EX-3.3 - EX-3.3 - Lipocine Inc. | d562293dex33.htm |

| EX-10.1 - EX-10.1 - Lipocine Inc. | d562293dex101.htm |

| EX-99.1 - EX-99.1 - Lipocine Inc. | d562293dex991.htm |

| EX-10.5 - EX-10.5 - Lipocine Inc. | d562293dex105.htm |

| EX-10.2 - EX-10.2 - Lipocine Inc. | d562293dex102.htm |

| EX-10.3 - EX-10.3 - Lipocine Inc. | d562293dex103.htm |

| EX-10.8 - EX-10.8 - Lipocine Inc. | d562293dex108.htm |

| EX-21.1 - EX-21.1 - Lipocine Inc. | d562293dex211.htm |

| EX-23.1 - EX-23.1 - Lipocine Inc. | d562293dex231.htm |

| EX-99.2 - EX-99.2 - Lipocine Inc. | d562293dex992.htm |

| EX-10.4 - EX-10.4 - Lipocine Inc. | d562293dex104.htm |

| EX-10.7 - EX-10.7 - Lipocine Inc. | d562293dex107.htm |

| EX-10.9 - EX-10.9 - Lipocine Inc. | d562293dex109.htm |

| EX-99.3 - EX-99.3 - Lipocine Inc. | d562293dex993.htm |

| EX-10.6 - EX-10.6 - Lipocine Inc. | d562293dex106.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): July 24, 2013

Lipocine Inc.

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 333-178230 | 99-0370688 | ||

| (State of Incorporation) | (Commission File Number) |

(IRS Employer Identification No.) |

675 Arapeen Drive, Suite 202

Salt Lake City, Utah 84108

(Address of principal executive offices)

Registrant’s telephone number, including area code: (801) 994-7383

Marathon Bar Corp.

427 N. Tatnall Street

Wilmington, DE 19801-2230

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ¨ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Table of Contents

i

Table of Contents

Statements in this Current Report on Form 8-K that are not descriptions of historical facts are forward-looking statements that are based on management’s current expectations and are subject to risks and uncertainties that could negatively affect our business, operating results, financial condition and stock price. We have attempted to identify forward-looking statements by terminology including “anticipates,” “believes,” “can,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “should,” “will,” “would” or the negative of these terms or other comparable terminology. Factors that could cause actual results to differ materially from those currently anticipated include those set forth in the section titled “Risk Factors” including, in particular, risks relating to:

| • | the results of research and development activities; |

| • | uncertainties relating to preclinical and clinical testing, financing and strategic agreements and relationships; |

| • | the early stage of products under development; |

| • | our need for substantial additional funds; |

| • | government regulation; |

| • | our ability to obtain and maintain regulatory approval of our lead product candidate, LPCN 1021, and any of our other future product candidates, and any related restrictions, limitations, and/or warnings in the label of any approved product candidate; |

| • | our ability to obtain funding for our operations; |

| • | our ability to retain or hire key scientific or management personnel; |

| • | patent and intellectual property matters; |

| • | dependence on third-party manufacturers, suppliers, research organizations, and testing laboratories; and |

| • | competition. |

These forward-looking statements are subject to a number of risks, uncertainties and assumptions, including those described in the section titled “Risk Factors.” Moreover, we operate in a very competitive and rapidly-changing environment. New risks emerge from time to time. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. In light of these risks, uncertainties and assumptions, the forward-looking events and circumstances discussed in this prospectus may not occur and actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements. You should not rely upon forward-looking statements as predictions of future events. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee that the future results, levels of activity, performance or events and circumstances reflected in the forward-looking statements will be achieved or occur. Moreover, except as required by law, neither we nor any other person assumes responsibility for the accuracy and completeness of the forward-looking statements. We undertake no obligation to update publicly any forward-looking statements for any reason after the date of this prospectus to conform these statements to actual results or to changes in our expectations.

1

Table of Contents

ITEM 1.01 ENTRY INTO A MATERIAL DEFINITIVE AGREEMENT

On July 24, 2013, Marathon Bar Corp., a Delaware corporation, MBAR Acquisition Corp., a Delaware corporation and a wholly-owned subsidiary of Marathon Bar, or Merger Sub, and Lipocine Operating Inc., a Delaware corporation, entered into an Agreement and Plan of Merger and Reorganization, or the Merger Agreement. Pursuant to the Merger Agreement, Merger Sub merged with and into Lipocine Operating, and Lipocine Operating was the surviving corporation of the transaction, or the Merger. Following the closing of the Merger, Lipocine Operating became a wholly-owned subsidiary of Marathon Bar, with the former stockholders of Lipocine Operating owning 99.9% of the outstanding shares of common stock of the combined company.

Prior to the execution and delivery of the Merger Agreement, the board of directors of Marathon Bar approved the Merger Agreement and the transactions contemplated thereby. Similarly, the board of directors of Lipocine Operating approved the Merger Agreement. On July 24, 2013, immediately prior to the execution and delivery of the Merger Agreement, Marathon Bar amended its certificate of incorporation to change the name of Marathon Bar to “Lipocine Inc.” Prior to the execution and delivery of the Merger Agreement, Lipocine had changed its name to “Lipocine Operating Inc.”

The Merger closed concurrently with the execution and delivery of the Merger Agreement. Reference is hereby made to Item 2.01 regarding the completion of the Merger.

As used in this Current Report on Form 8-K, (1) all references to the “Combined Company” refer to Marathon Bar (renamed Lipocine Inc.) and its subsidiaries, including Lipocine (renamed Lipocine Operating Inc.), following the closing of the Merger, and (2) unless the context otherwise indicates or requires, all references to “we,” “our” and “us” refer to the Combined Company from and after the closing of the Merger.

ITEM 2.01 COMPLETION OF ACQUISITION OR DISPOSITION OF ASSETS

On July 24, 2013, Marathon Bar and Lipocine Operating closed the Merger. On July 24, 2013, immediately prior to the execution and delivery of the Merger Agreement, Marathon Bar amended its certificate of incorporation to effect a 100–for-1 reverse stock split, resulting in 35,000 outstanding shares of common stock and the board of directors of Marathon Bar declared a $8.00 per share cash dividend to its stockholders of record. Following the completion of the above actions, Marathon Bar repurchased 30,000 shares (on a post split basis) at a price of $1.16 per share from its principal stockholder, Israel Menahem Vizel. At the closing of the Merger, Marathon Bar issued 4,702,713 shares of common stock to the former stockholders of Lipocine Operating in exchange for all the outstanding shares of capital stock of Lipocine Operating. In addition, Marathon Bar assumed the Lipocine Operating 2011 Equity Incentive Plan and the obligation to issue shares pursuant to outstanding equity awards thereunder and pursuant to an outstanding warrant.

Background; Form 10 Information Requirements

Marathon Bar was incorporated on October 13, 2011, in the State of Delaware. A registration statement on Form S-1 (File No. 333-178230) was declared effective by the Securities and Exchange Commission, or the SEC, on February 13, 2012. In April 2012, Marathon Bar sold 5,000 shares of common stock (on a post split basis) under the Form S-1 for aggregate gross proceeds of $50,000. Prior to the Merger, Marathon Bar intended to create a fully functional website (www.m-bar.co) with updates as to health-related events to occur in Israel and post free organic recipes as a way to attract individuals to choose to purchase organic health bars. Marathon Bar secured the web domain and the current website was a template of what was expected to further develop. The website was still under construction. Marathon Bar expected to generate revenue by selling its organic health bars at local sporting events, through health stores; and over its website. In the fourth quarter of 2012, Marathon Bar completed the design of its graphic/web design materials for use as part of its advertising and promotional materials. Marathon Bar had not yet found a third party manufacturer, but has traveled to Europe to meet with potential manufacturers.

Marathon Bar is a “shell company,” as such term is defined in Rule 12b-2 under the Securities Exchange Act of 1934, or the Exchange Act. Accordingly, pursuant to the requirements of Item 2.01 of Form 8-K, this Item 2.01 sets forth the information that would be required if the Combined Company were filing a general form for registration of a class of securities on Form 10 under the Exchange Act, with such information reflecting the

2

Table of Contents

Combined Company and its securities upon consummation of the Merger. The Combined Company intends to carry on the business of Lipocine. As a result of closing the Merger, our executive office is the Salt Lake City, Utah office of Lipocine.

Accounting Treatment of the Merger

The Merger is being accounted for as a reverse-merger and recapitalization. Lipocine is the acquirer for financial reporting purposes and Marathon Bar is the acquired company. Consequently, the assets and liabilities and the operations that will be reflected in the historical financial statements prior to the Merger will be those of Lipocine and will be recorded at the historical cost basis of Lipocine, and the consolidated financial statements after completion of the Merger will include the assets and liabilities of Marathon Bar and Lipocine, and the historical operations of Lipocine and operations of the Combined Company from the closing date of the Merger.

Tax Treatment; Smaller Reporting Company

The Merger is intended to constitute a tax free reorganization within the meaning of the Internal Revenue Code of 1986. Following the Merger, the Combined Company continues to be a “smaller reporting company,” as defined in Item 10(f)(1) of Regulation S-K, as promulgated by the SEC.

Business

General

We are a specialty pharmaceutical company. Our proprietary delivery technologies are designed to improve patient compliance and safety through orally available treatment options. Our primary development programs are based on oral delivery solutions for poorly bioavailable drugs, which are drugs that are poorly absorbed and reach the circulatory system in insufficient amounts. We have a portfolio of proprietary product candidates designed to produce favorable pharmacokinetic characteristics and facilitate lower dosing requirements, bypass first-pass metabolism, reduction of side effects, and elimination of gastrointestinal interactions that limit bioavailability. Our lead product LPCN 1021 is a Phase III ready oral testosterone replacement therapy, or TRT, product designed for convenient twice-a-day dosing. Additionally, we have two earlier stage product candidates in our pipeline, a next generation oral testosterone therapy (LPCN 1111) and an oral product candidate for the prevention of preterm birth (LPCN 1107).

“Lipocine,” “Lip’ral,” the Lipocine logos and other trademarks or service marks of Lipocine appearing in this Current Report on Form 8-K are our property. This Form 8-K contains additional trade names, trademarks and service marks of others, which are the property of their respective owners. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, these other companies.

Industry

Testosterone Background

Testosterone, or T, is the primary circulating sex hormone in males and is critical to the development and maturation of reproductive tissues as well as other secondary male characteristics such as muscle growth and bone density. Developed in the gonads of both males (testis) and females (ovaries), testosterone circulates bound to sex hormone binding globulin (SHBG, ~60%), loosely bound to albumin (~40%), or as a free molecule (~1%). Once circulating, testosterone enters cells directly and activates a network of proteins that ultimately result in metabolic conversions, which in turn produce phenotypic effects. The concentration of circulating testosterone can vary drastically over time or between individuals and can be dependent on genetic factors, medical comorbidities, lifestyle behaviors, and/or concurrent medication administration. Although this large variability exists, the effects of testosterone are also determined by a number of factors including the amount of steroid penetration, sensitivity of enzymes and cellular proteins to the hormone, and the action of genomic receptors at the cellular level. As a result, assessing clinically low, or potentially high, levels of endogenous testosterone often requires a number of quantitative tests in conjunction with clinical evaluations.

3

Table of Contents

Hypogonadism Overview

Low serum testosterone causes significant clinical impact and can result in erectile dysfunction, low libido, decreased muscle mass and strength, increased body fat, decreased bone density, decreased vitality and depressed mood. Furthermore, low serum testosterone concentrations have been found to be an independent predictor of a number of cardiovascular risk factors including obesity, dyslipidemia, hypertension, type 2 diabetes, and systemic inflammation. Well-designed, prospective clinical trials have determined that low testosterone levels are also independently associated with mortality risk. These findings have generated interest amongst the medical community and general public regarding the importance of maintaining appropriate serum testosterone levels, which has stimulated growth of the testosterone replacement therapy market.

Hypogonadism typically refers to a permanent deficiency of sex hormones rather than a temporary deficiency that may be related to acute/chronic illnesses or other medical, personal, or environmental factors. Primary hypogonadism describes disease states that intrinsically affect the gonads. Examples of these include the genetic disorders Turner syndrome and Kleinfelter syndrome. Secondary hypogonadism refers to disease states that affect gonadal-related structures such as the hypothalamus and pituitary gland that directly impact the development of gonads and as such the release of testosterone and other sexual hormones. Kallmann syndrome, in which patients fail to undergo all of the changes associated with puberty, is a type of secondary hypogonadism. Although a number of inherited diseases are known to affect the gonads either directly or indirectly, these cases are rare and comprise a minority of treatable cases of hypogonadism. The overwhelming majority of individuals with hypogonadism develop the condition as a result of age-related declines in testosterone or other acquired conditions.

Diagnosis and Treatment of Hypogonadism

Epidemiological studies have determined that total testosterone follows an age-related decline with mean serum concentration at the age of 75 years approximately two thirds that at 25 years. Because endogenous testosterone exists at low concentrations, with normal testosterone levels in the range of 300 to 1140ng/dL, automated platform-based assays have been found to lack specificity and are prone to inter-lab variability. The lack of reliable laboratory tests is complicated further by the inter-individual variability seen in an unaffected population. Thus, in order to accurately diagnose hypogonadism in a male, multiple morning serum testosterone levels are performed in conjunction with a clinical assessment of patient symptoms. Patients can only be diagnosed when they present with symptomatology that is directly related to more than one low morning serum testosterone level.

The treatment for male hypogonadism (both primary and secondary) is testosterone replacement therapy. The benefits of testosterone replacement therapy include improved libido, sexual function, increased bone density, muscle development, and cognition, as well as a reduction in other risk factors caused by low testosterone. Although there are some adverse effects associated with the use of testosterone replacement, the benefits generally far outweigh the risks in patients being treated for hypogonadism.

Testosterone Replacement Market

Due to the wide variability in therapeutic range, difficulty of diagnosis, and co-morbid conditions that may confound an accurate diagnosis, there is a consensus that male hypogonadism is significantly undertreated. A large study of 2,162 men over the age of 45 visiting primary care practices in the United States revealed that the prevalence of hypogonadism is about 39%. This correlates to approximately 14 million patients in this age group. In the study, fewer than 4% of patients were receiving treatment for hypogonadism.

Testosterone replacement therapies have been commercially available in the United States for over 70 years and have followed a progression of delivery systems that included subcutaneous, or under-the-skin, intramuscular, transdermal patch, and finally topical gels, which initially surfaced in 1999. The difficulty in creating an easy to use/administer and clinically effective testosterone therapy is related to the molecule’s complex pharmacokinetics. For example, oral therapies, which would ideally be the most popular route of delivery, require multiple, high daily doses due to low bioavailability. Additionally, the few oral therapies that were used in the United States quickly went out of favor after significant side effects were revealed, most notably hepatotoxicity.

4

Table of Contents

Currently, the U.S. testosterone replacement market consists of therapies that exist in three forms:

| • | gel/patch; |

| • | injectable; and |

| • | buccal tablet. |

Although transdermal patches were previously the most desirable application type, gel-based testosterone replacement therapies have gained increasing popularity due to improved skin tolerability. Despite becoming the most popular approach to male hypogonadism treatment, topical gels are not without limitations. Topical gels place women and children at risk of testosterone transference (secondary exposure to gels), which has prompted the U.S. Food and Drug Administration, or FDA, to add black box warnings relating to testosterone transference in the label of approved topical products. Despite these limitations, gels have continued to demonstrate significant market penetration and show no signs of slowing; 67% of total prescriptions and 89% of the total value of the testosterone replacement market in 2012 were accounted for by gels.

According to Global Industry Analyst Inc., the male testosterone market was more than $2 billion in 2012, and it is expected to grow very rapidly to $5 billion by 2017, a compound annual growth rate above 20%. Gels are the dominant dosage form in this market, with about 89% of revenue in this segment derived from these products in 2012. The exponential growth is likely driven by increasing recognition by both patients and providers of the prevalence of hypogonadism and its far-reaching medical consequences. Top treatments are marketed by AbbVie, Eli-Lilly, and Auxilium.

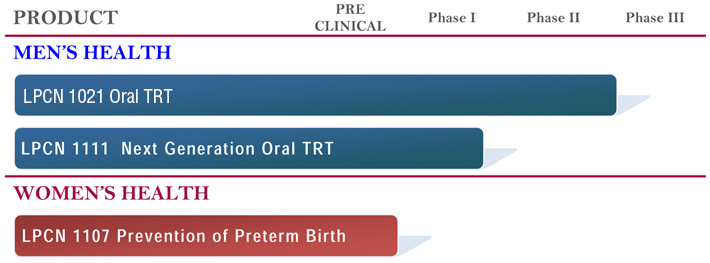

Product Candidates

Our current portfolio, shown below, includes our lead product candidate LPCN 1021, an oral testosterone replacement therapy, which we plan will soon enter a Phase III study. Additionally, we are currently in the process of establishing our pipeline of early clinical treatments including next generation testosterone replacement therapy (LPCN 1111) and an oral therapy for the prevention of preterm birth (LPCN 1107).

Our Development Pipeline

These products are based on our proprietary Lip’ral promicellar drug delivery technology platform. Our Lip’ral promicellar technology is a patented delivery system based on lipidic compositions for hydrophobic, or

5

Table of Contents

water insoluble, molecules which form an optimal dispersed phase in the gastrointestinal tract for improved absorption of insoluble drugs. Lip’ral presents insoluble drugs efficiently to the intestinal absorption site, thus bringing the absorption process under formulation control and making the product robust to physiological variables such as dilution, pH and food effects. Lip’ral enables improved solubilization and higher drug-loading capacity, which can lead to improved bioavailability, reduced dose, faster and more consistent absorption, reduced variability, reduced sensitivity to food effects, improved patient compliance, and targeted lymphatic delivery.

LPCN 1021: An Oral Product Candidate for Testosterone Replacement Therapy

LPCN 1021 is an oral formulation of the chemical testosterone undecanoate, an ester prodrug of testosterone designed for convenient twice daily dosing. The active ingredient has been approved for use outside the United States for decades for delivery via intra-muscular injection and in oral dosage form. However, this oral dosage form which is approved outside the United States provides sub-therapeutic serum testosterone levels at the approved dose. We are using our Lip’ral technology to facilitate steady gastrointestinal solubilization and absorption of the testosterone undecanoate, or TU. Proof of concept was initially established in 2006, and subsequently LPCN 1021 was licensed to Solvay Pharmaceuticals, Inc., or Solvay, which was then acquired by Abbott Products, Inc., or Abbott, in 2009. Following a portfolio review associated with the spin-off of AbbVie by Abbott in 2011, the rights to LPCN 1021 were reacquired by us. A review of the milestones and history of this development program is shown below.

LPCN 1021 Development History

| Date |

Milestone | |

| February 2006 |

First proof of concept study performed | |

| May 2009 |

Licensed to Solvay | |

| September 2009 |

Project transferred to Abbott via Solvay | |

| April 2010 |

Milestone payment received | |

| May 2011 |

Milestone payment received | |

| October 2011 |

Abbott announced spin-off of AbbVie | |

| March 2012 |

Lipocine re-acquires LPCN 1021 | |

| November 2012 |

Lipocine completes meeting with FDA to define requirements for an NDA filing | |

Clinical Data Discussion

We completed a successful Phase II study that produced results in line with FDA guidelines for approval of testosterone replacement therapies. The primary outcome of the trial, average serum testosterone levels in the eugonadal, or endocrinologically normal, range (300 – 1140 ng/dL), was met and there were no significant adverse events or unexpected changes in serum lipid profiles or liver enzymes. We presented the results of this study and a Phase III protocol synopsis to the FDA in November 2012 and obtained clear guidance on the requirements for a LPCN 1021 NDA filing, with no additional pre-clinical studies required. The FDA has indicated that only one pivotal Phase III trial may be necessary for the LPCN 1021 NDA filing. We intend to begin enrolling patients in the Phase III trial in the fourth quarter of 2013, with final results expected in 2015.

Phase II Study

The Phase II study for LPCN 1021 enrolled 84 hypogonadal men across five parallel groups. Four doses were used, starting at 75 mg and increasing to 150, 225, and then 300 mg to determine the effective dose for producing serum testosterone levels in the eugonadal range. Groups I through III received 75 mg, 150 mg, and 225 mg doses, respectively. The study duration was 15 days and doses were administered twice daily, 30 minutes after breakfast and dinner. Full (24 hour) pharmacokinetic profiles were taken the day prior to the first dose (day 0), day 1, day 8, and day 15. Groups IV and V received 300 mg and 225 mg doses respectively and the study duration was 29 days. In these two groups also the doses were administered twice daily 30 minutes after breakfast and dinner. Full pharmacokinetic profiles were obtained on day 0, day 15, and day 29. In this cohort, morning pharmacokinetic profiles were also obtained on days 8 and 22.

6

Table of Contents

The FDA criteria for approval of a TRT include successful completion of a pivotal Phase III trial meeting two primary endpoints and three secondary endpoints. Primary endpoints include 24-hour average serum testosterone levels between 300 and 1140ng/dL in at least 75% of patients, and the lower bound of the 95% confidence interval in at least 65% of patients. Secondary endpoints include a maximum serum testosterone level less than 1500 ng/dL in at least 85% of patients, maximum serum testosterone level between 1800 to 2500 ng/dL in £ 5% of patients, and no patients who experience maximum serum testosterone greater than 2500 ng/dL.

The 225 mg twice-a-day dose met all the primary and secondary endpoints required for approval of a TRT product. These requirements along with the results for the 225 mg group on day 15 are outlined in the table below.

FDA Requirements for TRT Approval and LPCN 1021 Phase II Results

| FDA Criteria for Approval of TRT |

LPCN 1021 Phase II Result |

|||||||

| Dose |

225 mg | |||||||

| Number of subjects |

24 | |||||||

| Primary endpoints |

||||||||

| Cave 300-1140ng/dL |

³ 75 | % | 83 | % | ||||

| Lower bound 95% CI |

³ 65 | % | 69 | % | ||||

| Secondary endpoints |

||||||||

| Cmax < 1500ng/dL |

³ 85 | % | 88 | % | ||||

| Cmax 1800-2500ng/dL |

£ 5 | % | 0 | % | ||||

| Cmax > 2500ng/dL |

0 | % | 0 | % | ||||

There was no dose titration in the Phase II study. Prior to any dose titration which is typical in TRT, the optimal dose was found to be 225 mg of testosterone undecanoate dosed twice-a-day, which met the FDA’s stated requirements for a successful Phase III trial. Additionally, there were no major clinical adverse events or significant changes in liver enzymes. The other key safety parameters, the ratio of dihydrotestosterone, or DHT, to T, and changes in estradiol, low-density lipoprotein, or LDL, high-density lipoprotein, or HDL, and prostate-specific antigen, or PSA, were within the range of other approved testosterone replacement therapies.

In addition to meeting the FDA criteria, an analysis of the Phase II study results for all groups revealed that, Cave and Cmax were highly correlated and there was a high probability of titrating to acceptable Cmax levels by maintaining Cave levels below about 600 ng/dL. This finding helped inform the appropriate design for the Phase III study.

We met with the FDA in November 2012 and presented the Phase II results and a protocol synopsis for a LPCN 1021 Phase III trial. The FDA accepted that LPCN 1021 would be considered as a testosterone replacement therapy. One pivotal Phase III trial was deemed necessary for FDA approval and no additional pre-clinical studies were required. For long term safety, the FDA required one year safety data on 100 subjects in the NDA.

Proposed Phase III Trial Design

The proposed Phase III trial for LPCN 1021 will enroll 300 hypogonadal male patients; 200 will be assigned to LPCN 1021 treatment, or Treatment Group, and 100 will be assigned to a marketed TRT product to serve as active control. The patients in Treatment Group will receive testosterone undecanoate doses ranging from 150 mg to 300 mg of LPCN 1021 orally twice daily with meals over the course of treatment. Each patient will have two chances to be titrated up or down by up to 75 mg to adjust each individual to their effective dose. The titration intervals will be at approximately one month intervals.

Following the final round of titration, all patients will have been on treatment for approximately between four and thirteen weeks at their final dose. During week 13 all subjects will undergo full PK profiling where primary and secondary endpoints will be assessed. Additionally, of the 200 people initially recruited into the treatment arm, approximately 120 will be followed for an additional 39 weeks (total of 52 weeks) in a safety only extension phase.

7

Table of Contents

Planning for the Phase III trial is already underway. A lead Clinical Research Organization, or CRO, has been identified. Clinical supplies manufacturing is expected to ensue in the third quarter of 2013 with the goal of enrolling patients in the fourth quarter of 2013. Completion of the Phase III trial, including the long-term safety data, and assuming successful outcomes, an NDA filing is anticipated in 2015.

LPCN 1111: A Next-Generation Oral Product Candidate for TRT

LPCN 1111 is a next-generation, novel ester prodrug of testosterone which uses the Lip’ral technology to enhance solubility and improve systemic absorption. A Phase I single dose, randomized, open label, crossover study in 8 postmenopausal women has been completed and the pharmacokinetics suggested feasibility of either once-daily dosing or twice daily dosing with high Cavg. The next steps in development for this program include a pre-investigational new drug, or IND, meeting with FDA followed by a Phase I/II proof-of-concept study in hypogonadal men.

LPCN 1107: An Oral Product for the Prevention of Preterm Birth

We believe LPCN 1107 has the potential to become the first oral hydroxyprogesterone caproate product indicated for the prevention of preterm birth. The product has completed a 28-day repeat dose toxicity study in dogs. A pre-IND meeting has also been completed with the FDA, paving the way for a proof-of-concept Phase I/II study in pregnant women with a history of preterm birth.

Competition

Testosterone Market Overview

The gel-based testosterone replacement products that are currently available include AndroGel, marketed by AbbVie, Auxilium’s Testim, Eli Lilly’s Axiron, and Endo’s Fortesta. Although AndroGel is the market leader, generating over $1 billion of sales in 2012, Testim has gained significant traction with providers and has experienced strong growth since it was launched. Transdermal patches include Actavis’s Androderm. Intramuscular forms of testosterone also exist although commercialized mostly in generic forms. Additionally, Auxilium markets the buccal testosterone replacement therapy Striant and the Testopel implantable testosterone pellets, which it acquired from Actient Pharmaceuticals in 2013.

Testosterone gels dominate the testosterone replacement therapy market. While gels are the most widely used form of testosterone replacement therapy, there is a risk of transference; additionally, the gels are messy to apply and have significant compliance issues leading to high rates of discontinuance among patients. Prescription data from the United States show that over 60% of hypogonadal men discontinue TRTs within 6 months. Only 41% of men remain on transdermal gel products at 6 months. A safe and effective oral therapy would increase patient convenience and compliance, while eliminating the testosterone transference risk associated with gels.

Other Therapies in Development

Recently there has been increased interest in developing an oral testosterone replacement therapies as well as testosterone therapies which are not considered testosterone replacement and as such will need to achieve efficacy endpoints in addition to endpoints related to serum testosterone levels that are required for replacement therapies.

Clarus Therapeutics, Inc. is in Phase III with CLR-610, a twice-daily oral softgel capsule of testosterone undecanoate, as a testosterone replacement therapy for the treatment of hypogonadism in men.

Trimel Pharmaceuticals Corporation has filed an NDA for an intranasal testosterone replacement therapy for the treatment of hypogonadal men.

8

Table of Contents

SOV Therapeutics, Inc. is developing a twice-daily testosterone undecanoate as a testosterone replacement therapy for the treatment of hypogonadism in men and in the treatment of Constitutional Delay of Growth and Puberty in adolescent boys (14-17 years of age).

Repros Therapeutics Inc. is in Phase III with Androxal (enclomiphene citrate), an orally-bioavailable isomer of the selective estrogen receptor modulator clomifene citrate as a testosterone therapy for the treatment of male hypogonadism.

Novartis is currently developing BGS649, an aromatase inhibitor as a testosterone therapy for the treatment of obese, hypogonadotropic hypogonadal men.

Hydroxyprogesterone caproate, or HPC/Preterm Birth, or PTB, Market Overview

PTB is defined as delivery before 37 weeks of gestation. The only approved therapy for prevention of PTB in women with a prior history of at least one preterm birth (~180,000 pregnancies annually) is a weekly intramuscular injection of hydroxyprogesterone caproate, marketed by KV Pharmaceutical Company under the brand name Makena. Treatment is initiated between 16 weeks and 20 weeks and is continued until up to delivery or week 37, whichever is earlier. The intramuscular injection is administered by a healthcare provider using a 21 gauge needle into the gluteus muscle, alternating sides each week. The intramuscular injections are associated with significant pain, discomfort and associated injection site reactions.

We believe LPCN 1107 has the potential to become the first oral HPC product for the prevention of preterm birth in women with a prior history of at least one preterm birth. Potential benefits of the product include the following:

| • | Elimination of pain and site reactions associated with weekly injections. |

| • | Elimination of weekly doctor visits or visits from the nurse. |

| • | Elimination of interference/disruption of personal, family or professional activities associated with weekly visits. |

LPCN 1107 has completed PK studies in dogs showing oral bioavailability comparable to an intramuscular injection. To the best of our knowledge, there is no report in the literature showing HPC oral bioavailability comparable to intramuscular injection. LPCN 1107 has also completed a 28-day repeated dose toxicity and toxicokinetics study in dogs. A pre-IND meeting with the FDA is completed, paving the way for a proof-of-concept Phase I/II study in pregnant women with a prior history of at least one preterm birth.

The oral product may also be eligible for orphan drug designation if it is deemed by the FDA to be a major contribution to patient care.

Intellectual Property

Drug Delivery Technologies for Lipophilic Drug Substances

LPCN 1021 is an oral formulation of the lipophilic prodrug testosterone undecanoate for convenient twice daily dosing, utilizing our proprietary technology for improved delivery of lipophilic therapeutic agents. Our patent portfolio is directed to various types of compositions and methods for delivery of lipophilic drugs, which are drugs that are soluble in lipids. As of July 1, 2013, we own seven issued U.S. patents, 15 pending U.S. patent applications, 31 corresponding issued foreign patents and associated pending foreign patent applications. Of the above, we have three issued U.S. patents, nine pending U.S. patent applications, five issued foreign patents and pending foreign patent applications relating to various aspects of LPCN 1021.

We also license in the fields other than cough and cold two U.S. patents and two U.S. applications (and related foreign patents and applications) we previously assigned to Spriaso LLC, which could be possibly used with future product candidates.

9

Table of Contents

Our issued U.S. Patent No. 6,267,985 covers pharmaceutical compositions comprising a therapeutic agent being solubilized in a triglyceride, and it is expected to expire in 2019. We have corresponding patents in Australia, Canada, and New Zealand, two corresponding pending applications in Japan, and one corresponding pending application in Europe. These corresponding foreign patents, and applications if they issue, are all expected to expire in 2020. Our issued U.S. Patents No. 6,569,463 and 6,923,988, and one further pending U.S. patent application cover various aspects of pharmaceutical compositions comprising a hydrophobic active ingredient admixed with a hydrophilic surfactant, which is water soluble bubble producing liquid, and a lipophilic additive, and are expected to expire in 2019 and 2020, respectively, and if the application were to issue, 2019. We have corresponding patent applications pending in Japan and Canada, which if they issue, are expected to expire in 2020.

We also have two pending U.S. patent applications and eight corresponding foreign patent applications (one each in Europe, Hong Kong, Australia, Brazil, Canada, India, Japan, and Mexico) directed to oral pharmaceutical composition comprising a testosterone ester and a hydrophilic and a lipophilic surfactant. These applications, if they issue, are expected to expire in 2029 in the U.S. and 2030 in foreign jurisdictions.

We also have two pending U.S. patent applications, two foreign patents (one each in Australia and New Zealand), and one allowed patent application (in Canada) directed to oral dosage forms comprising a drug, a solubilizer, and a release modulator. The pending U.S. patent applications, if they issue, are expected to expire as early as 2023, and the foreign patents, and application if it issues, are expected to expire in 2026.

We also have two pending U.S. patent applications directed to pharmaceutical compositions comprising a sex hormone. These applications, if they issue, are expected to expire in 2019.

We also have two pending U.S. applications directed to high strength capsule formulations of testosterone undecanoate. These applications, if they issue, are expected to expire in 2030.

Our remaining issued U.S. patents, pending U.S. patent applications, issued foreign patents, and pending foreign patent applications are not currently used in the LPCN 1021 technology, but may be used with alternate versions of, or future product candidates utilizing, our delivery technology for lipophilic drugs (as used for the LPCN 1111 and, LPCN 1107 product candidates).

We do not have patent protection for LPCN 1021 in many countries, including large territories such as India, Russia, and China, and we will be unable to prevent patent infringement in those countries. Additionally, the three U.S. patents that could be listed in the FDA Orange Book for LPCN 1021 are expected to expire in 2019 and 2020. Upon expiration and if we are actively marketing the LPCN 1021 product, if we have no other issued U.S. patents covering the product, we will lose certain advantages that come with Orange Book listing of patents and will no longer be able to prevent others in the U.S. from practicing the inventions claimed by the three patents.

Government Regulation

The Regulatory Process for Drug Development

The production and manufacture of our product candidates and our research and development activities are subject to regulation by various governmental authorities around the world. In the United States, drugs and products are subject to regulation by the FDA. There are other comparable agencies in Europe and other parts of the world. Regulations govern, among other things, the research, development, testing, manufacture, quality control, approval, labeling, packaging, storage, record-keeping, promotion, advertising, distribution, post-approval monitoring and reporting, marketing and export and import of products. Applicable legislation requires licensing of manufacturing and contract research facilities, carefully controlled research and testing of products, governmental review and/or approval of results prior to marketing therapeutic products. Additionally, adherence to good laboratory practices, or GLP, good clinical practices, or GCP, during clinical testing and good manufacturing practices, or GMP, during production is required. The system of new drug approval in the United States is generally considered to be the most rigorous in the world and is described in further detail below under “United States Pharmaceutical Product Development Process.”

10

Table of Contents

United States Pharmaceutical Product Development Process

In the United States, the FDA regulates pharmaceutical products under the Federal Food, Drug and Cosmetic Act and implementing regulations. Pharmaceutical products are also subject to other federal, state and local statutes and regulations. The process of obtaining regulatory approvals and the subsequent compliance with appropriate federal, state, local and foreign statutes and regulations require the expenditure of substantial time and financial resources. Failure to comply with the applicable United States requirements at any time during the product development process, approval process or after approval, may subject an applicant to administrative or judicial sanctions. FDA sanctions could include refusal to approve pending applications, withdrawal of an approval, a clinical hold, warning letters, product recalls, product seizures, total or partial suspension of production or distribution injunctions, fines, refusals of government contracts, restitution, disgorgement or civil or criminal penalties. Any agency or judicial enforcement action could have a material adverse effect on us.

It normally takes an average of 10 to 15 years for a typical experimental drug to go from concept to approval. The process required by the FDA before a pharmaceutical product may be marketed in the United States generally includes the following:

| • | Completion of preclinical laboratory tests and animal studies. The latter often conducted according to GLPs or other applicable regulations, as well as synthesis and drug formulation development leading ultimately to clinical drug supplies manufactured according to current GMPs; |

| • | Submission to the FDA of an IND, which must become effective before human clinical trials may begin in the United States; |

| • | Performance of adequate and well-controlled human clinical trials according to the FDA’s current GCPs, to establish the safety and efficacy of the proposed pharmaceutical product for its intended use; |

| • | Submission to the FDA of an NDA for a new pharmaceutical product; |

| • | Satisfactory completion of an FDA inspection of the manufacturing facility or facilities where the pharmaceutical product is produced to assess compliance with the FDA’s current good manufacturing practice, or cGMP, to assure that the facilities, methods and controls are adequate to preserve the pharmaceutical product’s identity, strength, quality and purity; |

| • | Potential FDA audit of the preclinical and clinical trial sites that generated the data in support of the NDA; and |

| • | FDA review and approval of the NDA. |

The lengthy process of seeking required approvals and the continuing need for compliance with applicable statutes and regulations require the expenditure of substantial resources and approvals are inherently uncertain.

Preclinical Studies: Prior to preclinical studies, a research phase takes place which involves demonstration of target and function, design, screening and synthesis of inhibitors. Preclinical studies include laboratory evaluations of product chemistry, toxicity and formulation, as well as animal studies to evaluate efficacy and activity, toxic effects, pharmacokinetics and metabolism of the pharmaceutical product candidate and to provide evidence of the safety, bioavailability and activity of the pharmaceutical product candidate in animals. The conduct of the preclinical safety evaluations must comply with federal regulations and requirements including GLPs. The results of the formal IND-enabling preclinical studies, together with manufacturing information, analytical data, any available clinical data or literature as well as the comprehensive descriptions of proposed human clinical studies, are then submitted as part of the IND application to the FDA.

The IND automatically becomes effective 30 days after receipt by the FDA, unless the FDA places the IND on a clinical hold within that 30-day time period. In such a case, the IND sponsor and the FDA must resolve any outstanding concerns before the clinical trial can begin. The FDA may also impose clinical holds on a pharmaceutical product candidate at any time before or during clinical trials due to safety concerns or non-compliance. Accordingly, we cannot be certain that submission of an IND will result in the FDA allowing clinical trials to begin, or that, once begun, issues will not arise that suspend or terminate such clinical trial.

11

Table of Contents

Clinical Trials: Clinical trials involve the administration of the pharmaceutical product candidate to healthy volunteers or patients under the supervision of qualified investigators, generally physicians not employed by the sponsor. Clinical trials are conducted under protocols detailing, among other things, the objectives of the clinical trial, dosing procedures, subject selection and exclusion criteria, and the parameters to be used to monitor subject safety. Each protocol must be submitted to the FDA if conducted under a U.S. IND. Clinical trials must be conducted in accordance with the FDA’s GCP requirements. Further, each clinical trial must be reviewed and approved by an independent institutional review board, or IRB, or ethics committee at or servicing each institution at which the clinical trial will be conducted. An IRB or ethics committee is charged with protecting the welfare and rights of trial participants and considers such items as whether the risks to individuals participating in the clinical trials are minimized and are reasonable in relation to anticipated benefits. The IRB or ethics committee also approves the informed consent form that must be provided to each clinical trial subject or his or her legal representative and must monitor the clinical trial until completed.

Human clinical trials are typically conducted in three sequential phases that may overlap or be combined:

Phase I Clinical Trials: Phase I clinical trials are usually first-in-man trials, take approximately one to two years to complete and are generally conducted on a small number of healthy human subjects to evaluate the drug’s activity, schedule and dose, pharmacokinetics and pharmacodynamics. However, in the case of life-threatening diseases, such as cancer, the initial Phase I testing may be done in patients with the disease. These trials typically take longer to complete and may provide insights into drug activity.

Phase II Clinical Trials: Phase II clinical trials can take approximately one to three years to complete and are carried out on a relatively small to moderate number of patients (as compared to Phase III) in a specific indication. The pharmaceutical product is evaluated to preliminarily assess efficacy, to identify possible adverse effects and safety risks, and to determine optimal dose, regimens, pharmacokinetics, pharmacodynamics and dose response relationships. This phase also provides additional safety data and serves to identify possible common short-term side effects and risks in a larger group of patients. Phase II clinical trials sometimes include randomization of patients.

Phase III Clinical Trials: Phase III clinical trials take approximately two to five years to complete and involve tests on a much larger population of patients (several hundred to several thousand patients) suffering from the targeted condition or disease. These studies usually include randomization of patients and blinding of both patients and investigators at geographically dispersed test sites (multi-center trials). These trials are undertaken to further evaluate dosage, clinical efficacy and safety and are intended to establish the overall risk/benefit ratio of the product and provide an adequate basis for product labeling. Generally, two adequate and well-controlled Phase III clinical trials are required by the FDA for approval of an NDA or foreign authorities for approval of marketing applications.

Post-approval studies, or Phase IV clinical trials, may be conducted after initial marketing approval. These studies are used to gain additional experience from the treatment of patients in the intended therapeutic indication and may be required by the FDA as a condition of approval.

Progress reports detailing the results of the clinical trials must be submitted at least annually to the FDA, and written IND safety reports must be submitted to the FDA and the investigators for serious and unexpected adverse events or for any finding from tests in laboratory animals that suggests a significant risk for human subjects. Phase I, Phase II and Phase III clinical trials may not be completed successfully within any specified period, if at all. The FDA or the sponsor or, if used, its data safety and monitoring board may suspend a clinical trial at any time on various grounds, including a finding that the research subjects or patients are being exposed to an unacceptable health risk. Similarly, an IRB or ethics committee can suspend or terminate approval of a clinical trial at its institution if the clinical trial is not being conducted in accordance with the IRB’s or ethics committee’s requirements or if the pharmaceutical product has been associated with unexpected serious harm to patients.

12

Table of Contents

Concurrent with clinical trials, companies usually complete additional animal studies and must also develop additional information about the chemistry and physical characteristics of the pharmaceutical product, as well as finalize a process for manufacturing the product in commercial quantities in accordance with GMP requirements. The manufacturing process must be capable of consistently producing quality batches of the pharmaceutical product candidate and, among other things, must develop methods for testing the identity, strength, quality and purity of the final pharmaceutical product. Additionally, appropriate packaging must be selected and tested and stability studies must be conducted to demonstrate that the pharmaceutical product candidate does not undergo unacceptable deterioration over its shelf life.

U.S. Pharmaceutical Review and Approval Process

New Drug Application: Upon completion of pivotal Phase III clinical studies, the sponsor assembles all the product development, preclinical and clinical data along with descriptions of the manufacturing process, analytical tests conducted on the chemistry of the pharmaceutical product, proposed labeling and other relevant information, and submits it to the FDA as part of an NDA. The submission or application is then reviewed by the regulatory body for approval to market the product. This process takes eight months to one year to complete. The FDA may refuse to approve an NDA if the applicable regulatory criteria are not satisfied or may require additional clinical data or other data and information. Even if such data and information is submitted, the FDA may ultimately decide that the NDA does not satisfy the criteria for approval. If a product receives regulatory approval, the approval may be significantly limited to specific diseases and dosages or the indications for use may otherwise be limited, which could restrict the commercial value of the product. Further, the FDA may require that certain contraindications, warnings or precautions be included in the product labeling.

Post-Approval Requirements

Any pharmaceutical products for which we receive FDA approvals are subject to continuing regulation by the FDA, including, among other things, record-keeping requirements, reporting of adverse experiences with the product, providing the FDA with updated safety and efficacy information, product sampling and distribution requirements, complying with certain electronic records and signature requirements and complying with FDA promotion and advertising requirements, which include, among others, standards for direct-to-consumer advertising, promoting pharmaceutical products for uses or in patient populations that are not described in the pharmaceutical product’s approved labeling (known as “off-label use”), industry-sponsored scientific and educational activities and promotional activities involving the internet. Failure to comply with FDA requirements can have negative consequences, including adverse publicity, enforcement letters from the FDA, mandated corrective advertising or communications with doctors and civil or criminal penalties.

The FDA also may require post-marketing testing, known as Phase IV testing, risk evaluation and mitigation strategies and surveillance to monitor the effects of an approved product or place conditions on an approval that could restrict the distribution or use of the product.

Other Healthcare Laws and Compliance Requirements

In the United States, our activities are potentially subject to regulation by various federal, state and local authorities in addition to the FDA, including the Centers for Medicare and Medicaid Services and other divisions of the United States government, including, the Department of Health and Human Services, the U.S. Department of Justice and individual U.S. Attorney offices within the Department of Justice, and state and local governments. For example, if a drug product is reimbursed by Medicare, Medicaid, or other federal or state healthcare programs, our company, including our sales, marketing and scientific/educational grant programs, must comply with the federal False Claims Act, as amended, the federal Anti-Kickback Statute, as amended, and similar state laws. If a drug product is reimbursed by Medicare or Medicaid, pricing and rebate programs must comply with, as applicable, the Medicaid rebate requirements of the Omnibus Budget Reconciliation Act of 1990, or OBRA, and the Medicare Prescription Drug Improvement and Modernization Act of 2003, or MMA. Among other things, OBRA requires drug manufacturers to pay rebates on prescription drugs to state Medicaid programs and empowers states to negotiate rebates on pharmaceutical prices, which may result in prices for our future products that will likely be lower than the prices we might otherwise obtain. Additionally, the Patient Protection and Affordable Care Act as

13

Table of Contents

amended by the Health Care and Education Reconciliation Act of 2010, collectively, PPACA, substantially changes the way healthcare is financed by both governmental and private insurers. Among other cost containment measures, PPACA establishes: an annual, nondeductible fee on any entity that manufactures or imports certain branded prescription drugs and biologic agents; a new Medicare Part D coverage gap discount program; and a new formula that increases the rebates a manufacturer must pay under the Medicaid Drug Rebate Program. There may continue to be additional proposals relating to the reform of the U.S. healthcare system, in the future, some of which could further limit coverage and reimbursement of drug products. If drug products are made available to authorized users of the Federal Supply Schedule of the General Services Administration, additional laws and requirements may apply.

Pharmaceutical Coverage, Pricing and Reimbursement

In the United States and markets in other countries, sales of any products for which we receive regulatory approval for commercial sale will depend in part on the availability of coverage and adequate reimbursement from third-party payers, including government health administrative authorities, managed care providers, private health insurers and other organizations. In the United States, private health insurers and other third-party payers often provide reimbursement for products and services based on the level at which the government (through the Medicare or Medicaid programs) provides reimbursement for such treatments. Third-party payers are increasingly examining the medical necessity and cost-effectiveness of medical products and services in addition to their safety and efficacy and, accordingly, significant uncertainty exists as to the coverage and reimbursement status of newly approved therapeutics. In particular, in the United States, the European Union and other potentially significant markets for our product candidates, government authorities and third-party payers are increasingly attempting to limit or regulate the price of medical products and services, particularly for new and innovative products and therapies, which has resulted in lower average selling prices. Further, the increased emphasis on managed healthcare in the United States and on country and regional pricing and reimbursement controls in the European Union will put additional pressure on product pricing, reimbursement and usage, which may adversely affect our future product sales and results of operations. These pressures can arise from rules and practices of managed care groups, judicial decisions and governmental laws and regulations related to Medicare, Medicaid and healthcare reform, pharmaceutical reimbursement policies and pricing in general. As a result, coverage and adequate third party reimbursement may not be available for our products to enable us to realize an appropriate return on our investment in research and product development.

The market for our product candidates for which we may receive regulatory approval will depend significantly on access to third-party payers’ drug formularies, or lists of medications for which third-party payers provide coverage and reimbursement. The industry competition to be included in such formularies often leads to downward pricing pressures on pharmaceutical companies. Also, third-party payers may refuse to include a particular branded drug in their formularies or may otherwise restrict patient access to a branded drug when a less costly generic equivalent or other alternative is available. In addition, because each third-party payer individually approves coverage and reimbursement levels, obtaining coverage and adequate reimbursement is a time-consuming and costly process. We would be required to provide scientific and clinical support for the use of any product to each third-party payer separately with no assurance that approval would be obtained, and we may need to conduct expensive pharmacoeconomic studies in order to demonstrate the cost-effectiveness of our products. This process could delay the market acceptance of any of our product candidates for which we may receive approval and could have a negative effect on our future revenues and operating results. We cannot be certain that our product candidates will be considered cost-effective. If we are unable to obtain coverage and adequate payment levels for our product candidates from third-party payers, physicians may limit how much or under what circumstances they will prescribe or administer them and patients may decline to purchase them. This in turn could affect our ability to successfully commercialize our products and impact our profitability, results of operations, financial condition, and future success.

The Development Process for Orphan Drugs

The United States Orphan Drug Act encourages the development of orphan drugs, which are intended to treat “rare diseases or conditions” within the meaning of this Act (i.e., those that affect fewer than 200,000 persons in the United States). The provisions of the Act are intended to stimulate the research, development and approval of

14

Table of Contents

products that treat rare diseases. Orphan Drug Designation provides a sponsor with several potential benefits: (1) sponsors are granted seven years of marketing exclusivity after approval of the orphan-designated indication for the drug product; (2) sponsors are granted U.S. tax incentives for clinical research; (3) the FDA’s office of orphan products development co-ordinates research study design assistance for sponsors of drugs for rare diseases; and (4) grant funding can be obtained to defray costs of qualified clinical testing.

Priority Review

Priority Review is a designation for an NDA after it has been submitted to the FDA for review. Reviews for NDAs are designated as either “Standard” or “Priority.” A Standard designation sets the target date for completing all aspects of a review and the FDA taking an action on 90% of applications (i.e., approve or not approve) at 12 months after the date it was submitted. A Priority designation sets the target date for the FDA action on 90% of applications at eight months after submission. A Priority designation is intended for those products that address unmet medical needs.

Accelerated Approval

Accelerated Approval or Subpart H Approval is a program described in the NDA regulations that is intended to make promising products for life threatening diseases available on the basis of evidence of effect on a surrogate endpoint prior to formal demonstration of patient benefit. A surrogate marker is a measurement intended to substitute for the clinical measurement of interest, usually prolongation of survival in oncology that is considered likely to predict patient benefit. The approval that is granted may be considered a provisional approval with a written commitment to complete clinical studies that formally demonstrate patient benefit.

Employees

As of June 30, 2013, we had 11 employees and we also utilize the services of consultants on a regular basis. Seven employees are engaged in drug development activities and four are in support and administration. None of our employees are represented by labor unions or covered by collective bargaining agreements.

Legal Proceedings

Although we may, from time to time, be a party to certain lawsuits in the ordinary course of business, we are not currently involved in any lawsuits that would have a material adverse effect on our results of operations, financial condition, or cash flows.

Properties

Our corporate headquarters are located in a leased facility in Salt Lake City, Utah. Our lease expires in November 2014. We have an option to renew the lease for an additional two years. We believe that our existing facilities are suitable and adequate and that we have sufficient capacity to meet our current anticipated needs.

15

Table of Contents

RISK FACTORS

Risks Relating to Our Business and Industry

Our research and development programs and processes are at an early stage of development, which makes it difficult to evaluate our business and prospects, or predict if or when we will successfully commercialize our product candidates

Our operations to date have primarily been limited to conducting research and development activities under license and collaboration agreements. Our current portfolio consists of our lead product candidate LPCN 1021, for which we have just completed Phase II clinical trials. We are also developing two additional earlier stage clinical candidates, LPCN 1111 and LPCN 1107. We have never marketed or commercialized a drug product. Consequently, any predictions about our future performance may not be as accurate as they could be if we were further along our commercialization path. In addition, as a pre-commercial stage business, we may encounter unforeseen expenses, difficulties, complications, delays and other unknown factors.

Our clinical product candidates are at an early stage of development and will require significant further investment and regulatory approvals prior to marketing and commercialization. As such, our product development processes for LPCN 1021, LPCN 1111 and LPCN 1107 are very risky and uncertain, and our product candidates may fail to advance beyond the current study. Even if we obtain required financing, we cannot ensure successful product development or that we will obtain regulatory approval or successfully commercialize any of our product candidates and generate product revenues.

All of our clinical candidates will be subject to extensive regulation which can be costly and time consuming, cause delays or prevent approval of the products for commercialization.

Our clinical development of LPCN 1021, LPCN 1111, LPCN1107 and any future product candidates, is subject to extensive regulations by the FDA in the United States. Product development is a very lengthy and expensive process and can vary significantly based upon the product candidate’s novelty and complexity. Regulations are subject to change and regulatory agencies have significant discretion in the approval process.

Numerous statutes and regulations govern human testing and the manufacture and sale of human therapeutic products in the United States. Such legislation and regulation bears upon, among other things, the approval of protocols and human testing, the approval of manufacturing facilities, safety of the product candidates, testing procedures and controlled research, review and approval of manufacturing, preclinical and clinical data prior to marketing approval including adherence to GMP during production and storage as well as regulation of marketing activities including advertising and labeling.

In order to obtain regulatory clearance for the commercial sale of any of our product candidates, we must demonstrate through preclinical studies and clinical trials that the potential product is safe, efficacious for use in humans for each target indication. Obtaining approval of any of our product candidates is an extensive, lengthy, expensive and uncertain process, and the FDA may delay, limit or deny approval for many reasons, including:

| • | we may not be able to demonstrate that the product candidate is safe and effective to the satisfaction of the FDA; |

| • | the results of our clinical trials may not meet the level of statistical or clinical significance required by the FDA for marketing approval; |

| • | the FDA may disagree with the number, design, size, conduct or implementation of our clinical trials; |

| • | the CRO that we retain to conduct our clinical trials may take actions outside of our control that materially adversely impact our clinical trials; |

| • | the FDA may not find the data from preclinical studies and clinical trials sufficient to demonstrate that a particular product candidate’s clinical and other benefits outweigh its safety risks; |

16

Table of Contents

| • | the FDA may disagree with our interpretation of data from our preclinical studies and clinical trials or may require that we conduct additional trials; |

| • | the FDA may not accept data generated at our clinical trial sites; |

| • | if our NDA is reviewed by an advisory committee, the FDA may have difficulties scheduling an advisory committee meeting in a timely manner or the advisory committee may recommend against approval of our application or may recommend that the FDA require, as a condition of approval, additional preclinical studies or clinical trials, limitations on approved labeling or distribution and use restrictions; |

| • | the FDA may require development of a Risk Evaluation and Mitigation Strategy, or REMS, as a condition of approval; |

| • | the FDA may require longer or additional duration of stability data on the clinical lots prior to initiation of further clinical trials; |

| • | the FDA may identify deficiencies in the formulation or stability of our product candidates or products, or relating to our manufacturing processes or facilities, or in the processes and facilities of the contract manufacturing organization, or CMO, our suppliers or other third parties that may be utilized in the production supply chain of our products; |

| • | with respect to LPCN 1021 and LPCN 1111, the FDA may not grant New Chemical Entity exclusivity to Testosterone prodrug present as the active; and |

| • | with respect to LPCN 1107, the FDA may not grant Orphan Drug Designation for the oral product if they do not deem it to be a major contribution to patient care over intramuscular injection, or for other reasons. |

Preclinical and clinical data are often susceptible to varying interpretations and analyses, and many companies that have believed their product candidates performed satisfactorily in preclinical studies and clinical trials have nonetheless failed to obtain FDA approval for their products.

No assurance can be given that current regulations relating to regulatory approval will not change or become more stringent. The FDA may also require that we amend clinical trial protocols and/or run additional trials in order to provide additional information regarding the safety, efficacy or equivalency of any compound for which we seek regulatory approval. Moreover, any regulatory approval of a drug which is eventually obtained may entail limitations on the indicated uses for which that drug may be marketed. Furthermore, product approvals may be withdrawn or limited in some way if problems occur following initial marketing or if compliance with regulatory standards is not maintained. FDA could become more risk averse to any side effects or set higher standards of safety and efficacy prior to reviewing or approving a product. This could result in a product not being approved.

Even if we receive marketing approval in the United States, we may never receive regulatory approval to market our products outside the United States, which could reduce the size of our potential markets and have a material adverse impact on our business.

In order to market any products outside of the United States, we must establish and comply with numerous and varying regulatory requirements of other countries regarding safety and efficacy.

Approval procedures vary among countries and can involve additional product candidate testing and additional administrative review periods. The time required to obtain approvals in other countries might differ from that required to obtain FDA approval. The marketing approval process in other countries may include all of the risks detailed above regarding FDA approval in the United States as well as other risks. In particular, in many countries outside of the United States, products must receive pricing and reimbursement approval before the product can be commercialized. This can result in substantial delays in such countries. Marketing approval in one country does not ensure marketing approval in another, but a failure or delay in obtaining marketing approval in one country may have a negative effect on the regulatory process in others. Failure to obtain marketing approval in other countries or

17

Table of Contents

any delay or setback in obtaining such approval would impair our ability to market our products in such foreign markets. Any such impairment would reduce the size of our potential markets, which could have a material adverse impact on our business, results of operations and prospects.

The timelines of our clinical trials may be impacted by numerous factors and any delays may adversely affect our ability to execute our current business strategy.

Our expectations regarding the success of our product candidates, including our clinical candidates and lead compounds, and our business are based on projections which may not be realized for many scientific, business or other reasons. We therefore cannot assure investors that we will be able to adhere to our current schedule. We set goals that forecast the accomplishment of objectives material to our success: selecting clinical candidates, product candidates, failures in research, the inability to identify or advance lead compounds, identifying target patient groups or clinical candidates, the timing and completion of clinical trials, and anticipated regulatory approval. The actual timing of these events can vary dramatically due to factors such as slow enrollment of patients in studies, uncertainties in scale-up, manufacturing and formulation of our compounds, failures in research, the inability to identify clinical candidates, failures in our clinical trials, and uncertainties inherent in the regulatory approval process and regulatory submissions. Decisions by our partners or collaborators may also affect our timelines and delays in achieving manufacturing capacity and marketing infrastructure sufficient to commercialize our biopharmaceutical products. The length of time necessary to complete clinical trials and to submit an application for marketing approval by applicable regulatory authorities may also vary significantly based on the type, complexity and novelty of the product candidate involved, as well as other factors.

The duration of our pre-clinical and clinical trial programs can be significantly extended as the attainment of an appropriate dose may be delayed, resulting in additional costs and overall program delays. If a trial or phase of a trial has commenced, it could be placed on clinical hold if the regulatory authorities determine a trial or its design may be unsafe or require clarifications regarding protocol design.

We depend primarily on the success of our lead product candidate, LPCN 1021, which is still under clinical development and may not receive regulatory approval or be successfully commercialized.

We currently have only one product candidate that has completed Phase II clinical trials, and our business currently depends primarily on its successful development, regulatory approval and commercialization. We are not permitted to market LPCN 1021 in the United States until we receive approval of an NDA from the FDA, or in any foreign countries until we receive the requisite approval from such countries. We have not scaled up the pivotal study formulation to commercial scale. We have not submitted an NDA to the FDA or comparable applications to other regulatory authorities. Before we submit an NDA to the FDA for LPCN 1021 as a TRT we must initiate and complete our pivotal Phase III trial, and the three pharmacokinetic studies for labeling purposes. We have not commenced any of these trials.

In addition, results from Phase II trials of LPCN 1021 may not be replicated in our pivotal Phase III trial. A number of companies in the pharmaceutical and biotechnology industries have suffered significant setbacks in late-stage clinical trials even after achieving positive results in early stage development. Our pivotal Phase III trial will evaluate the safety and efficacy of LPCN 1021 over a longer period of time in a patient population almost four times larger than our repeat-dose Phase II trials. Accordingly, the results from Phase II trials for LPCN 1021 may not be predictive of the results we may obtain in our pivotal Phase III trial of LPCN 1021. Our pivotal Phase III trial may produce negative or inconclusive results, and we may decide, or regulators may require us, to conduct additional preclinical studies or clinical trials, or even terminate further development.

LPCN 1107 is in a very early stage of development, has never been administered orally in humans, and may not be further developed for a variety of reasons.

LPCN 1107 is in a very early stage of development and consequently the risk we fail to commercialize related products is high. In particular, we have conducted a repeated dose toxicity and toxicokinetic study in dogs. Although preliminary data from the studies demonstrated oral absorption in dogs, to our knowledge, HPC has never been administered orally in humans. As such, our currently planned proof-of-concept Phase I/II study would be the “first in human” study with oral administration of HPC. In particular, any such study may not demonstrate that

18

Table of Contents

LPCN 1107 has adequate, or any, oral absorption in our targeted patient group. Furthermore, such study may not be predictive of safety concerns that may arise in pregnant women or demonstrate that LPCN 1107 has a adequate safety profile to warrant further development. The FDA may also require further preclinical studies and/or clinical studies in healthy women before proceeding to studies in pregnant women. All these factors can impact the timing of, and our ability to, continue development of LPCN 1107.