Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - FOX FACTORY HOLDING CORP | d520049dex231.htm |

| EX-10.27 - EX-10.27 - FOX FACTORY HOLDING CORP | d520049dex1027.htm |

Table of Contents

As filed with the Securities and Exchange Commission on July 17, 2013

Registration No. 333-189841

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1 to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Fox Factory Holding Corp.

(Exact name of Registrant as specified in its charter)

| Delaware | 3751 |

26-1647258 | ||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

915 Disc Drive

Scotts Valley, CA 95066

831.274.6500

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Larry L. Enterline

Chief Executive Officer

Fox Factory Holding Corp.

915 Disc Drive

Scotts Valley, CA 95066

831.274.6500

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Stephen D. Cooke, Esq. Justin T. Hughes, Esq. Paul Hastings LLP 695 Town Center Drive Seventeenth Floor Costa Mesa, California 92656 714.668.6200 |

David Haugen, Esq. Fox Factory Holding Corp. 915 Disc Drive Scotts Valley, California 95066 831.274.6500 |

Kevin P. Kennedy, Esq. Simpson Thacher & Bartlett LLP 2475 Hanover Street Palo Alto, California 94304 650.251.5000 | ||

| Jeffrey T. Hartlin, Esq. Paul Hastings LLP 1117 S. California Avenue Palo Alto, California 94304 650.320.1804 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||||

| Non-accelerated filer | x | (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | ||||

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of each class of securities to be registered | Proposed maximum aggregate offering price (1)(2) |

Amount of registration fee(3) | ||

| Common Stock, $0.001 par value per share |

$120,000,000 | $16,368(4) | ||

|

| ||||

|

| ||||

| (1) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Includes the aggregate offering price of additional shares that the underwriters have the option to purchase to cover overallotments, if any. |

| (3) | Calculated pursuant to Rule 457(o) under the Securities Act of 1933, as amended, based on an estimate of the proposed maximum aggregate offering price. |

| (4) | Previously paid in connection with the initial filing of this Registration Statement on July 8, 2013. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. Neither we nor the selling stockholders may sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities, and neither we nor the selling stockholders are soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to completion, dated July 17, 2013

Prospectus

shares

Fox Factory Holding Corp.

Common stock

This is an initial public offering of common stock by Fox Factory Holding Corp., a Delaware corporation. We are selling shares of common stock. The selling stockholders identified in this prospectus are selling shares of common stock. We will not receive any of the proceeds from the sale of the shares by the selling stockholders.

Prior to this offering, there has been no public market for our common stock. The estimated initial public offering price is between $ and $ per share.

We have applied to have our shares of common stock listed on the Nasdaq Global Select Market, subject to notice of issuance, under the symbol “FOXF.” We are an “emerging growth company” as that term is used in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act, and, as such, will be subject to reduced public company reporting requirements.

| Per share | Total | |||||||

| Initial public offering price |

$ | $ | ||||||

| Underwriting discounts and commissions |

$ | $ | ||||||

| Proceeds to us, before expenses(1) |

$ | $ | ||||||

| Proceeds to selling stockholders, before expenses |

$ | $ | ||||||

| (1) | We have agreed to reimburse the underwriters for certain FINRA-related expenses. See “Underwriting”. |

Delivery of the shares of common stock is expected to be made on or about , 2013. The selling stockholders identified in this prospectus have granted the underwriters an option for a period of 30 days to purchase, on the same terms and conditions as set forth above, up to an additional shares of our common stock. We will not receive any of the proceeds from the sale of shares by these selling stockholders if the underwriters exercise their option to purchase additional shares of common stock.

Investing in our common stock involves substantial risk. Please read “Risk factors” beginning on page 18.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| Baird |

William Blair |

Piper Jaffray |

, 2013

Table of Contents

Table of Contents

| Prospectus |

||||

| Page | ||||

| 1 | ||||

| 18 | ||||

| 41 | ||||

| 43 | ||||

| 44 | ||||

| 45 | ||||

| 47 | ||||

| 49 | ||||

| Management’s discussion and analysis of financial condition and results of operations |

52 | |||

| 80 | ||||

| 94 | ||||

| 103 | ||||

| 113 | ||||

| 119 | ||||

| 121 | ||||

| 127 | ||||

| Material U.S. federal income tax consequences to non-U.S. holders |

130 | |||

| 134 | ||||

| 140 | ||||

| 140 | ||||

| 140 | ||||

| F-1 | ||||

Neither we, the selling stockholders, nor any of the underwriters have authorized anyone to provide any information or to make any representations other than as contained in this prospectus or in any free writing prospectuses we have prepared. We do not, and the selling stockholders and underwriters do not, take responsibility for, and provide no assurance as to, the reliability of any information that others may give you. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date, regardless of the time of delivery of this prospectus or of any sale of the common stock.

-i-

Table of Contents

This summary highlights selected information that is presented in greater detail elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should read this entire prospectus carefully, including the sections titled “Risk factors,” “Management’s discussion and analysis of financial condition and results of operations” and our consolidated financial statements and the related notes included elsewhere in this prospectus, before deciding whether to purchase shares of our common stock. Unless the context otherwise requires, the terms “FOX,” the “company,” “we,” “us,” and “our” in this prospectus refer to Fox Factory Holding Corp. and its wholly-owned operating subsidiary, Fox Factory, Inc., on a consolidated basis, and this “offering” refers to the offering contemplated in this prospectus.

Our company

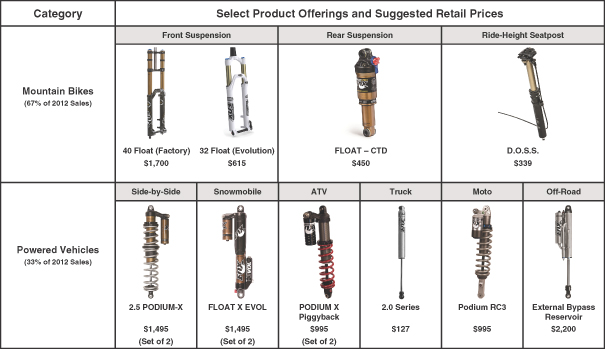

We are a designer, manufacturer and marketer of high-performance suspension products used primarily on mountain bikes, side-by-side vehicles, or Side-by-Sides, on-road vehicles with off-road capabilities, off-road vehicles and trucks, all-terrain vehicles, or ATVs, snowmobiles, specialty vehicles and applications, and motorcycles. Through our products we enhance ride dynamics, which we define as the interplay between the rider, the vehicle and the terrain, by improving performance and control. Our brand is associated with high-performance and technologically advanced products, by which we generally mean products that provide users with improved control and a smoother ride while riding over rough terrain in varied environments. We believe that the performance of our products has been demonstrated by, and our brand benefits from, the success of professional athletes who use our products in elite competitive events, such as the Union Cycliste Internationale Mountain Bike World Cup and the X Games. We believe the exposure our products receive when used by successful professional athletes positively influences the purchasing habits of enthusiasts and other consumers seeking high-performance products. We believe that our strategic focus on the performance and racing segments in our markets influences many aspiring and enthusiast consumers who we believe seek to emulate the performance of professional and other elite athletes. We believe our products are generally sold at premium prices, which to us means manufacturer suggested retail sale prices that are generally in the upper quartile of their respective product categories.

We design our products for, and market our products to, some of the world’s leading original equipment manufacturers, or OEMs, in our markets, and to consumers through the aftermarket channel. Many of our OEM customers, including Scott, Specialized and Trek in mountain bikes and BRP, Ford and Polaris in powered vehicles, are among the market leaders in their respective product categories, and help shape, as well as respond to, consumer trends in their respective categories. In addition, consumers select our products in the aftermarket channel where we market through a global network of dealers and distributors. We currently sell to more than 150 OEMs and distribute our products to more than 2,300 retail dealers and distributors worldwide. In 2012, 81% of our sales resulted from sales to OEM customers and 19% resulted from sales to dealers and distributors for resale in the aftermarket channel.

We have experienced strong sales and profit growth during the past few years. Our sales increased from approximately $45.7 million for the three months ended March 31, 2012 to

-1-

Table of Contents

$54.9 million for the three months ended March 31, 2013. Over the same period, our net income increased from $2.6 million to $3.5 million, and our adjusted EBITDA increased from approximately $6.4 million to $8.8 million. Our sales increased from approximately $131.7 million in 2008 to $235.9 million in 2012. Over the same period, our net income increased from approximately $3.8 million to $14.2 million. Our Adjusted EBITDA increased from approximately $26.8 million in 2010 to $36.0 million in 2012. See “Summary consolidated financial data—Non-GAAP financial measures” for the definition of Adjusted EBITDA and a reconciliation from net income to Adjusted EBITDA.

Market opportunity

We participate in the large global markets for mountain bikes and powered vehicles used by recreational and professional users. Today, our products for powered vehicles are used primarily on Side-by-Sides, on-road vehicles with off-road capabilities, off-road vehicles and trucks, ATVs, snowmobiles, specialty vehicles and applications, and motorcycles.

We focus on premium priced products within each of these categories, which we consider to be the high-end segment because of their higher retail sale prices, where we believe consumers have a preference for well-designed, performance-oriented equipment. We believe that suspension systems are critical to the performance of the mountain bikes and powered vehicles in the product categories in which we focus and that technical features, component performance, product design, durability, reliability and brand recognition strongly influence the purchasing decisions of consumers. Over the past decade, there have been significant technological advances in materials and features that have increased product functionality and performance, allowing our suspension products to be adapted for use in additional end-markets and in the mountain bike and powered vehicle categories.

We believe the high-end segments in which we participate are well positioned for growth due to several factors, including:

| • | increasing average retail sales prices, which we believe are driven by differentiated and feature-rich products with advanced technologies; |

| • | continuing product cycle innovation, which we have observed often motivates consumers to upgrade and purchase new products for enhanced performance; |

| • | branded auto OEMs introducing on-road vehicles with off-road capabilities, such as the Ford F-150 SVT Raptor; and |

| • | increased sales opportunities for high-end mountain bikes and powered vehicles in international markets. |

As vehicles in our end-markets evolve and grow more capable, suspension products and components have become, and we believe will continue to become, increasingly more important for improved performance and control. Additionally, we believe there are opportunities to continue to leverage our technical know-how in suspension products to provide solutions beyond our current end-markets.

-2-

Table of Contents

Our competitive strengths

Broad offering of high-performance products across multiple consumer markets

Our suspension products enhance ride dynamics across multiple consumer markets. Through the use of adjustable suspension, position sensitive damping, multiple air spring technologies, lightweight and rigid materials, and other technologies and methods, our products improve the performance and control of the vehicles used by our consumers. We believe our reputation for high-performance products is reinforced by the successful finishes in world class competitive events by athletes incorporating our products in their vehicles, including the following examples in 2012:

| • | three out of four Union Cycliste Internationale World Cup Mountain Bike Series titles; |

| • | World Off Road Championship Series Side x Side Production 1000 Class Championship; |

| • | American Motorcyclist Association, or AMA, Pro ATV Championship and first place finishes in 10 out of 10 races; |

| • | International Series of Champions National Pro Open Championship for snowmobiles and first place finishes in 16 out of 16 races; and |

| • | two out of two overall Pro 2 Championships and first place finishes in 21 out of 29 Pro 2 races in the TORC and LOORRS off-road short course racing series. |

Premium brand with strong consumer loyalty

We believe that we have developed a reputation for high-performance products and that we have established a premium brand, as our high-performance suspension products are generally sold at premium prices. Our logo is prominently displayed on our products used on mountain bikes and powered vehicles sold by our OEM customers, which helps further reinforce our brand image. To support our brand, we introduce new products that we believe feature innovative technologies designed to improve vehicle performance and enhance our brand loyalty with consumers. For instance, according to a 2012 independent survey conducted by Bike Germany Magazine, a leading European mountain bike magazine, FOX was voted as the best brand for suspension forks and 81.7% of FOX consumers surveyed stated that they would buy a FOX suspension fork again, and in a 2011 Audience Survey by Vital MTB, a popular mountain bike website: (i) of the 44.5% of survey respondents that stated they would buy a mountain bike suspension fork within 12 months, 41.0% of these respondents, the highest percentage of all brands included, stated that they would buy a FOX suspension fork; and (ii) of the 22.4% of survey respondents that stated they would buy a rear mountain bike shock within 12 months, 42.2% of these respondents, again the highest percentage of all brands included, stated that they would buy a FOX rear shock.

Track record of innovation and new product introductions

Innovation, including new product development, is a key component of our growth strategy. Due to our experience in suspension engineering and design in multiple markets and with a variety of

-3-

Table of Contents

vehicles, we are able to bring unique ride dynamics solutions to our customers, often developed for use in one market and ultimately deployed across multiple markets. For example, our success in the high-end ATV category led to the wide-spread adoption of our suspension technology in the Side-by-Side market, which became our second largest product category by sales in 2012. Our innovative product development and speed to market are supported by:

| • | our racing culture, including on-site technical race support of professional athletes, which provides us with unique real-time insights as to the evolving ride dynamic needs of those participating in world-class events; |

| • | ongoing research and development through a team of more than 20 full-time engineers and numerous other technicians and employees who spend at least part of their time testing and using our products and helping develop engineering-based solutions to enhance our product offerings; |

| • | feedback from professional athletes, race teams, enthusiasts and other consumers seeking to improve the performance and control of their vehicles through our products; |

| • | strategic and collaborative relationships with OEM customers, which furthers our ability to extend technologies and applications across end-markets; and |

| • | our integrated manufacturing facilities and performance testing center, which allow us to quickly move from concept to product. |

During 2012, we launched more than 20 new products and generated more than 70% of our sales from products introduced by us during the last three years, such as the:

| • | Podium RC3, which provides external adjustment that allows the shock to easily be tuned for different rider skill, terrain, and racing type without having to be disassembled; |

| • | Float X Evol, which allows the rider to tune the spring characteristics of the shock via an air pump without having to remove the shock; |

| • | ECS Shock, which has an external cooling system that significantly lowers shock temperatures, allowing powered vehicles to operate at higher speeds for extended periods without sacrificing driver control, particularly in extreme environments; and |

| • | Float iCD, which provides riders the ability to adjust modes for different skills, terrains and activity levels on mountain bikes, resulting in increased utilization of the modes and an overall more efficient ride dynamics experience. |

Strategic brand for OEMs, dealers and distributors

Through our strategic relationships, we are often sought out by our OEM customers and work closely with them to develop and design new products and product enhancements. We believe our collaborative approach and product development processes strengthen our relationships with our OEM customers. We believe consumers value our branded suspension products when selecting high-performance mountain bikes and powered vehicles, and as a result, OEMs purchase and incorporate our products in their mountain bikes and powered vehicles in order to increase the sales of their premium priced products. In addition, we believe the inclusion of our

-4-

Table of Contents

products on high-end mountain bikes and powered vehicles reinforces our premium brand image, which helps to drive our sales in the aftermarket channel where dealers and distributors sell our products to consumers.

Experienced management team

We have an experienced senior management team led by Larry L. Enterline, our Chief Executive Officer. Collectively, our eight member senior management team has an average tenure at FOX of approximately eight years per person. In addition, many members of our management team and many of our employees are avid users of our products, which further extends their knowledge of, and expertise in, our products and end-markets. We are able to attract and retain highly-trained and specialized employees who enhance our company culture and serve as strong brand advocates.

Our strategy

Our goal is to expand our leadership position as a designer, manufacturer and marketer of high-performance products designed to enhance ride dynamics. We intend to focus on the following key strategies in pursuit of this goal:

Continue to develop new and innovative products in current end-markets

We intend to continue to develop and introduce new and innovative products in our current end-markets to improve ride dynamics for our consumers. For example, our patented position sensitive damping systems provide terrain optimized ride characteristics across many of our product lines. We believe that high-performance and control are important to a large portion of our consumer base and that our frequent introduction of products with innovative and improved technologies increases both OEM and aftermarket demand as consumers seek out components for their vehicles that can deliver these characteristics. We also believe evolving market trends, such as changing mountain bike wheel sizes and increasing adoption rates of Side-by-Side vehicles, should increase demand for vehicles in our end-markets, which, in turn, should increase demand for our suspension products.

Leverage technology and brand to expand into new categories and end-markets

We believe that we have developed a reputation as a leader in ride dynamics, and that our reputation combined with our ability to improve the performance of vehicles by incorporating high-performance suspension products, results in us often being approached by OEM product development teams, athletes and others looking to improve the performance of their vehicles, including in end-markets in which we have not previously offered products. We believe that our ride dynamics technologies have applications in end-markets in which we do not currently participate in a meaningful way, and we intend to selectively develop products for and forge relationships with customers in additional markets. These markets may include military, recreational vehicles (RVs), on-road motorcycles, commercial trucks and “performance street” cars. We also intend to evaluate selective potential acquisition opportunities for high-performance products and technologies that we believe will help us extend our ride dynamics platform.

-5-

Table of Contents

Increase our aftermarket penetration

We currently have a broad aftermarket distribution network of more than 2,300 retail dealers and distributors worldwide. We intend to further penetrate the aftermarket channel by selectively adding dealers and distributors in certain geographic markets, increasing our internal sales force and strategically expanding aftermarket-specific products and services to existing vehicle platforms.

Accelerate international growth

While a significant percentage of our current sales are to OEMs and dealers and distributors located outside the United States, we believe international expansion represents a significant opportunity for us and we intend to selectively increase infrastructure investments and focus on identified geographic regions. We believe that rising consumer discretionary income in a number of developing markets and increasing consumer preferences for premium, high-performance mountain bikes and powered vehicles, should contribute to increasing demand for our products. We intend to leverage our brand recognition to capitalize on these trends by increasing our sales to both OEMs and dealers and distributors globally, particularly in markets where we perceive significant opportunities. Our areas of greatest interest include Asia-Pacific (including China, South Korea and Australia) and South America (particularly Brazil, Argentina and Chile).

Improve operating and supply chain efficiencies

We intend to improve operating margins in the medium term by enhancing our design and production processes to increase efficiencies, reducing new product time to market and lowering production costs. Specifically, we have begun the process of moving a majority of the manufacturing of our mountain bike products to Taiwan and intend to complete this process in 2015. We believe this transition to Taiwan, once completed, will shorten production lead times to our mountain bike OEM customers, improve supply chain efficiencies and reduce manufacturing costs.

Risks related to our business

Our business is subject to numerous risks and uncertainties, including those highlighted in the section titled “Risk factors,” which you should read carefully before making a decision to invest in our common stock. Some of these risks include:

| • | we may not be able to continue to enhance existing products and develop and market new products that respond to consumer needs and preferences and achieve market acceptance; |

| • | we face intense competition across all product lines and may be unable to effectively compete against our competitors, which would harm our business and operating results; |

| • | our suspension products, and the products into which they are incorporated, are discretionary purchases and may be adversely impacted by changes in the economy and economic conditions that impact consumer spending; |

| • | if we are unable to maintain our premium brand image, our business may suffer; |

-6-

Table of Contents

| • | our dependence on the demand for high-end mountain bikes and their suspension components to maintain and foster sales; |

| • | our dependence upon the expansion of the market for powered vehicles that require high-performance suspension systems to continue our growth in this product category; |

| • | a disruption in our operations or manufacturing facilities, including any disruption in connection with the transition of a majority of the manufacturing of our mountain bike products to Taiwan, would adversely affect our business, financial condition and results of operations; |

| • | we depend on the continuing efforts of our senior management and skilled engineers, and our business may be severely disrupted and adversely impacted if we lose their services; |

| • | we depend on a relatively small number of customers for a substantial portion of our sales; and |

| • | the trading price of our common stock may be volatile, a market for our securities may not develop or be maintained and our stock price may decline. |

Our history

Robert C. Fox, Jr. began developing suspension products in 1974 when, having participated in motocross racing, he sought to create a racing suspension shock that performed better than existing coil spring shocks. Working in a friend’s garage, Mr. Fox created the “Fox AirShox.” The product was successful, and went into production in 1975. The next year, in 1976, Fox AirShox were used by the rider who won the AMA 500cc National Motocross Championship.

Sales of Fox AirShox grew rapidly and, in 1978, our operating subsidiary, Fox Factory, Inc., was incorporated in California. From 1978 to 1983, FOX suspension users won numerous major races including 500cc Grand Prix races (motocross), Baja 1000 races (off-road), AMA SuperBike races (motorcycle road racing), and the Indianapolis 500 race (auto racing), generating greater market awareness of the FOX brand among enthusiasts.

As FOX grew, we applied many of the same core suspension technologies developed for motocross racing to other categories. For example, in 1987 we started selling high-performance suspension products for snowmobiles. By 1991, we began supplying the mountain bike industry with rear shocks and we entered the ATV and other off-road vehicle markets in the mid-1990s. Starting in 2001, we began offering front fork suspension products for mountain bikes.

Fox Factory Holding Corp., the registrant of this offering, is the holding company of Fox Factory, Inc. Fox Factory Holding Corp. was incorporated in Delaware on December 28, 2007 by Compass Group Diversified Holdings LLC, or our Sponsor. Our Sponsor purchased a controlling interest in us on January 4, 2008.

For clarification, we are not affiliated with Fox Head, Inc., or Fox Head, an action sports apparel company, although we have entered into an agreement with Fox Head clarifying the parties’ respective use of ”Fox” tradenames and service marks.

-7-

Table of Contents

Our Sponsor

Our Sponsor, Compass Group Diversified Holdings LLC, acquires and manages a diversified group of leading middle-market businesses headquartered in North America. Our Sponsor’s parent, Compass Diversified Holdings, is listed on the New York Stock Exchange, or NYSE, under the symbol “CODI.” As of March 31, 2013, in addition to us, our Sponsor owned a controlling interest in the following businesses: (i) Compass AC Holdings, Inc., or Advanced Circuits, a provider of prototype, quick-turn and volume production rigid printed circuit boards; (ii) American Furniture Manufacturing, Inc., a leading domestic manufacturer of upholstered furniture for the promotional segment of the marketplace; (iii) Arnold Magnetic Technologies Holdings Corporation, a leading global manufacturer of engineered magnetic solutions for a wide range of specialty applications and end-markets; (iv) CamelBak Products, LLC, a designer and manufacturer of personal hydration products for outdoor, recreation and military use; (v) The ERGO Baby Carrier, Inc., a premier designer, marketer and distributor of baby wearing products, a premium line of stroller travel systems and related accessories; (vi) Liberty Safe and Security Products, Inc., a designer, manufacturer and marketer of premium home and gun safes in North America; and (vii) Anodyne Medical Device, Inc., rebranded as Tridien, a leading designer and manufacturer of powered and non-powered medical therapeutic support surfaces and patient positioning devices serving the acute care, long-term care and home health care markets.

Our Sponsor is a selling stockholder in this offering, and upon completion of this offering, is expected to own approximately % of our outstanding common stock.

Recapitalization

In June 2012, we engaged in a recapitalization involving our debt, stock options and various share purchases. In connection with our recapitalization, we entered into an amendment to our credit facility with our Sponsor, which we refer to as our Existing Credit Facility, which, among other changes, provided for a $60.0 million term loan and increased the revolver commitment under that facility by $2.0 million to a total commitment of $30.0 million. Borrowings under our Existing Credit Facility in large part enabled us to fund a $67.0 million cash dividend to our stockholders as part of the recapitalization. The recapitalization also included other transactions, including various transactions involving our stock options and purchases and sales of shares of our stock among us, our sponsor and certain of our executives and directors. Concurrently with the closing of this offering, we intend to use the net proceeds that we will receive from this offering to repay our then outstanding indebtedness under our Existing Credit Facility and enter into a new credit facility with a third party lender, which we refer to as the New Credit Facility. The consummation of this offering is conditioned on the closing of the New Credit Facility. To the extent the net proceeds from this offering are insufficient to allow us to fully repay the indebtedness then outstanding under our Existing Credit Facility, we intend to use borrowings under our New Credit Facility to pay any remaining balance outstanding under our Existing Credit Facility. We intend to terminate the Existing Credit Facility upon the consummation of this offering. See “Use of proceeds,” “Management’s discussion and analysis of financial condition and results of operations” and “Related party transactions—Recapitalization.”

-8-

Table of Contents

Recent developments

Below is a summary of our results of operations for the three months ended June 30, 2013. The financial data below has been prepared by, and is the responsibility of, management. Management has completed its quarter-end financial closing procedures for the three months ended June 30, 2013 but complete financial statements for this period, including the related footnote disclosures, are not yet available.

This summary is not meant to be a comprehensive presentation of our unaudited financial results for June 30, 2013 and the three months then ended.

The following are our results of operations as of June 30, 2013 and for the three months then ended:

| • | sales of $ million; |

| • | cost of sales of $ million; |

| • | gross profit of $ million; |

| • | total operating expense of $ million; |

| • | income from operations of $ million; |

| • | net income of $ million; |

| • | Adjusted EBITDA of $ million; and |

| • | accounts receivable of $ million. |

Adjusted EBITDA is a financial measure that is not calculated in accordance with GAAP. See “Summary consolidated financial data—Non-GAAP financial measures” for a definition of Adjusted EBITDA, as well as reasons why management believes the inclusion of Adjusted EBITDA is appropriate. The following table presents a reconciliation of expected Adjusted EBITDA to our expected net income, the most comparable GAAP measure, for the three months ended June 30, 2013.

| For the three months

ended June 30, 2013 ( unaudited) |

||||

| (in thousands) | ||||

| Reconciliation of net income to Adjusted EBITDA |

||||

| Net income |

$ | |||

| Interest expense |

||||

| Other (income) expense, net(1) |

||||

| Provision for income taxes |

||||

| Depreciation and amortization |

||||

| Stock-based compensation(2) |

||||

| Management fee paid(3) |

||||

|

|

|

|||

| Adjusted EBITDA |

$ | |||

|

|

|

|||

|

|

|

|||

|

|

|

|||

| (1) | Other (income) expense, net includes gain or loss on the disposal of fixed assets, foreign currency transaction gain or loss, forgiveness of indebtedness under our loan with the Redevelopment Agency of the City of Watsonville, and other miscellaneous items. |

9

Table of Contents

| (2) | Represents non-cash, stock-based compensation (before tax effect). |

| (3) | Represents management fees paid to an affiliate of our Sponsor pursuant to a management services agreement that will terminate on the consummation of this offering. Such fees are paid by us quarterly in arrears and other than paying any accrued but unpaid fees for the quarter during which this offering closes, no separate termination fee will be due under this agreement when it is terminated. |

Corporate information

Our principal executive offices are located at 915 Disc Drive, Scotts Valley, CA 95066, and our telephone number is (831) 274-6500. Our website address is www.ridefox.com. In addition, we maintain a Facebook page at www.facebook.com/fox, a YouTube channel at www.youtube.com/foxracingshox1, a Vimeo page at www.vimeo.com/foxracingshox and a Twitter feed at www.twitter.com/foxracingshox. Information contained on, or that can be accessed through, our website, Facebook page, YouTube channel, Vimeo page or Twitter feed does not constitute part of this prospectus and inclusions of our website address, Facebook page address, YouTube channel address, Vimeo page address and Twitter feed address in this prospectus are inactive textual references only.

We have a number of registered marks, including, without limitation, FOX®, FOX RACING SHOX® and REDEFINE YOUR LIMITS® in several jurisdictions, including the United States, and we have also applied to register a number of other marks in various jurisdictions. This prospectus includes trademarks and trade names of other companies. All trademarks and trade names appearing in this prospectus are the property of their respective holders. We do not intend our use or display of other companies’ trade names or trademarks to imply a relationship with, or endorsement or sponsorship of us by, these other companies.

Emerging growth company status

We are an “emerging growth company,” as that term is defined in Section 2(A) of the Securities Act of 1933, as amended, or the Securities Act, as modified by the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. For as long as we qualify as an emerging growth company, we may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that do not qualify as emerging growth companies, including, without limitation, not being required to comply with the auditor attestation requirements of Section 404(b) of the Sarbanes-Oxley Act of 2002, reduced disclosure obligations relating to executive compensation and exemptions from the requirements of holding advisory “say-on-pay,” “say-when-on-pay” and “golden parachute” executive compensation votes.

Under the JOBS Act, we will remain an emerging growth company until the earliest of:

| • | the last day of the fiscal year during which we have total annual gross revenues of $1 billion or more; |

| • | the last day of the fiscal year following the fifth anniversary of the completion of this offering; |

| • | the date on which we have, during the previous three-year period, issued more than $1 billion in non-convertible debt; or |

10

Table of Contents

| • | the date on which we are deemed to be a “large accelerated filer” under the Securities Exchange Act of 1934, as amended, or the Exchange Act (i.e., the first day of the fiscal year after we have (i) more than $700 million in outstanding common equity held by our non-affiliates, measured each year on the last day of our second fiscal quarter, and (ii) been public for at least 12 months). |

The JOBS Act also provides that an emerging growth company can utilize the extended transition period provided in Section 7(a)(2)(B) of the Securities Act, for complying with new or revised accounting standards. However, we are choosing to “opt out” of such extended transition period, and, as a result, we will comply with new or revised accounting standards on the relevant dates on which adoption of such standards is required for companies that are not emerging growth companies. Section 107 of the JOBS Act provides that our decision to opt out of the extended transition period for complying with new or revised accounting standards is irrevocable.

-11-

Table of Contents

The offering

| Common stock offered by us |

shares |

| Common stock offered by the selling stockholders |

shares |

| Underwriters option to purchase additional shares |

The underwriters have an option, exercisable for 30 days after the date of this prospectus, to purchase up to an additional shares from the selling stockholders. |

| Common stock to be outstanding after this offering |

shares |

| Use of proceeds |

We estimate that the net proceeds from the sale of shares of our common stock that we are selling in this offering will be approximately $ million, after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us, assuming an initial public offering price of $ per share, which is the midpoint of the initial public offering price range listed on the cover page of this prospectus. We will not receive any proceeds from the sale of shares by the selling stockholders. |

| We currently intend to use the net proceeds that we will receive from this offering to repay the then outstanding indebtedness under our Existing Credit Facility. To the extent the net proceeds from this offering are insufficient to allow us to fully repay the indebtedness then outstanding under our Existing Credit Facility, we intend to use borrowings under our New Credit Facility to pay any remaining balance outstanding under the Existing Credit Facility. To the extent we receive net proceeds from this offering in excess of the then outstanding indebtedness under our Existing Credit Facility, we intend to use such excess net proceeds for working capital and other general corporate purposes. See “Use of proceeds.” |

| Directed share program |

The underwriters have reserved for sale, at the initial public offering price, up to approximately shares of our common stock being offered for sale to certain of our business associates, officers, directors, employees and certain of their family members. We will offer these shares to the extent permitted under applicable regulations in the United States and in various countries. The number of shares available for sale to the general public in this offering will be reduced to the extent these persons purchase reserved shares. Any reserved shares not purchased will be offered by the underwriters to the general public on the same terms as the other shares. |

-12-

Table of Contents

| Concentration of ownership |

Upon completion of this offering, our executive officers and directors, and their affiliates, will beneficially own, in the aggregate, approximately % of our outstanding shares of common stock, and our Sponsor will own approximately % of our outstanding shares of common stock. |

| Dividend policy |

Currently, we do not anticipate paying cash dividends. |

| Proposed Nasdaq Global Select Market symbol |

“FOXF” |

The number of shares of common stock that will be outstanding after this offering is based on shares outstanding as of March 31, 2013, and excludes:

| • | 54,062 shares of common stock issuable upon the exercise of options to purchase common stock that were outstanding as of March 31, 2013, with a weighted average exercise price of $226.22 per share; |

| • | shares of common stock issuable upon the exercise of options to purchase common stock granted after March 31, 2013, with a weighted average exercise price of $ per share; and |

| • | shares of common stock reserved for issuance under our 2013 Omnibus Plan. |

Except as otherwise indicated, all information in this prospectus assumes:

| • | a -for- split of our common stock, which will occur prior to the effectiveness of the registration statement of which this prospectus forms a part; |

| • | the filing and effectiveness of our Amended and Restated Certificate of Incorporation in Delaware and the adoption of our Amended and Restated Bylaws, each of which will occur immediately prior to the completion of this offering; and |

| • | no exercise by the underwriters of their option to purchase up to an additional shares of common stock from the selling stockholders in this offering. |

-13-

Table of Contents

Summary consolidated financial data

The following table sets forth our summary consolidated financial data as of the dates and for the periods indicated. We have derived the summary statements of income data for the years ended December 31, 2010, 2011 and 2012 from our audited consolidated financial statements included elsewhere in this prospectus. The summary statements of income for the three months ended March 31, 2012 and 2013, and the selected consolidated balance sheet data as of March 31, 2013 are derived from our unaudited consolidated financial statements appearing elsewhere in this prospectus. The unaudited consolidated financial statements were prepared on a basis consistent with our audited consolidated financial statements and include, in the opinion of management, all adjustments necessary for the fair presentation of the financial information set forth in those statements.

The historical results presented below are not necessarily indicative of the results to be expected for any future period, and the results for any interim period may not necessarily be indicative of the results for the full year. The following summaries of our consolidated financial data for the periods presented should be read in conjunction with “Risk factors,” “Selected consolidated financial data,” “Capitalization,” “Management’s discussion and analysis of financial condition and results of operations” and our consolidated financial statements and the related notes, which are included elsewhere in this prospectus.

| For the years ended December 31, |

For the three months ended March 31, |

|||||||||||||||||||

|

|

|

|||||||||||||||||||

| (in thousands, except per share data) | 2010 | 2011 | 2012 | 2012 | 2013 | |||||||||||||||

|

|

||||||||||||||||||||

| Sales |

$ | 170,983 | $ | 197,739 | $ | 235,869 | $ | 45,671 | $ | 54,878 | ||||||||||

| Cost of sales(1) |

122,373 | 140,849 | 173,040 | 32,572 | 39,163 | |||||||||||||||

|

|

|

|||||||||||||||||||

| Gross profit |

48,610 | 56,890 | 62,829 | 13,099 | 15,715 | |||||||||||||||

| Operating expenses: |

||||||||||||||||||||

| Sales and marketing(1) |

10,293 | 11,748 | 12,570 | 3,177 | 3,284 | |||||||||||||||

| Research and development(1) |

7,321 | 9,750 | 9,727 | 2,376 | 2,355 | |||||||||||||||

| General and administrative(1) |

6,202 | 7,588 | 9,063 | 1,951 | 2,673 | |||||||||||||||

| Amortization of purchased intangibles |

5,217 | 5,217 | 5,315 | 1,304 | 1,341 | |||||||||||||||

|

|

|

|||||||||||||||||||

| Total operating expenses |

29,033 | 34,303 | 36,675 | 8,808 | 9,653 | |||||||||||||||

|

|

|

|||||||||||||||||||

| Income from operations |

19,577 | 22,587 | 26,154 | 4,291 | 6,062 | |||||||||||||||

| Other expense, net: |

||||||||||||||||||||

| Interest expense |

(2,637 | ) | (1,982 | ) | (3,486 | ) | (233 | ) | (957 | ) | ||||||||||

| Other income (expense), net |

39 | (13 | ) | (277 | ) | (46 | ) | 34 | ||||||||||||

|

|

|

|||||||||||||||||||

| Total other expense, net |

(2,598 | ) | (1,995 | ) | (3,763 | ) | (279 | ) | (923 | ) | ||||||||||

|

|

|

|||||||||||||||||||

| Income before income taxes |

16,979 | 20,592 | 22,391 | 4,012 | 5,139 | |||||||||||||||

| Provision for income taxes |

6,210 | 7,054 | 8,181 | 1,373 | 1,590 | |||||||||||||||

|

|

|

|||||||||||||||||||

| Net income |

$ | 10,769 | $ | 13,538 | $ | 14,210 | $ | 2,639 | $ | 3,549 | ||||||||||

|

|

|

|||||||||||||||||||

| Earnings per share (actual and pro forma): |

||||||||||||||||||||

| Basic |

$ | 16.62 | $ | 20.92 | $ | 20.59 | $ | 4.04 | $ | 4.93 | ||||||||||

| Diluted |

$ | 15.72 | $ | 19.45 | $ | 20.30 | $ | 3.76 | $ | 4.83 | ||||||||||

| Weighted average common shares used to compute net income per share (actual and pro forma): |

||||||||||||||||||||

| Basic |

648 | 647 | 690 | 653 | 720 | |||||||||||||||

| Diluted |

685 | 696 | 700 | 701 | 735 | |||||||||||||||

| Supplemental pro forma net income per share (unaudited)(2) |

||||||||||||||||||||

| Shares used to calculate supplemental pro forma net income per share (unaudited) |

||||||||||||||||||||

| Dividends per share |

$ | — | $ | — | $ | 92.99 | $ | — | $ | — | ||||||||||

|

|

||||||||||||||||||||

-14-

Table of Contents

| (1) | Includes stock-based compensation (excluding tax effect) as follows: |

| For the years ended December 31, |

For the three months ended March 31, |

|||||||||||||||||||

|

|

|

|||||||||||||||||||

| (in thousands) |

2010 | 2011 | 2012 | 2012 | 2013 | |||||||||||||||

|

|

||||||||||||||||||||

| Cost of sales |

$ | — | $ | — | $ | — | $ | — | $ | — | ||||||||||

| Sales and marketing |

40 | 78 | 160 | 33 | 33 | |||||||||||||||

| Research and development |

12 | 12 | 29 | 3 | 17 | |||||||||||||||

| General and administrative |

472 | 940 | 1,959 | 267 | 652 | |||||||||||||||

|

|

|

|||||||||||||||||||

| Total |

$ | 524 | $ | 1,030 | $ | 2,148 | $ | 303 | $ | 702 | ||||||||||

|

|

|

|||||||||||||||||||

|

|

||||||||||||||||||||

| (2) | Unaudited supplemental pro forma net income per share has been presented in accordance with the SEC Staff Accounting Bulletin Topic 1.B.3, or SAB 1.B.3. As outlined in SAB 1.B.3, the special dividend paid in June 2012 was in excess of the net income for the twelve-months ended March 31, 2013 of $15.1 million. Accordingly, under SAB 1.B.3, the company has included all shares, for which proceeds accrue to the company, issued under this offering in the shares used to calculate supplemental pro forma net income per share. |

The following table presents our summary consolidated balance sheet data as of March 31, 2013 and is presented:

| • | on an actual basis; and |

| • | on a pro forma as adjusted basis: (i) reflecting the filing of our Amended and Restated Certificate of Incorporation immediately prior to the consummation of this offering; (ii) the sale of shares of common stock by us in this offering at an estimated initial offering price of $ per share, which is the midpoint of the range of the initial public offering price listed on the cover page of this prospectus, after deducting assumed underwriting discounts and commissions and estimated offering expenses payable by us; and (iii) the application of such proceeds to repay a majority of the then outstanding indebtedness under our Existing Credit Facility concurrently with the closing of this offering. |

| As of March 31, 2013 (in thousands) |

Actual | Pro forma as adjusted (unaudited) |

||||||

|

|

||||||||

| Consolidated balance sheet data(1): |

||||||||

| Cash and cash equivalents |

$ | 136 | $ | |||||

| Inventory |

42,734 | |||||||

| Working capital |

23,786 | |||||||

| Property and equipment, net |

12,105 | |||||||

| Total assets |

147,429 | |||||||

| Total debt, including current portion |

52,850 | |||||||

| Total stockholders’ equity |

$ | 33,828 | $ | |||||

|

|

||||||||

| (1) | A $1.00 increase in the assumed initial public offering price of $ per share would decrease total debt, including current portion, and would increase total stockholders’ equity by $ million, assuming the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting estimated underwriting discounts and commissions. A $1.00 decrease in the assumed initial offering price of $ per share would increase total debt, including current portion, and would decrease total stockholders’ equity by $ million, assuming the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting estimated underwriting discounts and commissions. An increase of 100,000 shares in the number of shares sold in this offering by us would decrease total debt, including current portion, and would increase total stockholders’ equity from this offering by $ million, assuming an initial public offering price of $ per share and after deducting estimated underwriting discounts and commissions. A decrease of 100,000 shares in the number of shares sold in this offering by us would increase total debt, including current portion, and would decrease total stockholders’ equity from this offering by $ million, assuming an initial public offering price of $ per share and after deducting estimated underwriting discounts and commissions. |

-15-

Table of Contents

Non-GAAP financial measures

Adjusted EBITDA is a financial measure that is not calculated in accordance with generally accepted accounting principles in the United States, or GAAP. We define Adjusted EBITDA as net income adjusted for interest expense, other income (expense), net, provision for income taxes, depreciation and amortization, stock-based compensation and the management fee payable to an affiliate of our Sponsor (which fee will be discontinued upon completion of this offering). Below, we have provided a reconciliation of Adjusted EBITDA to our net income, the most directly comparable financial measure calculated and presented in accordance with GAAP. Adjusted EBITDA should not be considered as an alternative to net income or any other measure of financial performance calculated and presented in accordance with GAAP.

We include Adjusted EBITDA in this prospectus because we believe it allows investors to understand and evaluate our core operating performance and trends. In particular, the exclusion of certain expenses in calculating adjusted EBITDA can provide a useful measure for period-to-period comparisons of our core business.

Our use of Adjusted EBITDA has limitations as an analytical tool. Some of these limitations are:

| • | Adjusted EBITDA does not include the impact of equity-based compensation; |

| • | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized may have to be replaced in the future, and Adjusted EBITDA does not reflect capital expenditure requirements for such replacements; |

| • | Adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital needs; |

| • | Adjusted EBITDA does not reflect the interest expense or the cash requirements necessary to service interest or principal payments on our indebtedness; |

| • | Adjusted EBITDA does not include other income or expense such as gain or loss on the disposal of fixed assets, foreign currency transaction gain or loss and other miscellaneous items; |

| • | Adjusted EBITDA does not reflect income tax payments that may represent a reduction in cash available to us; |

| • | Adjusted EBITDA does not reflect the cash fees which we paid to our Sponsor; and |

| • | other companies, including companies in our industry, may calculate Adjusted EBITDA measures differently, which reduces its usefulness as a comparative measure. |

In evaluating Adjusted EBITDA, you should be aware that in the future we will incur expenses similar to the adjustments in this presentation. Our presentation of Adjusted EBITDA should not be construed as an inference that our future results will be unaffected by these expenses or any unusual or non-recurring items. When evaluating our performance, you should consider Adjusted EBITDA alongside other financial performance measures, including our net income and other GAAP results.

-16-

Table of Contents

The following table presents a reconciliation of Adjusted EBITDA to our net income, the most comparable GAAP measure, for each of the periods indicated:

| For the years ended December 31, | For the three months ended March 31, |

|||||||||||||||||||

|

|

|

|||||||||||||||||||

| (in thousands) | 2010 | 2011 | 2012 | 2012 | 2013 | |||||||||||||||

|

|

||||||||||||||||||||

| Reconciliation of net income to Adjusted EBITDA |

||||||||||||||||||||

| Net income |

$ | 10,769 | $ | 13,538 | $ | 14,210 | $ | 2,639 | $ | 3,549 | ||||||||||

| Interest expense |

2,637 | 1,982 | 3,486 | 233 | 957 | |||||||||||||||

| Other (income) expense, net(1) |

(39 | ) | 13 | 277 | 46 | (34 | ) | |||||||||||||

| Provision for income taxes |

6,210 | 7,054 | 8,181 | 1,373 | 1,590 | |||||||||||||||

| Depreciation and amortization |

6,150 | 6,598 | 7,204 | 1,713 | 1,885 | |||||||||||||||

| Stock-based compensation(2) |

524 | 1,030 | 2,148 | 303 | 702 | |||||||||||||||

| Management fee paid(3) |

500 | 500 | 500 | 125 | 125 | |||||||||||||||

|

|

|

|||||||||||||||||||

| Adjusted EBITDA |

$ | 26,751 | $ | 30,715 | $ | 36,006 | $ | 6,432 | $ | 8,774 | ||||||||||

|

|

|

|||||||||||||||||||

|

|

||||||||||||||||||||

| (1) | Other (income) expense, net includes gain or loss on the disposal of fixed assets, foreign currency transaction gain or loss, forgiveness of indebtedness under our loan with the Redevelopment Agency of the City of Watsonville, and other miscellaneous items. |

| (2) | Represents non-cash, stock-based compensation (before tax effect). |

| (3) | Represents management fees paid to an affiliate of our Sponsor pursuant to a management services agreement that will terminate on the consummation of this offering. Such fees are paid by us quarterly in arrears and other than paying any accrued but unpaid fees for the quarter during which this offering closes, no separate termination fee will be due under this agreement when it is terminated. |

-17-

Table of Contents

Investing in our common stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below, together with all of the other information in this prospectus, before making a decision to invest in our common stock. If any of the risks actually occur, our business, financial condition, operating results and prospects could be materially and adversely affected. In that event, the trading price of our common stock could decline, and you could lose part or all of your investment.

Risks related to our business

If we are unable to continue to enhance existing products and develop and market new products that respond to consumer needs and preferences and achieve market acceptance, we may experience a decrease in demand for our products, and our business and financial results could suffer.

Our growth strategy involves the continuous development of innovative high-performance products. For instance, during 2012, we generated more than 70% of our sales from products that we introduced during the last three years. We may not be able to compete as effectively with our competitors, and ultimately satisfy the needs and preferences of our customers and the end users of our products, unless we can continue to enhance existing products and develop new, innovative products in the global markets in which we compete. In addition, we must continuously compete not only for end users who purchase our products through the dealers and distributors who are our customers, but also for the OEMs which incorporate our products into their mountain bikes and powered vehicles. These OEMs regularly evaluate our products against those of our competitors to determine if they are allowing the OEMs to achieve higher sales and market share on a cost-effective basis. Should one or more of our OEM customers determine that they could achieve overall better financial results by incorporating a competitors’ new or existing product, they would likely do so, which could harm our business, financial condition or results of operations.

Product development requires significant financial, technological and other resources. While we expended approximately $7.3 million, $9.8 million and $9.7 million for our research and development efforts in 2010, 2011 and 2012, respectively, there can be no assurance that this level of investment in research and development will be sufficient in the future to maintain our competitive advantage in product innovation, which could cause our business, financial condition or results of operations to suffer.

Product improvements and new product introductions require significant planning, design, development and testing at the technological, product and manufacturing process levels, and we may experience unanticipated delays in our introduction of product improvements or new products. Our competitors’ new products may beat our products to market, be more effective and/or less expensive than our products, obtain better market acceptance or render our products obsolete. Any new products that we develop may not receive market acceptance or otherwise generate any meaningful sales or profits for us relative to our expectations. In addition, one of our competitors could develop an unforeseen and entirely new product or technology that renders our products less desirable or obsolete, which could negatively affect our business, financial condition or results of operations.

-18-

Table of Contents

We face intense competition in all product lines, including from some competitors that may have greater financial and marketing resources. Failure to compete effectively against competitors would negatively impact our business and operating results.

The suspension industry is highly competitive. We compete with a number of other manufacturers that produce and sell suspension products to OEMs and aftermarket dealers and distributors, including OEMs that produce their own line of suspension products for their own use. Our continued success depends on our ability to continue to compete effectively against our competitors, some of which have significantly greater financial, marketing and other resources than we have. Also, several of our competitors offer broader product lines to OEMs, which they may sell in connection with suspension products as part of a package offering. In the future, our competitors may be able to maintain and grow brand strength and market share more effectively or quickly than we do by anticipating the course of market developments more accurately than we do, developing products that are superior to our products, creating manufacturing or distribution capabilities that are superior to ours, producing similar products at a lower cost than we can or adapting more quickly than we do to new technologies or evolving regulatory, industry or customer requirements, among other possibilities. In addition, we may encounter increased competition if our current competitors broaden their product offerings by beginning to produce additional types of suspension products or through competitor consolidations. We could also face competition from well-capitalized entrants into the high-performance suspension product market, as well as aggressive pricing tactics by other manufacturers trying to gain market share. As a result, our products may not be able to compete successfully with our competitors’ products, which could negatively affect our business, financial condition or results of operations.

Our business is sensitive to economic conditions that impact consumer spending. Our suspension products, and the mountain bikes and powered vehicles into which they are incorporated, are discretionary purchases and may be adversely impacted by changes in the economy.

Our business depends substantially on global economic and market conditions. In particular, we believe that currently a significant majority of the end users of our products live in the United States and countries in Europe. These areas are either in the process of recovering from recession or, in some cases, are still struggling with recession, disruption in banking and/or financial systems, economic weakness and uncertainty. In addition, our products are recreational in nature and are generally discretionary purchases by consumers. Consumers are usually more willing to make discretionary purchases during periods of favorable general economic conditions and high consumer confidence. Discretionary spending may also be affected by many other factors, including interest rates, the availability of consumer credit, taxes and consumer confidence in future economic conditions. During periods of unfavorable economic conditions, or periods when other negative market factors exist, consumer discretionary spending is typically reduced, which in turn could reduce our product sales and have a negative effect on our business, financial condition or results of operations.

There could also be a number of secondary effects resulting from an economic downturn, such as insolvency of our suppliers resulting in product delays, an inability of our OEM and distributor and dealer customers to obtain credit to finance purchases of our products, customers delaying payment to us for the purchase of our products due to financial hardship or an increase in bad debt expense. Any of these effects could negatively affect our business, financial condition or results of operations.

-19-

Table of Contents

If we are unable to maintain our premium brand image, our business may suffer.

Our products are selected by both OEMs and dealers and distributors in part because of the premium brand reputation we hold with them and our end users. Therefore, our success depends on our ability to maintain and build our brand image. We have focused on building our brand through producing products that we believe are innovative, high in performance and highly reliable. In addition, our brand benefits from our strong relationships with our OEM customers and dealers and distributors and through marketing programs aimed at mountain bike and powered vehicle enthusiasts in various media and other channels. For example, we sponsor a number of professional athletes and professional race teams. In order to continue to enhance our brand image, we will need to maintain our position in the suspension products industry and continue to provide high quality products and services. Also, we will need to continue to invest in sponsorships, marketing and public relations.

There can be no assurance, however, that we will be able to maintain or enhance the strength of our brand in the future. Our brand could be adversely impacted by, among other things:

| • | failure to develop new products that are innovative, high-performance and reliable; |

| • | internal product quality control issues; |

| • | product quality issues on the mountain bikes and powered vehicles on which our products are installed; |

| • | product recalls; |

| • | high profile component failures (such as a component failure during a race on a mountain bike ridden by an athlete that we sponsor); |

| • | negative publicity regarding our sponsored athletes; |

| • | high profile injury or death to one of our sponsored athletes; |

| • | inconsistent uses of our brand and our other intellectual property assets, as well as failure to protect our intellectual property; and |

| • | changes in consumer trends and perceptions. |

Any adverse impact on our brand could in turn negatively affect our business, financial condition or results of operations.

A significant portion of our sales are highly dependent on the demand for high-end mountain bikes and their suspension components and a material decline in the demand for these bikes or their suspension components could have a material adverse effect on our business or results of operations.

During 2012, approximately 67% of our sales were generated from the sale of suspension products for high-end mountain bikes. Part of our success has been attributable to the growth in the high-end mountain bike industry, including increases in average retail sales prices, as better-performing product designs and technologies have been incorporated into these products. If the popularity of high-end or premium priced mountain bikes does not increase or declines, the number of mountain bike enthusiasts seeking such mountain bikes or premium priced suspension products for their mountain bikes does not increase or declines, or the average price point of

-20-

Table of Contents

these bikes declines, we may fail to achieve future growth or our sales could decrease, and our business, financial condition or results of operations could be negatively affected. In addition, if current mountain bike enthusiasts stop purchasing our products due to changes in preferences, we may fail to achieve future growth or our sales could be decreased, and our business, financial condition or results of operations could be negatively affected.

Our growth in the powered vehicle category is dependent upon our continued ability to expand our product sales into powered vehicles that require high-performance suspension and the continued expansion of the market for these powered vehicles.

Our growth in the powered vehicle category is in part attributable to the expansion of the market for powered vehicles that require high-performance suspension products. Such market growth includes the creation of new classes of vehicles that need our products, such as Side-by-Sides, and our ability to create products for these vehicles. In the event these markets stopped expanding or contracted, or we were unsuccessful in creating new products for these markets or other competitors successfully enter into these markets, we may fail to achieve future growth or our sales could decrease, and our business, financial condition or results of operations could be negatively affected.

A disruption in the operations of our manufacturing facilities, including any disruption in connection with moving a majority of the manufacturing of our mountain bike products to Taiwan, could have a negative effect on our business, financial condition or results of operations.

During 2012, the sale of mountain bike suspension products accounted for approximately 67% of our sales. We recently began to transfer a majority of the manufacturing of our mountain bike products to Taiwan. We contemplate that this transition will continue through 2015, at which time we anticipate that virtually all of the manufacturing of our mountain bike products will be completed in Taiwan. During our transition process, we will incur some duplication of facilities, equipment and personnel, the amount of which could vary materially from our projections. Also, the transition process could cause manufacturing problems and give rise to execution risks, including disruptions to employees, negative impact on employee morale and retention, delays in recognizing efficiencies or increased costs of manufacturing, and adverse impacts on our product quality and delivery times. In addition, we could encounter unforeseen difficulties resulting from the distance and time zone differences between our main operations in California and our new Taiwan manufacturing facility. Should any of these problems occur, our business, financial condition or results of operations could be negatively affected.

Equipment failures, delays in deliveries or catastrophic loss at any of our facilities could lead to production or service disruptions, curtailments or shutdowns. In the event of a stoppage in production or a slowdown in production due to high employee turnover or a labor dispute at any of our facilities, even if only temporary, or if we experience delays as a result of events that are beyond our control, delivery times to our customers could be severely affected. If there was a manufacturing disruption in any of our manufacturing facilities, we might be unable to meet product delivery requirements and our business, financial condition or results of operations could be negatively affected, even if the disruption was covered in whole or in part by our business interruption insurance. Any significant delay in deliveries to our customers could lead to increased returns or cancellations, expose us to damage claims from our customers or damage our brand and, in turn, negatively affect our business, financial condition or results of operations.

-21-

Table of Contents

Our business depends substantially on the continuing efforts of our senior management, and our business may be severely disrupted if we lose their services.

We are heavily dependent upon the contributions, talent and leadership of our senior management team, particularly our Chief Executive Officer, Larry L. Enterline. We do not have a “key person” life insurance policy on Mr. Enterline or any other key employees. We believe that the top eight members of our senior management team are key to establishing our focus and executing our corporate strategies as they have extensive knowledge of our systems and processes. Given our senior management team’s knowledge of the suspension products industry and the limited number of direct competitors in the industry, we believe that it could be difficult to find replacements should any of the members of our senior management team leave. Our inability to find suitable replacements for any of the members of our senior management team could negatively affect our business, financial condition or results of operations.

We depend on skilled engineers to develop and create our products, and the failure to attract and retain such individuals could adversely affect our business.

We rely on skilled and well-trained engineers for the design and production of our products, as well as in our research and development functions. Competition for such individuals is intense, particularly in Silicon Valley near where our headquarters are located. Our inability to attract or retain qualified employees in our design, production or research and development functions or elsewhere in our company could result in diminished quality of our product and delinquent production schedules, impede our ability to develop new products and harm our business, financial condition or results of operations.

We may not be able to sustain our past growth or successfully implement our growth strategy, which may have a negative effect on our business, financial condition or results of operations.

We grew our sales from approximately $171.0 million in 2010 to approximately $235.9 million in 2012. This growth rate may be unsustainable. Our future growth will depend upon various factors, including the strength of our brand image, our ability to continue to produce innovative suspension products, consumer acceptance of our products, competitive conditions in the marketplace, the growth in emerging markets for products requiring high-end suspension products and, in general, the continued growth of the high-end mountain bike and powered vehicle markets into which we sell our products. Our beliefs regarding the future growth of markets for high-end suspension products are based largely on qualitative judgments and limited sources and may not be reliable. If we are unable to sustain our past growth or successfully implement our growth strategy, our business, financial condition or results of operations could be negatively affected.

The professional athletes and race teams who use our products are an important aspect of our brand image. The loss of the support of professional athletes for our products or the inability to attract new professional athletes may harm our business.

If our products are not used by current or future professional athletes and race teams, our brand could lose value and our sales could decline. While our sponsorship agreements typically restrict our sponsored athletes and race teams from promoting, endorsing or using competitors’ products that compete directly within our product categories during the term of the sponsorship agreements, we do not typically have long-term contracts with any of the athletes or race teams whom we sponsor.

-22-

Table of Contents

If we are unable to maintain our current relationships with these professional athletes and race teams, if these professional athletes and race teams are no longer popular, if our sponsored athletes and race teams fail to have success or if we are unable to continue to attract the endorsement of new professional athletes and race teams in the future, the value of our brand and our sales could decline.

We depend on our relationships with dealers and distributors and their ability to sell and service our products. Any disruption in these relationships could harm our sales.