Attached files

| file | filename |

|---|---|

| EX-23.1 - EXHIBIT 23.1 - VACCINOGEN INC | v349778_ex23-1.htm |

| EX-10.23 - EXHIBIT 10.23 - VACCINOGEN INC | v349778_ex10-23.htm |

As filed with the Securities and Exchange Commission on July 12, 2013

Registration No. _____________

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

VACCINOGEN, INC.

(Exact name of registrant as specified in its charter)

| Maryland | 5090 | 14-1997223 | ||

| (State or other Jurisdiction of Incorporation) | (Primary Standard Classification Code) | (IRS Employer Identification No.) |

5300 Westview Drive, Suite 406

Frederick, MD 21703

Tel.: (301) 668-8400

(Address and Telephone Number of Registrant’s Principal

Executive Offices and Principal Place of Business)

Michael G. Hanna, Jr., Ph.D

Chief Executive Officer

VACCINOGEN, INC.

5300 Westview Drive, Suite 406

Frederick, MD 21703

Tel.: (301) 668-8400

þ(Name, Address and Telephone Number of Agent for Service)

Copies of communications to:

Marc A. Indeglia, Esq.

Gregory R. Carney, Esq.

Indeglia& Carney, P.C.

1900 Main Street, Suite 300

Irvine, CA 92614

Tel No.: (949) 861-3321

Fax No.: (949) 861-3324

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. þ

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act of 1933, please check the following box and list the Securities Act registration Statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | Accelerated filer | o |

| Non-accelerated filer | o | Smaller reporting company | x |

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered | Amount to be Registered (1) | Proposed Maximum Offering Price Per Share (2) | Proposed Maximum Aggregate Offering Price (2) | Amount of Registration Fee | ||||||||||||

| Common Stock, par value $0.0001 | 6,000,000 | $ | 5.50 | $ | 33,000,000 | $ | 4501.20 | |||||||||

| (1) | This Registration Statement covers the Offering of common stock of the Company according to an Investment Agreement and for the resale by the selling stockholder named in this Prospectus. The Company is making a good faith estimate on the number of shares that it may issue under the Investment Agreement. |

| (2) | The proposed maximum offering price per share and the proposed maximum aggregate offering price have been estimated solely for the purpose of calculating the amount of the registration fee in accordance with Rule 457(c) under the Securities Act of 1933 on the basis of the average of the high and low prices of the Common Stock on the OTC Markets on July 9, 2013, a date within 5 trading days prior to the date of the filing of this registration statement. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with section 8(a) of the securities act of 1933 or until the registration statement shall become effective on such date as the commission, acting pursuant to said section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

| PREPRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION | DATED July 12, 2013 |

6,000,000 Common Shares

VACCINOGEN, INC.

This prospectus relates to the resale of up to 6,000,000 shares of the common stock of Vaccinogen, Inc., a Maryland corporation, by Kodiak Capital Group, LLC, a Delaware limited liability company (“Kodiak ” or “Selling Shareholder”), a selling shareholder pursuant to a Put Notice(s) under an Investment Agreement, as amended (the “Investment Agreement”) that we have entered into with Kodiak. The Investment Agreement permits us to sell shares of our common stock to Kodiak enabling us to put up to $26 million of common stock to Kodiak. The registration statement covers the offer and possible sale of approximately $33 million in common stock based on our July 9, 2013 closing market price of $5.50 per share before the discount offered to Kodiak. We will not receive any proceeds from the sale of these shares of common stock offered by Kodiak. However, we will receive proceeds from the sale of securities pursuant to each Put Notice we send to Kodiak. We will bear all costs associated with this registration.

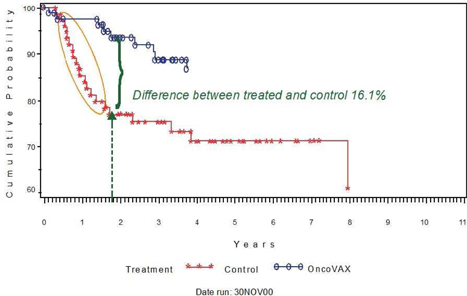

The total amount of shares of common stock which may be sold pursuant to this Prospectus would constitute 16.1% of our issued and outstanding common stock as of July 9, 2013, if all of the shares had been sold by that date. As of July 9, 2013, the closing market price of the Company’s common stock was $5.50. Based on that price, and disregarding limitations on the number of shares Kodiak may hold at any given time and the maximum advance provisions of the Investment Agreement, the maximum amount of shares of common stock which may be sold would be 5,909,091, representing 15.9% of the outstanding common stock as of July 9, 2013 if all shares were sold by that date.

Kodiak is an “underwriter” within the meaning of the Securities Act of 1933, as amended (the “Securities Act”) in connection with the resale of our common stock under the Investment Agreement. Kodiak will pay us 80% of the lowest daily VWAP of the common stock during the five consecutive trading days immediately following the date of our notice to Kodiak of our election to put shares pursuant to the Investment Agreement. There are no underwriting agreements in place.

Our shares of common stock are currently traded on the OTC Markets Group (OTC Pink Tier) under the symbol "VGEN." We have filed a general registration statement on Form 10 and we intend to immediately upgrade our tier on the OTC Link to OTC.QB upon effectiveness of such registration statement.

Our Independent Registered Public Accounting Firm has raised substantial doubts about our ability to continue as a going concern.

Investing in our common stock involves a high degree of risk. Before buying any shares, you should carefully read the discussion of material risks of investing in our common stock in “Risk Factors” beginning on page 4 of this prospectus.

Neither the U.S. Securities and Exchange Commission nor any state securities commission has approved or disapproved of anyone’s investment in these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The Date of This Prospectus Is: _____________, 2013

TABLE OF CONTENTS

| PAGE | |

| Forward-looking Statements | 1 |

| Prospectus Summary | 2 |

| Risk Factors | 4 |

| Use of Proceeds | 17 |

| Selling Shareholders | 17 |

| Plan of Distribution | 18 |

| Determination of Offering Price | 19 |

| Dilution | 19 |

| Penny Stock Considerations | 19 |

| Description of Business | 21 |

| Description of Property | 47 |

| Legal Proceedings | 47 |

| Security Ownership of Certain Beneficial Owners and Management | 48 |

| Directors, and Executive Officers | 49 |

| Executive Compensation | 53 |

| Certain Relationships and Related Transactions | 55 |

| Market For Common Equity and Related Stockholder Matters | 56 |

| Description of Securities | 57 |

| Legal Matters | 60 |

| Experts | 60 |

| Available Information | 61 |

| Index to Financial Statements | 62 |

| Management’s Discussion and Analysis of Financial Condition and Results of Operations | 63 |

| Selected Financial Data | 74 |

| Supplementary Financial Information | 74 |

| Changes in and Disagreements with Accounts on Accounting and Financial Disclosure | 74 |

| Quantitative and Qualitative Disclosures about Market Risk | 74 |

FORWARD-LOOKING STATEMENTS

Some of the statements contained in this Offering Circular are forward-looking statements within the meaning of the Securities Act of 1933 (the “Securities Act”) and the Securities Exchange Act of 1934 (the “Exchange Act”) and are subject to the safe harbor created by the Private Securities Litigation Reform Act of 1995. We have based these forward-looking statements largely on our expectations and projections about future events and financial trends affecting the financial condition and/or operating results of our business. Forward-looking statements involve risks and uncertainties; particularly those risks and uncertainties inherent in the process of discovering, developing and commercializing drugs that are safe and effective for use as human therapeutics. There are important factors that could cause actual results to be substantially different from the results expressed or implied by these forward-looking statements, including, among other things:

| · | whether we have adequate financial resources and access to capital to fund commercialization of OncoVAX®, the Human Monoclonal Antibodies (HuMabs) Program and that of other potential product candidates we may develop; |

| · | our ability to successfully manufacture OncoVAX® and other product candidates in necessary quantities with required quality; |

| · | our ability to successfully obtain regulatory approvals and commercialize our products that are under development and develop the infrastructure necessary to support commercialization if regulatory approvals are received; |

| · | our ability to complete and achieve positive results in ongoing and new clinical trials; |

| · | our dependence on single-source vendors for some of the components used in our product candidates; |

| · | the extent to which the costs of any products that we are able to commercialize will be reimbursable by third-party payers; |

| · | the extent to which any products that we are able to commercialize will be accepted by the market; |

| · | our dependence on our intellectual property and ability to protect our proprietary rights and operate our business without conflicting with the rights of others; |

| · | the effect that any intellectual property litigation, or product liability claims may have on our business and operating and financial performance; |

| · | our expectations and estimates concerning our future operating and financial performance; |

| · | the impact of competition and regulatory requirements and technological change on our business; |

| · | our ability to recruit and retain key personnel; |

| · | our ability to enter into future collaboration agreements; |

| · | anticipated trends in our business and the biotechnology industry generally; and |

| · | other factors set forth under the heading “Risk Factors” herein. |

In addition, in this Offering Circular, the words “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “plan,” “expect,” “potential,” or “opportunity,” the negative of these words or similar expressions, as they relate to us, our business, future financial or operating performance or our management, are intended to identify forward-looking statements. We do not intend to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Past financial or operating performance is not necessarily a reliable indicator of future performance and you should not use our historical performance to anticipate results or future period trends.

The terms "Vaccinogen," "our" and "we," and the “Company” as used in this prospectus, refer to Vaccinogen, Inc.

| 1 |

You should rely only on the information contained in this prospectus. We have not authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate as of the date on the front cover of this prospectus only. Our business, financial condition, results of operations and prospects may have changed since that date.

We intend to furnish our shareholders with annual reports containing consolidated financial statements audited by an independent accounting firm.

PROSPECTUS SUMMARY

This summary highlights selected information contained elsewhere in this prospectus. This summary does not contain all the information that you should consider before investing in the common stock. You should carefully read the entire prospectus, including “Risk Factors”, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the Consolidated Financial Statements, before making an investment decision.

Vaccinogen is a biotechnology company with more than three decades of research into combating cancer by using the body’s own immune system. It is the developer of OncoVAX®, the only patient specific immunotherapy for Stage II colon cancer and has the following mission:

| 1. | Complete the pivotal Phase III clinical trial of this autologous vaccine, OncoVAX®, which is a new paradigm to prevent the recurrence of stage II colon cancer. The planned trial will closely replicate a successful prior Phase IIIa study showing 50% improvement in recurrence free survival and overall survival in the Stage II target patient population. |

| 2. | Develop near term revenues by establishing licensing arrangements for distribution of OncoVAX® in certain territories as well as for additional carcinoma indications. |

| 3. | Develop diagnostic and therapeutic drug products as well as near-term revenues by exploiting its distinctive Human Monoclonal Antibodies (“HuMabs”) technology. |

Our executive office is located at 5300 Westview Drive, Suite 406, Frederick, MD 21703. Our telephone number is 301-668-8400. Our Internet address is www.vaccinogeninc.com.

Kodiak Investment Agreement

This prospectus relates to the resale of up to 6,000,000 shares of our common stock by Kodiak. Kodiak will obtain our common stock pursuant to the Investment Agreement entered into by Kodiak and us, dated July 18, 2012, as amended on July 8, 2013.

Although the Company is not mandated to sell shares under the Investment Agreement, the Investment Agreement gives the Company the option to sell to Kodiak, up to $26,000,000 worth of our common stock (“Shares”), par value $0.0001 per share over an eighteen (18) month period. At the date of filing, we may not obtain the full $26,000,000 in funding if the price of our common stock decreases (and remains below) 2% of the current market price. The $26,000,000 was stated as the total amount of available funding in the Agreement because this was the maximum amount that Kodiak agreed to offer us in funding. There is no assurance that the market price of our common stock will remain at its current price or increase substantially in the future. The number of common shares that remains issuable may not be sufficient, dependent upon the share price, to allow us to access the full amount contemplated under the Agreement. Therefore, we may not have access to the remaining commitment under the Investment Agreement unless the market price of our common stock remains at its current price or increases from it current level. Based on our stock price as of July 9, 2013, the registration statement covers the offer and possible sale of only approximately $26.4 million worth of our shares at current discounted market price of $4.40 or approximately 80% of $5.50 (our market price at July 9, 2013)

The purchase price of the common stock shall be set at eighty percent (80%) of the lowest daily VWAP of the common stock during the pricing period. The pricing period shall be the five (5) consecutive trading days immediately after the Put Notice Date.

In addition, there is an ownership limit for Kodiak of 9.99%.

| 2 |

On any Closing Date, we shall deliver to Kodiak the number of shares of the Common Stock registered in the name of Kodiak as specified in the Put Notice. In addition, we must deliver the other required documents, instruments and writings required. Kodiak is not required to purchase the shares unless:

| · | Our Registration Statement with respect to the resale of the shares of Common Stock delivered in connection with the applicable put shall have been declared effective. |

| · | We shall have obtained all material permits and qualifications required by any applicable state for the offer and sale of the Registrable Securities. |

| · | We shall have filed with the SEC in a timely manner all reports, notices and other documents required. |

We believe that we will be able to meet all of the above obligations mandated in Investment Agreement set forth above. We are aware that if we fail to perform our obligations and we fail to deliver to Kodiak on the Put Date the shares of Common Stock corresponding to the applicable Put, Kodiak shall suffer financial hardship and therefore we acknowledge that we will be liable for any and all losses, commission, fees, interest, legal fees or any other financial hardships caused to Kodiak. Fees and penalties for such losses (liquidated damages) to Kodiak shall be paid by the Company in accordance with the following schedule:

| Payments for Each Number of Days Overdue | For each $10,000 Worth of Common Stock | |||

| 1 | $ | 100 | ||

| 2 | $ | 200 | ||

| 3 | $ | 300 | ||

| 4 | $ | 400 | ||

| 5 | $ | 500 | ||

| 6 | $ | 600 | ||

| 7 | $ | 700 | ||

| 8 | $ | 800 | ||

| 9 | $ | 900 | ||

| 10 | $ | 1000 | ||

| Over 10 | $1000 + $200 for each Business Day beyond the tenth day | |||

| 3 |

RISK FACTORS

The following is a summary of the risk factors that we believe are most relevant to our business. You should understand that it is not possible to predict or identify all such factors. Consequently, you should not consider the following to be a complete discussion of all potential risks or uncertainties. We undertake no obligation to publicly update forward-looking statements, whether as a result of new information, future events, or otherwise.

RISK FACTORS RELATED TO THE OFFERING

Existing stockholders may experience significant dilution from the sale of our common stock pursuant to the Kodiak Capital Group Investment Agreement.

The sale of our common stock to Kodiak Capital Group, LLC in accordance with the Investment Agreement may have a dilutive impact on our shareholders. As a result, our net income per share could decrease in future periods and the market price of our common stock could decline. In addition, the lower our stock price is at the time we exercise our put options, the more shares of our common stock we will have to issue to Kodiak Capital Group LLC in order to exercise a put under the Investment Agreement. If our stock price decreases, then our existing shareholders would experience greater dilution for any given dollar amount raised through the Offering.

The perceived risk of dilution may cause our stockholders to sell their shares, which may cause a decline in the price of our common stock. Moreover, the perceived risk of dilution and the resulting downward pressure on our stock price could encourage investors to engage in short sales of our common stock. By increasing the number of shares offered for sale, material amounts of short selling could further contribute to progressive price declines in our common stock.

The issuance of shares pursuant to the Kodiak Investment Agreement may have a significant dilutive effect.

Depending on the number of shares we issue pursuant to the Kodiak Investment Agreement, it could have a significant dilutive effect upon our existing shareholders. Although the number of shares that we may issue pursuant to the Investment Agreement will vary based on our stock price (the higher our stock price, the less shares we have to issue) the information set out below indicates the potential dilutive effect to our shareholders, based on different potential future stock prices, if the full amount of the Investment Agreement is realized.

Dilution based upon common stock put to Kodiak Capital Group and the stock price discounted to Kodiak Capital Group’s purchase price of 80% of the lowest daily volume weighted average price (VWAP) during the pricing period. The example below illustrates dilution based upon a $5.50 market price/$4.40 purchase price and other increased/decreased prices:

$26,000,000 Put

| Stock Price(Kodiak Purchase Price) | Shares Issued | Percentage of Outstanding Shares (1) | ||||||

| $6.875 ($5.50) +25% | 4,727,273 | 13.15 | % | |||||

| $5.50 ($4.40) | 5,909,091 | 15.91 | % | |||||

| $4.125 ($3.30) -25% | 7,878,788 | 20.15 | % | |||||

| $2.75 ($2.20) -50% | 11,918,182 | 27.45 | % | |||||

| $1.375 ($1.10) -75% | 23,636,364 | 43.08 | % | |||||

| (1) | Based on 31,227,756 shares outstanding as of June 26, 2013. |

| 4 |

Kodiak Capital Group, LLC will pay less than the then-prevailing market price of our common stock which could cause the price of our common stock to decline.

Our common stock to be issued under the Kodiak Investment Agreement will be purchased at a twenty (20%) discount or 80% of the lowest daily VWAP during the five trading days immediately following our notice to Kodiak Capital Group, LLC of our election to exercise our "put" right.

Kodiak Capital Group, LLC has a financial incentive to sell our shares immediately upon receiving the shares to realize the profit between the discounted price and the market price. If Kodiak Capital Group, LLC sells our shares, the price of our common stock may decrease. If our stock price decreases, Kodiak may have a further incentive to sell such shares. Accordingly, the discounted sales price in the Investment Agreements may cause the price of our common stock to decline.

Kodiak Capital Group, LLC has entered into similar agreements with other public companies and may not have sufficient capital to meet our put notices.

Kodiak Capital Group LLC has entered into similar investment agreements with other public companies, and some of those companies have filed registration statements with the intent of registering shares to be sold to Kodiak pursuant to investment agreements. We do not know if management at any of the companies who have or will have effective registration statements intend to raise funds now or in the future, what the size or frequency of each put request would be, if floors will be used to restrict the amount of shares sold, or if the investment agreement will ultimately be cancelled or expire before the entire amount of shares are put to Kodiak. Since we do not have any control over the requests of these other companies, if Kodiak Capital Group LLC receives significant requests, it may not have the financial ability to meet our requests. If so, the amount of available funds may be significantly less than we anticipate.

We are registering an aggregate of 6,000,000 shares of common stock to be issued under the Kodiak Investment Agreement. The sale of such shares could depress the market price of our common stock.

We are registering an aggregate of 6,000,000 shares of common stock under the registration statement of which this Prospectus forms a part for issuance pursuant to the Kodiak Investment Agreement. The sale of these shares into the public market by Kodiak could depress the market price of our common stock.

We May Not Have Access to the Full Amount under the Investment Agreement.

During the period ended July 9, 2013, the closing price of our common stock was $5.50 based on very little volume. There is no assurance that the market price of our common stock will remain at its current price or increase from its current level. The entire commitment under the Investment Agreement is for $26,000,000. Therefore, we may not have access to the remaining commitment under the Investment Agreement unless the share price of our common stock remains at or increases from its current level.

Unless an active trading market develops for our securities, investors may not be able to sell their shares.

We are a reporting company and our common shares are quoted on the OTC Link (OTC Pink Tier under the symbol “VGEN” (and we will immediately upgrade our tier to OTC.QB upon effectiveness of our recently filed Form 10 registration statement). However, there is not currently an active trading market for our common stock and an active trading market may never develop or, if it does develop, may not be maintained. Failure to develop or maintain an active trading market will have a generally negative effect on the price of our common stock, and you may be unable to sell your common stock or any attempted sale of such common stock may have the effect of lowering the market price and therefore your investment could be a partial or complete loss.

Since our common stock is thinly traded it is more susceptible to extreme rises or declines in price, and you may not be able to sell your shares at or above the price paid.

Since our common stock is thinly traded its trading price is likely to be highly volatile and could be subject to extreme fluctuations in response to various factors, many of which are beyond our control, including (but not necessarily limited to):

| 5 |

| · | the trading volume of our shares; | |

| · | the number of securities analysts, market-makers and brokers following our common stock; | |

| · | changes in, or failure to achieve, financial estimates by securities analysts; | |

| · | new products or services introduced or announced by us or our competitors; | |

| · | actual or anticipated variations in quarterly operating results; | |

| · | conditions or trends in our business industries; | |

| · | announcements by us of significant contracts, acquisitions, strategic partnerships, joint ventures or capital commitments; | |

| · | additions or departures of key personnel; | |

| · | sales of our common stock and | |

| · | general stock market price and volume fluctuations of publicly-traded, and particularly microcap, companies. |

Investors may have difficulty reselling shares of our common stock, either at or above the price they paid for our stock, or even at fair market value. The stock markets often experience significant price and volume changes that are not related to the operating performance of individual companies, and because our common stock is thinly traded it is particularly susceptible to such changes. These broad market changes may cause the market price of our common stock to decline regardless of how well we perform as a company. In addition, there is a history of securities class action litigation following periods of volatility in the market price of a company’s securities. Although there is no such litigation currently pending or threatened against the Company, such a suit against us could result in the incursion of substantial legal fees, potential liabilities and the diversion of management’s attention and resources from our business. Moreover, and as noted below, our shares are currently traded on the OTC Bulletin Board and, further, are subject to the penny stock regulations. Price fluctuations in such shares are particularly volatile and subject to manipulation by market-makers, short-sellers and option traders.

RISKS RELATED TO OUR BUSINESS

Our success is dependent upon OncoVAX® achieving regulatory approval and acceptance in the marketplace, the failure of either will have a negative effect on our business, financial condition and results of operations.

Our future growth and profitability will depend on its ability to introduce and market OncoVAX®. There can be no assurance that we will be able to obtain necessary regulatory approvals for OncoVAX® in a timely manner, if at all. Our failure to introduce and market OncoVAX® in a timely manner would have a material adverse effect on our business, financial condition and results of operations.

Even if OncoVAX® is approved for marketing by the FDA and other regulatory authorities, there can be no assurance that it will be commercially successful or that we will be successful producing OncoVAX® on a commercial scale at a cost that will enable us to realize a profit. Despite the results of the clinical trials of OncoVAX®, there can be no assurance that oncologists and other physicians will refer patients for treatment with OncoVAX®. Market acceptance also could be affected by the availability of third-party reimbursement. Failure of OncoVAX® to achieve significant market acceptance could have a material adverse effect on our business, financial condition and results of operations.

We have a history of significant losses from continuing operations and expect to continue such losses for the foreseeable future.

Since our inception, our expenses have substantially exceeded our revenues, resulting in continuing losses and an accumulated deficit. Because we presently have no product revenues and we are committed to continuing our product research, development and commercialization programs, we will continue to experience significant operating losses unless and until we complete the development of OncoVAX® and other new products and these products have been clinically tested, approved by the FDA and successfully marketed.

| 6 |

We have devoted our resources to developing a new generation of products but will not be able to market these products until we have completed clinical testing and obtain all necessary governmental approvals. In addition, our products are still in development and testing and cannot be marketed until we have completed clinical testing and obtained necessary governmental approval. Accordingly, our revenue sources are, and will remain, extremely limited until our products are clinically tested, approved by the FDA and successfully marketed. We cannot guarantee that our product will be successfully tested, approved by the FDA or marketed, successfully or otherwise, at any time in the foreseeable future or at all.

We have no internal sales or marketing capability and must enter into alliances with others possessing such capabilities to commercialize our products successfully.

We intend to market our products, if and when such products are approved for commercialization by the FDA, either directly or through other strategic alliances and distribution arrangements with third parties. There can be no assurance that we will be able to enter into third-party marketing or distribution arrangements on advantageous terms or at all. To the extent that we do enter into such arrangements, we will be dependent on our marketing and distribution partners. In entering into third-party marketing or distribution arrangements, we expect to incur significant additional expense. There can be no assurance that, to the extent that we sell products directly or we enter into any commercialization arrangements with third parties, such third parties will establish adequate sales and distribution capabilities or be successful in gaining market acceptance for our products and services.

If we do not raise additional capital, we may not be able to complete the development, testing and commercialization of our treatment systems or continue as a going concern.

To complete the development and commercialization of our product, we will need to raise substantial amounts of additional capital. We do not have any committed sources of financing and we cannot offer any assurances that additional funding will be available in a timely manner, on acceptable terms or at all.

In the event we cannot raise sufficient capital, we may be required to delay, scale back or eliminate certain aspects of our operations or attempt to obtain funds through unfavorable arrangements with partners or others that may force us to relinquish rights to certain of our technologies, products or potential markets or that could impose onerous financial or other terms. Furthermore, if we cannot fund our ongoing development and other operating requirements we may no longer be able to continue as a going concern.

We rely on third parties to conduct all of our clinical trials. If these third parties do not successfully carry out their contractual duties, comply with budgets and other financial obligations or meet expected deadlines, we may not be able to obtain regulatory approval for or commercialize our product candidates in a timely or cost-effective manner.

We rely, and expect to continue to rely, on third-party Clinical Research Organizations to conduct all of our clinical trials. Because we do not conduct our own clinical trials, we must rely on the efforts of others and cannot always control or accurately predict the timing of such trials, the costs associated with such trials or the procedures that are followed for such trials. We do not anticipate significantly increasing our personnel in the foreseeable future and therefore, expect to continue to rely on third parties to conduct all of our future clinical trials. If these third parties do not successfully carry out their contractual duties or obligations or meet expected deadlines, if they do not carry out the trials in accordance with budgeted amounts, if the quality or accuracy of the clinical data they obtain is compromised due to their failure to adhere to our clinical protocols or for other reasons, or if they fail to maintain compliance with applicable government regulations and standards, our clinical trials may be extended, delayed or terminated or may become prohibitively expensive, and we may not be able to obtain regulatory approval for or successfully commercialize our product candidates.

| 7 |

We depend on key personnel for our continued operations and future success and a loss of certain key personnel could significantly hinder our ability to move forward with our business plan.

Because of the specialized nature of our business, we are highly dependent on our ability to identify, hire, train and retain highly qualified scientific and technical personnel for the research and development activities we conduct or sponsor. The loss of one or more certain key executive officers, or scientific officers, including Michael G. Hanna, Jr, Ph.D., would be significantly detrimental to us. In addition, recruiting and retaining qualified scientific personnel to perform research and development work is critical to our success. There is intense competition for qualified personnel in the areas of our present and planned activities, and there can be no assurance that we will be able to continue to attract and retain the qualified personnel necessary for the development of our business. The failure to attract and retain such personnel or to develop such expertise would adversely affect our business.

If an event of default is declared under agreements with Organon Teknika, including the security agreement, we could lose possession of the OncoVAX® intellectual property.

In connection with certain prior agreements between Intracel Holdings Corporation and Organon Teknika (now Merck), Intracel entered into a security agreement granting Organon Teknika a first priority security interest in all of intellectual property intellectual property and patents related to OncoVAX®. The security agreement states that if an event of default occurs, the secured party has the right to take possession of the OncoVAX® intellectual property to satisfy the obligations under these agreements. We assumed these obligations under our License and subsequent Asset Transfer Agreement. Certain required payments have not been made to Organon Teknika. Although no formal event of default has been issued and discussions and negotiations to resolve the matter is continuing, loss of our OncoVAX® intellectual property would adversely affect our business.

If an event of default is declared under our security agreement with The Abell Foundation, we could lose possession of the OncoVAX® intellectual property.

In connection with our promissory note issued to The Abell Foundation, we granted The Abell Foundation a security interest in our patents related to OncoVAX®. The security agreement states that if an event of default occurs, the secured party has the right to take possession of the OncoVAX® patents to satisfy the obligations under these agreements. Although we are not currently in default under these agreements, loss of our OncoVAX® patents would adversely affect our business.

Our business is subject to numerous and evolving state, federal and foreign regulations and we may not be able to secure the government approvals needed to develop and market our products.

Our research and development activities, pre-clinical tests and clinical trials, and ultimately the manufacturing, marketing and labeling of our products, all are subject to extensive regulation by the FDA and foreign regulatory agencies. Pre-clinical testing and clinical trial requirements and the regulatory approval process typically take years and require the expenditure of substantial resources. Additional government regulation may be established that could prevent or delay regulatory approval of our product candidates. Delays or rejections in obtaining regulatory approvals would adversely affect our ability to commercialize any product candidates and our ability to generate product revenues or royalties.

The FDA and foreign regulatory agencies require that the safety and efficacy of product candidates be supported through adequate and well-controlled clinical trials. If the results of pivotal clinical trials do not establish the safety and efficacy of our product candidates to the satisfaction of the FDA and other foreign regulatory agencies, we will not receive the approvals necessary to market such product candidates. Even if regulatory approval of a product candidate is granted, the approval may include significant limitations on the indicated uses for which the product may be marketed.

Many states in which we do, or in the future may do, business, or in which our products may be sold, impose licensing, labeling or certification requirements that are in addition to those imposed by the FDA. There can be no assurance that one or more states will not impose regulations or requirements that have a material adverse effect on our ability to sell our products.

In many of the foreign countries in which we may do business or in which our products may be sold, we will be subject to regulation by national governments and supranational agencies as well as by local agencies affecting, among other things, product standards, packaging requirements, labeling requirements, import restrictions, tariff regulations, duties and tax requirements. There can be no assurance that one or more countries or agencies will not impose regulations or requirements that could have a material adverse effect on our ability to sell our products.

| 8 |

Legislative and regulatory changes affecting the health care industry could adversely affect our business.

Political, economic and regulatory influences are subjecting the healthcare industry to potential fundamental changes that could substantially affect our results of operations. There have been a number of government and private sector initiatives during the last few years to limit the growth of healthcare costs, including price regulation, competitive pricing, coverage and payment policies, comparative effectiveness of therapies, technology assessments and managed-care arrangements. It is uncertain which legislative proposals, if any, will be adopted (or when) or what actions federal, state, or private payors for health care treatment and services may take in response to any health care reform proposals or legislation. We cannot predict the effect health care reforms may have on our business and we can offer no assurances that any of these reforms will not have a material adverse effect on our business. These actual and potential changes are causing the marketplace to put increased emphasis on the delivery of more cost-effective treatments. In addition, uncertainty remains regarding proposed significant reforms to the U.S. healthcare system.

The success of our products may be harmed if the government, private health insurers and other third-party payors do not provide sufficient coverage or reimbursement.

Our ability to commercialize our products successfully will depend in part on the extent to which reimbursement for the costs of such products and related treatments will be available from government health administration authorities, private health insurers and other third-party payors. The reimbursement status of newly approved medical products is subject to significant uncertainty. We cannot guarantee that adequate third-party insurance coverage will be available for us to establish and maintain price levels sufficient for us to realize an appropriate return on our investment in developing new therapies. Government, private health insurers and other third-party payors are increasingly attempting to contain health care costs by limiting both coverage and the level of reimbursement for new therapeutic products approved for marketing by the FDA. Accordingly, even if coverage and reimbursement are provided by government, private health insurers and third-party payors for uses of our products, market acceptance of these products would be adversely affected if the reimbursement available proves to be unprofitable for health care providers.

We face intense competition and the failure to compete effectively could adversely affect our ability to develop and market our products.

There are many companies and other institutions engaged in research and development of various technologies for cancer treatment products. We believe that the level of interest by others in investigating the potential of possible competitive treatments and alternative technologies will continue and may increase. Potential competitors engaged in all areas of cancer treatment research in the United States and other countries include, among others, major pharmaceutical companies, specialized technology companies, and universities and other research institutions. Most of our current and potential competitors have substantially greater financial, technical, human and other resources, and may also have far greater experience than do we, both in pre-clinical testing and human clinical trials of new products and in obtaining FDA and other regulatory approvals. One or more of these companies or institutions could succeed in developing products or other technologies that are more effective than the products and technologies that we have been or are developing, or which would render our technology and products obsolete and non-competitive. Furthermore, if we are permitted to commence commercial sales of any of our products, we will also be competing, with respect to manufacturing efficiency and marketing, with companies having substantially greater resources and experience in these areas.

OncoVAX® reg; is based on novel technologies, which may raise new regulatory issues that could delay or make FDA approval more difficult.

The process of obtaining required FDA and other regulatory approvals, including foreign approvals, is expensive, often takes many years and can vary substantially based upon the type, complexity and novelty of the products involved. OncoVAX® and our immunotherapies are novel; therefore, regulatory agencies may lack experience with them, which may lengthen the regulatory review process, increase our development costs and delay or prevent commercialization of OncoVAX® and our other active immunotherapy products under development.

| 9 |

Our products may not be accepted in the marketplace; therefore we may not be able to generate significant revenue, if any.

Even if OncoVAX® or any of our other potential products is approved and sold, physicians and the medical community may not ultimately use them or may use them only in applications more restricted than we expect. Our products, if successfully developed, will compete with a number of traditional products and immunotherapies manufactured and marketed by major pharmaceutical and other biotechnology companies. Our products will also compete with new products currently under development by such companies and others. Physicians will only prescribe a product if they determine, based on experience, clinical data, side effect profiles and other factors, that it is beneficial and preferable to other products currently in use. Many other factors influence the adoption of new products, including marketing and distribution restrictions, course of treatment, adverse publicity, product pricing, the views of thought leaders in the medical community, and reimbursement by government and private third party payers.

Technologies for the treatment of cancer are subject to rapid change, and the development of treatment strategies that are more effective than our technologies could render our technologies obsolete.

Various methods for treating cancer currently are, and in the future are expected to be, the subject of extensive research and development. Many possible treatments that are being researched, if successfully developed, may not require, or may supplant, the use of our technologies. The successful development and acceptance of any one or more of these alternative forms of treatment could render our technology obsolete as a cancer treatment method.

We may not be able to hire or retain key officers or employees that we need to implement our business strategy and develop our products and business.

Our success depends significantly on the continued contributions of our executive officers, scientific and technical personnel and consultants, and on our ability to attract additional personnel as we seek to implement our business strategy and develop our products and businesses. During our operating history, we have assigned many essential responsibilities to a relatively small number of individuals. However, as our business and the demands on our key employees expand, we have been, and will continue to be, required to recruit additional qualified employees. The competition for such qualified personnel is intense, and the loss of services of certain key personnel or our inability to attract additional personnel to fill critical positions could adversely affect our business. Further, we do not carry "key man" insurance on any of our personnel. Therefore, loss of the services of key personnel would not be ameliorated by the receipt of the proceeds from such insurance.

Products we may potentially commercialize and market may be subject to promotional limitations.

The FDA has the authority to impose significant restrictions on an approved product through the product label and allowed advertising, promotional and distribution activities. The FDA also may require us to undertake post-marketing clinical trials. If the results of such post-marketing studies are not satisfactory, the FDA may withdraw marketing authorization or may condition continued marketing on commitments from us that may be expensive and/or time consuming to fulfill. Even if we receive FDA and other regulatory approvals, if we or others identify adverse side effects after any of our products are on the market, or if manufacturing problems occur, regulatory approval may be suspended or withdrawn and reformulation of our products, additional clinical trials, changes in labeling of our products and additional marketing applications may be required, any of which could harm our business and cause our stock price to decline.

RISKS RELATING TO MANUFACTURING ACTIVITIES

We and our contract manufacturers are subject to significant regulation with respect to manufacturing of our products.

All of those involved in the preparation of a therapeutic drug for clinical trials or commercial sale, including our existing (and any future) supply contract manufacturers and clinical trial investigators, are subject to extensive regulation. Components of a finished therapeutic product approved for commercial sale or used in late-stage clinical trials must be manufactured in accordance with the FDA’s current Good Manufacturing Practices, or equivalent cGMP regulations developed by authorities in other countries. These regulations govern manufacturing processes and procedures and the implementation and operation of quality systems to control and assure the quality of investigational products and products approved for sale. Our facilities and quality systems and the facilities and quality systems of some or all of our third-party contractors must be inspected and audited routinely for compliance with applicable United States and other country regulations. Our current Emmen facility is operating under cGMP protocols with an expected cGMP recertification inspection in 3rd quarter 2013. We expect to receive recertificated cGMP status in 4th quarter 2013. If any such inspection or audit identifies a failure to comply with applicable regulations or if a violation of our product specifications or applicable regulation occurs independent of such an inspection or audit, we, the FDA, or governmental authorities in other countries may require remedial measures that may be costly and/or time consuming for us or a third-party to implement and that may include the temporary or permanent suspension or change of a clinical trial or commercial sales, recalls, market withdrawals, seizures or the temporary or permanent closure of a facility. Any such remedial measures imposed upon us or third parties with whom we contract could materially harm our business. In addition, we will be required to have a cGMP facility in the United States prior to receipt of FDA approval for our OncoVAX® and other products. Failure to procure or construct a U.S. cGMP facility will delay our ability to secure FDA approval and would have a material adverse effect on our operations.

| 10 |

RISKS FROM COMPETITIVE FACTORS

Our competitors may develop and market products that are less expensive, more effective, safer or reach the market sooner, which may diminish or eliminate the commercial success of any products we may commercialize.

Competition in the cancer therapeutics field is intense and is accentuated by the rapid pace of advancements in product development. In addition, we compete with other clinical-stage companies and institutions for clinical trial participants, which could reduce our ability to recruit participants for our clinical trials. Delay in recruiting clinical trial participants could adversely affect our ability to bring a product to market prior to our competitors. Further, research and discoveries by others may result in breakthroughs that render potential products obsolete before they generate revenue.

Some of our competitors in the cancer therapeutics field have substantially greater research and development capabilities and manufacturing, marketing, financial and managerial resources than we do. Acquisitions of competing companies by large pharmaceutical and biotechnology companies could enhance our competitors’ resources. In addition, our competitors may obtain patent protection or FDA approval and commercialize products more rapidly than we do, which may impact future sales of our products. We expect that competition among products approved for sale will be based, among other things, on product efficacy, price, safety, reliability, availability, patent protection, and sales, marketing and distribution capabilities. Our profitability and financial position will suffer if our products receive regulatory approval, but cannot compete effectively in the marketplace.

RISKS RELATING TO OUR CLINICAL TRIAL AND PRODUCT DEVELOPMENT INITIATIVES

Clinical trials for product candidates must satisfy stringent regulatory requirements or we may be unable to utilize the results.

The clinical trials for OncoVAX® and of any product candidates that we develop must comply with regulations by numerous federal, state and local government authorities in the United States, principally the FDA, and by similar governmental authorities in other countries. Clinical trials are subject to continuing oversight by governmental regulatory authorities and institutional review boards and must meet the requirements of these authorities in the United States and other countries, including those for informed consent and good clinical practices. We may not be able to comply with these requirements, which could disqualify completed or ongoing clinical trials. We may experience numerous unforeseen events during, or as a result of, the testing process that could delay or prevent commercialization of our product candidates, including the following:

| • | safety and efficacy results from human clinical trials may show the product candidate to be less effective or safe than desired or earlier results may not be replicated in later clinical trials; | ||

| • | the results of pre-clinical studies may be inconclusive or they may not be indicative of results that will be obtained in human clinical trials; | ||

| • | after reviewing relevant information, including pre-clinical testing or human clinical trial results, we may abandon or substantially restructure programs that we might previously have believed to be promising; | ||

| • | we, the FDA, an IRB, an EC, or similar regulatory authorities in other countries may suspend or terminate clinical trials if the participating patients are being exposed to unacceptable health risks or for other reasons; and | ||

| • | the effects of our product candidates may not be the desired effects or may include undesirable side effects or other characteristics that interrupt, delay or cause us or the FDA, or equivalent governmental authorities in other countries, to halt clinical trials or cause the FDA or non-United States regulatory authorities to deny approval of the product candidate for any or all target indications. |

| 11 |

Each phase of clinical testing is highly regulated, and during each phase there is risk that we will encounter serious obstacles or will not achieve our goals, and accordingly we may abandon a product in which we have invested substantial amounts of time and money. In addition, we must provide the FDA and foreign regulatory authorities with pre-clinical and clinical data that demonstrate that our product candidates are safe and effective for each target indication before they can be approved for commercial distribution. We cannot state with certainty when or whether any of our products now under development will be approved or launched; or whether any products, once approved and launched, will be commercially successful.

The FDA, other non-United States regulatory authorities, or an Advisory Committee may determine our clinical trials data regarding safety or efficacy are insufficient for regulatory approval.

Although we obtain guidance from regulatory authorities on certain aspects of our clinical development activities, these discussions are not binding obligations on regulatory authorities. Regulatory authorities may revise or retract previous guidance or may disqualify a clinical trial in whole or in part from consideration in support of approval of a potential product for commercial sale or otherwise deny approval of that product. Even if we obtain successful clinical safety and efficacy data, we may be required to conduct additional, expensive trials to obtain regulatory approval. FDA, or equivalent other country authorities, may elect to obtain advice from outside experts regarding scientific issues and/or marketing applications under FDA or other country authority review through the FDA’s Advisory Committee process or other country procedures. Views of the Advisory Committee or other experts may differ from those of the FDA, or equivalent other country authority, and may impact our ability to commercialize a product candidate.

If we encounter difficulties enrolling patients in our clinical trials, our trials could be delayed or otherwise adversely affected.

Clinical trials for our product candidates may require that we identify and enroll a large number of patients with the disease under investigation. We may not be able to enroll a sufficient number of patients, or those with required or desired characteristics to achieve diversity in a study, to complete our clinical trials in a timely manner.

Patient enrollment is affected by factors including:

| • | design of the trial protocol; | ||

| • | the size of the patient population; | ||

| • | eligibility criteria for the study in question; | ||

| • | perceived risks and benefits of the product candidate under study; | ||

| • | availability of competing therapies and clinical trials; | ||

| • | efforts to facilitate timely enrollment in clinical trials; | ||

| • | patient referral practices of physicians; | ||

| • | the ability to monitor patients adequately during and after treatment and | ||

| • | geographic proximity and availability of clinical trial sites for prospective patients. |

Additionally, even if we are able to identify an appropriate patient population for a clinical trial, there can be no assurance that the patients will continue in the clinical trial through completion.

If we have difficulty enrolling or maintaining a sufficient number of patients with sufficient diversity to conduct our clinical trials as planned, we may need to delay or terminate ongoing or planned clinical trials, either of which would have a negative effect on our business.

| 12 |

RISKS RELATED TO REGULATION OF THE PHARMACEUTICAL INDUSTRY

OncoVAX® and our other products in development cannot be sold if we do not maintain or gain required regulatory approvals.

Our business is subject to extensive regulation by numerous state and federal governmental authorities in the United States, including the FDA, and potentially by foreign regulatory authorities, with regulations differing from country to country. In the United States, the FDA regulates, among other things, the pre-clinical testing, clinical trials, manufacturing, safety, efficacy, potency, labeling, storage, record keeping, quality systems, advertising, promotion, sale and distribution of therapeutic products. Other applicable non-United States regulatory authorities have equivalent powers. Failure to comply with applicable requirements could result in, among other things, one or more of the following actions: withdrawal of product approval, notices of violation, untitled letters, warning letters, fines and other monetary penalties, unanticipated expenditures, delays in approval or refusal to approve a product candidate; product recall or seizure; interruption of manufacturing or clinical trials; operating restrictions; injunctions; and criminal prosecution. We are required in the United States and in foreign countries to obtain approval from regulatory authorities before we can manufacture, market and sell our products.

Obtaining regulatory approval for marketing of a product candidate in one country does not assure we will be able to obtain regulatory approval in other countries. However, a failure or delay in obtaining regulatory approval in one country may have a negative effect on the regulatory process in other countries. Once approved, the FDA and other United States and non-United States regulatory authorities have substantial authority to limit the uses or indications for which a product may be marketed, restrict distribution of the product, require additional testing, change product labeling or mandate withdrawal of our products. The marketing of our approved products will be subject to extensive regulatory requirements administered by the FDA and other regulatory bodies, including: the manufacturing, testing, distribution, labeling, packaging, storage, reporting and record-keeping related to the product, advertising, promotion, and adverse event reporting requirements. In addition, incidents of adverse drug reactions, unintended side effects or misuse relating to our products could result in required post-marketing studies, additional regulatory controls or restrictions, or even lead to withdrawal of a product from the market.

In general, the FDA and equivalent other country authorities require labeling, advertising and promotional materials to be truthful and not misleading, and marketed only for the approved indications and in accordance with the provisions of the approved label. If the FDA or other regulatory authorities were to challenge our promotional materials or activities, they may bring enforcement action.

Our failure to obtain approval, significant delays in the approval process, or our failure to maintain approval in any jurisdiction will prevent us from selling a product in that jurisdiction. Any product and its manufacturer will continue to be subject to strict regulations after approval, including but not limited to, manufacturing, quality control, labeling, packaging, adverse event reporting, advertising, promotion and record-keeping requirements. Any problems with an approved product, including the later exhibition of adverse effects or any violation of regulations could result in restrictions on the product, including its withdrawal from the market, which could materially harm our business. The process of obtaining approvals in foreign countries is subject to delay and failure for many of the same reasons.

Failure to comply with foreign regulatory requirements governing human clinical trials and failure to obtain marketing approval for product candidates could prevent us from selling our products in foreign markets, which may adversely affect our operating results and financial condition.

The requirements governing the conduct of clinical trials, manufacturing, testing, product approvals, pricing and reimbursement outside the United States vary greatly from country to country. In addition, the time required to obtain approvals outside the United States may differ significantly from that required to obtain FDA approval. We may not obtain foreign regulatory approvals in the timeframe we may desire, if at all. Approval by the FDA does not assure approval by regulatory authorities in other countries, and foreign regulatory authorities could require additional testing. Failure to comply with these regulatory requirements or obtain required approvals could impair our ability to develop foreign markets for our products and may have a material adverse effect on our business and future prospects.

RISKS IN PROTECTING OUR INTELLECTUAL PROPERTY

If we are unable to protect our proprietary rights or to defend against infringement claims, we may not be able to compete effectively or operate profitably.

We invent and develop technologies that are the basis for or incorporated in our potential products. We protect our technology through United States and foreign patent filings, trademarks and trade secrets. We have issued patents, and applications for United States and foreign patents in various stages of prosecution. We expect that we will continue to file and prosecute patent applications and that our success depends in part on our ability to establish and defend our proprietary rights in the technologies that are the subject of issued patents and patent applications.

| 13 |

The fact that we have filed a patent application or that a patent has issued, however, does not ensure that we will have meaningful protection from competition with regard to the underlying technology or product. Patents, if issued, may be challenged, invalidated, declared unenforceable or circumvented or may not cover all applications we may desire. Our pending patent applications as well as those we may file in the future may not result in issued patents. Patents may not provide us with adequate proprietary protection or advantages against competitors with, or who could develop, similar or competing technologies or who could design around our patents. Patent law relating to the scope of claims in the pharmaceutical field in which we operate is continually evolving and can be the subject of some uncertainty. The laws providing patent protection may change in a way that would limit protection.

We also rely on trade secrets and know-how that we seek to protect, in part, through confidentiality agreements. Our policy is to require our officers, employees, consultants, contractors, manufacturers, outside scientific collaborators and sponsored researchers and other advisors to execute confidentiality agreements. These agreements provide that all confidential information developed or made known to the individual during the course of the individual’s relationship with us be kept confidential and not disclosed to third parties except in specific limited circumstances. We also require signed confidentiality agreements from companies that receive our confidential data. For employees, consultants and contractors, we require confidentiality agreements providing that all inventions conceived while rendering services to us shall be assigned to us as our exclusive property. It is possible, however, that these parties may breach those agreements, and we may not have adequate remedies for any breach. It is also possible that our trade secrets or know-how will otherwise become known to or be independently developed by competitors.

We are also subject to the risk of claims, whether meritorious or not, that our products or immunotherapy candidates infringe or misappropriate third-party intellectual property rights. Defending against such claims can be quite expensive even if the claims lack merit. And if we are found to have infringed or misappropriated a third-party’s intellectual property, we could be required to seek a license or discontinue our products or cease using certain technologies or delay commercialization of the affected product or products, and we could be required to pay substantial damages, which could materially harm our business.

We may be subject to litigation with respect to the ownership and use of intellectual property that will be costly to defend or pursue and uncertain in its outcome.

Our business may bring us into conflict with our licensees, licensors or others with whom we have contractual or other business relationships, or with our competitors or others whose interests differ from ours. If we are unable to resolve those conflicts on terms that are satisfactory to all parties, we may become involved in litigation brought by or against us. That litigation is likely to be expensive and may require a significant amount of management’s time and attention, at the expense of other aspects of our business.

Litigation relating to the ownership and use of intellectual property is expensive, and our position as a relatively small company in an industry dominated by very large companies may cause us to be at a disadvantage in defending our intellectual property rights and in defending against claims that our immunotherapy candidates infringe or misappropriate third-party intellectual property rights. Even if we are able to defend our position, the cost of doing so may adversely affect our profitability. We may in the future be subject to patent litigation and may not be able to protect our intellectual property at a reasonable cost if such litigation is initiated. The outcome of litigation is always uncertain, and in some cases could include judgments against us that require us to pay damages, enjoin us from certain activities or otherwise affect our legal or contractual rights, which could have a significant adverse effect on our business.

Our Success Will Depend In Part On Our Ability To Grow And Diversify, Which In Turn Will Require That We Manage And Control Our Growth Effectively.

Our business strategy contemplates growth and diversification. Our ability to manage growth effectively will require that we continue to expend funds to improve our operational, financial and management controls, reporting systems and procedures. In addition, we must effectively expand, train and manage our employees. We will be unable to manage our businesses effectively if we are unable to alleviate the strain on resources caused by growth in a timely and successful manner. There can be no assurance that we will be able to manage our growth and a failure to do so could have a material adverse effect on our business.

| 14 |

A Significant Delay In Procuring Recertification of the cGMP Status Of Our Emmen-Based Manufacturing Facility Could Cause a Delay in the Commencement of Our Clinical Trials, Which Delay Could Have A Material Adverse Effect On Our Business.

Our Emmen-based manufacturing facility previously enjoyed a cGMP rating, which permits its use in the manufacturing the vaccines in the upcoming phase III trial. Certain on-going maintenance and re-qualification of the facility and its equipment are essential to maintain its cGMP rating. We expect to have a recertification inspection in 3rd quarter 2013 and expect to receive recertified cGMP status in the 4th quarter of 2013. Any delay in receiving recertified cGMP status will inhibit our ability to commence our Phase IIIb clinical trials which could ultimately have an adverse effect on our business.

RISKS RELATED TO OUR COMMON STOCK

Transfers of our securities may be restricted by virtue of state securities “blue sky” laws which prohibit trading absent compliance with individual state laws. These restrictions may make it difficult or impossible to sell shares in those states.

Transfers of our securities may be restricted under the securities regulations laws promulgated by various states and foreign jurisdictions, commonly referred to as “blue sky” laws. Absent compliance with such individual state laws, our common stock may not be traded in such jurisdictions. Because the securities registered hereunder have not been registered for resale under the blue sky laws of any state, the holders of such shares and persons who desire to purchase them should be aware that there may be significant state blue sky law restrictions upon the ability of investors to sell the securities and of purchasers to purchase the securities. These restrictions may prohibit the trading of our securities. Investors should consider the secondary market for our securities to be a limited one.

We have no immediate plans to pay dividends.

We have not paid any cash dividends to date and do not expect to pay dividends for the foreseeable future. We intend to retain earnings, if any, as necessary to finance the operation and expansion of our business.

Our officers, directors and principal stockholders collectively own a substantial portion of our outstanding common stock, and as long as they do, they may be able to control the outcome of stockholder voting.

Our officers and directors are collectively the beneficial owners of approximately 43% of the outstanding shares of our common stock as of the date of this Registration Statement. In addition, our principal stockholder is the beneficial owner of approximately 43% of the outstanding shares of our common stock as of the date of this Offering Circular. Accordingly, these stockholders, individually and as a group, may be able to control us and direct our affairs and business, including any determination with respect to a change in control, future issuances of common stock or other securities, declaration of dividends on the common stock and the election of directors.

We have the ability to issue additional shares of our common stock and shares of preferred stock without asking for stockholder approval, which could cause your investment to be diluted.

Our Articles of Incorporation authorizes the Board of Directors to issue up to 200,000,000 shares of common stock and up to 50,000,000 shares of preferred stock. The power of the Board of Directors to issue shares of common stock, preferred stock or warrants or options to purchase shares of common stock or preferred stock is generally not subject to stockholder approval. Accordingly, any additional issuance of our common stock, or preferred stock that may be convertible into common stock, may have the effect of diluting your investment.

| 15 |

By issuing preferred stock, we may be able to delay, defer, or prevent a change of control.

Our Articles of Incorporation permits us to issue, without approval from our stockholders, a total of 50,000,000 shares of preferred stock. Our Board of Directors can determine the rights, preferences, privileges and restrictions granted to, or imposed upon, the shares of preferred stock and to fix the number of shares constituting any series and the designation of such series. It is possible that our Board of Directors, in determining the rights, preferences and privileges to be granted when the preferred stock is issued, may include provisions that have the effect of delaying, deferring or preventing a change in control, discouraging bids for our common stock at a premium over the market price, or that adversely affect the market price of and the voting and other rights of the holders of our common stock.

Once publicly trading, the application of the “penny stock” rules could adversely affect the market price of our common shares and increase your transaction costs to sell those shares.

The Securities and Exchange Commission has adopted Rule 15g-9 which establishes the definition of a “penny stock,” for the purposes relevant to us, as any equity security that has a market price of less than $5.00 per share or with an exercise price of less than $5.00 per share, subject to certain exceptions. For any transaction involving a penny stock, unless exempt, the rules require:

| • | that a broker or dealer approve a person's account for transactions in penny stocks and |

| • | the broker or dealer receive from the investor a written agreement to the transaction, setting forth the identity and quantity of the penny stock to be purchased. |

In order to approve a person's account for transactions in penny stocks, the broker or dealer must:

| • | obtain financial information and investment experience objectives of the person and |

| • | make a reasonable determination that the transactions in penny stocks are suitable for that person and the person has sufficient knowledge and experience in financial matters to be capable of evaluating the risks of transactions in penny stocks. |

The broker or dealer must also deliver, prior to any transaction in a penny stock, a disclosure schedule prescribed by the Commission relating to the penny stock market, which, in highlight form:

| • | sets forth the basis on which the broker or dealer made the suitability determination and |

| • | that the broker or dealer received a signed, written agreement from the investor prior to the transaction. |

Generally, brokers may be less willing to execute transactions in securities subject to the “penny stock” rules. This may make it more difficult for investors to dispose of our common stock and cause a decline in the market value of our stock.

Disclosure also has to be made about the risks of investing in penny stocks in both public offerings and in secondary trading and about the commissions payable to both the broker-dealer and the registered representative, current quotations for the securities and the rights and remedies available to an investor in cases of fraud in penny stock transactions. Finally, monthly statements have to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks

Should our stock become quoted on the OTC bulletin board, if we fail to remain current on our reporting requirements, we could be removed from the OTC bulletin board which would limit the ability of broker-dealers to sell our securities and the ability of stockholders to sell their securities in the secondary market.

Companies quoted on the Over-The-Counter Bulletin Board, such as we are seeking to become, must be reporting issuers under Section 12 of the Securities Exchange Act of 1934, as amended, and must be current in their reports under Section 13, in order to maintain price quotation privileges on the OTC Bulletin Board. If we fail to remain current on our reporting requirements, we could be removed from the OTC Bulletin Board. As a result, the market liquidity for our securities could be severely adversely affected by limiting the ability of broker-dealers to sell our securities and the ability of stockholders to sell their securities in the secondary market. In addition, we may be unable to get re-quoted on the OTC Bulletin Board, which may have an adverse material effect on our Company.