Attached files

| file | filename |

|---|---|

| EX-31.7 - EXHIBIT 31.7 - Umami Sustainable Seafood Inc. | v349440_ex31-7.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

(Amendment No. 3)

T ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended June 30, 2012

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to ____________

Commission File Number 000-52401

UMAMI SUSTAINABLE SEAFOOD INC.

(Exact name of Registrant as specified in its charter)

1230 Columbia St.

Suite 440

San Diego, CA 94089

(Address of principal executive offices, including zip code)

Registrant’s telephone number, including area code: (619) 544-9177

__________________

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, par value $.001 per share

(Title of Class)

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ¨ No x

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No x

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ |

| Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company x |

Indicate by check mark whether the Registrant is a shell company (as defined by Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of voting and non-voting common equity held by non-affiliates of the registrant as of December 31, 2011: $25,005,000

The number of shares of the registrant’s common stock outstanding as of October 9, 2012 was 59,515,543.

DOCUMENTS INCORPORATED BY REFERENCE

The following documents (or parts thereof) are incorporated by reference into the following parts of this Form 10-K: None

EXPLANATORY NOTE

This Amendment No. 3 to Form 10-K (this “Amendment”) amends the Annual Report on Form 10-K for the fiscal year ended June 30, 2012 originally filed on October 12, 2012 (the “Original Filing”) by Umami Sustainable Seafood Inc., a Nevada corporation (“Umami,” the “Company,” “we,” or “us”). On October 30, 2012, we filed Amendment No. 1 to the Original 10-K (the “ First Amendment”) and on November 21, 2012, we filed Amendment No. 2 to the Original 10-K (the “Second Amendment”). We are filing this Amendment in response to a comment letter received from the Securities and Exchange Commission (“SEC”) to revise the disclosures in Item 1. Business, Item 1A. Risk Factors, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations, Item 10. Directors, Executive Officers and Corporate Governance, Item 11. Executive Compensation, Item 13. Certain Relationships and Related Transactions and Director Independence, and Item 15. Exhibits, Financial Statement Schedules.

You should read this Amendment in conjunction with the Original 10-K, the First Amendment, the Second Amendment and the Company’s other filings made with the SEC subsequent to the filing of the Original 10-K. The Original 10-K has not been amended or updated to reflect events occurring after June 30, 2012, except as specifically set forth in the First Amendment, the Second Amendment and this Amendment.

PART I

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains statements that do not relate to historical or current facts, but are "forward-looking" statements within the meaning of Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These statements relate to analyses and other information based on forecasts of future results and estimates of amounts not yet determinable. These statements may also relate to future events and trends, our future prospects and proposed new products, services, developments, or business strategies, among other things. These statements can generally (although not always) be identified by their use of terms and phrases such as "anticipate," "appear," "believe," "contemplate," "continue," "could," "estimate," "expect," "indicate," "intend," "may," "plan," "predict," "project," "pursue," "seek," "should," "will," "would," or the negative thereof and other similar terms and phrases, as well as the use of the future tense.

Examples of forward-looking statements in this report include, but are not limited to, the following categories of expectations about:

| • | customer demand for Bluefin Tuna and market prices; | ||||||||||||||

| • | potential changes to Bluefin Tuna quotas, concessions and regulations; | ||||||||||||||

| • | the implementation of our business model and strategic plans for our future business and products; | ||||||||||||||

| • | our ability to successfully increase the scale of our farming operations; | ||||||||||||||

| • | our ability to develop closed-lifecycle farming; | ||||||||||||||

| • | general economic conditions, particularly in Japan; | ||||||||||||||

| • | our reliance on a few customers for substantially all of our sales; | ||||||||||||||

| • | our financial performance; | ||||||||||||||

| • | the intensity of competition and the advantages of our products as compared to those of others; | ||||||||||||||

| • | our ability to collect outstanding receivables; | ||||||||||||||

| • | the amount of liquidity available at reasonable rates or at all for ongoing capital needs; | ||||||||||||||

| • | our ability to raise additional capital if necessary to execute our business plan; | ||||||||||||||

| • | our ability to attract and retain management, and to integrate and maintain technical information and management information systems; | ||||||||||||||

| • | the outcome of legal proceedings affecting our business; and | ||||||||||||||

| • | our insurance coverage being adequate to cover the potential risks and liabilities faced by our business. | ||||||||||||||

Actual results could differ materially from those expressed or implied in our forward-looking statements. Our future financial condition and results of operations, as well as any forward-looking statements, are subject to change and to inherent known and unknown risks and uncertainties. See Part 1, Item 1A, "Risk Factors" of this report for a discussion of these and other risks and uncertainties. You should not assume at any point in the future that the forward-looking statements in this report are still valid. We do not intend, and undertake no obligation, to update our forward-looking statements to reflect future events or circumstances, except as required by law.

In this report, unless otherwise specified, all dollar amounts are expressed in United States dollars and all references to “common shares” refer to shares of our common stock. The following discussion should be read in conjunction with the audited annual financial statements and the related notes filed herein.

METRIC SYSTEM CONVERSION INFORMATION

We reference various measurements throughout this report that utilize the metric system of measurement. The applicable conversion rates from the metric system of measurement to the U.S. system are as follows:

1 kilogram = 2.2046 pounds;

1 metric ton (or tonne) = 1.1023 short tons (U.S. ton); and

1 metric ton (or tonne) = 2,204.6 pounds.

| 3 |

Item 1. BUSINESS

Corporate Background

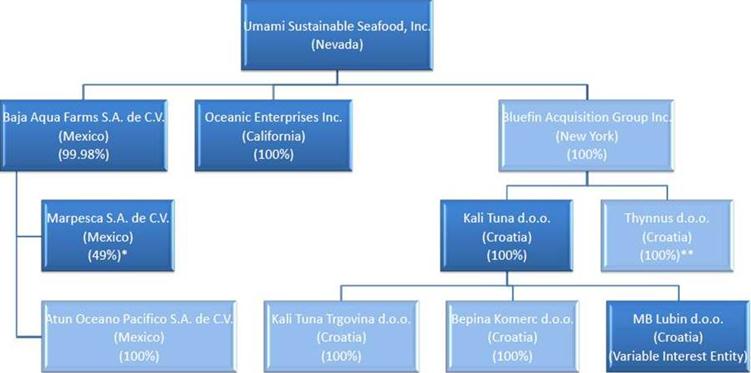

Umami Sustainable Seafood Inc. (including its subsidiaries unless the context indicates otherwise, "Umami," "the Company," "we," "us," and "our") fishes and farms for Atlantic and Pacific Bluefin Tuna. We have three direct subsidiaries, Bluefin Acquisition Group Inc. ("Bluefin"), Baja Aqua Farms, S.A. de C.V. ("Baja"), and Oceanic Enterprises, Inc. ("Oceanic"), and four indirect subsidiaries, Kali Tuna d.o.o. ("Kali Tuna"), Thynnus d.o.o. ("Thynnus"), Bepina Komerc d.o.o. ("Bepina") and Atún Oceano Pacifico S.A. de C.V. ("AOP"). In addition, based upon the criteria set forth in ASC 810, we have determined that we are the primary beneficiary in two VIEs, M.B. Lubin d.o.o. ("Lubin") in Croatia and Marpesca S.A. de C.V. ("Marpesca") in Mexico. We were the primary beneficiary in one additional VIE, Kali Tuna Trgovina d.o.o. ("KTT"), prior to May 23, 2012. See further discussion of our variable interest entities as discussed in Note 9 - Variable Interest Entities to our consolidated financial statements included elsewhere is this report.

We own and operate Kali Tuna, a limited liability company organized in 1996 under the laws of the Republic of Croatia, which is an Atlantic Bluefin Tuna farming operation located in the Adriatic Sea off the coast of Croatia. We also own and operate Baja, a corporation organized in 1999 under the laws of the Republic of Mexico, which is a Pacific Bluefin Tuna farming operation located in the Pacific Ocean off Baja California, Mexico.

Prior to June 30, 2010, we were a shell company known as Lions Gate Lighting Corp. ("Lions Gate"), which was incorporated in the State of Nevada in May 2005. On June 30, 2010, Lions Gate and Atlantis Group hf ("Atlantis"), our majority stockholder, completed a transaction in which Lions Gate purchased from Atlantis all of the issued and outstanding shares of its wholly-owned subsidiary, Bluefin Tuna Acquisition Group ("Bluefin") in consideration for the issuance to Atlantis of 30.0 million shares of Lions Gate common stock, resulting in a change of control of Lions Gate. As a result of this transaction, Kali Tuna, a wholly-owned subsidiary of Bluefin acquired in 2005, and an indirect subsidiary of Atlantis, became an indirect wholly-owned subsidiary of Lions Gate. This transaction was accounted for as a recapitalization effected by a reverse merger, with Bluefin and Kali Tuna considered the acquirer for accounting and financial reporting purposes.

On July 20, 2010, we acquired 33% of Baja and Oceanic, and on November 30, 2010, we acquired virtually all of the remaining shares of Baja and all of the shares of its related party Oceanic. We currently own 99.98% of Baja. See further discussion regarding the acquisition of Baja and Oceanic below at "- Acquisition of Baja Aqua Farms and Oceanic."

In August 2010, Lions Gate changed its name to Umami Sustainable Seafood Inc. The stock symbol on the OTC Bulletin Board was changed to UMAM on the same date.

Our corporate structure is as follows:

_________________________________

| * | Marpesca's remaining 51% is owned by Baja's General Manager, Victor Manuel Guardado France. Mr. Guardado is our nominee for Mexican regulatory purposes, does not have decision-making authority and is not an executive officer or significant employee of Umami. Decision-making authority for Marpesca lies solely with Baja’s management, including specifically Mr. Sarmiento. See "Note 9 - Variable Interest Entities" for further discussion. | |

| ** | Thynnus d.o.o. is an inactive Croatian company. | |

| 4 |

Acquisition of Baja Aqua Farms and Oceanic

On July 20, 2010, we entered into a stock purchase agreement with Corposa, S.A. de C.V. ("Corposa") and Holshyrna Ehf ("Holshyrna"), Oceanic and certain other parties, providing for the sale from Corposa and Holshyrna of 33% of the equity in Baja and Oceanic. The agreement provided for our acquisition of 33% interest in Baja and Oceanic for $8.0 million, which included $4.9 million that had been advanced to Baja previously.

As part of the stock purchase agreement, we also acquired the option, exercisable by September 15, 2010, to purchase all remaining Baja and Oceanic shares in consideration for the issuance of a) 10,000,000 restricted shares of our common stock and b) payment in cash of $10.0 million. On September 15, 2010, we exercised the option and on September 27, 2010, the parties entered into amendments to each of the agreements requiring certain capital distributions plus an additional $2.0 million related to the amendments to be made to the selling parties on or before November 30, 2010. On November 30, 2010, we consummated the acquisition of Baja and Oceanic. However, instead of making the $10.0 million cash payment described above, we paid $7.8 million in cash and issued zero interest promissory notes in the aggregate principal amount of $2.2 million on November 30, 2010. The notes, which were unsecured, were due and paid on December 10, 2010. As a result, on November 30, 2010, Baja became our 99.98% owned subsidiary and Oceanic became our 100% owned subsidiary.

Prior and subsequent to our acquisition of Baja, its administrative functions were performed by Oceanic. These functions included accounting, payroll, human resources and related matters. While Oceanic does not have an ongoing sales function, in 2008 and 2009 it sold Bluefin Tuna on Baja's behalf and was responsible for overseeing the processing and shipping of that Bluefin Tuna. In limited circumstances, Oceanic also acquires and exports certain equipment from U.S. vendors to Baja in cases where the U.S. vendors require a U.S. entity as a counterparty. It has no other functions or operations beyond providing these services to Baja and is not a significant subsidiary. Oceanic, which was formed in California in 2000 under the name Agritrade USA, Inc., was an affiliate of Baja that we acquired concurrently with the Baja acquisition. Oceanic holds no intellectual property, does not require any government approval to conduct its operations as currently conducted, has not engaged in research and development activities or incurred any costs or experienced any effects related to compliance with environmental laws. As of June 30, 2012, Oceanic had 7 employees, all of whom were full-time employees. Oceanic continues to perform some accounting, payroll and human resources functions for Baja.

Business Overview

Our core business activity is fishing, farming and selling Bluefin Tuna. We generate all of our revenue from the sale of Bluefin Tuna primarily into the Japanese sushi and sashimi market, and our sales are highly seasonal. Our fishing and farming operations increase the total weight of our Bluefin Tuna, which we refer to as biomass, by catching or, less frequently, purchasing Bluefin Tuna and then transporting them to our farms for growing over extended cycles.

We are a June 30-based fiscal year company and due to the optimal seasonality for harvesting Bluefin Tuna in winter, we typically generate little or no revenue in our first fiscal quarter (the three months ending September 30) or our fourth fiscal quarter (the three months ending June 30). In Croatia, our harvest months are typically from November through February, while in Mexico, our harvest months are typically from October through December.

We are a leading producer of farmed Bluefin Tuna. We have farming operations off the coast of Croatia in the Adriatic Sea and off the coast of Baja California, Mexico in the Pacific Ocean. Our existing farming concessions in Croatia enable us to hold 5,030 metric tons at our Croatian farm. We can add 1,972 metric tons of Bluefin Tuna to our Croatian farms each year, of which we can fish for and catch 133 metric tons based on our current allocation of the total annual ICCAT fishing quota by the Croatian Fishing Ministry for calendar 2012 (see further discussion at "- Regulation" below) and the remainder can be added through purchases of live Bluefin Tuna. Our Bluefin Tuna inventory of approximately 1,450 metric tons in Croatia as of June 30, 2012 represents just 29% of our holding allowance. We can add up to 2,720 metric tons of Bluefin Tuna to our Mexican farms each year. Our Bluefin Tuna inventory at June 30, 2012 was approximately 887 metric tons in Mexico. In Croatia and Mexico, there is no cap on the amount of biomass we have the right to export annually.

| 5 |

We are a practitioner of extended-cycle Bluefin Tuna farming, which we define as farming through one or more winters. Extended-cycle farming enables us to grow our tuna, or biomass, by as much as ten times prior to sale. In addition, our extended-cycle farming substantially increases the biomass of the Bluefin Tuna we sell from farming compared to the biomass of the Bluefin Tuna we take from the wild. By adding substantial biomass from extended-cycle farming, we can meet a given amount of market demand with a diminishing amount of wild-caught Bluefin Tuna. We also are working toward a closed lifecycle Bluefin Tuna farming process, which has the long-term potential to significantly reduce Bluefin Tuna fishing. We promote sustainability by meeting market demand through responsible farming practices that attempt to minimize reliance on wild resources. We support fishery management actions to achieve permanent sustainability of Bluefin Tuna by advocating policies to mitigate the effects of overfishing, including those directed at minimizing current overcapacity in the fishing fleets, as well as to eliminate illegal fishing.

Industry Overview

Bluefin Tuna is commonly regarded as the highest quality and most desirable species for sushi and sashimi consumption, and has become the centerpiece of the upscale sushi and sashimi plate. However, Bluefin Tuna accounted for less than three percent of global tuna production in 2008.

1 Bluefin Tuna itself is comprised of three distinct species: Atlantic Bluefin Tuna ("ABT"), which are found in the Mediterranean Sea and the western and eastern Atlantic Ocean; Pacific Bluefin Tuna ("PBT"), which are found in the northern Pacific Ocean; and Southern Bluefin Tuna ("SBT"), which are found in the southern hemisphere waters of all of the world's oceans. Atlantic Bluefin Tuna are further comprised of two varieties, western Atlantic Bluefin Tuna and eastern Atlantic (including the Mediterranean) Bluefin Tuna. Each of the three Bluefin Tuna species has its own distinct geographic distribution, migratory patterns and sustainability profile.

The amount of each species of Bluefin Tuna caught in the wild has declined significantly since the 1960s, primarily due to overfishing and the introduction of catch quotas and other regulations. Bluefin Tuna catches declined from 143,200 metric tons in 1961 to 49,096 metric tons in 2010. 2 However, consumer demand for Bluefin Tuna has substantially exceeded available wild catch supply. In addition to Japan, which remains the principal market for Bluefin Tuna, other markets have emerged and grown, such as in China, Eastern Europe and the United States. This has resulted in overfishing that has significantly reduced the Bluefin Tuna population.

The Atlantic and Southern Bluefin Tuna species are the most critically affected by historical overfishing, leading to their classification as a threatened species by several Regional Fisheries Management Organizations ("RFMOs"). As a result, the annual total allowable catch ("TAC") of ABT and SBT that may be caught per year has been significantly reduced. For example, the TAC for eastern ABT has been reduced from 29,500 metric tons in 2007 to 12,900 metric tons for 2012. 3 The PBT is not yet in a low-TAC regime and the species is not nearly as affected as ABT. However there are current attempts to introduce a low-TAC regime for PBT, such as implementation of decreasing TACs and increasingly stringent controls on illegal fishing. Regulatory actions in support of sustainability applied to the PBT fishery should help prevent a descent into critical status like that of ABT in the Mediterranean.

Current attempts to constrain Bluefin Tuna fishing are primarily through setting environmentally sound quota levels, increasing quota enforcement and enforcement against illegal fishing of Bluefin Tuna. In addition, other conservation measures, such as more stringent licensing and registration requirements, tighter documentation and traceability restrictions, and shortened allowable fishing seasons, have been implemented in various parts of the world to help conserve the wild Bluefin Tuna population. For example, the International Commission for the Conservation of Atlantic Tunas ("ICCAT") only allows Bluefin Tuna to be offloaded at designated, regulated ports and requires official monitors aboard fishing boats. As a result of the sustained periods of overfishing and the relatively recent regulatory response, the supply of Bluefin Tuna caught in the wild has been severely constrained and is expected to remain so for the foreseeable future.

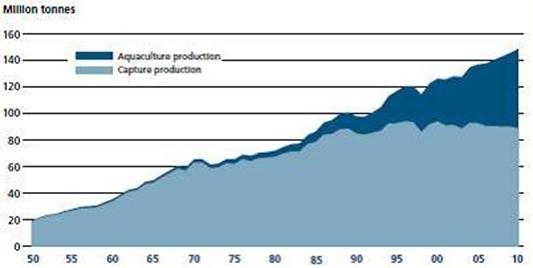

The large supply and demand imbalance for Bluefin Tuna has intensified the interest in Bluefin Tuna farming as a potential solution for the strong demand for the product and the desire to conserve the species over the long term. In general, farming seafood species, or aquaculture, has emerged as the bridge between increasing demand for seafood and the natural constraints on the amount of fish that can be caught in the wild. In the last two decades, the increase in the demand for seafood has largely been addressed through the rapid growth of aquaculture as the level of wild catch has leveled off, according to the Food and Agricultural Organization of the United Nations, or FAO.

1 Food and Agricultural Organization of the United Nations ("FAO"), Fisheries and Aquaculture Department. The data is available publicly via the FAO's Fishery Statistical Collections webpage at www.fao.org/fishery/statistics/tuna-catches/en.

2 Food and Agricultural Organization of the United Nations ("FAO"), Fisheries and Aquaculture Department. The data is available publicly via an online query on the FAO's website at www.fao.org/fishery/statistics/tuna-catches/en, "Global Tuna Nominal Catches."

3 International Seafood Sustainability Foundation, "ISSF Technical Report 2012-04, ISSF Stock Status Ratings - 2012, Status of the World Fisheries for Tuna," April 2012. The complete report is publicly available at www.iss-foundation.org/science/technical-reports.

| 6 |

Aquaculture Production

Source: FAO4

According to the FAO, total world fisheries production was estimated to be 154.0 million metric tons in 2011, of which 130.8 million metric tons was destined for human consumption. Aquaculture production was estimated to be 63.6 million metric tons, of which more than 86 percent was destined for human consumption, which means that aquaculture production represented nearly half of all fish consumed by humans in 2011. 5 This percentage is projected to increase to meet the anticipated increase in demand for seafood. In the same way that agriculture emerged in the last century to meet the demand for terrestrial animal proteins, aquaculture is poised to meet the increasing demand for sea-based proteins. In addition, sea-based aquaculture offers many benefits over agriculture, including the ability to farm without harmful fertilizers or the use of fresh water, which is critical in light of the impact many fertilizers have on the environment and the increasing strain on fresh water supplies globally.

Prior to the early 1990s, conventional Bluefin Tuna fishing methods meant it was not possible to keep bulk amounts of Bluefin Tuna alive after being caught. In the early 1990s, the emergence of purse seine fishing vessels, which surround schools of Bluefin Tuna, enabled live capture and transport back to farms for further growth. Historically, Bluefin Tuna farming occurred between the spring when the fish were caught and the winter. These short-term Bluefin Tuna farms are generally able to increase the biomass of the catch during this period up to 50 percent.

Going forward, significantly more farmed biomass is required to achieve sustainable Bluefin Tuna production in light of demand and reduced TAC. One way to accomplish this is to extend the farming cycle through one or more winters. Extended-cycle Bluefin Tuna farms have successfully created more than ten times the biomass on their farms compared to catch weights, which significantly reduces the strain on the Bluefin Tuna in the wild over the longer term. In order to farm Bluefin Tuna at commercial scale over one or more winters, extended-cycle farmers need the ability to catch or purchase live Bluefin Tuna, ample input quotas, and farming concessions in protected natural environments with key characteristics such as adequate space and depth, multi-directional currents and favorable water quality. In addition, if the industry continues moving towards fully sustainable Bluefin Tuna production as we expect, we believe successful Bluefin Tuna farmers will need to develop and utilize the ability to raise Bluefin Tuna from eggs generated from farmed fish.

Operations

Our operations consist of the fishing (or less frequently purchasing), farming (including feeding), harvesting and sale of Bluefin Tuna.

4 FAO, "The State of World Fisheries and Aquaculture - 2012," 2012. The complete report is publicly available at www.fao.org/fishery/publications/en.

5 FAO, "The State of World Fisheries and Aquaculture - 2012," 2012. The complete report is publicly available at www.fao.org/fishery/publications/en.

| 7 |

Fishing

Overview. We have developed the necessary expertise to allow us to cost-effectively catch Bluefin Tuna. Successfully catching Bluefin Tuna in a cost-effective manner requires knowledge, data and expertise at several points in the fishing process, including in locating, catching and towing the Bluefin Tuna back to our farms in a manner designed to minimize mortalities.

Locating Bluefin Tuna. The first step in the fishing process is locating Bluefin Tuna. Our extensive research and expertise allows us to identify likely places and times where Bluefin Tuna will school. In addition, at our Mexican operation, we closely monitor oceanographic and weather information to create predictive maps showing where we believe the most efficient fishing will take place. We gather and consider data from satellites and over ten years of internal records, including with respect to water temperature (both at the surface and at various depths), current flows and prevailing winds. The data is analyzed and provided to our vessel captains and our pilots (in Mexico), who collectively draw on decades of experience to determine where and when ideal fishing conditions exist.

Catching Bluefin Tuna. Once Bluefin Tuna have been located, we use our skills, expertise and specialized equipment to minimize mortality in the catching process. We catch Bluefin Tuna using purse seiners, which are the most efficient in drawing live fish from the wild fishery for our farming operations. Alternatives such as set nets, drift nets, and long-line fishing methods are not suitable for live fisheries. The seiner circles the Bluefin Tuna with a deep curtain of netting. The bottom of the net is then closed, or pursed, underneath the Bluefin Tuna by hauling a wire running from the seiner through rings along the bottom of the net. Purse seining, coupled with Bluefin Tuna schooling patterns, allow us to substantially reduce the catching of any other fish species, or by-catch. We never use fish aggregating devices ("FADs") which increase by-catch of marine life other than tuna. We do not need nets with panels to release dolphins (such as nets used for Yellowfin Tuna fishing) because dolphins do not school with Bluefin Tuna. Our specially designed nets are also easier to use than Yellowfin Tuna nets, making managing the catching process easier in order to minimize mortality. Key in minimizing mortality is how the nets are set and manipulated. Immediately upon setting the nets, we deploy highly specialized divers, who use their collective expertise to determine the optimal time and pace at which to purse the seine; if done too quickly, the Bluefin Tuna can panic and charge the sides of the net, resulting in substantial mortality.

Towing Bluefin Tuna. Once we have located and caught Bluefin Tuna, we must tow them to our farming sites while minimizing mortality. We employ divers with significant experience to transfer the tuna from our seine nets to our specialized towing pens. After successfully transferring the Bluefin Tuna to our towing cages, the tuna are then transported to our farms at extremely low rates of speed to minimize stress, ensuring they arrive healthy and with a low mortality rate. Throughout the towing process, our divers go into the towing pens to remove any deceased Bluefin Tuna and monitor the general condition of the live Bluefin Tuna, which they communicate to the captain in order to determine optimal towing speed.

Our Vessels and Fishing Periods. In Croatia, we use a combination of our fleet and contracted fishing vessels to catch Bluefin Tuna during May and June. In Mexico, we lease a fleet of purse seiners and tugboats for an 80-day period during the fishing season of May through August to catch Bluefin Tuna. These leased vessels are dry-leased, which means we provide all of the necessary equipment and personnel for Bluefin Tuna fishing. This provides us with the level of control we desire and allows us to take full advantage of our know-how, data, experience, expertise and developed skill sets. We also believe we can significantly lower our overall feed costs by purchasing sardine-fishing vessels for our Mexican operation, and we intend to purchase one or more of these vessels in fiscal 2013 to support this goal. We estimate that each of these sardine-fishing vessel acquisitions will require approximately $0.8 to $1.4 million until the purchase is consummated and the vessel reaches its ultimate destination, at which point we believe we will be able to mortgage the vessels or set up sale-leaseback arrangements and recover most of our initial cash outlay. Our current cash on hand and capital needs for the foreseeable future may not allow us to fund these acquisitions. Therefore, to fund these acquisitions, we may pursue joint ventures or debt or equity financing. Such funding may not be available on commercially reasonable terms or at all. Similarly, we may not be successful in mortgaging or entering into sale-leaseback arrangements with respect to any vessels we acquire on commercially reasonable terms or at all.

Farming

Overview. Our operations focus on extended-cycle Bluefin Tuna farming. Farming is the principal form of aquaculture and involves farming fish commercially in tanks or holding pens. Bluefin Tuna farming is conducted in the open water in circular holding pens typically measuring 30-50 meters in diameter and 20-30 meters deep. We have developed the expertise to farm our Bluefin Tuna for extended periods of time, up to 3.5 years, which achieves up to a ten-fold increase in the Bluefin Tuna biomass.

| 8 |

Transferring Bluefin Tuna to Holding Pens. Once the tow pen arrives at our farm locations (after approximately one to three weeks of towing), our biologists and farm staff study the Bluefin Tuna to determine whether they have acclimated to the towing pen and their stress level has adequately declined. We have sufficient infrastructure and additional towing pens to allow us to transfer the Bluefin Tuna to minimize mortality. First, we anchor the towing net to a farming pen and allow them to acclimate before transferring them to the holding pen. Having many farming sites allows us to choose the farming pen with optimal conditions and to avoid overcrowding the Bluefin Tuna. When our farm staff determine that the conditions are optimal for a transfer based on fish behavior, visibility and other conditions, we transfer the Bluefin Tuna into holding pens. We open the towing net and create a portal to the farm pen to accomplish the transfer. Divers then guide the Bluefin Tuna into the holding pen. Using high-speed cameras and a specialized software, we film, count and measure the Bluefin Tuna entering our pens to record total inventory and calculate biomass. We have a security team that monitors our farms 24 hours per day, seven days per week. We also have teams of marine biologists, feed providers, divers and maintenance staff that look after our Bluefin Tuna. Our staff ensures that the pens are secure and that any mortalities are removed.

Location. As with terrestrial farming, identifying and setting up favorable farming locations is one of the most important aspects to a successful open water aquaculture farming operation. We determine the optimal locations for our farming operations after a careful and thorough review of site-specific conditions by our operational teams and external environmental consultants. We currently operate our farming operations in two locations: Croatia and Mexico. Kali Tuna has been operating in the Adriatic Sea off the Croatian coast since 1996. The Adriatic Sea off the Croatian coast provides an ideal farming ground due to its infrequent storms and lack of natural predators of tuna. In 2010, we acquired a Bluefin Tuna farming operation in the Pacific Ocean off the coast of Baja California, Mexico. Both our Croatia and Mexico sites offer several advantages over other locations to farm Bluefin Tuna due to their favorable climate, water temperatures and quality, and multi-directional currents, which we believe aid in farm cleanliness and lower disease rates. In addition, our farms are located in close proximity to sources of sardines and other small fish we catch or purchase for feed, in locations with conveniently-located, well developed port infrastructure and in areas with competitively priced skilled labor. In Croatia, we own the right to hold 5,030 metric tons of biomass in our pens, and we own quotas to catch an additional 133 metric tons per year. In Mexico, we can add 2,720 metric tons of Bluefin Tuna to our farms each year.

Fish Farming. Our staff monitor the Bluefin Tuna and their reactions to the conditions on the farm. Stress can cause Bluefin Tuna mortality. We seek to minimize stress on our Bluefin Tuna throughout the farming cycle, but especially while introducing new Bluefin Tuna to our farms. Our staff continually assess potential contributors to stress and conduct regular histological testing to closely monitor the health of the tuna in our farms.

Procurement of Additional Bluefin Tuna

For a farming operation to be successful, Bluefin Tuna stock must be replenished. We obtain additional Bluefin Tuna stock for use in our farming operations through two primary methods: catching live fish and purchasing live fish from third parties. Fishing in Croatia takes place only from May 15 through June 15 and is subject to strict quotas, as set by the international regulatory body International Commission for the Conservation of Atlantic Tunas ("ICCAT"). In Mexico, the majority of our Bluefin Tuna is obtained through our own fishing efforts. The fishing season in Mexico generally takes place during the months of May through August. In Croatia, we also purchase live tuna from local and foreign-based farms and suppliers, including fish companies operating in the Mediterranean. Purchased fish are towed back to our farming sites off the Croatian coast for transfer into our farming pens. Since the acquisition of our Mexican operation, we have not purchased any live Bluefin Tuna in Mexico. Whether self-caught or purchased, we have extensive controls in place to ensure that our Bluefin Tuna is compliant with total traceability standards, meaning it was caught in compliance with all quotas and other regulations governing the fishery and fishing methods. We can trace the history of each farming pen of fish that we harvest back to the time and location where it was caught, what it has been fed, and how long it has been farmed as part of our compliance with total traceability standards required to sell Bluefin Tuna into Japan.

Feed and Inventory Management

We feed our Bluefin Tuna a diet of sardines, anchovies, mackerel, herring, squid and other small fish, the same diet the Bluefin Tuna would have in the wild. The quantity of feeding can be adjusted up or down depending on seasonal conditions and timing within the general farming cycle. Because our Bluefin Tuna are caged and spend much less energy hunting for their own food, the feed we provide them goes more towards growth than would a comparable amount of feed consumed by tuna in the wild. We amass feed with different nutritional specifications, such as higher or lower fat and protein content, and freeze feed to ensure that we maintain adequate supply. Our staff carefully monitors the feeding behavior and we are then able to increase or decrease the fat and protein content of our Bluefin Tuna's diet to achieve optimal food conversion. We use no antibiotics, additives or supplements.

| 9 |

In Croatia, we currently purchase most of our feed requirements from third-party vendors. In Mexico, we catch most of our feed requirements ourselves, and we supplement the caught feed by purchasing some additional fish from third parties. We believe we can significantly lower overall feed costs in Mexico by purchasing sardine-fishing vessels.

Harvesting

At harvest time, we set up specialized nets to partition the pens into sections. Divers guide a certain number of Bluefin Tuna into a quartered section of a pen where our dive team removes Bluefin Tuna from the holding pens one-by-one. The harvested Bluefin Tuna is either sold fresh or, more commonly, loaded onto a customer's freezer boat where it is frozen at ultra-low temperatures.

In Croatia, the optimal harvest months are from November through February. In Mexico, the optimal harvest months are from October through December. These months represent the months when water temperature is lowest, which increases the quality of tuna meat. Although we have proven the ability to farm Bluefin Tuna for several years, we have historically harvested fish after an average period of 2.5 to 3.5 years in Croatia (approximately 70-120 kilograms) and two to fourteen months in Mexico (approximately 20-35 kilograms) due to capital constraints that limited our ability to grow our tuna over the optimal growing cycle.

Strategic investments

We may seek to acquire stakes in tuna farming and fisheries with farming and/or fishing licenses in selected areas in countries with successful Bluefin Tuna farming history that will complement our existing operations. We have previously identified a number of potential targets but we have not yet entered into negotiations with any of them. We had preliminary discussions with certain potential acquisition targets, but those discussions have ceased. No acquisitions are probable for the foreseeable future. Any future acquisition will be subject to available financing, which could include cash on hand, the issuance of additional debt or equity, or alternative financing plans, such as refinancing or restructuring our debt, selling assets, or reducing or delaying capital investments.

Customers, Sales and Marketing

We sell virtually all of our Bluefin Tuna to a small number of Japanese customers. In fiscal 2011, sales to four customers, Atlantis Japan, Mitsubishi Corporation, Global Seafoods Co., LTD and Sirius Ocean Inc., accounted for 98.9% of our net revenue. In fiscal 2011, sales to Atlantis Japan accounted for 71.9% of our net revenue, sales to Mitsubishi accounted for 10.8%, sales to Global Seafoods accounted for 9.3% and sales to Sirius Ocean accounted for 6.9%. In fiscal 2012, sales to these four customers plus Daito Gyorui Co., Ltd. and Kykuyo Co., LTD accounted for 99.3% of our net revenues. In fiscal 2012, sales to Atlantis Japan accounted for 30.2% of our net revenue, sales to Mitsubishi accounted for 14.9%, sales to Global Seafoods accounted for 7.1%, sales to Sirius Ocean accounted for 19.5%, sales to Daito Gyorui accounted for 15.2% and sales to Kyokuyo accounted for 12.4% .We anticipate continuing to generate a significant percentage of our revenue from a small number of Japanese customers. See “Risk Factors - Risks Related to Our Business -We depend on a small number of customers for virtually all of our revenue.”

In Croatia, approximately 99% of our Atlantic Bluefin Tuna sales in fiscal 2012 were sold as frozen fish, which typically will be picked up by the customer in its own specially equipped freezer vessels for transport to Japan. When selling fresh fish to a customer, we ship the processed fish by express delivery to the requested location. In Mexico, approximately 83% of our production in fiscal 2012 was sold as frozen product. The remaining 17% was sold fresh where the fish is harvested, cooled, packed in ice and then sent via air-freight to Japan. Our Mexican operation has sold frozen fish through both land-based (rented) containers and specially equipped freezer vessels. We expect most frozen product will be sold utilizing freezer vessels as the freezer vessels are currently more efficient from a processing standpoint.

We previously contracted with Atlantis and its affiliated entities to handle Bluefin Tuna sales for us. Our current agreement was terminated effective March 31, 2012. We do not intend to renew this agreement and will handle all future sales and marketing of our Bluefin Tuna inventory in-house. We expect that this change will reduce our selling, general and administrative expenses in the future, as we expect our internal sales fixed costs are likely to be less than a customary percentage applied across the sales that we previously outsourced.

Sustainability and Research & Development

We fully endorse the idea of sustainable farming. Our extended-cycle farming can substantially increase the biomass of the Bluefin Tuna we sell after farming compared to the biomass of the Bluefin Tuna we take from the wild fisheries. The result would be that we could significantly decrease the amount of Bluefin Tuna that is caught in the wild each year to meet market demand, thereby improving the long-term sustainability of Bluefin Tuna. In addition, one of our long term goals is developing closed-lifecycle Bluefin Tuna farming, which has the long-term potential to significantly reduce Bluefin Tuna fishing in the wild by replacing wild caught tuna with tuna spawned, hatched and raised in captivity. Scientists have achieved some encouraging results in the area of breeding tuna in captivity. However, we believe that commercialization of propagation programs is still a number of years away. We are committed to continuing this research project with the ultimate goal of profitably commercializing the full circle farming process. We have consistently worked closely with the local fisheries ministry in Croatia to formulate rules governing the industry and we are committed to working closely with the local fisheries for both operations.

| 10 |

Environmental Practices

We believe that we employ industry-leading environmental practices to ensure a sustainable business model in the changing regulatory and environmental market. Prior to commencing operations, we conduct extensive environmental impact studies, which we submit for consideration to the relevant governmental authorities in the areas where we propose to operate. Even after these agencies authorize us to commence farming operations, they conduct routine tests of indicators of adverse environmental impact. We have never been found by any authority to have created any adverse impact.

At our farms we employ open water farming, through which we ensure our pens are located in areas with multi-directional currents and with sufficient space between them to minimize concentrations of farming-related natural debris and waste. In addition, our use of purse seiners virtually eliminates the inadvertent catching of fish other than Bluefin Tuna.

Employees

As of June 30, 2012, we directly, through contract with an independent labor contractor or indirectly, through one of our variable interest entities, employed 515 persons globally, including 3 part-time employees. Of these, Umami employed 8 full-time individuals and Oceanic employed 7 full-time individuals, including executive, finance and administrative personnel. In Croatia, we had 146 employees (including 3 part-time employees), of which 45 full-time employees were employed by our variable interest entity Lubin. In Mexico, we had 354 full-time staff, all of whom were employed pursuant to an agreement with Servicios Administrativos BAF, an independent labor contractor, including 24 administrative staff members, 250 farm workers, 13 fishermen and 67 employees active in other operations. Seasonal changes occur as a result of additional hires required during the fishing season. None of our staff is represented by a labor union, and we consider our staff relations to be excellent.

Insurance

Our involvement in the fish farming industry may result in our becoming subject to liability for pollution, property damage, personal injury or other hazards. Also, we are subject to loss or mortality of our tuna inventories. We carry insurance in both our Croatia operations and our Mexico operations to mitigate these risks.

Competition

In general, the Bluefin Tuna trade market is intensely competitive and highly fragmented. Gaining market share in the Bluefin Tuna trade market is difficult because of regulatory matters involving increasing quota enforcement and more stringent licensing and registration requirements. We compete with various companies, many of which are producing products similar to ours. Our competitors in the Adriatic and Mediterranean that produce Bluefin Tuna are Fuentes e Hijos (Spain), Aquadem (Turkey), Azzopardi (Malta), Sagun (Turkey) and Balfego (Spain). In Mexico, we compete with Maricultura del Norte and Aquacultura Baja California. As of June 30, 2012, we held approximately 72% of the Bluefin Tuna farming concessions issued in Croatia, or 5,030 metric tons out of 6,980 issued in total. 6 Our future competitors may have competitive advantages, including but not limited to greater resources that can be devoted to the development of extended-cycle Bluefin Tuna farming and gaining market share, more established sales channels, greater aquaculture operational experience, and/or greater name recognition.

6 International Commission for the Conservation of Atlantic Tunas, ICCAT Record of BFT Farming Facilities webpage filtered for Croatia publicly available at www.iccat.int/en/ffb.asp.

| 11 |

Regulation

Environmental Laws

We are subject to international quotas and to various national, provincial and local environmental protection laws and regulations, including certifications and inspections relating to the quality control of our production. During the years ended June 30, 2012 and June 30, 2011, we spent approximately $0.3 million and $0.2 million, respectively, on environmental law compliance, consisting primarily of various ICCAT and veterinary inspection fees, environmental monitoring fees and biological waste disposal costs.

Croatian Environmental Law

Our Croatian operation is subject to laws and rules that regulate the location, design and operation of its farming sites. Under Croatia's Environment Protection Act of 2007, we are required to apply for location permits, which are issued by the respective authority for each farming location and in accordance with local ordinances. Applications must be accompanied by an environmental impact assessment that will identify, describe and evaluate in an appropriate manner the impact of the relevant project on the environment, by establishing the possible direct and indirect effects of the project on the soil, water, sea, air, forest, climate, human beings, flora and fauna, landscape, material assets and cultural heritage, taking into account their mutual interrelations. Concession contracts (discussed below) relating to each site are entered into based on the relevant location permits.

We are also subject to ongoing environmental monitoring requirements in Croatia, including testing the quality of the water and performing emission measurements for all our installations. We are required to conduct monitoring of our impact on the environment from two to four times per year at all our Croatian sites, which is conducted by an independent company. The monitoring includes seawater analyses performed by the Institute for Public Health in Zadar pursuant to rules established by the respective location permits.

Each of our farming locations in Croatia is provided with a location permit approved by the Croatian Ministry of Environmental Protection. We believe that we are in material compliance with Croatian applicable environmental laws and regulations.

Mexican Environmental Law and Compliance

The Mexican General Act for Ecologic Balance and the Protection of the Environment of 1988, or the “General Act,” was influenced by U.S. environmental laws such as the Environmental Impact Act, the Clean Water Act, the Clean Air Act and the National Environmental Policy Act. The General Act provides for specific criminal and administrative sanctions assessable upon a failure to comply with regulations regarding hazardous materials and also serves as the main legal framework of the federal environmental agency in charge of issuing the technological standards for federal, state and local authorities to determine environmental for non-compliance.

The General Act for Sustainable Fishing and Aquaculture (Ley de Pesca, 2007) and its Regulations (Reglamento de la Ley de Pesca) constitute the main legal framework governing the conservation, preservation, exploitation and management of all aquatic flora and fauna in Mexico. There are also certain secondary statutes, such as Official Mexican Standards, or "NOMs." NOMs applicable to our business are mainly related to water waste and sanitary rules applicable to our product.

The Ministry of Agriculture, Livestock, Rural Development, Fisheries and Food, or "SAGARPA" and the National Commission of Aquaculture and Fisheries, or "CONAPESCA," are the authorities in Mexico responsible for the management, coordination and development of policies regarding the sustainable use and exploitation of fisheries and aquatic resources.

Our aquaculture activities are developed in federal water bodies under a concession title issued by CONAPESCA. In accordance with the General Act, the protection of aquatic ecosystems and their ecological balance must be taken into account when granting concession titles for aquaculture activities. In this same regard, as described herein, the application for a concession title must be accompanied with an environmental impact assessment. Authorization by the Ministry of Environment and Natural Resources, or "SEMARNAT," is required if the intended activities may cause ecological imbalances or otherwise may surpass the limits and conditions set forth in the applicable regulations that protect the environment and the preservation and restoring of the ecosystems. To initiate our activities, an application was filed before SEMARNAT. SEMARNAT resolved that our activities cause no imbalances and are within the limits and conditions set forth in the applicable regulations that protect the environment and the preservation and restoration of the ecosystems.

| 12 |

Under Mexican law, generators of waste are categorized in accordance with the volume of waste they generate, as follows: (i) micro-generators (up to 400 kilograms per year); (ii) small-generators (from 400 kilograms to 10 tons per year), and (iii) large-generators (more than 10 tons per year). Our activities produce a volume of waste that categorizes us as micro-generators.

Our activities in Mexico produce hazardous and non-hazardous waste. Hazardous waste includes industrial waste with corrosive, reactive, explosive, toxic, flammable or biological-infectious characteristics. Although all residues may entail environmental obligations for generators, hazardous residues are subject to compliance with the most stringent rules. In our case, our business generates waste oils. Therefore, among our obligations in respect of hazardous waste are: (i) obtaining a registration before SEMARNAT of our management program for hazardous waste, and (ii) maintaining a record for our disposals (through official forms). There is no obligation to report this information.

In respect of the non-hazardous waste generated by our activities (mainly animal organic waste), we are subject to the provisions of the Environmental Protection Act of Baja California, or the “Environmental Provincial Act.” This statute provides for the management of special waste and the generators' responsibility to handle, transport and dispose of solid waste, unless that waste is transferred to the competent authority or to an authorized private company. Liability ceases upon deposit of the waste in authorized containers or at sites approved by the competent authority. In addition, the Environmental Provincial Act establishes that generators of special waste must maintain a Waste Management Program that specifies the form in which special waste is selected, gathered, transported and recycled after treatment or their final disposal in controlled terms. All non-hazardous waste must be handled by authorized companies registered as non-hazardous waste generators. It is mandatory to file annual reports to the relevant authority.

As mentioned above, we are also subject to the National Waters Act and the General Act for Sustainable Fishing and Aquaculture in Mexico, which, among other things, governs the grant of concessions for commercial fisheries. Concession holders have, among others, the following environmental obligations:

| • | Assist in the preservation of the environment and the conservation and reproduction of species, including repopulation programs; | ||

| • | comply with the NOMs and measures of aquatic health; and | ||

| • | maintain in good condition land-based establishments and permanent or temporary cultivation equipment in water bodies. | ||

We are also required to monitor our activities on all our farming sites for ongoing compliance and we are subject to periodic inspections. Our environmental monitoring requirements in Mexico include testing the quality of the water for harm caused by normal daily feeding activities (including the water's oxygen level, temperature and visibility), performing bi-weekly nutrient analysis of the water column, and performing sediment testing at each site twice per year to measure any impact on the local marine environment.

We have obtained permits for each farming location in Mexico and believe that we are in material compliance with applicable environmental laws and regulations.

Fishing Quotas

Internationally, ICCAT regulates Atlantic Bluefin Tuna quotas that are allocated to and enforced by individual countries, including Croatia. ICCAT quotas for individual countries can vary each year depending on the status of tuna stock worldwide. The Croatian Fishing Ministry allocates the ICCAT-mandated quota for Croatia annually on a boat-by-boat basis. Each boat permitted to engage in fishing activities each year by the Croatian Fishing Ministry is allocated a percentage of the total annual ICCAT fishing quota for that calendar year by the Croatian Fishing Ministry. For calendar year 2012, ICCAT allocated a quota of 367 metric tons to Croatia, of which we secured 36%, or 133 metric tons.

Fishing quotas in Croatia can be transferred, leased or assigned to other boat operators. In addition to the quota we own in Croatia, we also regularly lease quota from other boat operators. The Croatian Fishing Ministry also limits the number of boats that can fish for Bluefin Tuna in any given fishing season. In calendar year 2012, of the 39 boats allocated fishing quotas by ICCAT, only nine were permitted by the Croatian Fishing Ministry to engage in fishing activities. We had the right to receive the fish caught by three of those boats. In 2013, the number of boats will be decreased to seven. The number of boats allowed in subsequent years has not yet been determined.

ICCAT divides the boat allocations into three categories-boats up to 24 meters, boats from 24 meters to 40 meters and boats over 40 meters. ICCAT determines which boats to allow to fish by reviewing the fish quota allocations for all the boats over the past several years. The boats with the highest quotas (either quotas expressly granted to the boat or assigned to the boat by another operator) are granted fishing permits.

| 13 |

If any boat violates a provision of the ICCAT regulations, its fishing license is revoked and it is prohibited from any further fishing.

Farming Concessions

We operate our farming sites under concession permits granted by the applicable national authorities of Croatia and Mexico.

In Croatia, we currently operate five farming sites with an aggregate input quota of 1,972 metric tons of new Bluefin Tuna per annum. Following is a detailed breakdown of our farming sites and the terms of our concessions in Croatia as of June 30, 2012, which are based on both new fish allowed to enter farms annually and total farm fish holding capacity:

| Site | Annual New Fish Input Quota (in metric tons) (1) | Maximum Farming Capacity (in metric tons) | Surface (in m2) | Expiration Date | Renewal Process | |||||

| Mrdjina Field B | 674 | 1,240 | 160,000 | February 28, 2026 | Restricted public bid | |||||

| Fulija (2) | - | 500 | 120,000 | December 23, 2018 | Restricted public bid | |||||

| Zverinac | 314 | 1,500 | 140,000 | December 14, 2026 | Restricted public bid | |||||

| Mrdjina Field A | 100 | 230 | 30,000 | February 28, 2026 | Restricted public bid | |||||

| Lavdara (3) | 884 | 1,560 | 197,000 | April 23, 2032 | Restricted public bid | |||||

| Total | 1,972 | 5,030 | 647,000 | |||||||

_________________________________

| (1) | Each input quota is based on historical records of the respective farm location. We believe the quotas can be re-allocated to other existing farms (to the extent it would not exceed the farm's maximum farming capacity) or to any new farming site, although any change to the terms of the permit (including the farming quotas) are subject to approval. | ||

| (2) | Fulija's annual new fish input quota is combined with Mrdjina Field B. | ||

| (3) | Our award of the Lavdara concession requires a minimum utilization of twenty-four cages by April 2013. We plan to move currently unused cages to this location to meet this requirement once our Fiscal 2012-2013 harvest has been completed. | ||

All concession permits are awarded until the indicated expiration dates. Concession permits can be revoked due to a violation or breach of the respective concession permit, including failure to pay the concession fees or misuse, such as using the farming sites in contravention of the purpose set out in the permit, failing to comply with environment protection regulations and damaging the area surrounding farming sites. Prior to the revocation of the respective permit due to the violation and breach of the permit terms, the competent state authority gives the permit holder a chance to cure the non-compliance. Upon expiration, each of these concessions will be open for public bid if the competent local authority determines it is appropriate to subject the concession to a public bidding process. Concession permits may be terminated prior to the expiration of the term, even without any breach or violation, if the Croatian Parliament determines it is in the public interest to terminate the concession permit. Upon such termination, the concession user is entitled to recover damages.

| 14 |

In Mexico, we currently operate five sites, which are allowed an aggregate input of 2,720 additional metric tons of Bluefin Tuna per annum. Following is a detailed breakdown of our farming sites and the terms of our concessions in Mexico as of June 30, 2012:

| Site | Farm (in metric tons) (1) | Maximum Number of Cages | Expiration Date | Renewal Process | ||||

| Isla Coronado 1 | 720 | 18 | November 23, 2020 | Auto-renewal by the Mexico Department of Fisheries | ||||

| Bahia Salsipuedes 1 (2) | 400 | 10 | August 15, 2022 | Auto-renewal by the Mexico Department of Fisheries | ||||

| Isla de Coronado 2 | 800 | 20 | October 10, 2014 | Auto-renewal by the Mexico Department of Fisheries | ||||

| Bahia Salsipuedes 2 | 400 | 10 | November 8, 2015 | Auto-renewal by the Mexico Department of Fisheries | ||||

| Punta Banda | 400 | 10 | August 16, 2020 | Auto-renewal by the Mexico Department of Fisheries | ||||

| Total | 2,720 | 68 | ||||||

_________________________________

| (1) | Based on maximum input per annum. | |

| (2) | This concession site was moved to Punta Banda in fiscal 2012. | |

All concession permits are awarded until the indicated expiration dates, but can be suspended or revoked by the authorities citing the public interest. All four of these concessions may be extended with CONAPESCA's approval. For such purposes, an application requesting the extension of the concession period must be filed with CONAPESCA at least 30 days in advance of expiration; where applicable, the environmental impact authorizations must be in full force and effect. A concession title may be extended for an equivalent period, and the extension is subject to: (i) assessment of compliance with all the obligations established in the concession title; (ii) the opinion of the National Institute of Fishing, or “INAPESCA”, and (iii) compliance with the Programs of Aquaculture Management. Like in Croatia, we monitor various indicators of sea water quality in our Mexico operations daily or monthly, as applicable.

In addition, Croatian and Mexican governmental agencies require commercial fishing vessels to be licensed. Individual operators of the vessels are also subject to permit requirements. In Mexico, in connection with applicable regulations, these permits are issued by CONAPESCA. The permits require us to inform the competent authorities of the volume and location of the catch and report all the activities in the vessel through a log book.

We believe that our Croatian and Mexican operations are currently in compliance with all material aspects of these quota and licensing requirements.

Reports to Securityholders

We file annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and proxy and information statements and amendments to reports filed or furnished pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended. You may read and copy these materials at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. You may obtain information on the operation of the public reference room by calling the SEC at 1-800-SEC-0330. The SEC also maintains a website (http://www.sec.gov) that contains reports, proxy and information statements and other information regarding us and other companies that file materials with the SEC electronically.

Item 1A. RISK FACTORS

The following factors could cause our actual results to differ materially from those contained in forward-looking statements made in this Annual Report on Form 10-K and presented elsewhere by our management from time to time. This list should not be considered to be a complete statement of all potential risks or uncertainties as it does not describe additional risks of which we are not presently aware or that we do not currently consider material. We may update our risk factors from time to time in our future periodic reports. Any of these factors may have a material adverse effect on our business, financial condition, operating results and cash flows.

| 15 |

RISKS RELATED TO OUR BUSINESS

We rely on a single product, Bluefin Tuna, for all of our revenues and therefore are highly susceptible to changes in market demand, which may be affected by factors over which we have limited or no control.

We rely on a single product, Bluefin Tuna, for all of our revenues. We therefore are highly susceptible to changes in market demand, which may be impacted by factors over which we have limited or no control. Factors that could lead to a decline in market demand for Bluefin Tuna include, but are not limited to:

| • | economic conditions, particularly in Japan; | |||

| • | evolving consumer preferences; | |||

| • | consumer perceptions about possible health risks related to Bluefin Tuna; and | |||

| • | consumer perceptions about Bluefin Tuna fishing. | |||

We sell substantially all of our Bluefin Tuna inventory to Japanese customers and distributors. Sales to Japanese customers and distributors accounted for 98.9% and 98.1% for the years ended June 30, 2012 and 2011, respectively. Changes in economic conditions may negatively impact consumer spending. Prolonged negative trends in the Japanese or global economies can adversely affect consumer spending and demand for Bluefin Tuna, which could materially and adversely affect our business in terms of results of operations, financial position and liquidity.

Research has shown that wild tuna contains relatively high levels of mercury, a toxic substance. Studies have suggested that mercury may cause health problems, including an increased risk of cardiovascular disease and neurological symptoms. The high mercury concentration in tuna relative to other fish species is due to its large size and resulting high position in the food chain and the subsequent accumulation of mercury from its diet. As awareness of the real or perceived risks associated with the consumption of a fish that contains this substance spreads, increasing numbers of people may refrain from consuming tuna.

Responding to fears of a collapse of Bluefin Tuna stock in the Mediterranean and the Pacific Ocean, a number of tuna buyers have occasionally threatened boycotts unless drastic measures are taken to protect the tuna stock. In addition, some restaurants in Europe and the United States have stopped buying Mediterranean and Pacific Bluefin Tuna and replaced the Bluefin with other tuna species. If these boycotts become more widespread, they may have a negative impact on our results of operations.

Changes in market demand for Bluefin Tuna could materially and adversely affect our business in terms of results of operations, financial position and liquidity.

We will continue to encounter risks and difficulties that companies at a similar stage of development frequently experience, including the potential failure to:

| • | obtain sufficient working capital to support our expansion; | |||||

| • | expand our product offerings and maintain the high quality of our products; | |||||

| • | manage our expanding operations; | |||||

| • | maintain adequate control of our expenses allowing us to realize anticipated income growth; | |||||

| • | implement our product development, sales, and acquisition strategies and adapt and modify them as needed; | |||||

| • | successfully integrate any future acquisitions; and | |||||

| • | anticipate and adapt to changing conditions in the tuna farming industry resulting from changes in government regulations, mergers and acquisitions involving our competitors, technological developments and other significant competitive and market dynamics. | |||||

If we are not successful in addressing any or all of the foregoing risks, our results of operations may be materially and adversely affected.

| 16 |

Because we derive all of our revenue from our Bluefin Tuna inventory and carry a significant portion of our assets in fish inventory, deterioration in inventory value and levels, which may be due to various factors over which we exercise limited or no control, could materially impact our business, results of operations, financial condition and liquidity.

We derive all of our revenue from Bluefin Tuna sales and carry a significant portion of our assets in fish inventory. For the year ended June 30, 2012, we generated net revenue of $97.4 million from inventory sales. At June 30, 2012, our fish inventory accounted for $40.7 million, or 37% of our total assets. Because of our reliance on a single inventory item for all of our revenue, we are highly susceptible to changes in Bluefin Tuna market prices and dependent on Bluefin Tuna sales as a source of liquidity. Bluefin Tuna market prices can be materially affected by foreign exchange rate changes, changes in consumer discretionary spending, macro-economic conditions, particularly in Japan, evolving consumer preferences, consumer perceptions about possible health risks related to sushi and sashimi in general, and Bluefin Tuna sushi or sashimi in particular, consumer perceptions about Bluefin Tuna fishing, changing conditions in Bluefin Tuna fisheries, customer consolidation and price seasonality.

We are also subject to significant changes in inventory value due to factors related to inventory losses. In particular, mortality occurring during the farming process and inclement weather can have a significant impact on inventory levels. For example, in the years ended June 30, 2012 and 2011, we suffered storm losses totaling approximately $0.2 million and $2.9 million in book value, respectively. Finally, while we have not had historical problems with infectious disease or water quality, each of these has the potential to have a material negative effect on our inventory.

Market price and inventory changes caused by factors over which we have limited or no control can also materially and adversely affect our liquidity. A significant reduction in our inventory levels or value could impair or prevent us from obtaining financing and executing our growth strategies, and could materially and adversely affect our financial condition and results of operations. Such reduction in inventory could also result in a default under our credit agreements and make any outstanding amounts immediately due and payable.

We may be adversely affected by fluctuations in raw material prices used in our farming operations.

Aside from original acquisition costs, feed costs, including sardines, anchovies, mackerel, herring, squid and other small fish related to farming our Bluefin Tuna is the largest component of our cost of goods sold. Feed costs experience price volatility caused by events such as market fluctuations, weather conditions, contamination of or disease outbreak in the population of fish used as feed or changes in governmental programs. The market price of these feed materials may also experience significant upward adjustment, if, for instance, there is a material under-supply or over-demand in the market resulting in a limitation on the availability of raw materials, which would hinder our ability to create biomass through our farming operations. These price changes may ultimately result in increases in the selling prices of our products, and may, in turn, adversely affect our sales volume, revenue and operating profit. If we are unable to pass on increases in our raw material costs, our margins could be materially and adversely affected.

We farm a significant portion of our Bluefin Tuna, and variations in our Bluefin Tuna's growth rates could have a material adverse effect on our business.

We farm a significant portion of our Bluefin Tuna and rely on biomass increases resulting from our farming efforts for a substantial portion of inventory growth. For example, in the years ended June 30, 2012 and 2011, biomass increases from farming accounted for 55% and 30% of our Bluefin Tuna inventory increases. Bluefin Tuna growth rates are subject to significant variation due to numerous factors, many of which are partially or completely beyond our control, including:

| • | water temperatures; | ||

| • | the average size and overall size distribution of our Bluefin Tuna in any given period; and | ||

| • | the quality of the feed we are able to obtain for our Bluefin Tuna. | ||

Variations in Bluefin Tuna growth rates could have a material and adverse effect on our liquidity and results of operations.

Our Mexico operations rely primarily on catching Bluefin Tuna to replace or increase inventory levels, and variations in the quantity of Bluefin Tuna we catch during a fishing season can materially impact our potential future revenues.

We have historically sold a significant percentage of our Bluefin Tuna inventory at our Baja Mexico operations each year. To replace or increase inventory, we rely on our ability to catch Bluefin Tuna during the fishing period. Fishing results can be highly variable, and we may be unable to catch an adequate number of Bluefin Tuna necessary to replace or increase inventory levels during a fishing season. Any inability to do so would negatively impact our potential future revenue and liquidity.

| 17 |

We may decide to purchase Bluefin Tuna from third parties, which can be significantly more expensive than catching Bluefin Tuna ourselves and therefore would negatively impact our margins.

Depending in part upon our success in fishing, we may be required to purchase Bluefin Tuna from third parties to meet our revenue targets. Certain purchases Bluefin Tuna from third parties has historically been much more expensive than the acquisition costs associated with fishing. Further, adequate supplies of Bluefin Tuna may not be available at reasonable prices, or at all. If we are required to purchase Bluefin Tuna from third parties, our margins will be negatively affected. If adequate supplies of Bluefin Tuna are not available at all, our results of operations and liquidity could be negatively affected.

Our management has significant discretion over how much Bluefin Tuna to harvest each year, and a decision to harvest a significant portion of our inventory in a given year could materially impact our future potential revenues.

Our management has significant discretion over how much Bluefin Tuna to harvest each year. A decision to harvest a significant portion of our inventory in a given year could materially and negatively impact our future potential revenues. A decision to farm an increased portion of our inventory in a given year could materially and negatively impact revenues in that period because it would result in a small amount of fish harvested and sold during that period, which is our only source of revenue.

We sell substantially all of our Bluefin Tuna to only a few customers.

We have derived, and expect to continue to derive, nearly all of our revenue from sales to a small number of customers. For the year ended June 30, 2012, our top six customers accounted for 99.3% of our net revenue. These customers sell almost all of their Bluefin Tuna to only a few trading houses for further sale into the Japanese market. We do not have long-term agreements with our customers. Accordingly, a customer may, on short or no notice, decide that it wishes to cease purchasing our Bluefin Tuna. The loss of any of these customers or non-payment of outstanding amounts due to us by any of them could materially and adversely affect our business in terms of results of operations, financial position and liquidity.

All of our significant customer contracts and some of our supplier contracts are short-term and may not be renewable on terms favorable to us, or at all.

All of our customers and some of our suppliers operate through purchase orders or short-term contracts. Though we have long-term business relationships with many of our customers and suppliers and alternative sources of supply for key items, we cannot be sure that any of these customers or suppliers will continue to do business with us on the same basis. Additionally, although we try to renew these contracts as they expire, there can be no assurance that these customers or suppliers will renew these contracts on terms that are favorable to us, if at all. The termination of, or modification to, any number of these contracts may adversely affect our business and prospects, including our financial performance and results of operations.

A decline in discretionary consumer spending may adversely affect our industry, our operations, and ultimately our profitability.

Luxury products, such as premium grade Bluefin Tuna sushi and sashimi, are discretionary purchases for consumers. Any reduction in consumer discretionary spending or disposable income may affect the Bluefin Tuna industry more significantly than other industries. Many economic factors outside of our control could affect consumer discretionary spending, including the financial markets, consumer credit availability, prevailing interest rates, energy costs, employment levels, salary levels, and tax rates. Any reduction in discretionary consumer spending could materially adversely affect our business and financial condition.

Consolidation among our customers could lead to a reduction in selling prices and customer loss, which would harm our business, financial condition, operating margins, and operating results.