Attached files

| file | filename |

|---|---|

| 8-K - 8-K - VEREIT, Inc. | v347274_8-k.htm |

| EX-99.2 - EXHIBIT 99.2 - VEREIT, Inc. | v347274_ex99-2.htm |

American Realty Capital Properties Pending Acquisition of GE Capital Portfolio in a $807 Million Transaction June 2013 CapLeaseMerger and GE Capital Acquisition will Create Pro Forma Enterprise Value of Nearly $7 Billion GE Capital Acquisition Will Further Diversify ARCP’s Net Lease Portfolio by Adding 471 Net Lease Properties 2013 Acquisitions Will Create a Portfolio of at Least 1,264 Net Lease Properties ARCP Raises $900 Million via Private Placements of Common Stock and Convertible Preferred Stock

2 ARCP considers funds from operations (“FFO”) and adjusted FFO (“AFFO”), which is FFO as adjusted to exclude acquisition- related fees and expenses, amortization of above-market lease assets and liabilities, amortization of deferred financing costs, straight-line rent, non-cash mark-to-market adjustments, amortization of restricted stock, non-cash compensation and gains and losses useful indicators of the performance of a real estate investment trust (“REIT”). Because FFO calculations exclude such factors as depreciation and amortization of real estate assets and gains or losses from sales of operating real estate assets (which can vary among owners of identical assets in similar conditions based on historical cost accounting and useful-life estimates), they facilitate comparisons of operating performance between periods and between other REITs in our peer group. Accounting for real estate assets in accordance with generally accepted accounting principles (“GAAP”) implicitly assumes that the value of real estate assets diminishes predictably over time. Since real estate values have historically risen or fallen with market conditions, many industry investors and analysts have considered the presentation of operating results for real estate companies that use historical cost accounting to be insufficient by themselves. FFO and AFFO are not in accordance with, or a substitute for, measures prepared in accordance with GAAP, and may be different from non-GAAP measures used by other companies. In addition, FFO and AFFO are not based on any comprehensive set of accounting rules or principles. Non-GAAP measures, such as FFO and AFFO, have limitations in that they do not reflect all of the amounts associated with ARCP's results of operations that would be reflected in measures determined in accordance with GAAP. These measures should only be used to evaluate ARCP's performance in conjunction with corresponding GAAP measures. Additionally, ARCP believes that AFFO, by excluding acquisition-related fees and expenses, amortization of above-market lease assets and liabilities, amortization of deferred financing costs, straight-line rent, non-cash mark-to-market adjustments, amortization of restricted stock, non-cash compensation and gains and losses, provides information consistent with management's analysis of the operating performance of the properties. By providing AFFO, ARCP believes it is presenting useful information that assists investors and analysts to better assess the sustainability of our operating performance. Further, ARCP believes AFFO is useful in comparing the sustainability of our operating performance with the sustainability of the operating performance of other real estate companies, including exchange-traded and non-traded REITs. As a result, ARCP believes that the use of FFO and AFFO, together with the required GAAP presentations, provide a more complete understanding of our performance relative to our peers and a more informed and appropriate basis on which to make decisions involving operating, financing, and investing activities. Funds from Operations and Adjusted Funds from Operations

3 Forward-Looking Statements Information set forth herein contains “forward-looking statements” (as defined in Section 21E of the Securities Exchange Act of 1934, as amended), which reflect the Company’s expectations regarding future events. The forward-looking statements involve a number of risks, uncertainties and other factors that could cause actual results to differ materially from those contained in the forward-looking statements. Such forward-looking statements include, but are not limited to, whether and when the transactions contemplated by the CapLease, Inc. merger agreement and the purchase agreement for the acquisition of the GE Capital portfolio will be consummated, the new combined company’s plans, market and other expectations, objectives, intentions and other statements that are not historical facts. The following additional factors, among others, could cause actual results to differ from those set forth in the forward-looking statements: the occurrence of any event, change or other circumstances that could give rise to the termination of the merger agreement or the purchase agreement; unexpected costs or unexpected liabilities that may arise from the merger or the acquisition, whether or not consummated; continuation or deterioration of current market conditions; future regulatory or legislative actions that could adversely affect the Company; the business plans of the tenants of the properties; and risks to consummation of the merger or the acquisition, including the risk that the merger or the acquisition will not be consummated within the expected time period or at all. Additional factors that may affect future results are contained in the Company’s filings with the SEC, which are available at the SEC’s website at www.sec.gov. The Company disclaims any obligation to update and revise statements contained in these materials based on new information or otherwise.

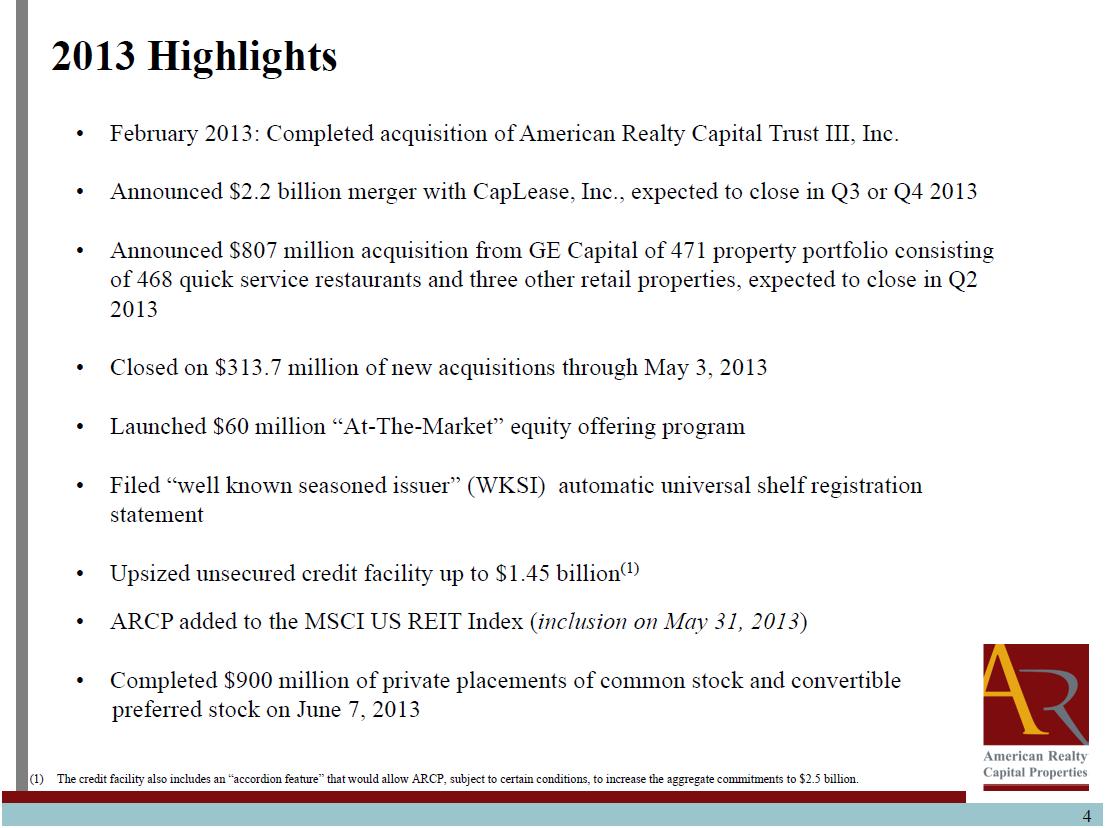

4 4 2013 Highlights • February 2013: Completed acquisition of American Realty Capital Trust III, Inc. • Announced $2.2 billion merger with CapLease, Inc., expected to close in Q3 or Q4 2013 • Announced $807 million acquisition from GE Capital of 471 property portfolio consisting of 468 quick service restaurants and three other retail properties, expected to close in Q2 2013 • Closed on $313.7 million of new acquisitions through May 3, 2013 • Launched $60 million “At-The-Market” equity offering program • Filed “well known seasoned issuer” (WKSI) automatic universal shelf registration statement • Upsized unsecured credit facility up to $1.45 billion (1) • ARCP added to the MSCI US REIT Index (inclusion on May 31, 2013) • Completed $900 million of private placements of common stock and convertible preferred stock on June 7, 2013 2013 Highlights (1) The credit facility also includes an “accordion feature” that would allow ARCP, subject to certain conditions, to increase the aggregate commitments to $2.5 billion.

5 Accretion to Earnings and Dividends: Expected to be immediately accretive to ARCP's AFFO per share by approximately $0.11 per share. Upon closing, ARCP will increase its dividend by $0.03 per share, or 3.2%, to $0.94 per share, while maintaining a conservative payout ratio. Increased Size and Scale: Pro forma enterprise value of approximately $6.0 billion, among the largest publicly traded net lease REITs. The increased size and scale resulting from the transaction significantly enhances ARCP's ability to execute large transactions and strengthens its position as an industry consolidator in the fragmented net lease real estate industry where size and cost of capital matter. Increased Diversification: ARCP's top ten tenant concentration reduces from 60% to 43% post merger (excluding the GE Capital acquisition). This transaction improves the quality of ARCP's revenue through additional diversification while strengthening the overall capital structure on a risk adjusted basis. Impact on Balance Sheet: With respect to LSE's $1.2 billion of outstanding debt, ARCP intends to assume approximately $580 million and repay the balance, thus materially reducing the legacy leverage and paying off LSE's high coupon debt and preferred equity. Management Additions, Integration and Operating Synergies: LSE's management team is expected to join American Realty Capital, the parent of ARCP's external advisor, upon completion of the merger. These additions increase the depth and breadth of the ARC team, provide management continuity of the LSE assets, add build-to-suit capabilities and bring ARCP closer to internalizing its management. $2.2 BnAcquisition of CapLease(NYSE: LSE). This acquisition provides ARCP with substantial strategic, financial and portfolio benefits.

6 Strategic Portfolio Construction:This portfolio acquisition significantly advances ARCP’s investment objectives by growing its net lease portfolio consistent with its investment strategy and further reduces its credit concentration by adding 137 new tenants. ARCP’s expected 2013 portfolio will include more than 225 distinct tenants (excluding the CapLeasemerger). High Portfolio Occupancy and Balance of Lease Duration:The Company reasonably expects its portfolio to remain approximately 100% occupied. The average remaining lease duration on the entire portfolio would be 9.0 years, reflecting the Company’s strong balance of mid-term and long-term lease durations. Only modest lease rollover would occur until 2018. Increased Size and Scale:Once ARCP completes its expected 2013 acquisitions, its portfolio of 1,264 net lease properties, containing over 30 million rentable square feet, will be one of the largest net lease portfolios among public REITs. Available Financing:Strong and diverse capital markets environment provides ARCP with flexibility in constructing attractive long-term capital structure. Increased Diversification/Reduced Concentration:2013 pro forma rental revenue generated by ARCP’s largest 10 tenants will decline from 60% to 36%. The Company’s portfolio would include tenants located in 48 states plus Puerto Rico spanning 27 industries. $807 Million GE Capital Portfolio Acquisition. 2013 acquisition targets achieved by mid-year.

7 On June 7, 2013, ARCP completed $900 million of private placements of $455 million of common stock and $445 million of preferred stock Combined net proceeds of $896 million were received, immediately reducing net leverage below $90 million Equity raise fully funds equity required for CapLeaseand GE Capital acquisitions Results in leverage neutral impact of CapLeaseand GE Capital acquisitions on balance sheet and eliminates uncertainty regarding funding for these purchases and additional pipeline acquisitions Offering led by existing institutional holders of ARCP common stock $900 Million Common and Preferred Stock Private Placement. $455 Million Common Stock Private Placement 29.4 million shares priced at $15.47 per share Priced at zero discount to prior day closing price Includes contingent value rights (CVR) agreement not to exceed $1.50 per share $445 Million Convertible Preferred Stock Private Placement 28.4 million 5.81% Series C Convertible Preferred shares with liquidation preference of $15.67 per share, a premium to prior day common stock closing price Includes CVR agreement not to exceed $2.00 per underlying common share Placement demonstrates capital structure flexibility, access to capital markets, management's execution capabilities and institutional sponsorship of ARCP strategy

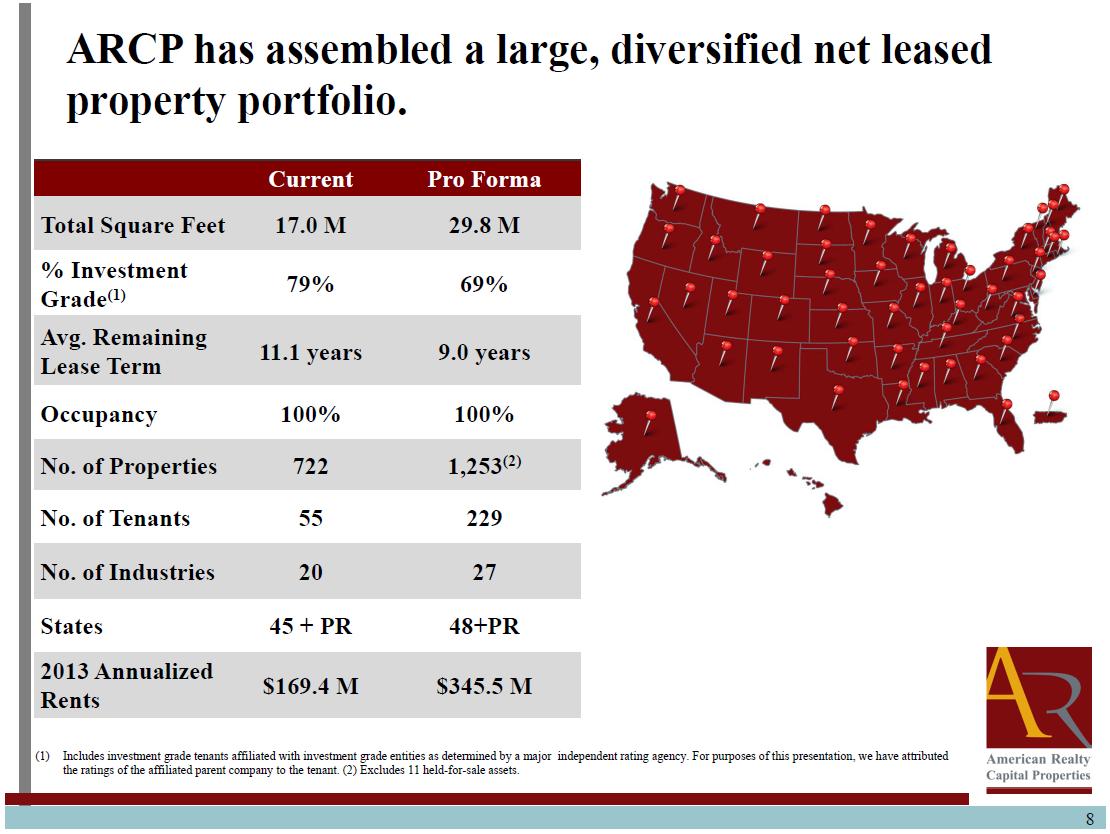

ARCP has assembled a large, diversified net leased property portfolio. 8 Current ProForma Total Square Feet 17.0 M 29.8 M % Investment Grade (1) 79% 69% Avg. Remaining Lease Term 11.1years 9.0 years Occupancy 100% 100% No. of Properties 722 1,253 (2) No. of Tenants 55 229 No. of Industries 20 27 States 45+ PR 48+PR 2013 Annualized Rents $169.4 M $345.5 M (1) Includes investment grade tenants affiliated with investment grade entities as determined by a major independent rating agency.For purposes of this presentation, we have attributed the ratings of the affiliated parent company to the tenant. (2) Excludes 11 held-for-sale assets.

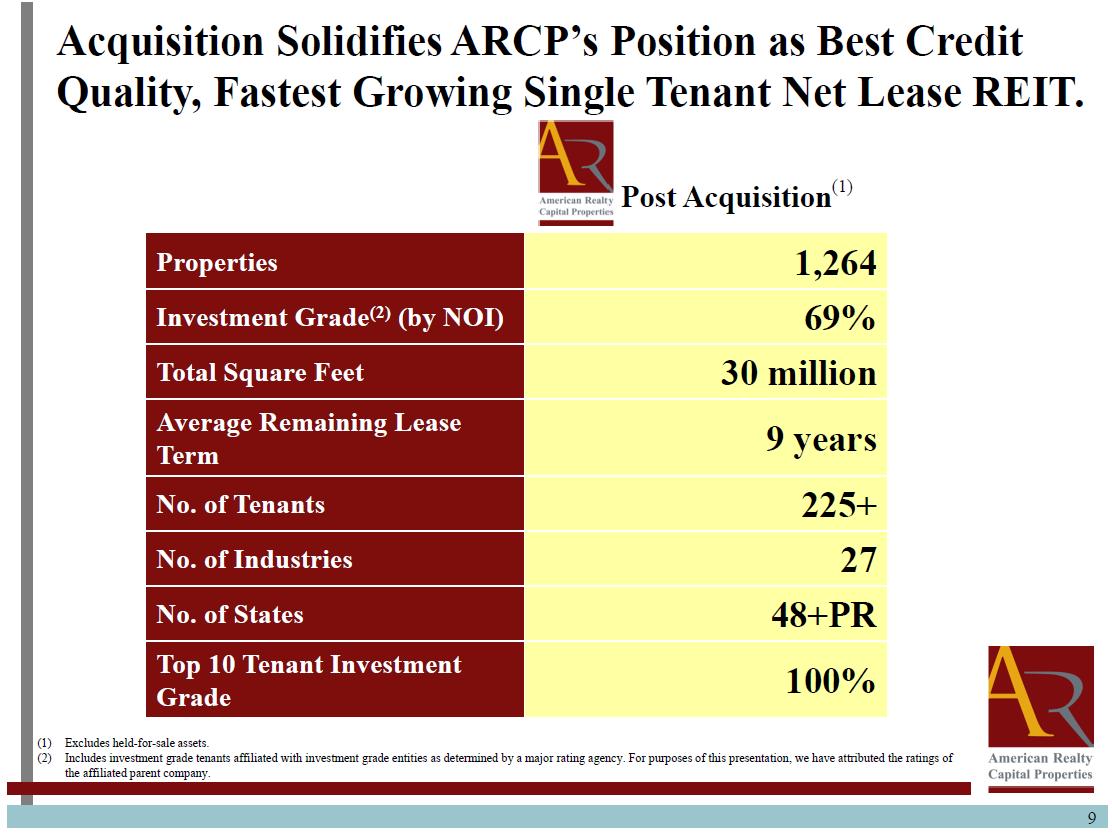

Properties 1,264 Investment Grade (2) (by NOI) 69% TotalSquare Feet 30 million Average RemainingLease Term 9 years No. of Tenants 225+ No. of Industries 27 No.of States 48+PR Top 10 Tenant Investment Grade 100% Acquisition Solidifies ARCP’s Position as Best Credit Quality, Fastest Growing Single Tenant Net Lease REIT. Post Acquisition (1) (1) Excludes held-for-sale assets. (2) Includes investment grade tenants affiliated with investment grade entities as determined by a major rating agency. For purposes of this presentation, we have attributed the ratings of the affiliated parent company. 9

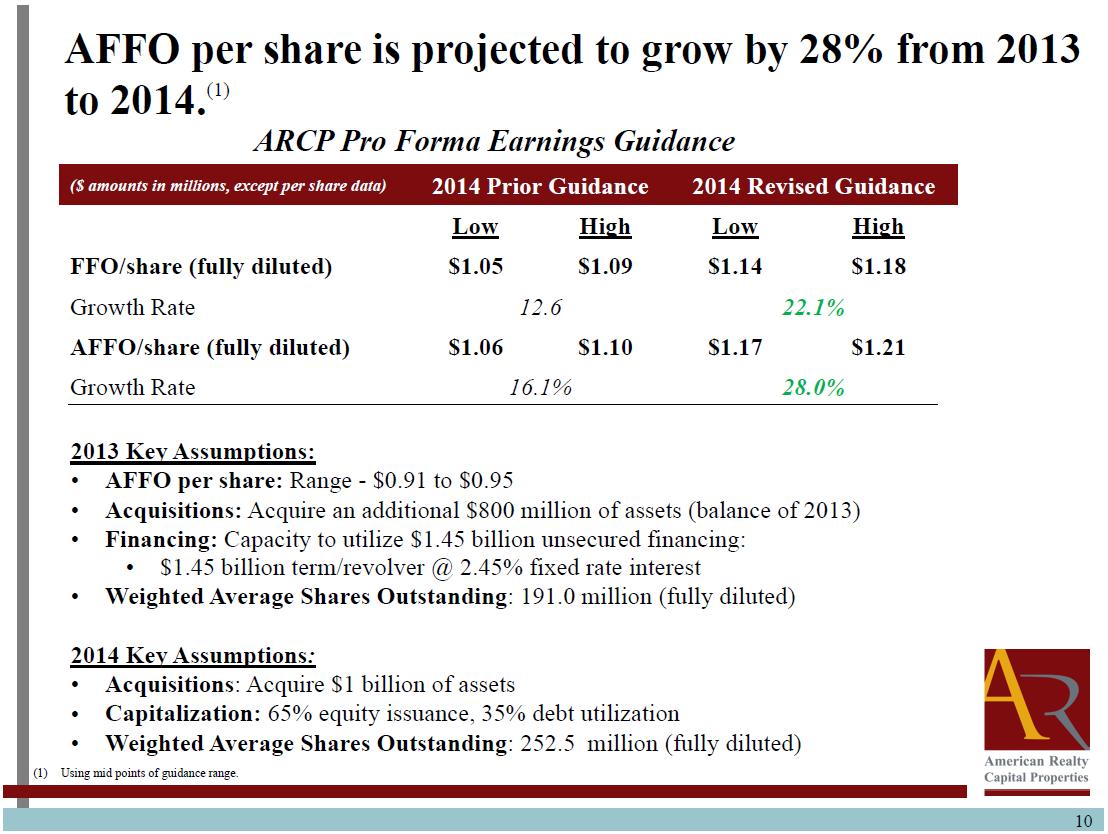

10 AFFO per share is projected to grow by 28% from 2013 to 2014. (1) ($ amounts in millions, except per share data) 2014 Prior Guidance 2014 Revised Guidance Low High Low High FFO/share(fully diluted) $1.05 $1.09 $1.14 $1.18 GrowthRate 12.6 22.1% AFFO/share(fully diluted) $1.06 $1.10 $1.17 $1.21 Growth Rate 16.1% 28.0% (1) Using mid points of guidance range. ARCP Pro Forma Earnings Guidance 2013 Key Assumptions: • AFFO per share: Range -$0.91 to $0.95 • Acquisitions:Acquire an additional $800 million of assets (balance of 2013) • Financing:Capacity to utilize $1.45 billion unsecured financing: • $1.45 billion term/revolver @ 2.45% fixed rate interest • Weighted Average Shares Outstanding: 191.0 million (fully diluted) 2014 Key Assumptions: • Acquisitions: Acquire $1 billion of assets • Capitalization:65% equity issuance, 35% debt utilization • Weighted Average Shares Outstanding:252.5 million (fully diluted)

11 Tenant %of NOI Rating (1) 5.4% BBB- 5.3% BBB+ 5.0% A 4.7% AA+ 4.7% BBB 3.9% BBB 2.0% BBB+ 1.8% A 1.7% A- 1.7% BBB- 36.2% 100.0% Top 10 Tenants = 100% Investment Grade Note: Excludes held-for-sale assets. (1) Includes investment grade tenants affiliated with investment grade entities as determined by a major independent rating agency. For purposes of this presentation, we have attributed the ratings of the affiliated parent company to the tenant. Pro Forma Top 10 Tenant Concentration Reduced to only 36%.