Attached files

| file | filename |

|---|---|

| 8-K - CURRENT REPORT - VEREIT, Inc. | v347387_8-k.htm |

Exhibit 99.1

IMMEDIATE RELEASE

American Realty Capital Properties Announces

Successful Completion of Previously Announced

$900 Million Private Placement of Common Stock and Convertible Preferred Stock

Net Proceeds to Fully Fund Recently Announced Acquisitions of CapLease and GE Capital Property Portfolio, Both of Which are Anticipated to be Immediately Accretive to ARCP upon Closing

ARCP Continues to Focus on Organic Growth and Strategic Acquisitions for Accretive External Growth

New York, New York, June 10, 2013 – American Realty Capital Properties, Inc. (“ARCP” or the “Company”) (NASDAQ: ARCP) announced today the successful completion on June 7, 2013, of two previously announced private placement transactions, pursuant to which ARCP sold approximately 29.4 million shares of its common stock at a price of $15.47 per share for gross proceeds of $455 million, and approximately 28.4 million shares of 5.81% Series C convertible preferred stock with an aggregate liquidation preference of $445 million (collectively, the “Placements”). Net proceeds from the Placements of approximately $896 million fully fund ARCP’s working capital needs and the common equity component of recently announced strategic acquisitions, including an $807 million property portfolio being acquired from GE Capital and the $2.2 billion acquisition of CapLease, Inc. (“CapLease”) (NYSE: LSE).

The Placements, originally intended to be $800 million, were oversubscribed and upsized to $900 million, and were led by existing institutional stockholders in ARCP.

“This outstanding execution has allowed the Company to raise equity to fund fully two important strategic and accretive transactions, namely CapLease and the GE Capital portfolio,” noted Nicholas S. Schorsch, Chairman and CEO of ARCP. “With the Placements, we have satisfied our target equity raise for these and our additional pipeline acquisitions, resulting in a leverage neutral impact of these acquisitions on our balance sheet on a weighted average basis, and eliminated any uncertainty regarding the sources of funding for these announced and additional pipeline purchases. This recent capitalization activity further positions the Company to continue to focus on our four-pronged growth strategy: contractual rental growth, diversification of our credit quality, organic and granular acquisitions, and strategic corporate and portfolio combinations through M&A activities.”

Added Brian S. Block, Chief Financial Officer of ARCP, “Due to the strong institutional support for our Company and demand for our equity, we have been able to place this equity at an exceedingly low cost when compared to market norms. The demand for this equity placement, especially given its size, demonstrates the attractiveness of ARCP’s property portfolio and management team, the positive market response to our growth strategy, built upon an active and accretive acquisition program, and the strength of our balance sheet and capital structure.”

RCS Capital, the investment banking and capital markets division of Realty Capital Securities, LLC and RCS Capital Corporation (NYSE: RCAP), and JMP Securities LLC served as co-placement agents in connection with the Placements.

Previously announced earnings estimates can be found in Annex A attached hereto.

Important Notice

This press release shall not constitute an offer to sell or the solicitation of an offer to buy securities. The securities sold in these private placements have not been registered under the Securities Act of 1933 and may not be offered or sold in the United States in the absence of an effective registration statement or exemption from registration requirements.

ARCP is a publicly traded Maryland corporation listed on The NASDAQ Global Select Market that qualified as a real estate investment trust for U.S. federal income tax purposes for the taxable year ended December 31, 2011, focused on acquiring and owning single tenant freestanding commercial properties subject to net leases with high credit quality tenants. Additional information about ARCP can be found on its website at www.arcpreit.com. The Company may disseminate important information regarding the company and its operations, including financial information, through social media platforms such as Twitter, Facebook and LinkedIn.

Basis of Pro Forma Data and Funds from Operations and Adjusted Funds from Operations

The rental revenue changes and statistics described above are based on the companies’ results for the three months ended March 31, 2013, and assume the acquisition occurred at the beginning of the period. Other data, such as occupancy and lease rollover figures, are based on data as of March 31, 2013.

ARCP considers FFO and AFFO, which is FFO as adjusted to exclude acquisition-related fees and expenses, amortization of above-market lease assets and liabilities, amortization of deferred financing costs, straight-line rent, non-cash mark-to-market adjustments, amortization of restricted stock, non-cash compensation and non-recurring gains and losses useful indicators of the performance of a REIT. Because FFO calculations exclude such factors as depreciation and amortization of real estate assets and gains or losses from sales of operating real estate assets (which can vary among owners of identical assets in similar conditions based on historical cost accounting and useful-life estimates), they facilitate comparisons of operating performance between periods and between other REITs in ARCP’s peer groups. Accounting for real estate assets in accordance with GAAP implicitly assumes that the value of real estate assets diminishes predictably over time. Since real estate values have historically risen or fallen with market conditions, many industry investors and analysts have considered the presentation of operating results for real estate companies that use historical cost accounting to be insufficient by themselves.

Additionally, ARCP believes that AFFO, by excluding acquisition-related fees and expenses, amortization of above-market lease assets and liabilities, amortization of deferred financing costs, straight-line rent, non-cash mark-to-market adjustments, amortization of restricted stock, non-cash compensation and non-recurring gains and losses, provides information consistent with management's analysis of the operating performance of the properties. By providing AFFO, ARCP believes they are presenting useful information that assists investors and analysts to better assess the sustainability of their operating performance. Further, ARCP believes AFFO is useful in comparing the sustainability of their operating performance with the sustainability of the operating performance of other real estate companies, including exchange-traded and non-traded REITs.

As a result, ARCP believes that the use of FFO and AFFO, together with the required GAAP presentations, provide a more complete understanding of our performance relative to our peers and a more informed and appropriate basis on which to make decisions involving operating, financing, and investing activities.

FFO and AFFO are not in accordance with, or a substitute for, measures prepared in accordance with GAAP, and may be different from non-GAAP measures used by other companies. In addition, FFO and AFFO are not based on any comprehensive set of accounting rules or principles. Non-GAAP measures, such as FFO and AFFO, have limitations in that they do not reflect all of the amounts associated with ARCP’s results of operations that would be reflected in measures determined in accordance with GAAP. These measures should only be used to evaluate ARCP’s performance in conjunction with corresponding GAAP measures.

Additional Information and Where to Find It

This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. In connection with the proposed transaction, CapLease expects to prepare and file with the Securities and Exchange Commission (“SEC”) a proxy statement and other documents regarding the proposed transaction. The proxy statement will contain important information about the proposed transaction and related matters. STOCKHOLDERS ARE URGED TO READ THE PROXY STATEMENT (INCLUDING ALL AMENDMENTS AND SUPPLEMENTS THERETO) AND OTHER RELEVANT DOCUMENTS FILED BY ARCP OR CAPLEASE WITH THE SEC CAREFULLY IF AND WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT ARCP, CAPLEASE AND THE PROPOSED TRANSACTION.

Investors and security holders of CapLease will be able to obtain free copies of the proxy statement and other relevant documents filed by CapLease with the SEC (if and when then become available) through the website maintained by the SEC at www.sec.gov. Copies of the documents filed by CapLease with the SEC are also available on CapLease’s website at www.caplease.com, and copies of the documents filed by ARCP with the SEC are available on ARCP’s website at www.arcpreit.com.

Participants in Solicitation

The directors, executive officers and employees of CapLease may be deemed “participants” in the solicitation of proxies from stockholders of CapLease in favor of the proposed merger. Information regarding the persons who may, under the rules of the SEC, be considered participants in the solicitation of the stockholders of CapLease in connection with the proposed merger will be set forth in the proxy statement and the other relevant documents to be filed with the SEC. You can find information about CapLease’s executive officers and directors in its Annual Report on Form 10-K for the fiscal year ended December 31, 2012, and in its definitive proxy statement filed with the SEC on Schedule 14A on April 19, 2013.

Forward-Looking Statements

Information set forth herein (including information included or incorporated by reference herein) contains “forward-looking statements” (as defined in Section 21E of the Securities Exchange Act of 1934, as amended), which reflect ARCP’s and CapLease’s expectations regarding future events. The forward-looking statements involve a number of risks, uncertainties and other factors that could cause actual results to differ materially from those contained in the forward-looking statements. Such forward-looking statements include, but are not limited to whether and when the transactions contemplated by the merger agreement will be consummated, the new combined company’s plans, market and other expectations, objectives, intentions, as well as any expectations or projections with respect to the combined company, including regarding future dividends and market valuations, and estimates of growth, including FFO and AFFO, and other statements that are not historical facts.

The following additional factors, among others, could cause actual results to differ from those set forth in the forward-looking statements: (1) the occurrence of any event, change or other circumstances that could give rise to the termination of the merger agreement with CapLease; (2) the inability to complete the proposed merger due to the failure to obtain CapLease stockholder approval for the merger or the failure to satisfy other conditions to completion of the merger, including that a governmental entity may prohibit, delay or refuse to grant approval for the consummation of the merger; (3) risks related to disruption of management’s attention from the ongoing business operations due to announced transactions with CapLease and GE Capital; (4) the effect of the announcement of the proposed merger on CapLease’s or ARCP’s relationships with its customers, tenants, lenders, operating results and business generally; (5) the outcome of any legal proceedings relating to the merger or the merger agreement; (6) risks to consummation of the merger, including the risk that the merger will not be consummated within the expected time period or at all; (7) the occurrence of any event, change or other circumstances that could give rise to the termination of the purchase agreement with GE Capital; and (8) risks to consummation of the GE Capital portfolio acquisition, including the risk that the portfolio will not be acquired within the expected time period or at all. Additional factors that may affect future results are contained in ARCP’s and CapLease’s (solely with respect to the CapLease transaction) filings with the SEC, which are available at the SEC’s website at www.sec.gov. ARCP and CapLease (solely with respect to the CapLease transaction) disclaim any obligation to update and revise statements contained in these materials based on new information or otherwise.

| Contacts | |

| From: Anthony J. DeFazio | For: Brian S. Block, EVP & CFO |

| DDCWorks | American Realty Capital Properties, Inc. |

| tdefazio@ddcworks.com | bblock@arlcap.com |

| Ph: 484-342-3600 | Ph: 212-415-6500 |

Annex A

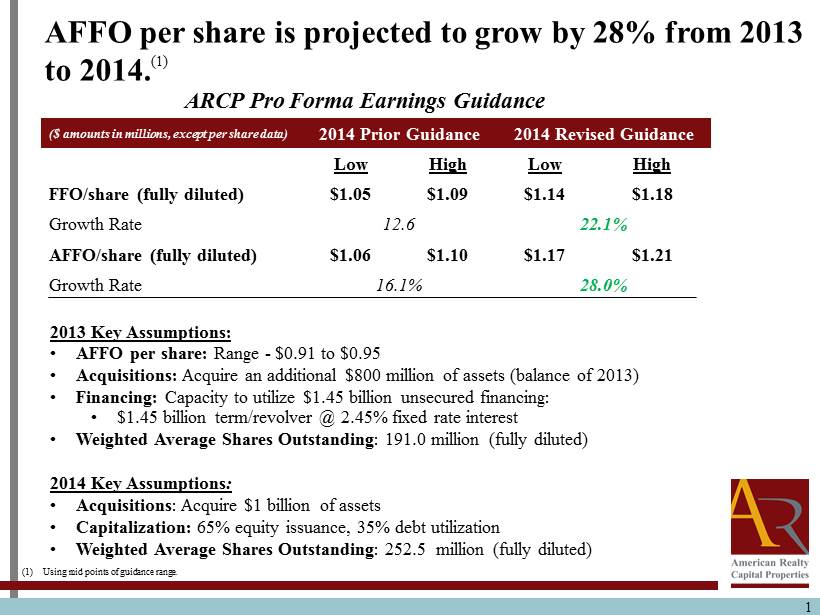

1 AFFO per share is projected to grow by 28% from 2013 to 2014. ( 1 ) ($ amounts in millions, except per share data) 2014 Prior Guidance 2014 Revised Guidance Low High Low High FFO/share (fully diluted) $1.05 $1.09 $1.14 $1.18 Growth Rate 12.6 22.1% AFFO/share (fully diluted) $1.06 $1.10 $1.17 $1.21 Growth Rate 16.1% 28.0 % (1) Using mid points of guidance range. ARCP Pro Forma Earnings Guidance 2013 Key Assumptions: • AFFO per share: Range - $0.91 to $0.95 • Acquisitions: Acquire an additional $800 million of assets (balance of 2013) • Financing: Capacity to utilize $1.45 billion unsecured financing: • $1.45 billion term/revolver @ 2.45% fixed rate interest • Weighted Average Shares Outstanding : 191.0 million (fully diluted) 2014 Key Assumptions : • Acquisitions : Acquire $1 billion of assets • Capitalization: 65% equity issuance, 35% debt utilization • Weighted Average Shares Outstanding : 252.5 million (fully diluted)