Attached files

| file | filename |

|---|---|

| EX-31.2 - EX-31.2 - SARATOGA INVESTMENT CORP. | a13-1985_1ex31d2.htm |

| EX-31.1 - EX-31.1 - SARATOGA INVESTMENT CORP. | a13-1985_1ex31d1.htm |

The following items are the subject of a Form 12b-25 and are not included herein: separate audited financial statements of GSC Investment Corp. CLO 2007, Ltd. required by Rule 3-09 of Regulation S-X to be included in Part II, Item 8, and the exhibits required by Item 601(b)(32) of Regulation S-K.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

|

x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

|

For the fiscal year ended February 28, 2013 | |

|

| |

|

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

|

For the transition period from to | |

Commission File No. 001-33376

SARATOGA INVESTMENT CORP.

(Exact name of Registrant as specified in its charter)

|

Maryland |

|

20-8700615 |

535 Madison Avenue

New York, New York 10022

(Address of principal executive offices)

(212) 906-7800

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

|

Title of Each Class |

|

Name of Each Exchange on Which Registered |

|

|

|

Common Stock, par value $0.001 per share |

|

The New York Stock Exchange |

|

|

|

7.50% Notes due 2020 |

|

The New York Stock Exchange |

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days: Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer o |

|

Accelerated filer o |

|

|

|

|

|

Non-accelerated filer x |

|

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant as of August 31, 2012 was approximately $41.6 million based upon a closing price of $16.50 reported for such date by the New York Stock Exchange.

The number of outstanding common shares of the registrant as of May 29, 2013 was 4,730,116.

DOCUMENTS INCORPORATED BY REFERENCE

None.

EXPLANATORY NOTE

In accordance with a new position of the staff of the Division of Investment Management of the Securities and Exchange Commission (the “SEC”) with respect to the application of Rule 3-09 of Regulation S-X to business development companies, Saratoga Investment Corp. (the “Company”) is now required to include separate audited financial statements for one of its portfolio companies, GSC Investment Corp. CLO 2007, Ltd. (“Saratoga CLO”), in this Annual Report on Form 10-K for the fiscal year ended February 28, 2013 (the “Form 10-K”). The Company needs to complete some additional work with respect to the financial statements of Saratoga CLO prior to filing such financial statements with the Form 10-K. As a result, this Form 10-K omits such separate audited financial statements for Saratoga CLO. The omission of such separate audited financial statements has no affect on the financial statements for the Company included therein and is consistent with the Company’s previous reporting.

In addition, due to the omission of such separate audited financial statements for Saratoga CLO in the Form 10-K, the Company’s principal executive officer and principal financial officer are unable to provide the certifications required by Item 601(b)(32) of Regulation S-K with the Form 10-K.

The Company plans to file an amendment to the Form 10-K to include such separate audited financial statements and certifications as soon as practicable on or before the fifteenth calendar day following May 29, 2013 (the original due date for filing the Form 10-K with the SEC).

NOTE ABOUT REFERENCES

In this Annual Report on Form 10-K (the “Annual Report”), the “Company,” “we,” “us” and “our” refer to Saratoga Investment Corp. and its wholly owned subsidiary, Saratoga Investment Funding LLC, unless the context otherwise requires. We refer to Saratoga Investment Advisors LLC, our investment adviser, as “Saratoga Investment Advisors” or the “Investment Adviser.”

NOTE ABOUT FORWARD-LOOKING STATEMENTS

Some of the statements in this Annual Report constitute forward-looking statements. Forward-looking statements relate to expectations, beliefs, projections, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. In some cases, you can identify forward-looking statements by terms such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “project,” “should,” “will” and “would” or the negative of these terms or other comparable terminology.

The forward-looking statements are based on our beliefs, assumptions and expectations of our future performance, taking into account all information currently available to us. These beliefs, assumptions and expectations can change as a result of many possible events or factors, not all of which are known to us or are within our control. If a change occurs, our business, financial condition, liquidity and results of operations may vary materially from those expressed in our forward-looking statements.

The forward-looking statements contained in this Annual Report involve risks and uncertainties, including statements as to:

· our future operating results;

· our business prospects and the prospects of our portfolio companies;

· the impact of investments that we expect to make;

· our contractual arrangements and relationships with third parties;

· the dependence of our future success on the general economy and its impact on the industries in which we invest;

· the ability of our portfolio companies to achieve their objectives;

· our expected financings and investments;

· our regulatory structure and tax treatment, including our ability to operate as a business development company and a regulated investment company;

· the adequacy of our cash resources and working capital;

· the timing of cash flows, if any, from the operations of our portfolio companies; and

· the ability of our investment adviser to locate suitable investments for us and to monitor and effectively administer our investments.

For a discussion of factors that could cause our actual results to differ from forward-looking statements contained in this Annual Report, please see the discussion under Part I, Item 1A “Risk Factors”. You should not place undue reliance on these forward-looking statements. The forward-looking statements made in this Annual Report relate only to events as of the date on which the statements are made. We undertake no obligation to update any forward-looking statement to reflect events or circumstances occurring after the date of this Annual Report.

General

We are a specialty finance company that invests primarily in leveraged loans and mezzanine debt issued by private U.S. middle-market companies, which we define as companies having annual EBITDA (earnings before interest, taxes, depreciation and amortization) of $5 million and $50 million, both through direct lending and through participation in loan syndicates. Our investment objective is to generate current income and, to a lesser extent, capital appreciation from our investments. We are externally managed and advised by Saratoga Investment Advisors, LLC, a New York-based investment firm affiliated with Saratoga Partners, a middle market private equity investment firm.

Our portfolio is comprised primarily of investments in leveraged loans (both first and second lien term loans) issued by middle market companies. Term loans are loans that do not allow the borrowers to repay all or a portion of the loans prior to maturity and then re-borrow such repaid amounts under the loan again. Leveraged loans are generally senior debt instruments that rank ahead of subordinated debt of the portfolio company. Leveraged loans also have the benefit of security interests on the assets of the portfolio company, which may rank ahead of, or be junior to, other security interests. We also purchase mezzanine debt and make equity investments in middle market companies. Mezzanine debt is typically unsecured and subordinated to senior debt of the portfolio company.

While our primary focus is to generate current income and capital appreciation from our debt and equity investments in middle market companies, we may invest up to 30.0% of the portfolio in opportunistic investments in order to seek to enhance returns to stockholders. Such investments may include investments in distressed debt, including securities of companies in bankruptcy, foreign debt, private equity, securities of public companies that are not thinly traded and structured finance vehicles such as collateralized loan obligation funds.

As of February 28, 2013, we had total assets of $174.4 million and investments in 28 portfolio companies and an additional investment in the subordinated notes in one collateralized loan obligation fund (“Saratoga CLO”) with a fair value of $25.5 million. The overall portfolio composition as of February 28, 2013 consisted of 54.0% of first lien term loans, 6.2% of second lien term loans, 15.0% of senior secured notes, 3.1% of unsecured notes, 16.5% of subordinated notes of Saratoga CLO and 5.2% of common equity. The weighted average yield on all of our debt investments, including our investment in the subordinated notes in Saratoga CLO, as of February 28, 2013, was approximately 14.0%. Approximately 90% of our first lien debt investments are fully collateralized by the portfolio company having an enterprise value or an investment having an asset coverage equal to or greater than the principal amount of the related debt investment. Our investment in the subordinated notes of Saratoga CLO represents a first loss position in a portfolio that, at February 28, 2013, was composed of $383.3 million in aggregate principal amount of predominantly senior secured first lien term loans. A first loss position means that we will suffer the first economic losses if losses are incurred on loans held by the Saratoga CLO. This investment is subject to unique risks. See Part I, Item 1A. “Risk Factors—Our investment in Saratoga CLO constitutes a leveraged investment in a portfolio of predominantly senior secured first lien term loans and is subject to additional risks and volatility.”

We are an externally managed, closed-end, non-diversified management investment company that has elected to be regulated as a business development company (“BDC”) under the Investment Company Act of 1940 (“1940 Act”). As a BDC, we are required to comply with various regulatory requirements, including limitations on our use of debt. We finance our investments through borrowings. However, as a BDC, we are only generally allowed to borrow amounts such that our asset coverage, as defined in the 1940 Act, equals at least 200.0% after such borrowing. Pursuant to the 200.0% asset coverage ratio limitation, we are permitted to borrow one dollar for every dollar we have in assets less all liabilities and indebtedness not represented by debt securities issued by us or loans obtained by us.

We have elected to be treated for U.S. federal income tax purposes as a regulated investment company (“RIC”), under Subchapter M of the Internal Revenue Code of 1986 (the “Code”). As a RIC, we generally will not have to pay corporate-level federal income taxes on any net ordinary income or capital gains that we distribute to our stockholders if we meet certain source-of-income, distribution and asset diversification requirements.

In addition, we have a wholly-owned subsidiary that is licensed as a small business investment company (“SBIC”) and regulated by the Small Business Administration (“SBA”). See “Item 1. Business—Regulation—Small Business Investment Company Regulations.” The SBIC license allows us, through our wholly-owned subsidiary, to issue SBA-guaranteed debentures. We received exemptive relief from the Securities and Exchange Commission (“SEC”) to permit us to exclude the debt of our SBIC subsidiary guaranteed by the SBA from the 200.0% asset coverage ratio we are required to maintain under the 1940 Act. This allows us increased flexibility under the 200.0% asset coverage test by permitting us to borrow up to $150.0 million more than we would otherwise be able to absent the receipt of this exemptive relief.

Corporate History and Information

We commenced operations on March 23, 2007 as GSC Investment Corp. and completed an initial public offering (“IPO”) of shares of our common stock on March 28, 2007. From the date we commenced operations until July 30, 2010, we were managed and advised by GSCP (NJ), L.P., an entity affiliated with GSC Group, Inc. In connection with the consummation of a recapitalization

transaction on July 30, 2010, we engaged Saratoga Investment Advisors to replace GSCP (NJ), L.P. as our investment adviser and changed our name to Saratoga Investment Corp.

The recapitalization transaction consisted of (i) the private sale of 986,842 shares of our common stock for $15.0 million in aggregate purchase price to Saratoga Investment Advisors and certain of its affiliates and (ii) the entry into a $40.0 million senior secured revolving credit facility with Madison Capital Funding LLC (the “Credit Facility”). We used the net proceeds from the private sale of shares of our common stock and a portion of the funds available to us under the secured revolving credit facility with Madison Capital Funding LLC to pay the full amount of principal and accrued interest, including default interest, outstanding under our revolving securitized credit facility with Deutsche Bank AG, New York Branch. Specifically, in July 2009, we had exceeded permissible borrowing limits under the revolving securitized credit facility with Deutsche Bank, which resulted in an event of default under the revolving securitized credit facility. As a result of the event of default, Deutsche Bank had the right to accelerate repayment of the outstanding indebtedness under the revolving securitized credit facility and to foreclose and liquidate the collateral pledged under the revolving securitized credit facility. The revolving securitized credit facility with Deutsche Bank was terminated in connection with our payment of all amounts outstanding thereunder on July 30, 2010. In January 2011, we registered for public resale by Saratoga Investment Advisors and certain of its affiliates the 986,842 shares of our common stock issued to them in the recapitalization.

On March 28, 2012, our wholly-owned subsidiary, Saratoga Investment Corp. SBIC, LP, received an SBIC license from the SBA.

Our corporate offices are located at 535 Madison Avenue, New York, New York 10022. Our telephone number is (212) 906-7800. We maintain a website on the Internet at www.saratogainvestmentcorp.com. Information contained on our website is not incorporated by reference into this Annual Report, and you should not consider that information to be part of this Annual Report.

Saratoga Investment Advisors

General

Our investment adviser was formed in 2010 as a Delaware limited liability company and became our investment adviser in July 2010. Our investment adviser is led by five principals, Christian L. Oberbeck, Michael J. Grisius, Richard A. Petrocelli, Thomas V. Inglesby, and Charles G. Phillips, with 25, 23,15, 26 and 16 years of experience in leveraged finance, respectively. Our investment adviser is affiliated with Saratoga Partners, a middle market private equity investment firm. Saratoga Partners was established in 1984 to be the middle market private investment arm of Dillon Read & Co. Inc. and has been independent of Dillon Read since 1998. Saratoga Partners has a 27-year history of private investments in middle market companies and focuses on public and private equity, preferred stock, and senior and mezzanine debt investments.

Our Relationship with Saratoga Investment Advisors

We utilize the personnel, infrastructure, relationships and experience of Saratoga Investment Advisors to enhance the growth of our business. We currently have no employees and each of our executive officers is also an officer of Saratoga Investment Advisors.

We have entered into an investment advisory and management agreement with Saratoga Investment Advisors. The initial term of the investment advisory and management agreement was for two years from its effective date of July 30, 2010, with automatic, one-year renewals, subject to approval by our board of directors, a majority of whom must be our independent directors. On July 9, 2012, our board of directors approved the renewal of the investment advisory and management agreement for an additional one-year term. Pursuant to the investment advisory and management agreement, Saratoga Investment Advisors implements our business strategy on a day-to-day basis and performs certain services for us under the direction of our board of directors. Saratoga Investment Advisors is responsible for, among other duties, performing all of our day-to-day functions, determining investment criteria, sourcing, analyzing and executing investments, asset sales, financings and performing asset management duties.

Saratoga Investment Advisors has formed an investment committee to advise and consult with its senior management team with respect to our investment policies, investment portfolio holdings, financing and leveraging strategies and investment guidelines. We believe that the collective experience of the investment committee members across a variety of fixed income asset classes will benefit us. The investment committee must unanimously approve all investments in excess of $1.0 million made by us. In addition, all sales of our investments must be approved by four out of five investment committee members. The current members of the investment committee are Messrs. Oberbeck, Grisius, Petrocelli, Inglesby, and Phillips.

We pay Saratoga Investment Advisors a fee for investment advisory and management services consisting of two components—a base management fee and an incentive fee. The base management fee is calculated at an annual rate of 1.75% of our gross assets which includes assets purchased with borrowed funds but excludes cash and cash equivalents. As a result, Saratoga

Investment Advisors will benefit as we incur debt or use leverage to purchase assets. Our board of directors will monitor the conflicts presented by this compensation structure by approving the amount of leverage that we may incur.

In addition to the base management fee, we pay Saratoga Investment Advisors an incentive fee which consists of two parts. First, we pay Saratoga Investment Advisors an incentive fee with respect to our pre-incentive fee net investment income in each calendar quarter as follows:

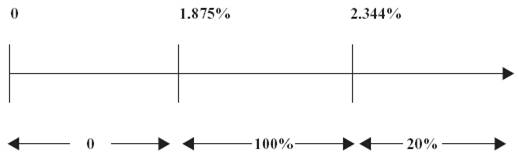

· no incentive fee in any calendar quarter in which our pre-incentive fee income does not exceed a fixed “hurdle rate” of 1.875% per quarter (7.5% annualized); and

· 100.0% of our pre-incentive fee net investment income with respect to that portion of such pre-incentive fee net investment income, if any, that exceeds the hurdle rate but is less than or equal to 2.344% in any fiscal quarter (9.376% annualized) is payable to the investment adviser. We refer to this portion of our pre-incentive fee net investment income (which exceeds the hurdle rate but is less than or equal to 2.344%) as the “catch-up.” The “catch-up” provision is intended to provide our investment adviser with an incentive fee of 20.0% on all of our pre-incentive fee net investment income as if a hurdle rate did not apply when our pre-incentive fee net investment income exceeds 2.344% in any fiscal quarter. Notwithstanding the foregoing, with respect to any period ending on or prior to December 31, 2010, our investment adviser was only entitled to 20.0% of the amount of our pre-incentive fee net investment income, if any, that exceeded 1.875% in any fiscal quarter (7.5% annualized) without any catch-up provision; and

· 20.0% of the amount of our pre-incentive fee net investment income, if any, that exceeds 2.344% in any fiscal quarter (9.376% annualized) is payable to the investment adviser (once the hurdle is reached and the catch-up is achieved, 20.0% of all pre-incentive fee net investment income thereafter is allocated to the investment adviser).

Pre-incentive fee net investment income means interest income, dividend income and other income (including any other fees, such as commitment, origination, structuring, diligence, managerial and consulting fees or other fees that we receive from portfolio companies) earned during the calendar quarter, minus our operating expenses for the quarter.

The second part of the incentive fee is determined and payable in arrears as of the end of each fiscal year (or upon termination of the investment advisory and management agreement) and equals 20.0% of our “incentive fee capital gains,” which equals our realized capital gains on a cumulative basis from May 31, 2010 through the end of the year, if any, computed net of all realized capital losses and unrealized capital depreciation on a cumulative basis, less the aggregate amount of any previously paid capital gain incentive fee. Importantly, the capital gains portion of the incentive fee is based on realized gains and realized and unrealized losses from May 31, 2010. Therefore, realized and unrealized losses incurred prior to such time will not be taken into account when calculating the capital gains portion of the incentive fee, and Saratoga Investment Advisors will be entitled to 20.0% of incentive fee capital gains that arise after May 31, 2010. In addition, for the purpose of the “incentive fee capital gains” calculations, the cost basis for computing realized gains and losses on investments held by us as of May 31, 2010 will equal the fair value of such investments as of such date.

We have also entered into a separate administration agreement with Saratoga Investment Advisors pursuant to which Saratoga Investment Advisors furnishes us with office facilities, equipment and clerical, bookkeeping and record keeping services. The administration agreement has an initial term of two years from its effective date of July 30, 2010, with automatic one-year renewals, subject to approval by our board of directors, a majority of whom must be our independent directors. On July 9, 2012, our board of directors approved the renewal of the Administration Agreement for an additional one-year term and determined to maintain the cap on the payment or reimbursement of expenses by us thereunder to $1.0 million for the additional one-year term. Under the administration agreement, Saratoga Investment Advisors also performs, or oversees the performance of our required administrative services, which include, among other things, being responsible for the financial records which we are required to maintain, preparing reports for our stockholders and reports required to be filed with the SEC. Payments under the administration agreement will be equal to an amount based upon the allocable portion of Saratoga Investment Advisors’ overhead in performing its obligations under the administration agreement, including rent and the allocable portion of the cost of our officers and their respective staffs relating to the performance of services under the administration agreement.

Investments

Our portfolio is comprised primarily of investments in leveraged loans (both first and second lien term loans) issued by middle market companies. Investments in middle market companies are generally less liquid than equivalent investments in companies with larger capitalizations. These investments are sourced in both the primary and secondary markets through a network of relationships with commercial and investment banks, commercial finance companies and financial sponsors. The leveraged loans that we purchase are generally used to finance buyouts, acquisitions, growth, recapitalizations and other types of transactions.

Leveraged loans are generally senior debt instruments that rank ahead of subordinated debt of the portfolio company. Leveraged loans also have the benefit of security interests on the assets of the portfolio company, which may rank ahead of, or be junior to, other security interests. For a discussion risks pertaining to our secured investments, see Part I, Item 1A. “Risk Factors—Our investments may be risky, and you could lose all or part of our investment.”

As part of our long-term strategy, we also purchase mezzanine debt and make equity investments in middle market companies. Mezzanine debt is typically unsecured and subordinated to senior debt of the portfolio company. See Part I, Item 1A. “Risk Factors—If we make unsecured debt investments, we may lack adequate protection in the event our portfolio companies become distressed or insolvent and will likely experience a lower recovery than more senior debtholders in the event our portfolio companies defaults on their indebtedness.”

Substantially all of the debt investments held in our portfolio hold a non-investment grade rating by one or more rating agencies or, if not rated, would be rated below investment grade if rated, which are often referred to as “junk.” As of February 28, 2013, 47.9% of our debt portfolio at fair value consisted of debt securities for which issuers were not required to make principal payments until the maturity of such debt securities, which could result in a substantial loss to us if such issuers are unable to refinance or repay their debt at maturity. In addition, 56.1% of our debt investments at February 28, 2013, had variable interest rates that reset periodically based on benchmarks such as LIBOR and the prime rate. As a result, significant increases in such benchmarks in the future may make it more difficult for these borrowers to service their obligations under the debt investments that we hold.

As a BDC, we are required to comply with certain regulatory requirements. For instance, we have to invest at least 70.0% of our total assets in “qualifying assets,” including securities of U.S. operating companies whose securities are not listed on a national securities exchange (i.e., New York Stock Exchange, NYSE MKT and The NASDAQ Stock Market), U.S. operating companies with listed securities that have market capitalizations of less than $250.0 million, cash, cash equivalents, U.S. government securities and high-quality debt investments that mature in one year or less.

While our primary focus is to generate current income and capital appreciation from our debt and equity investments in middle market companies, we may invest up to 30.0% of the portfolio in opportunistic investments in order to seek to enhance returns to stockholders. Such investments may include investments in distressed debt, private equity, securities of public companies that are not thinly traded and structured finance vehicles such as collateralized loan obligation funds.

Leveraged loans

Our leveraged loan portfolio is comprised primarily of first lien and second lien term loans. First lien term loans are secured by a first priority perfected security interest on all or substantially all of the assets of the borrower and typically include a first priority pledge of the capital stock of the borrower. First lien term loans hold a first priority with regard to right of payment. Generally, first lien term loans offer floating rate interest payments, have a stated maturity of five to seven years, and have a fixed amortization schedule. First lien term loans generally have restrictive financial and negative covenants. Second lien term loans are secured by a second priority perfected security interest on all or substantially all of the assets of the borrower and typically include a second priority pledge of the capital stock of the borrower. Second lien term loans hold a second priority with regard to right of payment. Second lien term loans offer either floating rate or fixed rate interest payments, generally have a stated maturity of five to eight years, and may or may not have a fixed amortization schedule. Second lien term loans that do not have fixed amortization schedules require payment of the principal amount of the loan upon the maturity date of the loan. Second lien term loans have less restrictive financial and negative covenants than those that govern first lien term loans.

Mezzanine debt

Mezzanine debt usually ranks subordinate in priority of payment to senior debt and is often unsecured. However, mezzanine debt ranks senior to common and preferred equity in a borrowers’ capital structure. Mezzanine debt typically has fixed rate interest payments and a stated maturity of six to eight years and does not have fixed amortization schedules.

In some cases, our debt investments may provide for a portion of the interest payable to be paid-in-kind interest (“PIK”). To the extent interest is paid-in-kind, it will be payable through the increase of the principal amount of the obligation by the amount of interest due on the then-outstanding aggregate principal amount of such obligation.

Equity Investments

Equity investments may consist of preferred equity that is expected to pay dividends on a current basis or preferred equity that does not pay current dividends. Preferred equity generally has a preference over common equity as to distributions on liquidation and dividends. In some cases, we may acquire common equity. In general, our equity investments are not control-oriented investments and we expect that in many cases we will acquire equity securities as part of a group of private equity investors in which we are not the lead investor.

Opportunistic Investments

Opportunistic investments may include investments in distressed debt, which may include securities of companies in bankruptcy, debt and equity securities of public companies that are not thinly traded, emerging market debt, structured finance vehicles such as collateralized loan obligation funds and debt of middle market companies located outside the United States.

In January 2008, we purchased for $30.0 million all of the outstanding subordinated notes of GSC Investment Corp. CLO 2007 LTD., (“Saratoga CLO”), a collateralized loan obligation fund managed by us that invests primarily in leveraged loans. As of February 28, 2013, the Saratoga CLO portfolio consisted of $383.3 million in aggregate principal amount of primarily senior secured first lien term loans in 155 obligors with an average obligor exposure of $2.5 million and $28.8 million in uninvested cash. The weighted average maturity of the portfolio is 4.4 years.

Prospective portfolio company characteristics

Our investment adviser generally selects portfolio companies with one or more of the following characteristics:

· a history of generating stable earnings and strong free cash flow;

· well-constructed balance sheets, including an established tangible liquidation value;

· reasonable debt-to-cash flow multiples;

· industry leadership with competitive advantages and sustainable market shares in attractive sectors; and

· capital structures that provide appropriate terms and reasonable covenants.

Investment selection

In managing us, Saratoga Investment Advisors employs the same investment philosophy and portfolio management methodologies used by Saratoga Partners. Through this investment selection process, based on quantitative and qualitative analysis, Saratoga Investment Advisors seeks to identify portfolio companies with superior fundamental risk-reward profiles and strong, defensible business franchises with the goal of minimizing principal losses while maximizing risk-adjusted returns. Saratoga Investment Advisors’ investment process emphasizes the following:

· bottoms-up, company-specific research and analysis;

· capital preservation, low volatility and minimization of downside risk; and

· investing with experienced management teams that hold meaningful equity ownership in their businesses.

Our investment adviser’s investment process generally includes the following steps:

· Initial screening. A brief analysis identifies the investment opportunity and reviews the merits of the transaction. The initial screening memorandum provides a brief description of the company, its industry, competitive position, capital structure, financials, equity sponsor and deal economics. If the deal is determined to be attractive by the senior members of the deal team, the opportunity is fully analyzed.

· Full analysis. A full analysis includes:

· Business and Industry analysis—a review of the company’s business position, competitive dynamics within its industry, cost and growth drivers and technological and geographic factors. Business and industry research often includes meetings with industry experts, consultants, other investors, customers and competitors.

· Company analysis—a review of the company’s historical financial performance, future projections, cash flow characteristics, balance sheet strength, liquidation value, legal, financial and accounting risks, contingent liabilities, market share analysis and growth prospects.

· Structural/security analysis—a thorough legal document analysis including but not limited to an assessment of financial and negative covenants, events of default, enforceability of liens and voting rights.

· Approval of the investment committee. The investment is then presented to the investment committee for approval. The investment committee must unanimously approve all investments in excess of $1 million made by us. In addition, all sales of our investments must be approved by four out of five investment committee members. The members of our investment committee are Christian L. Oberbeck, Michael J. Grisius, Richard A. Petrocelli, Thomas V. Inglesby, and Charles G. Phillips.

Investment structure

In general, our investment adviser intends to select investments with financial covenants and terms that reduce leverage over time, thereby enhancing credit quality. These methods include:

· maintenance leverage covenants requiring a decreasing ratio of debt to cash flow;

· maintenance cash flow covenants requiring an increasing ratio of cash flow to the sum of interest expense and capital expenditures; and

· debt incurrence prohibitions, limiting a company’s ability to re-lever.

In addition, limitations on asset sales and capital expenditures should prevent a company from changing the nature of its business or capitalization without our consent.

Our investment adviser seeks, where appropriate, to limit the downside potential of our investments by:

· requiring a total return on our investments (including both interest and potential equity appreciation) that compensates us for credit risk;

· requiring companies to use a portion of their excess cash flow to repay debt;

· selecting investments with covenants that incorporate call protection as part of the investment structure; and

· selecting investments with affirmative and negative covenants, default penalties, lien protection, change of control provisions and board rights, including either observation or participation rights.

Valuation process

We carry our investments at fair value, as approved in good faith using written policies and procedures adopted by our board of directors. Investments for which market quotations are readily available are recorded in our financial statements at such market quotations subject to any decision by our board of directors to approve a fair value determination to reflect significant events affecting the value of these investments. We value investments for which market quotations are not readily available at fair value as approved in good faith by our board of directors based on input from Saratoga Investment Advisors, our audit committee and, if our board or audit committee so request, a third party independent valuation firm. Determinations of fair value may involve subjective judgments and estimates. The types of factors that may be considered in determining the fair value of our investments include the nature and realizable value of any collateral, the portfolio company’s ability to make payments, the markets in which the portfolio company does business, market yield trend analysis, comparison to publicly traded companies, discounted cash flow and other relevant factors.

Our investment in the subordinated notes of Saratoga CLO is carried at fair value, which is based on a discounted cash flow model that utilizes prepayment, re-investment and loss assumptions based on historical experience and projected performance, economic factors, the characteristics of the underlying cash flow, and comparable yields for similar collateralized loan obligation fund subordinated notes or equity, when available. Specifically, we use Intex cash flow models, or an appropriate substitute, to form the basis for Saratoga CLO’s valuation. The models use a set of assumptions including projected default rates, recovery rates, reinvestment rate and prepayment rates in order to arrive at estimated cash flows. The assumptions are based on available market data and projections provided by third parties as well as management estimates. We use the output from the Intex models (i.e., the estimated cash flows from our investment in Saratoga CLO) to perform a discounted cash flows analysis on expected future cash flows from our investment in Saratoga CLO to determine a valuation for the subordinated notes of Saratoga CLO held by us.

We undertake a multi-step valuation process each quarter when valuing investments for which market quotations are not readily available, as described below:

· each investment is initially valued by the responsible investment professionals of Saratoga Investment Advisors and preliminary valuation conclusions are documented and discussed with our senior management; and

· an independent valuation firm engaged by our board of directors independently values at least one quarter of our investments each quarter so that the valuation of each investment for which market quotes are not readily available is independently valued by an independent valuation firm at least annually.

In addition, all our investments are subject to the following valuation process:

· the audit committee of our board of directors reviews each preliminary valuation and our investment adviser and independent valuation firm (if applicable) will supplement the preliminary valuation to reflect any comments provided by the audit committee; and

· our board of directors discusses the valuations and approves the fair value of each investment in good faith based on the input of our investment adviser, independent valuation firm (if applicable) and audit committee.

Because such valuations, and particularly valuations of private investments and private companies, are inherently uncertain, they may fluctuate over short periods of time and may be based on estimates. The determination of fair value may differ materially from the values that would have been used if a ready market for these investments existed. Our net asset value could be materially affected if the determinations regarding the fair value of our investments were materially higher or lower than the values that we ultimately realize upon the disposal of such investments.

Ongoing relationships with and monitoring of portfolio companies

Saratoga Investment Advisors will closely monitor each investment we make and, when appropriate, will conduct a regular dialogue with both the management team and other debtholders and seek specifically tailored financial reporting. In addition, in certain circumstances, senior investment professionals of Saratoga Investment Advisors may take board seats or board observation seats.

Distributions

Our distributions, if any, will be determined by our board of directors and paid out of assets legally available for distribution. Any such distributions generally will be taxable to our stockholders, including to those stockholders who receive additional shares of our common stock pursuant to our dividend reinvestment plan. Prior to January 2009, we paid quarterly dividends to our stockholders. However, in January 2009, we suspended the practice of paying quarterly dividends to our stockholders and have only paid four dividend distributions (December 2012, 2011, 2010 and 2009) to our stockholders since such time.

In order to maintain our qualification as a RIC, we must for each fiscal year distribute an amount equal to at least 90.0% of our ordinary net taxable income and realized net short-term capital gains in excess of realized net long-term capital losses, if any, reduced by deductible expenses. In addition, we will be subject to federal excise taxes to the extent we do not distribute during the calendar year at least (1) 98.0% of our ordinary income for the calendar year, (2) 98.2% of our capital gains in excess of capital losses for the one year period ending on October 31 of the calendar year and (3) any ordinary income and net capital gains for preceding years that were not distributed during such years and on which we paid no federal income tax. For the 2012 calendar year, we made distributions sufficient such that we did not incur any federal excise taxes. We may elect to withhold from distribution a portion of our ordinary income for the 2013 calendar year and/or portion of the capital gains in excess of capital losses realized during the one year period ending October 31, 2013, if any, and, if we do so, we would expect to incur federal excise taxes as a result.

We maintain an “opt out” dividend reinvestment plan for our common stockholders. As a result, if we declare a dividend, then stockholders’ cash dividends will be automatically reinvested in additional shares of our common stock, unless they specifically “opt out” of the dividend reinvestment plan so as to receive cash dividends.

We may distribute taxable dividends that are payable in cash or shares of our common stock at the election of each stockholder. Under certain applicable provisions of the Code and the Treasury regulations, distributions payable in cash or in shares of stock at the election of stockholders are treated as taxable dividends. The Internal Revenue Service has issued private rulings indicating that this rule will apply even where the total amount of cash that may be distributed is limited to no more than 20.0% of the total distribution. Under these rulings, if too many stockholders elect to receive their distributions in cash, each such stockholder would receive a pro rata share of the total cash to be distributed and would receive the remainder of their distribution in shares of stock. If we decide to make any distributions consistent with these rulings that are payable in part in our stock, taxable stockholders receiving such dividends will be required to include the full amount of the dividend (whether received in cash, our stock, or a combination thereof) as ordinary income (or as long-term capital gain to the extent such distribution is properly reported as a capital gain dividend) to the extent of our current and accumulated earnings and profits for United States federal income tax purposes. As a result, a U.S. stockholder may be required to pay tax with respect to such dividends in excess of any cash received. If a U.S. stockholder sells the stock it receives as a dividend in order to pay this tax, the sales proceeds may be less than the amount included in income with respect to the dividend, depending on the market price of our stock at the time of the sale. Furthermore, with respect to non-U.S. stockholders, we may be required to withhold U.S. tax with respect to such dividends, including in respect of all or a portion of such dividend that is payable in stock. In addition, if a significant number of our stockholders determine to sell shares of our stock in order to pay taxes owed on dividends, it may put downward pressure on the trading price of our stock.

Competition

Our primary competitors in providing financing to private middle market companies include public and private investment funds (including private equity funds, mezzanine funds, BDCs and SBICs), commercial and investment banks and commercial financing companies. Many of our competitors are substantially larger and have considerably greater financial and marketing resources than us. For example, some competitors may have access to funding sources that are not available to us. In addition, some of our competitors may have higher risk tolerances or different risk assessments, which may allow them to consider a wider variety of investments. Furthermore, many of our competitors are not subject to the regulatory restrictions that the 1940 Act imposes on us as a BDC. For additional information concerning the competitive risks we face, please see Part I, Item 1A, “Risk Factors—We operate in a highly competitive market for investment opportunities.”

Staffing

We do not currently have any employees and do not expect to have any employees in the future. Services necessary for our business are provided by individuals who are employees of Saratoga Investment Advisors, pursuant to the terms of the investment advisory and management agreement and the administration agreement. For a discussion of the investment advisory and management agreement, see “Business—Investment Advisory and Management Agreement” below. We reimburse Saratoga Investment Advisors for our allocable portion of expenses incurred by it in performing its obligations under the administration agreement, including rent and our allocable portion of the cost of our officers and their respective staffs, subject to certain limitations. For a discussion of the administration agreement, see “Business—Administration Agreement” below.

Investment Advisory and Management Agreement

Saratoga Investment Advisors serves as our investment adviser. Our investment adviser was formed in 2010 as a Delaware limited liability company and became our investment advisor in July 2010. Subject to the overall supervision of our board of directors, Saratoga Investment Advisors manages our day-to-day operations and provides investment advisory and management services to us. Under the terms of an investment advisory and management agreement, Saratoga Investment Advisors:

· determines the composition of our portfolio, the nature and timing of the changes to our portfolio and the manner of implementing such changes;

· identifies, evaluates and negotiates the structure of the investments we make (including performing due diligence on our prospective portfolio companies);

· closes and monitors the investments we make; and

· determines the securities and other assets that we purchase, retain or sell.

Saratoga Investment Advisors services under the investment advisory and management agreement are not exclusive, and it is free to furnish similar services to other entities.

Management Fee and Incentive Fee

Pursuant to the investment advisory and management agreement with Saratoga Investment Advisors, we pay Saratoga Investment Advisors a fee for investment advisory and management services consisting of two components—a base management fee and an incentive fee.

The base management fee is paid quarterly in arrears, and equals 1.75% per annum of our gross assets (other than cash or cash equivalents but including assets purchased with borrowed funds) and calculated at the end of each fiscal quarter based on the average value of our gross assets (other than cash or cash equivalents but including assets purchased with borrowed funds) as of the end of such fiscal quarter and the end of the immediate prior fiscal quarter. Base management fees for any partial month or quarter are appropriately pro-rated.

The incentive fee has the following two parts:

The first part is calculated and payable quarterly in arrears based on our pre-incentive fee net investment income for the immediately preceding fiscal quarter. Pre-incentive fee net investment income means interest income, dividend income and any other income (including any other fees such as commitment, origination, structuring, diligence, managerial and consulting fees or other fees that we receive from portfolio companies) accrued during the fiscal quarter, minus our operating expenses for the quarter (including the base management fee, expenses payable under the administration agreement, and any interest expense and dividends paid on any issued and outstanding preferred stock or debt security, but excluding the incentive fee). Pre-incentive fee net investment income includes, in the case of investments with a deferred interest feature (such as market discount, debt instruments with payment-in-kind interest, preferred stock with payment-in-kind dividends and zero coupon securities), accrued income that we have not yet received in cash. Pre-incentive fee net investment income does not include any realized capital gains, realized capital losses or unrealized capital appreciation or depreciation. Pre-incentive fee net investment income, expressed as a rate of return on the value of our net assets (defined as total assets less liabilities) at the end of the immediately preceding fiscal quarter, is compared to a “hurdle rate” of 1.875% per quarter (7.5% annualized), subject to a “catch up” provision. The base management fee is calculated prior to giving effect to the payment of any incentive fees.

We pay Saratoga Investment Advisors an incentive fee with respect to our pre-incentive fee net investment income in each fiscal quarter as follows: (A) no incentive fee in any fiscal quarter in which our pre-incentive fee net investment income does not exceed the hurdle rate; (B) 100.0% of our pre-incentive fee net investment income with respect to that portion of such pre-incentive fee net investment income, if any, that exceeds the hurdle rate but is less than or equal to 2.344% in any fiscal quarter (9.376% annualized) is payable to Saratoga Investment Advisors; and (C) 20.0% of the amount of our pre-incentive fee net investment income, if any, that exceeds 2.344% in any fiscal quarter (9.376% annualized). We refer to the amount specified in clause (B) as the “catch-up.” The “catch-up” provision is intended to provide Saratoga Investment Advisors with an incentive fee of 20.0% on all of our pre-incentive fee net investment income as if a hurdle rate did not apply when our pre-incentive fee net investment income exceeds 2.344% in any fiscal quarter. Notwithstanding the foregoing, with respect to any period ending on or prior to December 31, 2010, Saratoga Investment Advisors was only entitled to 20.0% of the amount of our pre-incentive fee net investment income, if any, that exceeded 1.875% in any fiscal quarter (7.5% annualized) without any catch-up provision. These calculations are appropriately pro-rated when such calculations are applicable for any period of less than three months.

The following is a graphical representation of the calculation of the income- related portion of the incentive fee subsequent to any period ending after December 31, 2010:

Quarterly Incentive Fee Based on “Pre-Incentive Fee Net Investment Income”

Pre-Incentive Fee Net Investment Income

(expressed as a percentage of the value of net assets)

Percentage of Pre-Incentive Fee Net Investment

Income allocated to income-related portion of incentive fee

The second part of the incentive fee, the capital gains fee, is determined and payable in arrears as of the end of each fiscal year (or, upon termination of the investment advisory and management agreement), and is calculated at the end of each applicable year by subtracting (1) the sum of our cumulative aggregate realized capital losses and aggregate unrealized capital depreciation from (2) our cumulative aggregate realized capital gains, in each case calculated from May 31, 2010. If such amount is positive at the end of such year, then the capital gains fee for such year is equal to 20.0% of such amount, less the cumulative aggregate amount of capital gains fees paid in all prior years. If such amount is negative, then there is no capital gains fee for such year.

Under the investment advisory and management agreement, the capital gains portion of the incentive fee is based on realized gains and realized and unrealized losses from May 31, 2010. Therefore, realized and unrealized losses incurred prior to such time will not be taken into account when calculating the capital gains portion of the incentive fee, and Saratoga Investment Advisors will be entitled to 20.0% of net capital gains that arise after May 31, 2010. In addition, the cost basis for computing our realized gains and losses on investments held by us as of May 31, 2010 equals the fair value of such investments as of such date.

Examples of Quarterly Incentive Fee Calculation

Example 1: Income Related Portion of Incentive Fee(1):

Assumptions

· Hurdle rate(2) = 1.875%

· Management fee(3) = 0.4375%

· Other expenses (legal, accounting, custodian, transfer agent, etc.)(4) = 0.33%

Alternative 1

Additional Assumptions

· Investment income (including interest, dividends, fees, etc.) = 1.25%

· Pre-incentive fee net investment income (investment income-(management fee + other expenses)) = 0.4825%

Pre-incentive fee net investment income does not exceed hurdle rate, therefore there is no incentive fee.

Alternative 2

Additional Assumptions

· Investment income (including interest, dividends, fees, etc.) = 3.0%

· Pre-incentive fee net investment income (investment income-(management fee + other expenses)) = 2.2325%

Pre-incentive fee net investment income exceeds hurdle rate, but does not fully satisfy the “catch-up” provision, therefore the income related portion of the incentive fee is 0.3575%.

|

Incentive Fee |

= |

(100.0% × (pre-incentive fee net investment income-1.875%) |

|

|

= |

100.0% (2.2325%-1.875%) |

|

|

= |

100.0% (0.3575%) |

|

|

= |

0.3575% |

(1) The hypothetical amount of pre-incentive fee net investment income shown is based on a percentage of total net assets.

(2) Represents 7.5% annualized hurdle rate.

(3) Represents 1.75% annualized management fee. For the purposes of this example, we have assumed that we have not incurred any indebtedness and that we maintain no cash or cash equivalents.

(4) The “catch-up” provision is intended to provide our investment adviser with an incentive fee of 20.0% on all pre-incentive fee net investment income as if a hurdle rate did not apply when our net investment income exceeds 2.344% in any fiscal quarter.

Alternative 3

Additional Assumptions

· Investment income (including interest, dividends, fees, etc.) = 3.5%

· Pre-Incentive Fee Net Investment Income (investment income-(management fee + other expenses) = 2.7325%

Pre-incentive fee net investment income exceeds the hurdle rate, and fully satisfies the “catch-up” provision, therefore the income related portion of the incentive fee is 0.5467%.

|

Incentive fee |

= |

100.0% × pre-incentive fee net investment income (subject to “catch-up”)(4) |

|

Incentive fee |

= |

100.0% × “catch-up” + (20.0% × (Pre-incentive fee net investment income-2.344%)) |

|

Catch up |

= |

2.344%-1.875% |

|

|

= |

0.469% |

|

Incentive fee |

= |

(100.0% × 0.469%) + (20.0% × (2.7325%-2.344%)) |

|

|

= |

0.469% + (20.0% × 0.3885%) |

|

|

= |

0.469% + 0.0777% |

|

|

= |

0.5467% |

Example 2: Capital Gains Portion of Incentive Fee:

Alternative 1:

Assumptions(1)

· Year 1: $20.0 million investment made in Company A (“Investment A”), and $30.0 million investment made in Company B (“Investment B”)

· Year 2: Investment A is sold for $50.0 million and fair market value (“FMV”) of Investment B determined to be $32.0 million

· Year 3: FMV of Investment B determined to be $25.0 million

· Year 4: Investment B sold for $31.0 million

The capital gains portion of the incentive fee, if any, calculated under the cumulative method would be:

· Year 1: None

· Year 2: $6 million (20.0% multiplied by $30.0 million realized capital gains on sale of Investment A)

· Year 3: None; $5 million (20.0% multiplied by ($30.0 million realized cumulative capital gains less $5.0 million cumulative capital depreciation)) less $6.0 million (capital gains incentive fee paid in Year 2)

· Year 4: $200,000; $6.2 million (20.0% multiplied by $31.0 million cumulative realized capital gains) less $6.0 million (capital gains incentive fee paid in Year 2)

Alternative 2

Assumptions(1)

(1) The examples assume that Investment A and Investment B were acquired by us subsequent to May 31, 2010. If Investment A and B were acquired by us prior to May 31, 2010, then the cost basis for computing our realized gains and losses on such investments would equal the fair value of such investments as of May 31, 2010.

· Year 1: $20.0 million investment made in Company A (“Investment A”), $30.0 million investment made in Company B (“Investment B”) and $25.0 million investment made in Company C (“Investment C”)

· Year 2: Investment A sold for $50.0 million, FMV of Investment B determined to be $25.0 million and FMV of Investment C determined to be $25.0 million

· Year 3: FMV of Investment B determined to be $27.0 million and Investment C sold for $30.0 million

· Year 4: FMV of Investment B determined to be $35.0 million

· Year 5: Investment B sold for $20.0 million

The capital gains portion of the incentive fee, if any, calculated under the cumulative method would be:

· Year 1: None

· Year 2: $5.0 million (20.0% multiplied by $25.0 million ($30.0 million realized capital gains on Investment A less $5.0 million unrealized capital depreciation on Investment B))

· Year 3: $1.4 million ($6.4 million (20.0% multiplied by $32.0 million ($35.0 million cumulative realized capital gains less $3.0 million unrealized capital depreciation)) less $5.0 million (capital gains incentive fee paid in Year 2))

· Year 4: None

· Year 5: None ($5.0 million (20.0% multiplied by $25.0 million (cumulative realized capital gains of $35.0 million less realized capital losses of $10.0 million)) less $6.4 million (cumulative capital gains incentive fee paid in Year 2 and Year 3))

The investment advisory and management agreement with Saratoga Investment Advisors was approved by our board of directors at an in-person meeting of the directors, including a majority of our independent directors, and was approved by our stockholders at the special meeting of stockholders held on July 30, 2010. On July 9, 2012, our board of directors approved the renewal of the investment advisory and management agreement for an additional one-year term.

In approving this agreement, the directors considered, among other things, (i) the nature, extent and quality of the advisory and other services to be provided to us by Saratoga Investment Advisors; (ii) our investment performance and the investment performance of Saratoga Investment Advisors; (iii) the expected costs of the services to be provided by Saratoga Investment Advisors (including management fees, advisory fees and expense ratios) and the profits expected to be realized by Saratoga Investment Advisors; (iv) the limited potential for economies of scale in investment management associated with managing us; and (v) Saratoga Investment Advisors estimated pro forma profitability with respect to managing us.

Payment of our expenses

The investment advisory and management agreement provides that all investment professionals of Saratoga Investment Advisors and its staff, when and to the extent engaged in providing investment advisory services required to be provided by Saratoga Investment Advisors, and the compensation and routine overhead expenses of such personnel allocable to such services, will be provided and paid for by Saratoga Investment Advisors and not by us.

We bear all costs and expenses of our operations and transactions, including those relating to:

· our organization;

· calculating our net asset value (including the cost and expenses of any independent valuation firm);

· expenses incurred by Saratoga Investment Advisors payable to third parties, including agents, consultants or other advisors, in monitoring financial and legal affairs for us and in monitoring our investments and performing due diligence on our prospective portfolio companies;

· interest payable on debt, if any, incurred to finance our investments;

· offerings of our common stock and other securities;

· investment advisory and management fees;

· fees payable to third parties, including agents, consultants or other advisors, relating to, or associated with, evaluating and making investments;

· transfer agent and custodial fees;

· federal and state registration fees;

· all costs of registration and listing our common stock on any securities exchange;

· federal, state and local taxes;

· independent directors’ fees and expenses;

· costs of preparing and filing reports or other documents required by governmental bodies (including the SEC and the SBA);

· costs of any reports, proxy statements or other notices to common stockholders including printing costs;

· our fidelity bond, directors and officers errors and omissions liability insurance, and any other insurance premiums;

· direct costs and expenses of administration, including printing, mailing, long distance telephone, copying, secretarial and other staff, independent auditors and outside legal costs; and

· administration fees and all other expenses incurred by us or, if applicable, the administrator in connection with administering our business (including payments under the administration agreement based upon our allocable portion of the administrator’s overhead in performing its obligations under the administration agreement, including rent and the allocable portion of the cost of our officers and their respective staffs (including travel expenses)).

Duration and Termination

The investment advisory and management agreement will remain in effect continuously, unless terminated under the termination provisions of the agreement. The investment advisory and management agreement provides that it may be terminated at any time, without the payment of any penalty, upon 60 days written notice, by the vote of stockholders holding a majority of our outstanding voting securities, or by the vote of our directors or by Saratoga Investment Advisors.

The investment advisory and management agreement will, unless terminated as described above, continue in effect until July 30, 2013 and will continue in effect from year to year thereafter so long as it is approved at least annually by (i) the vote of the board of directors, or by the vote of stockholders holding a majority of our outstanding voting securities, and (ii) the vote of a majority of our directors who are not parties to the investment advisory and management agreement or “interested persons” (as such term is defined in Section 2(a)(19) of the 1940 Act) of any party to such agreement, in accordance with the requirements of the 1940 Act.

Indemnification

Under the investment advisory and management agreement, Saratoga Investment Advisors and certain of its affiliates are not liable to us for any action taken or omitted to be taken by Saratoga Investment Advisors in connection with the performance of any of its duties or obligations under the agreement or otherwise as an investment adviser to us, except to the extent specified in Section 36(b) of the 1940 Act concerning loss resulting from a breach of fiduciary duty (as the same is finally determined by judicial proceedings) with respect to the receipt of compensation for services and except to the extent such action or omission constitutes gross negligence, willful misfeasance, bad faith or reckless disregard of its duties and obligations under the agreement.

We also provide indemnification to Saratoga Investment Advisors and certain of its affiliates for damages, liabilities, costs and expenses incurred by them in or by reason of any pending, threatened or completed action, suit, investigation or other proceeding arising out of or otherwise based upon the performance of any of its duties or obligations under the agreement or otherwise as an investment adviser to us. However, we would not provide indemnification against any liability to us or our security holders to which Saratoga Investment Advisors or such affiliates would otherwise be subject by reason of willful misfeasance, bad faith or gross negligence in the performance of any such person’s duties or by reason of the reckless disregard of its duties and obligations under the agreement.

Organization of the Investment Adviser

Saratoga Investment Advisors is registered as an investment adviser under the Investment Advisers Act of 1940. The principal executive offices of Saratoga Investment Advisors are located at 535 Madison Avenue, New York, New York 10022.

Administration Agreement

Pursuant to a separate administration agreement, Saratoga Investment Advisors, who also serves as our administrator, furnishes us with office facilities, equipment and clerical, book-keeping and record keeping services. Under the administration agreement, our administrator also performs, or oversees the performance of, our required administrative services, which include, among other things, being responsible for the financial records which we are required to maintain, preparing reports for our stockholders and reports required to be filed with the SEC. In addition, our administrator assists us in determining and publishing our net asset value, oversees the preparation and filing of our tax returns and the printing and dissemination of reports to our stockholders, and generally oversees the payment of our expenses and the performance of administrative and professional services rendered to us by others. Payments under the administration agreement equal an amount based upon our allocable portion of our administrator’s overhead in performing its obligations under the administration agreement, including rent and our allocable portion of the cost of our officers and their respective staffs relating to the performance of services under this agreement (including travel expenses). Our allocable portion is based on the proportion that our total assets bears to the total assets administered or managed by our administrator. Under the administration agreement, our administrator also provides managerial assistance, on our behalf, to those portfolio companies who accept our offer of assistance. The administration agreement may be terminated by either party without penalty upon 60 days written notice to the other party. The amount payable by us under the administration agreement is currently capped at $1.0 million for each annual term of the agreement. On July 9, 2012, our board of directors approved the renewal of the administration agreement for an additional one-year term and determined to maintain the cap on the payment or reimbursement of expenses by us thereunder to $1.0 million for the additional one-year term.

Indemnification

Under the administration agreement, Saratoga Investment Advisors and certain of its affiliates are not liable to us for any action taken or omitted to be taken by Saratoga Investment Advisors in connection with the performance of any of its duties or obligations under the agreement.

We also provide indemnification to Saratoga Investment Advisors and certain of its affiliates for damages, liabilities, costs and expenses incurred by them in or by reason of any pending, threatened or completed action, suit, investigation or other proceeding arising out of or otherwise based upon the performance of any of its duties or obligations under the agreement or otherwise as an administrator to us. However, we do not provide indemnification against any liability to us or our security holders to which Saratoga Investment Advisors or such affiliates would otherwise be subject by reason of willful misfeasance, bad faith or gross negligence in the performance of any such person’s duties or by reason of the reckless disregard of its duties and obligations under the agreement.

License Agreement

We entered into a trademark license agreement with Saratoga Investment Advisors, pursuant to which Saratoga Investment Advisors grants us a non-exclusive, royalty-free license to use the name “Saratoga.” Under this agreement, we have a right to use the “Saratoga” name, for so long as Saratoga Investment Advisors or one of its affiliates remains our investment adviser. Other than with respect to this limited license, we have no legal right to the “Saratoga” name. Saratoga Investment Advisors has the right to terminate the license agreement if it is no longer acting as our investment adviser. In the event the investment advisory and management agreement is terminated, we would be required to change our name to eliminate the use of the name “Saratoga.”

Business Development Company Regulations

We have elected to be treated as a BDC under the 1940 Act. As with other companies regulated by the 1940 Act, a BDC must adhere to certain substantive regulatory requirements. The 1940 Act contains prohibitions and restrictions relating to transactions between BDCs and their affiliates (including any investment advisers or sub-advisers), principal underwriters and affiliates of those affiliates or underwriters, and requires that a majority of the directors be persons other than “interested persons,” as that term is defined in the 1940 Act. In addition, the 1940 Act provides that we may not change the nature of our business so as to cease to be, or to withdraw our election as, a BDC, unless approved by a majority of our outstanding voting securities. A majority of the outstanding voting securities of a company is defined under the 1940 Act as the lesser of: (i) 67.0% or more of such company’s stock present at a meeting if more than 50.0% of the outstanding stock of such company is present and represented by proxy or (ii) more than 50.0% of the outstanding stock of such company.

Qualifying assets

Under the 1940 Act, a BDC may not acquire any asset other than assets of the type listed in Section 55(a) of the 1940 Act, which are referred to as qualifying assets, unless, at the time the acquisition is made, qualifying assets represent at least 70.0% of the company’s total assets. The principal categories of qualifying assets relevant to our business are the following:

(1) Securities purchased in transactions not involving any public offering from the issuer of such securities, which issuer (subject to certain limited exceptions) is an eligible portfolio company, or from any person who is, or has been during the preceding 13 months, an affiliated person of an eligible portfolio company, or from any other person, subject to such rules as may be prescribed by the SEC. An eligible portfolio company is defined in the 1940 Act as any issuer which:

(a) is organized under the laws of, and has its principal place of business in, the United States;

(b) is not an investment company (other than a small business investment company wholly owned by the BDC) or a company that would be an investment company but for certain exclusions under the 1940 Act; and

(c) satisfies either of the following:

(i) does not have any class of securities listed on a national securities exchange;

(ii) has a class of securities listed on a national securities exchange but has an aggregate market value of outstanding voting and non-voting common equity of less than $250.0 million;

(iii) is controlled by a BDC or a group of companies including a BDC and the BDC has an affiliated person who is a director of the eligible portfolio company;

(iv) is a small and solvent company having total assets of not more than $4.0 million and capital and surplus of not less than $2.0 million; or

(v) meets such other criteria as may established by the SEC.

(2) Securities of any eligible portfolio company which we control.

(3) Securities purchased in a private transaction from a U.S. issuer that is not an investment company or from an affiliated person of the issuer, or in transactions incident thereto, if the issuer is in bankruptcy and subject to reorganization or if the issuer, immediately prior to the purchase of its securities was unable to meet its obligations as they came due without material assistance other than conventional lending or financing arrangements.

(4) Securities of an eligible portfolio company purchased from any person in a private transaction if there is no ready market for such securities and we already own at least 60.0% of the outstanding equity of the eligible portfolio company.

(5) Securities received in exchange for or distributed on or with respect to securities described in (1) through (4) above, or pursuant to the exercise of options, warrants or rights relating to such securities.

(6) Cash, cash equivalents, U.S. Government securities or high-quality debt securities maturing in one year or less from the time of investment.

Managerial assistance to portfolio companies

As a BDC we offer, and must provide upon request, managerial assistance to our portfolio companies. This assistance could involve, among other things, monitoring the operations of our portfolio companies, participating in board and management meetings, consulting with and advising officers of portfolio companies and providing other organizational and financial guidance. Pursuant to a separate administration agreement, our investment adviser provides such managerial assistance on our behalf to portfolio companies that request this assistance, recognizing that our involvement with each investment will vary based on factors including the size of the company, the nature of our investment, the company’s overall stage of development and our relative position in the capital structure. We may receive fees for these services.

In addition, a BDC must have been organized and have its principal place of business in the United States and must be operated for the purpose of making investments in the types of securities described in (1), (2) or (3) above under “—Qualifying assets.” However, in order to count portfolio securities as qualifying assets for the purpose of the 70.0% test, the BDC must either control the issuer of the securities or must offer to make available to the issuer of the securities (other than small and solvent companies described above) significant managerial assistance; except that, where the BDC purchases such securities in conjunction with one or more other persons acting together, one of the other persons in the group may make available such managerial assistance. Making available significant managerial assistance means, among other things, any arrangement whereby the BDC, through its directors, officers or employees, offers to provide, and, if accepted, does so provide, significant guidance and counsel concerning the management, operations or business objectives and policies of a portfolio company.

Temporary investments