Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Independent Bank Group, Inc. | d544116d8k.htm |

NASDAQ: IBTX

KBW Texas Field Trip

May 2013

Exhibit 99.1 |

Safe

Harbor Statement 2

From time to time, our comments and releases may contain

“forward-looking statements” within the meaning of the Private Securities Litigation

Reform Act of 1995 (the “Act”). Forward-looking

statements can be identified by words such as “believes,” “anticipates,” “expects,” “forecast,”

“guidance,” “intends,” “targeted,”

“continue,” “remain,” “should,” “may,” “plans,” “estimates,” “will,” “will continue,” “will remain,” variations on

such words or phrases, or similar references to future occurrences or

events in future periods; however, such words are not the exclusive means of

identifying such statements. Examples of forward-looking statements

include, but are not limited to: (i) projections of revenues, expenses, income or

loss, earnings or loss per share, and other financial items; (ii)

statements of plans, objectives, and expectations of Independent Bank Group or its

management or Board of Directors; (iii) statements of future economic

performance; and (iv) statements of assumptions underlying such statements.

Forward-looking statements are based on Independent Bank

Group’s current expectations and assumptions regarding its business, the economy, and

other future conditions. Because forward-looking statements relate

to the future, they are subject to inherent uncertainties, risks, and changes in

circumstances that are difficult to predict. Independent Bank

Group’s actual results may differ materially from those contemplated by the forward-

looking statements, which are neither statements of historical fact nor

guarantees or assurances of future performance. Factors that could cause

actual results to differ from those discussed in the

forward-looking statements include, but are not limited to: (1) local, regional, national, and

international economic conditions and the impact they may have on us

and our customers and our assessment of that impact; (2) volatility and

disruption in national and international financial markets; (3)

government intervention in the U.S. financial system, whether through changes in the

discount rate or money supply or otherwise; (4) changes in the level of

non-performing assets and charge-offs; (5) changes in estimates of future

reserve requirements based upon the periodic review thereof under

relevant regulatory and accounting requirements; (6) adverse conditions in the

securities markets that lead to impairment in the value of securities

in our investment portfolio; (7) inflation, deflation, changes in market interest

rates, developments in the securities market, and monetary

fluctuations; (8) the timely development and acceptance of new products and services

and perceived overall value of these products and services by

customers; (9) changes in consumer spending, borrowings, and savings habits; (10)

technological changes; (11) the ability to increase market share and

control expenses; (12) changes in the competitive environment among banks,

bank holding companies, and other financial service providers; (13) the

effect of changes in laws and regulations (including laws and regulations

concerning taxes, banking, securities, and insurance) with which we and

our subsidiaries must comply; (14) the effect of changes in accounting

policies and practices, as may be adopted by the regulatory agencies,

as well as the Public Company Accounting Oversight Board, the Financial

Accounting Standards Board, and other accounting standard setters; (15)

the costs and effects of legal and regulatory developments including the

resolution of legal proceedings; and (16) our success at managing the

risks involved in the foregoing items and (17) the other factors that are

described in the Company’s Form S-1 Registration Statement, as

amended, which became effective April 2, 2013, under the heading “Risk Factors.”

Any forward-looking statement made by the Company in this release

speaks only as of the date on which it is made. Factors or events that could

cause the Company’s actual results to differ may emerge from time

to time, and it is not possible for the Company to predict all of them. The

Company undertakes no obligation to publicly update any

forward-looking statement, whether as a result of new information, future developments

or otherwise, except as may be required by law.

|

Company Snapshot

3

Overview

Branch Map

Financial Highlights

•

Headquartered in McKinney, Texas

•

100+ years of operating history

•

30 banking offices in 26 communities

•

Dallas-Fort Worth metropolitan area

•

Greater Austin area

•

Focused on relationship-driven commercial banking

products

(1) Includes IPO proceeds of $86.7 million received April 8, 2013.

(2) Adjusted for C-Corp status. See Appendix for GAAP reconciliation.

Note: Financial data as of and for the quarter ended March 31, 2013.

Balance Sheet ($ in millions)

Total Assets

$1,764

Total Loans

1,422

Total Deposits

1,415

Pro Forma Equity

(1)

211

Pro Forma Equity

(1)

/ Assets

11.55%

Asset Quality

NPAs / Assets

1.35%

NPLs / Loans

0.40

Allowance / NPLs

209.73

Allowance / Loans

0.85

NCO Ratio (annualized)

0.15

Profitability

ROAA

(2)

0.89%

ROAE

(2)

12.43

Net Interest Margin

4.68

Efficiency Ratio

67.5 |

First Quarter 2013 Highlights

4

•

Organic loan production grew for the twenty-first consecutive quarter.

•

Continued year over year balance sheet growth, reflecting not only organic growth

but also completed strategic acquisitions in the second and fourth quarters

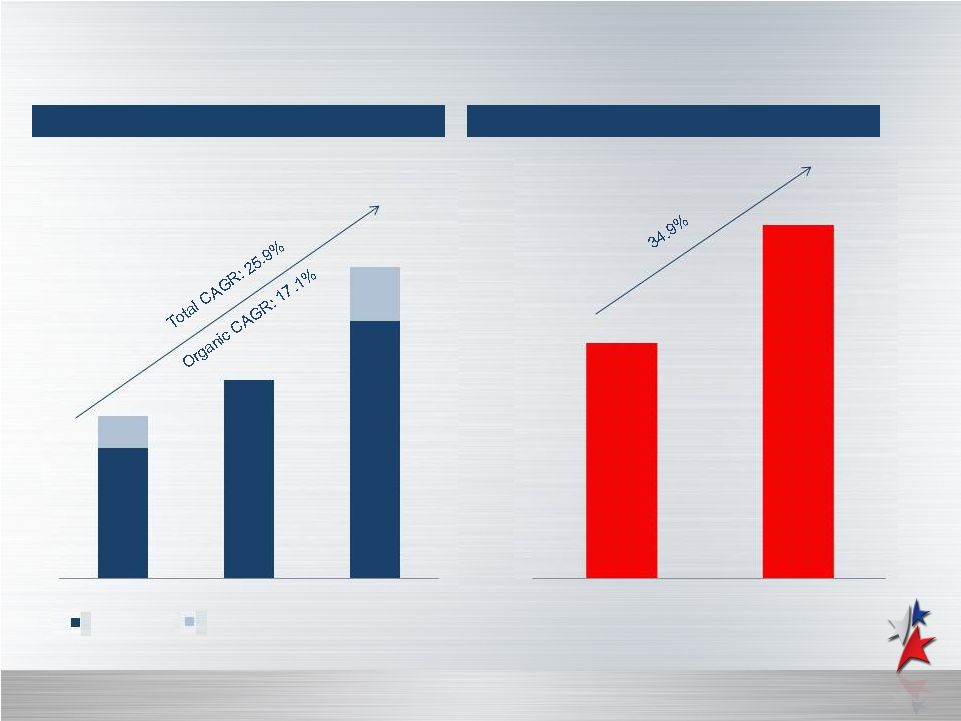

of 2012, with an increase in total assets of $456 million, 34.9%.

•

Net interest margin increased to 4.68% for first quarter 2013 compared to 4.41% for

fourth quarter 2012 and

4.31%

for

first

quarter

2012.

Net

interest

margin,

excluding

the

impact

of

purchase

accounting

accretion, was 4.40% for first quarter 2013 compared to 4.35% for fourth quarter

2012 and 4.29% for first quarter 2012.

•

Average cost of interest bearing deposits declined by 10 basis points from fourth

quarter 2012 and by 37 basis points year over year.

•

The efficiency ratio improved to 67.5% compared to 73.9% for first quarter 2012. On

an adjusted basis, the core efficiency ratio improved to 66.8% for first

quarter 2013 compared to 70.3% for first quarter 2012.

•

Continued strong asset quality, as reflected by an annualized nonperforming assets

to total assets ratio of 1.35% and a nonperforming loans to total loans

ratio of 0.40%. |

Demonstrated Growth

5

Total Assets Prior Years

Total Assets Q1 2013 v. Q1 2012

Note: Dollars in millions.

Total Assets Prior Years

Note: Dollars in millions.

$1,098

$1,254

$1,740

2010

2011

2012

Organic Growth

Impact of Acquisitions (In Year Acquired)

Q1 2012

Q1 2013

$1,764

$1,308 |

Expanded Profitability

6

Core Pre-Tax Pre-Provision Earnings Income

(1)

Net Interest Margin

(1)

(1) Net interest margin adjusted to exclude accretion on acquired loans is 4.43%,

4.37%, 4.39% and 4.40% for 2010, 2011, 2012, and Q1 2013, respectively. (2)

See Appendix for reconciliation of GAAP and adjusted measures. Note: Dollars

in thousands. Core Efficiency Ratio

(2) |

Continued Improvement in Deposit

Pricing

7

Deposit Composition at 3/31/13

Deposit Growth versus Average Rate

(1)

Rate on Interest-Bearing Deposits: 0.61%

(1) Annual average rate for total deposits.

Note: Dollars in millions. Financial data as of and for years ended through 2012

and YTD for 2013. |

Solid Capital for Continued Growth

8

(dollars in thousands, except per share data)

As of March 31, 2013

Actual

As Adjusted

(1)

Stockholders' Equity

Common Stock, $0.01 Par Value

$83

$120

Additional Paid-In Capital

88,973

209,225

Retained Earnings

33,624

-

Treasury Stock, at Cost (8,647 Shares)

(232)

(232)

Accumulated Other Comprehensive Income

1,694

1,694

Total Stockholders' Equity

$124,142

$210,807

Capital Ratios

Tier 1 Capital to Average Assets

6.29%

11.33%

Tier 1 Capital to Risk-Weighted Assets

(2)

8.01

14.43

Total Capital to Risk-Weighted Assets

10.20

15.82

Total Equity to Assets

7.04

11.55

Tangible Common Equity to Tangible Assets

(2)

5.33

9.98

Per Share Data

Book Value

$15.01

$17.64

Tangible Book Value

(2)

11.16

14.98

(1) On an as adjusted basis after giving effect to (i) the receipt of

the net proceeds from the initial public offering on April 8, 2012 of 3.680 million shares of its common stock at an offering price of $26.00 per share,

after deducting the underwriting discounts and commissions and the offering expenses

payable by Independent ; (ii) repayment of $12.3 million of senior secured notes and $13.1 million of subordinated

debentures; and (iii) the reclassification of undistributed S corporation earnings of

$33.6 million from retained earnings to additional paid-in capital as a result of the Independent’s conversion to a C corporation.

(2) See Appendix for GAAP reconciliation. |

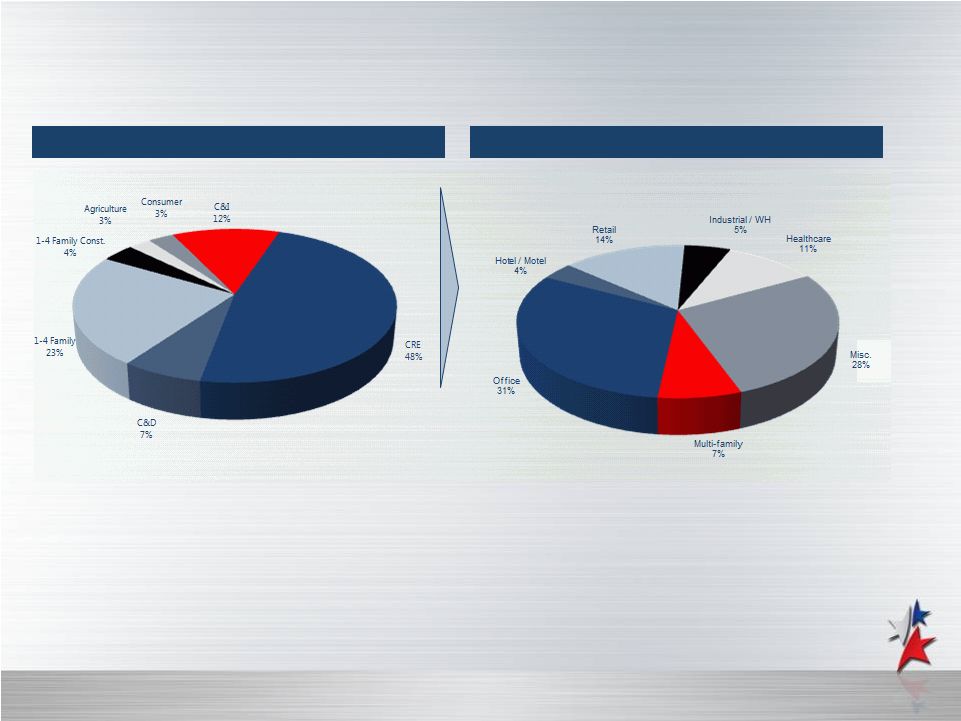

Diversified Loan Portfolio

9

Loan Composition at 3/31/13

CRE Loan Composition at 3/31/13

Q1 2013 Yield on Loans: 6.03%

Net of Acquired Loan Accretion: 5.72%

52% of CRE Loans are Owner-Occupied

Loan Composition at 3/31/13

CRE Loan Composition at 3/31/13 |

Strong Credit Culture

10

NPLs / Loans

N

NPLs / Loans

NCOs / Average Loans

Source: U.S. and Texas Commercial Bank numbers from SNL Financial. Note: Prior year financial data as of and

for years ended, current year financial data as of and for the quarter ended 3/31/13. Q1 2013 charge-off information has been annualized. |

APPENDIX

11 |

Reconciliation of GAAP and Adjusted

Measures

12

($ in thousands)

2010

2011

2012

2012

2013

Net Interest Income -

Reported

$38,065

$46,281

$58,553

$12,302

$18,215

(a)

Income recognized on acquired loans

(45)

(477)

(233)

(58)

(1,068)

(b)

Net interest income less accretion on acquired loans

$38,020

$45,804

$58,320

$12,244

$17,147

(a + b = c)

Provision Expense -

Reported

$4,043

$1,650

$3,184

$575

$1,030

(d)

Noninterest Income -

Reported

(e)

Bargain Purchase Loss / (Gain)

($6,692)

$0

$0

$0

$0

Loss / (Gain) on Sale of Branch

0

0

(38)

0

0

Loss / (Gain) on Sale of OREO

(136)

(918)

(1,135)

53

(25)

Loss / (Gain) on Sale of Securities

0

0

3

3

0

Loss / (Gain) on Sale of PP&E

(1)

(21)

343

(1)

(1)

Adjusted Noninterest Income

$5,327

$6,769

$8,341

$1,946

$2,400

(f)

Noninterest Expense -

Reported

$33,062

$38,639

$47,160

$10,494

$13,923

(g)

Adriatica Expenses

$0

($871)

($832)

($300)

($197)

OREO Impairment

(805)

(184)

(94)

0

(541)

Acquisition Expense

(668)

0

(1,401)

(216)

(137)

Adjusted Noninterest Expense

$31,589

$37,584

$44,833

$9,978

$13,048

(h)

Pre-Tax Pre-Provision Earnings

$17,159

$15,350

$20,561

$3,699

$6,718

(a) + (e) -

(g)

Core Pre-Tax Pre-Provision Earnings

$11,758

$14,989

$21,828

$4,212

$6,499

(c) + (f) -

(h)

Reported Efficiency Ratio

65.8%

71.6%

69.6%

73.9%

67.5%

(g) / (a + e)

Adjusted Efficiency Ratio

72.9%

71.5%

67.3%

70.3%

66.8%

(h) / (c + f)

Year Ended December 31,

Quarter Ended March 31,

$2,426

$12,156

$7,708

$9,168

$1,891 |

Reconciliation of GAAP and Adjusted

Measures

13

($ in thousands)

2010

2011

2012

2012

2013

Net Income -

Reported

$13,116

$13,700

$17,377

$3,124

$5,688

Effective Tax Rate

33.1%

31.7%

30.1%

30.1%

32.8%

Pro Forma Net Income

$8,775

$9,357

$12,147

$2,184

$3,822

Average Assets

$969,322

$1,180,693

$1,487,614

$1,271,901

$1,733,924

Average Stockholders' Equity

$68,350

$78,922

$105,055

$91,776

$124,731

Pro Forma ROAA

0.91%

0.79%

0.82%

0.70%

0.89%

Pro Forma ROAE

12.84%

11.86%

11.56%

9.65%

12.43%

Year Ended December 31,

Quarter Ended March 31, |

($ in thousands,

except per share data) As of

3/31/2013

Total Stockholders' Equity

$124,142

Goodwill

(28,742)

Core Deposit Intangibles

(3,075)

Tangible Common Equity

$92,325

Common Shares Outstanding

8,269,707

Book Value per Share

$15.01

Tangible Book Value per Share

$11.16

Reconciliation of GAAP and Adjusted

Measures

14

($ in thousands)

As of

3/31/2013

Total Stockholders' Equity

$124,142

Unrealized Gain on AFS Securities

(1,694)

Goodwill

(28,742)

Other Intangibles

(3,075)

Qualifying Restricted Core Capital

17,600

Tier 1 Capital

$108,231

Risk-Weighted Assets

On Balance Sheet

$1,339,808

Off Balance Sheet

10,623

Total Risk-Weighted Assets

$1,350,431

Tier 1 Capital to Risk-Weighted Capital Ratio

8.01% |

Contact Information

15

Corporate Headquarters

Analysts/Investors:

Independent Bank

Torry Berntsen

1600 Redbud Blvd

President and Chief Operating Officer

McKinney, TX 75069

(972) 562-9004

tberntsen@independent-bank.com

972-562-9004 Telephone

972-562-7734 Fax

Michelle Hickox

independent-bank.com

Chief Financial Officer

(972) 562-9004

mhickox@independent-bank.com

Media:

Eileen Ponce

(469) 742-9437

eponce@independent-bank.com |