Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - FIFTH THIRD BANCORP | d541509d8k.htm |

Barclays Capital

2013 Americas Select Franchise Conference

Daniel T. Poston

Executive Vice President & Chief Financial Officer

May 22, 2013

Please refer to earnings release dated April 18, 2013 and

10-Q dated May 9, 2013 for further information

Exhibit 99.1

©

Fifth Third Bank | All Rights Reserved |

2

©

Fifth Third Bank | All Rights Reserved

A strong franchise with strong momentum

Return on avg. assets

Net charge-off ratio

Net income available to

common shareholders ($MM)

Generated highest level of net income

to common shareholders since 2005.

Improving profitability approaching

target for normalized environment.

Problem assets are at the lowest

levels in five years.

Tier 1 common ratio*

Total payout ratio

ALLL / NPLs

Coverage levels more than adequate

to protect against potential losses.

Capital ratios continue to be strong

and grow to record levels.

Payouts to shareholders

approached $1B in 2012.

31%

63%

11%

Vantiv

Other

* Non-GAAP measure; see Reg. G reconciliation in appendix.

|

©

Fifth Third Bank | All Rights Reserved

Fifth Third franchise

$121 billion assets (#12)

$92 billion total deposits (#13)

$14 billion market cap (#12)

18 affiliates in 12 states

1,320 banking centers

2,426 ATMs

Leading market share in mature

Midwest market; strong presence in

higher growth Southeastern markets

Source: SNL Financial. Rankings based on U.S. headquartered commercial banks.

Data as of 3/31/13

Kentucky

Tennessee

Georgia

Florida

North

Carolina

West

Virginia

Pennsylvania

Ohio

Michigan

Illinois

Indiana

Missouri

3 |

4

©

Fifth Third Bank | All Rights Reserved

—

Return on assets of 1.41%; return on average common equity of 12.5%; return on

average tangible common equity** of 15.5%

Credit trends remain favorable

—

Net charge-offs (NCOs) of $133MM (0.63% of loans and leases) down $14MM (7 bps)

vs. 4Q12 —

Total NPAs of $1.2B including loans held-for-sale (HFS) down $86MM, or 7%,

from 4Q12; NPA ratio of 1.41% down 8 bps from 4Q12, NPL ratio of 1.11% down 8

bps from 4Q12 —

Total

delinquencies

(loans

30-89

days

past

due

and

90

days

past

due)

lowest

since

1Q01

Strong capital ratios*

—

Tier 1 common ratio 9.70%**, up 19 bps sequentially (Basel III pro forma estimate of

~8.9%) —

Tier 1 capital ratio 10.83%, Total capital ratio 14.35%, Leverage ratio 10.03%

—

Tangible common equity ratio** of 9.03% excluding unrealized gains/losses; 9.29%

including them

—

Repurchased ~8MM common shares in 1Q13; new 100MM share repurchase authorization in

March

1Q13 highlights

Net income available to common shareholders of $413MM ($0.46 per diluted

share), vs. $390MM ($0.43 per share) in 4Q12 and $421MM ($0.45 per share) in 1Q12 * Capital ratios presented under

current U.S. capital regulations. The pro forma Tier I common equity ratio is management’s estimate based upon its current

interpretation of the three draft Federal Register notices proposing enhancements to regulatory

capital requirements published in June 2012. The actual impact to the Bancorp’s Tier I

common equity ratio may change significantly due to revisions to the agencies’ final rules.

** Non-GAAP measure; see Reg. G reconciliation in appendix. |

©

Fifth Third Bank | All Rights Reserved

5

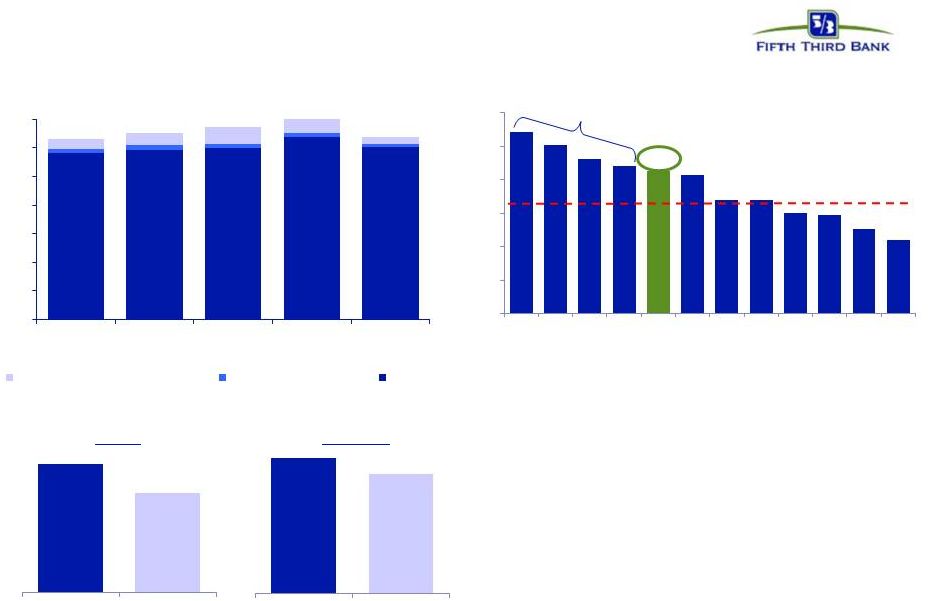

Strong revenue and profit generation

Peer med. 1.7%

2.1%

1Q13 returns strong relative to peers

ROAA

ROATCE

•

Business mix provides higher than

average diversity among spread and fee

revenues (45+% of revenue)

•

Relatively strong margin and relatively

high fee income contribution drives

strong profitability despite interest rate

environment

Pre-provision net revenue (PPNR) trend

1Q13 PPNR* / Average Assets

Source: SNL Financial and Company Reports. Data as of 1Q13. Peer median includes:

BBT, CMA, HBAN, KEY, MTB, PNC, RF, STI, USB, WFC, and ZION.PPNR and ROATCE

are Non-GAAP measures. See Reg. G reconciliation in the Appendix to the presentation.

^ See Page 18 in the Appendix for adjustments

* Excludes securities gains / losses for FITB and peers. Also excludes goodwill

impairment charge for peers as applicable. Significant purchase

accounting

benefit

PPNR

$694 $636

$568

$616

$653 583

593

598

638

602

14

17

14

13

10

34

40

59

68

24

$0

$100

$200

$300

$400

$500

$600

$700

1Q12

2Q12

3Q12

4Q12

1Q13

Noninterest Expense Credit Items

Fee Income Credit Items

Adjusted^

15.5%

13.7%

FITB

Peer Median

1.41%

1.09%

FITB

Peer Median

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

USB

WFC

MTB

BBT

FITB

PNC

HBAN

STI

RF

KEY

CMA

ZION |

6

©

Fifth Third Bank | All Rights Reserved

NII results reflect continued moderate NIM

pressure offset by balance sheet growth

* Represents purchase accounting adjustments included in net interest income.

^ Estimate; funding (DDAs + interest-bearing liabilities); liabilities

attributed to fixed or floating using terms and expected beta Fixed / Floating

Portfolio •

Negative impact of lower rates on net interest

income generally offset by loan growth

•

Spreads on new originations of variable rate

assets consistent with historical spreads

–

Emphasis on variable rate C&I lending

•

Coupons on new fixed rate loan originations

converging with portfolio average coupons

Interest-Earning

Assets

Funding^

Fixed

~55-60%

NII and NIM (FTE)

($MM)

Loans

52%

Loans

32%

Investment

Portfolio 3%

Trend: fixed rate loan origination coupons

relative to fixed portfolio weighted avg

Larger portfolio repricing effects

3.61%

3.56%

3.56%

3.49%

3.42%

903

899

907

903

893

$450

$550

$650

$750

$850

$950

2.0%

2.5%

3.0%

3.5%

4.0%

1Q12

2Q12

3Q12

4Q12

1Q13

Net Interest Income (right axis)

PAA*

NIM

0.00

0.50

1.00

1.50

2.00

Fixed

45%

Floating

55%

Investment

Portfolio

13%

Floating

Fixed

Floating

~40-45% |

7

©

Fifth Third Bank | All Rights Reserved

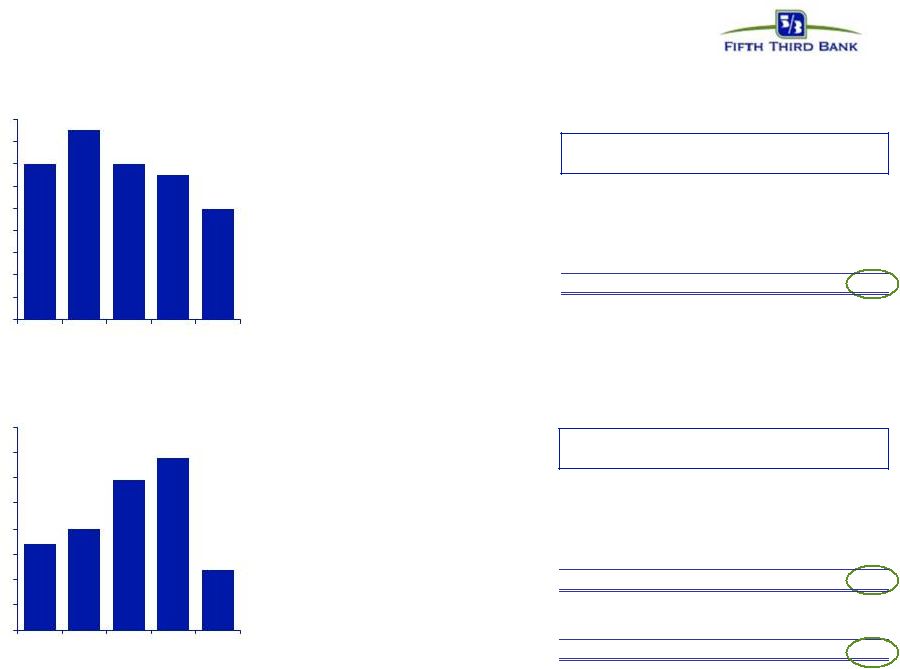

Strong loan growth,

ample opportunities for ongoing growth

Loan balances ($B)

Loan composition (EOP HFI)

47% C&I / lease

11% Commercial real estate

Commercial

25% Resi. mtg. / home equity

14% Auto

3% Card / other

Consumer

•

Solid loan growth with

disciplined lending standards

•

C&I and residential mortgage

balance growth more than

offset run-off in both home

equity and commercial real

estate loans (CRE run-off

continues to slow)

$82.1

$85.7

$81.5

$82.6

$82.9

$83.9

$85.9

1Q12

2Q12

3Q12

4Q12

1Q13

EOP loans HFI

Avg loans HFI |

8

©

Fifth Third Bank | All Rights Reserved

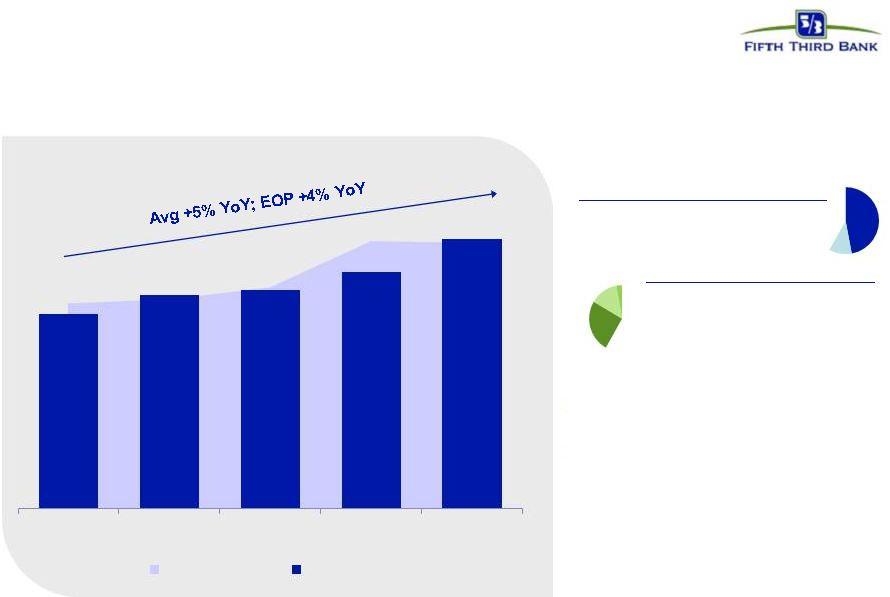

Strengthened deposit profile

and increased value proposition to customers

Average deposit balances ($B)

Simplified deposit products

•

Straightforward,

easy

to

use

accounts

•

Reduced complexity

•

Elimination of certain fees

•

Total relationship earns better

rates and lower costs

•

Compatible with Fifth Third’s

strategic direction and new

regulatory landscape

Deposit growth benefited

from focus on

full customer relationship

$77.1

$77.6

$77.5

$80.2

$80.9

$81.7

$84.9

1Q12

2Q12

3Q12

4Q12

1Q13

Transaction deposits

Other time deposits |

9

©

Fifth Third Bank | All Rights Reserved

Diverse revenue stream

45% Fee income

NII

Fee income as % of 1Q13 revenue

1Q13 Fee income distribution

Economic trends should support long-term improvement in results through

balance sheet growth and higher business activity

Strong momentum in key businesses:

•

Corporate banking: recent investments in capital markets capabilities, increased

syndication and business lending fees

•

Investment advisors: 1Q13 strongest in company history due to increased brokerage

production, seasonal trust tax preparation fees and higher market values

•

Retail banking: listening to voice of customer and enhancing channels and products to

meet consumer preferences

•

Consumer lending: record mortgage originations and strong auto lending supporting

business Deposit

Fees

18%

Corporate

Banking

13%

Investment

Advisors

13%

Other^

17%

Mortgage

30%

Card and

Processing

9%

55%

^ Includes other noninterest income and securities gains. |

10

©

Fifth Third Bank | All Rights Reserved

Disciplined expense management

•

Long-term target for mid-50% efficiency

ratio in normalized environment (with

higher interest rate environment)

Expense trend ($MM)

* Non-recurring items listed on page 18 in the appendix.

Managing expenses carefully in response to revenue

environment; continuous process of expense evaluation

Efficiency ratio trend

Reported expense

$973

$937

$1,006

$1,163

$978

Non-recurring items*:

Decreasing Expense

$23

$18

$5

--

$9

Increasing Expense

($29)

--

($55)

($173)

($9)

Adjusted Expense

$967

$955

$956

$990

$978

$600

$700

$800

$900

$1,000

$1,100

$1,200

1Q12

2Q12

3Q12

4Q12

1Q13

58%

59%

64%

65%

60%

62%

62%

61%

60%

62%

1Q12

2Q12

3Q12

4Q12

1Q13

Efficiency Ratio

Adjusted*

–

Current impact of credit costs on

revenue and expenses; impact of

regulatory reforms not fully mitigated

–

Reflects below-capacity balance sheet

and lower revenue than we expect and

can support longer term

–

~ 60% for year end 2013 |

11

©

Fifth Third Bank | All Rights Reserved

Continued improvement in credit trends

Peer average includes: BBT, CMA, HBAN, KEY, MTB, PNC, RF, STI, USB, WFC, and

ZION. Source: SNL Financial and Company Reports. Data as of 1Q13. All ratios

exclude loans held-for-sale and covered assets for peers where appropriate.

* 4Q08 NCOs included $800MM in NCOs related to commercial loans moved to

held-for-sale, NCO ratio of 7.5%, 3.8% before credit actions; 3Q10 NCOs included $510MM

in NCOs related to loans sold or moved to held-for-sale.

NPA ratio vs. peers

Net charge-off ratio vs. peers

Loans 90+ days delinquent % vs. peers

Loans 30-89 days delinquent % vs. peers

5.0%*

2.3%

before credit

actions

FITB credit metrics are in line with or better than peers

0.5%

1.5%

2.5%

3.5%

4.5%

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

FITB

Peer Average

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

4Q08*

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

FITB

Peer Average

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

FITB

Peer Average

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

FITB

Peer Average |

12

©

Fifth Third Bank | All Rights Reserved

Strong reserve position

Peer median includes: BBT, CMA, HBAN, KEY, MTB, PNC, RF,STI, USB, WFC, and

ZION. Source: SNL Financial and Company Reports. Data as of 1Q13. NPAs

/

NPLs exclude held-for-sale portion for all banks as well as covered assets

for BBT, USB, and ZION. 1Q13 coverage ratios strong

relative to peers

Industry leading reserve levels

Fifth Third

Peer Median

187%

137%

Reserves / NPLs

$220

$181

$156

$147

$133

($129)

($110)

($91)

($71)

($71)

2.59%

2.45%

2.32%

2.16%

2.08%

($150)

($100)

($50)

$0

$50

$100

$150

$200

$250

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

1Q12

2Q12

3Q12

4Q12

1Q13

Net Charge-offs

Additional Provision

Reserves

147%

126%

Reserves / NPAs

331%

290%

Reserves / Annualized NCOs |

13

©

Fifth Third Bank | All Rights Reserved

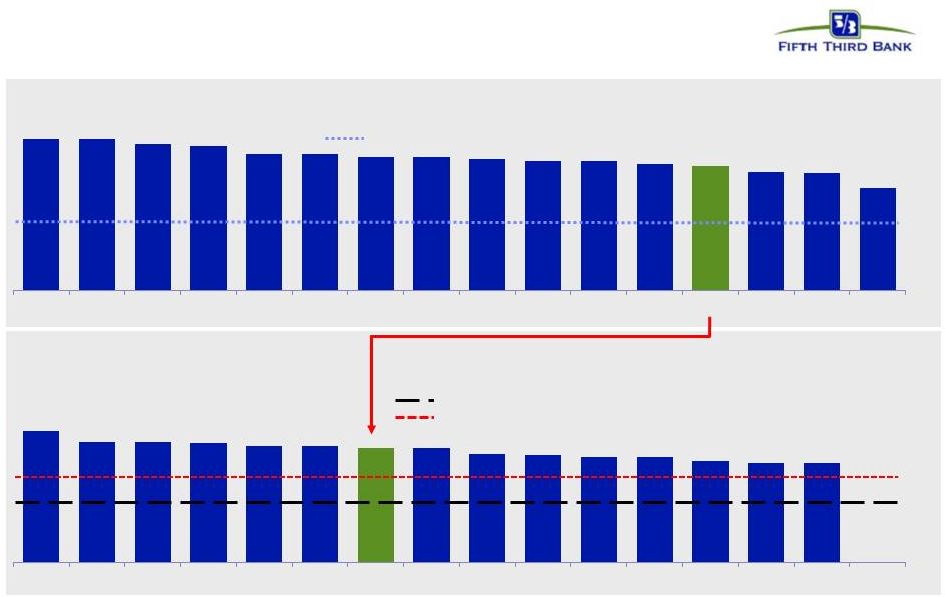

Fifth Third’s balance sheet and business model

relatively advantaged under new capital standards

Fifth Third’s capital position already well in excess of any established

standards, likely standards, and most peers 5.0%

7.0%

4.5%

Unofficial CCAR supervisory reference minimum

1Q13 Pro forma Tier 1 common / RWA

U.S. proposed Basel III**

1Q13 Tier 1 common / RWA

Basel I

2019 Basel III buffered minimum

2015 Basel III minimum

Not

disclosed

~9.1%

11.8%

11.8%

11.4%

11.2%

10.6%

10.6%

10.4%

10.4%

10.2%

10.1%

10.1%

9.8%

9.7%

9.2%

9.1%

7.9%

C

COF

KEY

RF

HBAN

BAC

CMA

WFC

JPM

STI

ZION

PNC

FITB

BBT

USB

MTB

10.3%

9.4%

9.4%

9.3%

9.1%

8.9%

8.9%

8.5%

8.4%

8.2%

8.2%

7.9%

7.8%

7.8%

0

KEY

BAC

CMA

C

RF

HBAN*

FITB

JPM

COF

WFC

STI

USB

PNC

BBT

ZION*

MTB

Source: SNL Financial and Company Reports. Data as of 1Q13.

* In 2Q12, HBAN stated Basel III Tier 1 common ratio would be negatively impacted by approximately 150

basis points and in their 1Q13 Earning Conference Call, they stated this again. In 2Q12, ZION

stated Tier 1 common ratio would be in the 7.75% area. ** Note: Fifth Third’s pro forma

Tier I common equity ratio is management’s estimate based upon its current interpretation of the three draft Federal Register notices proposing

enhancements to regulatory capital requirements published in June 2012. The actual impact to the

Bancorp’s Tier I common equity ratio may change significantly due to further clarification

of the agencies proposals or revisions to the agencies final rules, which remain subject to public comment. Not adjusted for potential mitigation efforts.

|

14

©

Fifth Third Bank | All Rights Reserved

Capital management philosophy

* Subject to Board of Directors and regulatory approval

Organic growth opportunities

•

Support growth of core banking franchise

•

Continued loan growth despite sluggish

economy

Strategic opportunities

*

•

Prudently evaluate opportunities to increase

density of franchise via disciplined

acquisitions or selective de novos

•

Expect future acquisition opportunities

although activity likely to remain muted in

near-term

•

Attain top 3 market position in 65% of

markets or more longer term

Dividends*

•

As previously indicated, move towards levels

more consistent with Fed’s near-term payout

ratio guidance of 30%

•

Strong levels of profitability would support

higher dividend than current level

•

Quarterly dividend increased to $0.11 in 1Q13

(increase to $0.12 not objected to in 2013 CCAR)

Repurchases / Redemptions

*

•

Common share repurchases to limit / manage

growth of excess capital levels

•

2013 CCAR included:

–

Potential conversion of $398MM in outstanding

Series G 8.5% convertible preferred stock into

~35.5MM common shares

–

Potential repurchase of up to $984MM common

shares including any issued in a Series G

preferred stock conversion (up to $550MM)

–

Potential issuance of $500MM in preferred stock

Consistent and prudent capital management philosophy

Capital Deployment

Capital Return

–

Other considerations: regulatory environment,

alternatives, maintenance of desired / required

buffers, stock price |

15

©

Fifth Third Bank | All Rights Reserved

Well-positioned for the future

•

Cash currently sufficient to satisfy all fixed obligations in a stressed

environment for approximately 2 years (debt maturities, common and preferred

dividends, interest and other expenses) without accessing capital markets; relying

on dividends from subsidiaries or any other discretionary actions

•

Fifth Third has completely exited all crisis-era government support

programs Superior capital and liquidity position

•

NCOs of 0.63%; 3.3x reserves / annualized NCOs

•

Substantial reduction in exposure to CRE since 1Q09; relatively low CRE exposure

versus peers •

Very low relative exposure to areas of concern, e.g. European financials, mortgage

repurchase risk Proactive approach to risk management

•

Traditional commercial banking franchise built on customer-oriented localized

operating model •

Strong market share in key markets with focus on further improving density

•

Fee income ~45% of total revenue

Diversified traditional banking platform

•

PPNR has remained strong throughout the credit cycle

•

PPNR substantially exceeds annual net charge-offs (491% PPNR / NCOs^ in

1Q13) •

1.4% ROAA; 15.5% return on average tangible common equity^

Industry leader in earnings power

^ Non-GAAP measure. See Reg. G reconciliation in Appendix.

|

16

©

Fifth Third Bank | All Rights Reserved

Cautionary statement

This report contains statements that we believe are “forward-looking statements” within

the meaning of Section 27A of the Securities Act of 1933, as amended, and Rule 175 promulgated

thereunder, and Section 21E of the Securities Exchange Act of 1934, as amended, and Rule

3b-6 promulgated thereunder. These statements relate to our financial condition, results of operations, plans, objectives, future

performance or business. They usually can be identified by the use of forward-looking language

such as “will likely result,” “may,” “are expected to,” “is

anticipated,” “estimate,” “forecast,” “projected,” “intends to,” or may include other similar words or phrases such as

“believes,” “plans,” “trend,” “objective,”

“continue,” “remain,” or similar expressions, or future or conditional verbs such as “will,” “would,”

“should,” “could,” “might,” “can,” or similar verbs. You

should not place undue reliance on these statements, as they are subject to risks and

uncertainties, including but not limited to the risk factors set forth in our most recent Annual Report on Form 10-K. When considering

these forward-looking statements, you should keep in mind these risks and uncertainties, as well

as any cautionary statements we may make. Moreover, you should treat these statements as

speaking only as of the date they are made and based only on information then actually known to

us. There are a number of important factors that could cause future results to differ

materially from historical performance and these forward- looking statements. Factors that

might cause such a difference include, but are not limited to: (1) general economic conditions and

weakening in the economy, specifically the real estate market, either nationally or in the states in

which Fifth Third, one or more acquired entities and/or the combined company do business, are

less favorable than expected; (2) deteriorating credit quality; (3) political developments,

wars or other hostilities may disrupt or increase volatility in securities markets or other economic conditions; (4) changes in

the interest rate environment reduce interest margins; (5) prepayment speeds, loan origination and

sale volumes, charge-offs and loan loss provisions; (6) Fifth Third’s ability to

maintain required capital levels and adequate sources of funding and liquidity; (7) maintaining

capital requirements may limit Fifth Third’s operations and potential growth; (8) changes and

trends in capital markets; (9) problems encountered by larger or similar financial institutions

may adversely affect the banking industry and/or Fifth Third; (10) competitive pressures among

depository institutions increase significantly; (11) effects of critical accounting policies and judgments; (12) changes in

accounting policies or procedures as may be required by the Financial Accounting Standards Board

(FASB) or other regulatory agencies; (13) legislative or regulatory changes or actions, or

significant litigation, adversely affect Fifth Third, one or more acquired entities and/or the

combined company or the businesses in which Fifth Third, one or more acquired entities and/or the combined company are engaged,

including the Dodd-Frank Wall Street Reform and Consumer Protection Act; (14) ability to maintain

favorable ratings from rating agencies; (15) fluctuation of Fifth Third’s stock price;

(16) ability to attract and retain key personnel; (17) ability to receive dividends from its

subsidiaries; (18) potentially dilutive effect of future acquisitions on current shareholders’

ownership of Fifth Third; (19) effects of accounting or financial results of one or more

acquired entities; (20) difficulties from the separation of or the results of operations of Vantiv,

LLC from Fifth Third; (21) loss of income from any sale or potential sale of businesses that could

have an adverse effect on Fifth Third’s earnings and future growth; (22) ability to secure

confidential information and deliver products and services through the use of computer systems

and telecommunications networks; and (23) the impact of reputational risk created by these developments on such matters as

business generation and retention, funding and liquidity.

You should refer to our periodic and current reports filed with the Securities and Exchange

Commission, or “SEC,” for further information on other factors, which could cause

actual results to be significantly different from those expressed or implied by these forward-looking

statements.

|

©

Fifth Third Bank | All Rights Reserved

Appendix |

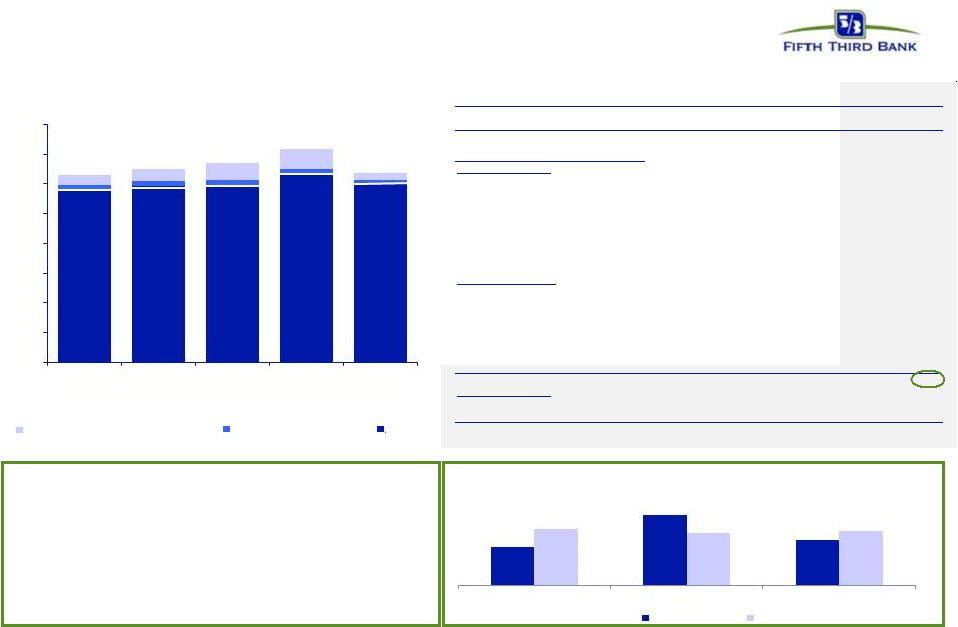

18

©

Fifth Third Bank | All Rights Reserved

($ in millions)

1Q12

2Q12

3Q12

4Q12

1Q13

Income before income taxes (U.S. GAAP) (a)

$603

$565

$503

$540

$591

Add: Provision expense (U.S. GAAP) (b)

91

71

65

76

62

PPNR (a) + (b)

$694

$636

$568

$616

$653

Adjustments to remove (benefit) / detriment^:

In noninterest income:

Gain from Vantiv IPO (1Q12) and sale of shares (4Q12)

(115)

-

-

(157)

-

Vantiv debt refinancing

34

-

-

-

-

Valuation of 2009 Visa total return swap

19

11

1

15

7

Vantiv warrant & puts

(46)

(56)

16

19

(34)

Valuation of bank premises moved to HFS

-

17

-

-

-

Litigation reserve additions in revenue

-

6

-

-

-

Sale of certain Fifth Third funds

-

-

(13)

-

(7)

Securities (gains) / losses

(9)

(3)

(2)

(2)

(17)

In noninterest expense:

Debt extinguishment (gains) / losses

9

-

26

134

-

Non-income tax related assessment resolution

(23)

-

-

-

-

Sale of certain Fifth Third funds

-

-

2

-

-

Severance expense

6

-

-

-

-

FDIC insurance expense

-

(9)

-

-

-

Gain on sale of affordable housing

-

(8)

(5)

-

(9)

Litigation reserve additions in expense

14

(1)

5

13

9

Adjusted PPNR

$583

$593

$598

$638

$602

Credit-related items^^:

In noninterest income

14

17

14

13

10

In noninterest expense

34

40

59

68

24

Credit-adjusted PPNR**

$631

$650

$671

$719

$636

Pre-tax pre-provision earnings*

PPNR trend

* Non-GAAP measure. See Reg. G reconciliation on page 21.

^ Prior quarters include similar adjustments.

^^ See Slide 19 for detailed breakout of credit-related items.

# 60% also excluding 4Q12 mortgage repurchase reserve build

•

PPNR of $653MM up 6% from 4Q12 levels and down 6% from

prior year

•

Adjusted PPNR of $602MM, down 6% sequentially and up 3%

from prior year

–

Sequential change due primarily to lower mortgage

revenue and seasonal increase in FICA and

unemployment expense, partially offset by lower credit

costs

PPNR reconciliation

Efficiency ratio

583

593

598

638

602

14

17

14

13

10

34

40

59

68

24

$0

$100

$200

$300

$400

$500

$600

$700

$800

1Q12

2Q12

3Q12

4Q12

1Q13

Noninterest Expense Credit Items

Fee Income Credit Items

Adjusted

PPNR

$694 $636 $568

$616 $653

58%

65%

60%

62%

61%

#

62%

1Q12

4Q12

1Q13

Efficiency Ratio

Adjusted

** There are limitations on the usefulness of credit-adjusted PPNR, including the significant

degree to which changes in credit and fair value are integral, recurring components of the

Bancorp’s core operations as a financial institution. This measure has been included herein to

facilitate a greater understanding of the Bancorp’s financial condition. |

19

©

Fifth Third Bank | All Rights Reserved

Credit-related costs

In noninterest income ($MM)

In noninterest expense ($MM)

Note: Numbers may not sum due to rounding

Total credit-related costs

$48

$57

$73

$81

$34

34

40

59

68

24

$0

$10

$20

$30

$40

$50

$60

$70

$80

1Q12

2Q12

3Q12

4Q12

1Q13

14

17

14

13

10

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

1Q12

2Q12

3Q12

4Q12

1Q13

Actual

($ in millions)

1Q12

2Q12

3Q12

4Q12

1Q13

Gain / (loss) on sale of loans

$5

$8

$2

$4

$2

Commercial loans HFS FV adjustment

(1)

(5)

(3)

(3)

(1)

Gain / (loss) on sale of OREO

properties

(17)

(19)

(11)

(10)

(10)

Mortgage repurchase costs

(2)

(2)

(2)

(3)

(2)

Total credit-related revenue impact

($14)

($17)

($14)

($13)

($10)

Actual

($ in millions)

1Q12

2Q12

3Q12

4Q12

1Q13

Mortgage

repurchase expense

$15

$18

$36

$44

$20

Provision for unfunded commitments

(2)

(1)

(2)

3

(11)

Derivative valuation adjustments

(4)

(0)

(2)

(2)

(1)

OREO expense

5

5

6

5

4

Other problem asset related expenses

19

19

21

19

12

Total credit-related operating expenses

$34

$40

$59

$68

$24 |

20

©

Fifth Third Bank | All Rights Reserved

Regulation G Non-GAAP reconciliation

Fifth Third Bancorp and Subsidiaries

Regulation G Non-GAAP Reconcilation

$ and shares in millions

(unaudited)

March

December

September

June

March

2013

2012

2012

2012

2012

Income before income taxes (U.S. GAAP)

$591

$540

$503

$565

$603

Add:

Provision expense (U.S. GAAP)

62

76

65

71

91

Pre-provision net revenue (a)

653

616

568

636

694

Net income available to common shareholders (U.S. GAAP)

413

390

354

376

421

Add:

Intangible amortization, net of tax

1

2

2

2

3

Tangible net

income available to common shareholders 414

392

356

378

424

Tangible net income available to common

shareholders (annualized) (b) 1,679

1,559

1,416

1,520

1,705

Average Bancorp shareholders' equity (U.S. GAAP)

13,779

13,855

13,887

13,628

13,366

Less:

Average preferred stock

(398)

(398)

(398)

(398)

(398)

Average goodwill

(2,416)

(2,417)

(2,417)

(2,417)

(2,417)

Average intangible assets

(26)

(28)

(31)

(34)

(38)

Average tangible common equity

(c) 10,939

11,012

11,041

10,779

10,513

Total Bancorp shareholders' equity (U.S. GAAP)

13,882

13,716

13,718

13,773

13,560

Less:

Preferred stock

(398)

(398)

(398)

(398)

(398)

Goodwill

(2,416)

(2,416)

(2,417)

(2,417)

(2,417)

Intangible assets

(25)

(27)

(30)

(33)

(36)

Tangible common equity, including

unrealized gains / losses (d) 11,043

10,875

10,873

10,925

10,709

Less: Accumulated other comprehensive income / loss

(333)

(375)

(468)

(454)

(468)

Tangible common equity, excluding unrealized gains /

losses (e) 10,710

10,500

10,405

10,471

10,241

Total assets (U.S. GAAP)

121,382

121,894

117,483

117,543

116,747

Less:

Goodwill

(2,416)

(2,416)

(2,417)

(2,417)

(2,417)

Intangible assets

(25)

(27)

(30)

(33)

(36)

Tangible assets, including

unrealized gains / losses (f) 118,941

119,451

115,036

115,093

114,294

Less: Accumulated other comprehensive income / loss, before tax

(512)

(577)

(720)

(698)

(720)

Tangible assets, excluding unrealized gains / losses

(g) 118,429

118,874

114,316

114,395

113,574

Common shares outstanding (h)

875

882

897

919

920

Net charge-offs (i)

133

147

156

181

220

Ratios:

Return on average tangible common equity (b) / (c)

15.5%

14.1%

12.8%

14.1%

16.2%

Tangible common equity (excluding unrealized gains/losses) (e) / (g)

9.03%

8.83%

9.10%

9.15%

9.02%

Tangible common equity (including unrealized gains/losses) (d) / (f)

9.29%

9.10%

9.45%

9.49%

9.37%

Tangible book value per share (d) / (h)

12.63

12.33

12.12

11.89

11.64

PPNR / NCOs (a) / (i)

491%

419%

364%

351%

315%

For the Three Months Ended |

21

©

Fifth Third Bank | All Rights Reserved

Regulation G Non-GAAP reconciliation

Fifth Third Bancorp and Subsidiaries

Regulation G Non-GAAP Reconcilation

$ and shares in millions

(unaudited)

March

December

September

June

March

2013

2012

2012

2012

2012

Total Bancorp shareholders' equity (U.S. GAAP)

$13,882

$13,716

$13,718

$13,773

$13,560

Goodwill and certain other intangibles

(2,504)

(2,499)

(2,504)

(2,512)

(2,518)

Unrealized gains

(333)

(375)

(468)

(454)

(468)

Qualifying trust preferred securities

810

810

810

2,248

2,248

Other

23

33

38

38

38

Tier I capital

11,878

11,685

11,594

13,093

12,860

Less:

Preferred stock

(398)

(398)

(398)

(398)

(398)

Qualifying trust preferred securities

(810)

(810)

(810)

(2,248)

(2,248)

Qualifying noncontrolling interest in consolidated subsidiaries

(38)

(48)

(51)

(51)

(50)

Tier I common equity (a)

10,632

10,429

10,335

10,396

10,164

Risk-weighted assets, determined in accordance with

prescribed regulatory requirements (b)

109,626

109,699

106,858

106,398

105,412

Ratio:

Tier I common equity (a) / (b)

9.70%

9.51%

9.67%

9.77%

9.64%

Basel III - Estimates

March

December

September

June

2013

2012

2012

2012

Tier 1 common equity (Basel I)

$10,632

$10,429

$10,335

$10,396

Add:

Adjustment related to AOCI for AFS securities

397

429

506

551

Estimated Tier 1 common equity under Basel III rules (c)

$11,029

$10,858

$10,841

$10,947

Estimated risk-weighted assets under Basel III rules (d)

$123,696

$123,725

$120,308

$119,428

Estimated Tier 1 common equity ratio under Basel III rules

8.91%

8.78%

9.01%

9.17%

(c)

(d)

Tier 1 common equity under Basel III includes the unrealized gains and losses for AFS securities.

Other adjustments include mortgage servicing rights and deferred tax assets subject to threshold

limitations and deferred tax liabilities related to intangible assets.

Key differences under Basel III in the calculation of risk-weighted assets compared to Basel I

include: (1) Risk weighting for commitments under 1 year; (2) Higher risk weighting for exposures to

residential mortgage, home equity, past due loans, foreign banks and certain commercial real estate;

(3) Higher risk weighting for mortgage servicing rights and deferred tax assets that are under

certain thresholds as a percent of Tier 1 capial; (4) Incremental capital requirements for stress VaR;

and (5) Derivatives are differentiated between exchange clearing and over-the-counter and the

50% risk-weight cap is removed. The estimated Basel III risk-weighted assets are based upon

the Bancorp’s interpretations of the three draft Federal Register notices proposing enhancements to

the regulatory capital requirements that were published in June of 2012. These amounts are preliminary

and subject to change depending on the adoption of final Basel III capital rules by the

Regulatory Agencies.

For the Three Months Ended

For the Three Months Ended |

22

©

Fifth Third Bank | All Rights Reserved

Regulation G Non-GAAP reconciliation

Fifth Third Bancorp and Subsidiaries

Regulation G Non-GAAP Reconcilation

$ and shares in millions

(unaudited)

2012

2011

2010

2009

Total Bancorp shareholders' equity (U.S. GAAP)

$13,716

$13,201

$14,051

$13,497

Goodwill and certain other intangibles

(2,499)

(2,514)

(2,546)

(2,565)

Unrealized gains

(375)

(470)

(314)

(241)

Qualifying trust preferred securities

810

2,248

2,763

2,763

Other

33

38

11

(26)

Tier I capital

11,685

12,503

13,965

13,428

Less:

Preferred stock

(398)

(398)

(3,654)

(3,609)

Qualifying trust preferred securities

(810)

(2,248)

(2,763)

(2,763)

Qualifying noncontrolling interest in consolidated subsidiaries

(48)

(50)

(30)

-

Tier I common equity (a)

10,429

9,807

7,518

7,056

Risk-weighted assets, determined in accordance with

prescribed regulatory requirements (b)

109,699

104,945

100,561

100,933

Ratio:

Tier I common equity (a) / (b)

9.51%

9.35%

7.48%

6.99%

For the Year Ended |