Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Ally Financial Inc. | v342308_8k.htm |

Ally Financial Inc. Annual Shareholders’ Meeting Contact Ally Investor Relations at (866) 710 - 4623 or investor.relations@ally.com April 25, 2013

2 2013 Ally Annual Shareholders’ Meeting Forward - Looking Statements and Additional Information The following should be read in conjunction with the financial statements, notes and other information contained in the Compa ny’ s Annual Reports on Form 10 - K, Quarterly Reports on Form 10 - Q, and Current Reports on Form 8 - K . In the presentation that follows and related comments by Ally Financial Inc. (“Ally”) management, the use of the words “expect,” “a nticipate,” “estimate,” “forecast,” “initiative,” “objective,” “plan,” “goal,” “project,” “outlook,” “priorities,” “target,” “intend,” “e val uate,” “pursue,” “seek,” “may,” “ would, ” “ could, ” “ should, ” “ believe, ” “ potential, ” “ continue,” , or the negative of these words, or similar expressions is intended to identify forward - looking statements. All statements herein and in related management comments, other than statements of historical fact, including without limitation, statements about future events and financial performance, are forward - looking statements that involve certain risks and uncertainties. While these statements represent Ally’s current judgment on what the future may hold, and Ally believes these judgments are reasonable, these statements are not guarantees of any events or financial results, and Ally’s actual results may differ materially due to nume rou s important factors that are described in the most recent reports on SEC Forms 10 - K and 10 - Q for Ally, each of which may be revised or supplemented in subsequent reports filed with the SEC. Such factors include, among others, the following: maintaining the mutually beneficial relationsh ip between Ally and General Motors (“GM”), and Ally and Chrysler Group LLC (“Chrysler”); the profitability and financial condition of GM and Chrysler; resolution of the Residential Capital, LLC and certain of its subsidiaries; our ability to realize the anticipated benefits associated with being a bank ho ldi ng company, and the increased regulation and restrictions that we are now subject to; the potential for deterioration in the res idu al value of off - lease vehicles; disruptions in the market in which we fund our operations, with resulting negative impact on our liquidity; changes in our accounting assumptions that may require or that result from changes in the accounting rules or their application, which could result in an impact on earnings; changes in the credit ratings of Ally, Chrysler, or GM; changes in economic conditions, currency exchange rates or political sta bility in the markets in which we operate; and changes in the existing or the adoption of new laws, regulations, policies or other activities of go ver nments, agencies and similar organizations (including as a result of the Dodd - Frank Act and Basel III). Investors are cautioned not to place undue reliance on forward - looking statements. Ally undertakes no obligation to update publi cly or otherwise revise any forward - looking statements except where expressly required by law. Reconciliation of non - GAAP financial measures incl uded within this presentation are provided in this presentation. Use of the term “loans” describes products associated with direct and indirect lending activities of Ally’s global operations . T he specific products include retail installment sales contracts, loans, lines of credit, leases or other financing products. The term “originate” ref ers to Ally’s purchase, acquisition or direct origination of various “loan” products .

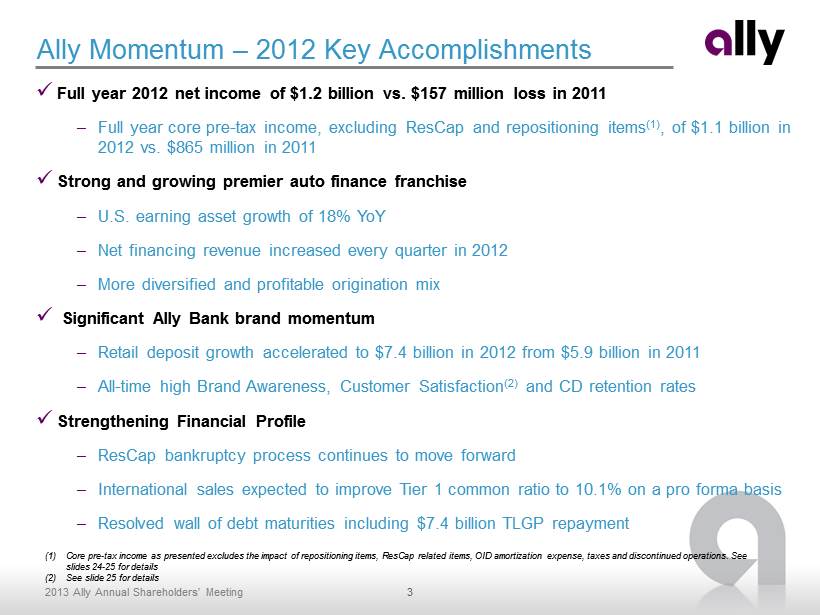

3 2013 Ally Annual Shareholders’ Meeting Ally Momentum – 2012 Key Accomplishments x Full year 2012 net income of $1.2 billion vs. $157 million loss in 2011 – Full year core pre - tax income, excluding ResCap and repositioning items (1) , of $1.1 billion in 2012 vs. $865 million in 2011 x Strong and growing premier auto finance franchise – U.S. earning asset growth of 18% YoY – Net financing revenue increased every quarter in 2012 – More diversified and profitable origination mix x Significant Ally Bank brand momentum – Retail deposit growth accelerated to $7.4 billion in 2012 from $5.9 billion in 2011 – All - time high Brand Awareness, Customer Satisfaction (2) and CD retention rates x Strengthening Financial Profile – ResCap bankruptcy process continues to move forward – International sales expected to improve Tier 1 common ratio to 10.1% on a pro forma basis – Resolved wall of debt maturities including $7.4 billion TLGP repayment (1) Core pre - tax income as presented excludes the impact of repositioning items, ResCap related items, OID amortization expense, tax es and discontinued operations. See slides 24 - 25 for details (2) See slide 25 for details

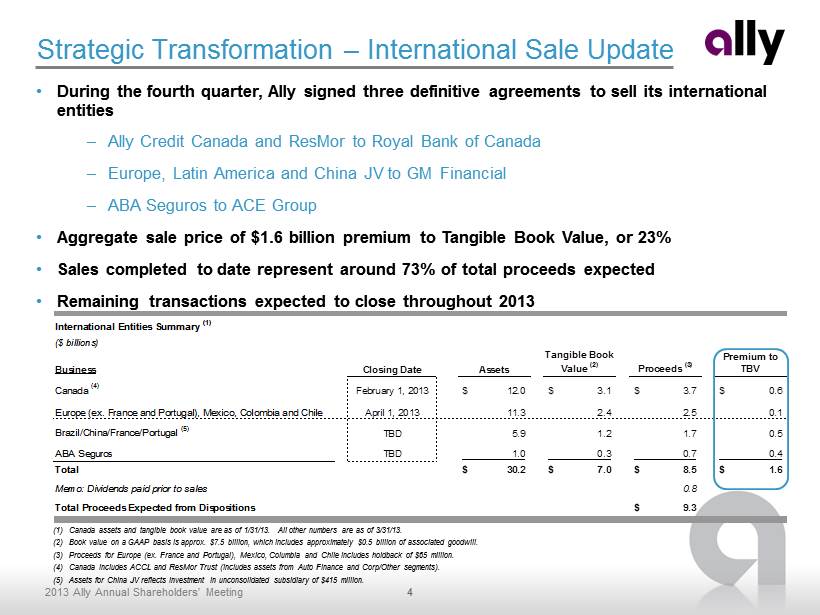

4 2013 Ally Annual Shareholders’ Meeting International Entities Summary (1) ($ billions) Business Closing Date Assets Tangible Book Value (2) Proceeds (3) Premium to TBV Canada (4) February 1, 2013 12.0$ 3.1$ 3.7$ 0.6$ Europe (ex. France and Portugal), Mexico, Colombia and Chile April 1, 2013 11.3 2.4 2.5 0.1 Brazil/China/France/Portugal (5) TBD 5.9 1.2 1.7 0.5 ABA Seguros TBD 1.0 0.3 0.7 0.4 Total 30.2$ 7.0$ 8.5$ 1.6$ Memo: Dividends paid prior to sales 0.8 Total Proceeds Expected from Dispositions 9.3$ Strategic Transformation – International Sale Update • During the fourth quarter, Ally signed three definitive agreements to sell its international entities – Ally Credit Canada and ResMor to Royal Bank of Canada – Europe, Latin America and China JV to GM Financial – ABA Seguros to ACE Group • Aggregate sale price of $1.6 billion premium to Tangible Book Value, or 23% • Sales completed to date represent around 73% of total proceeds expected • Remaining transactions expected to close throughout 2013 (1) Canada assets and tangible book value are as of 1/31/13. All other numbers are as of 3/31/13. (2) Book value on a GAAP basis is approx . $ 7.5 billion, which includes approximately $0.5 billion of associated goodwill. (3) Proceeds for Europe (ex. France and Portugal), Mexico, Columbia and Chile includes holdback of $65 million. (4) Canada includes ACCL and ResMor Trust (includes assets from Auto Finance and Corp/Other segments). (5) Assets for China JV reflects investment in unconsolidated subsidiary of $415 million.

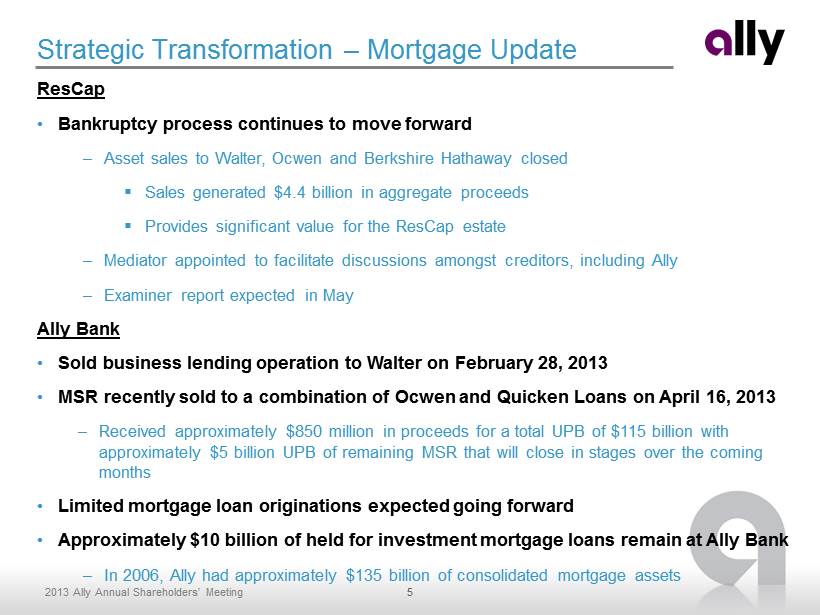

5 2013 Ally Annual Shareholders’ Meeting Strategic Transformation – Mortgage Update ResCap • Bankruptcy process continues to move forward – Asset sales to Walter, Ocwen and Berkshire Hathaway closed ▪ Sales generated $4.4 billion in aggregate proceeds ▪ Provides significant value for the ResCap estate – Mediator appointed to facilitate discussions amongst creditors, including Ally – Examiner report expected in May Ally Bank • Sold business lending operation to Walter on February 28, 2013 • MSR recently sold to a combination of Ocwen and Quicken Loans on April 16, 2013 – Received approximately $850 million in proceeds for a total UPB of $115 billion with approximately $5 billion UPB of remaining MSR that will close in stages over the coming months • Limited mortgage loan originations expected going forward • Approximately $10 billion of held for investment mortgage loans remain at Ally Bank – In 2006, Ally had approximately $135 billion of consolidated mortgage assets

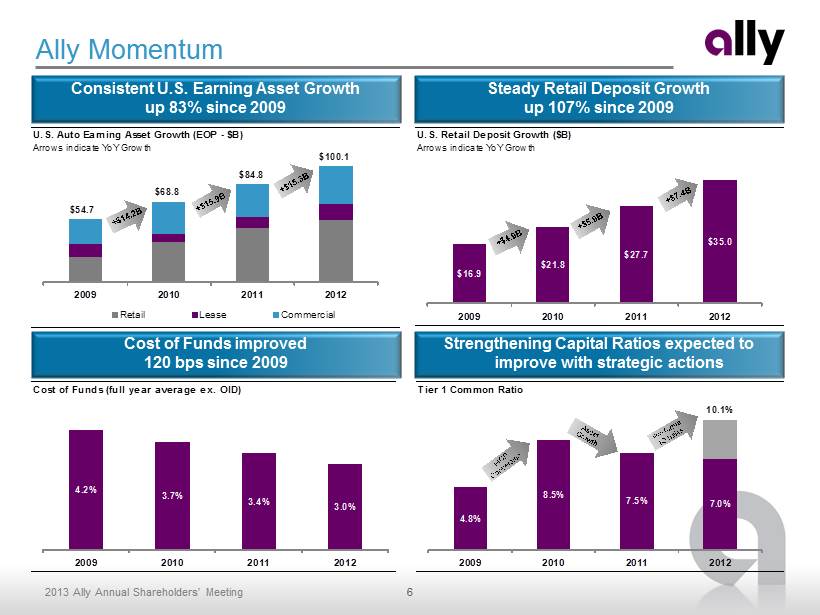

6 2013 Ally Annual Shareholders’ Meeting Ally Momentum Cost of Funds improved 120 bps since 2009 Strengthening Capital Ratios expected to improve with strategic actions Steady Retail Deposit Growth up 107% since 2009 U.S. Auto Earning Asset Growth (EOP - $B) Arrows indicate YoY Growth 2009 2010 2011 2012 Retail Lease Commercial $54.7 $68.8 $84.8 $100.1 Consistent U.S. Earning Asset Growth up 83% since 2009 U.S. Retail Deposit Growth ($B) Arrows indicate YoY Growth $16.9 $21.8 $27.7 $35.0 2009 2010 2011 2012 Cost of Funds (full year average ex. OID) 4.2% 3.7% 3.4% 3.0% 2009 2010 2011 2012 Tier 1 Common Ratio 4.8% 8.5% 7.5% 7.0% 10.1% 2009 2010 2011 2012

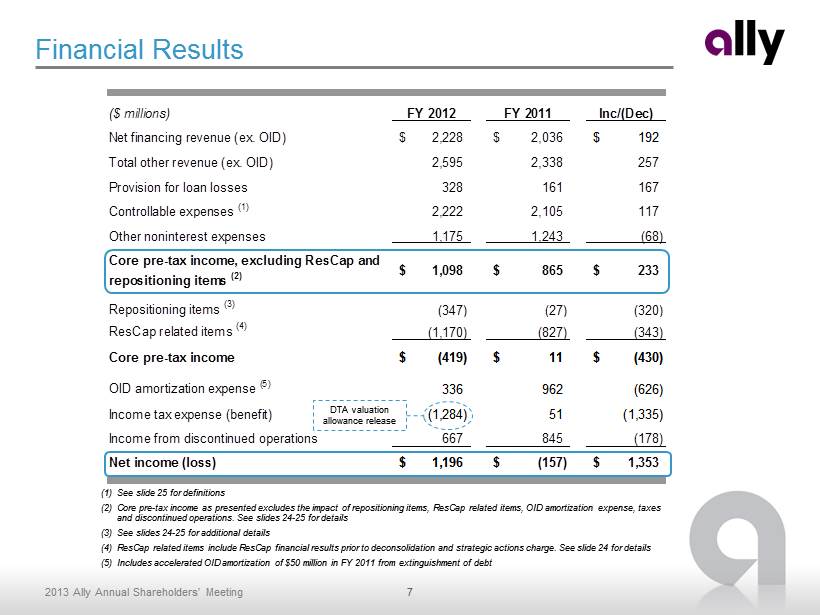

7 2013 Ally Annual Shareholders’ Meeting ($ millions) FY 2012 FY 2011 Inc/(Dec) Net financing revenue (ex. OID) 2,228$ 2,036$ 192$ Total other revenue (ex. OID) 2,595 2,338 257 Provision for loan losses 328 161 167 Controllable expenses (1) 2,222 2,105 117 Other noninterest expenses 1,175 1,243 (68) Core pre-tax income, excluding ResCap and repositioning items (2) 1,098$ 865$ 233$ Repositioning items (3) (347) (27) (320) ResCap related items (4) (1,170) (827) (343) Core pre-tax income (419)$ 11$ (430)$ OID amortization expense (5) 336 962 (626) Income tax expense (benefit) (1,284) 51 (1,335) Income from discontinued operations 667 845 (178) Net income (loss) 1,196$ (157)$ 1,353$ Financial Results (1) See slide 25 for definitions (2) Core pre - tax income as presented excludes the impact of repositioning items, ResCap related items, OID amortization expense, tax es and discontinued operations. See slides 24 - 25 for details (3) See slides 24 - 25 for additional details (4) ResCap related items include ResCap financial results prior to deconsolidation and strategic actions charge. See slide 24 for de tails (5) Includes accelerated OID amortization of $50 million in FY 2011 from extinguishment of debt DTA valuation allowance release

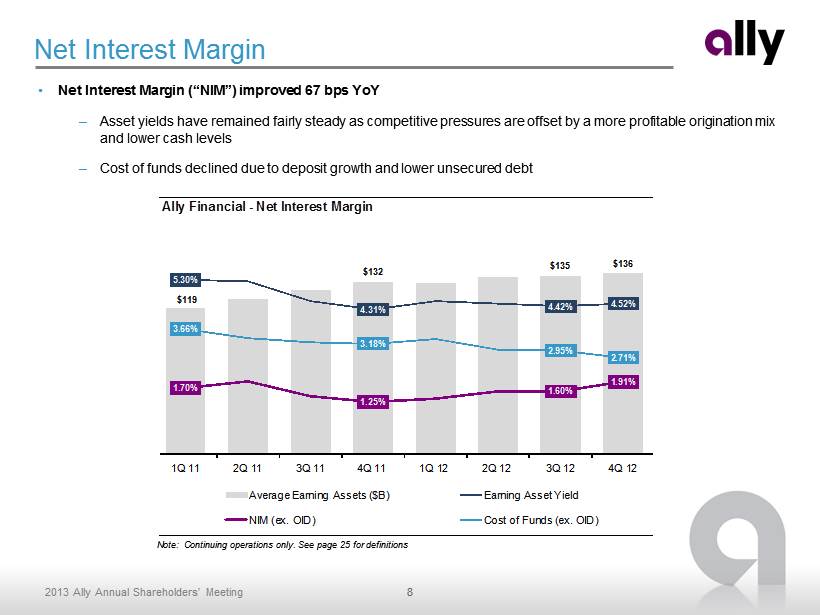

8 2013 Ally Annual Shareholders’ Meeting Ally Financial - Net Interest Margin $119 $132 $135 $136 5.30% 4.31% 4.42% 4.52% 1.70% 1.25% 1.60% 1.91% 3.66% 3.18% 2.95% 2.71% 1Q 11 2Q 11 3Q 11 4Q 11 1Q 12 2Q 12 3Q 12 4Q 12 Average Earning Assets ($B) Earning Asset Yield NIM (ex. OID) Cost of Funds (ex. OID) Net Interest Margin • Net Interest Margin (“NIM”) improved 67 bps YoY – Asset yields have remained fairly steady as competitive pressures are offset by a more profitable origination mix and lower cash levels – Cost of funds declined due to deposit growth and lower unsecured debt Note: Continuing operations only. See page 25 for definitions

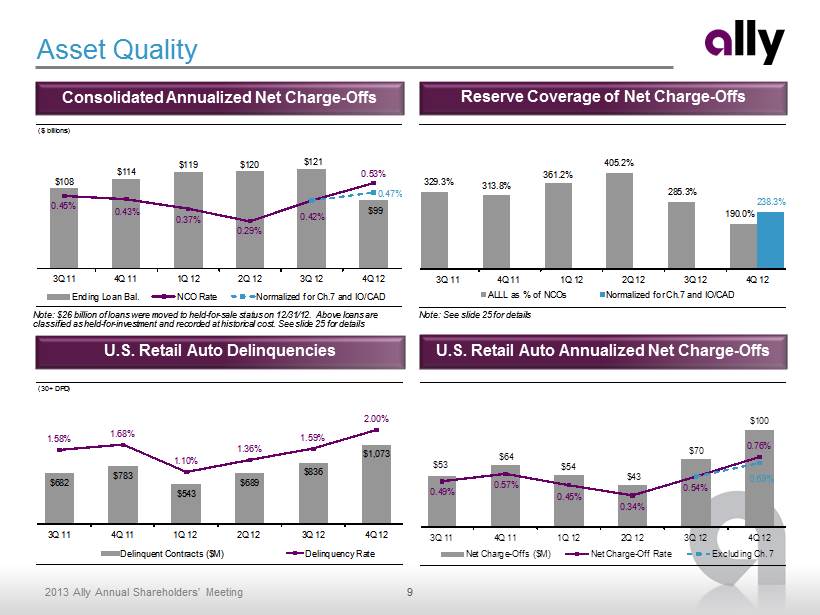

9 2013 Ally Annual Shareholders’ Meeting (30+ DPD) $682 $783 $543 $689 $836 $1,073 1.58% 1.68% 1.10% 1.36% 1.59% 2.00% 3Q 11 4Q 11 1Q 12 2Q 12 3Q 12 4Q 12 Delinquent Contracts ($M) Delinquency Rate Consolidated Annualized Net Charge - Offs Reserve C overage of Net Charge - Offs Asset Quality U.S. Retail Auto Annualized Net Charge - Offs U.S. Retail Auto Delinquencies Note: $26 billion of loans were moved to held - for - sale status on 12/31/12. Above loans are classified as held - for - investment and recorded at historical cost. See slide 25 for details Note: See slide 25 for details $53 $64 $54 $43 $70 $100 0.49% 0.57% 0.45% 0.34% 0.54% 0.76% 0.69% 3Q 11 4Q 11 1Q 12 2Q 12 3Q 12 4Q 12 Net Charge - Offs ($M) Net Charge - Off Rate Excluding Ch. 7 ($ billions) $108 $114 $119 $120 $121 $99 0.45% 0.43% 0.37% 0.29% 0.42% 0.53% 0.47% 3Q 11 4Q 11 1Q 12 2Q 12 3Q 12 4Q 12 Ending Loan Bal. NCO Rate Normalized for Ch.7 and IO/CAD 329.3% 313.8% 361.2% 405.2% 285.3% 190.0% 238.3% 3Q 11 4Q 11 1Q 12 2Q 12 3Q 12 4Q 12 ALLL as % of NCOs Normalized for Ch.7 and IO/CAD

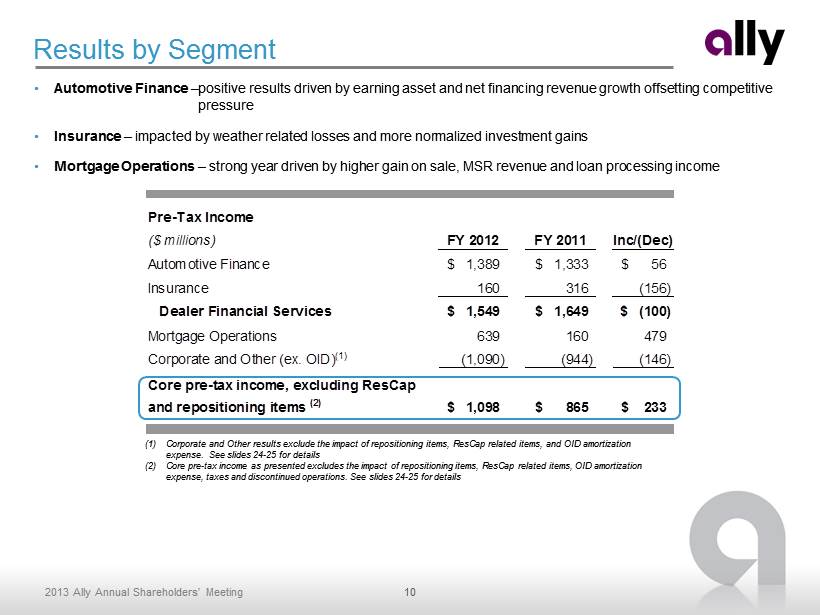

10 2013 Ally Annual Shareholders’ Meeting • Automotive Finance – positive results driven by earning asset and net financing revenue growth offsetting competitive pressure • Insurance – impacted by weather related losses and more normalized investment gains • Mortgage Operations – strong year driven by higher gain on sale, MSR revenue and loan processing income Results by Segment (1) Corporate and Other results exclude the impact of repositioning items, ResCap related items, and OID amortization expense. See slides 24 - 25 for details (2) Core pre - tax income as presented excludes the impact of repositioning items, ResCap related items, OID amortization expense, taxes and discontinued operations. See slides 24 - 25 for details Pre-Tax Income ($ millions) FY 2012 FY 2011 Inc/(Dec) Automotive Finance 1,389$ 1,333$ 56$ Insurance 160 316 (156) Dealer Financial Services 1,549$ 1,649$ (100)$ Mortgage Operations 639 160 479 Corporate and Other (ex. OID) (1) (1,090) (944) (146) Core pre-tax income, excluding ResCap and repositioning items (2) 1,098$ 865$ 233$

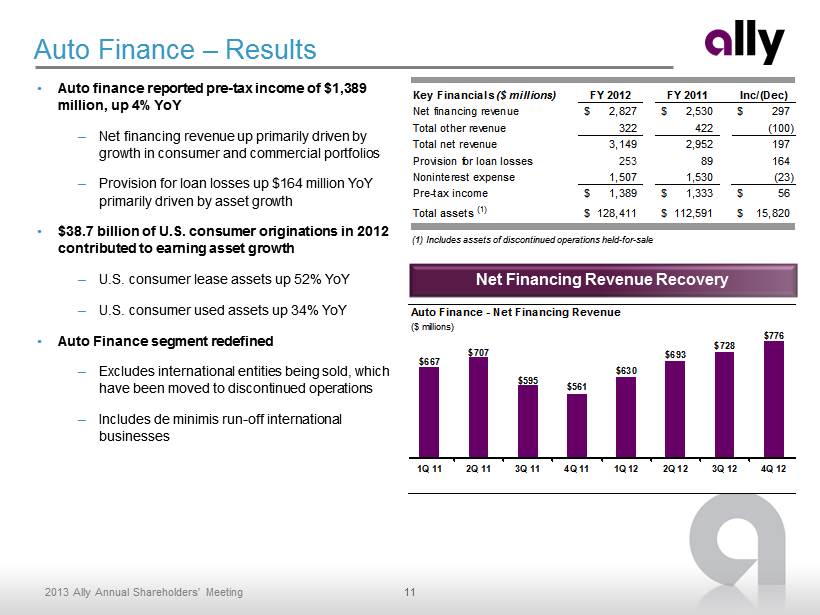

11 2013 Ally Annual Shareholders’ Meeting • Auto finance reported pre - tax income of $1,389 million, up 4% YoY – Net financing revenue up primarily driven by growth in consumer and commercial portfolios – Provision for loan losses up $164 million YoY primarily driven by asset growth • $38.7 billion of U.S. consumer originations in 2012 contributed to earning asset growth – U.S. consumer lease assets up 52% YoY – U.S. consumer used assets up 34% YoY • Auto Finance segment redefined – Excludes international entities being sold, which have been moved to discontinued operations – Includes de minimis run - off international businesses Auto Finance – Results Net Financing Revenue Recovery (1) Includes assets of discontinued operations held - for - sale Key Financials ($ millions) FY 2012 FY 2011 Inc/(Dec) Net financing revenue 2,827$ 2,530$ 297$ Total other revenue 322 422 (100) Total net revenue 3,149 2,952 197 Provision for loan losses 253 89 164 Noninterest expense 1,507 1,530 (23) Pre-tax income 1,389$ 1,333$ 56$ Total assets (1) 128,411$ 112,591$ 15,820$ Auto Finance - Net Financing Revenue ($ millions) $667 $707 $595 $561 $630 $693 $728 $776 1Q 11 2Q 11 3Q 11 4Q 11 1Q 12 2Q 12 3Q 12 4Q 12

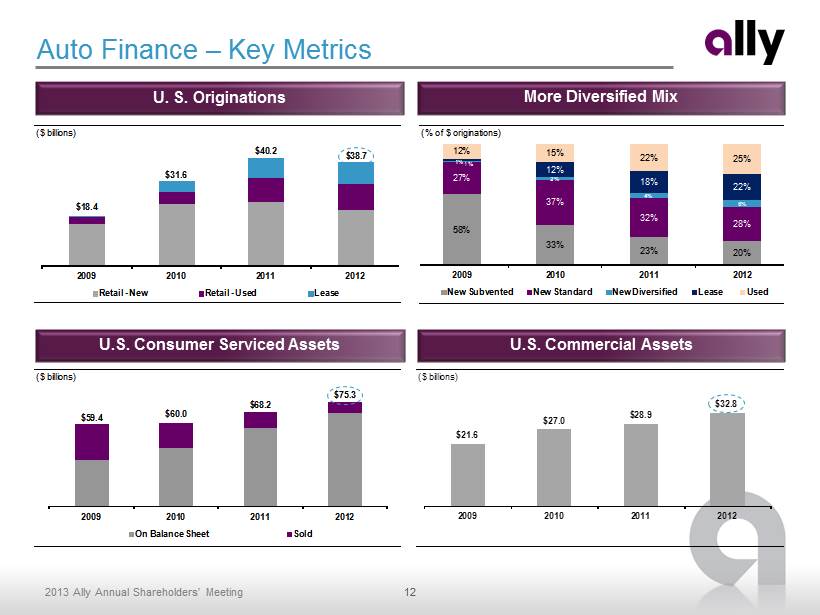

12 2013 Ally Annual Shareholders’ Meeting ($ billions) $21.6 $27.0 $28.9 $32.8 2009 2010 2011 2012 ($ billions) $18.4 $31.6 $40.2 $38.7 0.0 5.0 10.0 15.0 20.0 25.0 30.0 35.0 40.0 45.0 2009 2010 2011 2012 Retail - New Retail - Used Lease ($ billions) $59.4 $60.0 $68.2 $75.3 2009 2010 2011 2012 On Balance Sheet Sold U. S. Originations More Diversified Mix Auto Finance – Key Metrics U.S. Consumer Serviced Assets U.S. Commercial Assets (% of $ originations) 58% 33% 23% 20% 27% 37% 32% 28% 1% 2% 4% 6% 1% 12% 18% 22% 12% 15% 22% 25% 2009 2010 2011 2012 New Subvented New Standard New Diversified Lease Used

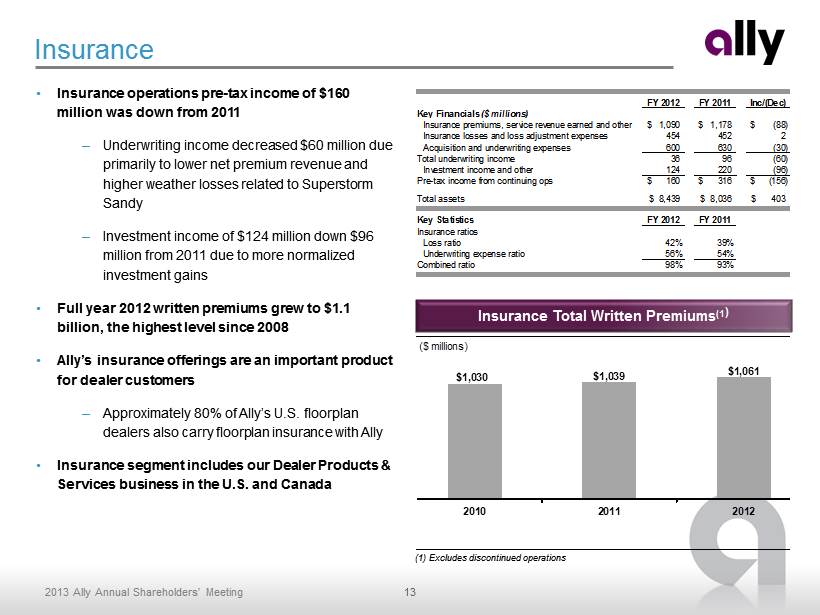

13 2013 Ally Annual Shareholders’ Meeting Insurance • Insurance operations pre - tax income of $160 million was down from 2011 – Underwriting income decreased $60 million due primarily to lower net premium revenue and higher weather losses related to Superstorm Sandy – Investment income of $124 million down $96 million from 2011 due to more normalized investment gains • Full year 2012 written premiums grew to $1.1 billion, the highest level since 2008 • Ally’s insurance offerings are an important product for dealer customers – Approximately 80% of Ally’s U.S. floorplan dealers also carry floorplan insurance with Ally • Insurance segment includes our Dealer Products & Services business in the U.S. and Canada (1) Excludes discontinued operations Insurance Total Written Premiums (1 ) FY 2012 FY 2011 Inc/(Dec) Key Financials ($ millions) Insurance premiums, service revenue earned and other 1,090$ 1,178$ (88)$ Insurance losses and loss adjustment expenses 454 452 2 Acquisition and underwriting expenses 600 630 (30) Total underwriting income 36 96 (60) Investment income and other 124 220 (96) Pre-tax income from continuing ops 160$ 316$ (156)$ Total assets 8,439$ 8,036$ 403$ Key Statistics FY 2012 FY 2011 Insurance ratios Loss ratio 42% 39% Underwriting expense ratio 56% 54% Combined ratio 98% 93% ($ millions) $1,030 $1,039 $1,061 2010 2011 2012

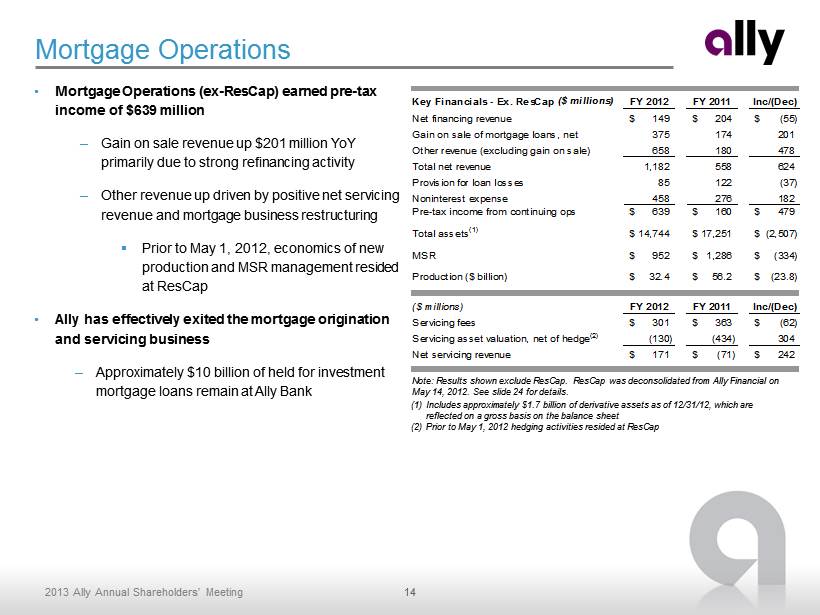

14 2013 Ally Annual Shareholders’ Meeting Mortgage Operations • Mortgage Operations (ex - ResCap) earned pre - tax income of $639 million – Gain on sale revenue up $201 million YoY primarily due to strong refinancing activity – Other revenue up driven by positive net servicing revenue and mortgage business restructuring ▪ Prior to May 1, 2012, economics of new production and MSR management resided at ResCap • Ally has effectively exited the mortgage origination and servicing business – Approximately $10 billion of held for investment mortgage loans remain at Ally Bank Note: Results shown exclude ResCap. ResCap was deconsolidated from Ally Financial on May 14, 2012. See slide 24 for details. (1) Includes approximately $1.7 billion of derivative assets as of 12/31/12, which are reflected on a gross basis on the balance sheet (2) Prior to May 1, 2012 hedging activities resided at ResCap Key Financials - Ex. ResCap ($ millions) FY 2012 FY 2011 Inc/(Dec) Net financing revenue 149$ 204$ (55)$ Gain on sale of mortgage loans, net 375 174 201 Other revenue (excluding gain on sale) 658 180 478 Total net revenue 1,182 558 624 Provision for loan losses 85 122 (37) Noninterest expense 458 276 182 Pre-tax income from continuing ops 639$ 160$ 479$ Total assets (1) 14,744$ 17,251$ (2,507)$ MSR 952$ 1,286$ (334)$ Production ($ billion) 32.4$ 56.2$ (23.8)$ TRUE ($ millions) FY 2012 FY 2011 Inc/(Dec) Servicing fees 301$ 363$ (62)$ Servicing asset valuation, net of hedge (2) (130) (434) 304 Net servicing revenue 171$ (71)$ 242$

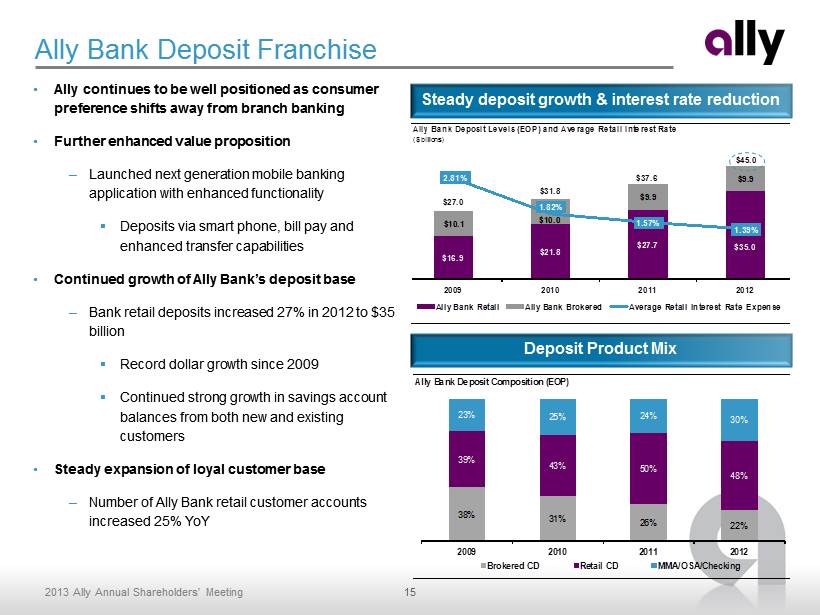

15 2013 Ally Annual Shareholders’ Meeting Ally Bank Deposit Levels (EOP) and Average Retail Interest Rate ($ billions) $16.9 $21.8 $27.7 $35.0 $10.1 $10.0 $9.9 $9.9 $27.0 $31.8 $37.6 $45.0 2.81% 1.82% 1.57% 1.39% 2009 2010 2011 2012 Ally Bank Retail Ally Bank Brokered Average Retail Interest Rate Expense Ally Bank Deposit Franchise • Ally continues to be well positioned as consumer preference shifts away from branch banking • Further enhanced value proposition – Launched next generation mobile banking application with enhanced functionality ▪ Deposits via smart phone, bill pay and enhanced transfer capabilities • Continued growth of Ally Bank’s deposit base – Bank retail deposits increased 27% in 2012 to $35 billion ▪ Record dollar growth since 2009 ▪ Continued strong growth in savings account balances from both new and existing customers • Steady expansion of loyal customer base – Number of Ally Bank retail customer accounts increased 25% YoY Steady deposit growth & interest rate reduction Deposit Product Mix Ally Bank Deposit Composition (EOP) 38% 31% 26% 22% 39% 43% 50% 48% 23% 25% 24% 30% 2009 2010 2011 2012 Brokered CD Retail CD MMA/OSA/Checking

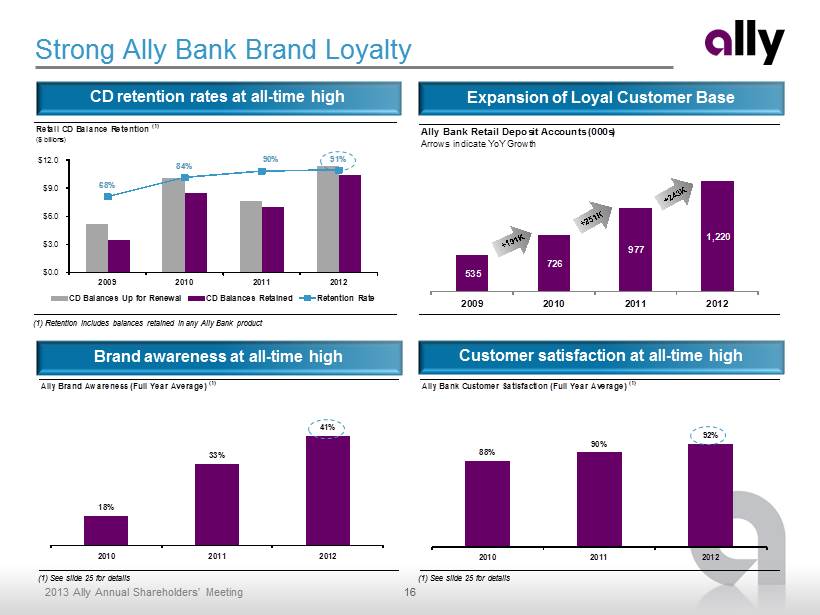

16 2013 Ally Annual Shareholders’ Meeting Ally Bank Customer Satisfaction (Full Year Average) (1) 88% 90% 92% 2010 2011 2012 Retail CD Balance Retention (1) ($ billions) 68% 84% 90% 91% $0.0 $3.0 $6.0 $9.0 $12.0 2009 2010 2011 2012 CD Balances Up for Renewal CD Balances Retained Retention Rate Ally Brand Awareness (Full Year Average) (1) 18% 33% 41% 2010 2011 2012 Strong Ally Bank Brand Loyalty Customer satisfaction at all - time high CD retention rates at all - time high Brand awareness at all - time high (1) Retention includes balances retained in any Ally Bank product (1) See slide 25 for details (1) See slide 25 for details Ally Bank Retail Deposit Accounts (000s) Arrows indicate YoY Growth 535 726 977 1,220 2009 2010 2011 2012 Expansion of Loyal Customer Base

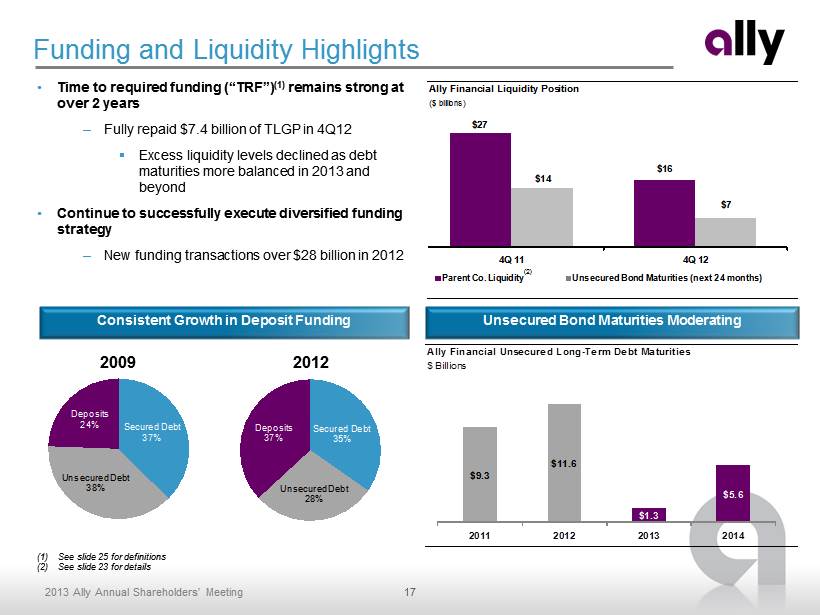

17 2013 Ally Annual Shareholders’ Meeting Ally Financial Liquidity Position ($ billions) $27 $16 $14 $7 4Q 11 4Q 12 Parent Co. Liquidity Unsecured Bond Maturities (next 24 months) Secured Debt 35% Unsecured Debt 28% Deposits 37% Secured Debt 37% Unsecured Debt 38% Deposits 24% • Time to required funding (“TRF”) (1) remains strong at over 2 years – Fully repaid $7.4 billion of TLGP in 4Q12 ▪ Excess liquidity levels declined as debt maturities more balanced in 2013 and beyond • Continue to successfully execute diversified funding strategy – New funding transactions over $28 billion in 2012 Funding and Liquidity Highlights (1) See slide 25 for definitions (2) See slide 23 for details (2) Unsecured Bond Maturities Moderating Ally Financial Unsecured Long-Term Debt Maturities $ Billions $9.3 $11.6 $1.3 $5.6 2011 2012 2013 2014 2009 2012 Consistent Growth in Deposit Funding

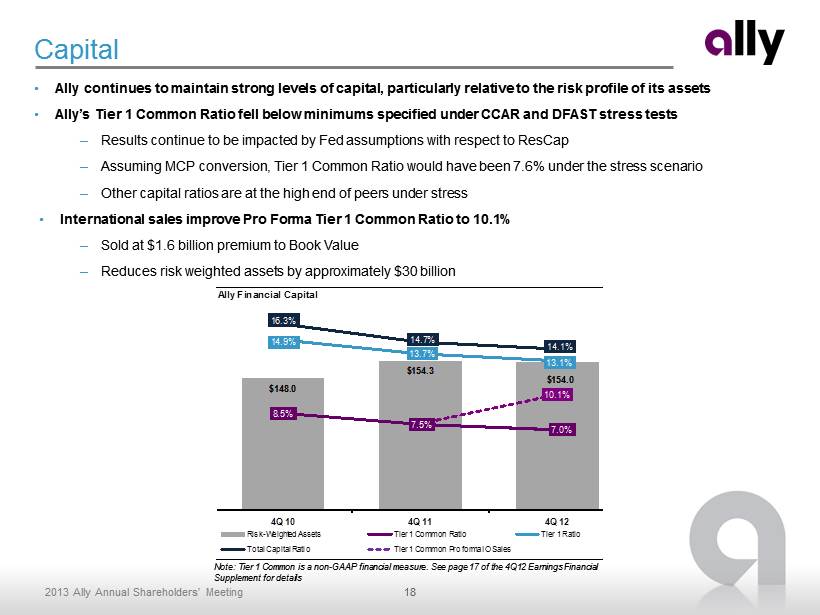

18 2013 Ally Annual Shareholders’ Meeting Capital • Ally continues to maintain strong levels of capital, particularly relative to the risk profile of its assets • Ally’s Tier 1 Common Ratio fell below minimums specified under CCAR and DFAST stress tests – Results continue to be impacted by Fed assumptions with respect to ResCap – Assuming MCP conversion, Tier 1 Common Ratio would have been 7.6% under the stress scenario – Other capital ratios are at the high end of peers under stress • International sales improve Pro Forma Tier 1 Common Ratio to 10.1% – Sold at $1.6 billion premium to Book Value – Reduces risk weighted assets by approximately $30 billion Note: Tier 1 Common is a non - GAAP financial measure. See page 17 of the 4Q12 Earnings Financial Supplement for details Ally Financial Capital $148.0 $154.3 $154.0 8.5% 7.5% 7.0% 14.9% 13.7% 13.1% 16.3% 14.7% 14.1% 10.1% 4Q 10 4Q 11 4Q 12 Risk - Weighted Assets Tier 1 Common Ratio Tier 1 Ratio Total Capital Ratio Tier 1 Common Pro forma IO Sales

19 2013 Ally Annual Shareholders’ Meeting 2013 Priorities • Complete strategic transformation and capitalize on momentum created in 2012 • Continue to create significant value for our auto dealers – Comprehensive products and services – Continue to innovate – Focus on expanding profitable dealer relationships, not market share • Stable deposit growth at Ally Bank • Establish path towards double - digit ROE – Continue cost of funds reduction ▪ Explore opportunities to accelerate trajectory – Improve business efficiencies and reduce noninterest expense – Regulatory environment • Repay U.S. Treasury Momentum created in 2012 positions Ally for additional strides in 2013

Supplemental Charts

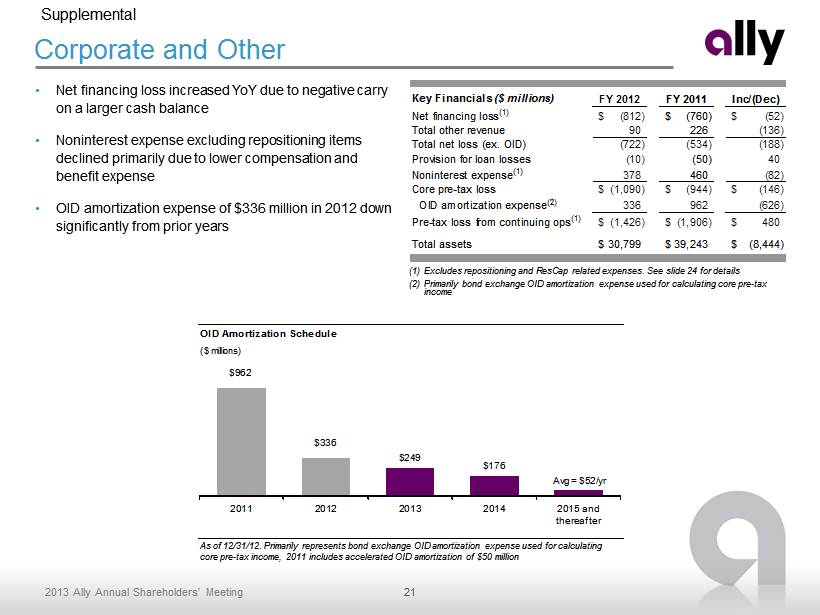

21 2013 Ally Annual Shareholders’ Meeting Key Financials ($ millions) FY 2012 FY 2011 Inc/(Dec) Net financing loss (1) (812)$ (760)$ (52)$ Total other revenue 90 226 (136) Total net loss (ex. OID) (722) (534) (188) Provision for loan losses (10) (50) 40 Noninterest expense (1) 378 460 (82) Core pre-tax loss (1,090)$ (944)$ (146)$ OID amortization expense (2) 336 962 (626) Pre-tax loss from continuing ops (1) (1,426)$ (1,906)$ 480$ Total assets 30,799$ 39,243$ (8,444)$ Corporate and Other • Net financing loss increased YoY due to negative carry on a larger cash balance • Noninterest expense excluding repositioning items declined primarily due to lower compensation and benefit expense • OID amortization expense of $336 million in 2012 down significantly from prior years Supplemental (1) Excludes repositioning and ResCap related expenses. See slide 24 for details (2) Primarily bond exchange OID amortization expense used for calculating core pre - tax income As of 12/31/12. Primarily represents bond exchange OID amortization expense used for calculating core pre - tax income, 2011 includes accelerated OID amortization of $50 million OID Amortization Schedule ($ millions) $962 $336 $249 $176 Avg = $52/yr 2011 2012 2013 2014 2015 and thereafter

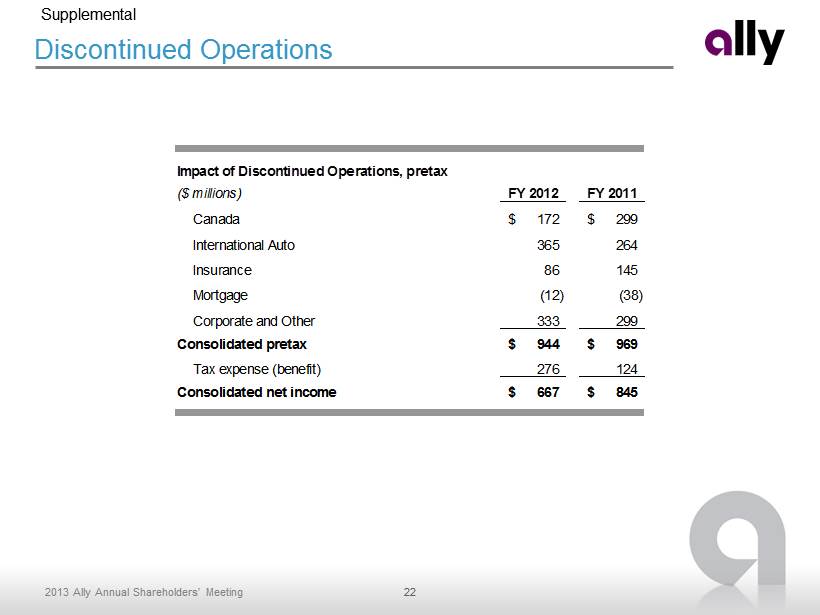

22 2013 Ally Annual Shareholders’ Meeting Discontinued Operations Supplemental Impact of Discontinued Operations, pretax ($ millions) FY 2012 FY 2011 Canada 172$ 299$ International Auto 365 264 Insurance 86 145 Mortgage (12) (38) Corporate and Other 333 299 Consolidated pretax 944$ 969$ Tax expense (benefit) 276 124 Consolidated net income 667$ 845$

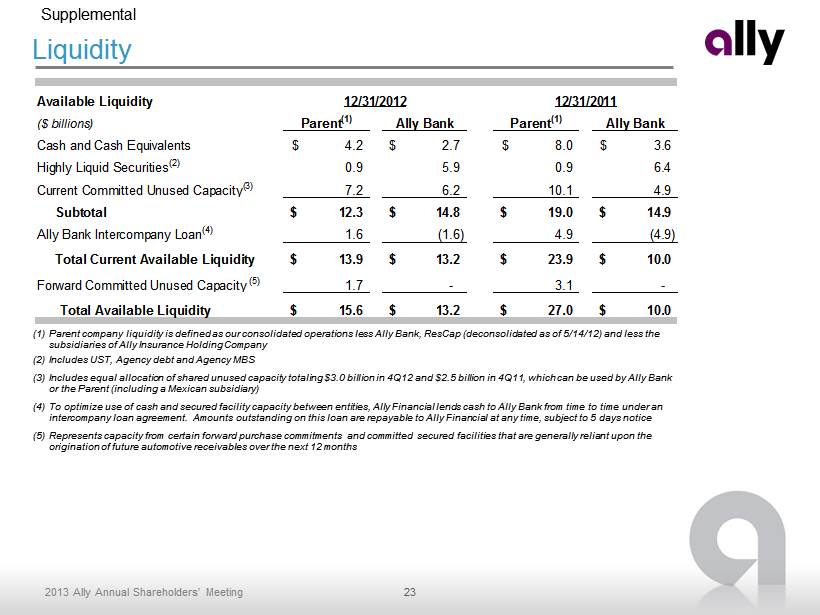

23 2013 Ally Annual Shareholders’ Meeting Liquidity Supplemental (1) Parent company liquidity is defined as our consolidated operations less Ally Bank, ResCap (deconsolidated as of 5/14/12) and les s the subsidiaries of Ally Insurance Holding Company (2) Includes UST, Agency debt and Agency MBS (3) Includes equal allocation of shared unused capacity totaling $3.0 billion in 4Q12 and $2.5 billion in 4Q11, which can be used by Ally Bank or the Parent (including a Mexican subsidiary) (4) To optimize use of cash and secured facility capacity between entities, Ally Financial lends cash to Ally Bank from time to time un der an intercompany loan agreement. Amounts outstanding on this loan are repayable to Ally Financial at any time, subject to 5 days notice (5) Represents capacity from certain forward purchase commitments and committed secured facilities that are generally reliant upo n t he origination of future automotive receivables over the next 12 months Available Liquidity 12/31/2012 12/31/2011 ($ billions) Parent (1) Ally Bank Parent (1) Ally Bank Cash and Cash Equivalents 4.2$ 2.7$ 8.0$ 3.6$ Highly Liquid Securities (2) 0.9 5.9 0.9 6.4 Current Committed Unused Capacity (3) 7.2 6.2 10.1 4.9 Subtotal 12.3$ 14.8$ 19.0$ 14.9$ Ally Bank Intercompany Loan (4) 1.6 (1.6) 4.9 (4.9) SubtotalTotal Current Available Liquidity 13.9$ 13.2$ 23.9$ 10.0$ Forward Committed Unused Capacity (5) 1.7 - 3.1 - Total Available Liquidity 15.6$ 13.2$ 27.0$ 10.0$

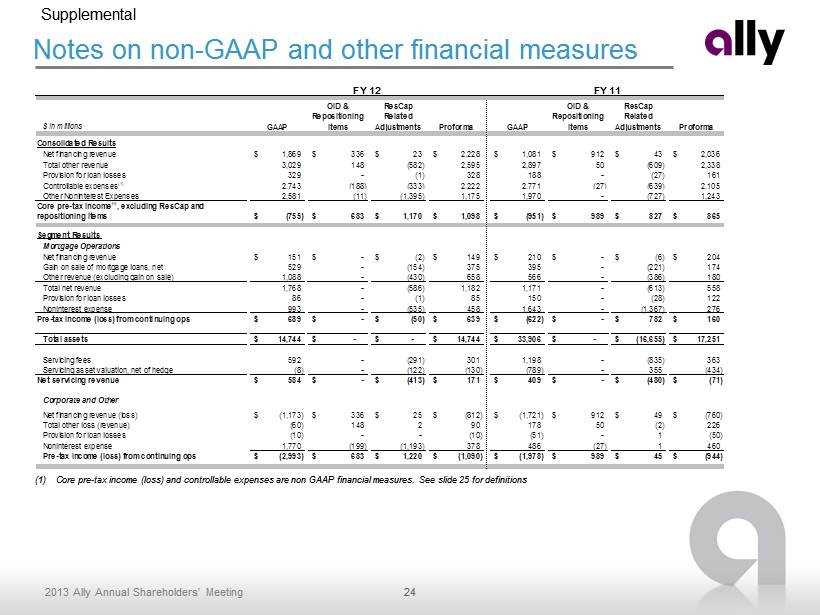

24 2013 Ally Annual Shareholders’ Meeting Notes on non - GAAP and other financial measures Supplemental (1) Core pre - tax income (loss) and controllable expenses are non GAAP financial measures. See slide 25 for definitions $ in millions GAAP OID & Repositioning Items ResCap Related Adjustments Proforma GAAP OID & Repositioning Items ResCap Related Adjustments Proforma Consolidated Results Net financing revenue 1,869$ 336$ 23$ 2,228$ 1,081$ 912$ 43$ 2,036$ Total other revenue 3,029 148 (582) 2,595 2,897 50 (609) 2,338 Provision for loan losses 329 - (1) 328 188 - (27) 161 Controllable expenses(1) 2,743 (188) (333) 2,222 2,771 (27) (639) 2,105 Other Noninterest Expenses 2,581 (11) (1,395) 1,175 1,970 - (727) 1,243 Core pre-tax income(1), excluding ResCap and repositioning items (755)$ 683$ 1,170$ 1,098$ (951)$ 989$ 827$ 865$ Segment Results Mortgage Operations Net financing revenue 151$ -$ (2)$ 149$ 210$ -$ (6)$ 204$ Gain on sale of mortgage loans, net 529 - (154) 375 395 - (221) 174 Other revenue (excluding gain on sale) 1,088 - (430) 658 566 - (386) 180 Total net revenue 1,768 - (586) 1,182 1,171 - (613) 558 Provision for loan losses 86 - (1) 85 150 - (28) 122 Noninterest expense 993 - (535) 458 1,643 - (1,367) 276 Pre-tax income (loss) from continuing ops 689$ -$ (50)$ 639$ (622)$ -$ 782$ 160$ Total assets 14,744$ -$ -$ 14,744$ 33,906$ -$ (16,655)$ 17,251$ Servicing fees 592 - (291) 301 1,198 - (835) 363 Servicing asset valuation, net of hedge (8) - (122) (130) (789) - 355 (434) Net servicing revenue 584$ -$ (413)$ 171$ 409$ -$ (480)$ (71)$ Corporate and Other Net financing revenue (loss) (1,173)$ 336$ 25$ (812)$ (1,721)$ 912$ 49$ (760)$ Total other loss (revenue) (60) 148 2 90 178 50 (2) 226 Provision for loan losses (10) - - (10) (51) - 1 (50) Noninterest expense 1,770 (199) (1,193) 378 486 (27) 1 460 Pre-tax income (loss) from continuing ops (2,993)$ 683$ 1,220$ (1,090)$ (1,978)$ 989$ 45$ (944)$ FY 12 FY 11

25 2013 Ally Annual Shareholders’ Meeting Notes on non - GAAP and other financial measures Supplemental 1) Core pre - tax income (loss) is a non - GAAP financial measure. It is defined as income (loss) from continuing operations before taxes and primarily bond exchange original issue discount ("OID") amortization expense . 2) Repositioning Items for 4Q12 include: ($94) million for legacy pension and compensation expense resulting from the company’s strategic decision t o d e - risk its long - term pension liability through lump - sum buy - outs and annuity placements for former subsidiaries; ($148) million incurre d for the early prepayment of certain Federal Home Loan Bank (FHLB) debt to further reduce Ally’s funding costs; and ($46) million in legal, advisory fees, an d other expenses related to the ResCap bankruptcy and disposition of our International Operations. 3) Time to required funding (“TRF”) is a liquidity risk measure expressed as the number of months that Ally Financial can meet its ongoing liquidity needs as they arise without issuing unsecured debt. The TRF metric assumes that auto asset growth projections remain unchanged and tha t t he auto ABS markets remain open. 4) Corporate and Other primarily consists of Ally’s centralized treasury activities, the residual impacts of the company’s corporate funds transfer pri cing and asset liability management activities, and the amortization of the discount associated with new debt issuances and bond excha nge s. Corporate and Other also includes the Commercial Finance business, certain equity investments and reclassifications, eliminations between the reportab le operating segments, and overhead previously allocated to operations that have since been sold or discontinued. 5) Controllable expenses include employee related costs, consulting and legal fees, marketing, information technology, facility, portfolio servicing a nd restructuring expenses. 6) Net interest margin (“NIM”) and cost of funds (“COF”) exclude OID amortization expense. 7) U.S. consumer auto originations ▪ New Subvented – subvented rate new vehicle loans from GM and Chrysler dealers ▪ New Standard – standard rate new vehicle loans from GM and Chrysler dealers ▪ New Diversified – new vehicle loans from non - GM/Chrysler dealers ▪ Lease – new vehicle lease originations from all dealers ▪ Used – used vehicle loans from all dealers 8) Net charge - off ratios are calculated as annualized net charge - offs divided by average outstanding finance receivables and loans excluding loans measur ed at fair value and loans held - for - sale. 9) Allowance coverage ratios are based on the allowance for loan losses related to loans held - for - investment excluding those loans held at fair value as a percentage of the unpaid principal balance, net of premiums and discounts . 10) Brand Awareness is a measure of Ally Bank recognition in the marketplace, measured by TNS Custom Research, a third party market research firm . 11) Customer Satisfaction is measured via an online banking survey presented to Ally Bank customers.