Attached files

| file | filename |

|---|---|

| EX-31.2 - EX-31.2 - FREEPORT-MCMORAN INC | d523624dex312.htm |

| EX-31.1 - EX-31.1 - FREEPORT-MCMORAN INC | d523624dex311.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

Amendment No. 1

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2012

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 001-11307-01

Freeport-McMoRan Copper & Gold Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 74-2480931 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| 333 North Central Avenue Phoenix, Arizona |

85004-2189 | |

| (Address of principal executive offices) | (Zip Code) | |

(602) 366-8100

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock, par value $0.10 per share | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. x Yes ¨ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period than the registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

| x | Large accelerated filer | ¨ | Accelerated filer | |||

| ¨ | Non-accelerated filer | ¨ | Smaller reporting company |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ¨ Yes x No

The aggregate market value of common stock held by non-affiliates of the registrant was $31.1 billion on March 22, 2013, and $32.1 billion on June 29, 2012.

Common stock issued and outstanding was 949,739,265 shares on March 22, 2013, and 949,186,881 shares on June 29, 2012.

DOCUMENTS INCORPORATED BY REFERENCE

None

Table of Contents

EXPLANATORY NOTE

Freeport-McMoRan Copper & Gold Inc. (the Company or FCX) is filing this Amendment No. 1 (this Amendment) to its Annual Report on Form 10-K for the fiscal year ended December 31, 2012 (the Form 10-K) previously filed with the Securities and Exchange Commission (SEC) on February 22, 2013 for the purpose of amending Part III of the Form 10-K to include the information that was to be incorporated by reference to its definitive proxy statement relating to its 2013 Annual Meeting. There are no other changes to the Registrant’s Form 10-K. As a result of this Amendment, Part IV of the Form 10-K is being amended solely to add as exhibits certain new certifications in accordance with Rule 13a-14(a) promulgated by the SEC under the Securities Exchange Act of 1934, as amended, with paragraphs 3, 4 and 5 omitted since no financial statements are contained within this Amendment. Because no financial statements are contained within this Amendment, the Company also is not including certifications pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 nor any disclosure with respect to Items 307 or 308 of Regulation S-K.

Except as otherwise expressly stated herein, this Amendment does not reflect events occurring after the date of the Form 10-K nor does it modify or update the disclosure contained in the Form 10-K in any way other than as required to reflect the amendments to Part III discussed above and reflected below. Accordingly, this Amendment should be read in conjunction with our Form 10-K and our other filings made with the SEC subsequent to the filing of the Form 10-K.

As used in this Amendment, when the Company refers to “us”, “we”, “our”, “ours”, “the company”, or “FCX”, the Company is describing Freeport-McMoRan Copper & Gold Inc. and/or its consolidated subsidiaries.

Table of Contents

| Page | ||||||

| Part III | ||||||

| Item 10. |

Directors, Executive Officers and Corporate Governance | 1 | ||||

| Item 11. |

Executive Compensation | 9 | ||||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 43 | ||||

| Item 13. |

Certain Relationships and Related Transactions, and Director Independence | 46 | ||||

| Item 14. |

Principal Accounting Fees and Services | 47 | ||||

| Part IV | ||||||

| Item 15. |

Exhibits, Financial Statement Schedules | 49 | ||||

| S-1 | ||||||

| E-1 | ||||||

Table of Contents

Item 10. Directors, Executive Officers and Corporate Governance.

The information required by Item 10 regarding our executive officers appeared in a separately captioned heading after Item 4 in Part I of our Annual Report on Form 10-K for the fiscal year ended December 31, 2012 filed with the SEC on February 22, 2013, which information is incorporated herein by reference.

Information About Directors

The following table provides certain information as of March 1, 2013, with respect to each director, including information regarding the person’s business experience, director positions with other public companies held currently or at any time during the last five years, and the experiences, qualifications, attributes or skills that caused our nominating and corporate governance committee and the board to determine that the person should be nominated to serve as a director of the company. Unless otherwise indicated, each person has been engaged in the principal occupation shown for the past five years. Each director was elected to serve a one-year term at our 2012 annual meeting of stockholders held on June 14, 2012.

| Name of Director |

Age |

Principal Occupation, Business Experience, and Other Public Company Directorships |

Year First | |||

| Richard C. Adkerson |

66 | Chief Executive Officer of the company since December 2003. President of the company since January 2008 and from April 1997 to March 2007. Chief Financial Officer of the company from October 2000 to December 2003. Current Co-Chairman of the Board of McMoRan Exploration Co. (McMoRan). President and Chief Executive Officer of McMoRan from 1998 to 2004. Vice Chairman of Freeport-McMoRan Inc. from 1995 to 1997. Chairman, Chief Executive Officer & President of Stratus Properties Inc. from 1992 to 1998. Partner in Arthur Andersen & Co. where he served as a Managing Director and head of the firm’s global oil and gas industry services from 1978 to 1989. Professional Accounting Fellow with the Securities and Exchange Commission and Presidential Exchange Executive from 1976 to 1978. Holds B.S. in Accounting with highest honors and M.B.A. from Mississippi State University and completed Advanced Management Program at Harvard Business School. |

2006 | |||

| Mr. Adkerson is an experienced business leader making him highly qualified to serve as a member of the board of directors. As Chief Executive Officer and President, he is responsible for the executive management of the company. He has demonstrated exceptional leadership abilities in developing and executing a financial strategy that has benefited our stockholders, and in building an operational, financial and administrative organization that efficiently supports our business. Mr. Adkerson is recognized as a mining industry leader, having served as past Chairman of the International Council on Mining and Metals and on the Executive Board of the International Copper Association. |

||||||

1

Table of Contents

| Name of Director |

Age |

Principal Occupation, Business Experience, and Other Public Company Directorships |

Year First | |||

| Robert J. Allison, Jr. |

74 | Retired Chairman of the Board and Chief Executive Officer of Anadarko Petroleum Corporation. Chairman of the Board of Anadarko Petroleum Corporation from 1986 to 2005. President and Chief Executive Officer of Anadarko Petroleum Corporation from 1979 to 2002 and March 2003 to December 2003. Holds B.S. in Petroleum Engineering from The University of Kansas. Former director of Anadarko Petroleum Corporation. |

2001 | |||

| Mr. Allison’s experience serving as the former President and Chief Executive Officer and Chairman of the Board of one of the largest independent oil and gas exploration and production companies in the world provides him with a wealth of knowledge in dealing with operational, strategic, financial, regulatory and international matters at the board level. His business and board experience make him highly qualified to serve as the chairman of our nominating and corporate governance committee. |

||||||

| Robert A. Day |

69 | Chairman of the Board and founder of Trust Company of the West, an investment management company and one of the largest independent trust companies in the U.S. Chairman of Oakmont Corporation, a registered investment advisor. Chairman and Chief Executive Officer of W. M. Keck Foundation, a national philanthropic organization. Holds B.S. in Economics from Claremont McKenna College. Current director of McMoRan. Former director of Société Générale. |

1995 | |||

| Mr. Day is an experienced entrepreneur and financial leader with the skills necessary to serve on the board of directors and to lead our audit committee. With his background in economics and extensive experience in the financial services industry, Mr. Day is well-versed in accounting standards and regulations, and is equipped to evaluate financial results and generally oversee the financial reporting process of a large corporation. Mr. Day brings significant business and finance experience to the board and provides insight into strategies and solutions to address an increasingly complex business environment. |

||||||

2

Table of Contents

| Name of Director |

Age |

Principal Occupation, Business Experience, and Other Public Company Directorships |

Year First | |||

| Gerald J. Ford |

68 | Principal Shareholder and Chairman of the Board of Hilltop Holdings Inc. since August 2007, and a director of Hilltop Holdings Inc. since June 2005. General Partner of Ford Financial Fund, L.P., a private equity firm, from January 2010 to present. Chairman of the Board and Chief Executive Officer of Golden State Bancorp, Inc. and its wholly owned subsidiary, California Federal Bank, FSB, a Federal Savings Bank, from 1998 through its 2002 merger with Citigroup Inc. Chairman of the Board of First Acceptance Corporation from 1996 to 2010 and Chief Executive Officer of First Acceptance Corporation from 1996 to 2002. Holds B.A. in Economics and J.D. from Southern Methodist University. Current director of McMoRan, Hilltop Holdings Inc., SWS Group, Inc. and Scientific Games Corporation. Former director of First Acceptance Corporation, Liberté Investors, Inc., Americredit Corp., Affordable Residential Communities, Inc. and Pacific Capital Bancorp. |

2000 | |||

| Mr. Ford is a banking and financial institutions entrepreneur who has been involved in numerous mergers and acquisitions of private and public sector financial institutions, primarily in the Southwestern United States, over the past 30 years. In that capacity, he acquired and consolidated 30 commercial banks from 1975 to 1993, forming First United Bank Group, Inc., a multi-bank holding company for which he functioned as Chairman of the Board and Chief Executive Officer until its sale in 1994. During this period, he also led investment consortiums that acquired numerous financial institutions, forming in succession, First Gibraltar Bank, FSB, First Madison Bank, FSB and First Nationwide Bank. His extensive banking industry experience and educational background provide him with significant knowledge in dealing with financial, accounting and regulatory matters, making him a valuable member of the board of directors. In addition, his service on the board of directors and audit and corporate governance committees of a variety of public companies gives him a deep understanding of the role of the board and positions him well to serve as a member of our nominating and corporate governance and our audit committees. |

||||||

3

Table of Contents

| Name of Director |

Age |

Principal Occupation, Business Experience, and Other Public Company Directorships |

Year First | |||

| H. Devon Graham, Jr. |

78 | President of R. E. Smith Interests, an asset management company, from 1997 to present. U.S. Regional Managing Partner, Arthur Andersen from 1985 to 1997. Chairman of the Board of Partners of Arthur Andersen from 1984 to 1986. Holds B.S. in Accounting from Mississippi State University. Current director of McMoRan. |

2000 | |||

| Mr. Graham has over 40 years of experience in public accounting and has served in various leadership positions with an international accounting firm, including Chairman of the Board of Partners, member of the Worldwide Executive Committee, U.S. Regional Managing Partner, member of the U.S. Leadership Committee and Chairman of the Industry Steering Committee, making him a valuable member of the board of directors and our audit committee as well as chair of our compensation committee. In addition, Mr. Graham brings invaluable management and administrative experience as President of an asset management company. His experience provides him with the necessary skills to lead our compensation committee. |

||||||

| Charles C. Krulak |

70 | President of Birmingham-Southern College from March 2011 to present. Former Commandant, United States Marine Corps, the Marine Corps’ highest-ranking officer. Retired from United States Marine Corps in 1999 after serving 35 years. Executive Vice Chairman and Head of Mergers and Acquisitions of MBNA Corp., a financial services company, from March 2004 to June 2005. Chief Executive Officer of MBNA Europe Bank, Ltd. from January 2001 to March 2004, and Senior Vice Chairman of MBNA America Bank, N.A. from 1999 to 2001. Holds B.S. in Engineering from U.S. Naval Academy and M.S. in Labor Relations from George Washington University. Current director of Union Pacific Corporation and the Aston Villa Football Club, U.K. Former director of ConocoPhillips and Phelps Dodge Corporation. |

2007 | |||

| As a retired Commandant of the United States Marine Corps, General Krulak brings a unique perspective to the board. His successful record of leadership and military service makes him highly suited to understand and oversee the complex managerial, strategic and international considerations addressed by the board. In addition, General Krulak’s service on the boards of other public companies allows him to provide the board with a variety of insights. |

||||||

4

Table of Contents

| Name of Director |

Age |

Principal Occupation, Business Experience, and Other Public Company Directorships |

Year First | |||

| Bobby Lee Lackey |

75 | Consultant. President and Chief Executive Officer of McManus-Wyatt-Hidalgo Produce Marketing Co., shipper of fruits and vegetables from 1998 to 2000. Chairman of the Board and Chief Executive Officer of McManus Produce Co., Inc., McManus Cotton Gin, Inc. and McManus Ice Co., Inc. from 1968 to 1998. Former President of Texas Citrus and Vegetable Growers & Shippers Association. Attended The University of Texas at Austin. |

1995 | |||

| Mr. Lackey’s over 40 years of experience in the agricultural business, where he served in various leadership positions, including President and Chief Executive Officer, makes him a valuable member of the board of directors. This experience provides him with a broad understanding of the operational, financial and strategic issues facing the company. |

||||||

| Jon C. Madonna |

69 | Retired Chairman and Chief Executive Officer of KPMG, an international accounting and consulting firm. Retired from KPMG in 1996 having held numerous senior leadership positions throughout his career spanning over 25 years. Chairman of DigitalThink, Inc. from April 2002 to May 2004 and Chief Executive Officer of DigitalThink, Inc. from 2001 to 2002. President and Chief Executive Officer of Carlson Wagonlit Corporate Travel, Inc. from 1999 to 2000 and Vice Chairman of Travelers Group, Inc. from 1997 to 1998. Holds B.S. in Accounting from The University of San Francisco. Current director of AT&T Inc. and Tidewater Inc. Former director of Albertson’s, Inc., Visa Inc., Jazz Technologies, Inc. and Phelps Dodge Corporation. |

2007 | |||

| Mr. Madonna’s long career in public accounting with an international accounting firm and his service as an executive and a director for several publicly traded companies provides him with extensive experience in dealing with financial, accounting and regulatory matters at the board level and gives him a deep understanding of the role of the board and expectations of our directors. In addition, his service on the audit and nominating committees of public companies in a variety of industries positions him well to serve as a member of our audit committee and to provide insights into strategies and solutions to address the challenges of our business. |

||||||

5

Table of Contents

| Name of Director |

Age |

Principal Occupation, Business Experience, and Other Public Company Directorships |

Year First | |||

| Dustan E. McCoy |

63 | Chairman and Chief Executive Officer since December 2005 of Brunswick Corporation, a leading, publicly traded, global manufacturer and marketer of recreation products including marine engines, boats, fitness equipment and bowling and billiards equipment. President of the Brunswick Boat Group from 2000 until 2005. Joined Brunswick in 1999 as Vice President, General Counsel and Corporate Secretary. Prior to joining Brunswick, served as Executive Vice President for Witco Corporation, a publicly traded specialty chemical products company, with operating responsibility for a variety of global businesses and functions and served as Senior Vice President, General Counsel and Corporate Secretary. Holds B.S. in Political Science from Eastern Kentucky University and J.D. in Law from Salmon P. Chase College of Law. Current director of Louisiana-Pacific Corporation and Brunswick Corporation. Former director of Phelps Dodge Corporation. |

2007 | |||

| Mr. McCoy’s experience serving as Chairman and Chief Executive Officer of a large, global publicly traded company provides him with a broad understanding of the operational, financial and strategic issues facing the company. In addition, his experience and qualifications as a general counsel enable him to provide insight in addressing legal and regulatory matters. |

||||||

| James R. Moffett |

74 | Chairman of the board from 1992 to present. Chief Executive Officer of the company from 1995 to 2003. Co-Chairman of the Board, President and Chief Executive Officer of McMoRan. Received Horatio Alger Association of Distinguished Americans Award in 1990. Received Norman Vincent Peale Award in 2000 for exceptional humanitarian contributions to society. Holds B.S. with special honors in Geology from The University of Texas at Austin and M.S. in Geology from Tulane University. |

1992 | |||

| Mr. Moffett, one of the founders of the company, has extensive expertise as a practicing geologist and with respect to our business operations, making him uniquely qualified to lead the board. In 1969, he and two associates founded McMoRan Oil & Gas Co., which developed into one of America’s leading independent oil and gas companies. In 1981, Mr. Moffett led the effort to merge McMoRan Oil & Gas Co. and Freeport Minerals Company. The merger resulted in the establishment of a new company, Freeport-McMoRan Inc., our former parent company, which became one of the world’s leading natural resource companies of which he served as Chairman and Chief Executive Officer from 1984 until 1997 when it was acquired. Through his leadership and skill as a geologist, Mr. Moffett has guided our growth through significant discoveries of metal reserves and the development of our mines, milling facilities and infrastructure. As executive chairman, he continues to further our business strategy by applying his exceptional talents and experience as a geologist. He directs our global exploration programs and continues to be instrumental in fostering our relationships with host governments, including the government of Indonesia, the location of our Grasberg mine. |

||||||

6

Table of Contents

| Name of Director |

Age |

Principal Occupation, Business Experience, and Other Public Company Directorships |

Year First | |||

| B. M. Rankin, Jr. |

83 | Private investor. Vice Chairman of the board from 2001 to present. Current Vice Chairman of the Board of McMoRan. Director and member of the Executive Committee of U.S. Oil and Gas Association, serving as Chairman from 2008 to 2010. McCombs School of Business, The University of Texas at Austin Hall of Fame, 2006. Hunt Oil Company from 1955 to 1967. Director of Texas Oil and Gas Association. Holds B.B.A. from The University of Texas at Austin. |

1995 | |||

| Mr. Rankin is one of the founders of the company and has more than 50 years of experience in the natural resources industry. In 1969, along with Mr. Moffett and another associate, he founded McMoRan Oil & Gas Co., which developed into one of America’s leading independent oil and gas companies. In 1981, McMoRan Oil & Gas Co. and Freeport Minerals Company merged, resulting in the establishment of one of the world’s leading natural resource companies, Freeport-McMoRan Inc., our former parent company. As a founder, he has a comprehensive understanding of the company and its management, operations and financial requirements. With his detailed knowledge of our business and his perspectives regarding strategic and operational opportunities and challenges facing us, he continues to provide valuable insight to the board of directors. |

||||||

| Stephen H. Siegele |

52 | Private investor. Founder and Chief Executive of Advanced Delivery & Chemical Systems, Inc. (ADCS), a worldwide leader in advanced chemicals and delivery hardware serving markets in Asia, Europe and the U.S., from 1988 to 1997. In 1997, ADCS merged with Advanced Technology Materials, Inc., a public company, where Mr. Siegele became a divisional president and Vice Chairman of the Board of Directors until his retirement in 2000. He then founded and served as Chairman of Fluorine On Call, Ltd., a private company that designs and manufactures high purity fluorine generators. Mr. Siegele retired from Fluorine On Call, Ltd. in April 2006. Holds B.S. in Chemical Engineering from the University of Wisconsin-Madison and is an inventor of numerous U.S. patents. |

2006 | |||

| Mr. Siegele has extensive experience as an entrepreneur and inventor within the semiconductor, microelectronics and chemical industries, and as a director and senior manager of public and private companies. These experiences provide him with a strong background in addressing the strategic, operational, financial and technical matters presented to the board, and make him highly qualified to serve as chairman of our corporate responsibility committee. |

||||||

Board Committees

The board has four standing committees: an audit committee, a compensation committee (formerly the corporate personnel committee), a nominating and corporate governance committee and a corporate responsibility committee (formerly the public policy committee). Each of our audit, compensation and nominating and corporate governance committees are composed entirely of independent directors. Each committee operates under a written charter adopted by the board. All of the committee charters are available on our web site at www.fcx.com under

7

Table of Contents

Investor Center – Corporate Governance and are available in print upon request. The members and primary functions of each board committee are described below.

| Audit Committee Members |

Primary Functions of the Audit Committee | |

| Robert A. Day, Chairman Gerald J. Ford H. Devon Graham, Jr. Jon C. Madonna Stephen H. Siegele |

• monitors the Company’s continuing development and effectiveness of its system of financial reporting and internal controls • monitors the operation and integrity of the system of financial reporting and the integrity of the financial statements • monitors the Company’s compliance with legal and regulatory requirements • monitors the qualifications and independence of the Company’s independent registered public accounting firm • monitors the performance of the Company’s independent registered public accounting firm and internal auditors | |

| Compensation Committee Members |

Primary Functions of the Compensation Committee | |

| H. Devon Graham, Jr., Chairman Robert J. Allison, Jr. Charles C. Krulak Bobby Lee Lackey |

• oversees the discharge of the board’s responsibilities relating to compensation of our executive officers • administers our cash-based and equity-based incentive compensation plans | |

| Nominating and Corporate Governance Committee Members |

Primary Functions of the Nominating and Corporate Governance Committee | |

| Robert J. Allison, Jr., Chairman Robert A. Day Gerald J. Ford |

• identifies individuals qualified to serve as directors and recommends to the board director nominees for election at the next annual meeting of stockholders consistent with criteria approved by the board • monitors the composition of the board and its committees • maintains our corporate governance guidelines and recommends to the board any desirable changes • evaluates the effectiveness of the board, its committees and management • oversees the form and amount of director compensation | |

| Corporate Responsibility Committee Members |

Primary Functions of the Corporate Responsibility Committee | |

| Stephen H. Siegele, Chairman Robert J. Allison, Jr. Charles C. Krulak Bobby Lee Lackey Dustan E. McCoy B. M. Rankin, Jr. |

• oversees our environmental policy and implementation programs • oversees our human rights policy and practices • oversees our safety and health policies and programs • oversees our community health programs and related public health and medical matters • oversees our community policy and practices, governmental and stakeholder relations, and social investment and sustainable development programs • oversees our charitable contributions • oversees our political activity and spending practices | |

8

Table of Contents

On May 24, 2012, the board of directors authorized a special committee of independent directors, comprised of Messrs. Allison, Krulak, Lackey, Madonna and McCoy, with the power and authority to oversee the company’s efforts to evaluate potential merger transactions with McMoRan Exploration Co. (McMoRan) and Plains Exploration & Production Company (PXP). As previously disclosed, on December 5, 2012, we entered into: (1) an agreement and plan of merger, by and among PXP, the company and IMONC LLC, our wholly-owned subsidiary (PXP Merger Sub), pursuant to which PXP will merge with and into PXP Merger Sub, with PXP Merger Sub surviving the merger as a wholly owned subsidiary of the company; and (2) an agreement and plan of merger, by and among McMoRan, the company and INAVN Corp., our wholly owned subsidiary (MMR Merger Sub), pursuant to which MMR Merger Sub will merge with and into McMoRan, with McMoRan surviving the merger as a wholly-owned subsidiary of the company. Each of the merger agreements has been approved by the board of directors of each of FCX and PXP and FCX and McMoRan, respectively.

Corporate Governance Guidelines; Principles of Business Conduct

Our corporate governance guidelines and our principles of business conduct are available at www.fcx.com under Investor Center – Corporate Governance. Both are available in print upon request. Amendments to or waivers of our principles of business conduct granted to any of our directors or executive officers will be published promptly on our web site.

Section 16(a) Beneficial Ownership Reporting Compliance

Section 16(a) of the Securities Exchange Act of 1934, as amended, requires our directors and executive officers and persons who own more than 10% of our common stock to file reports of ownership and changes in ownership with the SEC. Based solely upon our review of the Forms 3, 4 and 5 filed during 2012, and written representations from certain reporting persons that no Forms 5 were required, we believe that all required reports were timely filed.

Audit Committee Independence and Financial Experts

The board has determined that each of the members of the audit committee has no material relationship with the company and satisfies the independence criteria (including the enhanced criteria with respect to members of the audit committee) set forth in the applicable NYSE listing standards and SEC rules. In addition, the board has determined that each of the following members of the audit committee – Messrs. Day, Ford, Graham and Madonna – qualifies as an “audit committee financial expert,” as such term is defined by the rules of the SEC.

Item 11. Executive Compensation.

Executive Officer Compensation

Compensation Discussion and Analysis

This Compensation Discussion and Analysis, or CD&A, describes and analyzes our executive compensation philosophy and program in the context of the compensation paid during the last fiscal year to our chief executive officer, our chief financial officer, and each of our two other executive officers (referred to as our named executive officers or NEOs). For fiscal year 2012, our named executive officers are:

| • | James R. Moffett, our chairman of the board; |

| • | Richard C. Adkerson, our president and chief executive officer; |

| • | Kathleen L. Quirk, our executive vice president, chief financial officer and treasurer; and |

| • | Michael J. Arnold, our executive vice president and chief administrative officer. |

In this CD&A, we provide an Executive Summary of our actions and highlights from 2012. We explain the principles that guide our compensation committee’s (our committee’s) executive compensation decisions and discuss in detail each component of executive compensation, including the actual results yielded for each named executive officer for 2012. We also explain the process we follow when setting executive compensation.

9

Table of Contents

Executive Summary

Our committee has implemented an executive compensation program that links our performance (as measured by key financial and business objectives) to incentive compensation. Specifically, our committee believes that a significant portion of the named executive officers’ compensation corresponds to the key measures that our stockholders use in assessing company value. The primary quantitative measures are operating cash flow, return on investment (ROI), and total shareholder return (TSR). Our committee further believes in maintaining a straightforward executive compensation program using cash (short-term), performance-based restricted stock units (long-term), and stock options (long-term). Our stockholder-approved annual incentive plan (AIP) uses operating cash flow and ROI as performance measures in awarding annual cash incentives and performance-based restricted stock units (RSUs). Stock options are annually awarded and vest over four years.

Revisions to our Executive Compensation Program

During the last few years, we have conducted an extensive effort to engage our investors in conversations to identify areas of our program that could be improved, in part in an effort to respond to stockholder concerns evidenced by a negative say-on-pay vote at our 2011 annual meeting. We have held conversations with over 25 of our largest institutional investors and two of the largest proxy advisory firms, and received comments on our executive compensation program. During the discussions, we reviewed our committee’s long-standing pay for performance philosophy and the company’s entrepreneurial culture, the history of our executive compensation programs, including modifications in response to changes in market practices as well as changes following the Phelps Dodge transaction in 2007, and our long track record of being responsive to the concerns of our stockholders. After our committee worked to develop proposed changes to our executive compensation program, we also sought input from these stockholders and advisory firms in December 2011 and January 2012 on the proposed changes. The Chairman of our committee participated in many of these discussions.

During our discussions, many of our investors noted that the company is well managed and recognized (1) the company’s strong performance over the years and (2) that the company’s executive compensation has been linked to performance. Investors who voted against say-on-pay and the proxy advisory firms cited pay magnitude as the primary concern. Many of our stockholders also noted that our AIP had a ROI performance metric that they believed lacked sufficient rigor and expressed interest in seeing more information on the qualitative factors that the committee considers in determining the AIP awards.

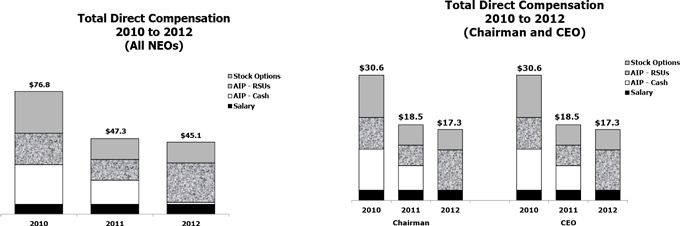

During 2011 and continuing into 2012, our committee worked with its independent consultant to revise our executive compensation program to respond to these concerns. In response to stockholder feedback, we implemented significant changes to the executive compensation program, including adding new caps and increasing the rigor of the ROI performance metric in the AIP beginning for awards under the AIP for 2011, and incorporating a TSR element into our performance-based restricted stock unit grants. As a result of these changes, as shown below, the total direct compensation awarded to each of the Chairman and the CEO for performance in each of 2011 and 2012 was approximately 40% less than the amount awarded for 2010 In addition, the AIP awards for 2012 were approximately 20% below the plan funding amount.

At our 2012 annual meeting, we were encouraged by the increase in stockholder support for our program from the prior year, with approximately 68% of the total votes cast approving our say-on-pay proposal. While this result indicates that there are still some concerns about our program, our committee continues to believe that the core elements of the program, including the revisions made to the AIP during 2012, support our business strategy by encouraging high performance. We also believe that the implementation of our revised program during the course of the past year and a half demonstrates our commitment to be responsive to the views of our stockholders.

In addition to the changes made to our program in early 2012 that began impacting pay for 2011 (with respect to the AIP payments for 2011 and the option awards in 2012 that related to 2011 performance), the following highlights additional actions taken during 2012 and early 2013 that impact our executives’ compensation and use of company securities:

| • | Annual Incentive Awards Based on Performance. Awards earned under the AIP are based on our ROI performance and are funded based on our operating cash flow, with downward adjustments related to |

10

Table of Contents

| copper prices and the committee’s subjective evaluation of other financial and non-financial achievements. Following the evaluation of our performance under these metrics and goals during 2012, the committee concluded that although awards under the AIP were earned by our executive officers, the payouts should be reduced in the aggregate by approximately 20% of the plan funding amount. |

| • | Payout of 2012 AIP in Performance-Based RSUs. The committee elected to deliver the 2012 AIP payment to our Chairman, CEO and CFO solely in performance-based RSUs, with only Mr. Arnold receiving a portion of his AIP in cash. No cash incentive awards were paid to our Chairman, CEO and CFO for 2012. Accordingly, the entire 2012 AIP award for these executives was made contingent on future performance. |

| • | Adoption of Anti-Hedging Policy. We recently amended our insider trading policy to prohibit our executives and directors from entering into hedging arrangements with respect to our securities. This new policy will apply prospectively. |

| • | Revisions to Policy on Pledging. We recognize that in certain circumstances an insider’s pledge of company securities could have potential negative impacts. We believe, however, that pledging can be done in a responsible manner and that given the significant level of ownership of our securities by our executives and many of our directors and the significant trading volume of our shares, we should not adopt a blanket prohibition of these transactions. Alternatively, to address some of the concerns surrounding insider pledging of company securities, we recently amended our policies to provide the following limits on the ability of our executives and directors to pledge our securities: |

| • | our securities may not be pledged as collateral for a margin loan, |

| • | the executive or director must notify the company prior to execution of the pledge, |

| • | the executive or director must establish that he or she has the financial capacity to repay the loan without resort to the pledged securities, and |

| • | any shares pledged will not be considered as owned for purposes of the stock ownership guidelines applicable to the executive or director. |

Our committee recognizes that executive compensation is an evolving area and will continue to monitor market developments. We are still awaiting rules to be adopted to implement provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (Dodd Frank) relating to compensation clawbacks, hedging transactions, and pay ratio and pay for performance disclosures. Our committee expects to consider adopting new, or modifying current, policies and practices relating to these matters as these new rules are implemented.

Highlights of our Executive Compensation Program

What We Do:

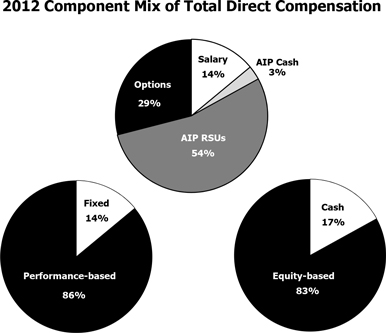

| • | Pay for Performance – a significant portion of executive pay (86% for our chairman and chief executive officer) is tied to performance of our company and increases in our stock price. |

| • | Cap Total Incentive Compensation – total incentive awards under our AIP, both the cash and equity components, and stock option grants that may be received in any one year by each of our chairman and chief executive officer, may not exceed $20 million. |

| • | Limit Awards under our AIP – the total value of annual awards under the AIP (cash and equity) may not exceed six times each executive’s base salary, and while the committee has discretion to determine the form of payment, cash awards may not exceed three times the executive’s base salary. |

| • | Clawback Pay – we may recover incentive awards paid based on restated financial statements under certain circumstances. |

11

Table of Contents

What We Don’t Do:

| • | No Excise Tax Gross-Ups – we have eliminated all excise tax gross-up provisions from our change in control arrangements. |

| • | No Single Trigger Vesting of Equity since 2012 – stock option and RSU awards granted since February 2012 will not accelerate upon a change in control, and will only accelerate upon the recipient’s actual or constructive termination of employment within one year of the change of control. |

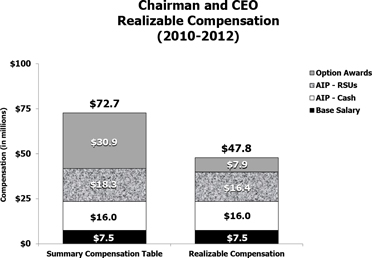

2012 Total Direct Compensation for Chairman and CEO drops over 40% from 2010

Our committee views each executive’s “total direct compensation” for a given year as the sum of the executive’s base salary, awards under the AIP for that year (both cash and performance-based RSUs), and the value of other long-term incentives granted in recognition of our performance for that year. As indicated in the following graphs (dollars in millions), the revisions to the executive compensation program in early 2012 had a significant impact on each executive’s total direct compensation for performance in 2011 and 2012, with the total direct compensation awarded to each of the Chairman and the CEO for 2011 being 40% less than the amounts awarded for 2010, and dropping another 6% in 2012 as compared to 2011. In addition, no cash incentive awards were paid to our Chairman, CEO or CFO for 2012. See “Summary of 2012 Total Direct Compensation” below for more information on how we calculate total direct compensation and how these amounts differ from the information contained in the 2012 Summary Compensation Table.

2012 Company Performance Highlights

The following highlights certain of our accomplishments during 2012, many of which are also discussed under “Overview of Principal Components of Executive Compensation – Annual Incentive Awards – Factors Considered in Determination of 2012 AIP Awards”:

| • | Solid operational performance and cost management |

| • | Operating cash flow for 2012 of $5.2 billion (as adjusted for working capital changes) |

| • | Production growth in North America and Africa |

| • | Achievement of important milestones in the development of financially attractive projects to increase copper and molybdenum production |

| • | Continued active exploration program, with results focused on generating future reserve growth |

| • | Strong management of environmental and social programs with positive international recognition for corporate social responsibility |

12

Table of Contents

| • | Completed debt refinancing, issuing $3 billion in new debt at 3% average cost, resulting in a $160 million annual interest savings |

| • | Maintained strong balance sheet and increased regular annual common stock dividend rate by 25% to $1.25 per year |

During 2012, we also faced a number of challenges, including:

| • | Labor and security issues, as well as regulatory uncertainty, in Indonesia |

| • | Six fatalities worldwide |

| • | A 7% decrease in our share price, including a 14% decrease in the 2012 fourth quarter |

Executive Compensation Philosophy

The fundamental tenets of our company’s executive compensation philosophy are to:

| • | pay for performance by emphasizing performance-based compensation that balances rewards for both short- and long-term results and provides our executives with high reward opportunities for high corporate performance, |

| • | tie compensation to the interests of stockholders, and |

| • | provide a competitive level of compensation. |

Our committee believes that its pay for performance philosophy complements the company’s entrepreneurial culture. In order to achieve these goals, our committee believes that not only should a significant portion of the named executive officers’ compensation be performance-based, such compensation should also correspond to the key measures used by our stockholders in assessing our company’s value. The primary elements of the performance-based pay under our program are the awards under our stockholder-approved AIP, which focus on operating cash flow and ROI, and also include a TSR requirement.

As described below, our annual incentive plan contains both a quantitative component pursuant to which the plan is funded based on our achievement of certain financial measures, and a qualitative component pursuant to which our committee exercises its discretion in determining the ultimate awards. If our company achieves the required ROI threshold, our annual incentive plan is funded by a percentage of operating cash flow (excluding working capital changes), which we believe is a key measure of our company’s performance. Our executive compensation program also contains certain caps on the awards payable to individual executives. Our committee then uses its discretion to determine individual awards within this framework, based on its evaluation of metrics that our committee believes are critical to our success and indicative of management’s performance during the year. Our committee believes that this dual approach appropriately awards our executives if the company performs well, but also gives the members of our committee the ability to exercise their judgment and consider qualitative factors that may not be easily measurable but that also impact our success. Our stockholders have indicated an interest in learning more about the other measures our committee considers, and we have included disclosure in this CD&A describing our committee’s discretionary assessment.

13

Table of Contents

Overview of Principal Components of Executive Compensation

The principal components of executive officer compensation for 2012 were base salaries, annual incentive awards, and long-term incentive awards, the sum of which our committee views as the executives’ “total direct compensation.” In addition, we provide our executives with certain personal benefits and perquisites, as well as post-employment compensation, which our committee considers separately from total direct compensation and which are further described below. The following charts illustrate the component mix of the aggregate total direct compensation paid to our named executive officers for 2012:

The following is an explanation of each principal component of our executive compensation program, including a description of our committee’s compensation decisions for 2012.

Base Salaries

| How base salaries support our compensation philosophy and objectives: |

• Base salaries help us meet the objective of attracting and retaining the executive officers needed to manage our business successfully.

• Fixed compensation in the form of base salary represents an average of 14% of our executive officers’ compensation, reflecting our goal to allocate more compensation to the performance-dependent elements of the total compensation package. |

Individual base salary amounts reflect our committee’s judgment with respect to each executive officer’s responsibility, performance, work experience and the individual’s historical salary level. We have not increased the base salaries of our executive officers since May 2007, when increases to the base salaries of certain executive officers were approved to address the increased responsibilities of these executives following the acquisition of Phelps Dodge. The base salaries of Messrs. Moffett and Adkerson and Ms. Quirk are contractually set pursuant to their employment agreements.

14

Table of Contents

Annual Incentive Awards

Our annual incentive plan, or AIP, is designed to provide performance-based awards to our executive officers, each of whose performance has a significant impact on our financial stability, profitability and future growth.

| How the overall design of the AIP supports our compensation philosophy and objectives: | • It encourages the entrepreneurial spirit of the organization and the alignment of executive management with stockholder objectives.

• Its focus on operating cash flow and returns on invested capital, the underlying metrics of the plan, reflects our goal to maximize cash flows and long-term returns for our stockholders.

• The variability of cash flows associated with changes in commodity prices, changes in production volumes, cost management and other changes in business conditions closely aligns management and stockholder interests.

• Its revised cap on overall awards to six times the executive’s base salary limits the value of cash and equity awards while providing significant compensation opportunities if the company’s performance warrants high payouts.

• Mandating that all payments over three times the executive’s base salary be made in performance-based RSUs having an equivalent value converts a portion of the annual award to a long-term incentive dependent upon the company’s continued performance. |

General Structure of the AIP. The current AIP was approved by our stockholders in 2009, and its design is intended to provide compensation opportunities that reflect the performance of our business, which may vary significantly from year to year, and that are consistent with observed market pay levels. As noted above, the financial measure used to fund the AIP pool is operating cash flow, excluding working capital changes, reflecting our committee’s belief that operating cash flow is a meaningful indicator of overall performance for our company.

Our committee allocates a percentage of the plan funding amount to each participant at the beginning of the year. If our five-year ROI (as defined in the AIP) is 6% or greater, our executive officers would share in a plan funding amount equal to 0.625% of our operating cash flow, as adjusted. After the end of the year, our committee then uses its discretion to determine the payouts under the plan for the year, subject to the limits on the payouts depending on ROI and other factors set forth in the plan and described below. The plan also specifically enumerates a non-exclusive list of qualitative factors that our committee may consider in exercising this discretion.

Additional Requirements under the AIP. Beginning with the AIP awards for fiscal year 2011, our committee implemented the following guidelines that will be used in the exercise of the committee’s discretion to reduce awards when determining awards under the AIP:

| • | Reduced Individual Caps Under the AIP – No participant in the AIP may receive an award under the plan having an aggregate value in excess of six times his or her salary (reduced from the eight times limit in the plan). In addition, the total value of the cash award under the AIP may not exceed three times the executive’s salary (reduced from the four times in the plan). These changes reduce the magnitude of each executive’s potential awards under the plan. |

15

Table of Contents

| • | Increased the Rigor of the AIP Performance Measure – The company’s operating cash flows are significantly impacted by changes in copper prices. Accordingly, as an additional overlay to the AIP metrics and the individual award caps, our committee adopted a matrix of potential awards, expressed as a multiple of salary, designed to increase the rigor of the ROI performance metric as copper prices increase. The matrix is used as a guideline and our committee considers various additional factors, as more fully described below, to determine the ultimate payouts under the AIP. Under this matrix, as copper prices increase (determined by the average consolidated realized copper price reported by the company), the company’s annual ROI must also increase in order for an increased salary multiple to apply (up to the six times cap). If ROI does not increase, the individual cap will be reduced as set forth in the table below. The matrix is only applicable if the average consolidated realized copper price reported by the company for the year is above $2.50 per pound. In developing the matrix, our committee and its consultants reviewed the company’s projections with an objective of establishing the upper end of the salary multiple opportunity as a stretch target. The annual ROI calculation will exclude costs of major projects until the project is operational. |

| Salary Multiples – Annual ROI Thresholds | ||||||||||||||||||||

| Average Copper Price per Pound |

2x | 3x | 4x | 5x | 6x | |||||||||||||||

| $2.51-$3.00 |

6 | % | 7 | % | 10 | % | 13 | % | 16 | % | ||||||||||

| $3.01-$3.50 |

9 | % | 10 | % | 13 | % | 16 | % | 19 | % | ||||||||||

| $3.51-$4.00 |

12 | % | 13 | % | 16 | % | 19 | % | 23 | % | ||||||||||

| >$4.01 |

15 | % | 17 | % | 20 | % | 23 | % | 27 | % | ||||||||||

The following example illustrates the application of these guidelines. For this example, we are assuming that the five-year ROI measure is met for the plan year, and that the company’s operating cash flow is sufficient to generate a plan funding amount in excess of six times the executives’ aggregate salaries (the revised cap). Under these guidelines, if the average copper price per pound for the year is $3.00, in order for the executives to be eligible for an aggregate payout under the AIP of six times his or her salary (the revised cap), the company’s annual ROI must be at least 16%. If the average copper price per pound for the year is $4.20, in order for the executives to be eligible for an aggregate payout under the AIP of six times his or her salary, the company’s annual ROI must be at least 27%.

| • | Additional TSR Conditions Applicable to AIP Awards Delivered as Performance-Based RSUs – Any RSUs granted as part of the AIP will cliff vest after three years if the ROI measure has been achieved, with 20% of the award subject to forfeiture if our TSR for the three-year period ending on the December 31st prior to the vesting date is below the median TSR of our peer group (the Peer Group). For purposes of the performance-based RSUs, TSR, as applied to the company or any company in the Peer Group, means stock price appreciation from the beginning to the end of the performance period, including dividends and distributions made or declared (assuming such dividends or distributions are reinvested in the common stock of the applicable company) during the performance period, expressed as a percentage return. In addition, the Peer Group against which we will measure our TSR for these performance-based RSUs is comprised of the following companies: |

| Alcoa Inc. | Rio Tinto plc | |

| Anglo American plc | Southern Copper Corporation | |

| Antofagasta plc | Teck Resources Limited | |

| Barrick Gold Corporation | United States Steel Corporation | |

| BHP Billiton plc | Vale S.A. | |

| Newmont Mining Corp. | Xstrata plc |

16

Table of Contents

In selecting the Peer Group for these performance-based RSUs, we selected metals and mining companies that the investment community generally tracks as an industry group, many of which are based outside the U.S. Because there are limited U.S.-based metals and mining companies, we expanded our selection of U.S. companies to include two industrial metal companies, which resulted in a group of 12 companies, with one-third being comprised of U.S.-based companies.

Factors Considered in Determination of 2012 AIP Awards. In February 2012, we assigned each of our executive officers a percentage of the aggregate plan funding amount under the stockholder-approved AIP for 2012: 40% to each of Messrs. Moffett and Adkerson, 11% to Ms. Quirk and 9% to Mr. Arnold. These allocations were based on each officer’s position and were consistent with the prior year’s allocations.

Quantitative Measures. For 2012, operating cash flow as adjusted for working capital changes as reflected in our consolidated statements of cash flows was $5.2 billion, thus producing a maximum plan funding amount of $32.5 million. During the five-year period ending in 2012, the average ROI was 17.1%. In addition, under our new guidelines, the average recorded copper price per pound was $3.60 and the 2012 ROI was 21.7%, allowing for a guideline maximum payout opportunity of 5.7 times base salary for each executive, subject to the maximum plan funding amount and the committee’s discretion to reduce the awards after review of the qualitative measures.

Qualitative Measures. In addition to reviewing the quantitative results discussed above, our committee evaluated and considered the company’s and our management group’s performance relative to other factors in determining payouts under the AIP. Specifically, our committee evaluated performance relative to safety results, environmental and social factors, certain operational metrics, results of growth initiatives, the company’s relative TSR and ROI compared to peer companies, exploration results, financial management and management’s response to labor and governmental challenges that the company continued to face during 2012. The following is a summary of the information relative to these matters reviewed and considered by our committee when determining the 2012 AIP awards.

Safety. Our committee assessed the company’s safety performance for 2012 based in part on pre-established targets for the total reportable rates in each area of operation and the company as a whole. Although the company’s total reportable rate in 2012 met the 2012 performance target, the company regrettably had six reportable fatalities in 2012. Our committee also recognized a number of significant safety initiatives that management completed in 2012, including the following:

| • | Completion of OHSAS 18001 accredited certification for all sites |

| • | Enhancements to the company’s fatality prevention program |

| • | Enhancements to industrial hygiene processes at sites |

| • | Successful rollout of crisis management initiative to all FM Americas and Climax sites |

| • | Receipt of Chilean National Mining Society Award for Chilean operations |

| • | Receipt of U.S. National Institute for Occupational Safety and Health award for implementation of practices to prevent accidents in the surface mining environment |

Environmental and Social. Our committee recognized management’s continued efforts during 2012 to conduct business in an environmentally and socially responsible manner for the benefit of its stakeholders. Specifically, our operations in North and South America incurred no significant environmental events. We maintained ISO 14001 Environmental Management System certifications at all major operations with Tenke being recommended for certification in December 2012. We also completed internal, external and government compliance audits, which confirmed that PT Freeport Indonesia is in full compliance with applicable environmental

17

Table of Contents

laws and regulations. In addition, we received approval from the Peruvian Government of the environmental impact statement for the Cerro Verde expansion. During 2012, the company had several sustainability accomplishments, including:

| • | Maintained the company’s Working Toward Sustainable Development Report at the A+ level of the Global Reporting Initiative, including third-party assurance |

| • | Completed a three-year cycle to conduct site-level external assurance of the International Council on Mining and Metals Sustainable Development Framework at all major operations |

| • | Named to the Civic 50, a list of the most community-minded companies in America and a national initiative to survey and rank America’s S&P 500 corporations on how they engage with the communities they serve and institutionalize practices in their corporate culture |

| • | Completed the Cerro Verde water treatment plant for Arequipa, Peru and inaugurated the plant in partnership with President Humala |

| • | Awarded ISO 50001 certification for Atlantic Copper’s energy management system |

| • | Honored by the New Mexico Mining and Minerals Division with the Excellence in Reclamation Award for large scale and innovative reclamation at the Tyrone Mine and successfully implementing tailings and stockpile reclamation projects at Chino |

| • | Provided funding to State of Colorado Inactive Mine Reclamation Program and to Trout Unlimited to clean-up abandoned mine sites that are not associated with the company or our historic operations |

| • | Continued to strategically advance community development and investment programs in key regions where we operate: |

| • | In Africa, we continued to invest in community infrastructure projects, resettled 70 households in Tenke for the Phase II expansion project and received the Workplace/Workforce Engagement Award in the Special Focus HIV/AIDS, Tuberculosis or Malaria category from GBCHealth |

| • | In Indonesia, we launched new community infrastructure investment projects in and around Timika and received an award from the Government for Best HIV/AIDS Program in the Work Place |

| • | In the United States, we established a new community investment fund in Arizona, implemented a Native American Scholarship Program and cultivated partners to support an effort to recruit and retain new STEM (science, technology, engineering and math) teachers in the U.S. (specifically Arizona, Colorado and New Mexico) |

Operational Metrics. Our committee also evaluated the company’s achievement of production and sales targets, operational efficiencies and cost management.

Sales. The company’s consolidated sales were slightly below plan, primarily because of the labor disputes in Indonesia during the first half of 2012. Following is a summary of the company’s 2012 sales results:

| • | North America sales exceeded forecast, reflecting the successful initiatives to increase mining and milling activities at Morenci and the ramp up of production from restarts at Miami and Chino. |

| • | South America sales were slightly below forecast and were impacted by lower recoveries at the El Abra mine, which were successfully addressed in the second half of 2012. |

| • | Tenke sales exceeded forecast and were nearly 20% higher than 2011 sales as a result of successful initiatives to increase mining rates and optimize mill performance. |

| • | Grasberg sales were below forecast because of labor disruptions in the first half of 2012 and a slower ramp-up of the underground DOZ mine following the prolonged labor strike in 2011. |

Costs. During 2012, management continued to aggressively manage costs despite inflationary pressures in a number of areas. As anticipated, unit costs in 2012 were higher than in 2011, primarily because of lower copper sales volumes in Indonesia and higher mining costs in North and South America. Consolidated unit site production and delivery costs were slightly below the unit costs estimated at the start of the year.

Growth Initiatives. Our committee recognized the significant efforts of management to grow our business and enhance returns for stockholders. Some of the projects involve restarting idled production or replacing

18

Table of Contents

production from depleting reserves and others involve major expansions. Through exploration and technical evaluations, management is pursuing three major projects that have the potential to increase production by nearly 1 billion pounds of copper over the next three years. Our committee noted the following major accomplishments on growth initiatives during 2012:

| • | Successful completion of the construction of the Climax molybdenum mine, which commenced production in 2012 |

| • | Achievement of significant milestones in the development of Grasberg Underground to prepare for transition from open pit operations in 2016 |

| • | Received Peruvian government approval for the environmental impact statement for Cerro Verde expansion to triple concentrator rates |

| • | Obtained key permits and commenced construction of projects at Morenci to increase production by 40% by 2014 |

| • | Completed construction of Phase II expansion at Tenke to increase production by 50% (the project was completed on time and within budget in a challenging environment) |

TSR & ROI Compared to Peers. Our committee noted that the company’s one-year TSR was -4.0% compared to the median of 3.3% for the Peer Group; the company’s three-year TSR of -7.5% compared to the median of -1.0%; and the company’s five-year TSR was -25.5% compared to the median of -22.3%. The company’s ROI for the first nine months of 2012, which was the data available at the time of our committee’s review, was 17.1%, which was above the 75th percentile of 16.3%. Our three-year ROI of 31.5% was above the 75th percentile and our five-year ROI of 16.2% was the median. Thus, despite the stock price volatility we have experienced, management has effectively managed the business to deliver strong operational results.

Exploration Results. Our committee noted the company’s aggressive exploration program to define the size of our resources, identify new resources, and develop expansion plans and growth initiatives, all with the view of generating long-term values for our shareholders. In particular, through recent exploration drilling activities, including the 2012 program, the company has identified potential new future copper reserve additions over the next few years. In addition, our committee noted the addition since 2007 of 46 billion pounds of copper reserves, replacing production by more than two times.

Financial Management. The company has maintained a strong balance sheet, which provides financial strength to pursue aggressively its growth objectives, manage volatile market conditions and provide strong cash returns to shareholders. Following completion of the pending acquisitions, the company plans to reduce debt incurred in the transactions through operating cash flows and disciplined management of capital expenditures. For 2012, our committee noted the following items:

| • | Completed a highly successful refinancing of its debt in February 2012, through $3 billion in bond financings at an average cost of 3% (the proceeds were used to refinance higher cost debt resulting in annual interest cost savings of approximately $160 million) |

| • | Year-end 2012 net cash position of $0.2 billion, compared with $17.6 billion in debt ($14.2 billion net of cash) at the time of the Phelps Dodge transaction in 2007; interest cost savings from debt repayments and refinancings since January 1, 2009 approximated $420 million per year |

| • | Maintained investment grade ratings with three credit rating agencies |

| • | Paid $1.1 billion in common stock dividends during 2012, and increased the annual common dividend rate from $1.00 to $1.25 per share |

| • | Obtained financing commitments for low cost debt financing for the pending acquisitions |

Other Factors. Our committee also considered the continued labor and governmental relations challenges faced by the company during 2012. Specifically, the company continued to address challenges with changes in the regulatory environment and significant labor and security challenges at its Grasberg operations. Following a three month strike in late 2011, the company successfully re-integrated the work force and improved productivity. During 2012, management dedicated significant resources to improving relations with the company’s large Indonesian work force and addressing the challenging security situation and complex regulatory environment in Indonesia.

19

Table of Contents

Organizational changes at PT Freeport Indonesia were implemented in early 2012, including a change in the President Director and other senior management positions to address complex issues that had not been experienced in our 40-year operating history. Significant “quality of life” initiatives for our workforce and the local community were implemented, which are consistent with our objective of maintaining a productive and healthy work environment.

Executive management maintained active discussions with Indonesian government officials to address the labor and security issues. In addition, executive management continues to work proactively with local management and with Indonesian government officials to conclude the ongoing review of our Contract of Work in a mutually satisfactory manner. Substantial progress has been made in developing a framework for a mutually acceptable Contract of Work resolution.

We maintained good labor relations in South America and the 2011 Cerro Verde labor agreement was implemented without disruption. In addition, we were successful in reaching a new four-year labor agreement in late 2012 with the Candelaria labor union in advance of the 2013 expiration. A new labor agreement was also reached at Tenke Fungurume during 2012.

Executive management also maintained positive relations with key governmental officials in the Democratic Republic of Congo, Peru, Chile and the U.S. Management committed significant resources, personal involvement, and leadership in communicating with key government stakeholders on the benefits of the company’s operations.

Long-Term Incentive Awards

Long-term incentives granted by the company may consist of a variety of incentives, but we have historically granted stock options, RSUs, or a combination of the two. Since 2009, our committee’s practice has been to make annual equity-based awards to the executives in the form of stock options.

20

Table of Contents

| How long-term incentive awards, specifically stock options, support our compensation philosophy and objectives: | • Long-term incentives are a variable component of compensation intended to reward our executives for the company’s success in achieving sustained, long-term profitability and increases in stock value.

• Stock options align the executives’ interests with those of our stockholders as their value is dependent on an increase in our stock price. We recognize that some institutional shareholders have expressed reservations about using stock options as performance-based compensation, but our committee strongly believes that stock options continue to be an excellent performance-based compensation vehicle that links compensation to shareholder return.

• We also provide long-term incentive awards in the form of performance-based RSUs in connection with the AIP, which strengthen focus on stock price performance and encourage executive ownership of our stock. |

2012 Executive Compensation

AIP Payout and Stock Option Awards for 2012

In determining the AIP payout and stock option awards for 2012, our committee considered (1) the company’s performance in 2012, including the quantitative and qualitative measures described above, (2) the umbrella cap adopted by our committee, which limits total incentive awards to $20 million for each of our chairman and chief executive office and (3) the grant date value of the stock option awards and how those awards related to total compensation and base salary.

Although the new ROI guideline provided a maximum payout opportunity of 5.7 times base salary for each executive, this would have exceeded the maximum plan funding amount ($32.5 million), thus the maximum plan funding amount set the upper limit of awards under the AIP for 2012. Our committee recognized that the company’s stock price had declined 7% in 2012, including a 14% decrease in the 2012 fourth quarter, and the company faced challenges during 2012 as described above. The committee also remained mindful of the views of our stockholders regarding pay magnitude. Based on these factors and pursuant to its discretionary authority to reduce awards, our committee made aggregate awards under the AIP for 2012 that were approximately 20% less than the plan funding amount. In addition, the committee elected to award only performance-based RSUs to three of the named executive officers under the AIP (no cash awards). Further, our committee awarded stock options valued at approximately 2.0 times base salary for each of our chairman and our chief executive officer and 2.5-2.7 times base salary for each of our two other named executive officers.

The table below reflects the value of the 2012 AIP and stock option awards (i.e. all of the 2012 incentive compensation awards), which were awarded in January 2013. As noted below, the value of the performance-based RSUs and the stock options reflected in the table below are not included in the 2012 Summary Compensation Table on page 30, as SEC regulations require that they be reflected in the 2013 Summary Compensation Table for 2013 because they were granted during 2013. The performance-based RSUs and stock options included as part of 2012 compensation in the Summary Compensation Table were granted as part of 2011 compensation.

21

Table of Contents

AIP and Stock Options Awards to the NEOs for 2012

($ millions)

| Actual 2012 AIP Awards | ||||||||||||||||||||||||||||||||

| Name |

Value Paid in Cash |

Salary Multiple |

Value Paid in Perf.- Based RSUs (1) |

Salary Multiple |

Aggregate Value Awarded |

Salary Multiple |

Black-Scholes Value of Options Granted for 2012(1) |

Salary Multiple |

||||||||||||||||||||||||

| Mr. Moffett |

$ | 0.0 | n/a | $ | 9.860 | 3.9 | $ | 9.860 | 3.9 | $ | 4.94 | 2.0 | ||||||||||||||||||||

| Mr. Adkerson |

0.0 | n/a | 9.860 | 3.9 | 9.860 | 3.9 | 4.94 | 2.0 | ||||||||||||||||||||||||

| Ms. Quirk |

0.0 | n/a | 3.287 | 5.1 | 3.287 | 5.1 | 1.65 | 2.5 | ||||||||||||||||||||||||

| Mr. Arnold |

1.2 | 2.2 | 1.643 | 3.0 | 2.843 | 5.2 | 1.48 | 2.7 | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Totals |

$ | 1.2 | $ | 24.650 | $ | 25.850 | $ | 13.01 | ||||||||||||||||||||||||

| (1) | Awards were granted on January 29, 2013, and the performance-based RSU values are calculated using the Monte Carlo valuation model. |

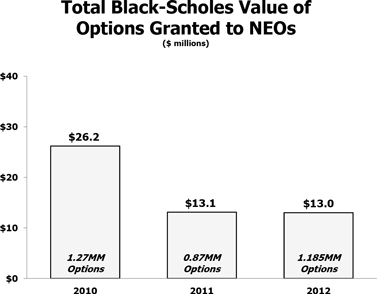

Our committee has always considered the value of the options on the grant date but did not historically use this to determine the appropriate grant level due to the significant changes in value that can occur from one year to the next. Beginning with awards made in February 2011, our committee considered both the number of options granted and the grant date values when approving awards. For awards made for 2012 (granted in January 2013), the committee approved awards with a grant date fair value that was consistent with the options awarded the prior year and approximately 50% less than the value of the options awarded for 2010. Although the awards made in February 2012 are viewed by our committee as part of 2011 total direct compensation, SEC regulations require that they be reflected in the 2012 Summary Compensation Table because they were granted during 2012.

The following chart shows the varying Black-Scholes values of the options granted to the named executive officers for each of the previous three fiscal years:

22

Table of Contents

Summary of 2012 Total Direct Compensation

As noted above, our committee views each executive’s “total direct compensation” for a given year as the sum of the executive’s base salary, aggregate awards under the AIP for that year, and the value of long-term incentives granted in recognition of our performance for that year. In making its decisions regarding the appropriate levels of annual incentive and long-term incentive awards, our committee evaluates the impact of its decisions on the amount of total direct compensation and the percentage of each component to total direct compensation of the executive team as a group. Our committee concluded that the award levels, the form of the awards and the resulting total direct compensation set forth below for the executive team were appropriate considering the company’s performance during 2012. See “Executive Compensation Market Assessment” below.

2012 Total Direct Compensation(1)

(in millions)

| 2012 AIP Awards | Black-Scholes | |||||||||||||||||||||||

| Executive |

Base Salary |

Value Paid in Cash |

Value Paid in RSUs |

Value of Stock Options Granted(2) |

Total

Incentive Compensation(3) |

Total Direct Compensation |

||||||||||||||||||

| James R. Moffett |

$ | 2.50 | $ | 0 | $ | 9.860 | $ | 4.94 | $ | 14.800 | $ | 17.300 | ||||||||||||

| Richard C. Adkerson |

2.50 | 0 | 9.860 | 4.94 | 14.800 | 17.300 | ||||||||||||||||||

| Kathleen L. Quirk |

0.65 | 0 | 3.287 | 1.65 | 4.937 | 5.587 | ||||||||||||||||||

| Michael J. Arnold |

0.55 | 1.2 | 1.643 | 1.48 | 4.323 | 4.873 | ||||||||||||||||||

| (1) | Does not include the value of perquisites and personal benefits, as well as commitments for post-employment compensation, which amounts are included in the 2012 Summary Compensation Table and supplementary tables below. |

| (2) | Although our committee granted these stock options in January 2013, our committee views these grants as part of the executives’ 2012 total direct compensation. See the description of these awards under “Overview of Principal Components of Executive Compensation — Long-Term Incentive Awards.” |

| (3) | Represents total of AIP awards (cash and performance-based RSUs) and stock option awards. |