Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2013

or

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 333-08322

KANSAS CITY SOUTHERN DE MÉXICO, S.A. DE C.V.

(Exact name of Company as specified in its charter)

Kansas City Southern of Mexico

(Translation of Registrant’s name into English)

Mexico |  | 98-0519243 | ||

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||

Montes Urales 625 Lomas de Chapultepec 11000 Mexico, D.F. Mexico (Address of Principal Executive Offices) | ||||

(5255) 9178-5686

(Company’s telephone number, including area code)

No Changes

(Former name, former address and former fiscal year, if changed since last report.)

______________________________________________________________

Indicate by check mark whether the Company (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Company was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o Accelerated filer o Non-accelerated filer x Smaller reporting company o

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of March 31, 2013: 4,785,510,235

Kansas City Southern de México, S.A. de C.V. meets the conditions set forth in General Instruction H(1)(a) and (b) of Form 10-Q and is therefore filing this Form with the reduced disclosure format.

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Form 10-Q

March 31, 2013

Index

Page | ||

Item 1. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 1. | ||

Item 1A. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 5. | ||

Item 6. | ||

2

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Form 10-Q

March 31, 2013

PART I—FINANCIAL INFORMATION

Item 1. | Financial Statements |

Introductory Comments

The unaudited Consolidated Financial Statements included herein have been prepared by Kansas City Southern de México, S.A. de C.V. (“KCSM” or the “Company”) pursuant to the rules and regulations of the Securities and Exchange Commission (“SEC”). For the purposes of this report, unless the context otherwise requires, all references herein to “KCSM” and the “Company” shall mean Kansas City Southern de México, S.A. de C.V. and its subsidiaries. Certain information and footnote disclosures normally included in financial statements prepared in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”) have been condensed or omitted pursuant to such rules and regulations. The Company believes that the disclosures are adequate to enable a reasonable understanding of the information presented. The Consolidated Financial Statements and Management’s Discussion and Analysis of Financial Condition and Results of Operations included in this Form 10-Q should be read in conjunction with the consolidated financial statements and the related notes, as well as Management’s Discussion and Analysis of Financial Condition and Results of Operations, included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2012. Results for the three months ended March 31, 2013, are not necessarily indicative of the results expected for the full year ending December 31, 2013.

3

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Consolidated Statements of Comprehensive Income

Three Months Ended | |||||||

March 31, | |||||||

2013 | 2012 | ||||||

(In millions) (Unaudited) | |||||||

Revenues | $ | 255.3 | $ | 245.2 | |||

Operating expenses: | |||||||

Compensation and benefits | 28.6 | 35.1 | |||||

Purchased services | 35.8 | 36.2 | |||||

Fuel | 42.0 | 39.5 | |||||

Equipment costs | 20.0 | 18.1 | |||||

Depreciation and amortization | 24.6 | 22.1 | |||||

Materials and other | 14.7 | 11.3 | |||||

Total operating expenses | 165.7 | 162.3 | |||||

Operating income | 89.6 | 82.9 | |||||

Equity in net earnings of unconsolidated affiliates | 0.7 | 0.8 | |||||

Interest expense | (21.5 | ) | (22.5 | ) | |||

Foreign exchange gain | 12.9 | 2.9 | |||||

Other expense, net | (0.1 | ) | (0.1 | ) | |||

Income before income taxes | 81.6 | 64.0 | |||||

Income tax expense | 27.4 | 27.2 | |||||

Net income | 54.2 | 36.8 | |||||

Other comprehensive income, net of tax: | |||||||

Foreign currency translation adjustments, net of tax of $0.0 million for all periods presented | 0.6 | 0.9 | |||||

Other comprehensive income | 0.6 | 0.9 | |||||

Comprehensive income | $ | 54.8 | $ | 37.7 | |||

See accompanying notes to consolidated financial statements.

4

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Consolidated Balance Sheets

March 31, 2013 | December 31, 2012 | ||||||

(In millions, except share amounts) | |||||||

(Unaudited) | |||||||

ASSETS | |||||||

Current assets: | |||||||

Cash and cash equivalents | $ | 49.8 | $ | 9.2 | |||

Accounts receivable, net | 123.2 | 109.9 | |||||

Related company receivables | 1.0 | 40.0 | |||||

Materials and supplies | 43.0 | 32.9 | |||||

Deferred income taxes | 42.7 | 42.8 | |||||

Other current assets | 66.4 | 79.0 | |||||

Total current assets | 326.1 | 313.8 | |||||

Investments | 14.4 | 13.1 | |||||

Property and equipment (including concession assets), net | 2,528.5 | 2,522.3 | |||||

Other assets | 50.6 | 60.3 | |||||

Total assets | $ | 2,919.6 | $ | 2,909.5 | |||

LIABILITIES AND STOCKHOLDERS’ EQUITY | |||||||

Current liabilities: | |||||||

Debt due within one year | $ | 114.1 | $ | 18.8 | |||

Accounts payable and accrued liabilities | 105.1 | 87.4 | |||||

Related company payables | 9.6 | 6.9 | |||||

Total current liabilities | 228.8 | 113.1 | |||||

Long-term debt | 837.2 | 938.0 | |||||

Related company debt | 121.4 | 178.3 | |||||

Deferred income taxes | 129.9 | 131.6 | |||||

Other noncurrent liabilities and deferred credits | 9.3 | 10.3 | |||||

Total liabilities | 1,326.6 | 1,371.3 | |||||

Commitments and contingencies | — | — | |||||

Stockholders’ equity: | |||||||

Common stock, 4,785,510,235 shares authorized, issued without par value | 286.1 | 286.1 | |||||

Additional paid-in capital | 243.6 | 243.6 | |||||

Retained earnings | 1,065.9 | 1,011.7 | |||||

Accumulated other comprehensive loss | (2.6 | ) | (3.2 | ) | |||

Total stockholders’ equity | 1,593.0 | 1,538.2 | |||||

Total liabilities and stockholders’ equity | $ | 2,919.6 | $ | 2,909.5 | |||

See accompanying notes to consolidated financial statements.

5

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Consolidated Statements of Cash Flows

Three Months Ended | |||||||

March 31, | |||||||

2013 | 2012 | ||||||

(In millions) (Unaudited) | |||||||

Operating activities: | |||||||

Net income | $ | 54.2 | $ | 36.8 | |||

Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

Depreciation and amortization | 24.6 | 22.1 | |||||

Deferred income taxes | (1.6 | ) | 13.3 | ||||

Equity in net earnings of unconsolidated affiliates | (0.7 | ) | (0.8 | ) | |||

Deferred compensation | — | 7.3 | |||||

Changes in working capital items: | |||||||

Accounts receivable | (13.3 | ) | (24.6 | ) | |||

Related companies | 62.7 | (4.8 | ) | ||||

Materials and supplies | (9.3 | ) | (0.4 | ) | |||

Other current assets | 1.4 | 0.3 | |||||

Accounts payable and accrued liabilities | 18.1 | 24.7 | |||||

Other, net | 2.9 | 1.8 | |||||

Net cash provided by operating activities | 139.0 | 75.7 | |||||

Investing activities: | |||||||

Capital expenditures | (33.2 | ) | (32.6 | ) | |||

Proceeds from disposal of property | 0.2 | 1.6 | |||||

Other, net | (0.1 | ) | (0.2 | ) | |||

Net cash used for investing activities | (33.1 | ) | (31.2 | ) | |||

Financing activities: | |||||||

Repayment of long-term debt | (5.8 | ) | (5.4 | ) | |||

Repayment of related company debt | (59.4 | ) | — | ||||

Debt costs | (0.1 | ) | — | ||||

Net cash used for financing activities | (65.3 | ) | (5.4 | ) | |||

Cash and cash equivalents: | |||||||

Net increase during each period | 40.6 | 39.1 | |||||

At beginning of year | 9.2 | 15.7 | |||||

At end of period | $ | 49.8 | $ | 54.8 | |||

See accompanying notes to consolidated financial statements.

6

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Notes to Consolidated Financial Statements

1. | Accounting Policies, Interim Financial Statements and Basis of Presentation |

In the opinion of the management of KCSM, the accompanying unaudited consolidated financial statements contain all adjustments necessary for a fair presentation of the results for interim periods. All adjustments made were of a normal and recurring nature. Certain information and note disclosures normally included in financial statements prepared in accordance with U.S. GAAP have been condensed or omitted. These consolidated financial statements should be read in conjunction with the consolidated financial statements and accompanying notes included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2012. The results of operations for the three months ended March 31, 2013, are not necessarily indicative of the results to be expected for the full year ending December 31, 2013.

2. | Property and Equipment (including Concession Assets) |

Property and equipment, including concession assets, and related accumulated depreciation and amortization are summarized below (in millions):

March 31, 2013 | December 31, 2012 | ||||||

Land | $ | 76.9 | $ | 76.9 | |||

Concession land rights | 141.2 | 141.2 | |||||

Road property | 2,257.5 | 2,244.1 | |||||

Equipment | 553.7 | 552.5 | |||||

Technology and other | 31.2 | 31.6 | |||||

Construction in progress | 54.1 | 50.4 | |||||

Total property | 3,114.6 | 3,096.7 | |||||

Accumulated depreciation and amortization | 586.1 | 574.4 | |||||

Property and equipment (including concession assets), net | $ | 2,528.5 | $ | 2,522.3 | |||

Concession assets, net of accumulated amortization of $424.9 million and $413.3 million, totaled $1,923.1 million and $1,916.5 million at March 31, 2013 and December 31, 2012, respectively.

3. | Fair Value Measurements |

Assets and liabilities recognized at fair value are required to be classified into a three-level hierarchy. In general, fair values determined by Level 1 inputs utilize quoted prices (unadjusted) in active markets for identical assets or liabilities that the Company has the ability to access. Level 2 inputs include quoted prices for similar assets and liabilities in active markets and inputs other than quoted prices that are observable for the asset or liability. Level 3 inputs are unobservable inputs for the asset or liability and include situations where there is little, if any, market activity for the asset or liability. In certain cases, the inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, the level in the fair value hierarchy within which the fair value measurement in its entirety falls has been determined based on the lowest level input that is significant to the fair value measurement in its entirety. The Company’s assessment of the significance of a particular input to the fair value in its entirety requires judgment and considers factors specific to the asset or liability.

The Company’s derivative financial instruments are measured at fair value on a recurring basis and consist of foreign currency forward contract agreements, which are classified as Level 2 instruments. The Company determines the fair value of its derivative financial instrument positions based upon pricing models using inputs observed from actively quoted markets and also takes into consideration the contract terms as well as other inputs, including forward interest rate curves and market currency exchange rates. The fair value of the foreign currency forward contracts assets was $9.1 million as of March 31, 2013.

The Company’s short-term financial instruments include cash and cash equivalents, accounts receivable and accounts payable. The carrying value of the short-term financial instruments approximates their fair value.

7

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Notes to Consolidated Financial Statements—(Continued)

The fair value of the Company’s debt, including related company debt, is estimated using quoted market prices when available. When quoted market prices are not available, fair value is estimated based on current market interest rates for debt with similar maturities and credit quality. The fair value of the Company’s debt was $1,165.4 million and $1,240.9 million at March 31, 2013 and December 31, 2012, respectively. The carrying value was $1,072.7 million and $1,135.1 million at March 31, 2013 and December 31, 2012, respectively. If the Company’s debt were measured at fair value, the individual debt instruments would have been classified as either Level 1 or Level 2 in the fair value hierarchy.

4. | Derivative Instruments |

In general, the Company enters into derivative transactions in certain situations based on management’s assessment of current market conditions and perceived risks. Management intends to respond to evolving business and market conditions and in doing so, may enter into such transactions more frequently as deemed appropriate.

Credit Risk. As a result of the use of derivative instruments, the Company is exposed to counterparty credit risk. The Company manages this risk by limiting its counterparties to large financial institutions which meet the Company’s credit rating standards and have an established banking relationship with the Company. As of March 31, 2013, the Company did not expect any losses as a result of default of its counterparties.

Foreign Currency Forward Contracts. The Company has net U.S. dollar-denominated liabilities (primarily debt) which, for Mexican income tax purposes, are subject to periodic revaluation based on changes in the value of the U.S. dollar against the Mexican peso. This revaluation creates fluctuations in the Company’s income tax expense and the amount of income taxes paid. In the first quarter of 2013, the Company entered into foreign currency forward contracts with an aggregate notional amount of $250.0 million to hedge its exposure to this foreign currency risk. The contracts mature on December 31, 2013, and obligate the Company to purchase a total of Ps.3,275.3 million at a weighted average exchange rate of Ps.13.10 to each U.S. dollar. The Company has not designated these forward contracts as hedging instruments for accounting purposes. The Company marks the contracts to market and recognizes any gain or loss on the foreign currency forward contracts in foreign exchange gain (loss) within the consolidated statements of comprehensive income.

The following table presents the fair value of derivative instruments included in the consolidated balance sheet (in millions):

Asset Derivatives | ||||||||||

Balance Sheet Location | March 31, 2013 | December 31, 2012 | ||||||||

Derivatives not designated as hedging instruments: | ||||||||||

Foreign currency forward contracts | Other current assets | $ | 9.1 | $ | — | |||||

Total derivatives not designated as hedging instruments | 9.1 | — | ||||||||

Total asset derivatives | $ | 9.1 | $ | — | ||||||

The following table presents the amounts affecting the consolidated statements of comprehensive income for the three months ended March 31 (in millions):

Location of Gain/(Loss) Recognized in Income on Derivative | Amount of Gain/(Loss) Recognized in Income on Derivative | |||||||||

Derivatives not designated as hedging instruments: | 2013 | 2012 | ||||||||

Foreign currency forward contracts | Foreign exchange gain | $ | 9.1 | $ | — | |||||

Total | $ | 9.1 | $ | — | ||||||

8

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Notes to Consolidated Financial Statements—(Continued)

5. | Long-Term Debt |

In March 2013, the Company announced that it would redeem all of the remaining $98.1 million aggregate principal amount of the 12½% senior unsecured notes due April 1, 2016 (the “12½% Senior Notes”) pursuant to a provision which allows KCSM to redeem the 12½% Senior Notes on or after April 1, 2013, at a redemption price equal to 106.250% of the principal amount. As a result, the Company has classified the outstanding amount of the 12½% Senior Notes as a current liability as of March 31, 2013.

On April 1, 2013, the Company redeemed the 12½% Senior Notes using $65.0 million of borrowings under KCSM’s revolving credit facility and cash on hand. The Company will recognize approximately $10.4 million of debt retirement costs associated with the redemption in the second quarter of 2013.

6. | Commitments and Contingencies |

Concession Duty. Under KCSM’s 50-year railroad concession from the Mexican government (the “Concession”), KCSM paid concession duty expense of 0.5% of gross revenues for the first 15 years of the Concession period, and on June 24, 2012, KCSM began paying 1.25% of gross revenues, which is effective for the remaining years of the Concession. For the three months ended March 31, 2013, the concession duty expense, which is recorded within materials and other in operating expenses, was $3.4 million, compared to $1.3 million for the same period in 2012.

Litigation. The Company is a party to various legal proceedings and administrative actions, all of which, except as set forth below, are of an ordinary, routine nature and incidental to its operations. KCSM aggressively defends these matters and has established liability provisions, which management believes are adequate to cover expected costs. Although it is not possible to predict the outcome of any legal proceeding, in the opinion of management, other than those proceedings described in detail below, such proceedings and actions should not, individually or in the aggregate, have a material adverse effect on the Company’s consolidated financial statements.

Environmental Liabilities. The Company’s operations are subject to Mexican federal and state laws and regulations relating to the protection of the environment through the establishment of standards for water discharge, water supply, emissions, noise pollution, hazardous substances and transportation and handling of hazardous and solid waste. The Mexican government may bring administrative and criminal proceedings, impose economic sanctions against companies that violate environmental laws and temporarily or even permanently close non-complying facilities.

The risk of incurring environmental liability is inherent in the railroad industry. As part of serving the petroleum and chemicals industry, the Company transports hazardous materials and has a professional team available to respond to and handle environmental issues that might occur in the transport of such materials.

The Company performs ongoing reviews and evaluations of the various environmental programs and issues within the Company’s operations and, as necessary, takes actions intended to limit the Company’s exposure to potential liability. Although these costs cannot be predicted with certainty, management believes that the ultimate outcome of identified matters will not have a material adverse effect on the Company’s consolidated financial statements.

Certain Disputes with Ferromex. KCSM and Ferrocarril Mexicano, S.A. de C.V. (“Ferromex”) use certain trackage rights, haulage rights and interline services (the “Services”) provided by each other. The rates to be charged after January 1, 2009, were agreed to pursuant to the Trackage Rights Agreement, dated February 9, 2010 (the “Trackage Rights Agreement”), between KCSM and Ferromex. The rates payable for these Services for the period beginning in 1998 through December 31, 2008, are still not resolved. KCSM is currently involved in discussions with Ferromex regarding the amounts payable to each other for the Services for this period. If KCSM cannot reach an agreement with Ferromex for rates applicable for Services which were provided prior to January 1, 2009, which are not subject to the Trackage Rights Agreement, the Secretaría de Comunicaciones y Transportes (“Secretary of Communications and Transportation” or “SCT”) is entitled to set the rates in accordance with Mexican law and regulations. KCSM and Ferromex both initiated administrative proceedings seeking a determination by the SCT of the rates that KCSM and Ferromex should pay each other in connection with the Services. The SCT issued rulings in 2002 and 2008 setting the rates for the Services, and both KCSM and Ferromex challenged these rulings. Although KCSM and Ferromex have challenged these matters based on different grounds and these cases continue to evolve, management believes the amounts recorded related to these matters are adequate.

While the outcome of these matters cannot be predicted with certainty, the Company does not believe, when resolved, that these disputes will have a material effect on its consolidated financial statements.

9

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Notes to Consolidated Financial Statements—(Continued)

Contractual Agreements. In the normal course of business, the Company enters into various contractual agreements related to commercial arrangements and the use of other railroads’ or governmental entities’ infrastructure needed for the operations of the business. The Company is involved or may become involved in certain disputes involving transportation rates, product loss or damage, charges and interpretations related to these agreements. While the outcome of these matters cannot be predicted with certainty, the Company does not believe, when resolved, that these disputes will have a material effect on its consolidated financial statements.

Credit Risk. The Company continually monitors risks related to economic changes and certain customer receivables concentrations. Significant changes in customer concentration or payment terms, deterioration of customer creditworthiness or further weakening in economic trends could have a significant impact on the collectability of KCSM’s receivables and operating results. If the financial condition of KCSM’s customers were to deteriorate, resulting in an impairment of their ability to make payments, additional allowances may be required. The Company has recorded provisions for uncollectability based on its best estimate at March 31, 2013.

Income Tax. Tax returns filed for periods after 2006 remain open to examination by the taxing authorities. KCSM's 2007 tax return is currently under examination by the Servicio de Administracion Tributaria (the “SAT”), the Mexican equivalent of the U.S. Internal Revenue Service. The Company received an audit assessment for the year ended December 31, 2005, from the SAT. The Company initiated administrative proceedings with the SAT, and if a settlement is not reached, the matter will be litigated. The Company believes that it will more likely than not prevail in challenging the 2005 assessment. The Company believes that an adequate provision has been made for any adjustment (taxes and interest) that will be due for all open years. However, an unexpected adverse resolution could have a material effect on the consolidated financial statements in a particular quarter or fiscal year.

7. | Subsequent Event |

On April 10, 2013, KCSM commenced a cash tender offer for (i) any and all of its 8.0% Senior Notes due 2018 (the “8.0% Senior Notes”), (ii) any and all of its 65/8% Senior Notes due 2020 (the “65/8% Senior Notes”) and (iii) an amount of its 61/8% Senior Notes due 2021 (the “61/8% Senior Notes”) such that the aggregate consideration (including any tender offer consideration and early tender payment, but excluding accrued and unpaid interest) paid to the holders of the 61/8% Senior Notes does not exceed $650.0 million less the aggregate consideration paid or payable by KCSM to the holders of its 8.0% Senior Notes and 65/8% Senior Notes accepted for payment in connection with the tender offer. In addition, KCSM concurrently commenced consent solicitations to amend the indentures governing the 8.0% Senior Notes and the 65/8% Senior Notes to eliminate substantially all of the restrictive covenants and certain events of default contained therein. These cash tender offers and consent solicitations will expire on May 7, 2013, unless extended by KCSM and are subject to various conditions, including that KCSM completes a debt financing transaction on terms and conditions acceptable to KCSM.

10

Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

The discussion below, as well as other portions of this Form 10-Q, contain forward-looking statements that are not based upon historical information. Readers can identify these forward-looking statements by the use of such verbs as “expects,” “anticipates,” “believes” or similar verbs or conjugations of such verbs. Such forward-looking statements are based upon information currently available to management and management’s perception thereof as of the date of this Form 10-Q. However, such statements are dependent on and, therefore, can be influenced by, a number of external variables over which management has little or no control, including: competition and consolidation within the transportation industry; the business environment in industries that produce and consume rail freight; revocation of KCSM’s concession; the termination of, or failure to renew, agreements with customers, other railroads and third parties; interest rates; access to capital; disruptions to the Company’s technology infrastructure, including its computer systems; natural events such as severe weather, hurricanes and floods; market and regulatory responses to climate change; credit risk of customers and counterparties and their failure to meet their financial obligations; legislative and regulatory developments and disputes; rail accidents or other incidents or accidents along KCSM’s rail network, facilities or customer facilities involving the release of hazardous materials, including toxic inhalation hazards; fluctuation in prices or availability of key materials, in particular diesel fuel; dependency on certain key suppliers of core rail equipment; changes in securities and capital markets; labor difficulties, including strikes and work stoppages; insufficiency of insurance to cover lost revenue, profits or other damages; acts of terrorism or risk of terrorist activities; war or risk of war; domestic and international economic conditions; political and economic conditions in Mexico and the level of trade between Mexico and the United States; and the outcome of claims and litigation. For more discussion about each risk factor, see Part I, Item 1A –“Risk Factors” in the Company’s Annual Report on Form 10-K for the year ended December 31, 2012, which is on file with the U.S. Securities and Exchange Commission (File No. 333-08322) and any updates contained herein. Readers are strongly encouraged to consider these factors when evaluating forward-looking statements. Forward-looking statements should not be read as a guarantee of future performance or results and will not necessarily be accurate indications of the timing when, or by which, such performance or results will be achieved. As a result, actual outcomes or results could materially differ from those indicated in forward-looking statements. We are not under any obligation, and we expressly disclaim any obligation, to update or alter any forward-looking statements.

This discussion is intended to clarify and focus on Kansas City Southern de México, S. A. de C.V.’s (“KCSM” or the “Company”) results of operations, certain changes in its financial position, liquidity, capital structure and business developments for the periods covered by the consolidated financial statements included under Item 1 of this Form 10-Q, and has been abbreviated pursuant to General Instruction H(2)(a) of Form 10-Q. This discussion should be read in conjunction with those consolidated financial statements and the related notes and is qualified by reference to them.

Critical Accounting Policies and Estimates

The Company’s discussion and analysis of its financial position and results of operations is based upon its consolidated financial statements. The preparation of these consolidated financial statements requires estimation and judgment that affect the reported amounts of revenue, expenses, assets and liabilities. The Company bases its estimates on historical experience and on various other factors that are believed to be reasonable under the circumstances, the results of which form the basis for making judgments about the accounting for assets and liabilities that are not readily apparent from other sources. If the estimates differ materially from actual results, the impact on the consolidated financial statements may be material. The Company’s critical accounting policies are disclosed in the 2012 Annual Report on Form 10-K.

First Quarter Analysis

The Company reported net income of $54.2 million for the three months ended March 31, 2013, compared to net income of $36.8 million for the same period in 2012.

The Company reported a 4% increase in revenues during the three months ended March 31, 2013, as compared to the same period in 2012, due to a 4% increase in revenue per carload/unit, which includes positive pricing and fuel surcharge impacts, partially offset by commodity mix due to the unfavorable impact from agriculture and minerals. Carloads/unit volumes were flat for the three months ended March 31, 2013, compared to the same period in 2012. Revenues increased for all commodity groups other than agriculture and minerals, which decreased by $17.7 million due to a 49% decrease in import grain volumes resulting from the severe drought conditions experienced in the Midwestern region of the U.S. during 2012.

Operating expenses increased 2% during the three months ended March 31, 2013, as compared to the same period in 2012, due to the market-based premium for employee services paid to KCSM Servicios, S.A. de C.V. (“KCSM Servicios”), higher diesel fuel prices and an increase in depreciation and amortization expense. These increases were partially offset by lower deferred statutory profit sharing expense. Operating expenses as a percentage of revenues decreased to 64.9% for the three months ended March 31, 2013, as compared to 66.2% for the same period in 2012.

11

KCSM’s revenues and operating expenses are affected by fluctuations in the value of the Mexican peso against the U.S. dollar. Based on the volume of revenue and expense transactions denominated in Mexican pesos, revenue and expense fluctuations generally offset, with insignificant net impacts to operating income.

Results of Operations

The following summarizes KCSM’s consolidated statements of comprehensive income components (in millions):

Three Months Ended | Change Dollars | ||||||||||

March 31, | |||||||||||

2013 | 2012 | ||||||||||

Revenues | $ | 255.3 | $ | 245.2 | $ | 10.1 | |||||

Operating expenses | 165.7 | 162.3 | 3.4 | ||||||||

Operating income | 89.6 | 82.9 | 6.7 | ||||||||

Equity in net earnings of unconsolidated affiliates | 0.7 | 0.8 | (0.1 | ) | |||||||

Interest expense | (21.5 | ) | (22.5 | ) | 1.0 | ||||||

Foreign exchange gain | 12.9 | 2.9 | 10.0 | ||||||||

Other expense, net | (0.1 | ) | (0.1 | ) | — | ||||||

Income before income taxes | 81.6 | 64.0 | 17.6 | ||||||||

Income tax expense | 27.4 | 27.2 | 0.2 | ||||||||

Net income | $ | 54.2 | $ | 36.8 | $ | 17.4 | |||||

Revenues

The following summarizes revenues (in millions), carload/unit statistics (in thousands) and revenue per carload/unit:

Revenues | Carloads and Units | Revenue per Carload/Unit | ||||||||||||||||||||||||||||

Three Months Ended March 31, | Three Months Ended March 31, | Three Months Ended March 31, | ||||||||||||||||||||||||||||

2013 | 2012 | % Change | 2013 | 2012 | % Change | 2013 | 2012 | % Change | ||||||||||||||||||||||

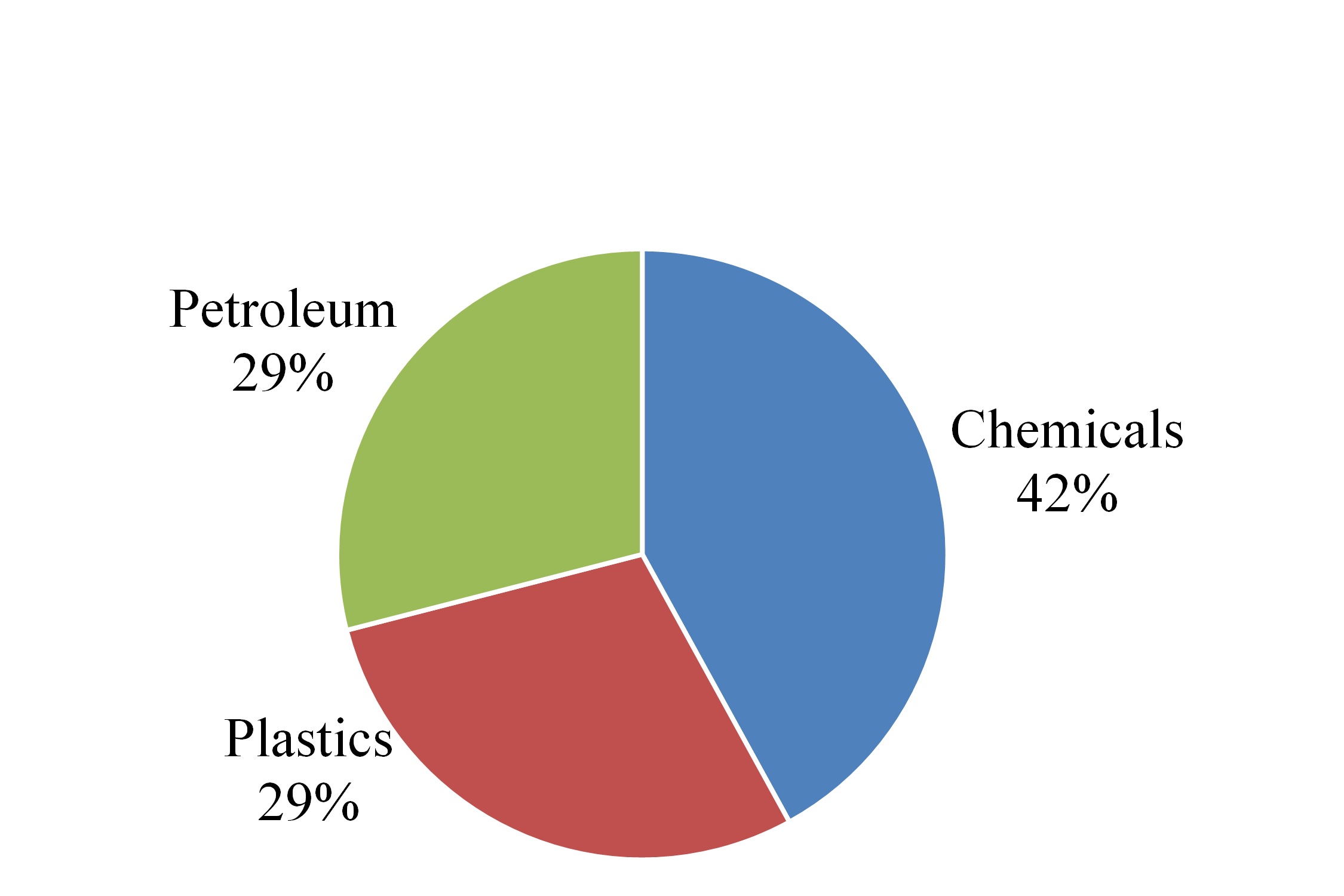

Chemical and petroleum | $ | 49.5 | $ | 47.0 | 5 | % | 23.7 | 23.9 | (1 | %) | $ | 2,089 | $ | 1,967 | 6 | % | ||||||||||||||

Industrial and consumer products | 66.8 | 60.6 | 10 | % | 43.1 | 41.3 | 4 | % | 1,550 | 1,467 | 6 | % | ||||||||||||||||||

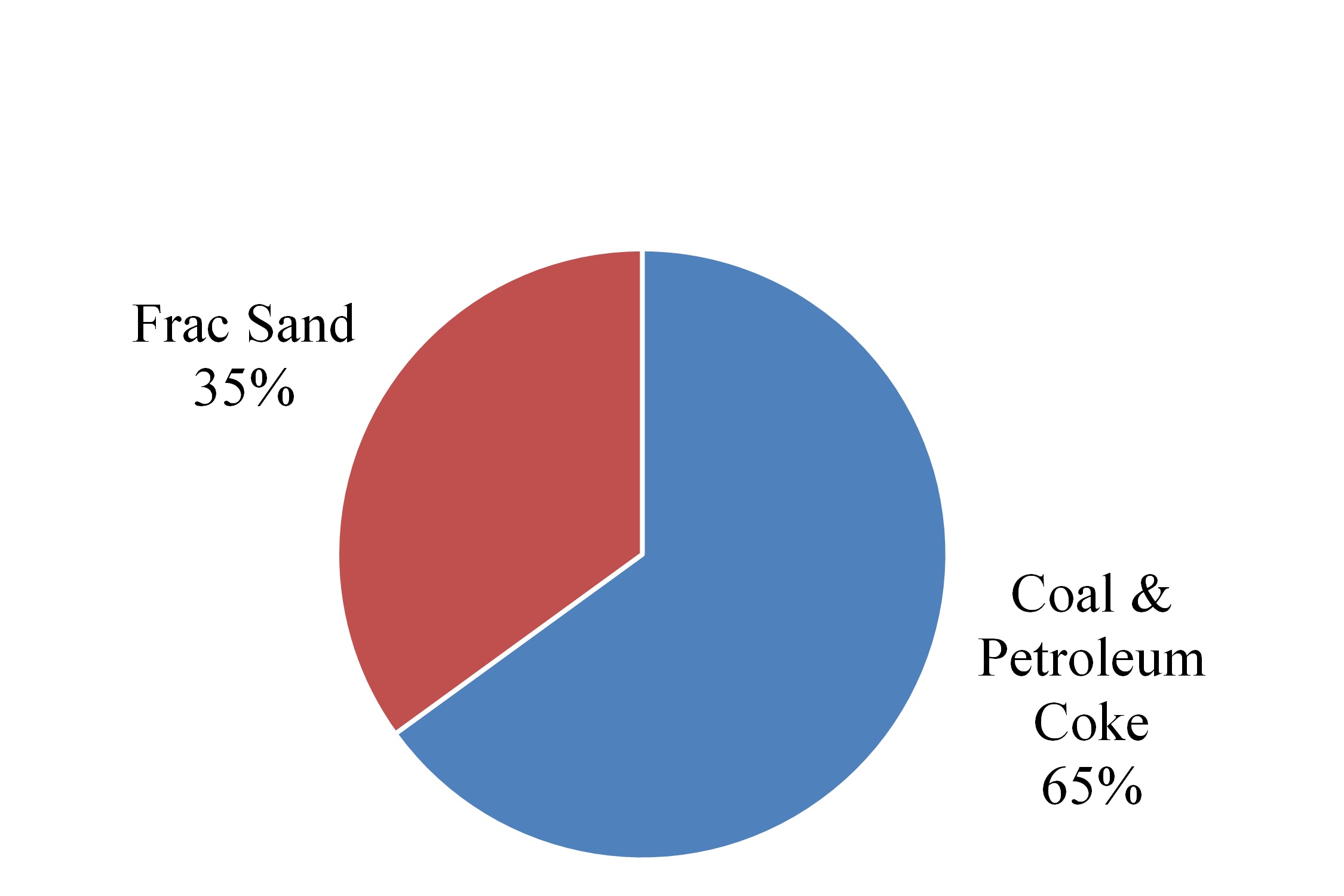

Agriculture and minerals | 33.1 | 50.8 | (35 | %) | 19.2 | 28.1 | (32 | %) | 1,724 | 1,808 | (5 | %) | ||||||||||||||||||

Energy | 7.0 | 6.4 | 9 | % | 7.1 | 7.0 | 1 | % | 986 | 914 | 8 | % | ||||||||||||||||||

Intermodal | 50.2 | 42.2 | 19 | % | 114.5 | 109.5 | 5 | % | 438 | 385 | 14 | % | ||||||||||||||||||

Automotive | 44.6 | 34.5 | 29 | % | 24.0 | 20.7 | 16 | % | 1,858 | 1,667 | 11 | % | ||||||||||||||||||

Carload revenues, carloads and units | 251.2 | 241.5 | 4 | % | 231.6 | 230.5 | — | % | $ | 1,085 | $ | 1,048 | 4 | % | ||||||||||||||||

Other revenue | 4.1 | 3.7 | 11 | % | ||||||||||||||||||||||||||

Total revenues (i) | $ | 255.3 | $ | 245.2 | 4 | % | ||||||||||||||||||||||||

(i) Included in revenues: | ||||||||||||||||||||||||||||||

Fuel surcharge | $ | 38.9 | $ | 33.4 | ||||||||||||||||||||||||||

Freight revenues include both revenue for transportation services and fuel surcharges. For the three months ended March 31, 2013, revenues increased $10.1 million compared to the same period in 2012. This 4% increase in revenues is due to a 4% increase in revenue per carload/unit, which includes positive pricing and fuel surcharge impacts, partially offset by commodity mix due to the unfavorable impact from agriculture and minerals. Carloads/unit volumes were flat for the three months ended March 31, 2013, compared to the same period in 2012. Revenues increased for all commodity groups other than agriculture and minerals, which decreased $17.7 million due to a 49% decrease in import grain volumes resulting from the severe drought conditions experienced in the Midwestern region of the U.S. during 2012.

12

KCSM’s fuel surcharge is a mechanism to adjust revenue based upon changing fuel prices. Fuel surcharge is calculated using a fuel price from a prior time period that can be up to 60 days earlier. In a period of volatile fuel prices or changing customer business mix, changes in fuel expense and fuel surcharge may differ.

The following discussion provides an analysis of revenues by commodity group:

Revenues by commodity group for the three months ended March 31, 2013 | |

Chemical and petroleum. Revenues increased $2.5 million for the three months ended March 31, 2013, compared to the same period in 2012, due to a 6% increase in revenue per carload/unit and a 1% decrease in carload/unit volumes. The increase in revenues is due to increases in pricing, fuel surcharge and petroleum volume due to the recovery of a portion of a customer’s lost business. This was partially offset by decreases in chemical volumes due to slow demand and alternate sourcing. |  |

Industrial and consumer products. Revenues increased $6.2 million for the three months ended March 31, 2013, compared to the same period in 2012, due to a 6% increase in revenue per carload/unit and a 4% increase in carload/unit volumes. Metals and scrap revenues increased due to a high demand for slab and steel coil driven by strength in the automotive and oil and gas industries. |  |

Agriculture and minerals. Revenues decreased $17.7 million for the three months ended March 31, 2013, compared to the same period in 2012, due to a 32% decrease in carload/unit volumes and a 5% decrease in revenue per carload/unit. Import grain volumes decreased 49% primarily as a result of the severe drought conditions experienced in the Midwestern region of the U.S. during 2012. |  |

13

Revenues by commodity group for the three months ended March 31, 2013 | |

Energy. Revenues increased $0.6 million for the three months ended March 31, 2013, compared to the same period in 2012, due to an 8% increase in revenue per carload/unit due to pricing and a 1% increase in carload/unit volumes. |  |

Intermodal. Revenues increased $8.0 million for the three months ended March 31, 2013, compared to the same period in 2012, due to a 14% increase in revenue per carload/unit and a 5% increase in carload/unit volumes. The increase in revenue per carload/unit is due to increases in pricing and fuel surcharge. The increase in volume was driven by strong cross border auto part business and conversion of cross border general commodity truck traffic to rail.

Automotive. Revenues increased $10.1 million for the three months ended March 31, 2013, compared to the same period in 2012, due to a 16% increase in carload/unit volumes and an 11% increase in revenue per carload/unit. The growth was driven by new business, increased import/export volume through the Port of Lazaro Cardenas and strong year-over-year growth in North American automobile sales for Original Equipment Manufacturers.

Operating Expenses

Operating expenses, as shown below (in millions), increased $3.4 million for the three months ended March 31, 2013, compared to the same period in 2012, due to the market-based premium for employee services paid to KCSM Servicios, higher diesel fuel prices and an increase in depreciation and amortization expense. These increases were partially offset by a decrease in deferred statutory profit sharing expense as a result of the organizational restructuring in the second quarter of 2012.

KCSM pays KCSM Servicios, a wholly-owned subsidiary of KCS, market-based rates for employee services. For comparative purposes, amounts paid to KCSM Servicios are classified according to the nature of the services provided to KCSM and the market-based premium paid to KCSM Servicios is included within materials and other expense.

Three Months Ended | ||||||||||||||

March 31, | Change | |||||||||||||

2013 | 2012 | Dollars | Percent | |||||||||||

Compensation and benefits | $ | 28.6 | $ | 35.1 | $ | (6.5 | ) | (19 | %) | |||||

Purchased services | 35.8 | 36.2 | (0.4 | ) | (1 | %) | ||||||||

Fuel | 42.0 | 39.5 | 2.5 | 6 | % | |||||||||

Equipment costs | 20.0 | 18.1 | 1.9 | 10 | % | |||||||||

Depreciation and amortization | 24.6 | 22.1 | 2.5 | 11 | % | |||||||||

Materials and other | 14.7 | 11.3 | 3.4 | 30 | % | |||||||||

Total operating expenses | $ | 165.7 | $ | 162.3 | $ | 3.4 | 2 | % | ||||||

Compensation and benefits. Compensation and benefits decreased $6.5 million for the three months ended March 31, 2013, compared to the same period in 2012, due to a $7.3 million reduction in deferred statutory profit sharing expense as a result of the organizational restructuring in the second quarter of 2012, partially offset by annual salary and benefit rate increases.

Purchased services. Purchased services expense decreased $0.4 million for the three months ended March 31, 2013, compared to the same period in 2012, due to a decrease in track maintenance expense as a result of a termination of a maintenance contract, offset by increases in volume-sensitive costs, primarily joint facilities and security services expenses.

14

Fuel. Fuel expense increased $2.5 million for the three months ended March 31, 2013, compared to the same period in 2012, due to higher diesel fuel prices as the average price per gallon, including the unfavorable impact of fluctuations in the value of the Mexican peso against the U.S. dollar, increased from $2.54 to $2.88, partially offset by lower consumption and improved fuel efficiency.

Equipment costs. Equipment costs increased $1.9 million for the three months ended March 31, 2013, compared to the same period in 2012, due to an increase in the use of other railroads’ freight cars as a result of increased automotive traffic volumes.

Depreciation and amortization. Depreciation and amortization expense increased $2.5 million for the three months ended March 31, 2013, compared to the same period in 2012, due to a larger asset base.

Materials and other. Materials and other expense increased $3.4 million for the three months ended March 31, 2013, compared to the same period in 2012, due to the market-based premium for employee services paid to KCSM Servicios as a result of the organizational restructuring in the second quarter of 2012 and increased concession duty expense. KCSM paid concession duty expense of 0.5% of gross revenues for the first 15 years of the Concession period, and on June 24, 2012, KCSM began paying 1.25% of gross revenues, which is effective for the remaining years of the Concession.

Non-Operating Income and Expenses

Equity in net earnings of unconsolidated affiliates. Equity in earnings from the operations of Ferrocarril y Terminal del Valle de Mexico, S.A. de C.V. was $0.7 million for the three months ended March 31, 2013, compared to $0.8 million for the same period in 2012. This decrease was due to higher track maintenance costs.

Interest expense. Interest expense decreased $1.0 million for the three months ended March 31, 2013, compared to the same period in 2012, due to lower average debt balances, partially offset by higher average interest rates. During the three months ended March 31, 2013, the average debt balances and average interest rates were $1,100.2 million and 7.7% compared to $1,216.8 million and 7.3%, respectively, for the same period in 2012.

Foreign exchange gain. Fluctuations in the value of the Mexican peso against the U.S. dollar resulted in a foreign exchange gain of $12.9 million for the three months ended March 31, 2013, which includes a $9.1 million gain on foreign currency forward contracts, compared to a foreign exchange gain of $2.9 million for the same period in 2012. The Company did not enter into any foreign currency forward contracts during 2012.

Other expense, net. Other expense, net, was flat for the three months ended March 31, 2013, compared to the same period in 2012.

Income tax expense. Income tax expense increased $0.2 million for the three months ended March 31, 2013, compared to the same period in 2012, due to higher pre-tax income, partially offset by a lower effective tax rate due to foreign exchange rate fluctuations. The effective income tax rate was 33.6% for the three months ended March 31, 2013, compared to 42.5% for the same period in 2012.

Liquidity and Capital Resources

Overview

In recent years, KCSM has improved its financial strength and flexibility by extending debt maturities and increasing liquidity. As a result, the Company has recently received investment grade credit ratings from rating agencies as described in the Credit Ratings section below.

Though KCSM’s cash flows from operations are sufficient to fund operations, capital expenditures and debt service, the Company may, from time to time, incur debt to refinance existing indebtedness, buy out operating leases, or to fund equipment additions or new investments. On March 31, 2013, total available liquidity (the unrestricted cash balance plus revolving credit facility availability) was approximately $249.8 million, of which about $104.2 million was used to redeem the 12½% senior unsecured notes due April 1, 2016 (the “12½% Senior Notes”) in the second quarter of 2013 as further described below.

In March 2013, the Company announced that it would redeem all of the remaining $98.1 million aggregate principal amount of its 12½% Senior Notes, on April 1, 2013, at a redemption price equal to 106.250% of the principal amount. The Company redeemed the 12½% Senior Notes using $65.0 million of borrowings under KCSM’s revolving credit facility and cash on hand. The Company will recognize approximately $10.4 million of debt retirement costs associated with the redemption in the second quarter of 2013.

15

The Company believes, based on current expectations, that cash and other liquid assets, operating cash flows, access to debt capital markets and other available financing resources will be sufficient to fund anticipated operating expenses, capital expenditures, debt service costs and other commitments in the foreseeable future. The Company’s current financing instruments contain restrictive covenants which limit or preclude certain actions; however, the covenants are structured such that the Company has sufficient flexibility to conduct its operations. The Company was in compliance with all of its debt covenants as of March 31, 2013.

For a discussion of the agreements representing the indebtedness of KCSM, see “Item 8 Financial Statements and Supplemental Data – Note 7. Long-Term Debt” in KCSM’s Annual Report on Form 10-K for the year ended December 31, 2012.

KCSM’s operating results and financing alternatives can be unexpectedly impacted by various factors, some of which are outside of its control. For example, if KCSM were to experience a reduction in revenues or a substantial increase in operating costs or other liabilities, its earnings could be significantly reduced, increasing the risk of non-compliance with debt covenants. Additionally, KCSM is subject to external factors impacting debt and capital markets and its ability to obtain financing under reasonable terms is subject to market conditions. Volatility in capital markets and the tightening of market liquidity could impact KCSM’s access to capital. Further, KCSM’s cost of debt can be impacted by independent rating agencies, which assign debt ratings based on certain factors including credit measurements such as interest coverage and leverage ratios, liquidity and competitive position.

Credit Ratings. Three credit rating agencies provide their views of the Company’s outlook and ratings. In the first quarter of 2013, Standard & Poor’s Rating Services (“S&P”) upgraded the KCSM debt to investment grade. Fitch Ratings (“Fitch”) has assigned an investment grade Issuer Default Rating (“IDR”) to KCSM and rates the senior unsecured debt as investment grade. On April 17, 2013, Moody’s Investors Service (“Moody’s”) upgraded KCSM's senior unsecured debt to investment grade. Ratings and outlooks change from time to time and can be found on the websites of S&P, Moody’s and Fitch.

The upgrade of KCSM’s senior unsecured debt to investment grade by S&P in the first quarter of 2013, combined with the investment grade ratings previously assigned to KCSM by Fitch, triggered a “fall-away collateral” provision whereby KCSM’s credit facility became an unsecured obligation.

Cash Flow Information

Summary cash flow data follows (in millions):

Three Months Ended | |||||||

March 31, | |||||||

2013 | 2012 | ||||||

Cash flows provided by (used for): | |||||||

Operating activities | $ | 139.0 | $ | 75.7 | |||

Investing activities | (33.1 | ) | (31.2 | ) | |||

Financing activities | (65.3 | ) | (5.4 | ) | |||

Net increase in cash and cash equivalents | 40.6 | 39.1 | |||||

Cash and cash equivalents beginning of year | 9.2 | 15.7 | |||||

Cash and cash equivalents end of period | $ | 49.8 | $ | 54.8 | |||

Cash flows from operating activities increased $63.3 million for the three month period ended March 31, 2013, compared to the same period in 2012, primarily as a result of the $64.4 million increase in changes in working capital items, resulting mainly from the timing of certain payments and receipts. Net cash used for investing activities increased $1.9 million, due to lower proceeds received from disposal of properties and an increase in capital expenditures. Information regarding capital expenditures is provided below. Net cash used for financing activities increased $59.9 million due to related company debt payments.

Capital Expenditures

KCSM’s cash flows from operations are sufficient to fund capital expenditures; however, the Company may, from time to time, use external sources of cash (principally bank debt, public debt and private debt) to fund capital expenditures.

16

The following table summarizes capital expenditures by type (in millions):

Three Months Ended | |||||||

March 31, | |||||||

2013 | 2012 | ||||||

Roadway capital program | $ | 23.3 | $ | 18.3 | |||

Equipment | 6.5 | 2.6 | |||||

Information technology | 0.9 | 0.7 | |||||

Other | 2.3 | 1.4 | |||||

Total capital expenditures (accrual basis) | 33.0 | 23.0 | |||||

Change in capital accruals | 0.2 | 9.6 | |||||

Total cash capital expenditures | $ | 33.2 | $ | 32.6 | |||

For 2013, internally generated cash flows are expected to fund cash capital expenditures, which are currently estimated at approximately $200.0 million.

Other Matters

KCSM Servicios union employees are covered by one labor agreement, which was signed on June 23, 1997, between KCSM and the Sindicato de Trabajadores Ferrocarrileros de la República Mexicana (“Mexican Railroad Union”), for a term of 50 years, for the purpose of regulating the relationship between the parties. Approximately 80% of KCSM Servicios employees are covered by this labor agreement. The compensation terms under this labor agreement are subject to renegotiation on an annual basis and all other benefits are subject to negotiation every two years. As a result of the labor agreement signed on April 19, 2012, compensation terms for the period from July 1, 2012 through June 30, 2013, were finalized. KCSM Servicios provides employee services to KCSM, and KCSM pays KCSM Servicios market-based rates for these services. The union labor negotiations with the Mexican Railroad Union have not historically resulted in any strike, boycott or other disruption in KCSM’s business operations.

Item 3. | Quantitative and Qualitative Disclosures About Market Risk |

Omitted pursuant to General Instruction H(2)(c) of Form 10-Q.

Item 4. | Controls and Procedures |

(a) Disclosure Controls and Procedures.

As of the end of the period for which this Quarterly Report on Form 10-Q is filed, the Company’s President and Executive Representative and Chief Financial Officer have each reviewed and evaluated the effectiveness of the Company’s disclosure controls and procedures (as defined in Rules 13a-15(e) and 15d-15(e) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”)). Based on that evaluation, the President and Executive Representative and Chief Financial Officer have each concluded that the Company’s current disclosure controls and procedures are effective to ensure that information required to be disclosed by the Company in reports that it files or submits under the Exchange Act is recorded, processed, summarized and reported within the time periods specified in the Securities and Exchange Commission rules and forms, and include controls and procedures designed to ensure that information required to be disclosed by the Company in such reports is accumulated and communicated to the Company’s management, including the President and Executive Representative and Chief Financial Officer, as appropriate, to allow timely decisions regarding required disclosure.

(b) Changes in Internal Control over Financial Reporting.

There have not been any changes in the Company’s internal control over financial reporting that occurred during the first quarter of 2013 that have materially affected, or are reasonably likely to materially affect, the Company’s internal control over financial reporting.

17

PART II—OTHER INFORMATION

Item 1. | Legal Proceedings |

For information related to the Company’s legal proceedings, see Note 6 “Commitments and Contingencies,” under Part I, Item 1, of this quarterly report on Form 10-Q.

Item 1A. | Risk Factors |

There were no material changes during the quarter to the Risk Factors disclosed in Item 1A, “Risk Factors,” in KCSM’s Annual Report on Form 10-K for the year ended December 31, 2012.

Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds |

Omitted pursuant to General Instruction H(2)(b) of Form 10-Q.

Item 3. | Defaults Upon Senior Securities |

Omitted pursuant to General Instruction H(2)(b) of Form 10-Q.

Item 4. | Mine Safety Disclosures |

Omitted pursuant to General Instruction H(2)(b) of Form 10-Q.

Item 5. | Other Information |

None.

18

Item 6. | Exhibits |

Exhibit No. | Description of Exhibits Filed with this Report | |

31.1 | Principal Executive Officer’s Certification Pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 is attached to this Form 10-Q as Exhibit 31.1. | |

31.2 | Principal Financial Officer’s Certification Pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 is attached to this Form 10-Q as Exhibit 31.2. | |

32.1 | Principal Executive Officer’s Certification furnished Pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 is attached to this Form 10-Q as Exhibit 32.1. | |

32.2 | Principal Financial Officer’s Certification furnished Pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 is attached to this Form 10-Q as Exhibit 32.2. | |

101 | The following unaudited financial information from Kansas City Southern de México, S.A. de C.V.’s Quarterly Report on Form 10-Q for the quarter ended March 31, 2013, formatted in XBRL (Extensible Business Reporting Language) includes: (i) Consolidated Statements of Comprehensive Income for the three months ended March 31, 2013 and 2012, (ii) Consolidated Balance Sheets as of March 31, 2013 and December 31, 2012, (iii) Consolidated Statements of Cash Flows for the three months ended March 31, 2013 and 2012, and (iv) the Notes to Consolidated Financial Statements. | |

Exhibit No. | Description of Exhibits Incorporated by Reference | |

10.1 | Third Amendment to that certain Asset Pledge Agreement dated January 10, 2013, entered into by and among KCSM, Arrendadora KCSM, S. de R.L. de C.V., Highstar Harbor Holdings México, S. de R.L. de C.V., MTC Puerta Mexico, S. de R.L. de C.V., Vamos a México, S.A. de C.V. and, JPMorgan Chase Bank, N.A., as collateral agent, filed as Exhibit 10.1 to the Company's Current Report on Form 8-K, filed on January 16, 2013 (File No. 333-08322), is hereby incorporated by reference as Exhibit 10.1. | |

10.2 | Second Amendment Agreement to that certain Partnership Interest Pledge Agreement, dated January 10, 2013, entered into by and among KCSM, Nafta Rail, S.A. de C.V., Highstar Harbor Holdings México, S. de R.L. de C.V. and JPMorgan Chase Bank, N.A., as collateral agent, filed as Exhibit 10.2 to the Company's Current Report on Form 8-K, filed on January 16, 2013 (File No. 333-08322), is hereby incorporated by reference as Exhibit 10.2. | |

10.3 | Second Amendment Agreement to that certain Partnership Interest Pledge Agreement, dated January 10, 2013, entered into by and among KCSM, KCSM Holdings, LLC, Arrendadora KCSM, S. de R.L. de C.V. and JPMorgan Chase Bank, N.A., as collateral agent, filed as Exhibit 10.3 to the Company's Current Report on Form 8-K, filed on January 16, 2013 (File No. 333-08322), is hereby incorporated by reference as Exhibit 10.3. | |

10.4 | Second Amendment Agreement to that certain Stock Interest Pledge Agreement, dated January 10, 2013, entered into by and among MTC Puerta México, S. de R.L. de C.V., Highstar Harbor Holdings México, S. de R.L. de C.V, Vamos a México, S.A. de C.V. and JPMorgan Chase Bank, N.A., as collateral agent, filed as Exhibit 10.4 to the Company's Current Report on Form 8-K, filed on January 16, 2013 (File No. 333-08322), is hereby incorporated by reference as Exhibit 10.4. | |

10.5 | Second Amendment Agreement to that certain Partnership Interest Pledge Agreement, dated January 10, 2013, entered into by and among Highstar Harbor Holdings México, S. de R.L. de C.V., Nafta Rail, S.A. de C.V., MTC Puerta México, S. de R.L. de C.V. and JPMorgan Chase Bank, N.A., as collateral agent, filed as Exhibit 10.5 to the Company's Current Report on Form 8-K, filed on January 16, 2013 (File No. 333-08322), is hereby incorporated by reference as Exhibit 10.5. | |

19

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the Company has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized and in the capacities indicated on April 22, 2013.

Kansas City Southern de México, S.A. de C.V. | |

/s/ MICHAEL W. UPCHURCH | |

Michael W. Upchurch | |

Chief Financial Officer | |

(Principal Financial Officer) | |

/s/ MARY K. STADLER | |

Mary K. Stadler | |

Chief Accounting Officer | |

(Principal Accounting Officer) | |

20