Attached files

EXHIBIT 99.2

* First Quarter 2013 Conference Call April 22, 2013

* Forward-Looking Statements This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. All such statements, other than statements of historical fact, are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, including, without limitation, any projections of financial items; the timing of the closing of our pipelay vessel sales; projections of contracting services activity; future operations expenditures; projections of utilization; any statements of the plans, strategies and objectives of management for future operations; any statements concerning developments; any statements regarding future economic conditions or performance; any statements of expectation or belief; and any statements of assumptions underlying any of the foregoing. These statements involve certain assumptions we made based on our experience and perception of historical trends, current conditions, expected future developments and other factors we believe are reasonable and appropriate under the circumstances. The forward-looking statements are subject to a number of known and unknown risks, uncertainties and other factors that could cause our actual results to differ materially. The risks, uncertainties and assumptions referred to above include the performance of contracts by suppliers, customers and partners; delays, costs and difficulties related to the pipelay vessel sales; actions by governmental and regulatory authorities; operating hazards and delays; our ultimate ability to realize current backlog; employee management issues; local, national and worldwide economic conditions; complexities of global political and economic developments; geologic risks, volatility of oil and gas prices and other risks described from time to time in our reports filed with the Securities and Exchange Commission (“SEC”), including the Company’s most recently filed Annual Report on Form 10-K and in the Company’s other filings with the SEC. Free copies of the reports can be found at the SEC’s website, www.SEC.gov. You should not place undue reliance on these forward-looking statements which speak only as of the date of this presentation and the associated press release. We assume no obligation or duty and do not intend to update these forward-looking statements except as required by the securities laws.

* Presentation Outline Executive Summary Summary of Q1 2013 Results (pg. 4) Operational Highlights by Segment Contracting Services (pg. 9) Key Balance Sheet Metrics (pg. 14) 2013 Outlook (pg. 17) Non-GAAP Reconciliations (pg. 21) Questions & Answers

* Executive Summary *

* Executive Summary ($ in millions, except per share data) See non-GAAP reconciliation on slide 24. 1Q 2013 includes $14.1 million loss in connection with the settlement of our commodity hedge contracts associated with the oil and gas business, which were not included with the sale of ERT.

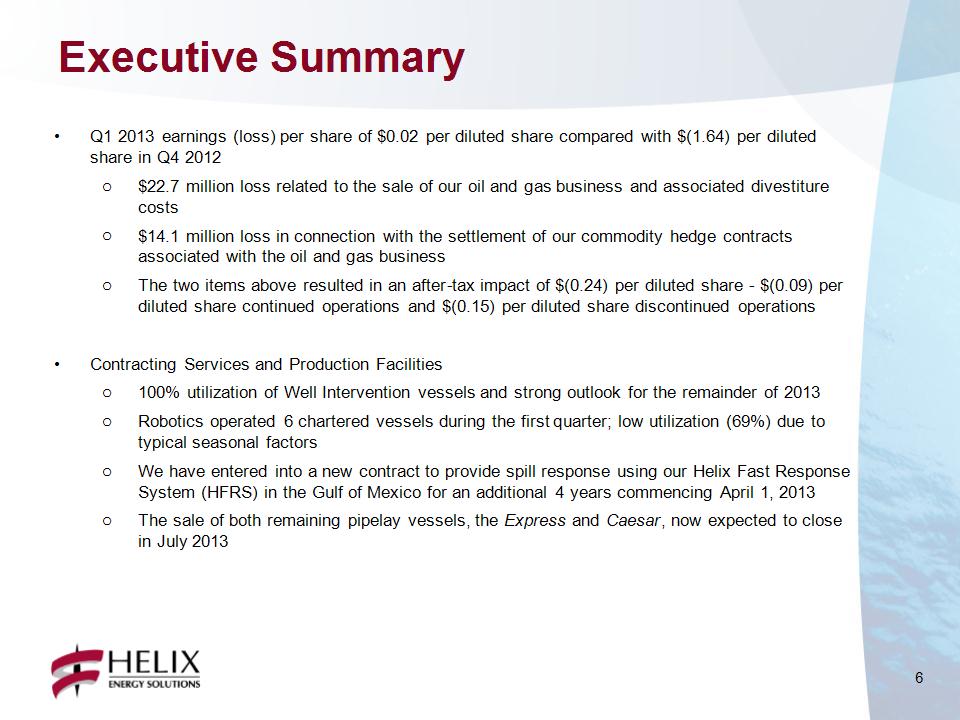

* Executive Summary Q1 2013 earnings (loss) per share of $0.02 per diluted share compared with $(1.64) per diluted share in Q4 2012 $22.7 million loss related to the sale of our oil and gas business and associated divestiture costs $14.1 million loss in connection with the settlement of our commodity hedge contracts associated with the oil and gas business The two items above resulted in an after-tax impact of $(0.24) per diluted share – $(0.09) per diluted share continued operations and $(0.15) per diluted share discontinued operations Contracting Services and Production Facilities 100% utilization of Well Intervention vessels and strong outlook for the remainder of 2013 Robotics operated 6 chartered vessels during the first quarter; low utilization (69%) due to typical seasonal factors We have entered into a new contract to provide spill response using our Helix Fast Response System (HFRS) in the Gulf of Mexico for an additional 4 years commencing April 1, 2013 The sale of both remaining pipelay vessels, the Express and Caesar, now expected to close in July 2013

* Executive Summary Balance sheet Cash increased to $626 million at 03/31/2013 from $437 million at 12/31/2012 Liquidity* at $1.1 billion at 03/31/2013 Net debt decreased to $72 million at 03/31/2013 from $582 million at 12/31/2012 $624 million in pre-tax proceeds from the sale of our oil and gas business in February 2013 $318 million of term loan debt retired in February 2013 See updated debt maturity profile on slide 15 Liquidity, as we define it, is equal to cash and cash equivalents ($626 million), plus available capacity under our revolving credit facility ($514 million).

* Operational Highlights *

* ($ in millions, except percentages) See non-GAAP reconciliation on slide 23. Amounts are prior to intercompany eliminations. Before gross profit impact of asset impairment charges: $157.8 million for the Caesar in Q4. 100% utilization for the Well Intervention fleet IRS no. 2 utilized on the Ocean Victory drilling rig H534 expected to commence work in Q3 Entered into multi-year contract for the Q5000 69% chartered vessel utilization in Robotics due to seasonality Pipelay vessels expected to remain fully booked until the close of the sale transactions in July 2013 Contracting Services

* GOM Q4000 100% utilized during Q1 IRS no. 2 utilized for 59 days onboard the Ocean Victory during the quarter Helix 534 remains on schedule for Q3 with full backlog the remainder of 2013 Extended contract with major operator for the Q4000 for 150 days per year for 2014–2015 Entered into five-year contract for the Q5000 with BP; initial utilization of 270 days annually North Sea Seawell and Well Enhancer fully utilized during Q1 on various well intervention projects Skandi Constructor is currently under contract to provide ROV support services for windfarm project Recently awarded commitment in West Africa for Q4 of 2013 Seawell and Well Enhancer fully booked in Q2 and Q3, and partially booked in Q4 of 2013 Contracting Services – Well Ops Helix 534 in Singapore Q5000 artist rendering

* 69% chartered vessel utilization in Q1 Four vessels under long-term charter, plus two vessels of opportunity 55% utilization for ROVs, trenchers, and ROVDrills Deep Cygnus idle for 75 days in Q1 T1200 aboard the Grand Canyon trenched and buried 60km of cables in the London Array windfarm offshore UK Olympic Triton commenced seismic cable lay project offshore Brazil, which continues into Q2 Entered into long-term lease agreement for the Rem Installer; vessel is currently under construction Three-year charter commencing mid-2013 (2) new 200hp work class ROVs Contracting Services – Robotics XLX ROV mobilizing in the Gulf of Mexico

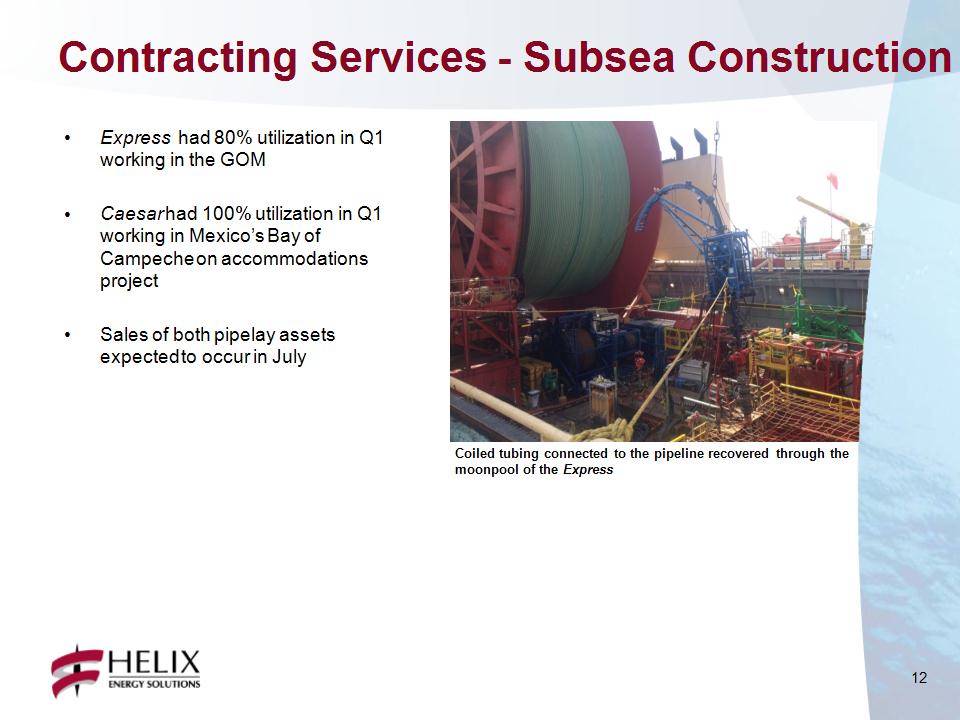

* Express had 80% utilization in Q1 working in the GOM Caesar had 100% utilization in Q1 working in Mexico’s Bay of Campeche on accommodations project Sales of both pipelay assets expected to occur in July Coiled tubing connected to the pipeline recovered through the moonpool of the Express Contracting Services – Subsea Construction

* Express Caesar Olympic Canyon (1) Deep Cygnus (1) Olympic Triton (1) Grand Canyon (1) (2) spot vessels (1) Seawell Well Enhancer Q4000 49 ROVs 2 ROVDrill Units 4 Trenchers (1) Chartered vessels. Contracting Services Utilization

* Key Balance Sheet Metrics *

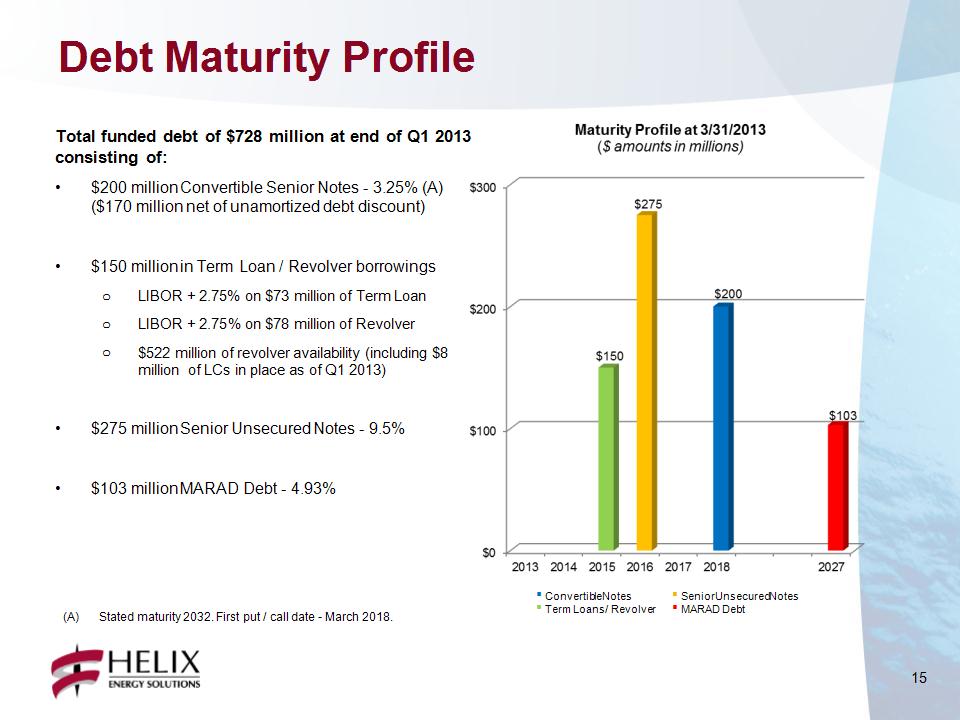

* Total funded debt of $728 million at end of Q1 2013 consisting of: $200 million Convertible Senior Notes – 3.25% (A) ($170 million net of unamortized debt discount) $150 million in Term Loan / Revolver borrowings LIBOR + 2.75% on $73 million of Term Loan LIBOR + 2.75% on $78 million of Revolver $522 million of revolver availability (including $8 million of LCs in place as of Q1 2013) $275 million Senior Unsecured Notes – 9.5% $103 million MARAD Debt – 4.93% Convertible Notes Term Loans / Revolver Senior Unsecured Notes MARAD Debt Debt Maturity Profile Stated maturity 2032. First put / call date – March 2018.

* Liquidity of approximately $1.1 billion at 3/31/2013 ($ amounts in millions) Includes impact of unamortized debt discount under our convertible senior notes. Liquidity, as we define it, is equal to cash and cash equivalents ($626 million), plus available capacity under our revolving credit facility ($514 million). Debt and Liquidity Profile

* 2013 Outlook *

* 2013 Outlook ($ in millions) 2013 Outlook and 2012 Actual includes $32 million and $367 million from Oil and Gas discontinued operations. 2013 Outlook excluding Subsea Construction and Oil and Gas, plus expected annualized contribution from Helix 534 and chartered Skandi Constructor vessel.

* 2013 Outlook Contracting Services Backlog as of March 31, 2013 was $1.6 billion (pro forma for Q4000 and Q5000 multi-year contracts signed the first week in April) Utilization expected to remain strong for the well intervention fleet Q4000 full backlog thru 2015 Q5000 initial backlog of 270 days annually over first 5 years of operations Helix 534 expected in service in Q3, full backlog for remainder of 2013 Building backlog into 2014 thru 2016 Seawell and Well Enhancer fully booked in Q2 and Q3, and partially booked in Q4 of 2013; backlog building into 2014 and 2015 Skandi Constructor initial backlog of 95 days; currently under contract providing ROV support services for windfarm project North Sea well intervention vessels have over 475 days of committed work in 2014 in the UK, Africa, and Canada Entered into long-term lease agreement for the Rem Installer and expect charter to commence mid-2013 Continuing to add ROV systems in 2013 to support commercial growth in our Robotics business The Express and Caesar expected to be fully utilized until the vessel sales close Ingleside shorebase now leased to EMAS-AMC thru the end of 2013

* 2013 Outlook - Capex Capital Expenditures Contracting Services (approximately $365 million in 2013) $61 million incurred in Q1 Q5000 new build (approximately $135 million in 2013) On schedule for delivery in 2015 Newly acquired Helix 534 continues conversion in Singapore into a well intervention vessel Estimated $190 million for vessel, conversion and intervention riser system (approximately $45 million remaining be incurred in 2013) Expect to deploy vessel in the Gulf of Mexico in Q3 2013 Approximately $45 million for intervention riser system and deck modifications for the Skandi Constructor (approximately $24 million remaining to be incurred in 2013) Continued incremental investment in Robotics business Maintenance capital for Seawell life extension and Helix Producer I dry dock

* Non-GAAP Reconciliations *

* Non-GAAP Reconciliations We calculate Adjusted EBITDA from continuing operations as earnings before net interest expense and other, taxes, depreciation and amortization. Adjusted EBITDAX is Adjusted EBITDA from continuing operations plus the earnings of our former oil and gas business before net interest expense and other, taxes, depreciation and amortization, and exploration expense. These non-GAAP measures are useful to investors and other internal and external users of our financial statements in evaluating our operating performance; they are widely used by investors in our industry to measure a company’s operating performance without regard to items which can vary substantially from company to company, and help investors meaningfully compare our results from period to period. Adjusted EBITDA from continuing operations and Adjusted EBITDAX should not be considered in isolation or as a substitute for, but instead is supplemental to, income from operations, net income and other income data prepared in accordance with GAAP. Non-GAAP financial measures should be viewed in addition to, and not as an alternative to our reported results prepared in accordance with GAAP. Users of this financial information should consider the types of events and transactions which are excluded from this measure. ($ in millions)

* Non-GAAP Reconciliations ($ in millions)

* * Follow Helix ESG on Twitter: www.twitter.com/Helix_ESG Join the discussion on LinkedIn: www.linkedin.com/company/helix