Attached files

| file | filename |

|---|---|

| 8-K - 8-K - KEYCORP /NEW/ | d521997d8k.htm |

| EX-99.3 - EX-99.3 - KEYCORP /NEW/ | d521997dex993.htm |

| EX-99.1 - EX-99.1 - KEYCORP /NEW/ | d521997dex991.htm |

KeyCorp

First Quarter 2013 Earnings Review

April 18, 2013

Beth E. Mooney

Chairman and

Chief Executive Officer

Jeffrey B. Weeden

Chief Financial Officer

Exhibit 99.2 |

2

FORWARD-LOOKING STATEMENTS AND ADDITIONAL

INFORMATION DISCLOSURE

This presentation contains and we may, from time to time, make forward-looking statements within

the meaning of the Private Securities Litigation Reform Act of 1995, including statements about

Key’s financial condition, results of operations, asset quality trends, capital levels and profitability. Forward-looking statements

are not historical facts but instead only represent management’s current expectations and

forecasts regarding future events, many of which, by their nature, are inherently uncertain and

outside of Key’s control. Forward-looking statements usually can be identified by the use of words such as “goal,” “objective,” “plan,”

“expect,” “anticipate,” “intend,” “project,”

“believe,” “estimate” or other words of similar meaning.

Our forward-looking statements are subject to the following principal risks and uncertainties:

continued strain on the global financial markets as a result of economic slowdowns and

concerns; the slow progress of the U.S. economic recovery; changes in trade, monetary and fiscal policies of various governmental

bodies and central banks in the economies in which we operate; our ability to anticipate interest rate

changes correctly and manage interest rate risk presented through unanticipated changes

in our interest rate risk position and/or short- and long-term interest rates; changes in local, regional and international business,

economic or political conditions in the regions where we operate or have significant assets; current

regulatory initiatives in the U.S., including the Dodd-Frank Wall Street Reform and

Consumer Protection Act of 2010, as amended, subjecting us to a variety of new and more stringent legal and regulatory requirements and

increased scrutiny from our regulators; the deterioration of unemployment or real estate asset values

or their failure to recover for an extended period of time; adverse changes in credit

quality trends; our ability to determine accurate values of certain assets and liabilities; adverse behaviors in securities, public debt, and

capital markets, including changes in market liquidity and volatility; unanticipated changes in our

liquidity position, including but not limited to our ability to enter the financial markets to

manage and respond to any changes to our liquidity position; the soundness of other financial institutions; our ability to satisfy new capital and

liquidity standards such as those imposed by the Dodd-Frank Act and those adopted by the Basel

Committee; our ability to receive dividends from our subsidiary, KeyBank; reductions of

the credit ratings assigned to KeyCorp and KeyBank; unexpected or prolonged changes in the level or cost of liquidity; our ability to secure

alternative funding sources under stressed liquidity conditions; our ability to timely and effectively

implement our strategic initiatives; operational or risk management failures; breaches of

security or failures of our technology systems due to technological, cybersecurity threats or other factors; the occurrence of

natural or man-made disasters or conflicts or terrorist attacks disrupting the economy or our

ability to operate; the adequacy of our risk management programs; adverse judicial

proceedings; increased competitive pressure due to consolidation; our ability to attract and/or retain talented executives and employees; our ability

to effectively sell additional products or services to new or existing customers; our ability to

manage our reputational risks; unanticipated adverse effects of acquisitions and

dispositions of assets, business units or affiliates. We provide greater detail regarding some

of these factors in our 2012 Form 10-K, including in Item 1. Business under the heading “Supervision and Regulation”, in

Item 1A. Risk Factors and in Item 7. Management’s Discussion and Analysis of Financial Condition

and Results of Operation under the heading “Risk Management,” as well as in our

subsequent SEC filings, all of which are accessible on our website at www.key.com/ir and on the SEC’s website at www.sec.gov.

Key does not undertake any obligation to update the forward-looking statements to reflect the

impact of circumstances or events that may arise after the date of the forward-looking

statements. Actual results or future events could differ, possibly materially, from those anticipated in forward-looking statements, as well as

from historical performance.

This presentation also includes certain Non-GAAP financial measures related to

“tangible common equity,” “Tier 1 common equity,” “pre-provision net revenue,”

and “cash efficiency ratio.” Management believes these ratios may assist investors,

analysts and regulators in analyzing Key’s financials. Although Key has

procedures in place to ensure that these measures are calculated using the appropriate GAAP or

regulatory components, they have limitations as analytical tools and should not be

considered in isolation, or as a substitute for analysis of results under GAAP. For more information on these calculations and to view the

reconciliations to the most comparable GAAP measures, please refer to the Appendix to this

presentation or our most recent earnings press release, which is accessible at

www.key.com/ir. Web addresses referenced in this slide are inactive textual references only. Information on

these websites is not part of this document. |

3

Net interest income up 5% compared to the prior year

Grew average C&I loans by 16% from the prior year

Pursuing growth opportunities: payments and technology

Achieved $105 million in annualized expense savings through 1Q13;

remainder of the $200 million target to be achieved by December 2013

Cash efficiency ratio improved to 66%

Improve

Efficiency

Actively managing businesses, with sale of Victory announced in February

No objection from Federal Reserve on 2013 capital plan submission

Repurchased $65 million in common shares during 1Q13 at an

average

cost of $9.56 per share

Optimize and

Grow

Revenue

Investor Highlights –

1Q13

Execution of strategy and differentiated business model driving results

Effectively

Manage

Capital

Investments in our businesses and work to create a more variable cost

structure will continue to impact expense levels

|

2013

Focus Areas 4

Execute Strategy with Distinctive Business Model

Maintain Moderate Risk Profile

Accelerate Revenue Growth with Opportunistic Investing

Align Cost Structure with Operating Environment

Leverage Strong Capital Position to Maximize Value |

5

Financial Review |

6

Financial Summary –

First Quarter 2013

Capital

(b)

Asset Quality

(a)

Financial

Performance

(a)

TE = Taxable equivalent, EOP = End of Period

(a)

From continuing operations

(b)

From consolidated operations

(c)

3-31-13 ratios are estimated

(d)

Non-GAAP measure: see Appendix for reconciliation

Income from continuing operations attributable to Key

$.21

$.20

$.20

common shareholders –

assuming dilution

Net interest margin (TE)

3.24%

3.37%

3.16%

Return on average total assets

.99

.96

1.01

Tier 1 common equity

(c), (d)

11.4%

11.4%

11.5%

Tier 1 risk-based capital

(c)

12.2

12.2

13.3

Tangible common equity to tangible assets

(d)

10.2

10.2

10.3

Book value per common share

$10.89

$10.78

$10.26

Net loan charge-offs to average loans

.38%

.44%

.82%

NPLs to EOP portfolio loans

1.24

1.28

1.35

NPAs to EOP portfolio loans + OREO + Other NPAs

1.34

1.39

1.55

Allowance for loan losses to period-end loans

1.70

1.68

1.92

Allowance for loan losses to NPLs

137.4

131.8

141.7

Metrics

1Q13

4Q12

1Q12 |

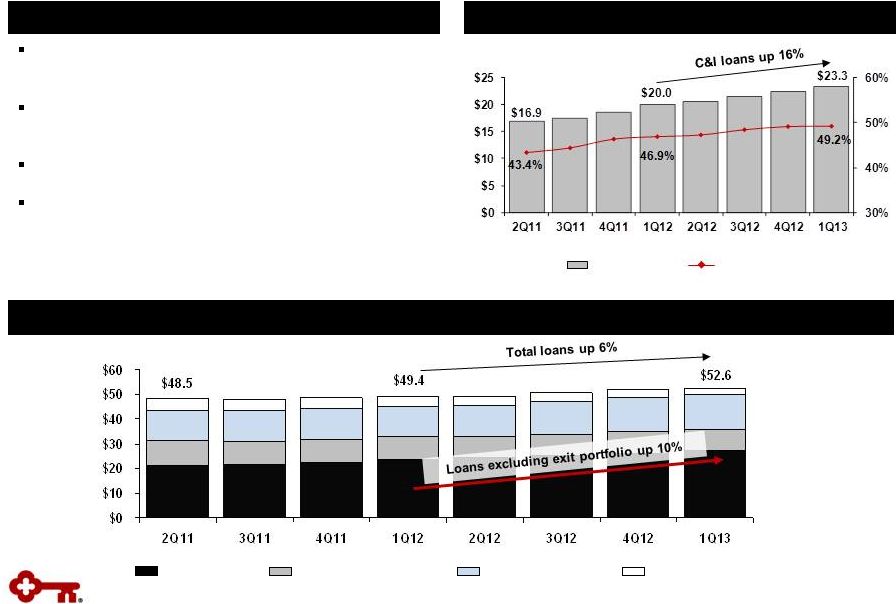

7

Average loan growth driven by C&I, while the exit

portfolio continues to run-off

Originated $8.5 billion in new or renewed lending

commitments during 1Q13

C&I commitment utilization increased to 49.2%

Clients remained cautious in their borrowing

following a strong 4Q12

Loan Growth

$ in billions

Highlights

Average Commercial & Industrial Loans

C&I loans

Utilization rate

Average Loans

Exit Portfolios

Home Equity & Other

C&I & Leasing

Commercial Real Estate

$ in billions |

Improving Deposit Mix

Highlights

Funding Cost

Overall funding cost continues to improve, with

total deposit cost declining to 29 bps

Transaction deposit balances up 14% from 1Q12

Total CD maturities and average cost

2013 Q2: $2.0 billion at 0.85%

2013 Q3: $1.3 billion at 1.30%

2013 Q4: $0.8 billion at 1.37%

2014: $2.2 billion at 1.97%

2015 & beyond: $1.1 billion at 2.60%

Average

Deposits

(a)

$ in billions

(a)

Excludes deposits in foreign office

(b)

Transaction deposits include noninterest-bearing, NOW, and MMDA

Cost of total deposits

(a)

Interest-bearing liability cost

CDs and other time deposits

Savings

Noninterest-bearing

NOW and MMDA

8

–

–

–

–

– |

9

Total Revenue

TE = Taxable equivalent

Continuing Operations

Net interest margin

Highlights

Net Interest Margin (TE) Trend

Net interest income increased 5% from prior

year, with net interest margin up 8 basis points

Net interest margin compared to prior quarter

impacted by lower asset yields and higher

liquidity

Noninterest income reflects seasonal change

from strong 4Q12

Total Revenue Mix

Noninterest income

$ in millions

$570

$559

$589

$422

$442

$425

$0

$400

$800

$1,200

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

Impact of leveraged lease

early termination

Net interest income (TE)

$1,001

$1,014

$992

3.19%

3.16%

3.24%

2.00%

2.50%

3.00%

3.50%

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13 |

10

Focused Expense Management

Significant progress made on efficiency initiative

–

Achieved $105 million in annualized expense

savings through 1Q13

–

On target for $200 million in expense savings

by December 2013, with full-year impact

expected in 2014

1Q13 expense included $15 million related to

efficiency initiative

Focused on disciplined expense management

with variability in 2013 anticipated from:

–

Technology investments

–

Costs related to efficiency initiative

(a)

Includes ongoing, one-time and amortization expenses

Highlights

Noninterest Expense

Q-o-Q Change in Noninterest Expense

(a) |

11

Nonperforming Assets

Net Charge-offs & Provision for Loan and Lease Losses

NPLs

NPLs to period-end loans

NCOs

Provision for loan and

lease losses

NCOs to average loans

$ in millions

$ in millions

NPLs held for sale,

OREO & other NPAs

Continued Improvement in Asset Quality

Highlights

Net loan charge-offs decreased 51% from 1Q12

to $49 million, or 38 bps of average loans

1Q13 commercial loan net charge-offs

were $5 million or 6 bps

Asset quality reaching normalized levels, with

net charge-offs expected to be within targeted

range

Allowance for Loan and Lease Losses

Allowance for loan and

lease losses to NPLs

Allowance for loan

and lease losses

$ in millions

$950

$767

$705

1.76%

1.35%

1.24%

.00%

1.00%

2.00%

3.00%

$0

$400

$800

$1,200

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

$1,230

$944

$893

146%

142%

137%

100%

120%

140%

160%

$0

$250

$500

$750

$1,000

$1,250

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13 |

12

No objection from Federal Reserve on capital plan

–

Board authorized share repurchase program

of up to $426 million

–

Dividend increase will be considered at May

Board meeting

Disciplined capital management process

–

Repurchased $65 million in common shares

during 1Q13, pursuant to 2012 capital plan

Estimated Basel III Tier 1 common equity

ratio of 10.3%

(a), (b)

Tier 1 Common Equity

(b), (c)

Tangible Common Equity to Tangible Assets

(b)

Strong Capital Ratios

Highlights

Book Value per Share

10.2%

9.7%

10.3%

0.0%

3.0%

6.0%

9.0%

12.0%

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

$10.89

$10.26

$9.88

$8.00

$9.00

$10.00

$11.00

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

11.4%

11.1%

11.5%

0.0%

3.0%

6.0%

9.0%

12.0%

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

(a)

Based upon March 31, 2013 pro forma analysis; see Appendix for further

detail (b)

Non-GAAP measure: see Appendix for reconciliations

(c)

3-31-13 ratio is estimated |

13

Appendix |

14

Progress on Targets for Success

KEY Business

Model

KEY Metrics

(a)

KEY

1Q13

KEY

4Q12

Targets

Action Plans

Core funded

Loan to deposit ratio

(b)

87%

86%

90-100%

Use integrated model to grow relationships

and loans

Improve deposit mix

Returning to a

moderate risk

profile

NCOs to average loans

.38%

.44%

40-60 bps

Focus on relationship clients

Exit noncore portfolios

Limit concentrations

Focus on risk-adjusted returns

Provision to average

loans

.42%

.44%

Growing high

quality, diverse

revenue streams

Net interest margin

3.24%

3.37%

>3.50%

Improve funding mix

Focus on risk-adjusted returns

Grow client relationships

Capitalize on Key’s total client solutions and

cross-selling capabilities

Noninterest income

to total revenue

42%

42%

>40%

Creating positive

operating

leverage

Cash

efficiency

ratio

(c)

66%

69%

60-65%

Improve efficiency and effectiveness

Better utilize technology

Change cost base to more variable from

fixed

Executing our

strategies

Return on average

assets

.99%

.96%

1.00-1.25%

Execute our client insight-driven

relationship model

Focus on operating leverage

Improved funding mix with lower cost core

deposits

(a)

Continuing operations, unless otherwise noted

(b)

Represents period-end consolidated total loans and loans held for sale (excluding education loans

in the securitization trusts) divided by period-end consolidated total deposits (excluding

deposits in foreign office) (c)

Excludes intangible asset amortization; Non-GAAP measure: see Appendix for reconciliation

|

15

$19.0

$17.5

$15.9

3.22%

3.01%

2.54%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

$0

$5

$10

$15

$20

$25

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

Average Total Investment Securities

Highlights

Average AFS securities

$ in billions

High Quality Investment Portfolio

Portfolio composed of Agency or GSE backed:

GNMA, Fannie & Freddie

–

No private label MBS or financial paper

Average portfolio life at 3/31/13: 2.8 years

Unrealized net gain of $330 million on available-

for-sale securities portfolio at 3/31/13

Mortgage cash flows of $1.5 billion in 1Q13

and $1.6 billion in 4Q12

Deployment of increased liquidity expected to

elevate portfolio size in 2Q13

Yields on reinvestments are approximately

150 bps lower than maturities

Securities to Total Assets

(b)

(a) Yield is calculated on the basis of amortized cost

(b) Includes end of period held-to-maturity and

available-for-sale securities Average yield

(a)

Average HTM securities |

Credit Quality by Portfolio

16

Credit Quality

$ in millions

N/M = Not Meaningful

(a) 3-31-13

ending

loan

balances

include

$93

million

of

commercial

credit

card

balances.

(a) 3-31-13 and 12-31-12 average loan balances include $91

million and 90 million, respectively, of assets from commercial credit cards.

(b)

Net loan charge-off amounts are annualized in calculation. NCO ratios for

discontinued operations and consolidated Key exclude education loans in the

securitization trusts since valued at fair-market value (c)

3-31-13 and 12-31-12 NPL amounts exclude $22 million and $23

million respectively of purchased credit impaired loans acquired in July

2012. (d) 3-31-13 allowance by portfolio is estimated.

Allowance/period loans ratios for discontinued operations and consolidated Key exclude

education loans in the securitization trusts since valued

at fair-market value

(e) 3-31-13 ending loan balances include purchased loans of $204

million of which $22 million were purchased credit impaired. Period-end

loans

Average

loans

3/31/13

1Q13

1Q13

4Q12

1Q13

4Q12

3/31/13

12/31/12

3/31/13

3/31/13

3/31/13

Allowance /

period-end

loans

(d)

Allowance /

NPLs

Net loan

charge-offs

Net

loan

charge-offs

(b)

/

average loans

Nonperforming

loans

(c)

Ending

allowance

(d)

Commercial, financial and agricultural

(a)

$23,412

$23,317

$2

($8)

.03

%

(.14)

%

$142

$99

$338

1.44

%

238.03

%

Commercial real estate:

Commercial mortgage

7,544

7,616

8

28

.43

1.47

114

120

193

2.56

169.30

Construction

1,057

1,034

(7)

3

(2.75)

1.12

27

56

35

3.31

129.63

Commercial lease financing

4,796

4,843

2

3

.17

.25

12

16

62

1.29

516.67

Real estate —

residential mortgage

2,176

2,173

6

7

1.12

1.29

96

103

33

1.52

34.38

Home equity:

Key Community Bank

9,809

9,787

16

(18)

.66

(.73)

199

210

106

1.08

53.27

Other

401

413

4

11

3.93

10.65

18

21

19

4.74

105.56

Consumer other —

Key Community Bank

1,353

1,343

7

8

2.11

2.38

3

2

33

2.44

N/M

Credit cards

693

704

8

9

4.61

5.01

13

11

32

4.62

246.15

Consumer other:

Marine

1,254

1,311

3

14

.93

3.97

25

34

38

3.03

152.00

Other

79

85

0

1

.00

4.37

1

2

4

5.06

400.00

Continuing total

(e)

$52,574

$52,626

$49

$58

.38

%

.44

%

$650

$674

$893

1.70

%

137.38

%

Discontinued operations

5,086

5,135

12

15

1.75

2.12

15

20

49

.96

326.67

Consolidated total

$57,660

$57,761

$61

$73

.45

%

.53

%

$665

$694

$942

1.63

%

141.65

% |

17

(a)

Average LTVs are at origination. Current average LTVs for Community Bank total

home equity loans and lines is approximately 78%, which compares to 77% at

the end of the fourth quarter 2012. Community Bank –

Home Equity

Exit Portfolio –

Home Equity

$ in millions, except average loan size

$ in millions, except average loan size

(a)

(a)

Home Equity Loans –

3/31/13

Vintage (% of Loans)

Loan Balances

Average Loan

Size ($)

Average

FICO

Average

LTV

% of Loans

LTV>90%

2012 and

later

2011

2010

2009

2008 and

prior

Home equity loans and lines

First lien

18

$

22,800

$

745

34

%

.3

%

-

%

-

%

-

%

2

%

98

%

Second lien

383

23,549

729

82

32.2

-

-

-

-

100

Total home equity loans and lines

401

$

23,514

$

730

80

30.8

-

-

-

-

100

Nonaccrual loans

First lien

1

$

19,503

$

714

33

%

-

%

-

%

-

%

-

%

-

%

100

%

Second lien

17

25,239

709

82

31.2

-

-

-

-

100

Total home equity nonaccrual loans

18

$

24,999

$

709

80

30.2

-

-

-

-

100

Exit Portfolio - Home Equity

First quarter net charge-offs

4

$

-

-

-

-

%

100

%

Net loan charge-offs to average loans

3.93

%

Vintage (% of Loans)

Loan Balances

Average Loan

Size ($)

Average

FICO

Average

LTV

% of Loans

LTV>90%

2012 and

later

2011

2010

2009

2008 and

prior

Home equity loans and lines

First lien

5,429

$

64,520

$

759

66

%

.6

%

28

%

8

%

5

%

5

%

54

%

Second lien

4,380

47,314

757

76

3.0

18

7

5

5

65

Total home equity loans and lines

9,809

$

55,507

$

758

70

1.8

24

7

5

5

59

Nonaccrual loans

First lien

100

$

58,275

$

711

74

%

.8

%

1

%

4

%

3

%

5

%

87

%

Second lien

99

47,369

714

78

2.8

1

1

1

3

94

Total home equity nonaccrual loans

199

$

52,292

$

712

76

1.6

1

2

2

4

91

Community Bank - Home Equity

First quarter net charge-offs

16

$

-

%

1

%

2

%

2

%

95

%

Net loan charge-offs to average loans

.66

% |

18

Exit Loan Portfolio Trend (Excluding Discontinued Operations)

Exit Loan Portfolio

$ in millions

(a)

Includes (1) the business aviation, commercial vehicle, office products,

construction and industrial leases; (2) Canadian lease financing portfolios;

and (3) all remaining balances related to lease in, lease out; sale in, lease out;

service contract leases; and qualified technological equipment leases (b)

Includes loans in Key’s consolidated education loan securitization

trusts (c)

Credit amounts indicate recoveries exceeded charge-offs

$ in millions

Exit Loan Portfolio

$2,758

$3,899

$4,736

$0

$3,000

$6,000

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

Change

3-31-13 vs.

3-31-13

12-31-12

12-31-12

1Q13

(c)

4Q12

3-31-13

12-31-12

Residential

properties

–

homebuilder

$29

$29

-

-

$1

$10

$10

Marine and RV floor plan

29

33

$(4)

$(3)

-

6

10

Commercial lease financing

(a)

966

997

(31)

(5)

-

6

6

Total commercial loans

1,024

1,059

(35)

(8)

1

22

26

Home

equity

–

Other

401

423

(22)

4

11

18

21

Marine

1,254

1,358

(104)

3

14

26

34

RV and other consumer

79

93

(14)

-

1

-

2

Total consumer loans

1,734

1,874

(140)

7

26

44

57

Total exit loans in loan portfolio

$2,758

$2,933

$(175)

$(1)

$27

$66

$83

Discontinued

operations

-

education

lending business (not included in exit loans above)

(b)

$5,086

$5,201

$(115)

$12

$15

$15

$20

Balance on

Nonperforming

Status

Balance

Outstanding

Charge-offs

Net Loan |

19

Credit Quality Trends

Quarterly Change in Criticized Outstandings

(a)

Delinquencies to Period-end Total Loans

(a)

Loan and Lease Outstandings

30 –

89 days delinquent

90+ days delinquent |

GAAP

to Non-GAAP Reconciliation 20

$ in millions

(a)

Three months ended March 31, 2013 and December 31, 2012 exclude $114 million and $123 million,

respectively, of period end purchased credit card receivable intangible assets. Three months

ended March 31, 2013 and December 31, 2012 exclude $118 million and $126 million, respectively, of average ending purchased credit card receivable intangible assets.

(b)

Includes net unrealized gains or losses on securities available for sale (except for net unrealized

losses on marketable equity securities), net gains or losses on cash flow hedges, and amounts

resulting from the application of the applicable accounting guidance for defined benefit and other

postretirement plans. (c)

Other assets deducted from Tier 1 capital and net risk-weighted assets consist of disallowed

intangible assets (excluding goodwill) and deductible portions of nonfinancial equity

investments. There were no disallowed deferred tax assets at March 31, 2013, December 31, 2012, and

March 31, 2012. (d)

3-31-13 amount is estimated.

Three months ended

3-31-2013

12-31-2012

3-31-2012

Tangible common equity to tangible assets at period end

Key shareholders’

equity (GAAP)

10,340

$

10,271

$

10,099

$

Less: Intangible assets

(a)

1,024

1,027

932

Preferred Stock, Series A

291

291

291

Tangible common equity (non-GAAP)

9,025

$

8,953

$

8,876

$

Total assets (GAAP)

89,198

$

89,236

$

87,431

$

Less: Intangible assets

(a)

1,024

1,027

932

Tangible assets (non-GAAP)

88,174

$

88,209

$

86,499

$

Tangible common equity to tangible assets ratio (non-GAAP)

10.24

%

10.15

%

10.26

%

Tier 1 common equity at period end

Key shareholders' equity (GAAP)

10,340

$

10,271

$

10,099

$

Qualifying capital securities

339

339

1,046

Less: Goodwill

979

979

917

Accumulated other comprehensive income (loss)

(b)

(204)

(172)

(70)

Other assets

(c)

108

114

69

Total Tier 1 capital (regulatory)

9,796

9,689

10,229

Less: Qualifying capital securities

339

339

1,046

Preferred Stock, Series A

291

291

291

Total Tier 1 common equity (non-GAAP)

9,166

$

9,059

$

8,892

$

Net risk-weighted assets (regulatory)

(c), (d)

80,446

$

79,734

$

76,956

$

Tier 1 common equity ratio (non-GAAP)

(d)

11.39

%

11.36

%

11.55

%

Pre-provision net revenue

Net interest income (GAAP)

583

$

601

$

553

$

Plus: Taxable-equivalent adjustment

6

6

6

Noninterest income (GAAP)

425

439

442

Less: Noninterest expense

681

734

679

Pre-provision net revenue from continuing operations (non-GAAP)

333

$

312

$

322

$ |

GAAP

to Non-GAAP Reconciliation (continued) $ in millions

21

(a)

Three months ended March 31, 2013 and December 31, 2012 exclude $114 million and $123 million,

respectively, of period end purchased credit card receivable intangible assets. Three months

ended March 31, 2013 and December 31, 2012 exclude $118 million and $126 million, respectively, of average ending purchased credit card receivable intangible assets.

Three months ended

3-31-2013

12-31-2012

3-31-2012

Average tangible common equity

Average

Key

shareholders’

equity

(GAAP)

10,279

$

10,261

$

9,992

$

Less: Intangible assets (average)

(a)

1,027

1,030

932

Preferred Stock, Series A (average)

291

291

291

Tangible common equity (non-GAAP)

8,961

$

8,940

$

8,769

$

Return on average tangible common equity from continuing operations

Net

income

(loss)

from

continuing

operations

attributable

to

Key

common

shareholders

(GAAP)

196

$

190

$

195

$

Average tangible common equity (non-GAAP)

8,961

8,940

8,769

Return on average tangible common equity from continuing operations

(non-GAAP) 8.87

%

8.45

%

8.94

%

Return on average tangible common equity consolidated

Net income (loss) attributable to Key common shareholders (GAAP)

199

$

197

$

194

$

Average tangible common equity (non-GAAP)

8,961

8,940

8,769

Return on average tangible common equity consolidated (non-GAAP)

9.01

%

8.77

%

8.90

%

Cash efficiency ratio

Noninterest expense (GAAP)

681

$

734

$

679

$

Less: Intangible asset amortization on credit cards

8

8

-

Other intangible asset amortization

4

4

1

Adjusted noninterest expense (non-GAAP)

669

$

722

$

678

$

Net interest income (GAAP)

583

$

601

$

553

$

Plus: Taxable-equivalent adjustment

6

6

6

Noninterest income (GAAP)

425

439

442

Total taxable-equivalent revenue (non-GAAP)

1,014

$

1,046

$

1,001

$

Cash efficiency ratio (non-GAAP)

65.98

%

69.02

%

67.73

% |

(a) Tier 1

common equity is a non-generally accepted accounting principle (GAAP) financial measure that is used by investors, analysis and bank

regulatory agencies to assess the capital position of financial services companies. Management

reviews Tier 1 common equity along with other measures of capital as part of its financial

analyses. (b) Includes AFS mark-to-market, cash flow hedges on items recognized

at fair value on the balance sheet, and defined benefit pension liability. (c) Deferred

tax asset subject to future taxable income for realization, primarily tax credit carryforwards, and the deductible portion of mortgage

servicing assets.

(d) The amount of regulatory capital and risk-weighted assets estimated under Basel III (as fully

phased-in on January 1, 2019) is based upon the federal banking agencies' notices of

proposed rulemaking, which implement Basel III and the Standardized Approach.

Tier 1 Common Equity under Basel III (estimated)

KeyCorp & Subsidiaries

22

TIER

1

COMMON

EQUITY

UNDER

BASEL

III

(ESTIMATES)

(a)

Quarter ended

Mar 31,

$ in billions

2013

Tier 1 Common Equity under current regulatory rules

$9.2

Adjustments from current regulatory rules to Basel III:

(0.2)

(0.1)

$8.9

Total risk-weighted assets under current regulatory rules

$80.4

Adjustments from current regulatory rules to Basel III:

Loan Commitments < 1 Year

0.8

Residential Mortgage & Home Equity Loans

3.1

Other

1.7

Total risk-weighted assets under Basel III

$86.1

Tier 1 common equity to total risk-weighted assets

anticipated under Basel III

10.3%

Cumulative

Other

Comprehensive

Income

(b)

Tier

1

common

equity

anticipated

under

Basel

III

(d)

Deferred

Tax

Assets

and

Other

(c) |