Attached files

| file | filename |

|---|---|

| 8-K - 8-K - NATIONAL FUEL GAS CO | d520550d8k.htm |

National Fuel Gas Company

Investor Presentation

April 2013

Exhibit 99 |

April 2013

National Fuel Gas Company

2

Safe Harbor For Forward Looking Statements

This presentation may contain “forward-looking statements” as defined by the

Private Securities Litigation Reform Act of 1995, including statements regarding future prospects, plans, performance

and capital structure, anticipated capital expenditures and completion of construction projects,

as well as statements that are identified by the use of the words “anticipates,” “estimates,”

“expects,” “forecasts,” “intends,” “plans,”

“predicts,” “projects,” “believes,” “seeks,” “will,” “may,” and similar expressions. Forward-looking statements involve risks and uncertainties, which could

cause actual results or outcomes to differ materially from those expressed in the

forward-looking statements. The Company’s expectations, beliefs and projections contained herein are expressed

in good faith and are believed to have a reasonable basis, but there can be no assurance that

such expectations, beliefs or projections will result or be achieved or accomplished.

In addition to other factors, the following are important factors that could cause actual

results to differ materially from results referred to in the forward-looking statements: factors affecting the

Company’s ability to successfully identify, drill for and produce economically viable

natural gas and oil reserves, including among others geology, lease availability, title disputes, weather conditions,

shortages, delays or unavailability of equipment and services required in drilling operations,

insufficient gathering, processing and transportation capacity, the need to obtain governmental

approvals and permits, and compliance with environmental laws and regulations; changes in laws,

regulations or judicial interpretations to which the Company is subject, including those involving

derivatives, taxes, safety, employment, climate change, other environmental matters, real

property, and exploration and production activities such as hydraulic fracturing; changes in the price of

natural gas or oil; impairments under the SEC’s full cost ceiling test for natural gas and

oil reserves; uncertainty of oil and gas reserve estimates; significant differences between the Company’s

projected and actual production levels for natural gas or oil; changes in demographic patterns

and weather conditions; changes in the availability, price or accounting treatment of derivative

financial instruments; governmental/regulatory actions, initiatives and proceedings, including

those involving rate cases (which address, among other things, allowed rates of return, rate design and

retained natural gas), environmental/safety requirements, affiliate relationships, industry

structure, and franchise renewal; delays or changes in costs or plans with respect to Company projects or

related projects of other companies, including difficulties or delays in obtaining necessary

governmental approvals, permits or orders or in obtaining the cooperation of interconnecting facility

operators; financial and economic conditions, including the availability of credit, and

occurrences affecting the Company’s ability to obtain financing on acceptable terms for working capital, capital

expenditures and other investments, including any downgrades in the Company’s credit

ratings and changes in interest rates and other capital market conditions; changes in economic conditions,

including global, national or regional recessions, and their effect on the demand for, and

customers’ ability to pay for, the Company’s products and services; the creditworthiness or performance of

the Company’s key suppliers, customers and counterparties; economic disruptions or

uninsured losses resulting from major accidents, fires, severe weather, natural disasters, terrorist activities, acts

of war, cyber attacks or pest infestation; changes in price differential between similar

quantities of natural gas at different geographic locations, and the effect of such changes on the demand for

pipeline transportation capacity to or from such locations; other changes in price differentials

between similar quantities of oil or natural gas having different quality, heating value, geographic

location or delivery date; significant differences between the Company’s projected and

actual capital expenditures and operating expenses; changes in laws, actuarial assumptions, the interest rate

environment and the return on plan/trust assets related to the Company’s pension and other

post-retirement benefits, which can affect future funding obligations and costs and plan liabilities; the

cost and effects of legal and administrative claims against the Company or activist shareholder

campaigns to effect changes at the Company; increasing health care costs and the resulting effect on

health insurance premiums and on the obligation to provide other post-retirement benefits;

or increasing costs of insurance, changes in coverage and the ability to obtain insurance.

Forward-looking statements include estimates of oil and gas quantities. Proved oil and

gas reserves are those quantities of oil and gas which, by analysis of geoscience and engineering data, can be

estimated with reasonable certainty to be economically producible under existing economic

conditions, operating methods and government regulations. Other estimates of oil and gas quantities,

including estimates of probable reserves, possible reserves, and resource potential, are by

their nature more speculative than estimates of proved reserves. Accordingly, estimates other than

proved reserves are subject to substantially greater risk of being actually realized. Investors

are urged to consider closely the disclosure in our Form 10-K available at

You can also obtain this form on the SEC’s website at For a

discussion of the risks set forth above and other factors that could cause actual results to differ materially from results referred to in the forward-looking statements, see “Risk Factors” in the

Company’s Form 10-K for the fiscal year ended September 30, 2012 and Form 10-Q for

the period ended December 31, 2012. The Company disclaims any obligation to update any forward-looking

statements to reflect events or circumstances after the date thereof or to reflect the

occurrence of unanticipated events. |

April 2013

National Fuel Gas Company

3

Our Business Mix Leads to Long-Term Value Creation

Upstream

Crude Oil

Midstream

Downstream

National Fuel Gas

Supply Corporation

Empire Pipeline, Inc.

National Fuel Gas

Midstream Corporation

National Fuel Gas

Distribution

Corporation

National Fuel

Resources, Inc.

The strategic, operational and financial benefits, along with capital

flexibility and consistent growth opportunities generated by this

integrated mix of businesses continues to create significant

long-term value for the Company’s shareholders in nearly all

economic and commodity price scenarios

Upstream

Natural Gas

Seneca Resources

Corporation

(West Division)

Seneca Resources

Corporation

(East Division) |

April 2013

National Fuel Gas Company

4

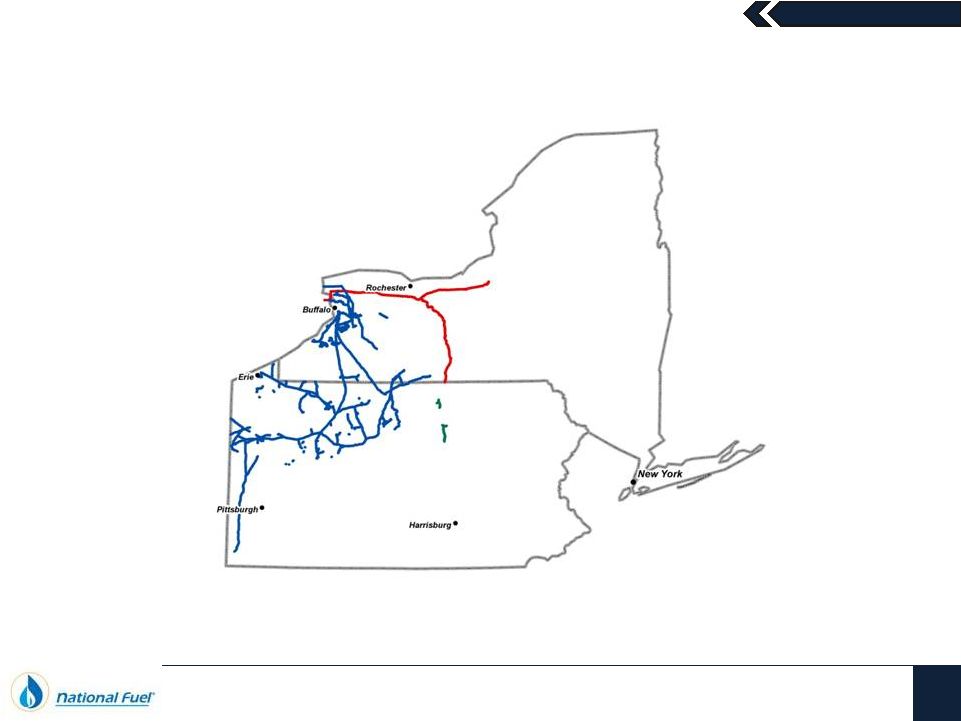

Integrated Businesses with Significant Marcellus Exposure… |

April 2013

National Fuel Gas Company

5

…And Exposure to Growth from the Utica Shale |

April 2013

National Fuel Gas Company

6

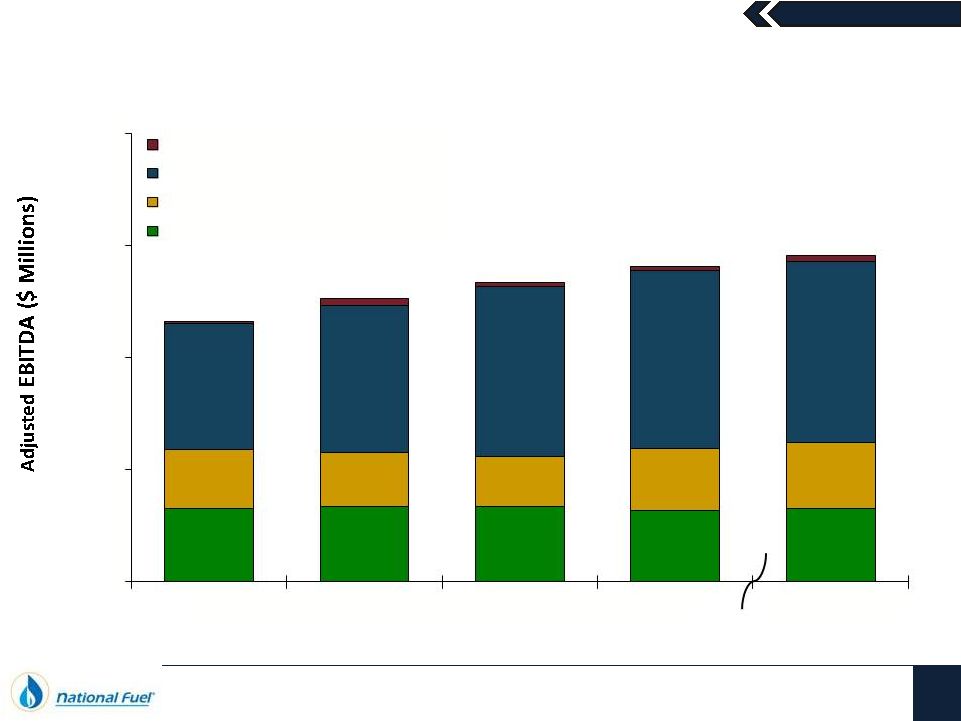

EBITDA Growth Driven by Stability and Continued Success

$0

$250

$500

$750

$1,000

2009

2010

2011

2012

12 Months Ended

12/31/2012

Midstream, Energy Marketing & Other

Exploration & Production Segment

Pipeline & Storage Segment

Utility Segment

$164

28%

$167

26%

$169

25%

$160

23%

$164

23%

$131

$121

19%

$111

17%

$137

19%

$146

20%

$280

48%

$327

52%

$377

57%

$397

56%

$404

56%

$581

$632

$668

$704

$727

23%

Fiscal Year

Note: A reconciliation of Adjusted EBITDA to Net Income as presented on the Consolidated

Statement of Income and Earnings is included at the end of this presentation. |

April 2013

National Fuel Gas Company

7

Capital Spending Flexibility to Maintain Financial Strength

$56

$58

$58

$58

$65-

$70

$65-$70

$53

$38

$129

$144

$70-

$80-

$100

$188

$398

$649

$694

$480-

$560

$550-

$650

$81

$50-

$75

$75-

$125

307

$501

$854

$977

$665-

$795

$770-

$945

$0

$250

$500

$750

$1,000

$1,250

2009

2010

2011

2012

2013 Forecast

2014 Forecast

Fiscal Year

Midstream, Energy Marketing & Other

Exploration & Production Segment

Pipeline & Storage Segment

Utility Segment

$90

$

(1)

Note: A reconciliation to Capital Expenditures as presented on the Consolidated Statement of

Cash Flows is included at the end of this presentation. Does not include the $34.9 MM

Seneca Resources Corporation’s acquisition of Ivanhoe’s U.S.-based assets in California, as this was accounted for as an

investment in subsidiaries on the Statement of Cash Flows, and was not included in the

Exploration & Production segment’s Capital Expenditures (1)

|

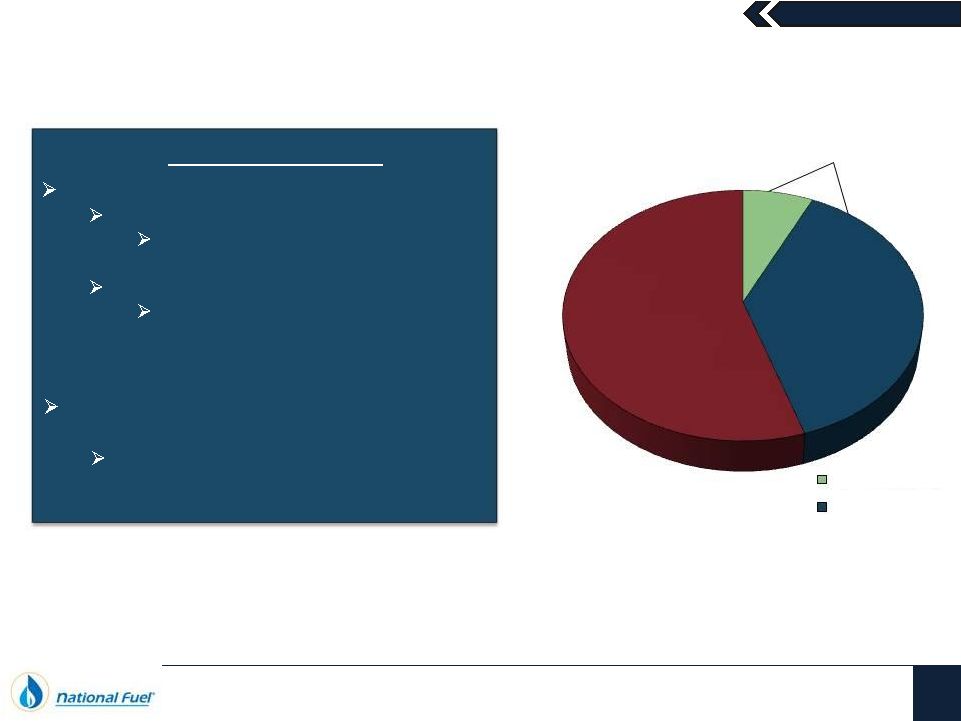

April 2013

Total Debt

(1)

45%

National Fuel Gas Company

8

Strong Balance Sheet and Liquidity Position

Capital Resources

Total Short-Term Capacity: $1,085 Million

Committed Credit Facility: $750 Million

Syndicated facility extends until

January 6, 2017

Uncommitted Lines of Credit: $335 Million

$18.0 million of outstanding short-

term notes payable to banks as of

December 31, 2012

$3.653 Billion

(2)

As of December 31, 2012

(1)

Includes Long-Term Debt of $1.149 billion, the Current Portion of Long-Term Debt of

$0.250 billion, and Notes Payable to Banks and Commercial Paper of $0.238 billion, as

of December 31, 2012. (2)

Includes Notes Payable to Banks and Commercial Paper of $238.0 million and Current Portion of

Long-Term Debt of $250.0 million as of December 31, 2012.

In February 2013, the Company issued $500

million in 10-year notes to repay a $250 maturity

and all

outstanding short-term debt

Short

-Term Debt

Long-Term Debt

Shareholders’

Equity

55 %

$300.0 Million Commercial Paper Program

backed by Committed Credit Facility

$220.0 million of outstanding commercial

paper as of December 31, 2012 |

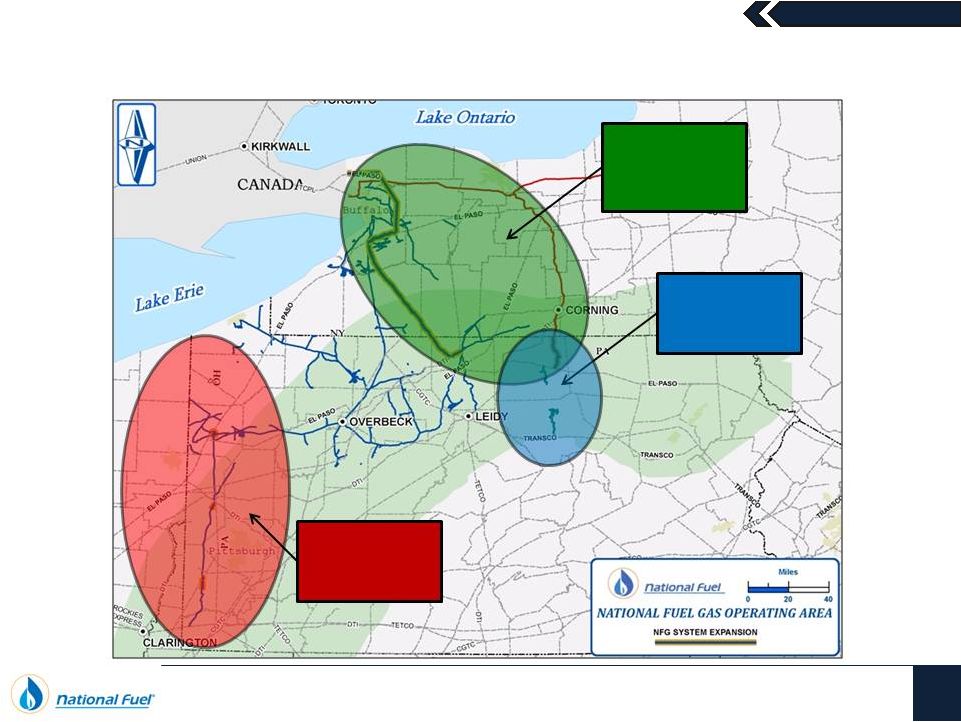

April 2013

Midstream Businesses

9

Pipeline & Storage/NFG Midstream |

April

2013 Midstream Businesses

10

Pipeline Expansions to Transport Appalachian Production

Gathering

Marcellus

Production

Shipping Gas

to Canada &

Northeast

Line N

Corridor

Expansions |

April

2013 Exploration & Production

11 |

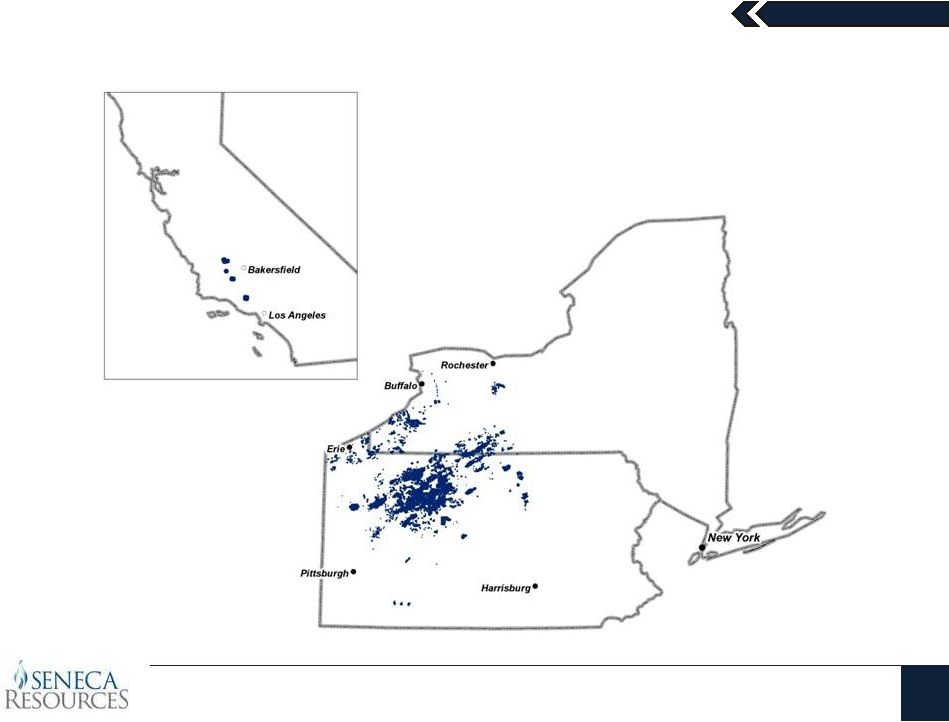

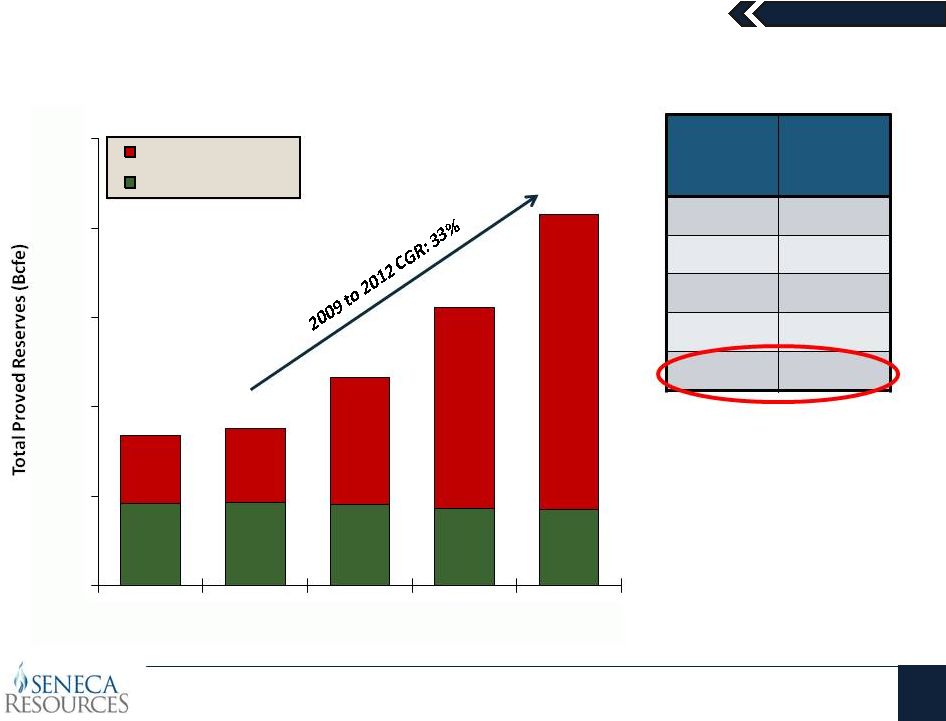

April

2013 Seneca Resources

12

Another Strong Year of Reserve Growth

Seneca has more than doubled

its proved reserves since 2009,

while maintaining a relatively

high percentage of proved

developed reserves (67%),

given its large resource base

(1)

Represents a three-year average U.S. finding and development cost

46.2

46.6

45.2

43.3

42.9

226

249

428

675

988

503

528

700

935

1,246

0

300

600

900

1200

1500

2008

2009

2010

2011

2012

At September 30

Natural Gas (Bcf)

Crude Oil (MMbbl)

Fiscal

Years

3-Year

F&D Cost

(1)

($/Mcfe)

2006-2008

$7.63

2007-2009

$5.35

2008-2010

$2.37

2009-2011

$2.09

2010-2012

$1.87 |

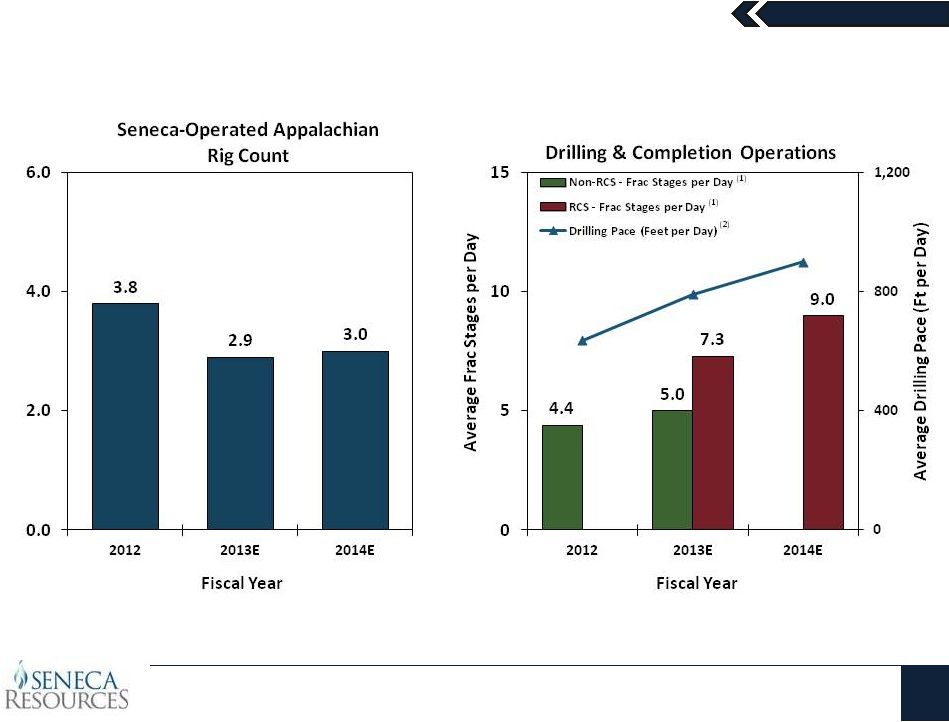

April

2013 Seneca Resources

13

Operational Efficiencies Continue to Drive Production Growth

Ongoing efficiency allows for more activity with a flat rig count

(1)

RCS –

Reduced Cluster Spacing

(2)

Drilling pace represents the average feet drilled per day from the time the well is spud

until it reaches total depth (TD) |

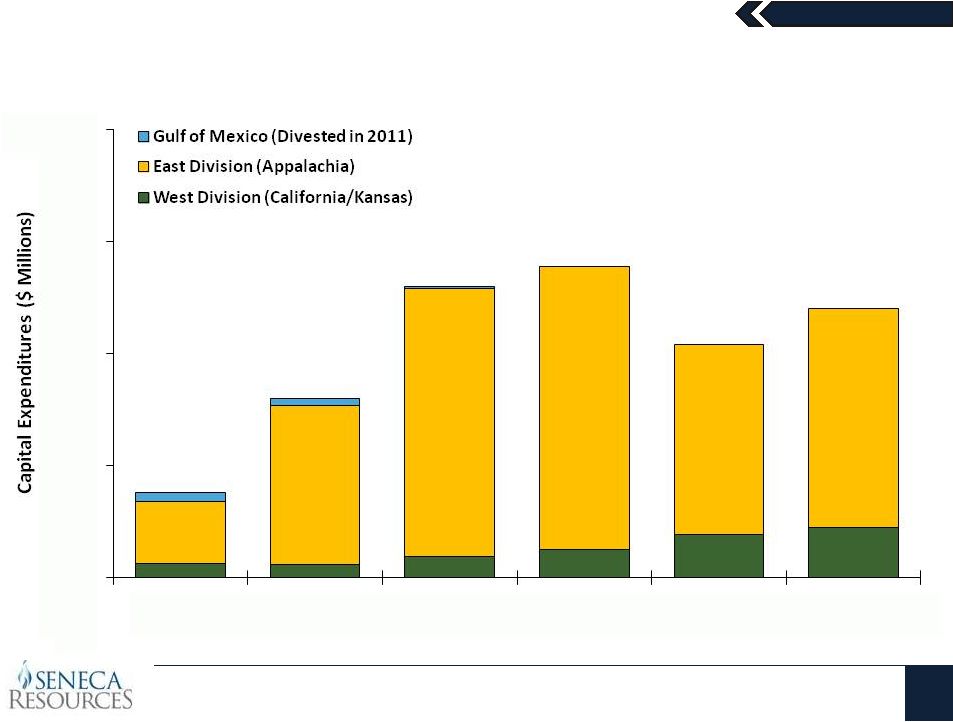

April

2013 Seneca Resources

14

Increased Oil Spending and Tempered Marcellus Spending

(1)

Does not include the $34.9 MM acquisition of Ivanhoe’s U.S.-based assets in

California, as this was accounted for as an investment in subsidiaries on the

Statement of Cash Flows, and was not included in Capital Expenditures

$31

$28

$47

$63

$80-$110

$90-$130

$139

$356

$596

$631

$400-

$450

$460-

$520

$188

(1)

$398

$649

$694

$480-$560

$550-$650

$0

$250

$500

$750

$1,000

2009

2010

2011

2012

2013 Forecast

2014 Forecast

Fiscal Year |

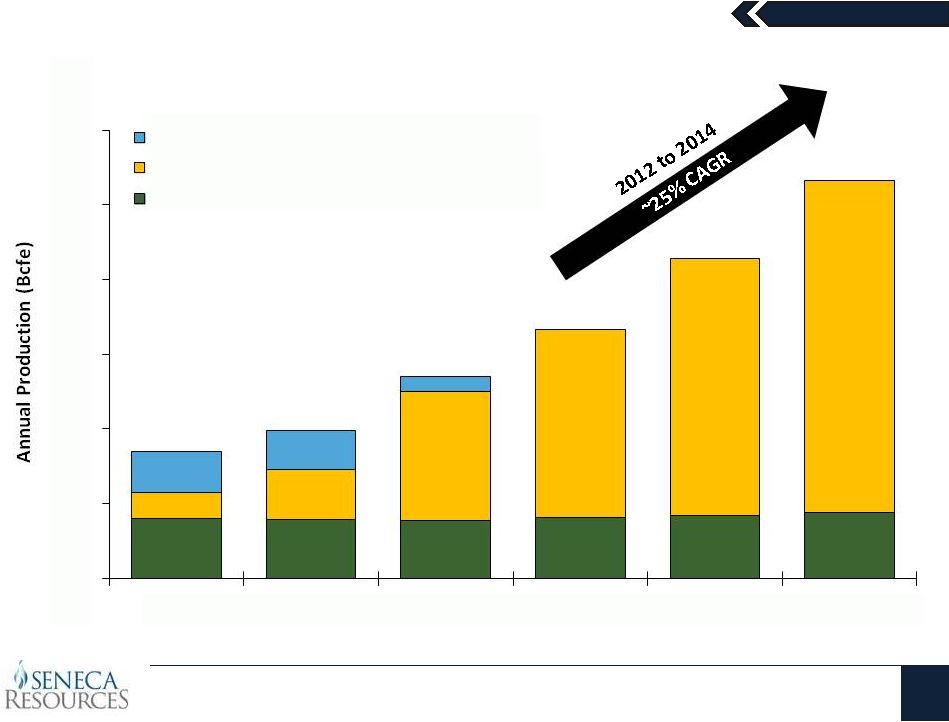

April

2013 Seneca Resources

15

Production Continues to Grow

20.1

19.8

19.2

20.5

20-22

21-23

8.7

16.5

43.2

62.9

82-90

105–115

13.7

13.3

5.2

42.5

49.6

67.6

83.4

102-112

126-138

0

25

50

75

100

125

150

2009

2010

2011

2012

2013 Forecast

2014 Forecast

Fiscal Year

Gulf of Mexico (Divested in 2011)

East Division (Appalachia)

West Division (California/Kansas) |

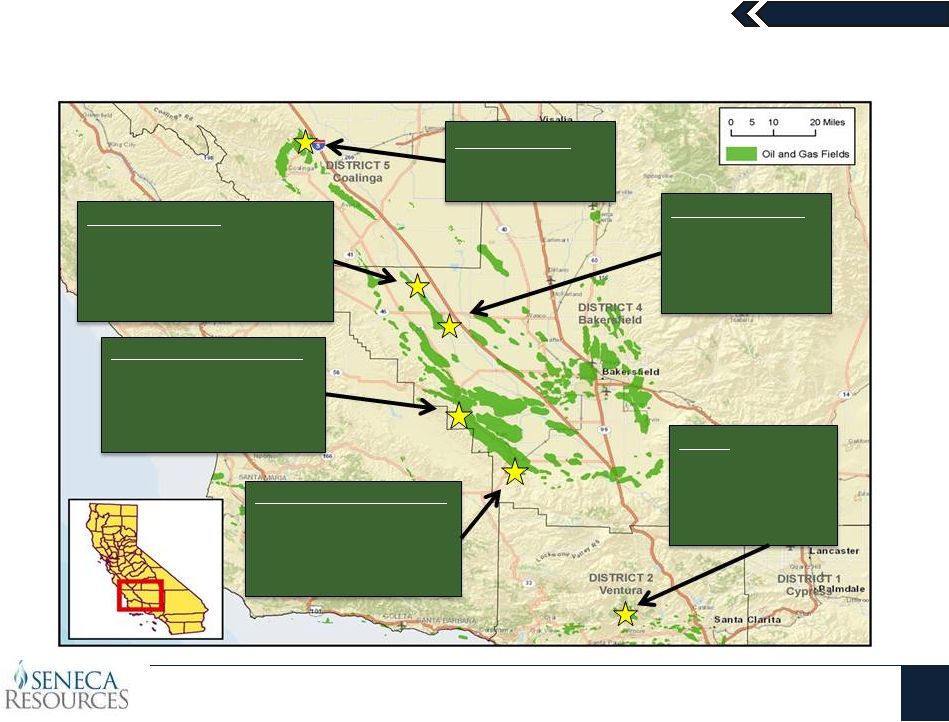

April

2013 Seneca Resources

16

California: Stable Production Fields

South Lost Hills

~1,500 BOEPD

Monterey Shale

Primary

219 Active Wells

Sespe

~1,100 BOEPD

Sespe Formation

Primary

172 Active Wells

North Lost Hills

~1,200 BOEPD

Tulare & Etchegoin Formation

Primary & Steamflood

175 Active Wells

North Midway Sunset

~4,100 BOEPD

Potter & Tulare Formation

Steamflood

728 Active Wells

South Midway Sunset

~1,100 BOEPD

Antelope Formation

Steamflood

110 Active Wells

East Coalinga

Temblor Formation

Primary |

April

2013 Seneca Resources

17

California: Strong Margins Support Significant Free Cash Flow

Average Revenue

(12 Months Ended 12/31/12)

$85.69 per BOE

$9.40

$3.35

$3.06

$2.32

$1.11

$66.45

Non

-

Steam Fuel LOE

Steam Fuel

G&A

Production & Other Taxes

Other Operating Costs

Adjusted EBITDA

Adjusted

EBITDA

per

BOE

(1)

(12 Months Ended December 31, 2012)

(1) Total production from the Exploration & Production segment’s properties in

California was 3,374 Mboe for the 12 months ended December 31, 2012.

Note: A reconciliation of Exploration & Production West Division Adjusted EBITDA to

Exploration & Production Segment Net Income is included at the end of this

presentation. |

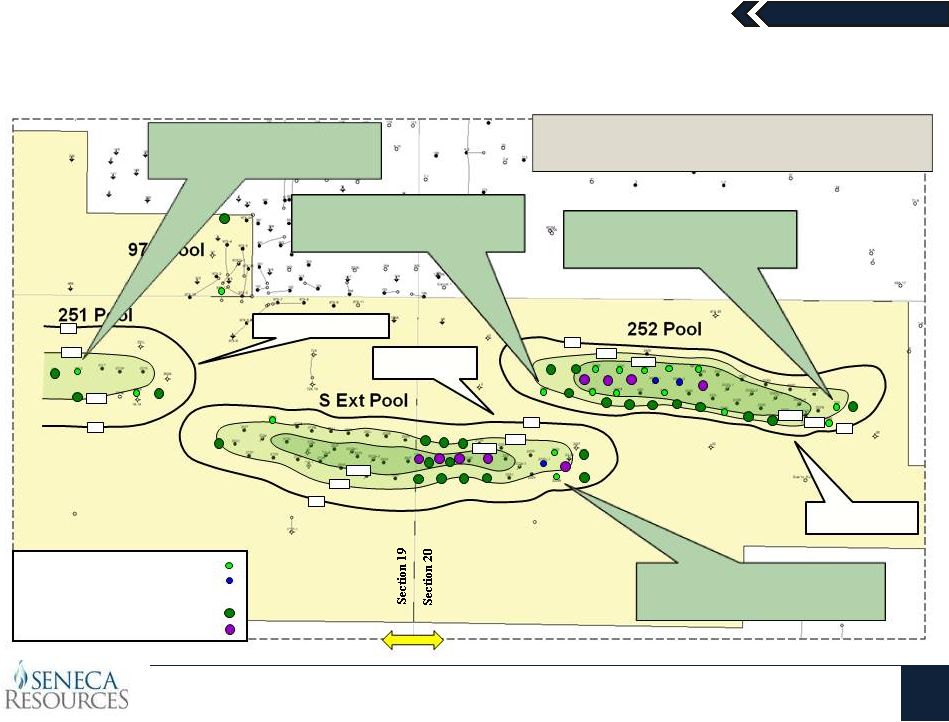

April

2013 California: Midway Sunset South Activity Update

Seneca Resources

18

500’

2012 Drill Program: 21 Wells / 3 Injectors

2013

Drill

Program:

17

-

23

Wells

/

5

-

9

Injectors

0 ft

50 ft

100 ft

100 ft

50 ft

50 ft

Antelope “A-1”

and “A-2”

Sands

Antelope “B”

and “C”

Sands

Antelope “A-1”

Sand

Seneca 232M

Extended 252 Pool to the West

Seneca 252I

Extended 252 Pool to the East

Seneca 222W

Extended S Ext Pool to the East

Seneca 251U

Extended 251 Pool to the West

100 ft

50 ft

100 ft

50 ft

0 ft

50 ft

0 ft

0 ft

0 ft

0 ft

2012 Drill Program

Injectors

2013 Drilling Locations

Producers

Injectors

Producers

? |

19

Seneca Resources

California: Sespe Field –

Drilling Programs and Results

1 Mile

2011 Sespe Wells (5)

2012 Sespe Wells (6)

2013 Sespe Wells (6)

TG 53-29

90 BOEPD

1

Oil

3/13

TG 562-29

190 BOEPD

1

Oil

2/13

FA 502-33

75 BOEPD

1

Oil

1/13

FA 501-33

100 BOEPD

1

Oil 1/13

WS 48-33

80 BOEPD

1

Oil 09/12

Oak Flat 2-31

100 BOEPD

1

Oil 08/12

Oak Flat 1-31

110 BOEPD

1

Oil

08/12

“X”

SANDS ISOCHORE (Thickness)

April 2013 |

April

2013 Seneca Resources

20

California: East Coalinga Overview

Seneca became operator on January 30, 2013

Previous Operator: Chevron

7,764 net acres

~170 wells (60 active)

~250 BOPD

$30 million capital commitment over first

three years

$100 million of potential opportunities over

the next five to seven years

2013 Plans

Drill ~12 evaluation wells across acreage

block

Place ~50% of currently idled wells back on

production

Upgrade surface facilities

Active Well

Idle Well |

April

2013 Seneca Resources

21

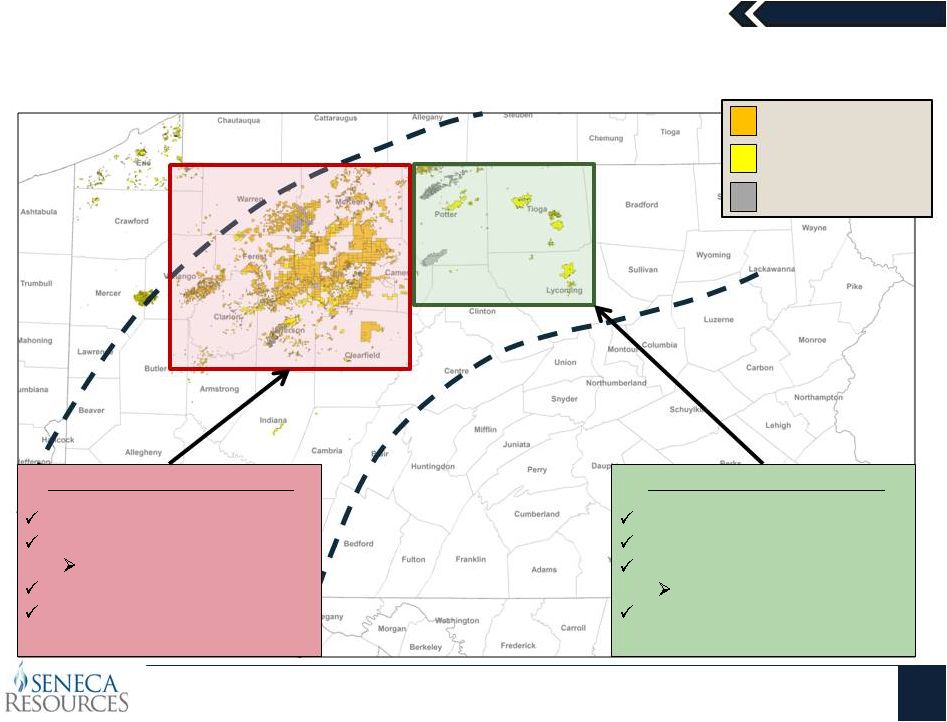

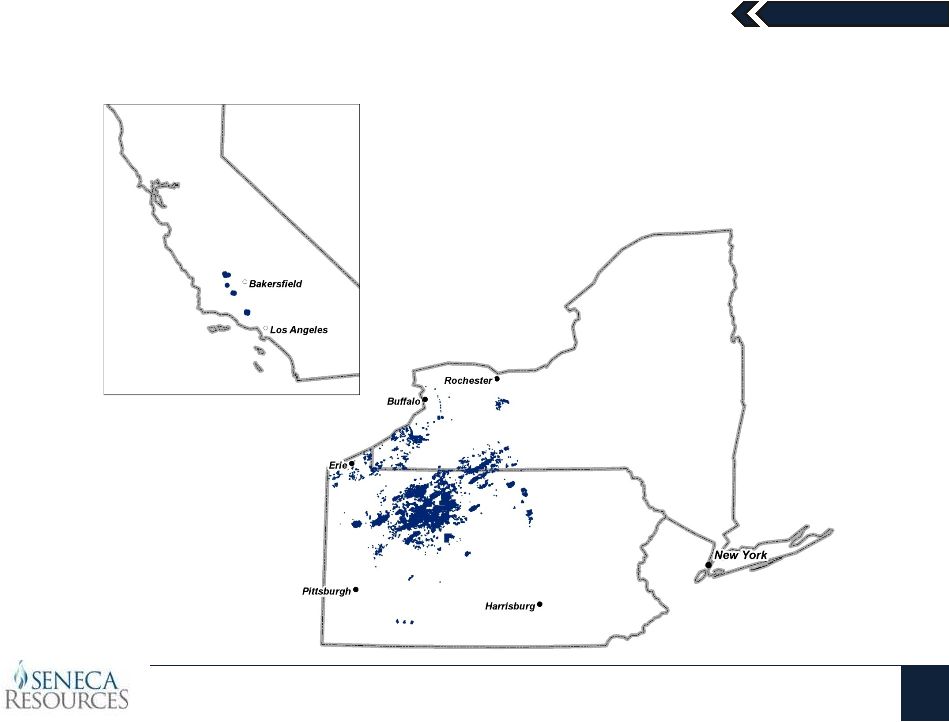

Expansive Pennsylvania Acreage Position

SRC Lease Acreage

SRC Fee Acreage

Eastern Development Area

Net Acreage: 55,000 acres

Mostly leased (16-18% royalty)

No near-term lease expiration

First large expiration: 2018

Ongoing development drilling

in Tioga and Lycoming Counties

Western Development Area

Net acreage:

~720,000 acres

Own most mineral rights

Minimal

royalty obligation

Minimal

lease expiration

Evaluating Marcellus rich-gas

and Utica Shale potential

NFG Storage Acreage |

April

2013 Seneca Resources

22

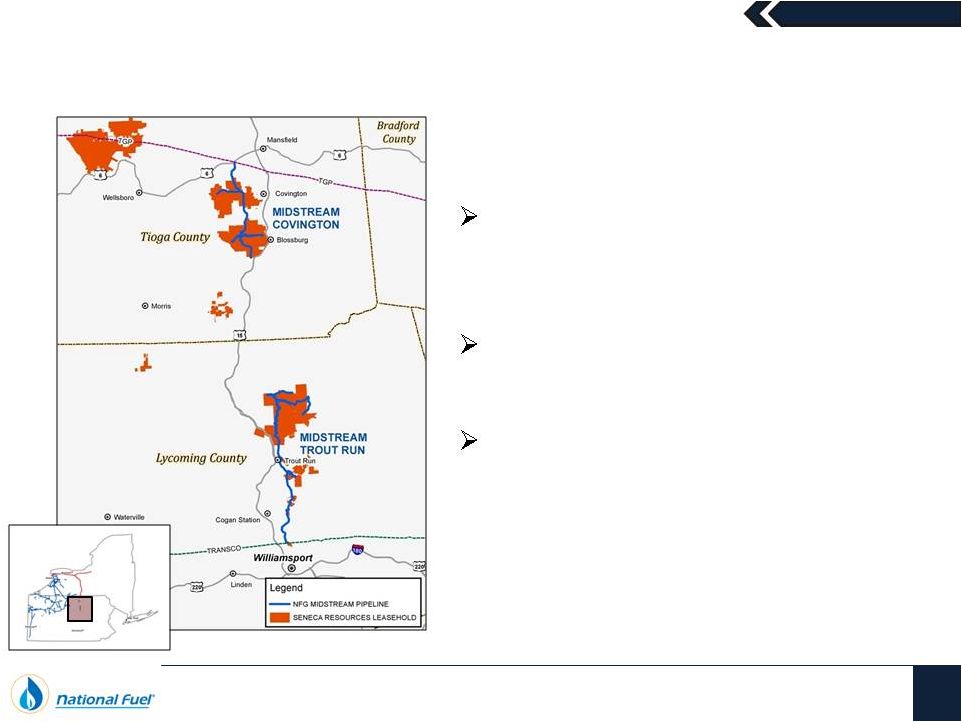

Eastern Development Area (EDA)

DCNR Tract 595

Gross Production: ~85 MMcf per Day

34 Wells Drilled

26 Wells Producing

Covington

–

Fully

Developed

Gross Production: ~65 MMcf per Day

47 Wells Drilled and Producing

DCNR Tract 100

Gross Production: ~165 MMcf per Day

31 Wells Drilled

21 Wells Producing

SRC Lease Acreage

SRC Fee Acreage |

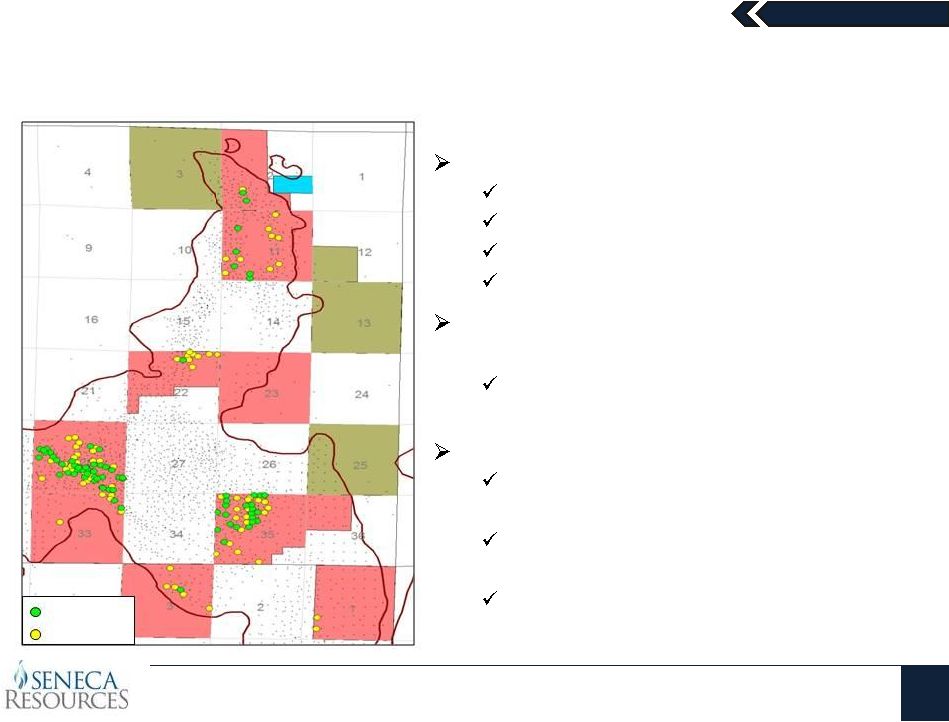

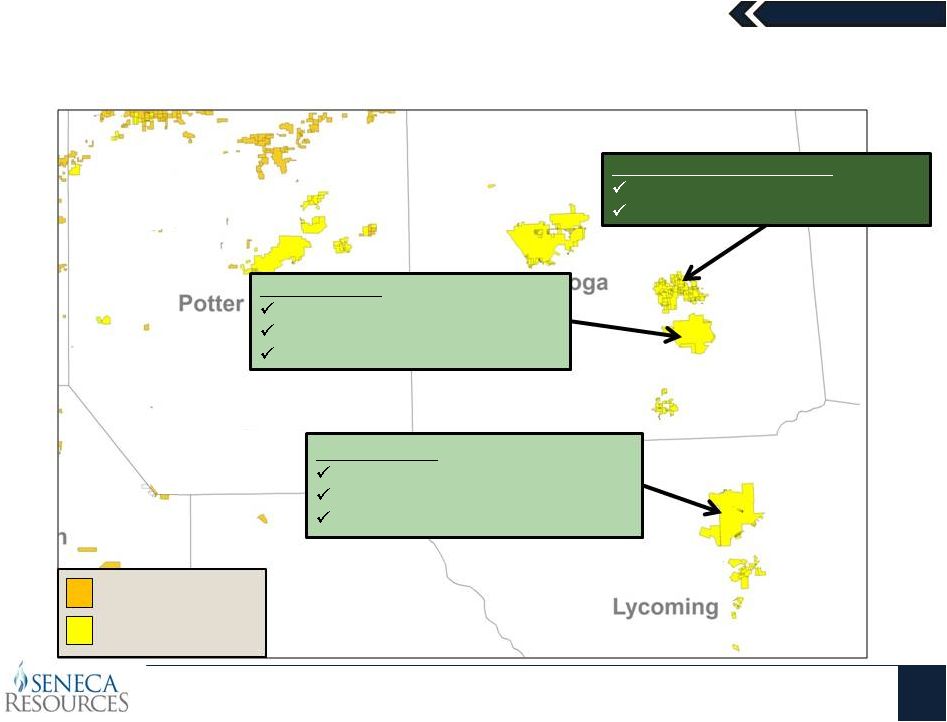

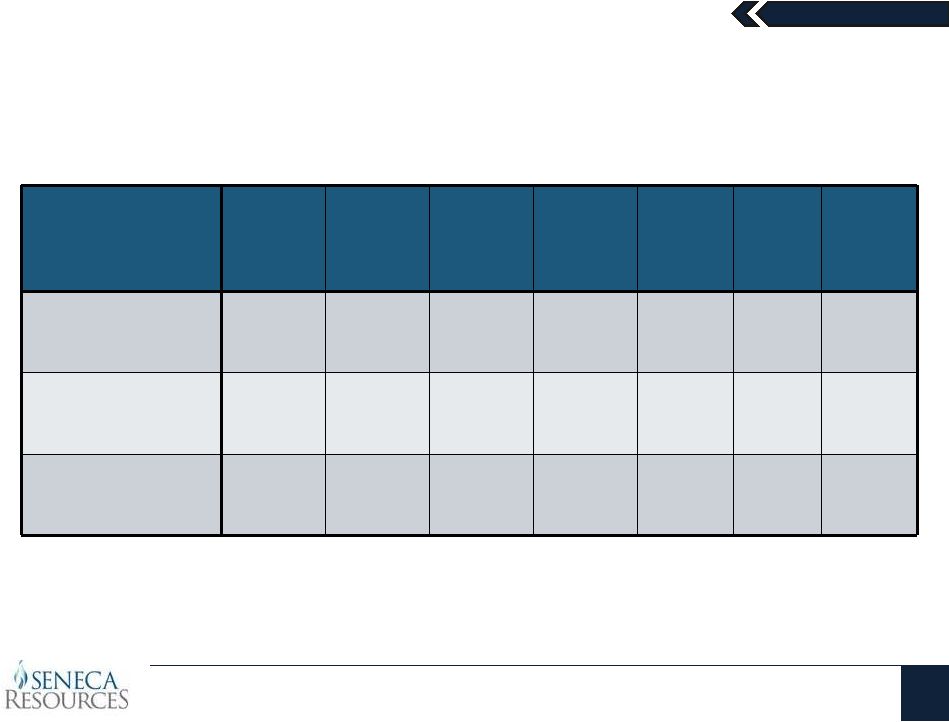

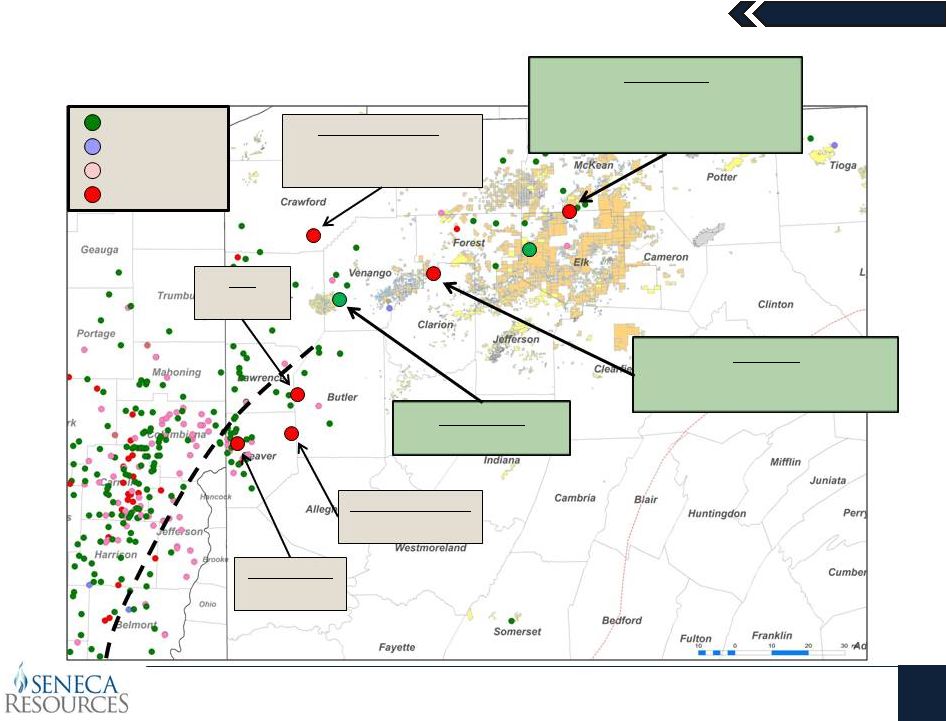

April

2013 Seneca Resources

23

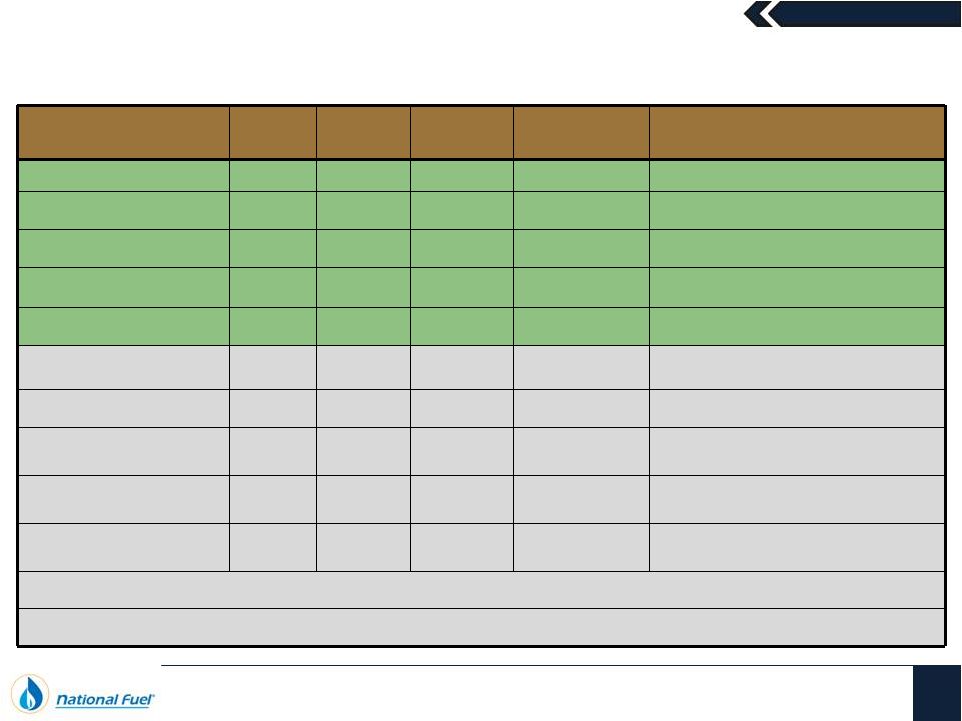

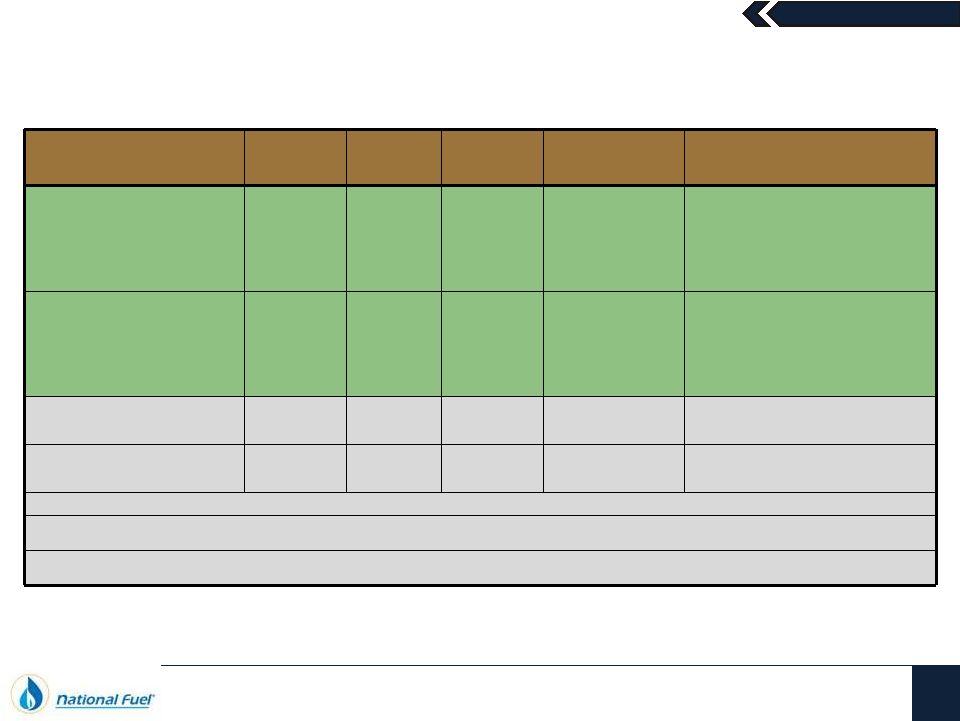

Lycoming and Tioga Counties Are Highly Productive Areas

Development Area

Producing

Well

Count

Average

IP Rate

(MMcf/d)

Average

7-Day

(MMcf/d)

Average

30-Day

(MMcf/d)

Average

EUR

per Well

(Bcf)

Average

Lateral

Length

EUR per

1,000’

of

Lateral

(Bcfe)

Covington

Tioga

County

47

5.2

4.7

4.1

5.3

4,049’

1.30

Tract 595

Tioga

County

19

(1)

6.9

6.0

5.1

7.7

4,455’

1.72

Tract 100

Lycoming

County

14

(2)

15.4

13.3

10.3

11.0

5,256’

2.09

(1)

Seven new wells on Tract 595 began production in February 2013 and are awaiting sufficient

production history to include within the table

(2)

Seven new wells on Tract 100 began production in March 2013 and are awaiting sufficient

production history to include within the table |

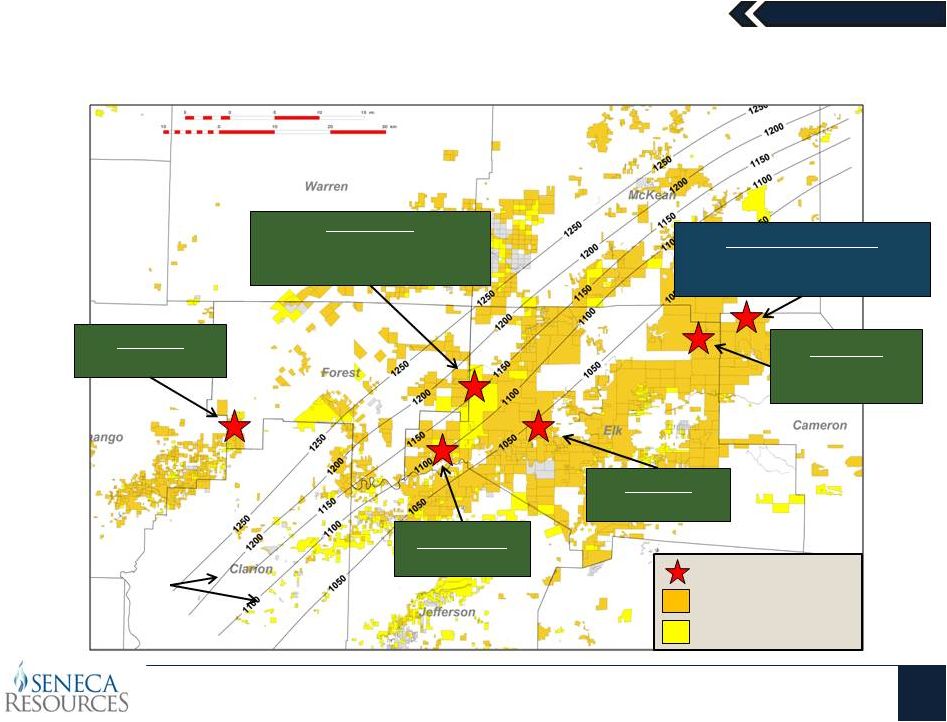

April

2013 Seneca Resources

24

Western Development Area Marcellus Delineation Program

Owl’s

Nest

2 Wells Drilled

3D Seismic Coverage Complete

Church Run

1 Well Drilled

Ridgway

1 Well Drilled

Clermont

Currently Drilling

the 2nd of 2 Wells

Tionesta

1 Well Planned

Rich Valley (1 Well)

Peak 7-Day IP: 7.8 MMcf per Day

Estimated EUR: 7 Bcf

SRC Lease Acreage

SRC Fee Acreage

Horizontal Well

BTU

Contours |

April

2013 Seneca Resources

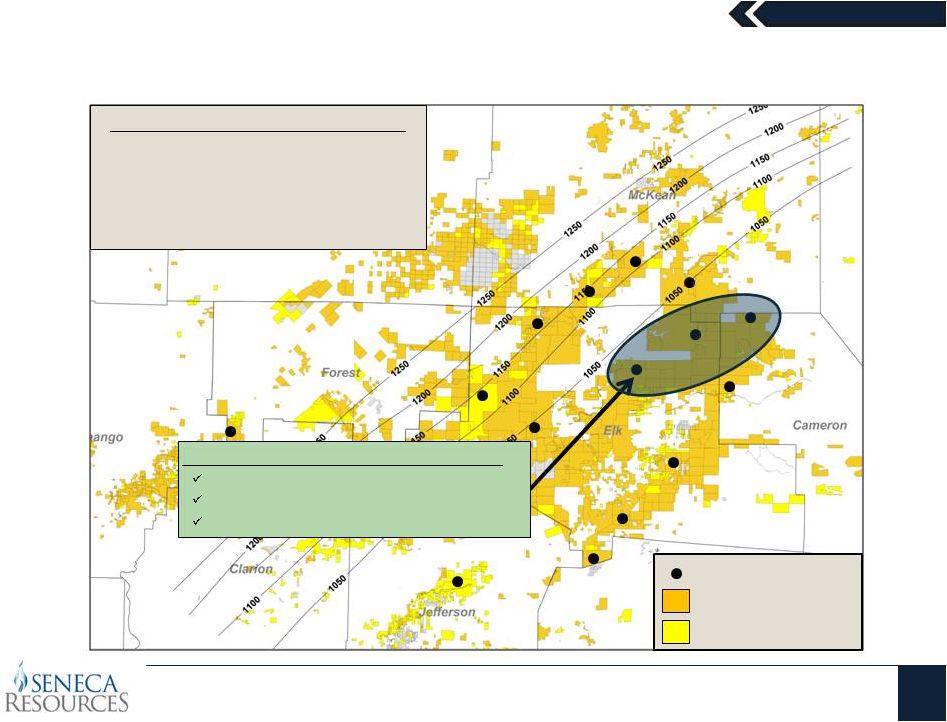

25

Rich Valley/Clermont Marcellus Development Area

Rich

Valley/Clermont

Development

Area

Area of high porosity and GIP

150-200 Horizontal Locations

Anticipated EURs: 5-8 Bcf

WDA Pilot Development Program

Upon completion of initial delineation

drilling, a pilot development program

will begin this summer. Full

development planned for 2014.

SRC Lease Acreage

SRC Fee Acreage

Delineation Well |

April

2013 Seneca Resources

26

Utica Shale –

Activity Summary

Permitted

Drilled/Drilling

Completed

Producing

Mt. Jewett

Tested 3 Frac Stages at 1.6 MMcfd

(Typical Well: 17 Frac Stages)

2

nd

Horizontal: FY 2013

Henderson

Vertical Well: Tested

Tionesta

Horizontal: Completed Fall 2012

Peak 24-Hour Rate: 3.9 MMcfd

Rex

9.2 MMcfd

Chesapeake

6.4 MMcfd

Range Resources

4.4 MMcfd

Range Resources

1.4 MMcfd

“Not Effectively Stimulated” |

April

2013 Seneca Resources

27

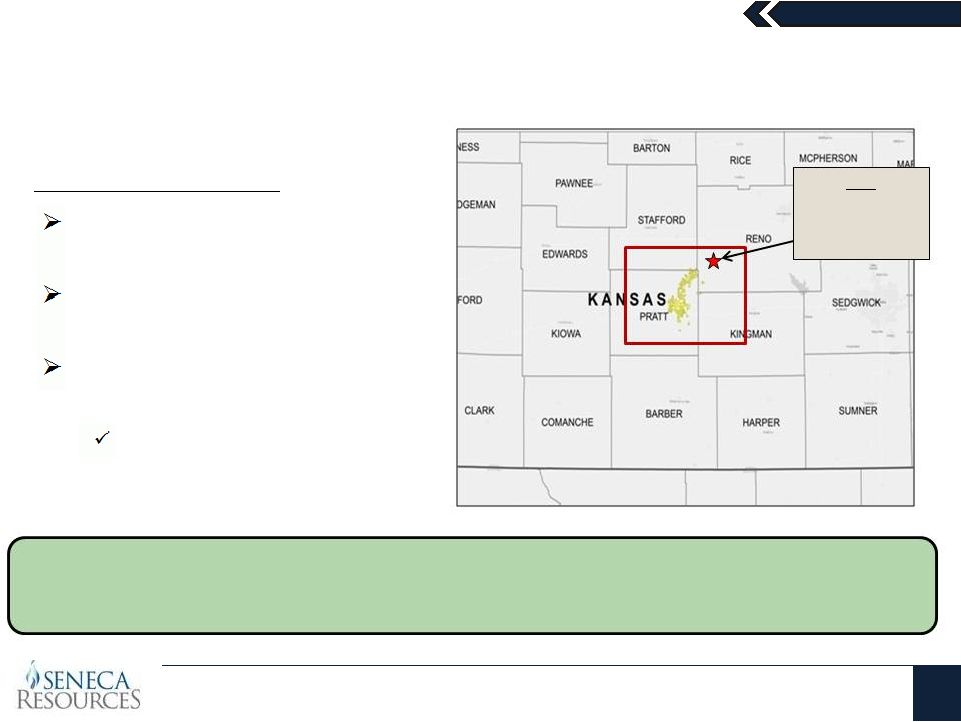

Initial Entry into the Mississippian Lime Play in Kansas

The initial entry into the Mississippian Lime play furthers the Company’s goal of

maintaining a significant contribution from oil-producing properties

Unit

30-day IP:

352 BOED

(92% Oil/NGLs)

100% working interest in 4,600 gross

acres

25% net working interest in 18,500

gross acres

2013: Participate in 3 to 5 gross

horizontal wells

Total Net Acres: 9,300

1

st

Well Spud: FY2013 –

Q3 |

National Fuel Gas

Company 28

Capital Deployment Has Led to Significant Accomplishments

Note: A reconciliation of Adjusted EBITDA to Net Income as presented on the Consolidated

Statement of Income and Earnings is included at the end of this presentation. 136%

Increase in Proved Reserves Since 2009 •

Total oil and gas proved reserves reached 1,246 Bcfe at September 30, 2012, with a

3-year average F&D cost of $1.87/Mcfe

•

Despite the 2011 sale of its offshore Gulf of Mexico properties, Seneca has increased

production from 42.5 Bcfe in 2009 to 83.4 Bcfe in 2012

96% Production Growth Since 2009

31% Increase in Pipeline & Storage Adjusted EBITDA since Fiscal 2011

44.3 Bcfe in 2012 NFG Midstream Gathering Volumes

•

As a result of major Appalachian pipeline expansions, Adjusted EBITDA reached $146

million for the last 12 months and new projects will continue to drive growth beyond

fiscal 2013 •

NFG Midstream gathered more than 44 Bcfe of volumes for Seneca Resources, eliminating

the need to rely upon and provide payment to third party infrastructure operators

April 2013 |

National Fuel Gas

Company Appendix

April 2013

29 |

National Fuel Gas

Company Fiscal Year 2013 Earnings Guidance Drivers

30

2013 Forecast

$2.75 -

$3.00

102 -

112

$2.10 -

$2.25

$0.90 -

$1.10

$58 -

$62 MM

+3%

$255 -

$265 MM

+3%

$5 -

$10 MM

GAAP Earnings per Share

Exploration & Production Drivers

Total Production (Bcfe)

DD&A Expense

LOE Expense

G&A Expense

Pipeline & Storage Drivers

O&M Expense

Revenue

Utility Drivers

O&M Expense

Normal Weather in PA

Energy Marketing Drivers

Operating Income

April 2013 |

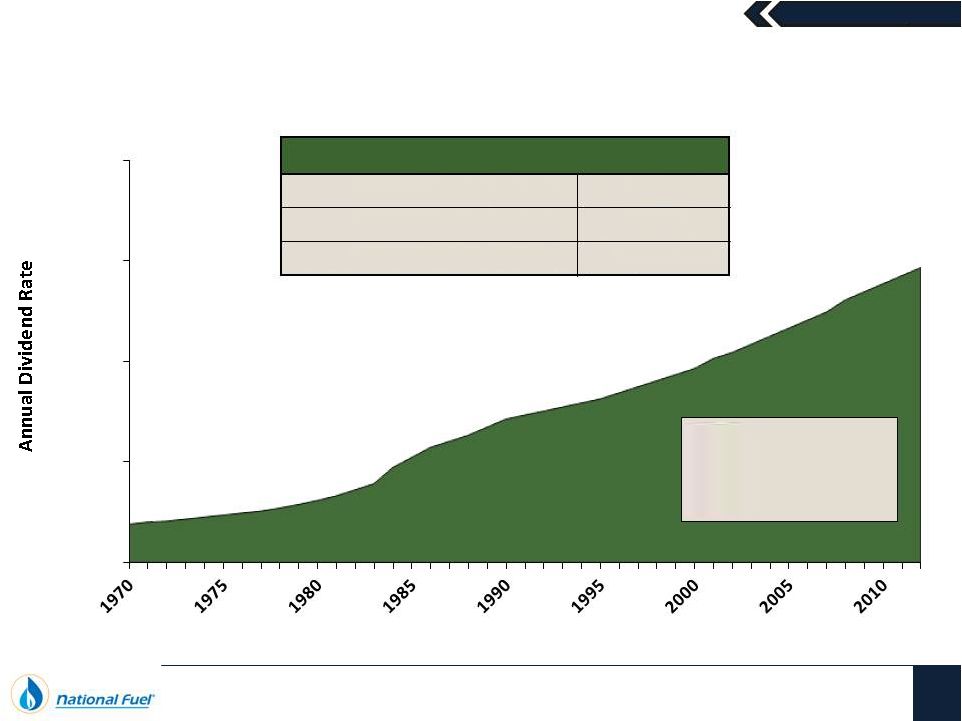

National Fuel Gas

Company 31

Dividend Track Record

(1) As of March 12, 2013

Dividend Consistency

Consecutive Dividend Payments

Consecutive Dividend Increases

Current Annualized Dividend Rate

110 Years

42 Years

$1.46 per Share

Current

Dividend Yield

(1)

2.5%

$2.00

$1.50

$1.00

$0.00

$0.50

April 2013

Annual Rate at Fiscal Year End |

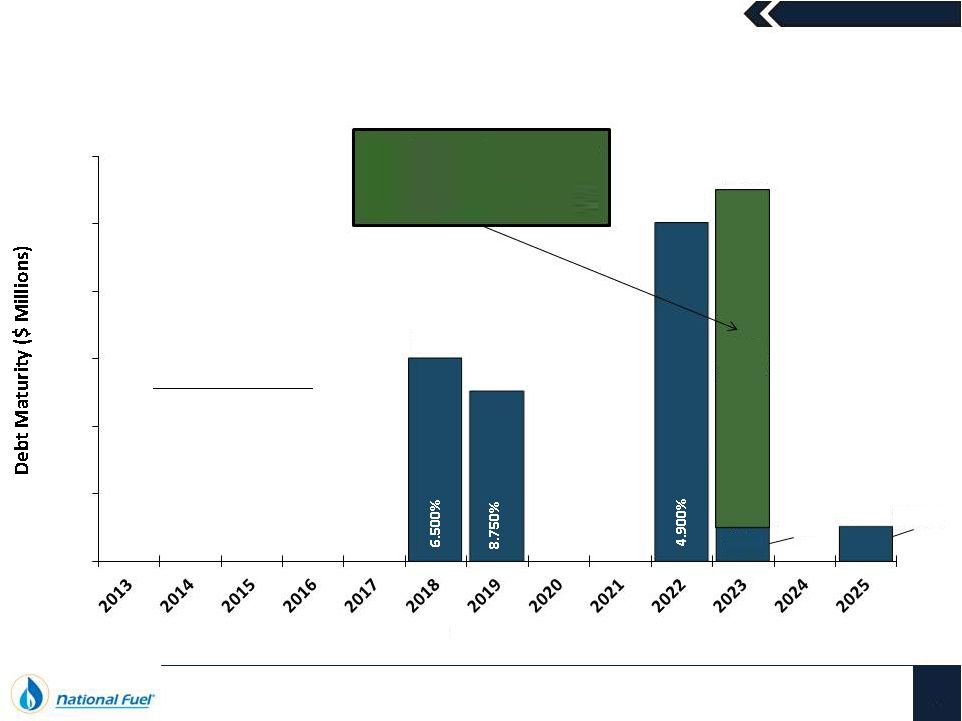

National Fuel Gas

Company No Debt Maturities Until Fiscal 2018

Embedded Cost of

Long-Term Debt

5.58%

In February, the Company

Issued $500 million in

10-year notes at 3.75%

$600

$500

$400

$300

$200

$100

$0

$300

$250

$500

$549

$50

7.395%

7.375%

$49

$500

3.750%

Fiscal Year

April 2013

32 |

Midstream

Businesses 33

Appendix

April 2013 |

Midstream

Businesses 34

A Closer Look at the Expansion Progress

COVINGTON

GATHERING

SYSTEM

(In-Service)

TROUT RUN

GATHERING SYSTEM

(In-Service)

TIOGA

COUNTY

EXTENSION

(In-Service)

LINE “N”

EXPANSION

(In-Service)

NORTHERN ACCESS

EXPANSION

(In-Service)

CENTRAL TIOGA

COUNTY EXTENSION

(2015/2016)

LINE “N”

2012

EXPANSION

(In-Service)

MERCER

EXPANSION

PROJECT

(Nov. 2014)

LINE “N”

2013

EXPANSION

(Nov. 2013)

WEST SIDE

EXPANSION

(2013 to 2015)

TIONESTA

GATHERING

SYSTEM

(Under Construction)

MT. JEWETT

GATHERING SYSTEM

(Under

Construction)

April 2013 |

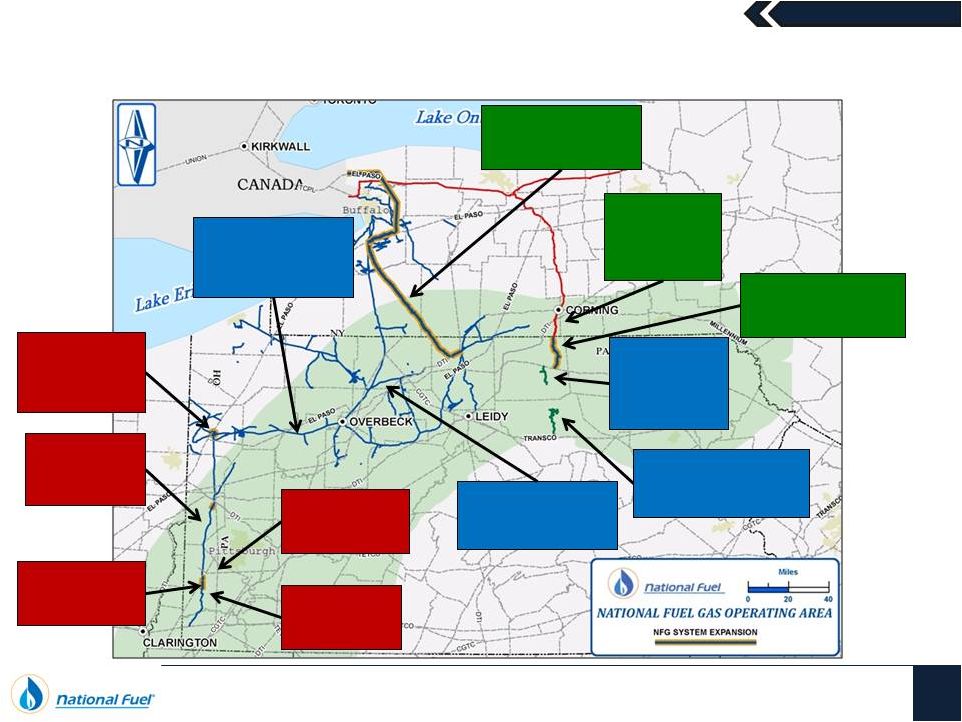

Midstream

Businesses Pursuing Additional Opportunities Near the Line N Corridor

Line N

Focus Area

April 2013

35

Activity in the Marcellus and Utica shales

along the Pennsylvania/Ohio border

continues to remain robust

NFG Supply Corporation’s Line N system is

well-positioned for continued expansion

NFG Midstream Corporation is focused on

building new high-pressure wet and dry gas

gathering systems

Significant expansion opportunities may be

present in the next few years

2013:

Smaller pipeline expansions

2014+:

Larger expansion projects, possibly

including an integrated wet gas solution,

with NFG Midstream focused on the high-

pressure wet gas gathering systems and

NFG Supply transporting dry gas on its

interstate system |

Midstream

Businesses Regulated Interstate Expansion Initiatives (Pipeline & Storage)

Project Name

Capacity

(Dth/D)

Est.

CapEx

In-Service

Market

Status

Lamont Compressor Station

90,000

$14 MM

2010/2011

Fully Subscribed

Completed –

Two Phases

Line “N”

Expansion

160,000

$22 MM

10/2011

Fully Subscribed

Completed

Tioga County Extension

350,000

$58 MM

11/2011

Fully Subscribed

Completed

Northern Access Expansion

320,000

$77 MM

11/2012

Fully Subscribed

Completed

Line “N”

2012 Expansion

163,000

$41 MM

11/2012

Fully Subscribed

Completed

Line “N”

2013 Expansion

30,000

~$5 MM

11/2013

Fully Subscribed

Executed Precedent Agreement

Mercer Expansion Project

105,000

~$30 MM

11/2014

Fully Subscribed

Executed Precedent Agreement

West Side Expansion

95,000+

TBD

2013 to

2015

OS Concluded

Negotiating Precedent Agreements

Central Tioga County

Extension

260,000

~$150 MM

2015/2016

OS Concluded

Discussions with anchor shipper

West to East

~425,000

~$290 MM

~2016

29% Subscribed

Marketing continues with producers in

various stages of exploratory drilling

Total Firm Capacity: ~1,998,000+ Dth/D

Capital Investment: ~$687+ MM

36

April 2013 |

Midstream

Businesses NFG Midstream is Focused on Serving Appalachian Producers

37

April 2013

Midstream’s gathering systems are

critical to unlock remote, but highly

productive Marcellus acreage

History of operational success and

efficiency within Pennsylvania

Current focus is on developing and

expanding gathering infrastructure

for both Seneca and other producers

in the Appalachian Basin |

(1)

Footnote #1 goes here

April 2013

Midstream Businesses

38

Gathering Expansion Initiatives (NFG Midstream)

Project Name

Capacity

(Mcf/D)

Est.

CapEx

In-Service

Date

Market

Comments

Covington Gathering System

220,000

$40 MM

Multiple

Phases -

Most

In-Service

Capacity

Available

[Marketing to

Third Parties]

Completed

–

Flowing

into

TGP

300

Line. This includes ~$10 million of

current and future spending to

build pipeline to connect additional

wells

Trout Run Gathering System

466,000

$185 MM

May 2012

Capacity

Available

[Marketing to

Third Parties]

Completed

–

Flowing

into

Transco

Leidy Line. This includes ~$90

million of current and future

spending to build compression and

pipeline to connect additional wells

Tionesta Gathering System

10,000

$2.1 MM

FY2013

Q2

Fully Subscribed

Under Construction

Mt. Jewett Gathering System

10,000

$3.9 MM

FY2013

Q2

Fully Subscribed

Under Construction

Total Firm Capacity: ~706,000 Mcf/D

Capital Investment: ~$231 MM |

April

2013 Exploration & Production

39

Appendix |

April

2013 Seneca Resources

40

Hedge Positions and Strategy

Natural Gas

Swaps

Volume

(Bcf)

Average

Hedge Price

Fiscal 2013

51.4

$4.55 / Mcf

Fiscal 2014

62.7

$4.28 / Mcf

Fiscal 2015

31.9

$4.21 / Mcf

Fiscal 2016

19.7

$4.11 / Mcf

Fiscal 2017

17.9

$4.07 / Mcf

Oil Swaps

Volume

(MMBbl)

Average

Hedge Price

Fiscal 2013

1.3

$94.68 / Bbl

Fiscal 2014

1.6

$100.26 / Bbl

Fiscal 2015

0.6

$93.66 / Bbl

Fiscal 2016

0.4

$88.39 / Bbl

Most hedges executed at sales point to eliminate basis risk

Seneca has hedged approximately 72% of its

forecasted production for Fiscal 2013

Note: Fiscal 2013 hedge positions are for the remaining nine months of the fiscal year

|

April

2013 Seneca Resources

41

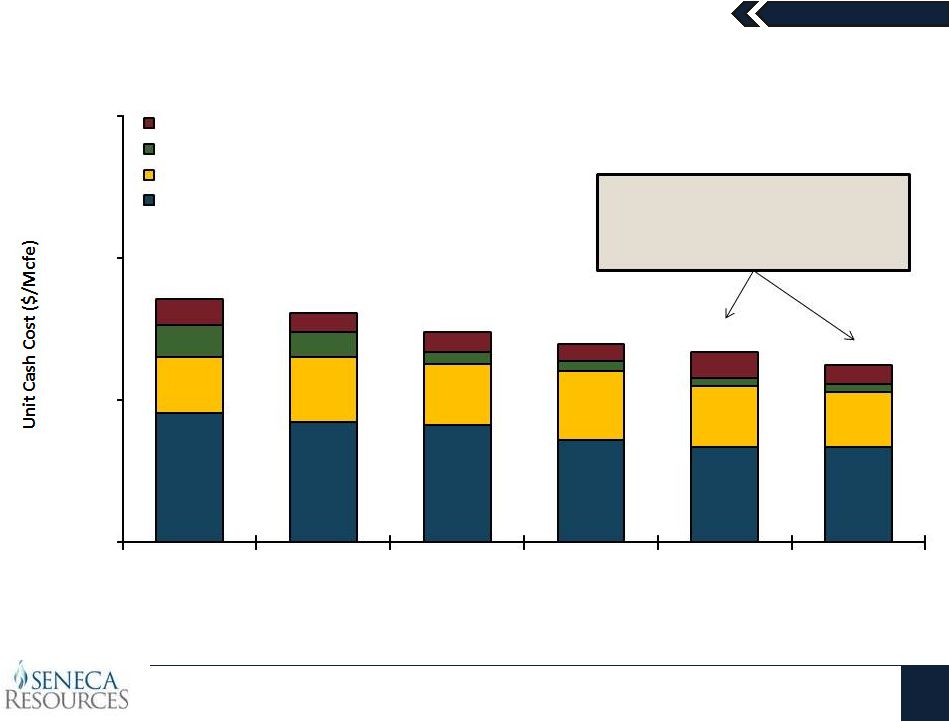

Continuing to Focus on Improving Its Cost Structure

Even after the new Pennsylvania Impact

Fee, 2012 unit cash costs decreased

from the prior year. We expect this

trend to continue in Fiscal 2013.

$1.36

$1.27

$1.24

$1.08

$1.00

1.00

$0.60

$0.69

$0.64

$0.73

$0.65

0.62

$2.57

$2.42

$2.22

$2.09

$2.01

$1.87

$0.00

$1.50

$3.00

$4.50

2008

2009

2010

2011

2012

2013 Forecast

Fiscal Year

Property, Franchise & Other Taxes

Other O&M Expense

General & Administrative Expense

Lease Operating Expense

$

(2)

$

(1)

(1)

Represents the midpoint of current General & Administrative Expense guidance of $58 to

$62 million, divided by the midpoint of current production guidance of 95 to 107 Bcfe (2)

Represents the midpoint of current Lease Operating Expense Guidance of $0.90 to

$1.10 per Mcfe |

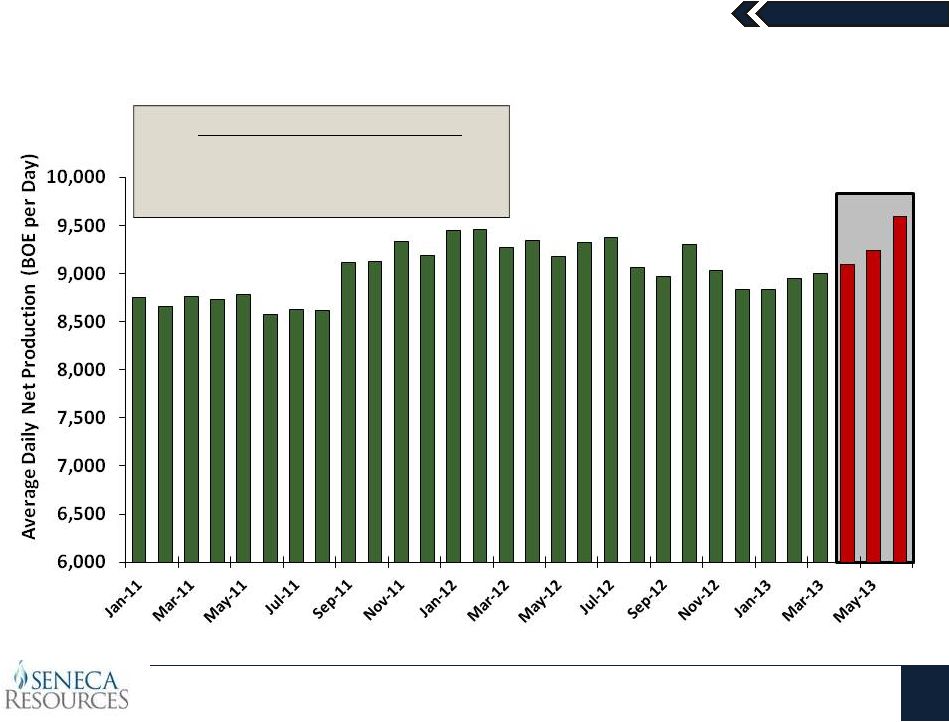

April

2013 Seneca Resources

42

California: Stable Production and Increasing Cash Flows

Net Acreage: 18,418 Acres

Net Wells: 1,478

Oil Gravity: 12 –

37°

Api

NRI: 87.64

Rank

Company

California

2011

BOEPD

1

Occidental

164,796

2

Chevron

163,153

3

Aera (Shell/Exxon)

149,974

4

Plains Exploration

36,775

5

Venoco Inc.

18,988

6

Berry Petroleum

18,872

7

Seneca Resources

9,209

8

Macpherson Oil

9,022

9

E&B Natural Resources

5,992

10

ExxonMobil

3,238 |

April

2013 Seneca Resources

43

California: Recent Initiatives Driving Near-Term Growth

Key Areas of Focus in 2013

1.

South Midway Sunset Field Extensions

2.

Sespe Infill Drill Program

3.

East Coalinga Evaluation

Forecast |

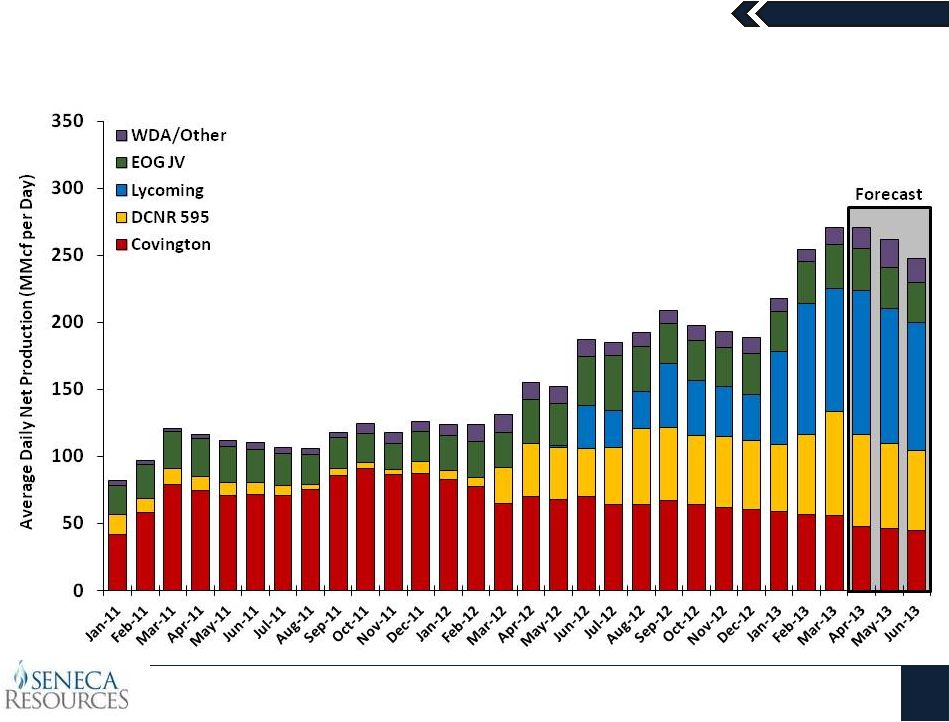

April

2013 Seneca Resources

44

Ramping Marcellus Shale Production |

April

2013 Marcellus Shale

45

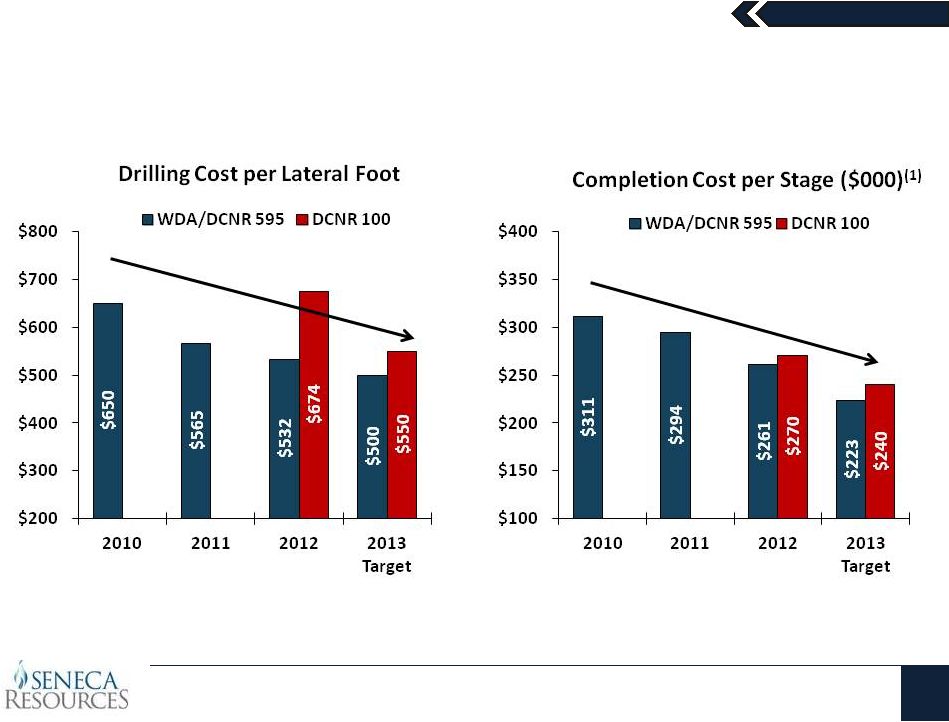

Targeting Continued Cost Reductions

(1) Completion Cost per Stage is for horizontal wells completed utilizing a standard

completion design, not a Reduced Cluster Spacing (RCS) completion design. |

April

2013 Utility

46 |

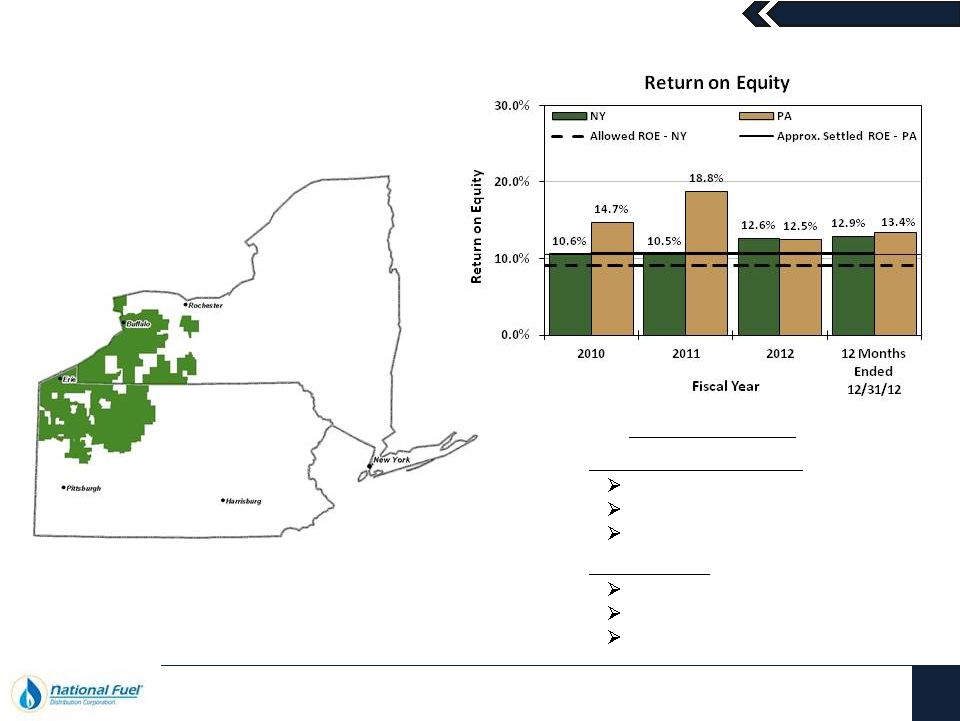

April

2013 New York & Pennsylvania

Low Income Rates

Choice Program/POR

Merchant Function Charge

New York only

Revenue Decoupling

90/10 Sharing

Weather Normalization

Utility

47

Providing Financial Stability

Rate Mechanisms |

April

2013 Utility

48

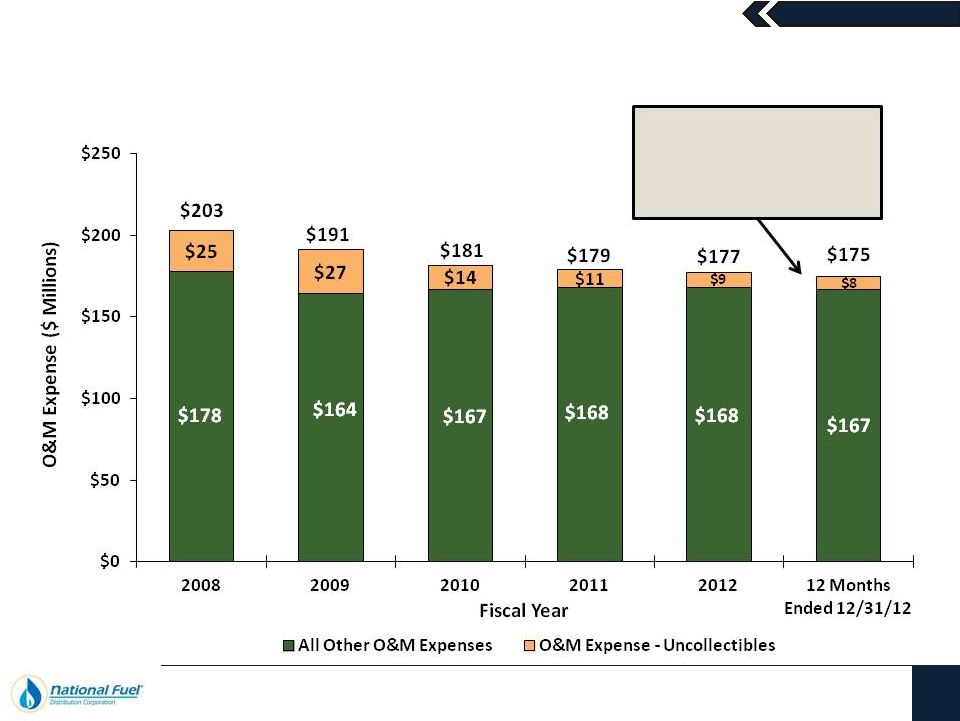

Continued Cost Control Helps Provide Earnings Stability

Low natural gas prices,

combined with a focus on

cost control, continue to

help reduce expenses |

April

2013 Utility

49

Strong Commitment to Safety

The anticipated increase in 2013

capital expenditures is largely due

to the implementation of a new

Customer Information System

The Utility remains

focused on consistent

spending to maintain

the ongoing safety and

reliability of its system |

April

2013 National Fuel Gas Company

50

Comparable GAAP Financial Measure Slides and Reconciliations

This presentation contains certain non-GAAP financial measures. For pages

that contain non-GAAP financial measures, pages containing the most directly

comparable GAAP financial measures and reconciliations are provided in the

slides that follow.

The Company believes that its non-GAAP financial measures are useful to

investors because they provide an alternative method for assessing the

Company’s operating results in a manner that is focused on the performance

of the Company’s ongoing operations, or on earnings absent the effect of

certain credits and charges, including interest, taxes, and depreciation,

depletion and amortization. The Company’s management uses these non-

GAAP financial measures for the same purpose, and for planning and

forecasting purposes. The presentation of non-GAAP financial measures is not

meant to be a substitute for financial measures prepared in accordance with

GAAP. |

April

2013 51

Reconciliation of Exploration & Production West Division Adjusted EBITDA

to Exploration & Production Segment Net Income

($ Thousands)

12 Months Ended

December 31, 2012

Exploration & Production -

West Division Adjusted EBITDA

224,201

$

Exploration & Production -

All Other Divisions Adjusted EBITDA

180,063

Total Exploration & Production Adjusted EBITDA

404,264

$

Minus:

Pennsylvania Impact Fee Related to Prior Fiscal Years (6,206)

Minus: Exploration & Production Net Interest Expense

(31,020)

Minus: Exploration & Production Income Tax Expense

(76,111)

Minus: Exploration & Production Depreciation, Depletion &

Amortization (198,064)

Exploration & Production Net Income

92,863

$

Exploration & Production Net Income

92,863

$

Pipeline & Storage Net Income

67,500

Utility Net Income

62,115

Energy Marketing Net Income

4,235

Corporate & All Other Net Income

609

Consolidated Net Income

227,322

$

|

April

2013 52

Reconciliation of Adjusted EBITDA to Consolidated Net Income

($ Thousands)

FY 2009

FY 2010

FY 2011

FY 2012

Exploration & Production - West Division Adjusted EBITDA

171,572

$

187,838

$

187,603

$

226,897

$

224,201

$

Exploration & Production - All Other Divisions Adjusted EBITDA

108,139

139,624

189,854

170,232

180,063

Total Exploration & Production Adjusted EBITDA

279,711

$

327,462

$

377,457

$

397,129

$

404,264

$

Total Adjusted EBITDA

Exploration & Production Adjusted EBITDA

279,711

$

327,462

$

377,457

$

397,129

$

404,264

$

Utility Adjusted EBITDA

164,443

167,328

168,540

159,986

164,386

Pipeline & Storage Adjusted EBITDA

130,857

120,858

111,474

136,914

146,147

Energy Marketing Adjusted EBITDA

11,589

13,573

13,178

5,945

6,065

Corporate & All Other Adjusted EBITDA

(5,575)

2,429

(2,960)

4,140

5,849

Total Adjusted EBITDA

581,025

$

631,650

$

667,689

$

704,114

$

726,711

$

Total Adjusted EBITDA

581,025

$

631,650

$

667,689

$

704,114

$

726,711

$

Minus: Net Interest Expense

(81,013)

(90,217)

(75,205)

(82,551)

(85,375)

Plus: Other Income

9,762

6,126

5,947

5,133

5,212

Minus: Income Tax Expense

(52,859)

(137,227)

(164,381)

(150,554)

(153,379)

Minus: Depreciation, Depletion & Amortization

(170,620)

(191,199)

(226,527)

(271,530)

(281,314)

Minus: Impairment of Oil and Gas Properties (E&P)

(182,811)

-

-

-

-

Plus/Minus: Income/(Loss) from Discontinued

Operations, Net of Tax (Corp. & All Other) (2,776)

6,780

-

-

-

Plus: Gain on Sale of Unconsolidated

Subsidiaries (Corp. & All Other) -

-

50,879

-

-

Plus: Elimination of Other Post-Retirement

Regulatory Liability (P&S) -

-

-

21,672

21,672

Minus: Pennsylvania Impact Fee Related to Prior Fiscal Years (E&P)

-

-

-

(6,206)

(6,206)

Rounding

-

-

-

(1)

2

Consolidated Net

Income 100,708

$

225,913

$

258,402

$

220,077

$

227,322

$

12-Months Ended

12/31/12 |

April

2013 53

Reconciliation of Segment Capital Expenditures to

Consolidated Capital Expenditures

($ Thousands)

FY 2013

FY 2009

FY 2010

FY 2011

FY 2012

Forecast

Capital Expenditures from Continuing Operations

Exploration & Production Capital Expenditures

188,290

$

398,174

$

648,815

$

693,810

$

$480,000-560,000

Pipeline & Storage Capital Expenditures - Expansion

52,504

37,894

129,206

144,167

$70,000-90,000

Utility Capital Expenditures

56,178

57,973

58,398

58,284

$65,000-70,000

Marketing, Corporate & All Other Capital Expenditures

9,829

7,311

17,767

81,133

$50,000-75,000

Total Capital Expenditures from Continuing Operations

306,801

$

501,352

$

854,186

$

977,394

$

$665,000-795,000

Capital Expenditures from Discountinued Operations

All Other Capital Expenditures

216

150

$

-

$

-

$

-

$

Plus (Minus) Accrued Capital Expenditures

Exploration & Production FY 2012 Accrued Capital Expenditures

-

$

-

$

-

$

(38,861)

$

-

$

Exploration & Production FY 2011 Accrued Capital Expenditures

-

-

(103,287)

103,287

-

Exploration & Production FY 2010 Accrued Capital Expenditures

-

(78,633)

78,633

-

-

Exploration & Production FY 2009 Accrued Capital Expenditures

(9,093)

19,517

-

-

-

Pipeline & Storage FY 2012 Accrued Capital Expenditures

-

-

-

(2,696)

-

Pipeline & Storage FY 2011 Accrued Capital Expenditures

-

-

(7,271)

7,271

-

Pipeline & Storage FY 2008 Accrued Capital Expenditures

16,768

-

-

-

-

All Other FY 2012 Accrued Capital Expenditures

-

-

-

(11,000)

-

All Other FY 2011 Accrued Capital Expenditures

-

-

(1,389)

1,389

-

All Other FY 2009 Accrued Capital Expenditures

(715)

715

-

-

-

Total Accrued Capital Expenditures

6,960

$

(58,401)

$

(33,314)

$

59,390

$

-

$

Eliminations

(344)

$

-

$

-

$

-

$

-

$

Total Capital Expenditures per Statement of Cash Flows

313,633

$

443,101

$

820,872

$

1,036,784

$

$665,000-795,000 |