Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - SMG Industries Inc. | v336853_ex31-1.htm |

| EX-32.1 - EXHIBIT 32.1 - SMG Industries Inc. | v336853_ex32-1.htm |

| EXCEL - IDEA: XBRL DOCUMENT - SMG Industries Inc. | Financial_Report.xls |

| EX-32.2 - EXHIBIT 32.2 - SMG Industries Inc. | v336853_ex32-2.htm |

| EX-31.2 - EXHIBIT 31.2 - SMG Industries Inc. | v336853_ex31-2.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark one)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the year ended December 31, 2012

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 000-54391

SMG INDIUM RESOURCES LTD.

(Exact name of registrant as specified in its charter)

| Delaware | 51-0662991 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 100 Park Ave., | |

| New York, New York, 10017 | (212) 984-0635 |

| (Address of principal executive offices, including zip code) | (Registrant’s telephone number, including are code) |

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

| Common Stock, par value $.001 per share | Warrants | Units | |||

| (Title of Class) | (Title of Class) | (Title of Class) |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirement for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§232.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10K. Yes ¨ No x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer”, and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ | |

| Non-accelerated filer ¨ (Do not check if a smaller reporting company) |

Smaller reporting company x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the registrant’s common stock held by non-affiliates computed by reference to the price at which the common stock was last sold as of June 30, 2012 was $12,627,296.

The number of shares of the registrant’s common stock outstanding as of March 8, 2013 was 8,803,817.

SMG Indium Resources Ltd.

Annual Report on Form 10-K

For the Year Ended December 31, 2012

TABLE OF CONTENTS

| Cautionary Note on Forward-Looking Statements | 1 | |

| PART I | ||

| ITEM 1. | Business | 2 |

| ITEM 1A. | Risk Factors | 17 |

| ITEM 1B. | Unresolved Staff Comments | 30 |

| ITEM 2. | Properties | 30 |

| ITEM 3. | Legal Proceedings | 30 |

| ITEM 4. | Mine Safety Disclosure | 30 |

| PART II | ||

| ITEM 5. | Market For Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 31 |

| ITEM 6. | Selected Financial Data | 32 |

| ITEM 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operation | 32 |

| ITEM 7A. | Quantitative and Qualitative Disclosures About Market Risk | 39 |

| ITEM 8. | Financial Statements | 39 |

| ITEM 9. | Changes In and Disagreements With Accountants on Accounting and Financial Disclosure | 39 |

| ITEM 9A. | Controls and Procedures | 39 |

| ITEM 9B. | Other Information | 40 |

| PART III | ||

| ITEM 10. | Directors, Executive Officers and Corporate Governance | 41 |

| ITEM 11. | Executive Compensation | 46 |

| ITEM 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 52 |

| ITEM 13. | Certain Relationships and Related Transactions, and Director Independence | 54 |

| ITEM 14. | Principal Accounting Fees and Services | 55 |

| PART IV | ||

| ITEM 15. | Exhibits and Financial Statement Schedules | 56 |

Cautionary Statement Regarding Forward-Looking Statements

Unless otherwise indicated, the terms “SMG Indium,” “SMG,” the “Company,” “we,” “us,” and “our” refer to SMG Indium Resources Ltd. In this Annual Report on Form 10-K, we may make certain forward-looking statements, including statements regarding our plans, strategies, objectives, expectations, intentions and resources that are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. The Securities and Exchange Commission (“SEC”) encourages companies to disclose forward-looking information so that investors can better understand a company’s future prospects and make informed investment decisions. This Annual Report on Form10-K contains such “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be made directly in this Annual Report, and they may also be made a part of this Annual Report by reference to other documents filed with the Securities and Exchange Commission, or SEC, which is known as “incorporation by reference”.

The statements contained in this Annual Report on Form 10-K that are not historical fact are forward-looking statements (as such term is defined in the Private Securities Litigation Reform Act of 1995), within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended,, and Section 27A of the Securities Act of 1933, as amended. Forward-looking statements may be identified by the use of forward-looking terminology such as “should,” “could,” “may,” “will,” “expect,” “believe,” “estimate,” “anticipate,” “intends,” “continue,” or similar terms or variations of those terms or the negative of those terms. All forward-looking statements are management’s present expectations of future events and are subject to a number of risks and uncertainties that could cause actual results to differ materially from those described in the forward-looking statements. These statements appear in a number of places in this Form 10-K and include statements regarding the intent, belief or current expectations of SMG Indium Resources Ltd. Forward-looking statements are merely our current predictions of future events. Investors are cautioned that any such forward-looking statements are inherently uncertain, are not guaranties of future performance and involve risks and uncertainties. Actual results may differ materially from our predictions. There are a number of factors that could negatively affect our business and the value of our securities, including and not limited to indium price volatility from supply and demand factors, international export quotas that could affect the availability of indium and our ability to purchase indium, lack of any internationally recognized exchanges for indium, limited number of potential suppliers of indium and potential customers who purchase indium, disruption of mining operations, technological obsolescence, substitution of other materials decreasing the demand for indium, regulatory requirements regarding indium, risks associated with international economic and political events, lack of operational liquidity, lack of investment liquidity, factors affecting our Net Market Value (“NMV”), and changes in interest rates. Such factors could materially affect our Company's future operating results and could cause actual events to differ materially from those described in forward-looking statements relating to our Company. Although we have sought to identify the most significant risks to our business, we cannot predict whether, or to what extent, any of such risks may be realized, nor is there any assurance that we have identified all possible issues that we might face.

In light of these assumptions, risks and uncertainties, the results and events discussed in the forward-looking statements contained in this Annual Report or Form 10-K or in any document incorporated by reference might not occur. Stockholders are cautioned not to place undue reliance on the forward-looking statements, which speak only as of the date of this Annual Report or Form 10-K or the date of the document incorporated by reference in this Annual Report or Form 10-K, as applicable. We are not under any obligation, and we expressly disclaim any obligation, to update or alter any forward-looking statements, whether as a result of new information, future events or otherwise except as may be required by applicable law. All subsequent forward- looking statements attributable to the Company or to any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. We urge readers to carefully review and consider the various disclosures we make in this report and our other reports filed with the SEC that attempt to advise interested parties of the risks, uncertainties and other factors that may affect our business including the risk factors included herein under Item 1A“Risk Factors.”

| 1 |

PART I

Item 1. Business

Introduction

We are a corporation established pursuant to the laws of Delaware on January 7, 2008. On April 2, 2008, we changed our name from Specialty Metals Group Indium Corp. to SMG Indium Resources Ltd. We operate a single-segment business whose primary business purpose is to purchase and stockpile indium, a specialty metal that is being increasingly used as a raw material in a wide variety of consumer electronics manufacturing applications. We may also lend, lease or sell indium if management believes it is advantageous. Effective with the quarter ended June 30, 2011 we are considered an operating company and are no longer considered a development stage company.

We were formed to purchase and stockpile the metal indium. Our strategy is to achieve long-term appreciation in the value of our indium stockpile, and not to actively speculate with regard to short-term fluctuations in indium prices. We plan to achieve long-term appreciation in the value of our indium stockpile primarily through price appreciation of the physical metal. Price appreciation of the metal indium held in our stockpile is critical for us to maintain our NMV and for investors to receive a return on their investment. However, there is no assurance that the price of indium or the value of our securities will increase over time. In fact, the price of indium has declined substantially from its high in March 2005. To our knowledge, this is currently the only investment that allows potential stockholders to participate in any price appreciation of indium other than through physical delivery of the metal itself. Our structure provides a simple and efficient mechanism by which a public stockholder may benefit from any appreciation in the price of indium. Our stockholders have the ability to effectively purchase an interest in indium in a manner that does not directly include the risks associated with ownership of companies that explore for, mine and process indium. Our common shares represent an indirect interest in the physical indium we own.

All of the indium we purchase and own is, and will be, insured and physically stored in reputable, adequately capitalized and insured third-party warehouses or storage facilities located in the United States, Canada, the Netherlands and/or the United Kingdom. These third party facilities provide storage and safeguard of our indium inventory, insurance, handle the transfer of our indium inventory in and out of the facility, visual inspections, spot checks, arrange and facilitate independent third-party random assays, confirmation of deliveries to supplier packing lists, and reporting of transfers of inventory to us.

We utilize and expect to continue to utilize facilities that meet our requirements that are either: (i) located closest in proximity to our indium suppliers in order to reduce transportation fees or (ii) located closest in proximity to our corporate headquarters or satellite offices in order to facilitate our ability to inspect our inventory and reduce future corporate expenses associated with travel. We believe there are numerous third-party storage facilities that provide more than adequate services that meet our criteria, which eliminates the need for hiring a custodian. From inception through December 31, 2012, our Manager, Specialty Metals Group Advisors LLC, which is a related party, purchased on our behalf approximately 47.0 metric tons (“mt”) of indium, which is currently stored in an insured, secure facility in New York owned and operated by Brink’s Global Services U.S.A., Inc. (‘‘Brink’s’’), a bonded warehouse. Our chief executive officer or our chief operating officer inspects the facilities. The facilities are visited at least once per year for inspection.

Our expenses will be required to be satisfied by cash on hand that is not set aside for the purchase of indium. Cash on hand that is not set aside to purchase indium is expected to be sufficient to satisfy our operating expenses for at least three years. Our annual cash operating expenses, including management fees, are estimated to be approximately $1.2 million. We may subsequently lend, lease or sell some, or all, of our indium stockpile to cover our operating expenses. Alternatively, we may seek to raise additional capital to cover our operating expenses through potentially dilutive equity offerings or debt financing. Our stockpile of indium may decrease over time due to sales of indium necessary to pay our annual operating expenses. Without increases in the price of indium sufficient to compensate for any such decreases, our net market value (“NMV”) will decline. Our stockpile of indium may also decrease over time due to sales of indium against purchases of common shares that are priced lower than our NMV per common share. In such instances, our NMV per common share would rise. NMV is a non-GAAP measure-see below under “GAAP verses non-GAAP Disclosure.”

All of our indium transactions are negotiated by our Manager, a related party. Our Manager is paid a 2.0% per annum fee based on our NMV as compensation for these services. The NMV is determined by multiplying the number of kilograms of our indium holdings by the last spot price for indium published by Metal Bulletin PLC posted on Bloomberg L.P., plus cash and any other assets, less any and all of our outstanding payables, indebtedness and any other liabilities.

| 2 |

Our officers and directors have limited experience in stockpiling the metal indium prior to joining the Company, although our chief executive officer had experience purchasing, selling, storing and lending precious metals, base metals, non-exchange traded metals, and illiquid metals.

Our Manager:

| • | first and foremost, purchases and stockpiles indium ingots with a minimum purity level of 99.99% on our behalf; |

| • | negotiates storage arrangements for our indium stockpile in warehouses or third-party facilities located in the United States, Canada, the Netherlands and/or the United Kingdom; |

| • | makes sure the stockpile is fully insured by either the storage facility’s insurance policy, a separately purchased insurance policy, or both; |

| • | purchases insurance on standard industry terms to insure the indium which we own during its transportation to and from the storage facility; |

| • | is responsible for conducting limited inspections of the indium delivered to us; |

| • | relies on the good faith of its suppliers to provide indium that meets our requirements. If indium is purchased from a third-party supplier that is not known to be a regular indium industry supplier, our Manager, at its discretion, may hire, at our expense, an independent lab to perform random assay tests to verify the purity of the indium. The Manager uses only reputable assayers recommended by reliable third-party sources; |

| • | may lend, lease and/or sell indium from our stockpile, based on market conditions; |

| • | publishes on our website the spot price of indium, our NMV and the quantity of indium held in inventory on a bi-weekly basis. |

Metal Bulletin’s bi-weekly indium price quotation is posted on our website, www.smg-indium.com. If for any reason, Metal Bulletin’s bi-weekly indium price quotation is not available, other independent indium quotation providers are available including Platt’s Metals Week, Metal-Pages Ltd., Asian Metal Ltd. and Metal Prices. Within two business days of any change in inventory held, the quantity of indium will be published on our website.

We are not legally prohibited from pursuing other business strategies pursuant to our certificate of incorporation, as amended, or any other corporate document. If based on market conditions our Manager determines that it may be in our best interest to expand our lending, leasing and/or selling activities beyond what is necessary to cover operating expenses or if the Manager determines that we should begin actively speculating on short-term fluctuations in indium prices or pursue strategic transactions with other companies operating in the indium market including the Federal Government, the Manager will be required to obtain the approval of our board of directors to adopt such a strategic change in our business directive. Additionally, we will promptly notify stockholders of any such modifications to our stated business plan. Our operations have been limited to purchasing, stockpiling, lending or leasing the metal indium. Recently, our board of directors granted management the authority to sell indium from inventory if management believes the price of indium is advantageous.

Suppliers

We have and intend to stockpile already mined and processed indium ingots with a minimum purity level of 99.99%, known as 4N or four nines grade. Based on common industry knowledge and our established indium industry relationships, we can determine which companies are regular indium industry suppliers. We consider companies granted indium export licenses from the Chinese government as regular indium industry suppliers. We consider companies such as Teck Resources Limited., Xstrata Plc, Indium Corporation of America, Umicore Indium Products Co. Ltd., Molycorp Inc. and Aim Specialty Materials as regular industry suppliers because they are all well known within the industry and have well established reputations. We consider metal trading houses listed in our ‘‘Competition’’ section like Traxys North America LLC, Glencore International AG, Wogen PLC, 5N Plus Inc., etc. that have years and in some cases, decades of experience within the industry as regular indium industry suppliers. We use subjective criteria to determine whom we do business with and for competitive reasons we do not disclose specifically which companies we intend to do business with. Currently, an established regular indium industry designated supplier list does not exist.

| 3 |

Strategy and Policies

Through December 31, 2012, we purchased approximately 47.0 metric tons of indium and we have fully met our commitment of utilizing 85% of the net proceeds from our initial public offering (“IPO”) to purchase indium. Our business model is premised on the long-term appreciation in the value of our indium stockpile. If there is a significant appreciation in the price of indium, we may sell some or all of the indium held in our stockpile. Our business plan could be adversely affected by the substantial competition we face in the marketplace. There are a substantial number of manufacturers that require indium for the production of flat panel displays (“FPDs”), liquid crystal display (“LCDs”), personal digital assistant (“PDAs”), light emitting diodes (“LEDs”) and copper indium gallium selenide (“CIGS”) thin film photovoltaics. We expect to compete with manufacturers for purchase of the primary indium supply or sales of our indium stockpile. The fact that many of these companies have more substantial resources than us and have established relationships with indium industry suppliers may prove to be detrimental to our ability to effectuate our business plan.

We may face direct competition from market participants in purchasing or selling our stockpile of indium. There are no other companies, known to us, that have a business model solely dedicated to the purchasing and stockpiling of indium. However, we would have to potentially compete with miners, refiners, suppliers, end-users, traders and other market participants in purchasing or selling indium. The companies listed in the ‘‘Competition’’ section are a partial list of companies that are well known indium industry participants that either mine, refine, use, and or trade indium. These companies would be considered indirect competition.

We have purchased only a limited quantity of indium from the recycling market. After extensive discussions with indium industry participants, we determined that it is not feasible for us to buy substantial quantities of indium directly from the recycling companies. Recycling scrap indium into 3N7 or higher purity metal ingot is a complex and time consuming process. Typically, end users (i.e. FPD manufacturers) establish contracts directly with the recyclers. Pursuant to such contracts, the end user supplies the recycler with scrap indium and the recycler specially processes, refines, and then returns the purified recaptured indium to the end user. Typically, recyclers do not sell the recycled indium to anyone else other than the end user who supplied the scrap indium. Industry insiders consider the recycling market a ‘‘closed loop.’’ End users and recyclers do not disclose the particulars of their relationships and contracts. This inaccessibility will limit us to the primary indium market. The primary market is smaller than the recycling market and may affect our ability to purchase any additional indium. Furthermore, Chinese export restrictions may serve to further reduce our access to more than 50% of the world’s primary indium production.

The indium market is illiquid and considered small compared to the base metals. There are a limited number of suppliers and purchasers of indium. If new companies are formed to purchase and stockpile indium, and in the event we raise additional capital to purchase more indium, this may adversely affect our ability to procure sufficient quantities of indium on a timely basis or even at all.

Indium Price Trends

The annual average price of indium, as published by Metal Bulletin and posted on Bloomberg L.P., decreased from $696 per kilogram in 2011 to $528 per kilogram in 2012; a decline of 24.1%. In 2012, indium traded in a range from $450 per kilogram to $600 per kilogram and ended the year at $485 per kilogram, which represented a decrease of 14.9% from the closing price of $570 per kilogram at the end of 2011. The average price of indium had increased from $567 per kilogram in 2010 to $696 per kilogram in 2011.

Accounting for Direct Sales and Lending Transactions

From time to time we may enter into ‘‘direct sales and or ‘‘lending’’ transactions. Under a ‘‘direct sale’’ transaction, we would record as income, or loss, the difference between the proceeds received from the sale of indium and the indium carrying value. We engage in lending indium from time to time as a means of generating income to help cover annual operating expenses. A typical loan contract would be for terms of six months or less, and in almost no circumstance would it exceed a period of one year. As lender, we negotiate an Unconditional Sale and Purchase Agreement (‘‘USPA’’) with a prospective borrower. As part of the USPA, once all terms are reviewed and approved by our management team, we physically deliver indium to the borrower.

| 4 |

In indium lending transactions, we exchange a specified tonnage and purity of indium for cash. Title and the risks and rewards of such indium ownership pass to the purchaser/counterparty in the lending transaction. We simultaneously enter into an agreement with such counterparty in which it unconditionally commits to purchase and the counterparty unconditionally commits to sell a specified tonnage and purity of indium that is to be delivered to us at a fixed price and at a fixed future date in exchange for cash (the USPA). In some cases, the USPA may contain terms providing the counterparty with substantial disincentives (“penalty fees”) for nonperformance of the return of indium to the Company as a means to assure our future supply of indium. While we believe that this risk would be mitigated by the penalty fee features of the USPA, it is nonetheless a risk associated with a transaction of this type. We account for USPA transactions on a combined basis (sale and purchase) and evaluate whether, and in what period, other income may be recognized based on the specific terms of any arrangements. We disclose unconditional purchase obligations under these arrangements and, if applicable, accrue net losses on such unconditional purchase obligations.

There is no established market lending rate for indium. The terms of the USPA contracts stipulate that the indium returned must be of equivalent quantity and purity. In the event of a loan to the producer, in which we have received dollars for the indium lent, there is a risk that the producer will not return the equivalent quantity or quality indium. Failure of the producer to perform is a risk to our business if the price of indium appreciates and we cannot replace the loaned indium at the same or a lower price than we loaned the indium. The ability of the borrower to satisfy the commitment to return the equivalent quantity and purity of indium is a business risk that we face in a lending transaction. However, the penalty fee aspect as detailed in our USPA, if included, would somewhat mitigate our overall business risk because the penalty fee would provide funds for us to purchase indium from other sources at less than favorable prices (if applicable). Notwithstanding the foregoing, if the borrower defaults on its obligations under the USPA, there is always the risk that we might not be able to replace the indium lent at favorable prices. In such instances, we may not be able to recoup our losses through litigation and we would assume the loss which could negatively impact our NMV.

Indium Market Overview

About Indium

Indium (symbol In) is a rare, very soft, silvery-white malleable metal with a bright luster. It is number 49 on the Periodic Table of Elements with an atomic weight of 114.81. Indium is chemically similar to aluminum and gallium, but more closely resembles zinc. Indium is a rare element and ranks 61st in abundance in the Earth’s crust at an estimated 240 parts per billion by weight. This makes it about three times more abundant than silver or mercury. Indium occurs predominantly in the zinc-sulfide ore mineral, sphalerite. Indium is produced mainly from residues generated during zinc ore processing, but is also found in iron, lead, and copper ores. According to the USGS, the average indium content of zinc deposits from which it is recovered, ranges from less than 1 part per million to 100 parts per million. Its occurrence in nature with other base metal ores is sub-economic for indium recovery. Pure indium in metal form is considered non-toxic by most sources.

Properties and Characteristics of Indium

Indium is very malleable and ductile and can be easily formed into a wide variety of fabrications. Another distinctive characteristic of indium is that it retains its softness at temperatures approaching absolute zero degrees, making it ideal for cryogenic (freezing or very low temperature) and vacuum applications. The properties of indium may be summarized as follows:

| • | Low melting point alloy: It is useful in the high-end optical industry where lenses can be held with the alloy instead of the lens surfaces during the polishing process to minimize surface distortion. |

| • | Lead-free and mercury-free solder industries: It is commonly used by environmentally friendly electronics goods manufacturers and high-energy alkaline dry cell batteries producers in their respective industries. This reduces or eliminates the use of lead and mercury in soldering. |

| • | Cold Welding: Oxide-free indium has the ability to cold-weld or attach to itself. Parts coated with indium can be bonded together without the application of heat or chemicals. |

| • | Reduce gold scavenging: When soldering to gold or gold-plated surface, solder has a tendency to dissolve gold into the joint. The addition of indium to solder will reduce this tendency. |

| 5 |

| · | Bond glass, quartz and ceramics: These materials cannot be bonded with traditional solders. Indium’s unique cold-welding properties allow it to produce a bond in a variety of non-metal applications. |

| · | Transparent Electrical Conductor: When indium (in the form of indium-tin-oxide) is coated onto various materials such as glass or plastic films, it acts as a transparent electrical conductor and an infrared reflector. |

| · | Malleable: Because indium is so soft and pliable (malleable), it can easily fill voids between two surfaces, even at cryogenic (freezing or very low) temperatures. |

Demand for Indium

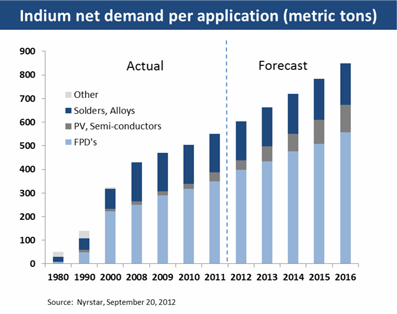

Indium is an indispensable raw material to the LCD market. Currently, a very small amount of indium is required in the fabrication of the vast majority of flat panel displays (“FPD’s”) produced. This is the primary use of indium today, accounting for nearly two thirds of indium consumption.

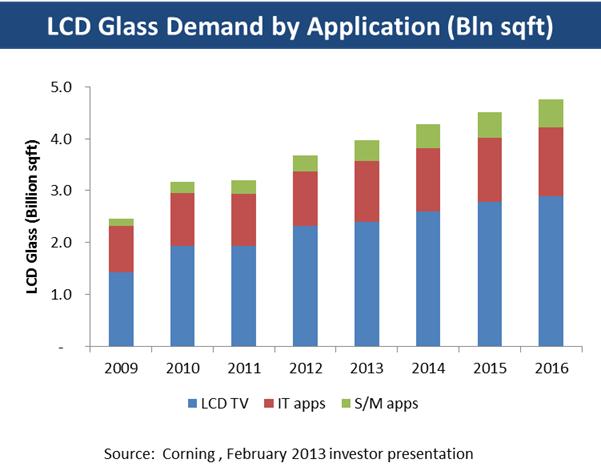

Demand for indium, driven by the LCD industry, has grown in the last decade as flat panel displays have effectively driven the once dominant cathode ray tube (“CRT”) into obsolescence. Indium, in the form of indium-tin-oxide (“ITO”), creates the optically transparent electrodes that drive LCD displays on TVs, computer monitors, laptops, tablets, cell phones and other devices. Beyond a few niche applications, LCDs currently do not function without indium and, there is no practical, large scale, substitute transparent conductive oxide. According to investor presentations made by Corning Incorporated, one of the world's largest LCD glass manufacturers, LCD glass demand has grown from 1.7 billion square feet in 2007 to about 3.5 billion square feet in 2012 and could grow to 3.76 billion square feet in 2013.

| 6 |

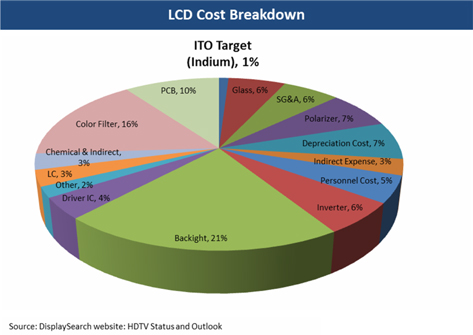

The cost of the indium contained within an LCD display, relative to the cost of the actual LCD display, is marginal, representing about 1% of the total cost of production. Therefore, industry experts believe that a sharp rise in the price of indium is unlikely to significantly reduce demand for the metal by the LCD industry.

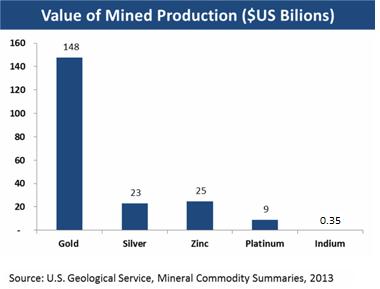

Indium supply is constrained by global smelting capacity capable of indium extraction and production levels, as reported by USGS, have increased over the last three years after decreasing from 2006 through 2009. Indium is a minor by-product of zinc mining (and to a lesser extent, lead and tin) representing a small credit to production. The value of indium mined in 2012 was approximately $354 million, representing 1.4% of the value of the $25 billion zinc market in 2012. Currently, there are no indium mines and zinc producers do not increase zinc production for the purpose of extracting additional quantities of indium.

Although production scrap is reworked in the normal course of operations, it is not currently economical to recycle indium from post-consumer scrap from sources such as used LCD displays.

| 7 |

New technology driven applications for indium are emerging in LED lighting, thin-film solar PVs and high performance semiconductors. In recent government sponsored reports, the U.S. and Europe have each identified indium as a critical metal upon which important industries, including clean energy, are dependent. China, Japan and South Korea also view indium as critical to their industries and are either developing strategic stockpiles, or laying the groundwork to do so.

According to USGS, the total production of primary indium was estimated to be 670 and 662 mt in 2012 and 2011, respectively. We calculated, based on the prices Metal Bulletin posted on Bloomberg L.P., that the average price for indium was $527.63 and $696.28 per kilogram in 2012 and 2011, respectively. Based on these figures, we determined that the size of the primary indium market was approximately $354 million and $461 million in 2012 and 2011, respectively. Industry information with regards to monthly sales volumes and dollar values of indium transactions is not readily available. Indium does not trade on any forwards or futures exchanges and there are no indium forwards or futures contracts.

In a June 2010 report titled "Critical Raw Materials for the EU" (http://ec.europa.eu/enterprise/policies/raw-materials/critical/index_en.html), the European Commission identified a list of 14 economically important raw materials, including indium, which is subject to a higher risk of supply interruption. There are a number of reasons for this heightened supply risk, one of which is the high concentration of the production of a raw material in a given non-EU country. In the case of indium, over 50% of production is based in China. In March 2012, the Commission provided a preliminary analysis into the added value and feasibility of a possible stockpiling program of raw materials, including indium. Based on a study commissioned by the German Federal Ministry of Economics and Technology, referenced in the 2010 report, the demand for indium from emerging technologies is expected to grow from 234 mt in 2006 to 1911 mt in 2030. Indium’s demand in 2030 could exceed 2006 supply levels by 3.29 times. Also, a December 2010 report published by the U.S. Department of Energy entitled, “Critical Materials”, suggests that over 1500 mt of indium could be consumed annually by 2025 for clean energy technologies alone.

Applications

FPDs, LCDs & LEDs

Indium is an essential raw material for a number of consumer electronics applications. The primary commercial application of indium is in coatings for the FPD industry. Indium is most useful when chemically processed with tin-oxide to form ITO, an optically transparent and electrically conductive material. Sputtering targets are placed in a vacuum and thin layers of ITO are then applied as electrical contacts onto LCD glass; the thin, technically pristine sheets of glass used to produce LCDs on electronic devices like television sets, computers and mobile phones. In addition to its unique combination of transparency and conductivity, ITO is also preferred for use in LCD technology due to its other unique qualities of low melting point, good uniformity (which is suitable for large LCDs), fast etching time and long life span. Production of ITO thin-film coatings accounted for approximately 66.0% of global indium consumption. Of the remaining 34.0% of the global indium market, other end uses include solders, alloys and compounds, 27.0%; electrical components, semiconductors and PV 7.0%.

Currently, the new generation of LED backlit LCD TVs and computer monitors, as well as organic light emitting (‘‘OLED’’) TVs and displays, all use indium. LED is a semiconductor device that emits visible light or infrared radiation when an electric current is passed. The visible emission, often a high-intensity light, is useful in a whole host of applications. Most LED’s, such as blue, green and white LEDs, require indium. LEDs are a rapidly expanding market. An early use of high brightness LEDs (“HB-LEDS”) was in the automotive sector in the form of lights, dashboard lights and in traffic signals. Backlighting for TVs, computers and cell phones currently drive the bulk of LED demand. LED use in general lighting is in the early stages of adoption and is expected to be a very large market. Japanese LED light bulb sales surpassed incandescent sales in 2011.

| 8 |

Solar Energy Technology

Indium-based CIGS is a new semiconductor material comprised of copper, indium, gallium, and selenium. Its main use is for high-efficiency photovoltaic cells (CIGS cells), in the form of thin-film photovoltaic. The thin-film photovoltaic has several advantages over traditional solar energy technologies. It is lightweight, can be applied on uneven surfaces and can be rolled up when not in use. CIGS shows great promise in the lab in achieving high conversion efficiencies at low costs. According to the USGS, CIGS solar cells require approximately 50 metric tons of indium to produce 1 gigawatt ("GW") of solar power. We believe that over time, as manufacturing efficiencies are achieved through mass production, consumption of indium per GW of CIGS production will decrease by as much as fifty percent compared to USGS's estimate. Research is underway to develop a low-cost manufacturing process for flexible CIGS solar cells that would yield high production throughput. Flexible CIGS solar cells are already in use in roofing materials, and we believe they could also be used in other building integrated photovoltaics (“BIPVs”) and in various applications in the aerospace, military and recreational industries.

Other Uses

| • | Indium is also used in the manufacture of low-melting-temperature alloys. An alloy consisting of 24.0% indium and 76.0% gallium is liquid at room temperature. |

| • | Some indium compounds such as indium antimonide, indium phosphide, and indium nitride are semiconductors with useful properties. |

| • | Indium is also used in Laser Diodes (LDs) based on compound semiconductors. |

| • | Ultrapure indium, specifically high purity trimethyl indium, is used in compound semiconductors. |

| • | Indium oxide is used as transparent conductive glass substrate in the making of electroluminescent panels. |

| • | Indium is also used as a light filter in low pressure sodium vapor lamps. |

| • | Indium is suitable for use in control rods for nuclear reactors, typically in an alloy containing 80.0% silver, 15.0% indium, and 5.0% cadmium. |

| • | 111-Indium (isotope) is used in medical imaging to monitor activity of white blood cells. |

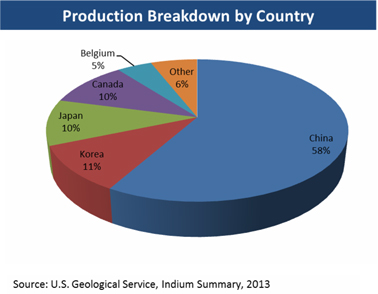

Supply of Indium

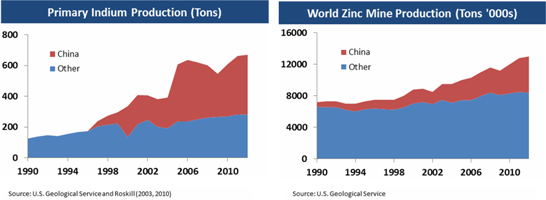

According to the USGS, the top five indium producing countries in the world in 2012 and 2011 were China, Japan, Canada, Republic of Korea and Belgium. China’s refinery production of indium was approximately 390 and 380 metric tons in 2012 and 2011, respectively. This is approximately 58% and 53% of the annual total global refined primary production of 670 mt. and 640 mt. in 2012 and 2011, respectively. According to the USGS, annual worldwide production had ranged between 546 mt to 609 mt per year from 2007 to 2010. Worldwide annual production further increased to an estimated 662 mt in 2011 and to 670 mt in 2012.

The recycling of indium has increased in recent years. The indium recycling market is now larger than primary refinery production. Recycling scrap indium into 3N7 or higher purity metal ingot is extremely complex and time consuming. Japan is the primary market for indium recycling, with over 450 metric tons per year (“tpy”) of secondary indium production capacity, according to Roskill. If recycling activity continues to grow and becomes more efficient, this may serve to increase the total worldwide indium supply.

China

According to the USGS, China controls over 50% of the world’s refined indium production. There are a number of major producers in China, but also numerous smaller producers, relying on purchasing the concentrates from the larger base-metal refiners. China produces approximately 390 metric tons of indium per year.

| 9 |

World Refined Indium Production (Metric Tons)

| 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | |||||||||||||||||||

| China | 320 | 310 | 280 | 340 | 380 | 390 | ||||||||||||||||||

| Korea, Republic of | 50 | 75 | 70 | 70 | 70 | 70 | ||||||||||||||||||

| Japan | 60 | 65 | 67 | 70 | 70 | 70 | ||||||||||||||||||

| Canada | 50 | 45 | 40 | 67 | 75 | 70 | ||||||||||||||||||

| Belgium | 30 | 30 | 30 | 30 | 30 | 30 | ||||||||||||||||||

| Russia | 12 | 12 | 4 | n/a | 5 | 5 | ||||||||||||||||||

| France | 10 | 0 | 0 | n/a | n/a | n/a | ||||||||||||||||||

| Brazil | n/a | n/a | n/a | 5 | 5 | 5 | ||||||||||||||||||

| Peru | 6 | 6 | 25 | n/a | n/a | n/a | ||||||||||||||||||

| United States | 0 | 0 | 0 | 0 | 0 | 0 | ||||||||||||||||||

| Other Countries | 25 | 25 | 30 | 27 | 27 | 30 | ||||||||||||||||||

| World Total | 563 | 568 | 546 | 609 | 662 | 670 | ||||||||||||||||||

(1) Table is taken from the U.S Geological Survey Minerals Commodities Summaries, January 2008 through January 2013.

China is responsible for most of the increased global zinc and indium production in the last two decades. China has now become the world’s largest producer and consumer of metals and minerals. Much of China’s demand for zinc is a result of infrastructure expansion. The massive development of their mining and smelting industry strained the resources of the country and had a detrimental impact on the environment. The Chinese government responded to this adversity with a policy of replacing small, dirty and inefficient plants with large, new and efficient smelters and refineries designed to comprehensively recover by-products that would otherwise be waste. Additionally, Chinese zinc ores are uncommonly high in their indium content. As Chinese zinc output swelled to approximately 40% of global production, the Chinese policy of comprehensive recovery resulted in a surge of indium production.

| 10 |

The Chinese government restricts the export of indium with taxes and quotas. In December 2009, China announced it would reduce export taxes on unwrought indium, indium scrap and indium powder from the 10.0% to 15.0% level in 2009 to 5.0% in 2010. In December 2012, China's Ministry of Commerce published the list of indium exporters with the first batch of export quotas for 2013. There are 16 companies on the list, one company less than 2012. The approved export quota volume for the first batch of 2013 represents approximately 60% of the total export quota volume for the year. According to the list, the first batch of quotas awarded to each company is the same as the previous year. The indium export quota volume for the first batch of 2013 is 138.26 mt. Therefore, the Chinese export quota for 2013 is approximately 231 mt of indium, essentially unchanged from 2012.

Canada

The USGS estimated that in 2012 Canada produced 70 mt of indium, a slight decrease from the 75 mt produced in 2011. Teck Resources Ltd. is the largest producer of indium in Canada.

United States

The United States does not produce any primary domestic indium and relies on imports from China, Canada, Japan, Russia, and other countries. Very little indium is recycled in the United States. We believe this is because there is no infrastructure for the collection of used indium-containing products.

New Production

“Critical Materials Strategy”, a 2010 U.S. Department of Energy report highlighting the availability of metals required for the development of clean energy technologies and identifies approximately 50 mt of new indium production they expect annually by 2015. The countries and respective supplies that are assumed to be coming online by 2015 are (i) Australia (15 mt per year), (ii) South America (15–20 mt per year), (iii) Brazil (15 mt per year) and (iv) Russia (2 mt per year).

Zinc Supply

According to the USGS, total worldwide zinc production was 12.8 million mt in 2011 and an estimated 13.0 million mt in 2012. Yearly zinc production dwarfs the 2012 estimated total primary refined indium production figures of 670 mt. Total indium production represents approximately one hundredth of one percent of total zinc production on an annual basis.

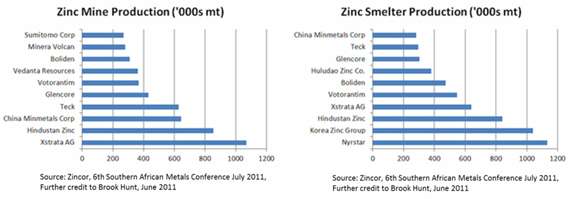

Zinc is a loosely amalgamated industry, with the top 10 producers accounting for only 40% and 44% respectively of mined and smelted zinc, as reported by Zincor at the July 2011 Southern African Metals Conference:

Flat Panel Displays (FPDs)

We believe the demand for indium will grow for the foreseeable future. We believe the markets for flat panel displays are strong, particularly for larger display televisions, tablet computers and smartphones. We expect that overall growth in the LCD industry will be driven by an increase in the average display size and as well as growth in unit sales of LCD displays which in turn will continue to generate increased demand for indium.

| 11 |

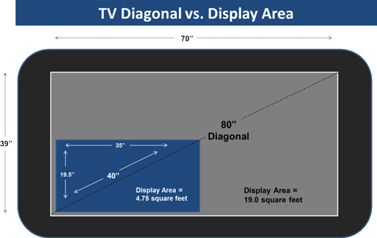

LCD TV demand has grown approximately 21% annually since 2008. According to the LCD TV Association, LCD TV unit sales grew from 105 million units in 2008 to an estimated 225 million units in 2012. The Association projects LCD TV shipments to increase to 273 million units in 2015. Although the annual rate of unit growth is slowing, there is a pronounced trend towards the consumption of larger screen sizes. Larger display panels consume substantially greater quantities of indium. The LCD TV Association stated in February 2012 that the percentage of sales of 40-inch+ LCD TVs has been increasing as consumers continue to adopt larger screen sizes. In 2015, 40-inch+ sizes are expected to account for 38% of total LCD TV panel demand, which was previously forecasted to reach only 34%. In October 2012, DisplaySearch reported that the average TV panel diagonal had increased from 34.8” in August 2011 to 36.8” in August 2012. Digitimes Research reported in November 2012 that they expect TV applications will see a significant increase in average panel area in 2013 amid growing demand for bigger screens. They expect the average TV panel size will be 38.8” in 2013, up from 36.6” in 2012, as shipments to the 29-inch, 39-inch and 50-inch and larger segments will all go up. From 2007 to 2011, the annual increase in average size was between 0.8" to 1.0". These larger increases are considered significant. The 2” average increase in LCD TV diagonals last year represents a 12% increase in the actual display size. This in turn equates to a 12% increase in indium consumed as a result of LCD TV manufacturing. The following example illustrates the exponential impact increased display diagonals (size) have on display area and, therefore, on indium consumption.

When a 40” TV is replaced by an 80” TV, the diagonal has doubled, but the total area of the TV screen has quadrupled.

According to DisplaySearch, there are several factors leading to increases in the average LCD TV panel size:

| · | The recent increase in the variety of new screen sizes has led many customers to choose the larger sizes, such as moving from 26” to 29”, from 37” to 39”, from 46” to 50”, and from 55" to 60”. |

| · | As consumers replace older LCD TVs, they tend to choose a larger size. Many consumers in North America originally had a 32” LCD TV in their bedroom and a 40-50” set in their living room, and are upgrading to a 39" or 40” set in their bedroom and a 50” or larger set for the living room. |

| · | LCD TV brands are promoting larger sizes in order to preserve profit margins. |

In the spring of 2012, DisplaySearch updated their global TV replacement study. They found that in the prior year, the TV replacement cycle had decreased on a global scale, from 8.4 to 6.9 years. The study found that the most critical driver of TV replacement in nearly all countries was a desire to trade up in size, followed by wanting to own a flat panel TV with improved picture quality. In general, mainstream LCD devices are trending toward larger panel sizes, which require more indium per unit. The desire to own the latest technology with the best picture quality is apparent in the sales of Apple’s new Retina Displays and the interest evident at the 2013 Consumer Electronics Show for Ultra HD 4K TVs. Demand for touch screens is also accelerating. Touch screens routinely use ITO in the touch subsystem as well as in the LCD front plane, requiring an extra layer of ITO. Apple’s iPhones and iPads are examples of capacitive touch screen technology utilizing ITO to offer higher clarity and quality of the display image. Nearly all of these display technologies rely on ITO as a transparent conductor, and NanoMarkets LLC, a leading provider of market and technology research and industry analysis services, expects the market for ITO to grow from $3.2 billion in 2009 to $10.9 billion in 2016.

| 12 |

LED Industry

The LED TV market has grown rapidly over the last few years, and is estimated to have reached nearly 150 million units in 2012, representing nearly 69% of the total TV market. The LED lighting market also continues to grow as declining prices drive increased market penetration.

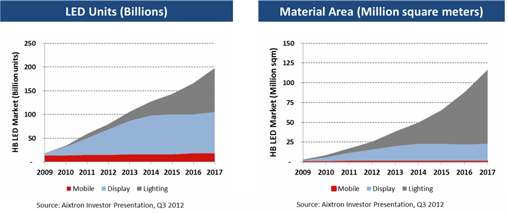

In a November 2012 investor presentation, Aixtron SE, a manufacturer of metal organic chemical vapor deposition ("MOCVD") equipment for the LED industry, reported that the number of LED units surpassed 50 million units in 2011 and is expected to surpass 100 million units in 2013 and should approach 200 million units in 2017; a fourfold increase in 6 years. More significantly, Aixtron reported that larger chip sizes are leading to substantially increased epitaxial area production, creating increased demand for raw materials, including indium. Specifically, Aixtron forecasts that the 8 year compound annual growth rate (“CAGR”) for material area growth in LED production from 2009 to 2017 will be 59%, rising to approximately 115 million square meters by 2017. Aixtron reported that the bulk of this growth is expected to come from the LED lighting market as LED lighting reaches the economic tipping point (the point at which it is more cost effective to purchase LED bulbs versus incandescent bulbs).

In September 2009, Bloomberg News reported that at a metals conference in Beijing, Feng Juncong, an analyst at Beijing Antaike Information Development Co., Ltd., the state-backed research group, stated that ‘‘Indium used in LED may exceed 100 mt by 2015.’’ We believe this would represent a very large new demand driver for indium and consume a substantial portion of the world’s primary indium supply, if this projection were to become a reality.

Solar Industry

Indium is increasingly being used as a crucial raw material in the solar energy industry, in the form of thin-film solar panels. According to the United States’ National Renewable Energy Laboratory, to produce 20 Gigawatts of solar power by the year 2050, the United States will need 400 mt of indium per year for the production of photovoltaic modules and systems alone.

Although investment in thin-film solar power slowed in 2012, GTM Research, in its June 2012 publication, “Thin Film 2012 – 2016: Technologies, Markets and Strategies for Survival,” forecasts global thin film production will rebound in 2015/2016, when the total market is expected to recover to $7.6 billion. In particular, the report forecasts strong growth in the CIGS technology segment, forecasting production at 4 GW in 2016. At current and projected efficiencies in CIGS production, 4 GW of production would consume between 100 mt and 200 mt of indium annually, representing a substantial increase in indium demand.

| 13 |

GTM Research further reported that in 2011, Solar Frontier established itself as a dominant supplier with roughly 400 MW of CIGS PV shipments, but companies such as MiaSole Inc., recently acquired by Hanergy of China, and Taiwan Semiconductor Manufacturing Company Ltd. of Taiwan could emerge in the next few years as top thin film suppliers with cost of manufacturing approaching $0.50 per watt. Nanosolar, Inc., another CIGS manufacturer, received $90 million in additional funding in 2012 to allow its CIGS thin-film photovoltaic factory to continue to scale and improve. With continued venture investments and increased interest from global industrial conglomerates, GTM Research predicts other major CIGS acquisitions in the near future.

Raw material costs typically account for the bulk share of thin film manufacturing costs. However, raw materials for the actual active photovoltaic layer of a thin-film module are typically quite small. GTM reports that for MiaSole Inc., the cost of the CIGS layer accounts for only $0.06/W, or 7% of production cost in 2011. They further report that even if indium prices doubled, CIGS module prices would only increase by $0.03/W, a 3.5% increase in the CIGS production. Therefore, as in the case of LCD, the cost of indium in CIGS production is a relatively small driver.

Government Stockpiling

The State Reserve Bureau of China (“SRB”) purchased 60 metric tons of indium from domestic producers in August of 2012 and another 20 metric tons in October 2012. This material was in addition to 30 metric tons purchased for a strategic stockpile in 2008. Most traders and producers believe that the SRB plans to continue stockpiling additional indium ingot in the future, although the exact tonnage is uncertain.

The European Commission’s 2012 stockpiling report stated that the South Korean government maintains a stockpile of 60 days of indium imports and that South Korea’s Public Procurement Service purchased 5 metric tons of indium in 2008.

The European Commission’s 2012 stockpiling report stated that Japan planned to stockpile 42 metric tons of indium plus 18 days of additional inventory. There are no official reports stating whether or not the Japanese government has purchased any indium as of December 31, 2012.

Substitutes and Alternatives to Indium

In a 2009 report titled, ‘‘Indium Tin Oxide and Alternative Transparent Conductor Markets,’’ NanoMarkets expects the market for ITO substitutes to grow from $30 million in 2009 to almost $940 million in 2016. Such alternatives include other transparent conductive oxides (TCOs), carbon nanotube-based formulations, other nanomaterials, composites and metals. NanoMarkets also expects the market for ITO to grow from $3.2 billion in 2009 to $10.9 billion in 2016. Based on these figures, ITO substitution is expected to grow from less than 1% of the total market in 2009 to approximately 8% of the total market in 2016. According to the USGS, indium’s recent price volatility and various supply concerns associated with the metal have accelerated the development of ITO substitutes. Antimony tin oxide (ATO) coatings, which are deposited by an ink-jetting process, have been developed as an alternative to ITO coatings in LCDs and have been successfully annealed to LCD glass. A potential drawback to using ATO is the fact that the metal antimony and many of its compounds are toxic. Materials such as carbon nanotubes and graphene have advantages over ITO such as relative lower cost, compatibility with flexible substrates and improved performance in certain applications. Carbon nanotube coatings, applied by wet-processing techniques, have been developed as an alternative to ITO coatings in flexible displays, solar cells and touch screens. ITO is considered brittle as are some other potential substitutes like aluminum-zinc-oxide. The resistive touch screen market and the flexible display market are most ripe for alternatives to ITO and other brittle TCOs that cannot stand up to repeated poking and flexing. Capacitive technology (used in screens for smartphones like Apple’s iPhone), on the other hand, offers high clarity and quality of the display image and since it does not work by poking with a stylus, the capacitive screen can more easily make use of ITO and other brittle TCOs. Graphene is another TCO developed as a substitute for ITO that works well in labs, especially for touch screens and flexible displays. Some labs actually manufacture graphene by growing it on an indium substrate. Poly (3, 4-ethylene dioxythiophene) (PEDOT) has also been developed as a substitute for ITO in flexible displays and organic light-emitting diodes (OLED). PEDOT can be applied in a variety of ways, including spin coating, dip coating and printing techniques. Researchers have recently developed a more adhesive zinc oxide nanopowder to replace ITO in LCDs. Although graphene, carbon nanotubes, PEDOTS and the other TCOs may be viable alternatives, there remain several unknowns. It is not known if manufacturers of special materials can successfully mass produce enough of these specialty materials to supply industry, how well these new materials will perform over the long-term in consumer based products and what the opportunity cost would be to the Flat Panel Display (FPD) Industry to transition from ITO to these other alternatives. The FPD manufacturers have already spent tens of billions of dollars building fabs designed to use ITO. Lastly, the cost per kilogram of some of these alternative materials may also be volatile. According to the USGS, indium phosphide can be substituted by gallium arsenide in solar cells and in many semiconductor applications. Hafnium can replace indium in nuclear reactor control rod alloys. Potential drawbacks using gallium and hafnium as replacements for indium is the fact that both these metals are also considered expensive, have highly volatile price histories and are both byproduct metals like indium. Gallium is a byproduct of aluminum production and hafnium is a byproduct of zirconium refinement. Total annual production of gallium is smaller than annual primary indium production. According to the USGS, world primary gallium production was estimated at 273 metric tons in 2012 and world primary hafnium production statistics are not available.

| 14 |

Government Regulation

General Description

There are no governmental regulations which will directly impact our intended operation of purchasing and lending indium. We intend to use standard industry commercial terms recognized by industry participants in connection with the storage and shipment of indium. A representative sample of such terms is listed below.

Purity. The recognized industry wide standard purity level is 99.99%.

Price. All purchases and sales of indium are individually negotiated. There is no fixed price ratio between 3N7, 4N or 5N material in the indium industry. Typically, in a regular indium market, balanced supply and demand, the higher the purity of the indium, the more it costs. 4N indium is slightly more expensive than 3N7. 5N is slightly more expensive than 4N. In a declining indium market, the price of 3N7 purity indium is often quoted at an even greater discount to indium with purities of 4N or 5N. In some cases, the prices may be as much as 2.0% to 5.0% lower. Typically, when the price of indium is appreciating, there is often no difference in the price of 3N7 purity indium compared to 4N or 5N purity metal.

Form. Indium Metal, 3N7 grade, Type 1 or Type 2, is received for storage in the form of ingots which have a uniform trapezoidal shape or uniform rectangular shape with square or rounded edges. The top and bottom surfaces are relatively flat and parallel.

Surface Characteristics. Indium is a silvery white metal with a bluish cast. Surfaces of the ingot are clean and free of dirt, grease, oil, cleaning residues, etc.

Dimensions. Nominal ingot dimensions are listed below for the two types of Indium.

| Weight | Length | Width | Height | |||||||||||

| Type 1 | 100 tr. oz (3.11 kg) | 8.50 in./ 215.9 mm | 3.25 in./ 82.5 mm | 1.25 in./ 31.75 mm | ||||||||||

| Type 2 | 10 kg | 340/345 mm (bottom/top) | 85/95 mm (bottom/top) | 45 mm | ||||||||||

Production Lot Size. Each ingot shall be traceable to the refining lot or melt from which it was produced.

Packaging

Ingots. Ingots in a production lot shall be individually wrapped in a new, clean, transparent polyethylene bag which has a minimum thickness of 0.004 inches (4 mm). Both ends of the bag shall be closed by heat sealing.

Boxes. Each box from the supplier shall contain either a maximum of twenty 100 tr. oz. ingots or six 10 kg ingots with a total net weight of approximately 63 kg (2,000 tr. oz.).

Marking

Ingot. Each ingot in a refining lot or melt shall be permanently marked or stamped with identification information.

Boxes. Sufficient aluminum tags shall be affixed to each box and shall be marked with identification information.

Storage

Indium ingots shall be stored indoors, in a vault or vault like area of a warehouse which has been equipped with fire prevention sprinklers. Storage identity shall be maintained by contract and production lot number as indicated on each box and in shipping instructions.

| 15 |

Security

Eight seals shall be affixed through holes bored in the top and bottom corners of the box to maintain the integrity of the box contents. Entry into vault areas for the purpose of shipments, inventory or qualitative maintenance inspections will be documented by use of logs and/or custodial reports.

Competition

Although we believe no other companies have our business model, we may have competition from miners, refiners, suppliers and traders of indium such as Huludao Zinc Industry Co. of China, Liuzhou China Tin Group, Jianxi Copper Co., Zhuzhou Smeltery Group Co., Ltd., Nanjing Foreign Economic & Trade Development Co., Ltd., Nanjing Sanyou Electronic Materials Co., Ltd., Huludao Nonferrous Metals (Group) I/E Co., Ltd., Nanjing Germanium Co., Ltd., Xiangten Zhengtan Nonferrous Metals Co., Ltd., Guangxi Intai Technology Co., Ltd., Hunan Jingshi Group, Laibin Debang Industry and Trade Co., Ltd., Shaoguan Huali Industrial Co., Ltd., Tianjin Indium Products Co. Ltd., Zhuzhou Keneng New Materials Co., Ltd., Teck Resources Limited, Xstrata Plc, Indium Corporation of America, Umicore Indium Products, Molycorp, Inc., Dowa Electronics Materials Co., Unionmet (Singapore) Limited, Aim Specialty Materials, Glencore International AG, Wogen PLC, RJH Trading Ltd., 5N Plus Inc., Hudson Metals Corporation, and Traxys North America LLC. We may also have competition from end users of indium. It is our belief that the top producers of FPD’s are the largest purchasers of indium. Major producers of FPDs listed in alphabetical order, are AU Optronics, Chi Mei Optoelectronics, Chunghwa Picture Tubes, HannStar Display Co., Innolux, LG Phillips LCD, Quanta Display Inc., Samsung Electronics, Sharp Corp., and Sony Corp. These companies are likely competing with us for purchasing indium from industry suppliers.

Employees

We have no full-time employees. Our chief executive officer, president and chief operating officer provide services to us through the Manager. Our chief financial officer is a part-time employee and our administrative assistant is a part-time independent contractor.

Corporate Information

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, Forms 3, 4 and 5 filed on behalf of directors and executive officers and any amendments to such reports filed pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, or the Exchange Act have been filed with the Securities and Exchange Commission, or SEC. Such reports and other information that we file with the SEC are available on our web site at http://www.smg-indium.com when such reports are available on the SEC website. Copies of this Annual Report on Form 10-K may also be obtained without charge electronically or by paper by contacting Alan Benjamin, SMG Indium Resources Ltd., by calling (212) 984-0635.

The public may also read and copy the materials we file with the SEC at its Public Reference Room at 100 F Street, N.E., Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains a web site at http://www.sec.gov that contains reports, proxy and information statements and other information regarding companies that file electronically with the SEC. The contents of these websites are not incorporated into this filing.

| 16 |

Item 1A. Risk Factors

Investing in our securities involves a high degree of risk. Before purchasing our units, common stock or warrants, you should carefully consider the following risk factors as well as other information contained in this Report, including our financial statements and the related notes. The risks and uncertainties described below are not the only ones facing us. Additional risks and uncertainties that we are unaware of, or that we currently deem immaterial, also may become important factors that affect us. If any of the following risks occur, our business, financial condition or results of operations could materially and adversely affected. In that case, the trading price of our securities could decline, and you may lose some or all of your investment.

Factors That May Affect Our Business and Results of Operations

We have an unproven business model and it is uncertain whether the purchase, lending or sale of indium will generate sufficient revenues for us to sustain operations.

Our model for conducting business is still new and unproven. We have no revenues and incur operating losses. Based on our business model of purchasing and stockpiling indium we do not expect to generate revenues to sustain operation. Our cash balance at December 31, 2012 was $6.2 million. We believe that we have sufficient funds to sustain our operations for at least three years even after considering the fact that we may use up to $1.0 million to repurchase shares of our common stock. After such time, our ability to support ongoing annual cash operating expenses may depend upon our ability to either raise capital or our ability to generate revenue streams from purchasing, lending, leasing and selling indium. However, it is uncertain whether we will be able to raise additional capital or that the purchase, lending, leasing and sale of indium can generate sufficient revenues for us to survive. Accordingly, we are not certain that our business model will be viable.

We address a new market which may not develop as we predict or in a way that will justify our purchase of indium.

There is no public market for the sale of indium. Since indium is primarily a byproduct of zinc mining, the supply does not necessarily vary directly with market price. Currently, increases in primary indium production have been correlated to increases in zinc production. We may not, and our Manager may not, be able to acquire indium, or once acquired, lend or sell indium for a number of years. The pool of potential purchasers and sellers is limited and each transaction may require the negotiation of specific provisions. In addition, the supply of indium is limited. World refinery production of indium was estimated by the U.S. Geological Survey or USGS to have increased from 662 mt in 2011 to 670 mt in 2012. The total size of the primary indium market was approximately $354 million in 2012 based on the USGS’s estimated production figure and Metal Bulletin’s average price for indium of $527.63 per kilogram in 2012 as posted on Bloomberg L.P. The inability to purchase or sell on a timely basis in sufficient quantities could have a material adverse effect on the share price of our common stock.

Information regarding the indium industry’s largest producers and users, including data regarding exclusive long-term purchase or supply agreements, is limited and not readily available. Such inability to access this information places us at a potential competitive disadvantage, which may adversely affect our ability to purchase and stockpile indium.

Indium industry producers and users do not publicly disclose sufficient information to determine with certainty the largest producers and users of indium. In addition, company-specific indium usage is not information that is typically publicly disclosed by industry participants. This makes it difficult for investors to assess indium industry dynamics, our competition, and various other risks we face.

Industry producers, recyclers, secondary fabs, and end users do not reveal industry data quantifying the amount of indium purchased or sold under long-term exclusive supply contracts. As a result, we may not be able to determine if certain suppliers have long-term supply contracts with other parties, which may adversely affect our ability to obtain indium from such supplier. The lack of industry information could hinder our ability to purchase and stockpile or sell indium. In addition, we are not aware of any additional information, if any, regarding the indium market or the type of market information other industry producers, purchasers, suppliers and other market participants may possess. Our inability to access this information, if any, places us at a potential relative competitive disadvantage to other market participants who may have access to such information. This may adversely affect our ability to purchase and stockpile indium.

| 17 |

Investors may face difficulty accessing the quoted price for indium on a daily basis, which may negatively impact an investor’s ability to assess the value of their investment.

Indium’s market price is infrequently quoted and investors may have to pay for subscriptions to various data service providers to access such information. Metal Bulletin PLC, as posted on Bloomberg L.P., publishes the spot price of indium on a bi-weekly basis. We post on our website Metal Bulletin’s published spot price of indium on a bi-weekly basis as well. Therefore, stockholders will not be able to access an updated spot price on a daily basis. Accordingly, investors in our common stock may not be able to readily access information regarding the current market price for indium prior to making an investment decision.

The lack of a recognized indium commodity exchange may negatively impact an investor's ability to assess the value of their investment.

Indium is not traded on any recognized commodity exchange. As such, direct hedging of the prices for future purchases cannot be undertaken. We do not currently have any long-term supply contracts with indium suppliers, so prices will vary with each transaction and the individual bids and offers received. Prices will vary based on the supply and demand for indium. There are no recognized futures or forwards market for indium. The pool of potential purchasers and sellers of indium is limited and each transaction may require the negotiation of specific provisions. Accordingly, a purchase or sale cycle may take several months to complete. In addition, the supply of indium is limited and we may experience additional difficulties purchasing indium in the event we are a significant buyer. The lack of a standardized indium exchange affects our ability to purchase and sell indium on a timely basis and could have a material adverse effect on the price of our securities.

In late April 2011, Metal-Pages.com, a subscription based metals information service provider, reported that the Kunming Fanya Non-ferrous Metals Exchange opened in China. Metal-Pages.com indicated that the exchange began trading silver and indium in standard lots of 100 grams. Based on indium closing price of $695 per kilogram on March 30, 2011, the Fanya Exchange's standard lot size of 100 grams is the equivalent of $69.50. Our average indium purchase order typically ranges from 500 kilograms to 2000 kilograms. This is approximately 5,000 to 20,000 times larger than the 100 gram standard lot size for indium on the Fanya Exchange. In mid-May 2011, Metal-Pages.com reported that physical delivery has not progressed smoothly on the Fanya Exchange. We have not been able to verify the veracity of these statements or if the Fanya Exchange is indeed a legitimate exchange and there is very little information available with regards to the Kunming Fanya Non-ferrous Metals Exchange. Based on the limited information available, it does not appear that the Fanya Exchange is large enough to satisfy the needs of regular indium industry market participants which may negatively impact an investor’s ability to assess the value of their investment.

We expect to rely on a limited number of potential suppliers and purchasers of indium, which could affect our ability to buy and sell indium in a timely manner and negatively influence market prices.

The indium market is illiquid and considered small compared to the markets for base metals. There are a limited number of suppliers and purchasers of indium. If new companies are formed to purchase and stockpile indium, this would adversely affect our ability to procure or sell sufficient quantities of indium on a timely basis or even at all.

Relying on a limited number of potential suppliers of indium and potential customers who purchase indium could (1) make it difficult to buy and sell indium in a timely manner, (2) negatively influence market prices by potentially having to sell indium to cover our operating expenses, or (3) drive up market prices if we are a large purchaser of indium and there is an indium shortage. As of December 31, 2012, we have purchased an aggregate of 47.0 mt of indium using seven regular indium suppliers at an average price of $609 per kilogram. Except for purchasing from these suppliers, we have had limited discussion with other potential suppliers of indium and no other contracts or negotiations have been entered into with any other suppliers or purchasers of indium, and we cannot be certain that we will be able to purchase inventory in a timely manner or at favorable prices to purchase indium.

One of our principal stockholders controls a substantial interest in us and thus may influence certain actions requiring a stockholder vote.

William C. Martin, a member of our board of directors and, through an entity he controls, a member of our Manger, beneficially owns approximately 45.0% of our outstanding common stock with voting rights through a wholly owned entity Raging Capital Master Fund, Ltd. (formerly Raging Capital Fund L.P and Raging Capital Fund (QP), L.P) and his Individual Retirement Account. This percentage ownership does not take into consideration the potential exercise of any stock options and warrants controlled by William C. Martin either individually or through his affiliates. Mr. Martin is able to influence the outcome of all matters requiring stockholder approval, including the election of directors, amendment of our certificate of incorporation and approval of significant corporate transactions, and he will have significant influence over our management and policies. The interests of Mr. Martin and our stockholders’ interests may not always align and taking actions which require stockholder approval, such as selling the company, may be more difficult to accomplish. Furthermore, in the event that Mr. Martin elects to sell a significant portion of his interest in the Company, such sale may materially affect the Company and our stock price would decrease.

| 18 |

The substitution of other materials for indium may decrease demand for indium and adversely affect the price of indium and, thus, our stock price.

Indium has substitutes in many, perhaps most, of its uses. Silicon has largely replaced indium in transistors. Gallium can be used in some applications as a substitute for indium in several alloys. In glass-coating applications, silver-zinc oxides or tin-oxides can be used. Zinc-tin oxides can be used in LCDs’. Other possible substitutes for indium glass coating are transparent carbon nanotubes and graphene. Indium phosphide can be substituted by gallium arsenide in solar cells and in many semiconductor applications. Hafnium can replace indium alloys in nuclear reactor control rods. The substitutions of such materials for indium may decrease the overall demand for indium, thereby lowering the price of indium and our common stock.

Our operating results are subject to fluctuation in the price of indium, which is subject to macroeconomic conditions that are largely outside of our control.

Our activities almost entirely will involve purchasing and stockpiling the metal indium. Therefore, the principal factors affecting the price of our securities are factors which affect the price of indium and are thus beyond our control. The value of our securities will depend upon, and typically fluctuate with, fluctuations in the price of indium. The market prices of indium are affected by rates of reclaiming and recycling of indium, rates of production of indium from mining, demand from end users of indium and indium-tin-oxide, and may be affected by a variety of unpredictable international economic, monetary and political considerations.

Macroeconomic considerations that may affect the price of indium include expectations of future rates of inflation, the strength of, and confidence in, the U.S. dollar, the currency in which the price of indium is generally quoted, and other currencies, interest rates and global or regional economic events. In addition to changes in production costs, shifts in political and economic conditions affecting indium producing countries may have a direct impact on their sales of indium. The fluctuation of the prices of indium is illustrated by the following table, which sets forth, for the periods indicated, the highs and lows of the spot price for indium:

| Spot Indium Prices(1) 99.99% Purity (U.S.$/KG) | ||||||||||||||||||||||||||||||||||||

| 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | ||||||||||||||||||||||||||||

| High | 910 | 1070 | 1025 | 750 | 730 | 530 | 650 | 870 | 600 | |||||||||||||||||||||||||||