Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - EveryWare Global, Inc. | Financial_Report.xls |

| EX-31.2 - EX-31.2 - EveryWare Global, Inc. | v336123_ex31-2.htm |

| EX-32.1 - EX-32.1 - EveryWare Global, Inc. | v336123_ex32-1.htm |

| EX-31.1 - EX-31.1 - EveryWare Global, Inc. | v336123_ex31-1.htm |

| EX-32.2 - EX-32.2 - EveryWare Global, Inc. | v336123_ex32-2.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| (Mark One) | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2012 |

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from ____________ to ____________ |

Commission File Number: 001-35437

ROI ACQUISITION CORP.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 45-3414553 |

| (State or Other Jurisdiction of Incorporation or Organization | (I.R.S. Employer Identification No.) |

601 Lexington Avenue, 51st Fl. New York, NY (Address of Principal Executive

Offices) |

10022 (Zip Code) |

(212) 825-0400

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act: None.

Securities registered pursuant to Section 12(g) of the Act:

Units consisting of one share of Common Stock and one Warrant

Common Stock included in the Units, par value $0.0001 per share

Warrants included in the Units, exercisable for Common Stock at an exercise price of $12.00 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large Accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer x | Smaller reporting company ¨ |

| Do not check if a smaller reporting company |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes x No ¨

The aggregate market value of the common stock held by non-affiliates of the registrant, computed as of June 30, 2012 (the last business day of the registrant’s most recently completed second fiscal quarter), was approximately $71,925,000.

As of March 13, 2013, there were 9,385,000 shares of the registrant’s common stock issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

TABLE OF CONTENTS

| Page | |

| FORWARD-LOOKING STATEMENTS | 1 |

| PART I | 2 |

| ITEM 1. DESCRIPTION OF BUSINESS | 2 |

| ITEM 1A. RISK FACTORS | 5 |

| ITEM 1B. UNRESOLVED STAFF COMMENTS | 22 |

| ITEM 2 PROPERTIES | 23 |

| ITEM 3 LEGAL PROCEEDINGS | 23 |

| ITEM 4 MINE SAFETY DISCLOSURES | 23 |

| PART II | 24 |

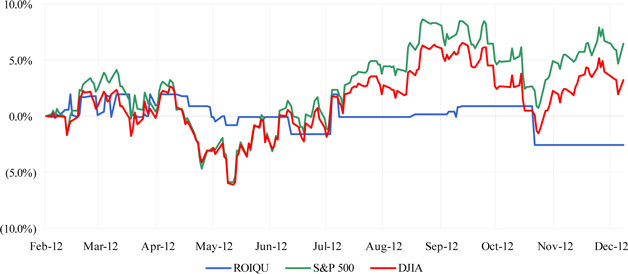

| ITEM 5 MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | 24 |

| ITEM 6 SELECTED FINANCIAL DATA | 26 |

| ITEM 7 MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 26 |

| ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 29 |

| ITEM 8 FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | 30 |

| ITEM 9 CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 30 |

| ITEM 9A. CONTROLS AND PROCEDURES | 30 |

| ITEM 9B OTHER INFORMATION | 30 |

| PART III | 31 |

| ITEM 10 DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE | 31 |

| ITEM 11 EXECUTIVE COMPENSATION | 34 |

| ITEM 12 SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | 34 |

| ITEM 13 CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE | 36 |

| ITEM 14 PRINCIPAL ACCOUNTING FEES AND SERVICES | 38 |

| PART IV | 39 |

| ITEM 15 EXHIBITS, FINANCIAL STATEMENT SCHEDULES | 39 |

| Signatures | S-1 |

| - i - |

| Index to Financial Statements | F-1 |

| Exhibit 31.1 | |

| Exhibit 31.2 | |

| Exhibit 32.1 | |

| Exhibit 32.2 |

| - ii - |

FORWARD-LOOKING STATEMENTS

The statements contained in this report that are not purely historical are forward-looking statements. Our forward-looking statements include, but are not limited to, statements regarding our or our management’s expectations, hopes, beliefs, intentions or strategies regarding the future. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this report may include, for example, statements about:

| · | our ability to complete our initial business combination; |

| · | our success in retaining or recruiting, or changes required in, our officers, key employees or directors following our initial business combination; |

| · | our officers and directors allocating their time to other businesses and potentially having conflicts of interest with our business or in approving our initial business combination; |

| · | our potential ability to obtain additional financing to complete our initial business combination; |

| · | our pool of prospective target businesses; |

| · | the ability of our officers and directors to generate a number of potential investment opportunities; |

| · | our public securities’ liquidity and trading; |

| · | the use of proceeds not held in the trust account or available to us from interest income on the trust account balance; or |

| · | our financial performance. |

The forward-looking statements contained in this report are based on our current expectations and beliefs concerning future developments and their potential effects on us. There can be no assurance that future developments affecting us will be those that we have anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described under the heading “Risk Factors” beginning on page 5. Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

| - 1 - |

PART I

References to “ROI”, the “Company,” “us” or “we” refer to ROI Acquisition Corp.

| ITEM 1. | DESCRIPTION OF BUSINESS |

General

We are a blank check company formed on September 19, 2011 for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses (“Business Combination”). On October 6, 2011, ROIC Acquisition Holdings LP (the “Sponsor”) purchased 2,156,250 shares of our common stock (“Founder Shares”) for an aggregate amount of $25,000, or approximately $0.01 per share.

The registration statement for our initial public offering (“Public Offering”) was declared effective on February 24, 2012. We consummated the Public Offering on February 29, 2012 and received net proceeds of approximately $75,000,000 which includes $3,225,000 received for the purchase of 4,166,667 warrants (the “Sponsor Warrants”) by the Sponsor and 10,000 units by our Chairman. On April 9, 2012, an aggregate of 281,250 Founder Shares were forfeited by the Sponsor since the over-allotment option was not exercised by the underwriters in the Public Offering.

On July 26, 2012, the Sponsor transferred 1,875,000 Founder Shares to its affiliate, Clinton Magnolia Master Fund, Ltd. (“Magnolia”) at a price of $0.0115942 per share and transferred 4,166,667 warrants to Magnolia at a price of $0.733962 per warrant. In connection with such transfers, Magnolia assumed all rights and obligations of the Sponsor with regard to the Founder Shares and Sponsor Warrants.

At December 31, 2012, we had not commenced any operations. All activity through December 31, 2012 relates to our formation and Public Offering. Our fiscal year-end is December 31.

Our management had broad discretion with respect to the specific application of the net proceeds of the Public Offering, although substantially all of the net proceeds of the Public Offering were intended to be generally applied toward effecting a Business Combination. Our efforts in identifying prospective target businesses was not limited to a particular industry or geographic region for purposes of consummating our initial Business Combination. While we may have pursued an acquisition opportunity in any business industry or sector, we intended to focus on industries or sectors that complemented our management team’s background, such as the consumer sector, and in particular the restaurant industry in the United States and globally.

Effecting our initial business combination

On January 31, 2013, we entered into a Business Combination Agreement and Plan of Merger (the “Merger Agreement”) by and between the Company, ROI Merger Sub Corp. (“Merger Sub Corp.”), ROI Merger Sub LLC (“Merger Sub LLC”), and EveryWare Global, Inc. (“EveryWare”), providing for the merger of Merger Sub Corp. with and into EveryWare, with EveryWare surviving the merger as our wholly-owned subsidiary of the Company, immediately followed by the merger of EveryWare with and into Merger Sub LLC, with Merger Sub LLC surviving the merger as a wholly-owned subsidiary of the Company.

The Merger Agreement provides for the merger of Merger Sub Corp. with and into EveryWare (the “Initial Merger”), with EveryWare continuing as the surviving corporation (the “Surviving Corporation”), immediately followed by the merger of the Surviving Corporation with and into Merger Sub LLC, with Merger Sub LLC continuing as the surviving company, and pursuant to which each share of outstanding capital stock, $0.001 par value per share, of EveryWare will be exchanged for cash and shares of our common stock, $0.0001 par value per share, as further described in, and subject to the terms of, the Merger Agreement.

Pursuant to the Merger Agreement, upon the effectiveness of the Initial Merger, each share of capital stock of EveryWare will be exchanged for cash and validly issued shares of our common stock (the “Shares”). The aggregate consideration will consist of (i) between $90 million and $107.5 million in cash, subject to adjustment in accordance with the terms of the Merger Agreement if the aggregate amount of cash available after redemption of shares of our common stock, in accordance with our Second Amended and Restated Certificate of Incorporation, from the trust account (the “Trust Account”) maintained for the benefit of the Company’s public stockholders (“Public Stockholders”) and receipt to be of proceeds from EveryWare’s refinancing of its existing indebtedness is less than $107.5 million, (ii) 10,440,000 shares of our common stock, subject to adjustment in accordance with the terms of the Merger Agreement if the aggregate amount of cash available after redemption of shares of our common stock, in accordance with our Second Amended and Restated Certificate of Incorporation from the Trust Account and receipt of proceeds from EveryWare’s refinancing of its existing indebtedness is less than $107.5 million (it is expected that the Shares issued to EveryWare’s existing stockholders will represent between 69.4% and 59.4% of the outstanding common stock of the post-merger company and that our existing stockholders will retain an ownership interest of between 23.1% and 33.0% of the post-merger company (depending on the level of redemptions by our existing stockholders and the aggregate proceeds from the proposed debt refinancing and disregarding warrants to purchase our common stock, which will remain outstanding following the Business Combination)) and (iii) an additional 3,500,000 shares of our common stock (the “Earnout Shares”), which Earnout Shares are subject to forfeiture in the event that the trading price of our common stock does not exceed certain price targets subsequent to the closing of the Business Combination, unless the Company consummates a change of control transaction under certain circumstances.

| - 2 - |

The Shares will be subject to certain restrictions on transfer for a period of time following the closing of the Business Combination.

The consummation of the transactions contemplated by the Merger Agreement is subject to a number of conditions set forth in the Merger Agreement including, among others, receipt of the requisite approval of the stockholders of the Company.

Redemption rights for holders of Public Shares

upon consummation of the Business Combination

We will provide our stockholders with the opportunity to redeem their public shares (“Public Shares”) for cash equal to their pro rata share of the aggregate amount then on deposit in the Trust Account, less franchise and income taxes payable, upon the consummation of the Business Combination, subject to the limitations described herein. There will be no redemption rights with respect to outstanding warrants or private placement units.

In connection with seeking stockholder approval, we will consummate the Business Combination only if a majority of the outstanding shares of common stock vote in favor of the Business Combination. In such case, Magnolia has agreed to vote its Founder Shares as well as any Public Shares purchased during or after the Public Offering in favor of the Business Combination. In addition, Magnolia has agreed to waive its redemption rights with respect to its Founder Shares and any Public Shares it may hold in connection with the consummation of the Business Combination. Our officers and directors have also agreed to waive their redemption rights with respect to any Public Shares in connection with the consummation of the Business Combination.

If we do not effect a Business Combination by November 29, 2013, 21 months from the closing of the Public Offering, we will liquidate the Trust Account and distribute the amount then held in the Trust Account, including interest but net of franchise and income taxes payable and less up to $50,000 of such net interest that may be released to us from the Trust Account to pay liquidation expenses, to our Public Stockholders, subject in each case to our obligations under Delaware law to provide for claims of creditors and the requirements of other applicable law.

Net proceeds of approximately $75.1 million from the Public Offering and simultaneous private placement of the Sponsor Warrants (as described below) are held in the Trust Account. Except for the interest income earned on the Trust Account balance that may be released to us to pay any income and franchise taxes and to fund our working capital requirements, and any amounts necessary to purchase up to 15% of our shares issued as part of the Units described below in connection with seeking stockholder approval for our initial Business Combination, none of the funds held in the Trust Account will be released until the earlier of the completion of our initial Business Combination and the redemption of 100% of our Public Shares if we are unable to consummate a Business Combination by November 29, 2013, 21 months from the closing of the Public Offering (subject to the requirements of law). The proceeds deposited in the Trust Account could become subject to the claims of our creditors, if any, which could have priority over the claims of our Public Stockholders.

Limitation on redemption rights upon consummation of a business combination if we seek a stockholder vote

Notwithstanding the foregoing, in connection with holding a stockholder vote to approve our initial Business Combination, our Second Amended and Restated Certificate of Incorporation provides that a Public Stockholder, together with any affiliate of such stockholder or any other person with whom such stockholder is acting in concert or as a “group” (as defined under Section 13 of the Exchange Act), will be restricted from seeking redemption rights with respect to more than an aggregate of 10% of the shares sold in our Public Offering. We believe this restriction will discourage stockholders from accumulating large blocks of shares, and subsequent attempts by such holders to use their ability to exercise their redemption rights as a means to force us or our management to purchase their shares at a significant premium to the then-current market price or on other undesirable terms. Absent this provision, a Public Stockholder holding more than an aggregate of 10% of the shares sold in our Public Offering could threaten to exercise its redemption rights if such holder’s shares are not purchased by us or our management at a premium to the then-current market price or on other undesirable terms. By limiting a stockholder’s ability to redeem more than 10% of the shares sold in our Public Offering, we believe we will limit the ability of a small group of stockholders to unreasonably attempt to block our ability to consummate the Business Combination. However, our Second Amended and Restated Certificate of Incorporation does not restrict our Public Stockholders’ ability to vote all of their shares for or against a Business Combination.

Redemption of common stock and liquidation if no Business Combination

Magnolia and our officers and directors have agreed that we will have only until November 29, 2013, which is the date that is 21 months after the closing of our Public Offering, to consummate our initial Business Combination. If we are unable to consummate the Business Combination within such time frame, we will:

| - 3 - |

| · | cease all operations except for the purpose of winding up; |

| · | as promptly as reasonably possible but not more than ten business days thereafter, redeem 100% of the Public Shares, at a per-share price, payable in cash, equal to the aggregate amount then on deposit in the Trust Account, including interest but net of franchise and income taxes payable and less up to $100,000 of such net interest that may be released to us from the Trust Account to pay dissolution expenses, divided by the number of then outstanding Public Shares, which redemption will completely extinguish Public Stockholders’ rights as stockholders (including the right to receive further liquidation distributions, if any), subject to applicable law, and subject to the requirement that any refund of income taxes that were paid from the Trust Account which is received after such redemption shall be distributed to the former Public Stockholders; and |

| · | as promptly as reasonably possible following such redemption, subject to the approval of our remaining stockholders and our board of directors, dissolve and liquidate; |

subject in each case to our obligations under Delaware law to provide for claims of creditors and the requirements of other applicable law.

Pursuant to the terms of our Second Amended and Restated Certificate of Incorporation, our powers following the expiration of the permitted time period for consummating the Business Combination will automatically thereafter be limited to acts and activities relating to dissolving and winding up our affairs.

Employees

We currently have five executive officers. These individuals are not obligated to devote any specific number of hours to our matters but they intend to devote as much of their time as they deem necessary to our affairs until we have completed the Business Combination.

Available Information

We are required to file Annual Reports on Form 10-K and Quarterly Reports on Form 10-Q with the Securities and Exchange Commission (“SEC”) on a regular basis, and are required to disclose certain material events (e.g., changes in corporate control, acquisitions or dispositions of a significant amount of assets other than in the ordinary course of business and bankruptcy) in a current report on Form 8-K. The public may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains an Internet website that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC. The SEC’s Internet website is located at http://www.sec.gov.

| - 4 - |

| ITEM 1A. | RISK FACTORS |

In addition to the other information included in this report, the following risk factors should be considered in evaluating our business and future prospects. The risk factors described below are not necessarily exhaustive and you are encouraged to perform your own investigation with respect to the Company and our business. You should also read the other information included in this report, including our financial statements and the related notes.

Risks Related to the Company and the Business Combination

We may not be able to timely and effectively implement controls and procedures required by Section 404 of the Sarbanes-Oxley Act of 2002 that will be applicable to us after the Business Combination.

EveryWare is not currently subject to Section 404 of the Sarbanes-Oxley Act of 2002. However, following the Business Combination, we will be subject to Section 404. The standards required for a public company under Section 404 of the Sarbanes-Oxley Act of 2002 are significantly more stringent than those required of EveryWare as a privately-held company. Management may not be able to effectively and timely implement controls and procedures that adequately respond to the increased regulatory compliance and reporting requirements that will be applicable to the Company after the Business Combination. If we are not able to implement the additional requirements of Section 404 in a timely manner or with adequate compliance, we may not be able to assess whether our internal controls over financial reporting are effective, which may subject us to adverse regulatory consequences and could harm investor confidence and the market price of our common stock.

Our working capital will be reduced if our stockholders exercise their redemption rights in connection with the Business Combination, which may adversely affect our business and future operations.

Pursuant to our second amended and restated certificate of incorporation, holders of public shares may demand that we redeem their shares for a pro rata share of the cash held in the Trust Account, less franchise taxes and income tax payable, calculated as of two business days prior to the closing.

If the Business Combination is consummated, the funds held in the Trust Account will be released to pay (i) a portion of the cash consideration pursuant to the Merger Agreement, (ii) our stockholders who properly exercise their redemption rights, (iii) up to $2.25 million in deferred underwriting compensation to the underwriters of our Public Offering and other designated persons and certain additional fees for advisory services, (iv) all fees, costs and expenses (including regulatory fees, legal fees, accounting fees, printer fees, and other professional fees) that were incurred by the Company, Merger Sub Corp., Merger Sub LLC or EveryWare in connection with the transactions contemplated by the Business Combination and (v) unpaid franchise and income taxes of the Company.

Our working capital will be reduced if we purchase shares from Public Stockholders who indicate an intention to vote against the Business Combination.

In connection with the stockholder vote to approve the proposed Business Combination, we may privately negotiate transactions to purchase shares after the closing of the Business Combination from stockholders who would have otherwise elected to have their shares redeemed for a per-share pro rata portion of the Trust Account. Magnolia, our directors, officers, or advisors or their respective affiliates may also purchase shares in privately negotiated transactions from Public Stockholders who indicate an intention to vote against the Business Combination. Such a purchase would include a contractual acknowledgement that such stockholder, although still the record holder of our shares is no longer the beneficial owner thereof and therefore agrees not to exercise its redemption rights or vote against the Business Combination. In the event that we, Magnolia, our directors, officers or advisors or our or their affiliates purchase shares in privately negotiated transactions from Public Stockholders who have already elected to exercise their redemption rights or vote against Business Combination, such selling stockholders would be required to revoke their prior elections to redeem their shares. Any such privately negotiated purchases may be effected at purchase prices that are in excess of the per-share pro rata portion of the Trust Account. In the event that we are the buyer in such privately negotiated purchases, we could elect to use Trust Account proceeds to pay the purchase price in such transactions after the closing of the Business Combination, which would have the effect of reducing the working capital available to the Company after the Business Combination.

Although permitted under our second amended and restated certificate of incorporation, we will not, prior to consummation of the Business Combination, release amounts from the Trust Account to purchase in the open market shares of common stock sold in our Public Offering. Further, although permitted pursuant to a securities purchase option agreement entered into prior to our Public Offering, Magnolia will not purchase up to 1,500,000 units from the Company in a private placement at $10.00 per unit.

| - 5 - |

Subsequent to the consummation of the Business Combination, we may be required to take writedowns or write-offs, restructuring and impairment or other charges that could have a significant negative effect on our financial condition, results of operations and stock price, which could cause you to lose some or all of your investment.

Although we have conducted due diligence on EveryWare, we cannot assure you that this diligence revealed all material issues that may be present in EveryWare’s business, that it would be possible to uncover all material issues through a customary amount of due diligence, or that factors outside of our and EveryWare’s control will not later arise. As a result, we may be forced to later writedown or write-off assets, restructure its operations, or incur impairment or other charges that could result in losses. Even if our due diligence successfully identifies certain risks, unexpected risks may arise and previously known risks may materialize in a manner not consistent with our preliminary risk analysis. Even though these charges may be non-cash items and not have an immediate impact on our liquidity, the fact that we report charges of this nature could contribute to negative market perceptions about the Company or its securities. In addition, charges of this nature may cause us to be unable to obtain future financing on favorable terms or at all.

Concentration of ownership after the Business Combination may have the effect of delaying or preventing a change in control.

It is anticipated that, upon completion of the Business Combination, Monomoy Capital Partners, L.P., MCP Supplemental Fund, L.P., Monomoy Executive Co-Investment Fund, L.P., Monomoy Capital Partners II, L.P. and MCP Supplemental Fund II, L.P. (collectively the “MCP Funds”) will own between approximately 57.7% and 85.6% of the post-merger company. These percentages are calculated based on a number of assumptions and are subject to adjustment in accordance with the terms of the Merger Agreement. These relative percentages assume that the Company receives $250.0 million in cash proceeds from the proposed issuance of senior secured notes in order to fund the $107.5 million in cash, subject to adjustment in accordance with the terms of the Merger Agreement (the “Cash Merger Consideration”) and refinance EveryWare’s existing debt and are based upon net debt of EveryWare at December 31, 2012. If the actual facts are different from these assumptions, the percentage ownership retained by ROI’s existing stockholders will be different. These percentages also do not take into account (i) the additional 3,500,000 shares of the Company’s common stock to be issued to EveryWare stockholders in connection with the closing of the Business Combination, which will be subject to forfeiture in the event that the trading price of the Company’s common stock does not exceed certain price targets subsequent to the closing of the Business Combination (the “Earnout Shares”) and 551,471 shares of outstanding Company common stock currently held by Magnolia, that could in each case be subject to forfeiture in the future if certain performance conditions relating to our trading price are not met following the Business Combination, (ii) options to purchase shares of ROI common stock that will be issued to former holders of EveryWare stock options in connection with the Business Combination and (iii) warrants to purchase ROI’s common stock that will remain outstanding following the Business Combination. As a result, the MCP Funds will have the ability to determine the outcome of corporate actions of the Company requiring stockholder approval. This concentration of ownership may have the effect of delaying or preventing a change in control and might adversely affect the market price of our common stock.

Future sales of our common stock may cause the market price of our securities to drop significantly, even if our business is doing well.

Upon the closing of the Business Combination, we will enter into an amended and restated registration rights agreement with respect to the Founder Shares and shares purchased by Thomas J. Baldwin, our Chairman of the Board and Chief Executive Officer in a private placement, shares of our common stock underlying the Sponsor Warrants, the shares of our common stock that we will issue under the Merger Agreement, any shares of issued or issuable upon the exercise of any equity security of the Company that is issuable upon conversion of any working capital loans in an amount up to $500,000 made to the Company and all shares issued to a holder with respect to the securities referred to above by way of any stock split, stock dividend, recapitalization, combination of shares, acquisition, consolidation, reorganization, share exchange, share reconstruction, amalgamation, contractual control arrangement or similar event, which securities we collectively refer to as “registrable securities.” This registration rights agreement amends and restates entirely the registration rights agreement we entered into in connection with our Public Offering. Under this agreement, we have agreed that the holders of a majority of the registrable securities are entitled to three long form registrations and unlimited short form registrations, known as demand registrations, whereby we are required to file a shelf registration statement with the SEC as soon as practicable after receipt of such demand registration. The holders of a majority of the registrable securities will be entitled to unlimited takedowns of the shelf, provided the shelf remains effective. However, the Company shall not be obligated to effect any demand registration within six months after the effective date of a previous demand registration. Holders of registrable securities will also have certain “piggyback” registration rights with respect to registration statements filed subsequent to the Business Combination.

Upon effectiveness of the registration statement we file pursuant to the registration rights agreement, or upon the expiration of the lockup periods applicable to the common stock that we will issue to EveryWare equity holders, these parties may sell large amounts of our stock in the open market or in privately negotiated transactions, which could have the effect of increasing the volatility in our stock price or putting significant downward pressure on the price of our stock.

| - 6 - |

Although we expect our common stock will be listed on NASDAQ after the closing, there can be no assurance that our common stock will be so listed or, if listed, that we will be able to comply with the continued listing standards of NASDAQ.

Our common stock, units and warrants are currently listed on NASDAQ. In connection with the closing of the Business Combination, we have applied to continue to list our common stock on NASDAQ after the closing under the symbol “EVRY.” As part of the application process, we are required to provide evidence that we are able to meet the continuing listing requirements of NASDAQ, including the requirement that our common stock is held by a minimum of 300 holders. If we are unable to list our common stock on NASDAQ or if, after the Business Combination, NASDAQ delists our common stock from trading on its exchange for failure to meet the listing standards, we and our stockholders could face significant material adverse consequences including:

| • | a limited availability of market quotations for our securities; |

| • | a determination that our common stock is a “penny stock” which will require brokers trading in our common stock to adhere to more stringent rules, possibly resulting in a reduced level of trading activity in the secondary trading market for our common stock; |

| • | a limited amount of analyst coverage; and |

| • | a decreased ability to issue additional securities or obtain additional financing in the future. |

ROI may apply the net proceeds released from the Trust Account together with the proceeds of the proposed acquisition financing in a manner that does not improve our results of operations or increase the value of your investment.

If the Business Combination is consummated, the funds held in the Trust Account will be released to pay (i) a portion of the cash consideration pursuant to the Merger Agreement, (ii) ROI stockholders who properly exercise their redemption rights, (iii) up to $2.25 million in deferred underwriting compensation to the underwriters of our Public Offering and other designated persons and certain additional fees for advisory services, (iv) all fees, costs and expenses (including regulatory fees, legal fees, accounting fees, printer fees, and other professional fees) that were incurred by the Company, Merger Sub Corp., Merger Sub LLC or EveryWare in connection with the transactions contemplated by the Business Combination and (v) unpaid franchise and income taxes of the Company.

Other than these uses, we do not have specific plans for any funds remaining from the proposed acquisition financing and the Trust Account and will have broad discretion regarding how we use such funds. These funds could be used in a manner with which you may not agree or applied in ways that do not improve the Company’s results of operations or increase the value of your investment.

If the Business Combination’s benefits do not meet the expectations of investors or securities analysts, the market price of our securities may decline.

If the benefits of the Business Combination do not meet the expectations of investors or securities analysts, the market price of the Company’s securities prior to the closing of the Business Combination may decline. The market values of our securities at the time of the Business Combination may vary significantly from their prices on the date the Merger Agreement was executed, the date of the Company’s proxy statement, or the date on which our stockholders vote on the Business Combination. Because the share exchange ratio in the Merger Agreement will not be adjusted to reflect any changes in the market price of our common stock, the market value of the Company common stock issued in the Business Combination may be higher or lower than the values of these shares on earlier dates.

In addition, following the Business Combination, fluctuations in the price of our securities could contribute to the loss of all or part of your investment. Prior to the Business Combination, there has not been a public market for EveryWare’s stock and trading in the shares of the Company’s common stock has not been active. Accordingly, the valuation ascribed to EveryWare and our common stock in the Business Combination may not be indicative of the price that will prevail in the trading market following the Business Combination. If an active market for our securities develops and continues, the trading price of our securities following the Business Combination could be volatile and subject to wide fluctuations in response to various factors, some of which are beyond our control. Any of the factors listed below could have a material adverse effect on your investment in our securities and our securities may trade at prices significantly below the price you paid for them. In such circumstances, the trading price of our securities may not recover and may experience a further decline.

Factors affecting the trading price of the Company’s securities may include:

| • | actual or anticipated fluctuations in our quarterly financial results or the quarterly financial results of companies perceived to be similar to us; | ||

| • | changes in the market’s expectations about our operating results; | ||

| • | success of competitors; | ||

| • | our operating results failing to meet the expectation of securities analysts or investors in a particular period; | ||

| • | changes in financial estimates and recommendations by securities analysts concerning the Company or the consumer goods market in general; |

| - 7 - |

| • | operating and stock price performance of other companies that investors deem comparable to the Company; | ||

| • | our ability to market new and enhanced products on a timely basis; | ||

| • | changes in laws and regulations affecting our business; | ||

| • | commencement of, or involvement in, litigation involving the Company; | ||

| • | changes in the Company’s capital structure, such as future issuances of securities or the incurrence of additional debt; | ||

| • | the volume of shares of our common stock available for public sale; | ||

| • | any major change in our board or management; | ||

| • | sales of substantial amounts of common stock by our directors, executive officers or significant stockholders or the perception that such sales could occur; and | ||

| • | general economic and political conditions such as recessions, interest rates, fuel prices, international currency fluctuations and acts of war or terrorism. |

Broad market and industry factors may materially harm the market price of our securities irrespective of our operating performance. The stock market in general, and NASDAQ have experienced price and volume fluctuations that have often been unrelated or disproportionate to the operating performance of the particular companies affected. The trading prices and valuations of these stocks, and of our securities, may not be predictable. A loss of investor confidence in the market for retail stocks or the stocks of other companies which investors perceive to be similar to the Company could depress our stock price regardless of our business, prospects, financial conditions or results of operations. A decline in the market price of our securities also could adversely affect our ability to issue additional securities and our ability to obtain additional financing in the future.

Warrants will become exercisable for our common stock, which would increase the number of shares eligible for future resale in the public market and result in dilution to our stockholders.

Outstanding warrants to purchase an aggregate of 11,676,667 shares of our common stock will become exercisable for a like number of shares of our common stock in accordance with the terms of the warrant agreement governing those securities. These warrants consist of 7,500,000 warrants originally sold as part of units in our Public Offering, 4,166,667 Sponsor Warrants originally sold by the Company to the Sponsor in a private sale simultaneously with our Public Offering (which were subsequently transferred to Magnolia) and 10,000 Sponsor Warrants originally sold as part of units issued simultaneously with our Public Offering to Mr. Baldwin. These warrants will become exercisable 30 days after the completion of the Business Combination, and will expire at 5:00 p.m., New York time, five years after the completion of the Business Combination or earlier upon redemption or liquidation. The exercise price of these warrants is $12.00 per share, or $140.1 million in the aggregate for all shares underlying these warrants. To the extent such warrants are exercised, additional shares of our common stock will be issued, which will result in dilution to the holders of common stock of the Company and increase the number of shares eligible for resale in the public market. Sales of substantial numbers of such shares in the public market could adversely affect the market price of our common stock.

If, following the Business Combination, securities or industry analysts do not publish or cease publishing research or reports about the Company, its business, or its market, or if they change their recommendations regarding our common stock adversely, the price and trading volume of our common stock could decline.

The trading market for our common stock will be influenced by the research and reports that industry or securities analysts may publish about us, our business, our market, or our competitors. Securities and industry analysts do not currently, and may never, publish research on the Company. If no securities or industry analysts commence coverage of the Company, our stock price and trading volume would likely be negatively impacted. If any of the analysts who may cover the Company change their recommendation regarding our stock adversely, or provide more favorable relative recommendations about our competitors, the price of our common stock would likely decline. If any analyst who may cover the Company were to cease coverage of the Company or fail to regularly publish reports on it, we could lose visibility in the financial markets, which in turn could cause our stock price or trading volume to decline.

Anti-takeover provisions contained in our certificate of incorporation and bylaws, as well as provisions of Delaware law, could impair a takeover attempt.

The Company’s certificate of incorporation and bylaws contain provisions that could have the effect of delaying or preventing changes in control or changes in our management without the consent of our board of directors. These provisions include:

| - 8 - |

| • | a classified board of directors with three-year staggered terms, which may delay the ability of stockholders to change the membership of a majority of our board of directors; | ||

| • | no cumulative voting in the election of directors, which limits the ability of minority stockholders to elect director candidates; | ||

| • | the exclusive right of our board of directors to elect a director to fill a vacancy created by the expansion of the board of directors or the resignation, death, or removal of a director, which prevents stockholders from being able to fill vacancies on our board of directors; | ||

| • | the ability of our board of directors to determine whether to issue shares of preferred stock and to determine the price and other terms of those shares, including preferences and voting rights, without stockholder approval, which could be used to significantly dilute the ownership of a hostile acquirer; | ||

| • | a prohibition on stockholder action by written consent, which forces stockholder action to be taken at an annual or annual meeting of our stockholders; | ||

| • | the requirement that an annual meeting of stockholders may be called only by the chairman of the board of directors, the chief executive officer, or the board of directors, which may delay the ability of our stockholders to force consideration of a proposal or to take action, including the removal of directors; | ||

| • | limiting the liability of, and providing indemnification to, our directors and officers; | ||

| • | controlling the procedures for the conduct and scheduling of stockholder meetings; | ||

| • | providing that directors may be removed prior to the expiration of their terms by stockholders only for cause; and | ||

| • | advance notice procedures that stockholders must comply with in order to nominate candidates to our board of directors or to propose matters to be acted upon at a stockholders’ meeting, which may discourage or deter a potential acquirer from conducting a solicitation of proxies to elect the acquirer’s own slate of directors or otherwise attempting to obtain control of the Company’s. |

These provisions, alone or together, could delay hostile takeovers and changes in control of the Company or changes in our management.

As a Delaware corporation, we are also subject to provisions of Delaware law, including Section 203 of the Delaware General Corporation Law (“DGCL”), which prevents some stockholders holding more than 15% of our outstanding common stock from engaging in certain business combinations without approval of the holders of substantially all of ROI’s outstanding common stock. Any provision of our certificate of incorporation or bylaws or Delaware law that has the effect of delaying or deterring a change in control could limit the opportunity for our stockholders to receive a premium for their shares of our common stock, and could also affect the price that some investors are willing to pay for our common stock.

If we are unable to effect a business combination by November 29, 2013, we will be forced to liquidate and the warrants will expire worthless.

If we do not complete a business combination by November 29, 2013, our second amended and restated certificate of incorporation provides that we will (i) cease all operations except for the purpose of winding up, (ii) as promptly as reasonably possible, subject to lawfully available funds therefor, redeem 100% of the public shares in consideration of a per-share price, payable in cash, equal to the quotient obtained by dividing (A) the aggregate amount then on deposit in the Trust Account, including interest but net of franchise and income taxes payable (less up to $50,000 of such net interest to pay dissolution expenses), by (B) the total number of then outstanding public shares, which redemption will completely extinguish rights of the Public Stockholders (including the right to receive further liquidation distributions, if any), subject to applicable law, and (iii) as promptly as reasonably possible following such redemptions, subject to the approval of the remaining stockholders and the board of directors in accordance with applicable law, dissolve and liquidate, subject in each case to the Company’s obligations under the DGCL to provide for claims of creditors and other requirements of applicable law. In the event of liquidation, there will be no distribution with respect to the company’s outstanding warrants. Accordingly, the warrants will expire worthless.

For illustrative purposes, based on funds in the Trust Account of $75.1 million on December 31, 2012, the estimated per share redemption price would have been approximately $10.00. We do not anticipate the Trust Account balance at the time the Business Combination is completed will be materially greater than the funds held in trust as of December 31, 2012.

| - 9 - |

If we are forced to liquidate, our stockholders may be held liable for claims by third parties against the Company to the extent of distributions received by them.

Under the DGCL, stockholders may be held liable for claims by third parties against a corporation to the extent of distributions received by them in a dissolution. The pro rata portion of the Trust Account distributed to our Public Stockholders upon the redemption of 100% of our public shares in the event we do not consummate an initial business combination by November 29, 2013 may be considered a liquidation distribution under Delaware law. If a corporation complies with certain procedures set forth in Section 280 of the DGCL intended to ensure that it makes reasonable provision for all claims against it, including a 60-day notice period during which any third-party claims can be brought against the corporation, a 90-day period during which the corporation may reject any claims brought, and an additional 150-day waiting period before any liquidating distributions are made to stockholders, any liability of stockholders with respect to a liquidating distribution is limited to the lesser of such stockholder’s pro rata share of the claim or the amount distributed to the stockholder, and any liability of the stockholder would be barred after the third anniversary of the dissolution. However, we intend to redeem our public shares as soon as reasonably possible following November 29, 2013 in the event we do not consummate an initial business combination and, therefore, we do not intend to comply with those procedures.

Because we will not be complying with Section 280, Section 281(b) of the DGCL requires the Company to adopt a plan, based on facts known to us at such time that will provide for the payment of all existing and pending claims or claims that may be potentially brought against the Company within the 10 years following dissolution. However, because we are a blank check company, rather than an operating company, and our operations have been limited to searching for prospective target businesses, the only likely claims to arise would be from vendors (such as lawyers, investment bankers, and consultants) or prospective target businesses. If the Company’s plan of distribution complies with Section 281(b) of the DGCL, any liability of our stockholders with respect to a liquidating distribution is limited to the lesser of such stockholder’s pro rata share of the claim or the amount distributed to the stockholder, and any liability of the stockholder would likely be barred after the third anniversary of the dissolution. There can be no assurance that we will properly assess all claims that may be potentially brought against us. As such, our stockholders could potentially be liable for any claims to the extent of distributions received by them (but no more) and any liability of its stockholders may extend beyond the third anniversary of such date. Furthermore, if the pro rata portion of the Trust Account distributed to our Public Stockholders upon the redemption of 100% of our public shares in the event we do not consummate an initial business combination within the required timeframe is not considered a liquidation distribution under Delaware law and such redemption distribution is deemed to be unlawful, then pursuant to Section 174 of the DGCL, the statute of limitations for claims of creditors could then be six years after the unlawful redemption distribution, instead of three years, as in the case of a liquidation distribution.

If we are forced to file a bankruptcy case or an involuntary bankruptcy case is filed against us which is not dismissed, any distributions received by stockholders could be viewed under applicable debtor/creditor and/or bankruptcy laws as either a “preferential transfer” or a “fraudulent conveyance.” As a result, a bankruptcy court could seek to recover all amounts received by our stockholders. Furthermore, because we intend to distribute the proceeds held in the Trust Account to our Public Stockholders promptly after November 29, 2013 in the event we do not consummate an initial business combination, this may be viewed or interpreted as giving preference to our stockholders over any potential creditors with respect to access to or distributions from the Company’s assets. Furthermore, our board of directors may be viewed as having breached its fiduciary duties to the Company’s creditors and/or may have acted in bad faith, thereby exposing itself and the Company to claims of punitive damages, by paying our stockholders from the Trust Account prior to addressing the claims of creditors. There can be no assurance that claims will not be brought against the Company for these reasons.

Unlike some other blank check companies, the Company does not have a specified maximum redemption threshold. The absence of such a redemption threshold will make it easier for us to consummate the Business Combination even if a substantial number of our stockholders do not agree.

Since the Company has no specified maximum redemption threshold, our structure is different in this respect from the structure that has been used by some blank check companies. Previously, blank check companies would not be able to consummate a business combination if the holders of the company’s public shares voted against a proposed business combination and elected to redeem or convert more than a specified percentage of the shares sold in such company’s Public Offering, which percentage threshold is typically between 19.99% and 39.99%. As a result, we may be able to consummate the Business Combination even though a substantial number of our Public Stockholders do not agree with the transaction and have redeemed their shares. In no event, however, will we redeem public shares in an amount that would cause our net tangible assets to be less than $5,000,001 (500,001 shares or 5.3% of the Company’s issued and outstanding public shares of common stock, as of December 31, 2012). In addition, it is a condition to closing under the Merger Agreement that we provide cash consideration of at least $90.0 million to EveryWare equityholders from the amount held in the Trust Account and from the proceeds of acquisition financing which we will seek to obtain in connection with the Business Combination. Each redemption of public shares by our Public Stockholders will decrease the amounts in our Trust Account and increase the number of additional shares of ROI common stock we would need to issue as a result of the cash shortfall. Therefore, in order to satisfy the condition to closing, the maximum redemption threshold is the amount that would allow us to maintain, in the aggregate, at least $90.0 million of available cash to pay the Cash Merger Consideration. If, however, redemptions by our public stockholders cause us to be unable to provide EveryWare’s equityholders with $90.0 million in cash consideration at the closing of the Business Combination, EveryWare, may, at its option, elect to receive additional shares of ROI common stock equal to the cash shortfall and thereby reduce the amount of cash it receives to as low as $55.0 million, which would increase the maximum redemption threshold.

| - 10 - |

Activities taken by the Company and its affiliates to purchase, directly or indirectly, public shares will increase the likelihood of approval of the Business Combination and may affect the market price of the Company’s securities during the buyback period.

We may enter into privately negotiated transactions to purchase public shares from stockholders following consummation of the Business Combination with proceeds released to it from the Trust Account immediately following consummation of the Business Combination. Magnolia and our directors, officers, advisors or their affiliates may also purchase shares in privately negotiated transactions either prior to or following the consummation of the Business Combination. Neither we nor Magnolia and our directors, officers, advisors or their affiliates will make any such purchases when such parties are in possession of any material non-public information not disclosed to the seller or during a restricted period under Regulation M under the Exchange Act of 1934, as amended (the “Exchange Act”). Although neither we nor Magnolia and our directors, officers, advisors or their affiliates currently anticipate paying any premium purchase price for such public shares, in the event such parties do, the payment of a premium may not be in the best interest of those stockholders not receiving any such additional consideration. In addition, the payment of a premium by the Company after the consummation of the Business Combination may not be in the best interest of the remaining stockholders who do not redeem their shares, because such stockholders will experience a reduction in book value per share compared to the value received by stockholders that have their shares purchased by the Company at a premium. Except for the limitations described above on use of trust proceeds released to the Company prior to consummating the Business Combination, there is no limit on the number of shares that could be acquired by the Company or Magnolia and our directors, officers, advisors or their affiliates, or the price such parties may pay.

If such transactions are effected, the consequence could be to cause the Business Combination to be approved in circumstances where such approval could not otherwise be obtained. Purchases of shares by the persons described above would allow them to exert more influence over the approval of the Business Combination and would likely increase the chances that the Business Combination would be approved. In addition, if the market does not view the Business Combination positively, purchases of public shares may have the effect of counteracting the market’s view, which would otherwise be reflected in a decline in the market price of our securities. In addition, the termination of the support provided by these purchases may materially adversely affect the market price of our securities.

As of the date of this Annual Report on Form 10-K, no agreements with respect to the private purchase of public shares by the Company or the persons described above have been entered into with any such investor or holder. We will file a Current Report on Form 8-K with the SEC to disclose private arrangements entered into or significant private purchases made by any of the aforementioned persons that would affect the vote on the Business Combination.

Our stockholders will experience immediate dilution as a consequence of the issuance of common stock as consideration in the Business Combination. Having a minority share position may reduce the influence that our current stockholders have on the management of the Company.

We will issue 10,440,000 shares of common stock of the Company at the closing to EveryWare’s equity holders, subject to adjustment as described herein, and an additional 3,500,000 Earnout Shares. As a result, our current stockholders will hold 9,385,000 shares or approximately 40.4% of the post-merger company. This percentage assumes that ROI receives $250.0 million in cash proceeds from the proposed issuance of senior secured notes in order to fund the Cash Merger Consideration and refinance EveryWare’s existing debt and are based upon net debt of EveryWare at December 31, 2012. If the actual facts are different than these assumptions, the percentage ownership retained by ROI’s existing stockholders will be different. This percentage also does not take into account (i) the additional 3,500,000 Earnout Shares and 551,471 shares of outstanding ROI common stock currently held by Magnolia, that could in each case be subject to forfeiture in the future if certain performance conditions relating to the trading price of ROI’s Common Stock are not met following the Business Combination, (ii) options to purchase shares of ROI common stock that will be issued to former holders of EveryWare stock option in connection with the Business Combination and (iii) warrants to purchase ROI’s common stock that will remain outstanding following the Business Combination. Consequently, the ability of our current stockholders following the Business Combination to influence management of the Company through the election of directors will be substantially reduced.

| - 11 - |

If we are unable to complete the Business Combination by November 29, 2013, our second amended and restated certificate of incorporation provides that its corporate existence will automatically terminate and we will dissolve and liquidate. In such event, third parties may bring claims against the Company and, as a result, the proceeds held in trust could be reduced and the per share liquidation price received by stockholders could be less than $10.00 per share.

We must complete a business combination by November 29, 2013, when, pursuant to our second amended and restated certificate of incorporation, our corporate existence will terminate and we will be required to liquidate. In such event, third parties may bring claims against the Company. Although we have obtained waiver agreements from many of the vendors and service providers we have engaged and prospective target businesses with which we have negotiated, whereby such parties have waived any right, title, interest or claim of any kind in or to any monies held in the Trust Account for the benefit of our public stockholders, there is no guarantee that such parties will not bring claims seeking recourse against the Trust Account including, but not limited to, fraudulent inducement, breach of fiduciary responsibility or other similar claims, as well as other claims challenging the enforceability of the waiver, in each case in order to gain advantage with respect to a claim against the Company’s assets, including the funds held in the Trust Account. Further, we could be subject to claims from parties not in contract with it who have not executed a waiver, such as a third party claiming tortious interference as a result of the Business Combination. GEH Capital Inc., Joseph A. De Perio and George E. Hall have agreed that they will be liable to the Company if and to the extent any claims by a vendor for services rendered or products sold to the Company, or a prospective target business with which we have discussed entering into a business combination agreement, reduce the amounts in the Trust Account to below $10.00 per share except as to any claims by a third party who executed a waiver of any and all rights to seek access to the Trust Account and except as to any claims under our indemnity of the underwriters of our Public Offering against certain liabilities, including liabilities under the Securities Act. Moreover, in the event that an executed waiver is deemed to be unenforceable against a third party, GEH Capital Inc., Joseph A. De Perio and George E. Hall will not be responsible to the extent of any liability for such third party claims. However, we have not asked GEH Capital Inc., Joseph A. De Perio or George E. Hall to reserve for such indemnification obligations and there can be no assurance that GEH Capital Inc., Joseph A. De Perio or George E. Hall would be able to satisfy those obligations. None of our officers will indemnify us for claims by third parties including, without limitation, claims by vendors and prospective target businesses. In addition, if GEH Capital Inc., Joseph A. De Perio or George E. Hall assert that they are unable to satisfy their obligations or that they have no indemnification obligations related to a particular claim, our independent directors would determine whether to take legal action against GEH Capital Inc., Joseph A. De Perio and George E. Hall to enforce their indemnification obligations. While we currently expect that the Company’s independent directors would take legal action on their behalf against GEH Capital Inc., Joseph A. De Perio and George E. Hall to enforce their indemnification obligations, it is possible that the Company’s independent directors in exercising their business judgment may choose not to do so in any particular instance.

Stockholders of ROI who wish to redeem their shares for a pro rata portion of the Trust Account must comply with specific requirements for redemption that may make it more difficult for them to exercise their redemption rights prior to the deadline for exercising redemption rights.

Public stockholders who wish to redeem their shares for a pro rata portion of the Trust Account must, among other things, tender their certificates to our transfer agent or deliver their shares to the transfer agent electronically through the DTC prior to 4:30 P.M., New York time, on the second business day prior to the special meeting of stockholders. In order to obtain a physical stock certificate, a stockholder’s broker and/or clearing broker, DTC and our transfer agent will need to act to facilitate this request. It is our understanding that stockholders should generally allot at least two weeks to obtain physical certificates from the transfer agent. However, because we do not have any control over this process or over the brokers or DTC, it may take significantly longer than two weeks to obtain a physical stock certificate. If it takes longer than anticipated to obtain a physical certificate, stockholders who wish to redeem their shares may be unable to obtain physical certificates by the deadline for exercising their redemption rights and thus will be unable to redeem their shares.

The financial statements included in this Annual Report on Form 10-K do not take into account the consequences to ROI of a failure to complete a business combination by November 29, 2013.

The financial statements included in this Annual Report on Form 10-K have been prepared assuming that we would continue as a going concern. As discussed in Note 1 to the Notes to the ROI financial statements for the year ended December 31, 2012, we are required to complete the Business Combination by November 29, 2013. The possibility of the Business Combination not being consummated raises some doubt as to our ability to continue as a going concern and the financial statements do not include any adjustments that might result from the outcome of this uncertainty.

The ROI board of directors did not obtain a third-party valuation or fairness opinion in determining whether or not to proceed with the Business Combination.

Our board of directors did not obtain a third-party valuation or fairness opinion in connection with their determination to approve the Business Combination. In analyzing the Business Combination, our board and management conducted due diligence on EveryWare, researched the industries in which EveryWare operates, and developed a long-range financial model and concluded that the Business Combination was in the best interest of our stockholders. The lack of a third-party valuation or fairness opinion may lead an increased number of our stockholders to vote against the Business Combination or demand redemption of their shares of our common stock, which could potentially impact our ability to consummate the Business Combination.

The Company and EveryWare will be subject to business uncertainties and contractual restrictions while the Business Combination is pending.

Uncertainty about the effect of the Business Combination on employees and customers may have an adverse effect on the Company and EveryWare. These uncertainties may impair our or EveryWare’s ability to retain and motivate key personnel and could cause customers and others that deal with any of us or them to defer entering into contracts or making other decisions or seek to change existing business relationships. If key employees depart because of uncertainty about their future roles and the potential complexities of the Business Combination, our or EveryWare’s business could be harmed.

| - 12 - |

We will incur significant transaction and transition costs in connection with the Business Combination.

We expect to incur significant, non-recurring costs in connection with consummating the Business Combination and EveryWare operating as a public company. We may incur additional costs to maintain employee morale and to retain key employees. We will also incur significant fees and expenses relating to financing arrangements and legal, accounting and other transaction fees and costs associated with the Business Combination. Some of these costs are payable regardless of whether the Business Combination is completed.

Registration of the shares underlying the warrants and a current prospectus may not be in place when an investor desires to exercise warrants, thus precluding such investor from being able to exercise its warrants and causing such warrants to expire worthless.

Under the warrant agreement, we will be obligated to use our best efforts to maintain the effectiveness of a registration statement under the Securities Act, and a current prospectus relating thereto, until the expiration of the warrants in accordance with the provisions of the warrant agreement. In addition, we will be obligated to use our best efforts to register the shares of common stock issuable upon exercise of a warrant under the blue sky laws of the states of residence of the exercising warrantholder to the extent an exemption is not available.

If any such registration statement is not effective on the 60th day following the closing of the Business Combination or afterward, we will be required to permit holders to exercise their warrants on a cashless basis, under certain circumstances specified in the warrant agreement. However, no warrant will be exercisable for cash or on a cashless basis, and we will not be obligated to issue any shares to holders seeking to exercise their warrants, unless the shares issuable upon such exercise are registered or qualified under the Securities Act and securities laws of the state of the exercising holder to the extent an exemption is unavailable. In no event will we be required to issue cash, securities or other compensation in exchange for the warrants in the event that the shares underlying such warrants are not registered or qualified under the Securities Act or applicable state securities laws. If the issuance of the shares upon exercise of the warrants is not so registered or qualified, the holder of such warrant shall not be entitled to exercise such warrant and such warrant may have no value and expire worthless. In such event, holders who acquired their warrants as part of a purchase of units will have paid the full unit purchase price solely for the shares of common stock included in the units. If and when the warrants become redeemable, we may exercise our redemption right even if we are unable to register or qualify the underlying shares of common stock for sale under all applicable state securities laws.

We may redeem the public warrants prior to their exercise at a time that is disadvantageous to warrantholders, thereby making their warrants worthless.

We will have the ability to redeem the outstanding public warrants at any time after they become exercisable (which would not be before 30 days after the consummation of the Business Combination) and prior to their expiration at a price of $0.01 per warrant, provided that (i) the last reported sale price of our common stock equals or exceeds $18.00 per share for any 20 trading days within the 30 trading-day period ending on the third business day before we send the notice of such redemption and (ii) on the date we give notice of redemption and during the entire period thereafter until the time the warrants are redeemed, there is an effective registration statement under the Securities Act covering the shares of our common stock issuable upon exercise of the public warrants and a current prospectus relating to them is available. Redemption of the outstanding public warrants could force holders of public warrants:

| • | to exercise their warrants and pay the exercise price therefor at a time when it may be disadvantageous for them to do so; | ||

| • | to sell their warrants at the then-current market price when they might otherwise wish to hold their warrants; or | ||

| • | to accept the nominal redemption price which, at the time the outstanding warrants are called for redemption, is likely to be substantially less than the market value of their warrants. |

We may not be able to complete the proposed financing transactions in connection with the Business Combination.

We may not be able to complete the proposed financing transactions, including the amendment of EveryWare’s existing senior credit facility and the issuance of senior secured notes offering, in connection with the Business Combination on terms that are acceptable to us, or at all. If we do not complete the proposed financing transactions contemplated by the Business Combination, we will be required to obtain alternative financing in order to fund a portion of the cash consideration for the Business Combination. If we are unable do so on terms that are acceptable to us, or at all, we may not be able to complete the Business Combination. Neither completing the amendment of EveryWare’s existing senior credit facility or the senior secured notes offering, nor obtaining any other financing, is a condition to the Business Combination under the Merger Agreement; however, it is a condition to closing under the Merger Agreement that we provide cash consideration of at least $90.0 million to EveryWare, from the amount held in the Trust Account and from the proceeds of acquisition financing.

| - 13 - |

Risks Related to EveryWare’s Business and Industry

Slowdowns in the retail and foodservice industries could adversely impact EveryWare’s results of operations, financial condition and liquidity.

EveryWare’s operations and financial performance are directly impacted by changes in the retail and foodservice industries, which in turn are impacted by changes in the global economy. The retail and foodservice industries are directly affected by general economic factors including recession, inflation, deflation, new home sales and housing starts, levels of disposable income, consumer credit availability, consumer debt levels, unemployment trends, fuel and energy costs, material input costs, foreign currency translation, labor cost inflation, interest rates, the impact of natural disasters, political and social unrest and terrorism and other matters that influence consumer spending. Any significant downturn in the global economy may significantly lower consumer discretionary spending, which may in turn lower the demand for EveryWare’s products, particularly in EveryWare’s consumer segment. In particular, demand for EveryWare’s consumer products is correlated to the strength of the housing industry because consumers are more likely to purchase tabletop, food preparation and pantry products in connection with purchasing a new home. When home sales and housing starts are weak, demand for EveryWare’s products can be adversely affected. Expenditures in the foodservice industry are also affected by discretionary spending levels and may decline during a general economic downturn. Hotels, airlines and restaurants are less likely to invest in new flatware, dinnerware, barware, hollowware and banquetware when there is a slowdown in their industry. Currently, uncertainty about global economic conditions and austerity measures adopted by some governments in order to address sovereign debt concerns may cause consumers of EveryWare’s products to postpone spending in response to tighter credit, negative financial news or declines in income or asset values. These factors could have adverse effects on the demand for EveryWare’s products and on EveryWare’s operating results and financial condition. A substantial deterioration in general economic conditions would likely exacerbate these adverse effects and could result in a wide-ranging and prolonged impact on general business conditions, which could negatively impact EveryWare’s results of operations, financial condition and liquidity.

EveryWare’s operations and financial performance are directly impacted by changes in the global economy.