Attached files

| file | filename |

|---|---|

| EX-31.1 - EQUAL ENERGY LTD. | ceocert302.htm |

| EX-32.1 - EQUAL ENERGY LTD. | ceocert906.htm |

| EX-31.2 - EQUAL ENERGY LTD. | cfocert302.htm |

| EX-32.2 - EQUAL ENERGY LTD. | cfocert906.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

|

For the fiscal year ended December 31, 2012

|

or

|

¨

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

Commission File Number 001-34759

EQUAL ENERGY LTD.

(Exact name of registrant as specified in its charter)

|

Alberta, Canada

|

98-0533758

|

|

|

(State of other jurisdiction of incorporation or organization)

|

(I.R.S. Employer identification No.)

|

|

|

500 – 4th Avenue S.W., Suite 2600, Calgary

|

T2P 2V6

|

|

|

(Address of principal executive offices)

|

(Zip code)

|

|

Registrant’s telephone number, including area code:

(403) 263-0262

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

|

Name of each exchange on which registered

|

|

Common stock, without par value

|

|

The New York Stock Exchange

|

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ Accelerated filer x Non- accelerated filer ¨ Smaller reporting company ¨

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the common stock held by non-affiliates of the registrant as of June 29, 2012, was approximately $87.3 million, based on the closing price as quoted by the New York Stock Exchange. As of March 14, 2013, 35,562,967 million shares of common stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Certain portions of the registrant’s definitive proxy statement to be filed with the Securities and Exchange Commission in connection with the 2013 annual meeting of stockholders are incorporated by reference into — Part III of this Annual Report on Form 10-K.

Various statements contained in this report, including those that express a belief, expectation, or intention, as well as those that are not statements of historical fact, are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These statements express a belief, expectation or intention and generally are accompanied by words that convey projected future events or outcomes. These forward-looking statements may include projections and estimates concerning capital expenditures, the Company’s

liquidity, capital resources, and debt profile, pending acquisitions or dispositions, the timing and success of specific projects, outcomes and effects of litigation, claims and disputes, elements of the Company’s business strategy, compliance with governmental regulation of the oil and natural gas industry, including environmental regulations, acquisitions and divestitures and the effects thereof on the Company’s financial condition and other statements concerning the Company’s operations, economic performance and financial condition. Forward-looking statements are generally accompanied by words such as “estimate,” “assume,” “target,” “project,” “predict,” “believe,” “expect,” “anticipate,” “potential,” “could,” “may,”

“foresee,” “plan,” “goal,” “should,” “intend” or other words that convey the uncertainty of future events or outcomes. The Company has based these forward-looking statements on its current expectations and assumptions about future events. These statements are based on certain assumptions and analyses made by the Company in light of its experience and perception of historical trends, current conditions and expected future developments as well as other factors the Company believes are appropriate under the circumstances. The actual results or developments anticipated may not be realized or, even if substantially realized, may not have the expected consequences to or effects on the Company’s business or results. Such statements are not guarantees of future performance and actual results or developments may differ materially

from those projected in such forward-looking statements. These forward-looking statements speak only as of the date hereof. The Company disclaims any obligation to update or revise these forward-looking statements unless required by law, and it cautions readers not to rely on them unduly. While the Company’s management considers these expectations and assumptions to be reasonable, they are inherently subject to significant business, economic, competitive, regulatory and other risks, contingencies and uncertainties relating to, among other matters, the risks and uncertainties discussed in “Risk Factors” in Item 1A of this report, including the following:

|

•

|

risks associated with drilling oil and natural gas wells;

|

|

•

|

the volatility of oil and natural gas prices;

|

|

•

|

uncertainties in estimating oil and natural gas reserves;

|

|

•

|

the need to replace the oil and natural gas the Company produces;

|

|

•

|

the Company’s ability to execute its growth strategy by drilling wells as planned;

|

|

•

|

risks and liabilities associated with acquired properties and risks related to the integration of acquired businesses;

|

|

•

|

amount, nature and timing of capital expenditures, including future development costs, required to develop the Company’s undeveloped areas;

|

|

•

|

concentration of operations in Central Oklahoma;

|

|

•

|

inability to retain drilling rigs and other services;

|

|

•

|

risk of currency fluctuations;

|

|

•

|

the potential adverse effect of commodity price declines on the carrying value of the Company’s oil and natural gas properties;

|

|

•

|

severe or unseasonable weather that may adversely affect production;

|

|

•

|

availability of satisfactory oil and natural gas marketing and transportation;

|

|

•

|

availability and terms of capital to fund capital expenditures;

|

|

•

|

amount and timing of proceeds of asset sales and asset monetizations;

|

|

•

|

ability to fund ongoing dividends;

|

|

•

|

limitations on operations resulting from debt restrictions and financial covenants;

|

|

•

|

potential financial losses or earnings reductions from commodity derivatives;

|

|

•

|

potential elimination or limitation of tax incentives;

|

|

•

|

competition in the oil and natural gas industry;

|

|

risks associated with consent solicitations and proxy contests conducted by dissident stockholders;

|

|

•

|

general economic conditions, either internationally or domestically or in the areas where the Company operates;

|

|

•

|

inability to obtain required regulatory approvals for development activities;

|

|

•

|

costs to comply with current and future governmental regulation of the oil and natural gas industry, including environmental, health and safety laws and regulations, and regulations with respect to hydraulic fracturing; and

|

|

•

|

the need to maintain adequate internal control over financial reporting.

|

The reader is further cautioned that the preparation of the financial statements in this report that are in accordance with GAAP requires management to make certain judgments and estimates that affect the reported amounts of assets, liabilities, revenues and expenses. Estimating reserves is also critical to several accounting estimates and requires judgments and decisions based upon available geological, geophysical, engineering and economic data. These estimates may change, having either a negative or positive effect on the financial status of the Company as further information becomes available, and as the economic environment changes.

Many of these risk factors and other specific risks and uncertainties are discussed in further detail throughout this report and in the Corporation’s management’s discussion and analysis for the year ended December 31, 2012 (the “MD&A”), which is available through the internet on the Corporation’s SEDAR profile at www.sedar.com, on EDGAR at www.sec.gov , and on the Corporation’s website at www.equalenergy.ca. Readers are also referred to the risk factors described in this

report under ”Risk Factors” and in other documents the Corporation’s files from time to time with securities regulatory authorities. Copies of these documents are available without charge from the Corporation’s or electronically on the internet on the Corporation’s SEDAR profile at www.sedar.com on EDGAR at www.sec.gov and on the Corporation’s website at www.equalenergy.ca.

BOE’s may be misleading, particularly if used in isolation. A BOE conversion ratio of 6 mcf to one boe is based on an energy equivalency conversion method primarily applicable at the burner tip and does not necessarily represent a value equivalence at the wellhead.

CONVENTIONS

Unless otherwise indicated, all references herein to dollar amounts are in Canadian dollars (CDN$) and references herein to “$” or “dollars” are to Canadian dollars or “M$” are to a thousand Canadian dollars or “MM$” are to a million Canadian dollars.

The information set out in this REPORT is stated as at December 31, 2012 unless otherwise indicated. Capitalized terms used but not defined in the text are defined in the Glossary.

EQUAL ENERGY LTD

FORM 10-K

TABLE OF CONTENTS

|

PART I

|

||

|

Items 1 and 2. Business and Properties

|

|

|

|

Item 1A. Risk Factors

|

|

|

|

Item 1B. Unresolved Staff Comments

|

|

|

|

Item 3. Legal Proceedings

|

|

|

|

Item 4. Mine Safety Disclosures

|

|

|

|

PART II

|

||

|

Item 5. Market for Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

|

|

|

Item 6. Selected Financial Data

|

|

|

|

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

|

|

|

Item 7A. Quantitative and Qualitative Disclosures about Market Risk

|

|

|

|

Item 8. Financial Statements and Supplementary Data

|

|

|

|

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

|

|

|

Item 9A. Controls and Procedures

|

|

|

|

Item 9B. Other Information

|

|

|

|

PART III

|

||

|

Item 10. Directors, Executive Officers and Corporate Governance

|

|

|

|

Item 11. Executive Compensation

|

|

|

|

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

|

|

|

Item 13. Certain Relationships and Related Transactions, and Director Independence

|

|

|

|

Item 14. Principal Accountant Fees and Services

|

|

|

|

PART IV

|

||

|

Item 15. Exhibits and Financial Statement Schedules

|

|

|

|

Signatures

|

|

PART I

General

Equal Energy Ltd. is an exploration and production oil and gas company which had its head office in Calgary, Alberta for 2012 which has subsequently moved to Oklahoma City, Oklahoma during 2013. Equal’s oil and gas properties located in Oklahoma.

Equal Energy is the successor to the Trust following the completion of the reorganization of the Trust from an income trust structure to a corporate structure by way of court approved plan of arrangement under the ABCA on May 31, 2010 (the Arrangement”). The Arrangement involved the exchange, on a three-for-one basis (the “Consolidation”), of all outstanding Trust Units for Common Shares.

Equal Energy was incorporated on April 8, 2010 under the ABCA and did not carry on any active business prior to the Arrangement, other than executing the arrangement agreement pursuant to which the Arrangement was implemented. On January 1, 2011, Equal Energy amalgamated with its wholly-owned subsidiary, Equal Energy Corp. (the successor of EEC). The Company’s head office is located at Suite 2600, 500 - 4th Avenue S.W., Calgary, Alberta, Canada T2P 2V6. The Company’s registered office is located at 4300 Bankers Hall West, 888 – 3rd Street S.W., Calgary, Alberta, Canada T2P

5C5.

EEUSHI is an indirect, wholly-owned subsidiary of Equal Energy. EEUSHI holds all of Equal’s Oklahoma oil and gas properties and associated assets through its wholly owned subsidiary, Equal Energy US Inc., corporation incorporated under the laws of the state of Oklahoma. Equal Energy also has a U.S. office located at 4801 Gaillardia Parkway, Suite 325 Oklahoma City, Oklahoma.

On December 12, 2012 Equal Energy Ltd. was amalgamated with Equal Energy Partner Corp. and Equal Energy Production Partnership.

Equal Energy is engaged in the exploration for, and acquisition development and production of, petroleum and natural gas with operations in Oklahoma. The Company also reviews new drilling opportunities and potential acquisitions in Oklahoma to supplement its exploration and development activities. Production during 2012 averaged 7,186 boe/d and was comprised of approximately 53% natural gas 2% crude oil and 45% NGLs. For 2013, production is expected to be approximately 52% natural gas, 2% crude oil and 46% NGLs. At December 31, 2012 The Company had 126 gross (106 net) producing wells virtually all of which it operates and approximately 83,803 gross (54,211 net) total acres under lease or held

by production.

Business Strategy

Equal’s strategy is to provide a balance between future growth and return of capital by way of a dividend and is focused on delivering results under the 2013 business plan and to position Equal to take advantage of the anticipated recovery in commodity prices. The Company plans to continue to exploit its proven resource play with near term drilling in the liquids rich Hunton play.

For 2013 Equal is anticipating production to average 6,400 boe/d net of royalties (7,900 boe/d gross working interest volumes). Cash from operations is estimated at $33 million based on the assumptions of Nymex Natural Gas: USD$3.90/mmbtu (Equal realization 87% of Nymex), Propane at Conway Kansas: USD$0.90/gallon (Equal NGL realization 89% of Conway Propane) and WTI Oil: USD$90.00/bbl (Equal realization 96% of WTI). Capital spending of $36 million ($30 million for drilling and related infrastructure; $6 million for land and maintenance capital). Equal operates all of its drilling and can dictate the pace and targets of its drilling programs. The Company can also adjust quickly to changing

circumstances, including any changes in commodity prices if necessary. Equal has an extensive drilling inventory so it can increase capital spending in a higher commodity price environment and has the financial flexibility to do so through the Credit Facility. Primary objectives of the plan are to maintain financial flexibility by ensuring ongoing balance sheet strength and to maintain its recently declared annual dividend of US$0.20 per common share.

2012 DEVELOPMENTS

In the first quarter of 2012, Equal sold non-core assets in Saskatchewan for proceeds of $8.3 million which was used to reduce amounts outstanding on the credit facility.

In the second quarter of 2012, Equal through its 100% owned subsidiary EEUSHI, sold 50% of its interest in approximately 14,500 net undeveloped acres prospective for Mississippian light oil for total cash consideration of approximately US$18 million. Concurrently with the sale, Equal entered into a joint venture with Atlas to embark on drilling program in the Mississippian play. On May 3, 2012 Equal’s Board of Directors initiated a strategic review process to identify, examine and consider alternatives with the view to enhancing shareholder value. Strategic alternatives considered but were not limited to, the sale of all or a portion of the Company's assets, the outright sale of the corporation, a merger or

other business combination, a recapitalization, acquisitions, as well as continued execution of its business plan, or any combination thereof.

In the third quarter of 2012, Equal, through its 100% subsidiary EEUSHI, sold its interest in its Northern Oklahoma assets located in Grant, Garfield and Alfalfa Counties for cash consideration of US$40.0 million. The assets sold included 1,130 barrels of oil equivalent per day from the Hunton formation, related infrastructure and interests in approximately 8,550 acres of Mississippian lands.

In the fourth quarter of 2012, Equal sold the following Canadian assets: Halkirk/Alliance/Wainwright/Clair assets for $15.4 million, Lochend Cardium assets for $62 million and its royalty fee title assets and the residual resource income tax pools for $12.1 million. As a result of these sales, Equal has discontinued operations in Canada.

On November 27, 2012, Equal announced the termination of its Strategic Review process and announced the initiation of a US$0.20 per share annual dividend beginning January 1, 2013 payable quarterly at the end of each calendar quarter.

Oil and Gas Properties

Property Profiles

The following is a description of the Company’s material oil and natural gas properties as at December 31, 2012. Production stated is sales production on a net revenue interest basis to the Company and, unless otherwise stated, is the average daily production for December 2012. Reserve amounts are total proved reserves based on constant prices and costs as at December 31, 2012. The estimates of reserves and future net revenue for individual properties may not reflect the same confidence level as for all properties, due to the effects of aggregation. Unless otherwise specified, gross and net acres and well count information are as at December 31, 2012.

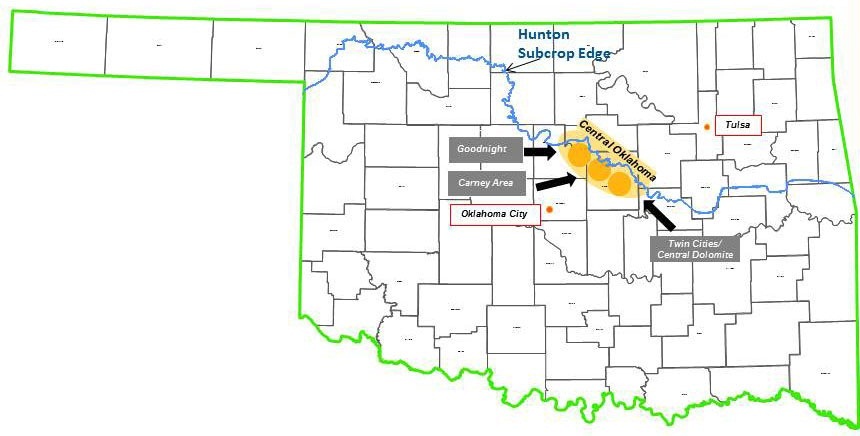

Overview

In December 2012 the Company’s production comes from its Oklahoma based operations. The U.S. core area assets are located mainly in Lincoln and Logan Counties of Oklahoma. The Corporation also has an inventory of minor producing assets, minor royalty interests and various exploration and exploitation prospects on undeveloped lands in Oklahoma.

Oklahoma

Hunton

In Oklahoma the key producing horizon is the Hunton formation. The Hunton is a carbonate rock formation which has been largely ignored by the industry in areas with high water/hydrocarbon production ratios. Over the last decade, new drilling and production techniques have enabled profitable development of the Hunton formation. Extensive dewatering lowers reservoir pressure allowing the liberation and mobilization of oil, natural gas and NGLs from smaller rock pores. Typical peak hydrocarbon production rates average 120 boe/d per horizontal well and are generally observed within six months of production commencement.

Average Hunton production for December 2012 was 19.0 Mmcf/d of natural gas, 3,207 bbl/d of NGLs and 169 bbl/d of oil from a total of 126 producing wells. The Haas Report has attributed total proved reserves of 268.0 Mbbl of crude oil, and 63.4 Bcf of natural gas and 8,894.0 mbbl of NGLs to the Company.

In Oklahoma, there are approximately 9,800 net undeveloped acres of land, at year end 2012. This acreage is centered in Lincoln and Logan Counties.

Proved Reserves

Preparation of Reserve Estimates

The estimates of oil and natural gas reserves in this report are based on reserve reports, all of which were prepared by Haas independent petroleum engineers. To achieve reasonable certainty, the Company’s engineers relied on technologies that have been demonstrated to yield results with consistency and repeatability. The technologies and economic data used to estimate the Company’s proved reserves include, but are not limited to, well logs, geological maps, seismic data, well test data, production data, historical price and cost information and property ownership interests. This data was reviewed by various levels of management for accuracy, before consultation with independent petroleum engineers.

Such consultation included review of properties, assumptions and any new data available. Internal reserves estimates and methodologies were compared to those prepared by independent petroleum engineers to test the reserves estimates and conclusions before the reserves estimates were included in this report. The accuracy of the reserve estimates is dependent on many factors, including the following:

|

•

|

the quality and quantity of available data and the engineering and geological interpretation of that data;

|

|

•

|

estimates regarding the amount and timing of future costs, which could vary considerably from actual costs;

|

|

•

|

the accuracy of mandated economic assumptions such as the future price of oil and natural gas; and

|

|

•

|

the judgment of the personnel preparing the estimates.

|

All evaluations and reviews of future net cash flow are stated prior to any provision for interest costs or general and administrative costs and after the deduction of estimated future capital expenditures for wells to which reserves have been assigned. It should not be assumed that the estimated future net cash flow shown below is representative of the fair market value of the Company’s properties. There is no assurance that such price and cost assumptions will be attained, and variances could be material. The recovery and reserve estimates of crude oil, NGL and natural gas reserves provided herein are estimates only and there is no guarantee that the

estimated reserves will be recovered. Actual crude oil, NGL and natural gas reserves may be greater than or less than the estimates provided herein.

Equal’s Senior Vice President of Engineering was the technical person primarily responsible for overseeing the preparation of the Company’s reserve estimates. He has a Bachelor of Science degree in Mechanical Engineering with over 20 years of practical engineering experience.

The qualifications of the technical personnel at Haas primarily responsible for overseeing Haas’ preparation of the Company’s reserves estimates are set forth below. The qualifications meet or exceed the Society of Petroleum Engineers’ standard requirements to be a professionally qualified Reserve Estimator and Auditor.

|

-

|

practical experience in petroleum engineering with more than 35 years and experience estimating and evaluating reserve information for more than 30 years.

|

|

-

|

Licensed Professional Engineers in the State of Texas; and

|

|

-

|

Bachelor of Science Degree in Petroleum Engineering.

|

In addition to conducting these internal and external reviews, we also have a Reserves Committee that consists of three independent members of our Board of Directors. This committee provides additional oversight of our reserves estimation and certification process. The Reserves Committee assists the Board of Directors with its duties and responsibilities in evaluating and reporting our proved reserves, much like our Audit Committee assists the Board of Directors in supervising our audit and financial reporting requirements. Besides being independent, the members of our Reserves Committee also have educational backgrounds in geology or petroleum engineering, as well as experience relevant to the reserves estimation

process.

Technologies

Under SEC rules, proved reserves are those quantities of oil and natural gas, which, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically producible, based on prices used to estimate reserves, from a given date forward from known reservoirs, and under existing economic conditions, operating methods, and government regulations prior to the time at which contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain. The term “reasonable certainty” implies a high degree of confidence that the quantities of oil and/or natural gas actually recovered will equal or exceed the estimate. Reasonable certainty

can be established using techniques that have been proved effective by actual production from projects in the same reservoir or an analogous reservoir or by other evidence using reliable technology that establishes reasonable certainty. Reliable technology is a grouping of one or more technologies (including computational methods) that have been field tested and have been demonstrated to provide reasonably certain results with consistency and repeatability in the formation being evaluated or in an analogous formation.

The area of a reservoir considered proved includes (i) the area identified by drilling and limited by fluid contacts, if any, and (ii) adjacent undrilled portions of the reservoir that can, with reasonable certainty, be judged to be continuous with it and to contain economically producible oil or natural gas on the basis of available geoscience and engineering data. In the absence of data on fluid contacts, proved quantities in a reservoir are limited by the lowest known hydrocarbons as seen in a well penetration unless geoscience, engineering or performance data and reliable technology establish a lower contact with reasonable certainty.

Where direct observation from well penetrations has defined a highest known oil elevation and the potential exists for an associated gas cap, proved oil reserves may be assigned in the structurally higher portions of the reservoir only if geoscience, engineering or performance data and reliable technology establish the higher contact with reasonable certainty.

Existing economic conditions include prices and costs at which economic producibility from a reservoir is to be determined. In determining the amount of proved reserves, the price used must be the average price during the 12-month period prior to the ending date of the period covered by the reserve report, determined as an unweighted arithmetic average of the first-day-of-the-month price for each month within such period, unless prices are defined by contractual arrangements, excluding escalations based upon future conditions.

The estimates of proved developed reserves included in the reserve report were prepared using decline curve analysis to determine the reserves of individual producing wells. After estimating the reserves of each proved developed well, it was determined that a reasonable level of certainty exists with respect to the reserves that can be expected from close offset undeveloped wells in the field

Reserve Quantities, PV-10 and Standardized Measure

The following estimates of proved oil, natural gas and NGL reserves are based on reserve reports as of December 31, 2012, 2011 and 2010, substantially all of which were prepared by independent petroleum engineers. The PV-10 values shown in the table below are not intended to represent the current market value of the Company’s estimated oil and natural gas reserves as of the dates shown. The reserve reports were based on the Company’s drilling schedule and the average price during the 12-month period ended December 31, 2012, 2011 and 2010, using first-day-of-the-month prices for each month. The Company estimates that approximately 80% of its current proved undeveloped reserves will

be developed by the end of 2014 and all of its current proved undeveloped reserves will be developed by the end of 2016. See “Critical Accounting Policies and Estimates” in Item 7 of this report for further discussion of uncertainties inherent to the reserves estimates. All historical Canadian reserves information has been excluded from the following reserve information because all Canadian assets were sold during 2012 and the results of the Canadian operations have been recorded as discontinued operations in the Company’s GAAP financial statements.

|

December 31

|

||||||||

|

2012

|

2011

|

2010

|

||||||

|

Estimated Proved Reserves(1)

|

||||||||

|

Developed

|

||||||||

|

Oil (MMBbls)

|

0.3

|

0.4

|

0.5

|

|||||

|

NGL (MMBbls)

|

7.4

|

7.8

|

4.5

|

|||||

|

Natural gas (Bcf)

|

52.3

|

59.6

|

31.1

|

|||||

|

Total proved developed (MMBoe)

|

16.4

|

18.2

|

10.2

|

|||||

|

Undeveloped

|

||||||||

|

Oil (MMBbls)

|

-

|

-

|

-

|

|||||

|

NGL (MMBbls)

|

1.5

|

2.8

|

2.4

|

|||||

|

Natural gas (Bcf)

|

11.1

|

22.0

|

19.2

|

|||||

|

Total proved undeveloped (MMBoe)

|

3.3

|

6.5

|

5.6

|

|||||

|

Total Proved

|

||||||||

|

Oil (MMBbls)

|

0.3

|

0.4

|

0.5

|

|||||

|

NGL (MMBbls)

|

8.9

|

10.6

|

6.9

|

|||||

|

Natural gas (Bcf)

|

63.4

|

81.6

|

50.3

|

|||||

|

Total proved (MMBoe)

|

19.7

|

24.6

|

15.8

|

|||||

|

PV-10 (in millions)(2)

|

$

|

152.8

|

$

|

316.6

|

$

|

197.1

|

||

|

Standardized Measure of Discounted Net Cash Flows (in millions)(3)

|

$

|

152.8

|

$

|

305.2

|

$

|

197.1

|

||

|

(1)The Company’s estimated proved reserves and the future net revenues, PV-10 and Standardized Measure were determined using a 12-month average price for oil and natural gas. The prices used in the Company’s external and internal reserve reports yield weighted average wellhead prices, which are based on index prices and adjusted for transportation and regional price differentials. The index prices and the equivalent weighted average wellhead prices are shown in the table below.

|

|

Index prices

|

Weighted average

wellhead prices

|

||||||||||||||||||

|

Oil

(US$

per Bbl)

|

Natural gas

(US$

per Mcf)

|

NGL realization as a % of Oil

|

Oil

(per Bbl)

|

Natural gas

(per Mcf)

|

Natural gas liquids

(% of oil)

|

||||||||||||||

|

December 31, 2012

|

$

|

94.71

|

$

|

2.76

|

37%

|

$

|

92.63

|

$

|

2.22

|

34%

|

|||||||||

|

December 31, 2011

|

$

|

96.19

|

$

|

4.18

|

53%

|

$

|

89.22

|

$

|

3.46

|

53%

|

|||||||||

|

December 31, 2010

|

$

|

79.43

|

$

|

4.39

|

51%

|

$

|

78.72

|

$

|

3.93

|

53%

|

|||||||||

|

(2)

|

PV-10 is a non-GAAP financial measure and represents the present value of estimated future cash inflows from proved oil and natural gas reserves, less future development and production costs, discounted at 10% per annum to reflect timing of future cash flows and using 12-month average prices for the years ended December 31, 2012, 2011 and 2010. PV-10 differs from Standardized Measure because it does not include the effects of income taxes on future net revenues. Neither PV-10 nor Standardized Measure represents an estimate of fair market value of the Company’s oil and natural gas properties. PV-10 is used by the industry and by the Company’s management as an arbitrary reserve asset value

measure to compare against past reserve bases and the reserve bases of other business entities that is not dependent on the taxpaying status of the entity. The following table provides a reconciliation of the Company’s Standardized Measure to PV-10:

|

|

December 31,

|

||||||||||||||||||||||

|

2012

|

2011

|

2010

|

||||||||||||||||||||

|

(In millions)

|

||||||||||||||||||||||

|

Standardized Measure of Discounted Net Cash Flows

|

$

|

158.8

|

$

|

307.9

|

$

|

197.1

|

||||||||||||||||

|

Present value of future income tax discounted at 10%

|

0.0

|

2.7

|

0.0

|

|||||||||||||||||||

|

PV-10

|

$

|

152.8

|

$

|

305.2

|

$

|

197.1

|

||||||||||||||||

3) Standardized Measure represents the present value of estimated future cash inflows from proved oil and natural gas reserves, less future development and production costs, and income tax expenses, discounted at 10% per annum to reflect timing of future cash flows and using the same pricing assumptions used to calculate PV-10. Standardized Measure differs from PV-10 as Standardized Measure includes the effect of future income taxes.

Undeveloped Reserves

In general, undeveloped reserves are reserves scheduled to be developed within the next three years.

Proved undeveloped reserves have been assigned to the Corporation’s properties.

Proved undeveloped reserves of 3,335 Mboe (56% natural gas) have been assigned in the December 31, 2012 Haas Report, representing 16.9% of the Oklahoma proved reserves on a boe basis. These proved undeveloped reserves represent 22 gross (7.8 net) well locations. All of the locations are in Lincoln County.

The Oklahoma assets provide a large inventory of undeveloped opportunity. As the current undeveloped location inventory is developed, it is anticipated that additional undeveloped locations will be recognized by Haas and added to the undeveloped inventory.

Proved Undeveloped Reserves. The following table summarizes activity associated with proved undeveloped reserves during the periods presented:

|

Year Ended December 31,

|

||||||||||||

|

2012

|

2011

|

2010

|

||||||||||

|

Reserves converted from proved undeveloped to proved developed (MMBoe)

|

1.1

|

1.7

|

0.1

|

|||||||||

|

Drilling capital expended to convert proved undeveloped reserves to proved developed reserves (in millions)

|

$

|

7.8

|

$

|

13.1

|

$

|

1.6

|

||||||

Production and Price History

The following tables set forth information regarding the Company’s net natural gas, NGL and oil production and certain price and cost information for each of the periods indicated.

|

Year Ended December 31,

|

||||||||||

|

2012

|

2011

|

2010

|

||||||||

|

Production Data

|

||||||||||

|

Oil (MBbls)

|

63

|

77

|

82

|

|||||||

|

Natural gas (MMcf)

|

8,272

|

6,373

|

4,363

|

|||||||

|

Natural gas liquids (MBbls)

|

1,182

|

877

|

662

|

|||||||

|

Total volumes (MBoe)

|

2,624

|

2,016

|

1,471

|

|||||||

|

Average daily total volumes (Boe/d)

|

7,186

|

5,523

|

4,030

|

|||||||

|

Average Prices(1)

|

||||||||||

|

Oil (per Bbl)

|

$

|

92.63

|

$

|

89.22

|

$

|

78.72

|

||||

|

Natural gas (per Mcf)

|

$

|

2.22

|

$

|

3.46

|

$

|

3.93

|

||||

|

Natural gas liquids (per Bbl)

|

$

|

31.41

|

47.46

|

41.73

|

||||||

|

Total (per Boe)

|

$

|

23.37

|

$

|

34.98

|

$

|

34.81

|

||||

|

(1)

|

Prices represent actual average prices for the periods presented and do not include effects of derivative transactions.

|

Expenses

|

Year Ended December 31,

|

|||||||||||||

|

2012

|

2011

|

2010

|

|||||||||||

|

Expenses per Boe

|

|||||||||||||

|

Lease operating expenses

|

|||||||||||||

|

Production and transportation

|

$

|

7.78

|

$

|

8.39

|

$

|

7.11

|

|||||||

|

Production taxes(1)

|

$

|

1.43

|

$

|

1.64

|

$

|

1.79

|

|||||||

|

Total operating expenses and ad valorem taxes

|

$

|

9.21

|

$

|

10.03

|

$

|

8.90

|

|||||||

|

(1)

|

Net of severance tax refunds.

|

||||||||||||

Productive Wells

The following table sets forth the number of producing wells in which the Company owned a working interest at December 31, 2012. Gross wells are the total number of producing wells in which the Company has a working interest and net wells are the sum of the Company’s fractional working interests owned in gross wells. A single, non-producing well was owned in Canada as at December 31, 2012.

|

Oil

|

Natural Gas

|

Total

|

|||||||||||||||

|

Gross

|

Net

|

Gross

|

Net

|

Gross

|

Net

|

||||||||||||

|

Oklahoma

|

2

|

0.8

|

124

|

105.2

|

126

|

106.0

|

|||||||||||

Developed and Undeveloped Acreage

The following table sets forth information regarding the Company’s developed and undeveloped acreage at December 31, 2012:

|

Developed Acreage

|

Undeveloped Acreage

|

||||||||||

|

Gross

|

Net

|

Gross

|

Net

|

||||||||

|

Oklahoma

|

54,432

|

44,413

|

29,371

|

9,798

|

|||||||

Many of the leases comprising the undeveloped acreage set forth in the table above will expire at the end of their respective primary terms unless production from the leasehold acreage is established prior to such date, in which event the lease will remain in effect until production has ceased. The following table sets forth as of December 31, 2012 the expiration periods of the gross and net acres that are subject to leases in the undeveloped acreage summarized in the above table.

|

Acres Expiring

|

||||||

|

Gross

|

Net

|

|||||

|

Twelve Months Ending

|

||||||

|

December 31, 2013

|

13,044

|

5,239

|

||||

|

December 31, 2014

|

9,921

|

2,496

|

||||

|

December 31, 2015

|

6,086

|

1,844

|

||||

|

December 31, 2016 and later

|

320

|

219

|

||||

|

Total

|

29,371

|

9,798

|

||||

Drilling Activity

The following table sets forth information with respect to wells the Company completed during the periods indicated. The information presented is not necessarily indicative of future performance, and should not be interpreted to present any correlation between the number of productive wells drilled and quantities or economic value of reserves found. Productive wells are those that produce commercial quantities of hydrocarbons, regardless of whether they produce a reasonable rate of return. Gross wells refer to the total number of wells in which the Company had a working interest and net wells are the sum of the Company’s fractional working interests owned in gross wells. The Company did not drill

any wells it classified as exploratory during this period.

|

2012

|

2011

|

2010

|

||||||||||||||||||||||||||||||||||||||||||||||

|

Gross

|

Drilling Success %

|

Net

|

Drilling Success%

|

Gross

|

Drilling Success%

|

Net

|

Drilling Success%

|

Gross

|

Drilling Success%

|

Net

|

Drilling Success%

|

|||||||||||||||||||||||||||||||||||||

|

Completed Wells

|

||||||||||||||||||||||||||||||||||||||||||||||||

|

Development

|

||||||||||||||||||||||||||||||||||||||||||||||||

|

Productive

|

9.0 | 100 | % | 7.2 | 100 | % | 13.0 | 100 | % | 11.3 | 100 | % | 3.0 | 100 | % | 1.6 | 100 | % | ||||||||||||||||||||||||||||||

|

Dry

|

- | - | - | - | - | - | - | - | - | - | - | - | ||||||||||||||||||||||||||||||||||||

|

Total

|

9.0 | 100 | % | 7.2 | 100 | % | 13.0 | 100 | % | 11.3 | 100 | % | 3.0 | 100 | % | 1.6 | 100 | % | ||||||||||||||||||||||||||||||

Title to Properties

Title to properties is subject to contractual arrangements customary in the oil and gas industry, liens for taxes not yet due and, in some instances, other encumbrances. We believe that such burdens do not materially detract from the value of properties or from the respective interests therein or materially interfere with their use in the operation of the business. As is customary in the industry, other than a preliminary review of local records, little investigation of record title is made at the time of acquisitions of undeveloped properties. Investigations, which generally include a title opinion of outside counsel, are made prior to the consummation of an acquisition of producing properties and

before commencement of drilling operations on undeveloped properties.

Oil, Gas and NGL Marketing

The spot markets for oil, gas and NGLs are subject to volatility as supply and demand factors fluctuate. The Company sells our production under both long-term (one year or more) and short-term (less than one year) agreements at prices negotiated with third parties. Regardless of the term of the contract, the production is all sold at variable, or market-sensitive, prices.

Additionally, we may periodically enter into financial hedging arrangements or fixed-price contracts associated with a portion of our oil, gas and NGL production. These activities are intended to support targeted price levels and to manage our exposure to price fluctuations. See Note 10 to the financial statements included in “Item 8. Financial Statements and Supplementary Data” of this report for further information.

Marketing and Customers

Our production of oil and natural gas is sold to a limited number of customers and the inability to accept our production due to capacity constraints, or a credit default of one of these customers, could have a temporary adverse effect on us. Our revenues are generated under contracts with a limited number of customers. All of the natural gas from our properties is sold to Copano Energy, LLC (formerly Scissortail Energy, LLC) and DCP Midstream, LP. The oil from our properties is sold to ConocoPhillips. Our results of operations would be adversely affected as a result of non-performance by any of our customers. A non-payment default by one of these large customers could have an adverse effect on us,

temporarily reducing our cash flow.

Equal does not have any commitments to deliver fixed and determinable quantities of natural gas, NGLs or oil in the future under existing contracts or sales agreements.

COMPETITION

The Company believes that its leasehold acreage position, concentration of operations, extensive water handling infrastructure and technical and operational capabilities enable it to compete effectively with other exploration and production operations. However, the oil and natural gas industry is intensely competitive, and the Company faces competition from other industry participants.

The Company competes with major oil and natural gas companies and independent oil and natural gas companies for leases, equipment, personnel and markets for the sale of oil and natural gas. Many of these competitors may be financially stronger or weaker than the Company, but generally all competitors can affect the market because of their need to develop and sell oil and natural gas to maintain cash flow. Certain companies may be able to pay more for producing properties and undeveloped acreage. In addition, these companies may have a greater ability to continue exploration activities during periods of low oil and natural gas prices. The Company’s larger or fully integrated competitors may be able to absorb

the burden of existing and any future federal, state and local laws and regulations more easily than the Company can, which would adversely affect its competitive position. The Company’s ability to acquire additional properties and to discover reserves in the future depends on its ability to evaluate and select suitable properties and to consummate transactions in a highly competitive environment. In addition, because the Company has fewer financial and human resources than many companies in its industry, the Company may be at a disadvantage in bidding for exploratory prospects and producing oil and natural gas properties.

SEASONAL NATURE OF BUSINESS

Generally, demand for natural gas and NGL decreases during the summer months and increases during the winter months. Certain natural gas and NGL users utilize natural gas storage facilities and purchase some of their anticipated winter requirements during the summer, which can lessen seasonal demand fluctuations. Seasonal weather conditions and lease stipulations can limit the Company’s drilling and producing activities and other oil and natural gas operations in a portion of its operating areas. For example winter storms and equipment freeze-ups can cause disruption and delays to both drilling activities and ongoing production performance. These seasonal anomalies can pose challenges for meeting the

Company’s well drilling objectives, can delay the installation of production facilities, and can increase competition for equipment, supplies and personnel during certain times of the year, which could lead to shortages and increase costs or delay the Company’s operations.

ENVIRONMENTAL REGULATIONS

General

The exploration, development and production of oil and natural gas are subject to stringent and comprehensive federal, state, tribal, regional and local laws and regulations governing the discharge of materials into the environment or otherwise relating to environmental protection or to employee health and safety. These laws and regulations may, among other things, require permits to conduct drilling, water withdrawal and waste disposal operations; govern the amounts and types of substances that may be disposed or released into the environment; limit or prohibit construction or drilling activities or require formal mitigation measures in sensitive areas such as wetlands, wilderness areas or areas inhabited by

endangered or threatened species; require investigatory and remedial actions to mitigate pollution conditions arising from the Company’s operations or attributable to former operations; impose restrictions designed to protect employees from exposure to hazardous substances; and impose obligations to reclaim and abandon well sites and pits. Failure to comply with these laws and regulations may result in the assessment of sanctions, including monetary penalties, the imposition of remedial obligations and the issuance of orders enjoining operations in affected areas. Pursuant to such laws, regulations and permits, the Company may be subject to operational restrictions and has made, and expects to continue to make, capital and other compliance expenditures.

Increasingly, restrictions and limitations are being placed on activities that may affect the environment. Any changes in environmental laws and regulations or re-interpretation of enforcement policies that result in more stringent and costly construction, drilling, water management, completion, waste handling, storage, transport, disposal, or remediation requirements or emission or discharge limits could have a material adverse effect on the Company. Moreover, accidental releases or spills may occur in the course of the Company’s operations, and there can be no assurance that the Company will not incur significant costs and liabilities as a result of such releases or spills, including any third-party claims

for damage to property and natural resources or personal injury.

The following is a summary of the more significant existing environmental and employee, health and safety laws and regulations applicable to the oil and natural gas industry and for which compliance may have a material adverse impact on the Company.

Hazardous Substances and Wastes

The Company currently owns, leases, or operates, and in the past has owned, leased, or operated, properties that have been used to explore for and produce oil and natural gas. The Company believes it has utilized operating and disposal practices that were standard in the industry at the applicable time, but hydrocarbons and wastes may have been disposed or released on or under the properties owned, leased, or operated by the Company or on or under other locations where these hydrocarbons and wastes have been taken for treatment or disposal. These properties and wastes disposed thereon may be subject to the Comprehensive Environmental Response, Compensation, and Liability Act, as amended

(“CERCLA”), the Resource Conservation and Recovery Act, as amended (“RCRA”) and analogous state laws. Under these laws, the Company could be required to remove or remediate previously disposed wastes, to investigate and clean up contaminated property and to perform remedial operations to prevent future contamination or to pay some or all of the costs of any such action.

CERCLA, also known as the Superfund law, and comparable state laws impose joint and several liability without regard to fault or legality of conduct on certain classes of persons who are considered to be responsible for the release of a “hazardous substance” into the environment. These persons include current and prior owners or operators of the site where the release occurred and entities that disposed or arranged for the disposal of the hazardous substances at the site. Under CERCLA, these “responsible persons” may be subject to strict, joint and several liability for the costs of cleaning up the hazardous substances that have been released into the environment, for damages to natural

resources and for the costs of certain environmental and health studies. In addition, it is not uncommon for neighboring landowners and other third parties to file claims for personal injury, natural resource damage, and property damage allegedly caused by the release of hazardous substances into the environment. CERCLA also authorizes the Environmental Protection Agency (“EPA”) and, in some instances, third parties to act in response to threats to the public health or the environment and to seek recovery from the responsible classes of persons the costs the third parties incur. The Company uses and generates materials in the course of its operations that may be regulated as hazardous substances. To date, no Company-owned or operated site has been designated as a Superfund site, and the Company has not been identified as a responsible party for any Superfund

site.

The Company also generates wastes that are subject to the requirements of RCRA and comparable state statutes. RCRA imposes strict requirements on the generation, transportation, treatment, storage, disposal and cleanup of hazardous and non-hazardous wastes. Drilling fluids, produced waters and other wastes associated with the exploration, production and/or development of crude oil and natural gas are currently exempt from regulation as hazardous wastes under RCRA. However, it is possible that certain oil and natural gas exploration and production wastes now classified as non-hazardous could be classified as hazardous wastes in the future. In September 2010, the Natural Resources Defense Council filed a petition

for rulemaking with the EPA requesting reconsideration of the RCRA exemption for exploration, production, and development wastes. To date, the EPA has not taken any formal action on the petition. Any change in the RCRA exemption for such wastes could result in an increase in costs to manage and dispose of wastes. In the course of the Company’s operations, it generates petroleum hydrocarbon wastes and ordinary industrial wastes that are subject to regulation under the RCRA. The Company believes it is in substantial compliance with all regulations regarding the handling and disposal of oil and natural gas wastes from its operations.

Air Emissions

The Clean Air Act, as amended, the Outer Continental Shelf Lands Act (the “OCSLA”) and comparable state laws and regulations restrict the emission of air pollutants from many sources and also impose various permitting, monitoring and reporting requirements. These laws and regulations may require the Company to obtain pre-approval for the construction or modification of certain projects or facilities expected to produce or significantly increase air emissions, obtain and strictly comply with air permit requirements or utilize specific equipment or technologies to control emissions. Obtaining permits has the potential to delay the development of oil and natural gas projects. The Company may be required

to incur certain capital expenditures for air pollution control equipment or other air emissions-related issues as a result of such requirements. Additionally, violations of lease conditions or regulations related to air emissions can result in civil and criminal penalties, as well as potential court injunctions curtailing operations and canceling leases. Such enforcement liabilities can result from either governmental or citizen prosecution.

In August 2012, the EPA issued final regulations that established new air emission controls for oil and natural gas production and natural gas processing, including, among other things, new source performance standards for volatile organic compounds that would apply to newly hydraulically fractured wells, existing wells that are re-fractured, compressors, pneumatic controllers, storage vessels and natural gas processing plants placed in service after August 2011. However, on January 16, 2013, the EPA made an unopposed motion in federal court to seek an abeyance of legal challenges to the regulations while it reconsiders and potentially revises portions of the new rules. The EPA has also implemented an engine emission

testing program to ensure certain categories of engines, depending on the date manufactured, meet the EPA emission standards. The federal standard for engines manufactured before 2006 also requires emission testing on engines greater than 500 horsepower and strict engine maintenance plans to be in place by October 2013. The Company currently has such maintenance plans in place.

Water Discharges

The Federal Water Pollution Act, as amended (the “Clean Water Act”), and analogous state laws impose restrictions and strict controls regarding the discharge of pollutants into navigable waters. Pursuant to these laws and accompanying regulations, permits must be obtained to discharge produced waters and sand, drilling fluids, drill cuttings and other substances related to the oil and natural gas industry into onshore, coastal and offshore waters of the United States or state waters. Any such discharge of pollutants into regulated waters must be performed in accordance with the terms of the permit issued by the EPA or the analogous state agency. The Clean Water Act and other laws, such as the OCSLA,

require the Company to develop and implement spill response plans intended to prepare the owner of the facility to respond to a hazardous substance or oil discharge. In addition, spill prevention, control and countermeasure requirements under federal law require appropriate containment berms and similar structures to help prevent the contamination of navigable waters or adjoining shorelines in the event of a spill, rupture or leak from an onshore, or offshore, facility. The Clean Water Act and analogous state laws also require individual permits or coverage under general permits for discharges of storm water runoff from certain types of facilities.

The Clean Water Act further imposes certain duties and liabilities on “responsible parties” related to the prevention of oil spills and damages resulting from such spills in, or threatening, U.S. waters. A liable responsible party includes the owner or operator of a facility, vessel, or pipeline that is a source, or a potential threat, of an oil discharge. The Clean Water Act assigns joint and several strict liability, without regard to fault, to each liable party for all containment and oil removal costs and a variety of public and private damages including, but not limited to, the costs of responding to a release of oil, natural resource damages, and economic damages suffered by persons adversely

affected by an oil spill. Although defenses exist to the liability imposed by the Clean Water Act, they are limited. If an oil discharge or substantial threat of discharge were to occur, the Company may be liable for costs and damages, which costs and damages could be material to its results of operations and financial position.

Climate Change

In December 2009, the EPA published its findings that emissions of CO2, methane and certain other greenhouse gases (“GHGs”) present an endangerment to public health and the environment because emissions of such gases are, according to the EPA, contributing to warming of the Earth’s atmosphere and other climatic changes. These findings allow the EPA to adopt and implement regulations that restrict emissions of GHGs under existing provisions of the Clean Air Act. Accordingly, the EPA has adopted rules that require a reduction in emissions of GHGs from motor vehicles and also trigger Clean Air Act construction and operating permit review for GHG emissions from certain stationary sources. EPA’s

endangerment finding and GHG rules were upheld by the United States Court of Appeals for the D.C. Circuit in a June 2012 decision, and a petition for review of the case by the entire D.C. Circuit was denied in December 2012.

The EPA has also adopted rules requiring the reporting of GHG emissions from onshore and offshore oil and natural gas production and processing facilities in the United States on an annual basis. The Company believes it has complied with all applicable reporting requirements to date. However, the adoption and implementation of any regulations imposing reporting obligations on, or limiting emissions of GHG gases from, the Company’s equipment and operations could require it to incur additional costs to reduce emissions of GHGs associated with its operations or could adversely affect demand for the oil and natural gas it produces. Finally, to the extent increasing concentrations of GHGs in the Earth’s

atmosphere may produce climate changes that have significant physical effects, such as increased frequency and severity of storms, droughts, floods and other climatic events. Such events could have a material adverse effect on the Company and potentially subject the Company to further regulation.

In addition, Congress has considered legislation to reduce emissions of GHGs and more than one-half of the states have begun taking actions to control and/or reduce emissions of GHGs, primarily through the adoption of a climate change action plan, completion of GHG emission inventories and/or regional GHG cap and trade programs. Any future federal laws or implemented regulations that may be adopted to address GHG emissions could require the Company to incur increased operating costs, adversely affect demand for the oil and natural gas that the Company produces and have a material adverse effect on the Company’s business, financial condition and results of operations.

Endangered Species

The federal Endangered Species Act (the “ESA”) restricts activities that may affect endangered or threatened species or their habitats. The Company believes its operations are in substantial compliance with the ESA. If endangered species are located in areas of the underlying properties where the Company wishes to conduct development activities or abandonment operations, the work could be prohibited or delayed or expensive mitigation may be required. Moreover, as a result of a settlement approved by the U.S. District Court for the District of Columbia on September 9, 2011, the U.S. Fish and Wildlife Service is required to consider listing more than 250 species as endangered under the ESA. Under

the September 9, 2011 settlement, the federal agency is required to make a determination on listing of the species as endangered or threatened over the six-year period ending with the agency’s 2017 fiscal year. The designation of previously unprotected species as threatened or endangered in areas where underlying property operations are conducted could cause the Company to incur increased costs arising from species protection measures or could result in limitations on its exploration and production activities that could have an adverse impact on its ability to develop and produce reserves.

Employee Health and Safety

The Company’s operations are subject to a number of federal and state laws and regulations, including the federal Occupational Safety and Health Act, as amended (“OSHA”), and comparable state statutes, whose purpose is to protect the health and safety of workers. In addition, the OSHA Hazardous Communication Standard requires that information be maintained concerning hazardous materials used or produced in the Company’s operations and that this information be provided to employees. Pursuant to the Emergency Planning and Community Right-to-Know Act, also known as Title III of the federal Superfund Amendment and Reauthorization Act, businesses that store threshold amounts of chemicals that

are subject to OSHA’s Hazardous Communication Standard must submit information to state and local authorities in order to facilitate emergency planning and response. That information is generally available to the public. The Company believes that it is in substantial compliance with all applicable laws and regulations relating to worker health and safety.

State Regulation

The state in which the Company operates, along with some municipalities and Native American tribal areas, regulate some or all of the following activities: the drilling for, and the production and gathering of, oil and natural gas, including requirements relating to drilling permits, the location, spacing and density of wells, unitization and pooling of interests, the method of drilling, casing and equipping of wells, the protection of fresh water sources, the orderly development of common sources of supply of oil and natural gas, the operation of wells, allowable rates of production, the use of fresh water in oil and natural gas operations, saltwater injection and disposal operations, the plugging and abandonment

of wells and the restoration of surface properties, the prevention of waste of oil and natural gas resources, the protection of the correlative rights of oil and natural gas owners and, where necessary to avoid unfair, unjust or discriminatory service, the fees, terms and conditions for the gathering of natural gas. These regulations may affect the number and location of the Company’s wells and the amounts of oil and natural gas that may be produced from the Company’s wells, and increase the costs of the Company’s operations.

Equal Energy believes that it is, and intends to continue to be, in material compliance with applicable environmental laws and regulations and is committed to meeting its responsibilities to protect the environment wherever it operates or holds working interests. Equal Energy anticipates that this compliance may result in increased expenditures of both a capital and expense nature as a result of increasingly stringent laws relating to the protection of the environment. Equal Energy believes that it is reasonably likely that the trend in environmental legislation and regulation will continue toward stricter standards. The oil and gas industry is subject to regulations that require that well and facility sites be

abandoned and reclaimed to the satisfaction of environmental authorities. As at December 31, 2012, Equal Energy recorded an obligation on its balance sheet of $5.5 million for asset retirement. The Corporation maintains an insurance program consistent with industry practice to protect against losses due to accidental destruction of assets, well blowouts, pollution and other operating accidents or disruptions. The Corporation also has operational and emergency response procedures and safety and environmental programs in place to reduce potential loss exposure. No assurance can be given that the application of environmental laws to the business and operations of Equal Energy will not result in a curtailment of production or a material increase in the costs of production, development or exploration activities or otherwise adversely affect Equal

Energy's financial condition, results of operations or prospects. See “Environmental Risks" and "Industry Conditions" under “Risk Factors”.

Hydraulic Fracturing

Oil and natural gas may be recovered from certain of the Company’s oil and natural gas properties through the use of hydraulic fracturing. Most of Equal’s wells are completed without the use of hydraulic fracturing but the Company may use this completion technique in the future. Hydraulic fracturing, which involves the injection of water, sand and chemicals under pressure into formations to fracture the surrounding rock and stimulate production, is typically regulated by state oil and gas commissions. However, the EPA has asserted federal regulatory authority over certain hydraulic fracturing practices, including the use of diesel, kerosene and similar compounds in the fracturing fluid. In

August 2012, the EPA issued final Clean Air Act regulations governing performance standards, including for the capture of air emissions released during hydraulic fracturing. However, in January 2013 the EPA submitted an unopposed motion to the United States Court of Appeals for the D.C. Circuit seeking to stay legal challenges to the Clean Air Act regulations while it reconsiders portions of the new rules. Also, federal legislation previously was introduced, but not enacted, to provide for federal regulation of hydraulic fracturing and to require disclosure of the chemicals used in the fracturing process. In May 2012, the Bureau of Land Management within the U.S. Department of the Interior issued a proposed rule containing disclosure requirements and other mandates for hydraulic fracturing on federal lands, but in January 2013 it announced that it would be submitting a revised rule

proposal. That revised proposal is expected to be published in the first quarter of 2013.

If new laws or regulations that significantly restrict hydraulic fracturing are adopted at either the state or federal level, the Company’s fracturing activities could become subject to additional permit requirements, reporting requirements or operational restrictions and also to associated permitting delays and potential increases in costs. These delays or additional costs could adversely affect the determination of whether a well is commercially viable. Restrictions on hydraulic fracturing could also reduce the amount of oil and natural gas that the Company is ultimately able to produce in commercial quantities.

In addition to asserting regulatory authority, a number of federal entities are analyzing, or have been requested to review, a variety of environmental issues associated with hydraulic fracturing. In April 2012, President Obama issued an executive order that established a working group for the purpose of coordinating policy, information sharing and planning across federal agencies and offices regarding “unconventional natural gas production,” including hydraulic fracturing. In December 2012, the EPA issued an initial progress report on a study begun in 2011 of the potential environmental effects of hydraulic fracturing on drinking water and groundwater, with a final report expected to be issued in late

2014. The EPA has also announced an intent to propose by 2014 effluent limit guidelines that waste water from shale gas extraction operations must meet before going to a treatment plant; the agency also projects that it will publish an Advance Notice of Proposed Rulemaking regarding the Toxic Substances Control Act reporting of the chemical substances and mixtures used in hydraulic fracturing. Additionally, a committee of the United States House of Representatives has conducted an investigation of hydraulic fracturing practices, and certain members of Congress have called upon the U.S. Government Accountability Office to investigate how hydraulic fracturing might adversely affect water resources; the SEC to investigate the natural gas industry and any possible misleading of investors or the public regarding the economic feasibility of pursuing natural gas deposits in shales by means of

hydraulic fracturing; and the U.S. Energy Information Administration to provide a better understanding of that agency’s estimates regarding natural gas reserves, including reserves from shale formations, as well as uncertainties associated with those estimates. The studies and initiatives described above, depending on their degree of pursuit and any meaningful results obtained, could spur efforts to further regulate hydraulic fracturing under the Safe Drinking Water Act or other regulatory mechanisms.

The Company reviews best practices and industry standards and complies with all regulatory requirements in the protection of potable water sources. Protective practices include, but are not limited to, setting multiple strings of protection pipe across the potable water sources and cementing these pipes from setting depth to surface, continuously monitoring the hydraulic fracturing process in real time and disposing of all non-commercially produced fluids in certified disposal wells at depths below the potable water sources.

OTHER REGULATION OF THE OIL AND NATURAL GAS INDUSTRY

The oil and natural gas industry is extensively regulated by numerous federal, state, local, and regional authorities, as well as Native American tribes. Legislation affecting the oil and natural gas industry is under constant review for amendment or expansion, frequently increasing the regulatory burden. Also, numerous departments and agencies, both federal and state, and Native American tribes are authorized by statute to issue rules and regulations affecting the oil and natural gas industry and its individual members, some of which carry substantial penalties for noncompliance. Although the regulatory burden on the oil and natural gas industry increases the Company’s cost of doing business and,

consequently, affects its profitability, these burdens generally do not affect the Company any differently or to any greater or lesser extent than they affect other companies in the industry with similar types, quantities and locations of production.

The availability, terms and cost of transportation significantly affect sales of oil and natural gas. The interstate transportation and sale for resale of oil and natural gas is subject to federal regulation, including regulation of the terms, conditions and rates for interstate transportation, storage and various other matters, primarily by the Federal Energy Regulatory Commission (“FERC”). Federal and state regulations govern the price and terms for access to oil and natural gas pipeline transportation. The FERC’s regulations for interstate oil and natural gas transmission in some circumstances may also affect the intrastate transportation of oil and natural gas.

Sales of oil and natural gas are not currently regulated and are made at market prices. Although oil and natural gas prices are currently unregulated, Congress historically has been active in the area of oil and natural gas regulation. The Company cannot predict whether new legislation to regulate oil and natural gas might be proposed, what proposals, if any, might actually be enacted by Congress or the various state legislatures, and what effect, if any, the proposals might have on the Company’s operations.

Drilling and Production

The Company’s operations are subject to various types of regulation at federal, state, local and Native American tribal levels. These types of regulation include requiring permits for the drilling of wells, drilling bonds and reports concerning operations. Most states, and some counties, municipalities and Native American tribal areas where the Company operates also regulate one or more of the following activities:

|

•

|

the location of wells;

|

|

•

|

the method of drilling and casing wells;

|

|

•

|

the timing of construction or drilling activities;

|

|

•

|

the rates of production, or “allowables”;

|

|

•

|

the use of surface or subsurface waters;

|

|

•

|

the surface use and restoration of properties upon which wells are drilled;

|

|

•

|

the plugging and abandoning of wells; and

|

|

•

|

the notice to surface owners and other third parties.

|