Attached files

| file | filename |

|---|---|

| EX-3.3 - EX-3.3 - Oryon Technologies, Inc. | d498377dex33.htm |

| EX-32.2 - EX-32.2 - Oryon Technologies, Inc. | d498377dex322.htm |

| EX-31.2 - EX-31.2 - Oryon Technologies, Inc. | d498377dex312.htm |

| EX-31.1 - EX-31.1 - Oryon Technologies, Inc. | d498377dex311.htm |

| EX-23.1 - EX-23.1 - Oryon Technologies, Inc. | d498377dex231.htm |

| EX-32.1 - EX-32.1 - Oryon Technologies, Inc. | d498377dex321.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

(Amendment No. 1)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2012

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 001-34212

ORYON TECHNOLOGIES, INC.

(Exact name of registrant as specified in its charter)

| Nevada | 26-2626737 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification Number) |

4251 Kellway Circle, Addison, Texas 75001

(Address of principal executive offices)

(214) 267-1321

(Registrant’s telephone number, including area code)

Securities Registered Pursuant to Section 12(b) of the Act

None

Securities Registered Pursuant to Section 12(g) of the Act

Common Stock, Par Value $0.001 Per Share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of the Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definition of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | x | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the registrant’s outstanding Common Stock held by non-affiliates of the registrant computed by reference to the price at which the Common Stock was last sold as of the last business day of the registrant’s most recently completed second fiscal quarter was $15,071,856.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date: As of March 7, 2013, there were 62,660,778 shares of common stock, par value $0.001 per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None

Table of Contents

EXPLANATORY NOTE

Oryon Technologies, Inc. is filing this Amendment No. 1 to its Annual Report on Form 10-K that was originally filed with the Securities and Exchange Commission (the “SEC”) on February 27, 2013, to include a description of certain provisions of its Amended & Restated Bylaws in Item 9B, which Amended & Restated Bylaws are filed as Exhibit 3.3 hereto.

Table of Contents

1

Table of Contents

| ITEM 14 | PRINCIPAL ACCOUNTING FEES AND SERVICES | 56 | ||

| PART IV | ||||

| ITEM 15 | EXHIBITS AND FINANCIAL STATEMENT SCHEDULES | 57 | ||

| SIGNATURES | ||||

2

Table of Contents

Cautionary Notice Regarding Forward-looking Statements

This Annual Report on Form 10-K contains certain “forward-looking” statements (as such term is defined in Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and the Private Securities Litigation Reform act of 1995) and information relating to the Registrant and its subsidiaries that are based upon beliefs of, and information currently available to, the Registrant’s management as well as estimates and assumptions made by the Registrant’s management. When used in this report, the words “anticipate,” “believe,” “estimate,” “expect,” “future,” “intend,” “plan,” “project,” “continuing,” “ongoing,” “may,” “will,” “should,” “could,” or the negative of these terms and similar expressions as they relate to the Registrant or the Registrant’s management, are intended to identify forward-looking statements. Such statements reflect the current view of the Registrant with respect to future events and are subject to risks, uncertainties, assumptions and other factors (including the risks contained in the section of this Annual Report on Form 10-K entitled “Risk Factors”) relating to the Registrant’s industry, the Registrant’s operations and results of operations and any businesses that may be acquired by the Registrant. Should one or more of these risks or uncertainties materialize, or should the underlying assumptions prove incorrect, actual results may differ significantly from those anticipated, believed, estimated, expected, intended or planned.

Although the Registrant believes that the expectations reflected in the forward-looking statements are reasonable, the Registrant cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the securities laws of the United States, the Registrant does not intend to update any of the forward-looking statements to conform these statements to actual results. The following discussion should be read in conjunction with the Registrant’s financial statements and the related notes filed herewith.

History of the Company

In the late 1990’s, EL Specialists, Inc. (“ELS”), a company organized under the laws of Texas, the predecessor company of Oryon, engineered a technological breakthrough and developed a three dimensional, elastomeric, membranous lamp that eliminated the semi-rigid nature of conventional electroluminescent (“EL”) lamps. ELS patented and trademarked this process under the name Elastolite®.

Elastolite® was created to replace conventional EL with a highly malleable, flexible, and economical elastomeric EL lamp technology that could be applied directly to fabrics for safety purposes. This concept required lamps that were ultra-thin, extremely flexible, washable, crushable, formable, elastic, and heat resistant. To accomplish this formidable goal, the ink formulas and manufacturing processes of conventional EL would need to be restructured.

In 2002, MRM Acquisitions, LLC, a company organized under the laws of Texas (“MRMA”), acquired the patents and intellectual property (“IP”) of ELS and began preparing Elastolite® for commercialization.

In addition to the textile and related apparel applications for which it was invented, Elastolite® opened multiple new and innovative opportunities for EL lighting in membrane switches, keypads, compression-molded plastics, athletic apparel, toys, occupational safety, point-of-sale displays, automotive and household utilitarian and decorative applications. In addition, the acquired IP also contained innovative patents in the biometric field that management believes, when it is developed, will permit the launch of multiple, high volume, cost effective biometric applications.

In October 2002, OryonTechnologies, LP, a limited partnership formed under the laws of the State of Texas, was formed as the operating company charged with exploiting and commercializing the acquired technology. In October 2004, OryonTechnologies, LP was converted to a limited liability company, OryonTechnologies, LLC, a Texas limited liability company (“Oryon”), and MRMA subsequently exchanged all the IP and patents held by MRMA for membership units of Oryon. Oryon spent its first years preparing Elastolite® to be marketed.

In management’s opinion, Oryon created the framework to commercialize and successfully launch Elastolite® through multiple innovations Oryon developed through market testing during the years 2003 through 2011. Oryon test marketed Elastolite® in clothing with Marmot Mountain Ltd (2004) and with Lands’ End in over 100,000 lit textile products (2006). While the test marketing provided Oryon with technical information leading to the improvement of its technology, insufficient funding prevented Oryon from capitalizing on the resulting new product developments and

3

Table of Contents

Oryon was unable to sustain the relationship with the early customers. In addition, Oryon licensed the technology to Rogers Corporation to light cell phone keypads which ultimately resulted in the Motorola Razr cell phone which sold over 100,000,000 units (2006-2009) and produced over $8,000,000 in revenues to Oryon. Subsequent innovations in smart phone and touch screen technologies have eliminated the large market for more expensive keypad-type cellphones that utilized Oryon’s technology.

In 2008, Oryon granted a license to a Fortune 100 company in the field of occupational safety, spent over a year developing and qualifying Elastolite® and the Elastolite® electronic system for apparel with a leading global sports apparel with the company’s advanced innovation team for product launch in 2009-10, and received the first volume production order from them in 2009. Further, Oryon produced light for costumes used by Disney in the December 2010 3-D release of the movie Tron Legacy, established a relationship with Disney Consumer Products (“DCP”) and has worked with a leading U.S. department store as well as Adidas, Puma and Under Armour, among others, in the development of lit products. However, without sufficient funding to be able to deliver Elastolite® to fulfill large orders, Oryon did not aggressively pursue major transactions with such customers. As a result of the completed Merger (defined below), the Company has capital resources to re-engage with previous customers and prospects to develop additional product applications utilizing the Company’s most updated technology and techniques, although additional capital will be required to enable the Company to fulfill large orders that might result from such re-engagement.

Based on the successful market testing and customer acceptance of the innovations developed by Oryon in the commercialization process of Elastolite® in the apparel (including sports apparel and shoes), textile, safety and gear markets, Oryon felt it would be ready to commercially launch Elastolite® in 2009. Consequently, in the summer of 2008, it hired an investment banker to raise the capital that would be required to support the launch of Elastolite® and to provide the time for Oryon’s Fortune 100 and 500 potential customers to incorporate it in their product development process.

Financial offering materials were prepared and a fund raising process was initiated in September 2008. Unfortunately, at that same time the deepening US financial crisis and the difficult economic environment made the financing process untenable. Oryon subsequently did not have the funds required to support the development of new products in conjunction with its customers. Management did not want its customers to launch products at a time when Oryon could not provide effective and timely customer support. In addition, the Motorola Razr cell phone was approaching its end-of-life as a product and future revenue from this source could not be counted on. Management of Oryon therefore began to take steps to (a) reduce overhead, (b) continue application development for potentially high volume future products, (c) hold and maintain its major customers until adequate funding was available to launch product with them and (d) maintain barriers to entry (Oryon’s extensive patent portfolio) for potential competition until adequate financial resources could be raised.

To accomplish the above, Oryon raised capital through the issuance of convertible notes primarily to angel investors, raising investment capital of $888,000 in late 2008 and 2009, $1,000,000 in December 2009 and early 2010, and $560,000 in 2011. The merger with the Registrant, the potential financial resources it can provide, both private and public, and access to the public financing market may provide an opportunity for Oryon to successfully launch Elastolite®, building upon the experience and customer relationships developed during the years 2008-2011.

Background of Transaction

The Registrant was organized under the laws of the State of Nevada on August 22, 2007 to explore mineral properties under the name “Eaglecrest Resources, Inc.” The Registrant was formed to engage in the exploration of mineral properties for gold. The Registrant had not generated any revenue from its business operations prior to the closing of the Merger, and the Registrant had been unable to raise sufficient funds to implement its operations.

As a result of the current difficult economic environment and the Registrant’s lack of funding to explore mineral properties, in 2011, the Registrant’s Board of Directors began to analyze strategic alternatives available to the Registrant to continue as a going concern. Such alternatives included raising additional debt or equity financing or consummating a merger or acquisition with a partner that may involve a change in the Registrant’s business plan. Through an introduction by an investment firm, Balanced Financial Securities, the Board of Directors identified Oryon as a potential strategic acquisition that the Board believed to be in the best interest of the Registrant and its shareholders. Oryon was attractive to the Registrant because it is a technology company with certain valuable products and intellectual property rights and has plans to grow its business. Oryon believed the Registrant to be an attractive business combination partner, due in part, to the perceived benefits of being a publicly registered company, allowing for increased access to capital. Accordingly, the parties entered into a letter of intent with respect to the Merger on October 24, 2011, executed the Merger Agreement on March 9, 2012, and closed the Merger on May 4, 2012.

4

Table of Contents

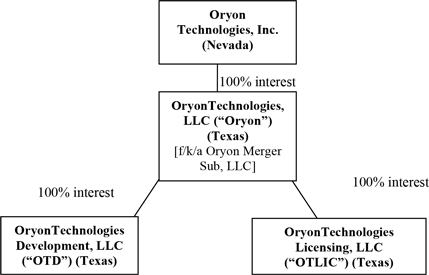

Corporate Structure

As a result of the Merger, the organizational structure of the Registrant is as follows:

Subsidiaries

As noted in the diagram above, the Registrant owns 100% of the membership interest of Oryon, which then owns:

| • | 100% of the membership interest of OryonTechnologiesDevelopment, LLC (“OTD”), a company organized under the laws of Texas. OTD currently conducts sales, customer relations, R&D and product development for Oryon. Oryon is evaluating whether to merge OTD into Oryon. |

| • | 100% of the membership interest of OryonTechnologies Licensing, LLC (“OTLIC”), a company organized under the laws of Texas. OTLIC currently conducts all licensing for Oryon. Oryon is evaluating whether to merge OTLIC into Oryon. |

Previously, Oryon owned 100% of Oryon Technologies International Pte, Ltd. (“OTI”), a company organized under the laws of Singapore that was liquidated in November 2012. The operations of OTI were not material to Oryon. OTI was officially deregistered in Singapore on November 6, 2012. In addition, Oryon owned 51% of Oryon Asia Pacific Safety, Ltd. (“OAPS”), a company organized under the laws of Hong Kong that is in the final stage of liquidation. The operations of OAPS were not material to Oryon.

In summary, although there are various subsidiaries and affiliates currently in existence, Oryon is in the process of streamlining and restructuring the Registrant by dissolving or merging them. The Registrant has only one subsidiary – Oryon. At Closing, Oryon was merged into Merger Sub, which had no corporate purpose other than to serve as the merger receptacle facilitating the transaction.

Strategy

Oryon acquired and continued to develop and patent an already highly patented and innovative next-generation technology in EL light. Oryon’s patented technology, trademarked Elastolite®, enables thin, flexible, malleable, crushable, water resistant lighting systems to be incorporated into many product applications in multiple markets that would not be feasible or, in some cases, even possible with current lighting technology. Elastolite® and its operating system, including electronics and harness, has been market tested and validated and is ready to be launched in support of its multiple market opportunities.

To take advantage of what management considers are its multiple market opportunities, Oryon intends to raise additional capital to support its growth strategy and its existing pipeline of opportunities. Even if successful in its capital formation efforts, Oryon will still not be able to take advantage of all the opportunities that now present themselves.

5

Table of Contents

Oryon recognized during the commercialization process that Elastolite’s strength of being a platform technology for multiple applications in numerous industries can also be its weakness. Due to the immense size and divergent requirements of the multiple industries Oryon can target, Oryon must focus and initially limit the applications and industries in which it can make the most immediate impact. In this manner it can optimize its resources and more readily leverage the positive results it achieves.

Oryon will initially focus its efforts on apparel, textiles, shoes and subsequently membrane switches. It, therefore, will evaluate its current opportunities and select those customer applications which are presently within Oryon’s core technical competence and that present Oryon with both high level volume and profit potential. Oryon feels opportunities are presently available in the apparel, safety-apparel, textile and membrane switch industries.

To the extent there is adequate available capital, Oryon intends to (i) support its existing pipeline of opportunities in its target markets with additional application and technical transfer engineers and customer service personnel and (ii) take advantage of new, but previously identified, market opportunities in apparel, textiles and shoes. Once traction is achieved in its initial target markets, and planned development of new opportunities are completed, Oryon will attempt to expand into other targeted opportunities that presently exist with lit molded product applications such as laptop keypads, remote controls, toys, lit cycling and biking helmets, lit cell phone cases and multiple automotive opportunities. Subsequently, other opportunities in the following fields will be evaluated at a later date: point-of-sale, outdoor displays, security systems, household furnishings, decorative floorings, various military applications and molding in all of the above.

Apparel, Textiles, Shoes and Gear: Within Oryon’s target textile markets, billions of units are shipped each year. This market includes outerwear, industrial safety, municipal safety, military, athletic apparel, men’s, women’s and children’s clothing, shoes and gear. These markets generate over $250 billion annual revenues and are second in size only to the food industry.

When Oryon originally purchased patents for a new evolutionary EL lamp, trademarked Elastolite®, the technology, although functional in the lab, had never been commercially developed or validated. Oryon needed to obtain corroboration on the soundness of its lamp system on a commercial level. Oryon determined that its initial marketing with Elastolite® should be in the apparel, textile, shoe and gear markets. In 2004, Oryon began, through normal commercial relationships between itself and its customers, testing the validity of its lamp system with multiple companies in multiple markets relating to textiles. Oryon obtained the market corroboration and validation in the apparel, textile and gear arena through its test marketing of Elastolite® in over 100,000 apparel and gear items sold by Marmot Mountain and Lands’ End; through its work with the innovation team of a leading Fortune 500 sports apparel brand; by lighting the costumes for the Disney film Tron Legacy that was released in December 2010 and through its relationship with its Fortune 100 licensee in occupational safety products. Based on Elastolite® being sold by these companies in their products to consumers, used promotionally by these companies promoting their own products and by working with the development teams and factories from most of the companies that used Elastolite®, Oryon was not only able to corroborate its technology in the uses for which it was intended, but also able to make additional improvements to the Elastolite® system. Until Oryon raised adequate capital to support a larger customer base, it elected not to pursue active further development of products with the companies mentioned above.

Now that additional capital has been raised by Oryon, and Elastolite® is ready to be commercially launched, Oryon is now actively working with leading companies in their respective fields in apparel, textiles and gear and selectively re-engaging the companies mentioned above. Oryon will attempt to both grow and leverage these relationships. Product development time cycles with the larger global companies ranges between 12 and 18 months and with the smaller companies in a 6 to 8 month time cycle. Oryon believes that revenue, other than revenue generated from product development with these companies, will begin in the 2nd quarter 2013 and increase throughout 2013 and thereafter. Oryon will build a marketing, sales and customer service team in addition to application engineering and research and development teams that will both service and exploit existing customers and develop and manage new prospects and projects within each segment of the apparel and textile market it undertakes. At present, Oryon’s marketing, business development and customer service team is comprised of two people and Oryon plans to hire several additional people to this team as the customer base is expanded. Oryon currently has five people engaged in its engineering and research and development team and plans to add incremental personnel as the client base increases.

Expansion of its application engineering and research and development teams will be critical to the future success of Oryon. A large percentage of Oryon’s operating expense is incurred upfront in the product cycle when Oryon engineers work with Oryon customers in their product development. Further Oryon engineering man power is also needed once an order has been received (prototype or volume) when Oryon transfers its technology to the customer’s factories. Without this added engineering support, Oryon will be limited in the rate of growth of its volume.

6

Table of Contents

As sales opportunities present themselves, Oryon will also expand its marketing and customer support teams. These teams will not only develop new customers and customer opportunities but will spend time interfacing between Oryon customers and Oryon engineering staff.

As of the current date, Oryon is actively working a prospect pipeline that management believes represents significant sales opportunities in the apparel and textile markets.

The timeline to market for major brands is approximately 12 to 18 months from inception of product development to shipment to retailer. While the sports apparel markets are prime targets for Oryon, Oryon will simultaneously develop the occupational safety and corporate identity markets which have a much shorter timeline to revenue. Oryon will establish strategic distribution and manufacturing relationships in the safety markets through which lit safety and corporate identity products will be sold.

Oryon is currently building the infrastructure and scalability required to service its customers in the apparel industry and to have the capability to expand its capacity to serve these customers as opportunities present themselves.

Membrane Switches, Gauges and Keypads: The primary applications in this target segment include cell phones and cell phone cases, appliances, remote controls, telecom equipment, medical instrumentation, industrial controls, gauges of all types and keypads. Oryon will hire marketing and sales management to work directly with large customers in these markets and manage the contract sales organizations that Oryon will utilize that are regionally focused and have existing channels and relationships that Elastolite® technology can leverage, complement and extend.

Compression and In-Molded Products: In late 2007, Oryon began testing the feasibility of in-molding and compression molding its lamps. Together with a significant international chemical company, Oryon lamps were successfully shaped and in-molded. To Oryon’s knowledge, Elastolite® is the only lamp technology that has been successfully in-molded. The success of this experiment opens up multiple applications such as lit cell phone cases, toys, in-molded lit keypads and decorative molding on many products. Oryon will actively continue its development of this technology for commercialization and launch the new technology as soon as traction is built in apparel, textiles, membrane switches and keypads.

Oryon will initially execute its growth strategy in its target markets as follows:

| • | Oryon will develop its existing brand name with targeted customers in specific markets through direct sales, strategic relationships and/or licensing. Oryon’s existing targeted customers are principally established brands or retailers with proven revenue streams, known channels of distribution and consumer acceptance. Oryon will simultaneously develop the occupational safety and corporate identity markets that have a much shorter timeline to revenue. |

| • | In parallel, Oryon will create a highly adaptive licensing or strategic relationship model for both manufacturing and selling Elastolite®. |

| • | Oryon will build the needed sales infrastructure, both internal and external that will be responsible for working with sales prospects to develop specifications for product prototypes and co-develop new product applications. |

| • | Oryon will build an infrastructure of supporting companies (approved suppliers) with capabilities that will permit Oryon to become a solution provider to its strategic partners, customers and licensees in each of the market segments it undertakes. |

| • | Oryon will continually evaluate and expand the intellectual property and patent portfolio that will permit and enable its future growth and market opportunities. |

As Oryon gains traction in its initial focus markets, it will gradually begin expanding into new market segments it has identified, such as in-molded products, membrane switches, point-of-sale, toys, automotive and military. Oryon will seek industry partners to either co-develop or license Elastolite® technology in promising new high technology fields that require extended developmental time horizons. Such fields include biometric fingerprint sensors in which Oryon holds two patents, high speed roll-to-roll printing that may permit Oryon to offer cost effective solutions for such product as floor lighting and printed flexible batteries. These new technological developments may provide expansive future growth opportunities for Oryon.

7

Table of Contents

Revenues and Capital Requirements

Oryon’s historical revenues have been minimal as the focus has been on product development. Past revenues were principally generated through the following:

| • | Market tests with Lands’ End and Marmot Mountain Ltd.; |

| • | Running jacket with leading Fortune 500 sports apparel brand; |

| • | Royalty from Rogers Corporation generated by the backlighting of the keypad of the Motorola RAZR cell phone |

| • | Prototypes created for prospective customers; and |

| • | Revenue generated by lighting the costumes for Disney’s movie Tron Legacy. |

Oryon believes it will require additional capital in the future. It is currently developing a specific multi-year fundraising plan based on the following considerations:

| • | The identification of potential new markets for our products; |

| • | Projected short and long term revenues and profits; |

| • | Personnel required to properly service its projected future sales; and |

| • | Future requirement for capital expenditures. |

See “Management’s Discussion and Analysis of Financial Condition and Results of Operations: Liquidity and Capital Resources”.

Technology

Oryon, utilizing polymer thick film technology, has created a new generation EL lamp. Oryon’s technology has created an elastomeric lamp that is capable of being placed on and over three dimensional shapes that require a high level of malleability in operation or performance. Traditional EL technologies require the EL lamp to be manufactured, or printed, on an indium tin oxide sputtered polyester foundation, which creates a semi-rigid structure. This structure is highly susceptible to both moisture and stress. Oryon’s patented innovation eliminates all rigid and semi-rigid materials used in constructing a traditional EL lamp and replaces those materials with membranous films, creating an elastomeric and membranous lamp that can be printed on many different surfaces. This breakthrough has opened multiple new and innovative opportunities for EL lighting in textiles and related apparel, membrane switches, keypads, toys, safety products, point of sale displays, automotive and household utilitarian and decorative applications and gear. Further, Oryon’s technology permits light to be printed only where it is needed on a cost effective basis.

Management of the Registrant believes that Elastolite®, Oryon’s trademarked electroluminescent lamp, is a disruptive platform lighting technology. Unlike reflective tapes, an electroluminescent lamp emits light by the direct conversion of electrical energy into light through energized phosphors. Although electroluminescent lamp technology is not new, Elastolite® broke through restrictive barriers previously existing that limited the growth of electroluminescent technology:

| • | Elastolite® is a unique form of electroluminescent lamp |

| • | Elastolite® is 3-dimensional, elastomeric, membranous Polymer Thick Film (PTF) |

| • | Elastolite® can be printed directly on almost any surface |

| • | Elastomeric is a polyurethane ink structure |

8

Table of Contents

Advantages of Elastolite®

|

|

|

|

|

|||||

| Edmund Castillo | Disney/Adidas | Occupational Safety | Life Preserver |

1. Edmundo Castillo – The Edmundo Castillo shoe shown above is currently being produced by Edmundo Castillo, a leading maker of couturier shoes, with plans for delivery to stores for 2013.

2. Disney/Adidas – The Adidas sneakers shown above were sneakers provided by Adidas and lit by Oryon for promotion of Disney’s movie Tron Legacy. They were displayed at Comic-Con in 2010. Adidas, Disney and Oryon worked together on this promotion. These shoes were sold at a charity event sponsored by Disney.

3. Occupational Safety – The occupational safety jacket above is not in the market. It was developed by Oryon to show potential customers the safety advantages of lighting occupational safety apparel for occupational safety workers such as police, fire, EMS, construction workers, etc.

4. Life Preservers – The life preserver shown above is a mockup demonstrating the added safety feature Elastolite® can bring to boaters or people working in a water environment. The life preserver is not currently in the market.

The above characteristics permit Oryon’s Elastolite® to be advantageously positioned alongside other lighting technologies such as traditional EL and light emitting diode (“LED”) technology. Oryon believes Elastolite® offers multiple advantages over existing light technologies such as:

| • | Water Resistant – Elastolite®, unlike LED’s and traditional EL lamps, is an all-weather lamp. Although it is not, in its natural state, totally waterproof, it is highly water resistant. It can be machine washed and dried. Unlike competitive lighting sources, it is a natural addition to any article of clothing, gear, or safety related product that is used or worn in an outdoor environment or to most outdoor displays where resistance to adverse weather is required. |

| • | Elastomeric and Moldable – Elastolite® is 3-Dimensional. Unlike traditional EL lamps or LED’s, it can stretch, bend, fold or literally be united with almost any application where flexibility and malleability are important. Elastolite® is extremely thin. The thinness and elastomeric malleable characteristics permit Elastolite® to be applied or printed to clothing where movement and comfort are important or it could, with some additional development, be placed directly under or in-molded into individual keys on keypads or push buttons on membrane switches thereby maintaining a tactile feel while providing a uniform high quality light literally unobtainable by competing light sources. |

| • | Durable – Distinct from traditional EL, due to its elastomeric, membranous and homogenous polyurethane structure, Elastolite® will not crease or break when folded, bent or compression molded. It can withstand both heat and cold, yet generates no heat of its own. In switch and keypad applications it has successfully been tested to over 10,000,000 actuations. These characteristics permit Elastolite® to be molded, used directly under laptop and membrane switch keypads, withstand the rigors clothing applications require and survive uses on outdoor applications such as outdoor displays, equipment, and rainwear in addition to multiple military applications. |

| • | Economical – Elastolite®, although capable of being created with thermally cured inks, is principally built based on Ultra Violet (“UV”) cured inks. This permits Elastolite® to be printed on high speed roll-to-roll printing equipment and can eliminate costly elongated thermal heating equipment required by traditional EL lamp systems. Additionally, as opposed to printing on an ITO PET substrate like traditional EL, Elastolite® can be printed on most substrates and printed only where light is needed thereby eliminating wasted materials and integration and assembly labor. Oryon’s membrane switch patents also eliminate most all hand assembly required when building a membrane switch. |

9

Table of Contents

| • | Moldable – Elastolite® can be in-molded or compression molded into or onto plastics. Because of the durable and elastomeric advantages described above, Elastolite® can withstand the pressure, heat and deformation required when in-molding it into plastic applications. This opens up multiple potential applications such as lit cell phone cases, lit logos on company products, and lit decorative effects printed with graphics on multiple plastic products. It permits light to take the shape of the product or application onto which it is placed. |

| • | Uniform Light – Elastolite® is a blanket uniform light as opposed to a LED point light. Although not as bright as an LED; in poor visibility or at night, it can be seen more easily. Since the light can be placed directly where light is needed, the resulting effort is a uniform high quality light thereby enhancing the value of any product where quality of light and image is important. |

Because of its unique characteristics and competitive advantages, Oryon believes Elastolite® is an enabling technology that allows new and innovative uses of light in product applications in which light, using any other lighting technology, previously was not practical or cost effective. Unlike other lighting technologies, due to its elastomeric, durable and cost effective features and thereby its ability to be folded, crushed, molded, and washed, Elastolite® opens up the possibility of multiple breakthrough innovative applications spanning numerous industries.

Intellectual Property

Oryon’s intellectual property (“IP”) position has provided the company with a strong competitive position. As of December 31, 2012, Oryon had 57 patents considered by management to be material, including 18 U.S. patents (all issued and none pending) and 39 international patents (32 issued and 7 pending). Oryon’s core patents are not related directly to specific products, but instead relate to technical processes, manufacturing methods, materials and other aspects of Oryon’s Elastolite® technology, including, for example, producing a lamp in a membranous form, the use of UV cured inks in a membranous lamp, construction of a lit membrane switch through a continuous printing methodology and others related to the manufacturing or construction of the lamps. Oryon has two biometric patents that Oryon management believes, when they are developed, will permit the launch of multiple, high volume, cost effective biometric applications. The following table lists Oryon’s patents, both issued and pending, the jurisdictions in which they were filed, the dates issued and the expiration dates.

| Name |

Jurisdiction |

Issue Date or Pending |

Expiration Date | |||

| Addressable PTF Receptor for Irradiated Images (Biometrics) |

US | 8/30/2005 | 12/21/2021 | |||

| Addressable PTF Receptor for Irradiated Images (Biometrics) |

Germany | Pending | 12/21/2021 | |||

| Alerting System Using Elastomeric EL Lamp Structure |

US | 8/7/2001 | 12/30/2016 | |||

| Alerting System Using Elastomeric EL Lamp Structure |

Taiwan | 4/15/2002 | 1/11/2021 | |||

| Deployment of EL Structures on Porous or Fibrous Substrates |

US | 4/22/2003 | 5/30/2016 | |||

| Elastomeric EL Lamp on Apparel |

US | 10/30/2001 | 10/15/2018 | |||

| Elastomeric Electroluminescent Lamp |

US | 1/5/1999 | 12/30/2016 | |||

| Elastomeric Electroluminescent Lamp |

South Korea | 8/21/2001 | 12/22/2017 | |||

| Elastomeric Electroluminescent Lamp |

Australia | 3/22/2001 | 12/22/2017 | |||

| Elastomeric Electroluminescent Lamp |

Belgium | 6/2/2010 | 12/22/2017 | |||

| Elastomeric Electroluminescent Lamp |

France | 6/2/2010 | 12/22/2017 |

10

Table of Contents

| Elastomeric Electroluminescent Lamp |

Great Britain | 6/2/2010 | 12/22/2017 | |||

| Elastomeric Electroluminescent Lamp |

Italy | 6/2/2010 | 12/22/2017 | |||

| Elastomeric Electroluminescent Lamp |

Netherlands | 6/2/2010 | 12/22/2017 | |||

| Elastomeric Electroluminescent Lamp |

Canada | 3/29/2005 | 12/22/2017 | |||

| Elastomeric Electroluminescent Lamp |

Germany | 6/2/2010 | 12/22/2017 | |||

| Elastomeric Electroluminescent Lamp |

Spain | 6/2/2010 | 12/22/2017 | |||

| Elastomeric Electroluminescent Lamp |

Hong Kong | 10/29/2010 | 12/22/2017 | |||

| Elastomeric Electroluminescent Lamp |

Mexico | 10/8/2003 | 12/22/2017 | |||

| Electroluminescent Lamp Membrane Switch (Continuation) |

US | 3/6/2007 | 6/9/2025 | |||

| Electroluminescent Lamp Membrane Switch (Continuation) |

EU | Pending | 4/6/2026 | |||

| Electroluminescent Lamp Membrane Switch (Continuation) |

China | 5/26/2010 | 4/6/2026 | |||

| Electroluminescent Lamp Membrane Switch (Continuation) |

Japan | Pending | 4/6/2026 | |||

| Electroluminescent Lamp Membrane Switch |

US | 5/23/2006 | 6/9/2025 | |||

| Electroluminescent Lamp Membrane Switch (CIP) |

US | 2/17/2012 | 6/14/2026 | |||

| Electroluminescent Lamp Membrane Switch (CIP) |

China | 6/5/2012 | 6/6/2027 | |||

| Electroluminescent Lamp Membrane Switch (CIP) |

Hong Kong | Pending | 6/6/2027 | |||

| Electroluminescent Lamp Membrane Switch (CIP) |

Taiwan | Pending | 6/12/2027 | |||

| Electroluminescent Lamp Membrane Switch (CIP) |

EU | Pending | 6/7/2027 | |||

| Electroluminescent System in Monolithic Structure |

US | 1/5/1999 | 5/30/2016 | |||

| Electroluminescent System in Monolithic Structure |

Spain | 7/14/2004 | 5/29/2017 | |||

| Electroluminescent System in Monolithic Structure |

Great Britain | 7/14/2004 | 5/29/2017 | |||

| Electroluminescent System in Monolithic Structure |

Germany | 7/14/2004 | 5/29/2017 | |||

| Electroluminescent System in Monolithic Structure |

Hong Kong | 12/24/2004 | 5/29/2017 | |||

| Irradiated Images Described by Electrical Contact |

US | 7/18/2000 | 6/8/2018 | |||

| Irradiated Images Described by Electrical Contact |

Singapore | 11/28/2003 | 6/8/2019 | |||

| Irradiated Images Described by Electrical Contact |

Taiwan | 5/1/2003 | 12/2/2019 | |||

| Irradiated Images Described by Electrical Contact |

Canada | 5/19/2009 | 6/8/2019 | |||

| Irradiated Images Described by Electrical Contact |

Japan | 5/14/2010 | 6/8/2019 | |||

| Irradiated Images Described by Electrical Contact |

South Korea | 6/14/2006 | 6/8/2019 |

11

Table of Contents

| Membranous EL System in UV-Cured Urethane Envelope |

US | 4/6/2004 | 10/10/2021 | |||

| Membranous EL System in UV-Cured Urethane Envelope |

China | 4/11/2007 | 10/10/2021 | |||

| Membranous EL System in UV-Cured Urethane Envelope |

EU | Pending | 10/10/2021 | |||

| Membranous EL System in UV-Cured Urethane Envelope |

Taiwan | 1/7/2004 | 10/11/2021 | |||

| Membranous EL System in UV-Cured Urethane Envelope |

Japan | 4/15/2011 | 10/10/2021 | |||

| Membranous Monolithic EL Structure with Urethane Carrier |

US | 2/24/2004 | 10/10/2021 | |||

| Membranous Monolithic EL Structure with Urethane Carrier |

Japan | 9/26/2008 | 10/10/2021 | |||

| Membranous Monolithic EL Structure with Urethane Carrier |

Taiwan | 1/13/2004 | 10/11/2021 | |||

| Membranous Monolithic EL Structure with Urethane Carrier |

China | 5/23/2007 | 10/10/2021 | |||

| Method of Construction of Elastomeric EL Lamp |

US | 8/7/2001 | 12/30/2016 | |||

| Method of Construction of Elastomeric EL Lamp |

China | 4/9/2008 | 10/15/2019 | |||

| Method and Apparatus for Illuminating a Key Pad |

US | 11/30/2004 | 6/8/2020 | |||

| Method for Constructing EL System in Monolithic Structure |

US | 11/9/1999 | 5/30/2016 | |||

| PTF Touch Enabled Image Generator |

US | 8/12/2003 | 6/8/2018 | |||

| UV-Curable Inks for PTF Laminates (Including Flexible Circuitry) |

China | 11/8/2006 | 6/19/2022 | |||

| Highly Transmissive Electroluminescent Lamp |

US | 1/31/2012 | 12/12/2026 | |||

| Translucent Layer including Metal/Metal Oxide |

US | 7/17/2001 | 10/15/2018 |

Oryon keeps developing its technology and, with the support of the funding provided by future financings, will continue to expand, maintain and enforce patent rights and protect its IP and trade secrets.

Oryon’s technology comprises three basic components: the core EL lamp, electronics to power the lamp, and the interconnect system between the lamp and the power system. Through outsourcing, Oryon believes that it has established the infrastructure, principally through third parties, to scale the manufacturing of the technology. Oryon continues to develop the technology to gain cost advantages, improve performance and functionality, and to support new applications. The technologies, processes and designs described in Oryon’s patents are incorporated into many of Oryon’s important products and expire at various times.

Oryon has developed significant processes and methodologies for integrating Elastolite® systems into end-user applications and products in the textile and membrane switch markets, successfully tested in molding Elastolite® into plastics and moving forward with the concept that Elastolite® can be printed on high speed roll-to-roll printers. Oryon also has successfully worked with many of its customers’ contract manufacturers and assemblers to integrate Elastolite® into their manufacturing operations. In addition, Oryon has setup and managed relationships with low cost, high quality contract manufacturers.

These patents that protect Oryon from certain potential competition come at a high cost. The average cost to obtain a patent ranges anywhere from $25,000 to $100,000 per patent in addition to the annual financial maintenance requirements Oryon must pay to maintain the patents. Failure to pay maintenance fees on each outstanding patent will cause a loss of the patent in the individual country in which the patent’s renewal fee is not paid. Fees can range as high as $5,000 per renewal.

12

Table of Contents

Each country has its own rules and regulations for both obtaining and maintaining patents although there is coordination and streamlining of processes between European Union countries. Patents can be filed in one filing for multiple countries, and once approved, individual countries where the patent will be effective can be selected. Cooperation also exists in filings between the European Union and the U.S.

Patents, even when approved and issued can still be challenged by third parties as not being valid. The possibility always exists that there are competing patents or technologies existing at the time the patent was issued that were overlooked when the patent was issued. Patents can be challenged and lost based on previously existing prior art. There are also multiple rules and regulations one must follow when challenging a patent or making claims when prosecuting a patent. Patent law is complex and expensive. Although Oryon feels secure with its patents, there always remains the possibility that challenges to these patents may arise and Oryon’s patents invalidated.

Oryon will continue to evaluate the business benefits in pursuing patents in the future. Oryon currently protects all of its development work with confidentiality agreements with its engineers, employees and any outside contractors. However, third parties may, in an unauthorized manner, attempt to use, copy or otherwise obtain and market or distribute Oryon’s intellectual property or technology or otherwise develop a product with the same functionality as Oryon’s IP. Policing unauthorized use of intellectual property rights is difficult, and nearly impossible on a worldwide basis. Therefore, Oryon cannot be certain that the steps it has taken or will take in the future will prevent misappropriation of its technology or intellectual property, particularly in foreign countries where Oryon may do business, where the laws may not protect proprietary rights as fully as do the laws of the United States or where the enforcement of such laws is not common or effective.

Products and Distribution

Although Oryon has the potential to create multiple applications and products in multiple industries, Oryon management has determined to attack these markets not with its own products that would require unique design, development, marketing and manufacturing expertise and capability, but rather by targeting established brands, retailers or companies with proven revenue streams, known channels of distribution and consumer acceptance and in cooperation with these companies let Oryon’s technology become an integral part of these companies’ products. Oryon’s targeted customers typically have design, development and marketing teams as well as factories capable of producing their products in mass. Oryon will work with the designers and product developers from these companies to design Oryon’s Elastolite® and supporting technology into their own products and through technology transfer teach their factories how to integrate Elastolite® into their manufacturing process. To date, Oryon has worked with or provided Elastolite®, through license agreements, to the following companies: a leading Fortune 100 company, a leading Fortune 500 sports apparel and shoe brand, Lands’ End, a leading international sport and shoe brand, Marmot Mountain, Rogers Corporation, Motorola, Puma, Under Armour and suppliers to Disney.

Oryon has and will distribute Elastolite® through multiple brands and corporations seeking the ability to differentiate their products with Oryon’s Elastolite®. Oryon’s customers have been and will principally be established leaders in their respective industries with defined channels of distribution and product acceptance. As Oryon expands into new industries or product applications, it will seek to partner with leading companies in each of its target markets.

Manufacturing

Oryon is not in the manufacturing business. Oryon has in the past established and trained third party manufacturers capable of producing Elastolite® in volume. Management anticipates continuing this policy and developing additional third party relationships in the future. These manufacturers typically will be established through licenses granted to them by Oryon. Other than samples or small lots created for sales purposes, Oryon will outsource the production of Elastolite® to these companies. Oryon does not have any exclusive manufacturing agreements and at present, no outsourced manufacturer represents a significant portion of Oryon’s manufacturing business.

Oryon either designs the technology needed to operate Elastolite® (principally inverters that power the Elastolite® lamp) or contracts the creation of the technology with third party design teams. All inverters must meet pre-established design and performance criteria established by Oryon. Once created and successfully tested, the manufacture of the electronics is contracted to third party manufacturers and assemblers, both domestic and foreign. Oryon itself does not manufacture, other than prototypes, any of the electronics needed to operate Elastolite®.

13

Table of Contents

To ensure that Elastolite® and the products in which Elastolite® is used is of the highest quality and standards, Oryon has and continues to establish quality control systems and procedures at all levels of product development, design and manufacturing regardless of the customer or the factory in which it is produced. Some of the procedures pertain to the following:

| • | Testing and understanding the specifications of all materials on which Elastolite® is placed. |

| • | Working closely with Oryon’s customers’ design and product development teams, at the earliest stages of product creation, to ensure that Elastolite® is properly designed into their product and is capable of low cost mass production. |

| • | Manufacturing guidelines and procedures are established with Oryon customers’ factories and Oryon technical transfer engineers to train the factories in low cost methods of integrating Elastolite® into the manufacturing process. |

| • | Continual audit of third party manufacturers. |

| • | Establishment of well-defined processes and standards that must be met in manufacturing. |

| • | Quality control on all materials used in each stage of manufacture. |

| • | Continual monitoring and adherence to environmental rules and regulations and the meeting of proper working conditions under which Elastolite® is produced. |

Industry and Competition

Oryon positions itself alongside other lighting technologies such as traditional EL and LED. In management’s opinion, Elastolite® is an enabling, innovative technology allowing the use of light in products and applications that heretofore were not practical or cost effective.

As a result, Elastolite® is defining its own application space. This is especially true in the textile market, where other lighting technologies have limited capabilities. Among its primary competitive advantages, Elastolite® is positioned in applications demanding ruggedness, durability, wearability and flexibility.

| Elastolite® | Traditional EL | LED | ||||

| Temperature |

Cool | Cool | Warm | |||

| Lighting |

Uniform | Uniform | Point | |||

| Thickness |

Ink Layer | Ink Layer + | Surf. Mount | |||

| Flexibility |

Rubber Like | Semi-Rigid | Rigid | |||

| Water Resistant |

Yes | No | No | |||

| Moldable |

Yes | No | No |

Traditional EL. Traditional EL is typically used as backlighting in conditions where high flexibility is not required, need for ruggedness is average and water resistance is not an issue. Traditional EL is at a distinct disadvantage to Elastolite® in the switch segment since Elastolite® is capable of applying its light directly behind, or directly onto, a key. Traditional EL providers actually cut out the key placements from a polyethylene terephthalate (PET) substrate containing EL. Through Oryon’s patented printing process for switches, customers can save money, improve manufacturing, and improve the quality of lighting. Within the apparel space, conventional EL products are very limited because traditional EL cannot be washed, without incurring additional costs to waterproof, and is rigid or semi-rigid in nature.

LED. LED is normally deployed as a point light source where there is average need for ruggedness, little need for large areas of uniform light, and no need for flexibility or water resistance. LEDs are typically used as indicator lights, in camera displays, and in cell phones. More recently LEDs have advanced in brightness characteristics and are being positioned as a replacement to incandescent lighting technology. The pointed nature of LEDs creates non-uniform light which cannot be channeled effectively onto the intended surface. This creates a low quality appearance, especially in switch applications. In addition, as the trend toward miniaturization continues, LEDs are in many cases not thin enough for membrane switch applications. Many switch applications require extensive flex at one or more connection points, which LEDs cannot handle. In addition, the price-power-quality tradeoff is not optimal. LED prices in the switch segment increase proportionately with the number of LEDs used in a particular application. Because Elastolite® is a blanket light, it can achieve full coverage of uniform light that cannot be achieved by LEDs. The more LEDs required in a particular application to achieve a given light effect, the higher the cost. In any given application, the cost advantages/disadvantages between LED’s and Elastolite® are based on the quality of light demanded and the number of LEDs required to obtain that quality.

14

Table of Contents

We believe that Elastolite® should be the light of choice where high-quality uniform lighting is required that needs to be thin, malleable, washable and durable when exposed to multiple stresses. It is not the light of choice for all applications. Traditional EL and LEDs may be preferred when used in non-stressed environments where brightness is needed. LEDs can be cheaper to use than Elastolite® where quality of light is not paramount. In addition, traditional EL presently requires less power than Elastolite® to achieve the same brightness, although Elastolite’s increased power demands permit applications with the same brightness, but with increased malleability, which is one of Elastolite’s differentiating characteristics. One of Oryon’s research objectives is the reduction in power demanded by Elastolite® while maintaining its increased malleability. LEDs can be used in full color active displays whereas neither Elastolite® nor traditional EL can presently be used in this manner. Nevertheless, we are not aware of any significant competitors utilizing LEDs or traditional EL for stressed applications such as apparel where we are focusing our marketing efforts.

To the extent that we pursue applications in non-stressed uses such as keypad backlighting or similar uses, we view our competition to consist of other light sources or technologies, such as traditional EL, LEDs, fiber optics or organic light-emitting diodes (OLED). Oryon has focused on target markets where it has significant advantages relative to these other technologies. Oryon views competitors in many of its market segments as potential customers because Elastolite® can offer solutions that are complementary to competitors’ existing applications. Traditional EL is a limited market, therefore no dominant player exists. There are many small companies in the field. Some of the leading players in the field include Rogers Corporation, Hansung, Planar, EL Korea and DuPont. Newer entrants include Lyttron (subsidiary of Bayer), Salux and others that may have pursued alternative EL technologies; however, Oryon is not aware of any market traction related to a competitive technology.

Oryon is focused on continuing the development of its IP and know-how, aligning itself with the strongest possible strategic partners and expanding its infrastructure to service customers in its target markets. We believe these activities will increase barriers to potentially competitive technologies.

Markets

Because Oryon’s Elastolite® is a platform lighting technology, management believes that lit applications heretofore untried, impractical or ineffective as a light solution are now possible to achieve. Two examples are the Motorola Razr cell phone and lighting on clothing and gear.

| • | Motorola, in building a state-of-the-art icon cell phone, wanted the phone to be both thin and provide uniform lighting in the keypad. Without adding a multiplicity of LED’s, uniform light would be hard to achieve as the LED could not be placed directly under the keypad and even if it were, the tactile feel of the keypad would be lost. Further, Elastolite®, being extremely thin, helped the overall objective of thinness of the cell phone. Traditional EL was not practical to use. Although it was thin, and even flexible, it was neither malleable nor durable. It would not wear satisfactorily and the tactile feel would be lost. The solution was Elastolite®. To date over 100,000,000 cell phones have been produced using Oryon’s Elastolite® technology. |

| • | Outdoor Apparel and Occupational Safety Clothing and Gear: Lighted clothing in the past, although possible, was either impractical, difficult to wear, not cost effective or suited for an outdoor environment or for washing. Elastolite® eliminated these obstacles. Being washable, malleable, durable and friendly to outdoor environments, it developed clothing applications that were market tested and validated. As a result of the information learned from these tests, Oryon was able to refine Elastolite® and its electronic system to where a Fortune 500 company and a leading sports apparel company, integrated it into a product for retail introduction in late fall/winter 2009-10. In addition, the world’s leading company in reflective materials and office products, a Fortune 100 company, licensed in December 2008 the use of Elastolite® to integrate with their existing product mix. |

Elastolite® caters to multiple multi-billion dollar companies and markets. The above are just a few examples of these markets. The premier markets for Elastolite® include:

| • Outdoor Apparel, Textiles and Gear |

• Gauges | |

| • Occupational Safety Apparel and Products |

• Lit bicycles and Motorbikes | |

| • Keypads and Membrane Switches |

• Carpet Runners | |

| • In-Molded and Compression Molded Products

• Cell Phone Cases

• Keypads |

• Household Appliances

• Microwaves

• Air Conditioning Units, Etc. | |

15

Table of Contents

| • Automotive

• Dashboards and Controls

• Decorative

• Safety |

• Security Systems | |

| • Costumes |

• Outdoor Advertising and Displays | |

| • Point of Sale |

• Outdoor Equipment | |

| • Decorative Floorings |

• Military | |

| • Toys and Games |

• Multiple Miscellaneous Applications | |

Seasonality

Elastolite® is global in usage and its seasonality is dependent on the applications to which it becomes attached. As an example, many outdoor utilitarian products, although used year round, will achieve their highest outdoor utility during periods of the greatest and longest darkness; fall through spring. Some products such as toys and decorations will reach their highest consumer consumption during the Christmas holiday season. Other applications, such as military and automotive, have no seasonality.

Government Regulation

Being a new technology, there are few governmental regulations that directly affect Elastolite®. Regardless, Oryon’s larger customers have established many environmental and work place regulations that do affect their suppliers and contractors. Oryon, although typically a second tier supplier to these customers, must meet the environmental and workplace standards established by each of its customers. Most of these standards overlap from one company to the next although Oryon must be careful that it meets, at a minimum, all standards established by its customers.

In addition, in the United States, Oryon is or may be required to comply with certain federal health and safety laws, laws governing equal employment opportunity, customs and foreign trade laws and regulations, laws regulating the sales of products in schools, and various other federal statutes and regulations. Oryon may also be subject to various state and local statutes and regulations, including California Proposition 65 which requires that a specific warning appear on any product that contains a component listed by the State of California as having been found to cause cancer or birth defects. Many of our customers who sell products in California may be required to provide warning labels on their products. Oryon relies on legal and operational compliance programs, as well as local counsel, to guide its businesses in complying with applicable laws and regulations of the jurisdictions in which it does or plans to do business. Further, the conduct of Oryon’s businesses, and the production, distribution, sale, advertising, labeling, safety, transportation and use of Elastolite®, are and will be subject to various foreign laws and regulations administered by government entities and agencies in markets where Oryon may operate and sell Elastolite®. It is Oryon’s policy to abide by the laws and regulations that apply to its business.

Also, Oryon must be careful it understands and adheres to standards established in the U.S., the European Union and multiple Asian countries where Elastolite® is produced and potentially distributed in addition to Underwriters Laboratories Inc. (UL) and Conformance European (CE) standards established on the electronic components used to power Elastolite®.

Oryon does not anticipate at this time that the cost of compliance with U.S. and foreign laws will have a material financial impact on its operations, business or financial condition, but new regulatory and tariff legislation or changes in existing regulations may have a material negative effect on Oryon’s business in the future. Oryon is also committed to meeting all applicable environmental compliance requirements. Environmental compliance costs are not expected to have a material impact on Oryon’s capital expenditures, earnings or competitive position.

Employees

Oryon has five full-time employees. Occasionally, Oryon engages temporary part-time workers or consultants to assist in the completion of specific assignments or projects. All full-time employees are offered the opportunity to receive healthcare benefits. No employees are covered by collective bargaining agreements. Certain management employees of Oryon have employment agreements with individually customized terms. Oryon has an equity incentive plan and all Oryon employees are eligible for grants under that plan.

16

Table of Contents

The statements contained in this document that are not historic facts are forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially from those set forth in or implied by forward-looking statements. If any of the following events described in these risk factors actually occurs, our business, financial condition or results of operations could be harmed.

Risks Relating to Our Company and Our Industry

Oryon has limited revenues and has incurred losses.

Oryon has limited revenues and we anticipate that our existing cash and cash equivalents will not be sufficient to fund our longer term business needs and we will need to generate additional revenue or receive additional investment to continue operations. In 2012 and 2011, Oryon had losses of approximately $2.6 million and $1.6 million, respectively. Based on our current internal forecast, we anticipate that we will continue to incur losses through the year ending December 2013.

We operate a business that is highly speculative and may not generate any profit.

There can be no assurance that our products will have commercial viability and/or that our plan to develop and exploit our technology is feasible. Because of the numerous risks and uncertainties associated with developing and marketing new technologies, we are unable to predict the extent of any future profits, if at all. We have financed operations and internal growth primarily through funding provided by investors and funds generated from operations. To date, we have devoted substantially all of our efforts to research and development, infrastructure building and initial marketing activities. There is no guarantee the cost estimates used by us or the sales volumes projected are accurate and will be attained. An inability to meet sales volumes as forecast or to achieve assumed cost figures could have a negative impact on our profitability, cash flow and survival. Some of the initial sales volumes that we are projecting are expected to be in the apparel and gear areas. These areas are highly volatile and sometimes affected by economic conditions beyond our control, which could impact planned sales volumes and could negatively impact our finances.

Our auditors have expressed uncertainty as to our ability to continue as a going concern.

Primarily as a result of our recurring losses and our lack of liquidity, we received a report from our independent auditors that includes an explanatory paragraph describing the substantial uncertainty as to our ability to continue as a going concern as of our fiscal year ended December 31, 2012.

If we fail to raise additional capital, our ability to implement our business model and strategy could be compromised.

We have limited capital resources and operations. To date, our operations have been funded entirely from the proceeds from limited revenues, equity and debt financings. We currently do not have adequate capital or revenue to meet current or projected operating expenses. We anticipate needing substantial additional capital in the near future to develop and market new products, services and technologies. We currently do not have commitments for financing to meet our expected needs and we may not be able to obtain additional financing on terms acceptable to us, or at all. Even if we obtain financing for our near term operations and product development, we expect that we will require additional capital beyond the near term. If we are unable to raise capital when needed, our business, financial condition and results of operations would be materially adversely affected, and we could be forced to reduce or discontinue our operations. Debt financing, if obtained, may involve agreements that include covenants limiting or restricting our ability to take specific actions, such as incurring additional debt and could increase our expenses, and would be required to be repaid regardless of our operating results. Moreover, we may issue equity securities in connection with such debt financing. Equity financing, even if obtained, could result in ownership and economic dilution to our existing stockholders and/or require us to grant certain rights and preferences to new investors. In addition, we may seek additional capital due to favorable market conditions or strategic considerations even if we believe we have sufficient funds for our current operations.

We do not currently have credit facilities or arrangements in place as a source of funds and there can be no assurance that we will be able to raise sufficient additional capital or raise such capital on acceptable terms or raise such capital when we need it. If such capital is not available on satisfactory terms, or is not available at all, we may be required to delay, scale back or stop the development of our products and/or cease our operations.

17

Table of Contents

If our products or technology do not gain market acceptance, we may not be able to fund future operations.

There can be no assurance that our products or technology will have commercial viability and/or that our plan to develop and exploit our technology is feasible. A number of factors may affect the market acceptance of our products, including, among others, the perception by consumers of the effectiveness of our products, our ability to fund our sales and marketing efforts, and the effectiveness of our sales and marketing efforts. If our products do not gain acceptance by consumers, we may not be able to fund future operations, including the development of new products, and/or our sales and marketing efforts for our current products, which inability would have a material adverse effect on our business, financial condition and operating results.

If we underestimate our operating expenses, we may not be able to fund future operations.

To date, we have devoted substantially all of our efforts to research and development, infrastructure building and initial marketing activities. There is no guarantee that our cost estimates or projected sales volumes are accurate and will be attained. An inability to meet sales volumes as forecast or to achieve assumed cost figures could have a negative impact on our profitability, cash flow and survival.

We expect our operating expenses to increase in connection with the continued development of our products and technology and expansion of our marketing activities. We may also incur costs and expenses that are unexpected, in excess of amounts anticipated or are otherwise not contemplated or provided for in connection with our business plan. If these or other costs or expenses are incurred, it could have a material adverse effect on our financial performance.

Any failure to adequately establish outsourcing capabilities and an internal and distributor sales force will impede our growth.

We require adequate arrangements with third party outsourcing sources to manufacture our products. Any failure to enter into and maintain such arrangements would adversely affect our growth. In addition, we expect to be substantially dependent on an internal and distributor sales force to attract new consumers of our products and technology. We believe that there may be significant competition for qualified, productive sales personnel and distributors who have the skills and technical knowledge necessary to promote and sell our products and technology. Our ability to achieve significant growth in revenue in the future will depend, in large part, on our success in establishing our sales network. If we are unable to develop an efficient sales network, it will make our growth more difficult and our business could suffer.

Our failure to accurately estimate demand for our products and technology could adversely affect our business and financial results.

We may not accurately estimate demand for our products and technology. Our ability to estimate the overall demand for our products and technology is imprecise and may be less precise in certain markets. If we materially underestimate demand for our products and technology we might not be able to satisfy demand on a short-term basis. Moreover, industry-wide shortages of certain electronic and lighting components, parts or raw materials have been, and could, from time to time in the future, be experienced. Such shortages could interfere with and/or delay production of our products by our customers and could have a material adverse effect on our business and financial results.

Changes in consumer preferences may reduce demand for our products and technology.

Our future success will depend upon our ability to develop and introduce different and innovative lighting solutions and applications for Elastolite®. In order to develop our market share, the impact of our products must address a consumer need and then meet that need in the areas of quality and derived benefits. There can be no assurance of our ability to meet that need and there is no assurance that consumers will purchase our products. Additionally, our products are considered premium products and to maintain market share during recessionary periods we may have to reduce profit margins which would adversely affect our results of operations. Product lifecycles for some consumer electronic products in which our products may be used may be limited to a few years before consumers’ preferences change. There can be no assurance that our products will become or remain profitable for us. Our industry is subject to changing consumer preferences and shifts in consumer preferences may adversely affect us if we misjudge such preferences. We may be unable to achieve volume growth through product initiatives. We also may be unable to penetrate new markets. If we are unable to address any or all of these issues, it may affect our ability to produce revenues and our business, financial condition and results of operations will be adversely affected.

18

Table of Contents

If we are unable to develop and establish brand image or product quality, or if we encounter product recalls, our business may suffer.

Our success depends on our ability to develop and establish brand image for our products, lighting solutions and applications for Elastolite®. We have no assurance that our advertising, marketing and promotional programs will have the desired impact on our products’ brand image or consumer preferences. Product quality issues, real or imagined, or allegations of product defects, even if false or unfounded, could tarnish the image of the affected brands and may cause consumers to choose other products. We may be required from time to time to recall products entirely. Product recalls could adversely affect our profitability and our brand image. We do not maintain recall insurance. While we do not expect to have any credible product liability litigation, there is no assurance that we will not experience such litigation in the future. In the event we do experience product liability claims or a product recall, our financial condition and business operations could be materially adversely affected.

We may acquire or make investments in companies or technologies that could cause loss of value to our stockholders and disruption of our business.

Subject to our capital constraints, we intend to continue to explore opportunities to acquire companies or technologies in the future. Entering into an acquisition entails many risks, any of which could adversely affect our business, including:

| • | Failure to integrate the acquired assets and/or companies with our current business; |

| • | The price we pay may exceed the value we eventually realize; |

| • | Loss of share value to our existing stockholders as a result of issuing equity securities as part or all of the purchase price; |

| • | Potential loss of key employees from either our current business or the acquired business; |

| • | Entering into markets in which we have little or no prior experience; |

| • | Diversion of management’s attention from other business concerns; |

| • | Assumption of unanticipated liabilities related to the acquired assets; and |

| • | The business or technologies we acquire or in which we invest may have limited operating histories, may require substantial working capital, and may be subject to many of the same risks we are subject to, as well as additional risks. |

If we do not respond effectively and on a timely basis to rapid technological change, our business could suffer.

Our industry is characterized by rapidly changing technologies, industry standards, customer needs and competition, as well as by frequent new product and service introductions. We must respond to technological changes affecting both our customers and suppliers. We may not be successful in developing and marketing, on a timely and cost-effective basis, new services that respond to technological changes, evolving industry standards or changing customer requirements. Our success will depend, in part, on our ability to accomplish all of the following in a timely and cost-effective manner:

| • | Effectively using and integrating new technologies; |

| • | Continuing to develop our technical expertise; |

| • | Enhancing our engineering and system design services; |

| • | Developing services that meet changing customer needs; |

| • | Advertising and marketing our services; and |

| • | Influencing and responding to emerging industry standards and other changes. |

An interruption in the supply of products and services that we obtain from third parties could cause a decline in sales of our products.