Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - WILLIS TOWERS WATSON PLC | d495977d8k.htm |

WILLIS

GROUP HOLDINGS

Fact Book

Fourth Quarter 2012

March 2013

EXHIBIT 99.1 |

2

2012 C&F: $3.46 billion

Willis: A leading global insurance broker

Willis Subsidiaries and Associates

Willis

Global

Franchise

2012 Commissions and Fees by Segment

Broad range of professional insurance, reinsurance, risk management, financial and

human resource consulting and actuarial services

Global distribution capabilities to meet risk management needs of middle market and

large multinational clients

More than 400 offices in 120 countries, with over 17,000 employees

Strong sales culture and relentless focus on cost control

|

Summary Q4

2012 financial results Q4 2012

Q4 2011

FY 2012

FY 2011

Organic

commission

and fee growth

7.5%

(2.3)%

3.1%

1.8%

Reported

operating

margin

(89.0)%

9.9%

(6.0)%

16.4%

Adjusted

operating

margin

19.1%

18.7%

21.6%

22.5%

Reported EPS

$(4.65)

$0.14

$(2.58)

$1.15

Adjusted EPS

$0.45

$0.45

$2.58

$2.74

See important disclosures regarding Non-GAAP measures starting on page 18

3 |

Organic Q4

2012 commissions and fees growth Q4 2012

Q4 2011

Global

11.6%

6.3%

North America

5.0%

(9.4)%

International

7.4%

2.2%

Willis Group

7.5%

(2.3)%

Growth across all segments

Global

Growth in all Global businesses; strong

new business at Willis Faber & Dumas;

solid growth in Global Specialties and

Reinsurance; WCM&A closed delayed

deals

North America

Best quarter since 2006; growth in all

geographic regions; improvement in

construction business

International

Growth in all regions except

Australasia; double-digit growth in

Latin America, mid-single digit growth

in Europe, and continued improvement

in UK

See important disclosures regarding Non-GAAP measures starting on page 18

4 |

Reported operating margin (89.0)%; 19.1% adjusted operating margin

Adjusted operating margin up 40 bps from prior year quarter, primarily driven

by: Higher commissions and fees

Reduction in other operating expenses

Partially offset by higher salaries and benefits and lower investment income

Reported EPS of $(4.65); Adjusted EPS of $0.45

Flat to prior year

Positive $0.01 impact from foreign exchange

Q4 2012 impacted by significant charges:

$200 million write-off of unamortized cash retention awards

$252 million accrual of 2012 cash bonuses

$492 million North America segment goodwill impairment

$113 deferred tax valuation allowance

See important disclosures regarding Non-GAAP measures starting on page 18

5

Q4 2012 financial results |

Note:

Peer

averages

are

based

on

Willis

estimates

using

public

information

regarding

insurance

brokerage

operations

of

AJG,

AON,

BRO,

MMC

See important disclosures regarding Non-GAAP measures starting on page 18

6

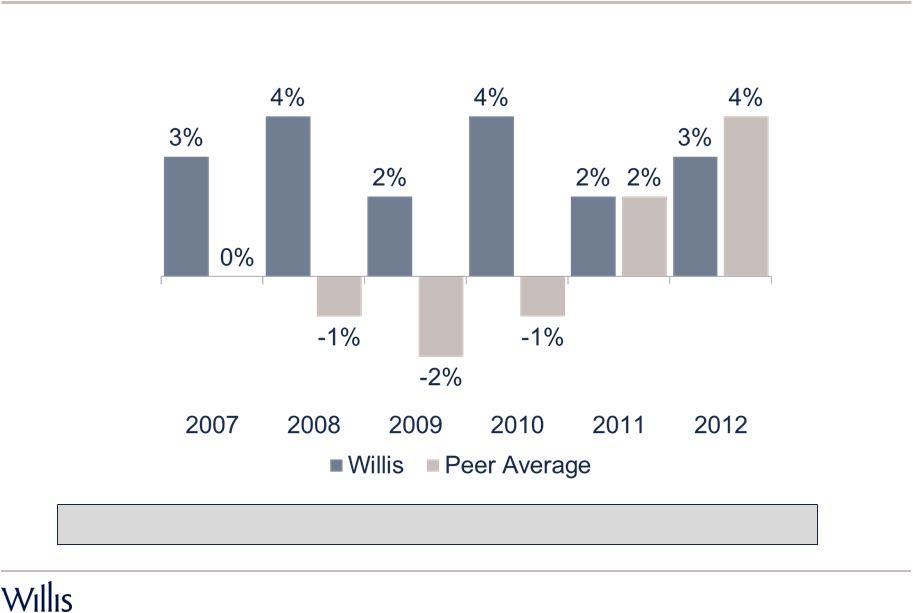

Track record of organic commission and fee growth

Average 2007 –

2012 Willis 3% Peers 0% |

See

important disclosures regarding Non-GAAP measures starting on page 18

7

Adjusted operating margins

Average 2007 –

2012 Willis 22% Peers 20%

Note: Peer averages are based on Willis estimates using public information regarding

insurance brokerage operations of AJG, AON, BRO, MMC |

($

millions) Dividends $185 million

Capex $135 million

Share buyback $100 million

M&A expenditures of $69 million

8

Strong cash flow from operations

$85 million increase in cash flow from operations in 2012

$500 million of cash and cash equivalents at December 31, 2012

2012 corporate/non-operating uses of cash |

99 Debt / Adjusted EBITDA

Adjusted EBITDA $890 million in 2012, a decline of $22 million versus 2011

Debt outstanding $2.35 billion as at December 31, 2012

Further reduction of leverage ratio driven by improved operating

performance and effective capital management

(a)

Includes impact from acquisition of HRH as of 10/1/2008.

See important disclosures regarding Non-GAAP measures starting on page 18

Leverage ratios |

SEGMENT

OVERVIEWS |

Extensive retail platform with Top 3

position in all major markets

Able to leverage industry and specialty

practice group expertise across Willis

network

Major practice groups include:

Employee Benefits (approximately 24%

of 2012 North America C&F)

Construction (approximately 14% of

2012 North America C&F)

Healthcare

Real Estate/Hospitality

Financial and Executive Risk

120

offices

across

Seven

regions

Other includes Canada and Mexico

Segment overview

2012 North America C&F: $1.31 billion

See important disclosures regarding Non-GAAP measures starting on page 19

11

Willis North America overview

2012 commissions and fees – by

region |

Segment overview

Retail operations in the United Kingdom,

Eastern and Western Europe, Asia

Pacific, the Middle East, South Africa

and Latin America

Provide services to businesses locally in

over 120 countries; leading positions in

UK, Scandinavia, China and

Russia

Offices designed to grow business locally

around the world, making use of the

skills, industry knowledge and expertise

available within segment and elsewhere

in the Group

2012 International C&F: $1.03 billion

See important disclosures regarding Non-GAAP measures starting on page 19

12

Willis International overview

2012 commissions and fees – by

region |

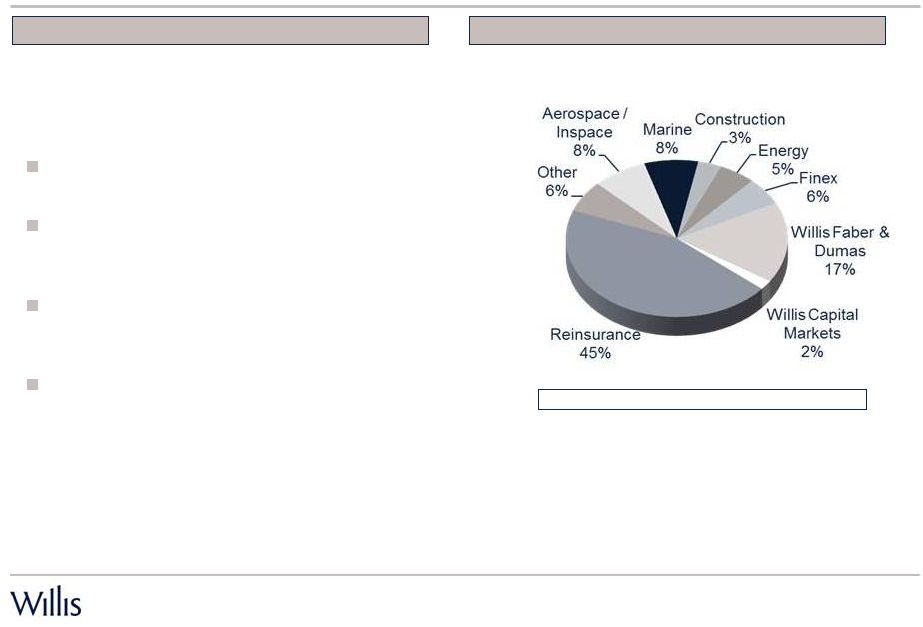

Segment overview

Reinsurance

Willis Re

One of only three global reinsurance

brokers

Significant market share in major

markets, particularly marine and

aviation

Cutting edge analytical and advisory

services, including Willis Research

Network

Complete range of transactional

capabilities including, in conjunction

with Willis Capital Markets & Advisory,

risk transfer via the capital markets

2012 Global C&F: $1.12 billion

See important disclosures regarding Non-GAAP measures starting on page 19

13

Willis Global overview

2012 commissions and fees –

by business |

Segment overview

Global

Specialties,

with

strong

global

positions in:

Aerospace/Inspace

FINEX

and

Financial

Solutions

–

political

risks

and UK financial institutions

Marine

Energy

Construction

Willis Faber & Dumas includes:

Faber

&

Dumas

-

wholesale

brokerage

including:

Glencairn

Limited

-

provides

access

to

London

& Bermuda markets

Niche –

Fine Art, Jewelry and Specie,

Bloodstock and Kidnap & Ransom

Global

Markets

International

-

provides

Willis Capital Markets & Advisory

Advises on M&A and capital markets products

See important disclosures regarding Non-GAAP measures starting on page 19

14

Willis Global overview (continued)

2012 Global C&F: $1.12 billion

access for retail clients to global markets

2012 commissions and fees –

by business |

APPENDIX |

See important disclosures regarding forward-looking statements on page 18

The Willis Cause

16 |

Important

disclosures regarding forward-looking statements 17

This presentation contains certain “forward-looking statements” within the meaning of

Section 27A of the Securities Act of 1933, and Section 21E of the Securities Exchange Act of 1934,

which are intended to be covered by the safe harbors created by those laws. These forward-looking

statements include information about possible or assumed future results of our operations.

All statements, other than statements of historical facts, included in this document that address

activities, events or developments that we expect or anticipate may occur in the future,

including such things as our outlook, potential cost savings and accelerated adjusted operating margin

and adjusted earnings per share growth, future capital expenditures, growth in commissions and

fees, business strategies, competitive strengths, goals, the benefits of new initiatives, growth of our business and operations, plans, and references to future successes

are forward-looking statements. Also, when we use the words such as ‘anticipate’,

‘believe’, ‘estimate’, ‘expect’, ‘intend’, ‘plan’, ‘probably’, or similar expressions, we are making forward-

looking statements.

There are important uncertainties, events and factors that could cause our actual results or

performance to differ materially from those in the forward-looking statements contained in this

document, including the following: the impact of any regional, national or global political, economic,

business, competitive, market, environmental or regulatory conditions on our global business

operations; the impact of current financial market conditions on our results of operations and financial condition, including as a result of those associated with the current

Eurozone crisis, any insolvencies of or other difficulties experienced by our clients, insurance

companies or financial institutions; our ability to implement and realize anticipated benefits

of any operational change or any revenue generating initiatives; volatility or declines in insurance

markets and premiums on which our commissions are based, but which we do not control; our

ability to continue to manage our significant indebtedness; our ability to compete effectively in our industry, including the impact of our refusal to accept contingent

commissions from carriers in the non-Human Capital areas of our retail brokerage business;

material changes in commercial property and casualty markets generally or the availability of

insurance products or changes in premiums resulting from a catastrophic event, such as a hurricane;

our ability to retain key employees and clients and attract new business; the timing or ability

to carry out share repurchases and redemptions; the timing or ability to carry out refinancing or take other steps to manage our capital and the limitations in our long-term debt

agreements that may restrict our ability to take these actions; any fluctuations in exchange and

interest rates that could affect expenses and revenue; the potential costs and difficulties in

complying with a wide variety of foreign laws and regulations and any related changes, given the

global scope of our operations; rating agency actions that could inhibit our ability to borrow

funds or the pricing thereof; a significant decline in the value of investments that fund our pension plans or changes in our pension plan liabilities or funding obligations; our ability

to achieve the expected strategic benefits of transactions, including any growth from associates;

further impairment of the goodwill of one of our reporting units, in which case we may be

required to record additional significant charges to earnings; our ability to receive dividends or

other distributions in needed amounts from our subsidiaries; fluctuations in our earnings as a

result of potential changes to our valuation allowance(s) on our deferred tax assets; changes in the tax or accounting treatment of our operations and fluctuations in our tax rate; any

potential impact from the US healthcare reform legislation; our involvements in and the results of any

regulatory investigations, legal proceedings and other contingencies; underwriting, advisory or

reputational risks associated with non-core operations as well as the potential significant impact our non-core operations (including the Willis Capital Markets and Advisory

operations) can have on our financial results; our exposure to potential liabilities arising from

errors and omissions and other potential claims against us; and the interruption or loss of our

information processing systems or failure to maintain secure information systems.

The foregoing list of factors is not exhaustive and new factors may emerge from time to time that

could also affect actual performance and results. For more information see the section

entitled ‘‘Risk Factors’’ included in Willis’ Form 10-K for the year

ended December 31, 2012 and our subsequent filings with the Securities and Exchange Commission. Copies are

available online at http://www.sec.gov or www.willis.com.

Although we believe that the assumptions underlying our forward-looking statements are reasonable,

any of these assumptions, and therefore also the forward-looking statements based on these

assumptions, could themselves prove to be inaccurate. In light of the significant uncertainties inherent in the forward-looking statements included in this presentation, our

inclusion of this information is not a representation or guarantee by us that our objectives and plans

will be achieved. Our forward-looking statements speak only as of the date made and

we will not update these forward-looking statements unless the securities laws require us to do

so. In light of these risks, uncertainties and assumptions, the forward-looking events

discussed in this presentation may not occur, and we caution you against unduly relying on these

forward-looking statements. |

Important

disclosures regarding Non-GAAP measures This

presentation

contains

references

to

"non-GAAP

financial

measures"

as

defined

in

Regulation

G

of

SEC

rules.

We

present these measures because we believe they are of interest to the investment

community and they provide additional meaningful methods of evaluating

certain aspects of the Company’s operating performance from period to period on a basis

that may not be otherwise apparent on a generally accepted accounting principles

(GAAP) basis. These financial measures should be viewed in addition

to, not in lieu of, the Company’s condensed consolidated income statements and balance sheet

as

of

the

relevant

date.

Consistent

with

Regulation

G,

a

description

of

such

information

is

provided

below

and

a

reconciliation

of

certain

of

such

items

to

GAAP

information

can

be

found

in

our

periodic

filings

with

the

SEC.

Our

method

of

calculating

these non-GAAP financial measures may differ from other companies and therefore

comparability may be limited. Adjusted earnings per share (Adjusted EPS)

is defined as adjusted net income per diluted share.

Adjusted

net

income

is

defined

as

net

income,

excluding

certain

items

as

set

out

on

pages

21

and

22.

Adjusted operating income

is defined as operating income, excluding certain items as set out on pages 19 and

20. Adjusted

operating

margin

is

defined

as

the

percentage

of

adjusted

operating

income

to

total

revenues.

Adjusted

EBITDA

is

defined

as

Adjusted

operating

income,

excluding

depreciation

and

amortization

as

set

out

on

page

23

Organic commissions & fees growth

excludes: (i) the impact of foreign currency translation; (ii) the first twelve

months of net commission and fee revenues generated from acquisitions; (iii)

the net commission and fee revenues related to operations disposed of in

each period presented; (iv) in North America, legacy contingent commissions assumed as part of

the HRH acquisition and that had not been converted into higher standard

commission; and (v) investment income and other income from reported

revenues, as set out on pages 25 and 26. Reconciliations to GAAP measures

are provided for selected non-GAAP measures. 18

|

Important

disclosures regarding Non-GAAP measures (continued) Operating Income to

Adjusted Operating Income See related footnotes on page 24

19

2007

2008

2009

2010

2011

2012

(In millions)

FY

FY

FY

FY

FY

FY

Operating Income

$620

$503

$690

$753

$566

($209)

Excluding:

Goodwill impairment charge

(a)

-

-

-

-

-

492

Write-off of unamortized cash retention awards

(b)

-

-

-

-

-

200

2012 cash bonus accrual

(c)

-

-

-

-

-

252

Insurance recovery

(d)

-

-

-

-

-

(10)

Write-off of uncollectible accounts receivable and

legal fees

(e)

-

-

-

-

22

13

India JV settlement

(f)

-

-

-

-

-

11

2011 Operational review

(g)

-

-

-

-

180

-

Financial Services Authority regulatory settlement

(h)

-

-

-

-

11

-

Venezuela currency devaluation

(k)

-

-

-

12

-

-

Net (gain)/loss on disposal of operations

(2)

-

(13)

2

(4)

3

Salaries and benefits -

severance programs

(l)

-

24

-

-

-

-

Salaries and benefits –

other

(m)

-

42

-

-

-

-

HRH integration costs

(n)

-

5

18

-

-

-

Other operating expenses

(o)

-

26

-

-

-

-

Accelerated amortization of intangibles assets

(p)

-

-

7

-

-

-

Redomicile costs

(q)

-

-

6

-

-

-

Adjusted Operating Income

$618

$600

$708

$767

$775

$752

Operating Margin

24.0%

17.8%

21.2%

22.6%

16.4%

(6.0%)

Adjusted Operating Margin

24.0%

21.2%

21.8%

23.0%

22.5%

21.6% |

Important

disclosures regarding Non-GAAP measures (continued) Operating Income to

Adjusted Operating Income 2011

(In millions)

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

Operating Income

$239

$156

$90

$81

$317

$179

$70

($775)

Excluding:

Goodwill impairment charge

(a)

-

-

-

-

-

-

-

492

Write-off of unamortized cash retention awards

(b)

-

-

-

-

-

-

-

200

2012 cash bonus accrual

(c)

-

-

-

-

-

-

-

252

Insurance recovery

(d)

-

-

-

-

-

(5)

-

(5)

Write-off of uncollectible accounts receivable and

legal fees

(e)

-

-

-

22

13

-

-

-

India JV settlement

(f)

11

-

2011 Operational review

(g)

97

18

15

50

-

-

-

-

Financial Services Authority regulatory settlement

(h)

-

11

-

-

-

-

-

-

Net (gain)/loss on disposal of operations

(4)

-

-

-

-

-

1

2

Adjusted Operating Income

$332

$185

$105

$153

$330

$174

$82

$166

Operating Margin

23.7%

18.1%

11.8%

9.9%

31.3%

21.3%

9.3%

(89.0%)

Adjusted Operating Margin

33.0%

21.5%

13.8%

18.7%

32.6%

20.7%

10.9%

19.1%

2012

See related footnotes on page 24

20 |

Important

disclosures regarding Non-GAAP measures (continued) Net Income to Adjusted

Net Income See related footnotes on page 24

21

2007

2008

2009

2010

2011

2012

(In millions, except per share data)

FY

FY

FY

FY

FY

FY

Net Income

$409

$302

$434

$455

$203

($446)

Excluding the following, net of tax:

Goodwill impairment charge

(a)

-

-

-

-

-

458

Write-off of unamortized cash retention awards

(b)

-

-

-

-

-

138

2012 cash bonus accrual

(c)

-

-

-

-

-

175

Insurance recovery

(d)

-

-

-

-

-

(6)

Write-off of uncollectible accounts receivable and legal fees

(e)

-

-

-

-

13

8

India JV settlement

(f)

-

-

-

-

-

11

2011 Operational review

(g)

-

-

-

-

128

-

Financial Services Authority regulatory settlement

(h)

-

-

-

-

11

-

Deferred tax valuation allowance

(i)

-

-

-

-

-

113

Make-whole amounts on repurchase and redemption of Senior

Notes and write-off of unamortized debt costs

(j)

-

-

-

-

131

-

Net (gain)/loss on disposal of operations

(2)

-

(11)

3

(4)

3

Venezuela currency devaluation

(k)

-

-

-

12

-

-

Salaries

and

benefits

-

severance

programs

(l)

-

17

-

-

-

-

Salaries

and

benefits

–

other

(m)

-

30

-

-

-

-

HRH financing (pre-close) and integration costs

(n)

-

10

13

-

-

-

Other operating expenses

(o)

-

19

-

-

-

-

Accelerated amortization of intangibles assets

(p)

-

-

4

-

-

-

Redomicile costs

(q)

-

-

6

-

-

-

Premium on early redemption of 2010 bonds

(r)

-

-

4

-

-

-

Adjusted Net Income

$407

$378

$450

$470

$482

$454

Diluted shares outstanding

147

148

169

171

176

176

Net income

per diluted share

Adjusted net income

per diluted share

$1.15

$2.74

$2.66

$2.66

$2.75

$2.57

$2.77

($2.58)

$2.58

$2.78

$2.04

$2.55 |

Important

disclosures regarding Non-GAAP measures (continued) Net Income to Adjusted

Net Income See related footnotes on page 24

22

(In millions, except per share data)

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

Net Income

$35

$84

$60

$24

$225

$107

$26

($804)

Excluding the following, net of tax:

Goodwill

impairment

charge

(a)

-

-

-

-

-

-

-

458

Write-off

of

unamortized

cash

retention

awards

(b)

-

-

-

-

-

-

-

138

2012

cash

bonus

accrual

(c)

-

-

-

-

-

-

-

175

Insurance

recovery

(d)

-

-

-

-

-

(3)

-

(3)

Write-off

of

uncollectible

accounts

receivable

and

legal

fees

(e)

-

-

-

13

8

-

-

-

India

JV

settlement

(f)

-

-

-

-

-

-

11

2011

Operational

review

(g)

69

12

11

36

-

-

-

-

Financial

Services

Authority

regulatory

settlement

(h)

-

11

-

-

-

-

-

-

Deferred

tax

valuation

allowance

(i)

-

-

-

-

-

-

-

113

Net (gain)/loss on disposal of operations

(4)

-

-

-

-

-

1

2

Make-whole amounts on repurchase and redemption of

Senior

Notes

and

write-off

of

unamortized

debt

costs

(j)

124

-

1

6

-

-

-

-

Adjusted Net Income

$224

$107

$72

$79

$233

$104

$38

$79

Diluted shares outstanding

174

176

176

176

176

176

175

175

Net income

per diluted share

Adjusted net income

per diluted share

$1.28

2011

$0.41

$1.29

$0.20

$0.14

$0.45

$0.48

$0.61

$0.34

$0.22

$1.32

2012

(4.65)

$0.45

$0.61

$0.59

$0.15 |

Important

disclosures regarding Non-GAAP measures (continued) Adjusted EBITDA and

Debt/Adjusted EBITDA See related footnotes on page 24

23

2007

2008

2009

2010

2011

2012

(In millions)

FY

FY

FY

FY

FY

FY

Operating Income

$620

$503

$690

$753

$566

($209)

Excluding:

Goodwill

impairment

charge

(a)

-

-

-

-

-

492

Write-off

of

unamortized

cash

retention

awards

(b)

-

-

-

-

-

200

2012

cash

bonus

accrual

(c)

-

-

-

-

-

252

Insurance

recovery

(d)

-

-

-

-

-

(10)

Write-off of uncollectible accounts receivable and

legal

fees

(e)

-

-

-

-

22

13

India

JV

settlement

(f)

-

-

-

-

-

11

2011

Operational

review

(g)

-

-

-

-

180

-

Financial

Services

Authority

regulatory

settlement

(h)

-

-

-

-

11

-

Venezuela

currency

devaluation

(k)

-

-

-

12

-

-

Net (gain)/loss on disposal of operations

(2)

-

(13)

2

(4)

3

Salaries

and

benefits

-

severance

programs

(l)

-

24

-

-

-

-

Salaries

and

benefits

–

other

(m)

-

42

-

-

-

-

HRH integration costs

(n)

-

5

18

-

-

-

Other operating expenses

(o)

-

26

-

-

-

-

Accelerated

amortization

of

intangibles

assets

(p)

-

-

7

-

-

-

Redomicile costs

(q)

-

-

6

-

-

-

Adjusted Operating Income

$618

$600

$708

$767

$775

$752

Add back

Depreciation

52

54

64

63

69

79

Amortization of intangibles

14

36

93

82

68

59

Adjusted EBITDA

$684

$690

$865

$912

$912

$890

Debt

1,250

2,650

2,374

2,267

2,369

2,353

Debt / Adjusted EBITDA

1.8x

3.8x

2.7x

2.5x

2.6x

2.6x |

Important

disclosures regarding Non-GAAP measures (continued) Notes to the GAAP to

non-GAAP reconciliations 24

(a)

Impairment charge to reduce carrying value of North America segment goodwill. (b)

Charge to write-off unamortized balance of past cash retention awards (c)

Accrual for 2012 bonuses to be paid in 2013 (d)

Insurance recovery related to previously disclosed improperly recorded revenue in Chicago (e)

Write-off of uncollectible accounts receivable balance, together with associated legal

costs, related to a fraudulent overstatement of Commissions and Fees from the years 2004 to

2011, in a stand-alone North America business.

(f)

Settlement with former partners related to the termination of a joint venture arrangement in India. In

the third quarter of 2012, a $1 million loss on disposal of operations was recorded related to

this termination.

(g)

$180 million pre-tax charge in FY2011 relating to the 2011 operational review, including $98

million of severance costs relating to the elimination of approximately 1,200 positions in

FY2011.

(h)

Regulatory settlement with the Financial Services Authority (FSA). (i)

Valuation allowance against deferred tax assets (j)

Make-whole amounts on repurchase and redemption of Senior Notes and write-off of unamortized

debt costs

(k)

With effect from January 1, 2010, the Venezuelan economy was designated as hyper-inflationary. The

Venezuelan government also devalued the Bolivar Fuerte in January 2010. As a result of these

actions, the Company recorded a one-time charge in other expenses to reflect the re-measurement of its net

assets denominated in Venezuelan Bolivar Fuerte. (l)

Severance costs excluded from adjusted operating income and adjusted net income in 2008 relate to

approximately 350 positions through the year ended December 31, 2008 that were eliminated as

part of the 2008 expense review. Severance costs also arise in the normal course of business and these

charges (pre-tax) amounted to $24 million and $2 million for the years ended December 31, 2009 and

2008, respectively.

(m)

Other 2008 expense review salaries and benefits costs relate primarily to contract buyouts. (n)

2009 HRH integration costs include $nil million severance costs ($2 million in 2008). (o)

Other operating expenses primarily relate to property and systems rationalization. (p)

The charge for the accelerated amortization for intangibles relates to the HRH brand name.

Following the successful integration of HRH into our North American operations, we announced on

October 1, 2009 that our North America retail operations would change their name from Willis HRH to Willis North

America. Consequently, the intangible asset recognized on the acquisition of HRH relating to the

HRH brand has been fully amortized.

(q)

These are legal and professional fees incurred as part of the Company’s redomicile of its parent

Company from Bermuda to Ireland.

(r)

On September 29, 2009 we repurchased $160 million of our 5.125 percent Senior Notes due July 2010 at a

premium of $27.50 per $1,000 face value, resulting in a total premium on redemption, including

fees, of $5 million. |

Commissions and Fees Analysis

Important disclosures regarding Non-GAAP measures (continued)

25

2012

2011

Change

Foreign

currency

translation

Acquisitions

and

disposals

Contingent

Commissions

Organic

commissions

and fees

growth

(a)

($ millions)

%

%

%

%

%

Three months ended

December 31, 2012

Global

$237

$213

11.3

(0.3)

-

-

11.6

North

America

(b)

331

316

4.7

(0.3)

-

-

5.0

International

299

281

6.4

(1.0)

-

-

7.4

Commissions and Fees

$867

$810

7.0

(0.5)

-

-

7.5

Twelve months ended

December 31, 2012

Global

$1,124

$1,073

4.8

(1.3)

-

-

6.1

North

America

(b)

1,306

1,314

(0.6)

-

-

-

(0.6)

International

1,028

1,027

0.1

(4.8)

-

-

4.9

Commissions and Fees

$3,458

$3,414

1.3

(1.8)

-

-

3.1

(a)

Organic commission and fees growth excludes: (i) the impact of foreign currency translation; (ii) the

first twelve months of net commission and fee revenues generated from

acquisitions; (iii) the net commission and fee revenues related to operations disposed of in each period presented; (iv) in North America,

legacy contingent commissions assumed as part of HRH acquisition and that had not been converted into

higher standard commission; and (v) investment income and other income from reported revenues

(b)

Included in North America reported commissions and fees were legacy HRH contingent commissions of $nil

in the fourth quarter of 2012 and the fourth quarter of 2011 and $2 million in 2012

compared with $5 million in 2011. |

(a)

Included in North America reported commissions and fees were legacy HRH contingent

commissions of $5 million in 2011 compared with $11 million in 2010 and $27

million in 2009. Important disclosures regarding Non-GAAP measures

(continued) Commissions and Fees Analysis

2011

2010

Change

Foreign

currency

translation

Acquisitions

and

disposals

Contingent

Commissions

Organic

commissions

and fees

growth

($ millions)

%

%

%

%

%

2011 Full year

Global

$1,073

$987

8.7

2.0

-

-

6.7

North America

(a)

1,314

1,369

(4.0)

-

(0.4)

-

(3.6)

International

1,027

937

9.6

4.8

-

-

4.8

Commissions and Fees

$3,414

$3,293

3.7

2.1

(0.2)

-

1.8

2010

2009

Change

Foreign

currency

translation

Acquisitions

and

disposals

Contingent

Commissions

Organic

commissions

and fees

growth

($ millions)

%

%

%

%

%

2010 Full year

Global

$987

$921

7.2

-

-

-

7.2

North America

(a)

1,369

1,381

(0.9)

0.2

-

(1)

-

International

937

898

4.3

(1.8)

0.8

-

5.3

Commissions and Fees

$3,293

$3,200

2.9

(0.8)

-

-

3.7

26 |

WILLIS

GROUP HOLDINGS

WILLIS GROUP HOLDINGS

Fact Book

Fourth Quarter 2012

March 2013

WILLIS GROUP

HOLDINGS |