Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - PEABODY ENERGY CORP | btu_8-k20130306.htm |

Exhibit 99.1

Energizing The World One BTU At A Time

Raymond James Annual Institutional Investors Conference

Vic Svec Senior Vice President Investor Relations and Corporate Communications

March 6, 2013

Peabody Energy

Statement on Forward-Looking Information Peabody Energy

The use of the words “Peabody,” “the company,” “our” and “we” relate to Peabody Energy Corporation, its subsidiaries and majority-owned affiliates. Certain statements in this presentation are forward-looking within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, as amended, and are intended to come within the safe harbor protection provided by those sections. These forward-looking statements are based on numerous assumptions that the company believes are reasonable, but they are open to a wide range of uncertainties and business risks that may cause actual results to differ materially from expectations as of March 6, 2013. These factors are difficult to accurately predict and may be beyond the company's control. The company does not undertake to update its forward-looking statements. Factors that could affect the company's results include, but are not limited to: global supply and demand for coal, including the seaborne thermal and metallurgical coal markets; price volatility, particularly in higher-margin products and in our trading and brokerage businesses; impact of alternative energy sources, including natural gas and renewables; global steel demand and the downstream impact on metallurgical coal prices; impact of weather and natural disasters on demand, production and transportation; reductions and/or deferrals of purchases by major customers and ability to renew sales contracts; credit and performance risks associated with customers, suppliers, contract miners, co-shippers, and trading, banks and other financial counterparties; geologic, equipment, permitting and operational risks related to mining; transportation availability, performance and costs; availability, timing of delivery and costs of key supplies, capital equipment or commodities such as diesel fuel, steel, explosives and tires; successful implementation of business strategies; negotiation of labor contracts, employee relations and workforce availability; changes in postretirement benefit and pension obligations and funding requirements; replacement and development of coal reserves; availability, access to and related cost of capital and financial markets; effects of changes in interest rates and currency exchange rates (primarily the Australian dollar); effects of acquisitions or divestitures; economic strength and political stability of countries in which we have operations or serve customers; legislation, regulations and court decisions or other government actions, including, but not limited to, new environmental and mine safety requirements and changes in income tax regulations, sales-related royalties or other regulatory taxes; litigation, including claims not yet asserted; terrorist attacks or threats, impacts of pandemic illness; and other risks detailed in the company's reports filed with the Securities and Exchange Commission (SEC). Adjusted EBITDA is defined as income from continuing operations before deducting net interest expense, income taxes, asset retirement obligation expenses, depreciation, depletion and amortization, asset impairment and mine closure costs and amortization of basis difference associated with equity method investments. Adjusted EBITDA, which is not calculated identically by all companies, is not a substitute for operating income, net income or cash flow as determined in accordance with United States generally accepted accounting principles. Management uses Adjusted EBITDA as a key measure of operating performance and also believes it is a useful indicator of the company's ability to meet debt service and capital expenditure requirements.

Adjusted (Loss) Income from Continuing Operations and Adjusted Diluted EPS are defined as income from continuing operations and diluted earnings per share excluding asset impairment and mine closure costs, net of tax, and the impact of the remeasurement of foreign income tax accounts. Management has included these measures because, in management's opinion, excluding such impacts is useful in comparing the company's current results with those of prior and future periods. Management also believes that excluding the impact of the remeasurement of foreign income tax accounts is a better indicator of the company's ongoing effective tax rate.

03/06/2013

2

Peabody Well Positioned in Face of Mixed Market Conditions Peabody Energy

Peabody delivered record 2012 safety results, revenues, Adjusted U.S. EBITDA and Australia sales volume

2013 coal markets show early signs of rebound

Emerging markets to drive significant near-and long-term met and thermal coal demand growth

Peabody best positioned to succeed

Leading presence in growing regions: Australia, PRB and Illinois Basin

Major capital and cost containment programs to succeed in all markets

3

2012 Accomplishments

BTU Delivers Notable 2012 Accomplishments Peabody Energy

Achieved safest incident rate in company history

Set record U.S. Adjusted EBITDA of $1.26 billion

Reached record Australian sales as volumes rose 30% to 33 million tons

Strong cost control limited per-ton increase to 4% in 2012

Delivered total Adjusted EBITDA of $1.84 billion; operating cash flows of $1.52 billion

Paid down >$400 million in debt

5

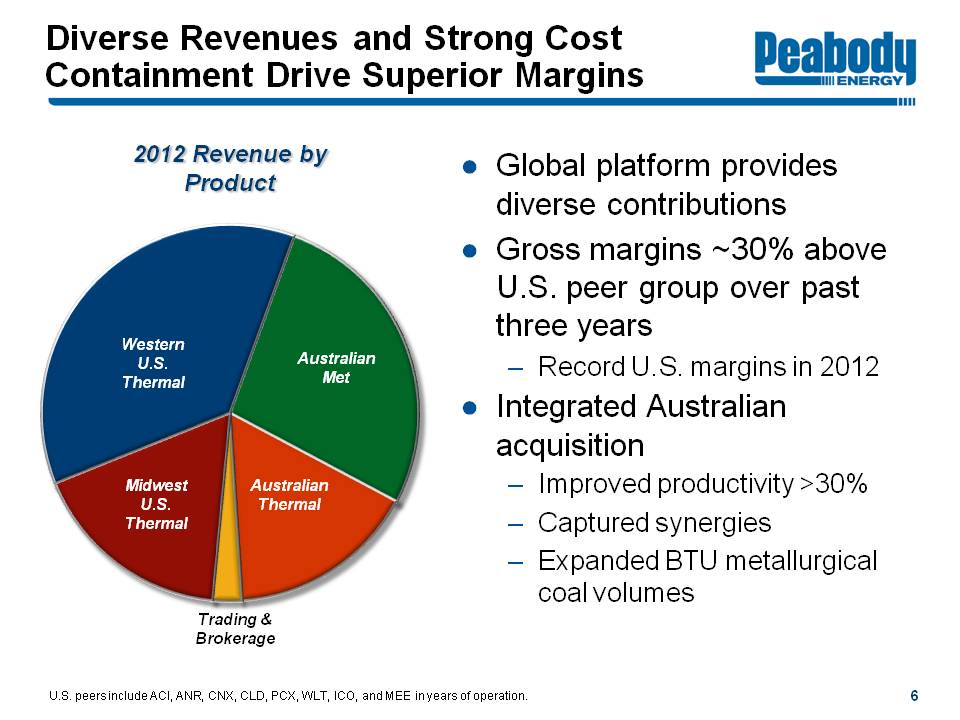

Diverse Revenues and Strong Cost Containment Drive Superior Margins Peabody Energy

2012 Revenue by Product

Western U.S. Thermal Australian Met Australian Thermal Trading & Brokerage Midwest U.S. Thermal

Global platform provides diverse contributions

Gross margins ~30% above U.S. peer group over past three years

Record U.S. margins in 2012

Integrated Australian acquisition

Improved productivity >30%

Captured synergies

Expanded BTU metallurgical coal volumes

U.S. peers include ACI, ANR, CNX, CLD, PCX, WLT, ICO, and MEE in years of operation.

6

Global Coal Markets

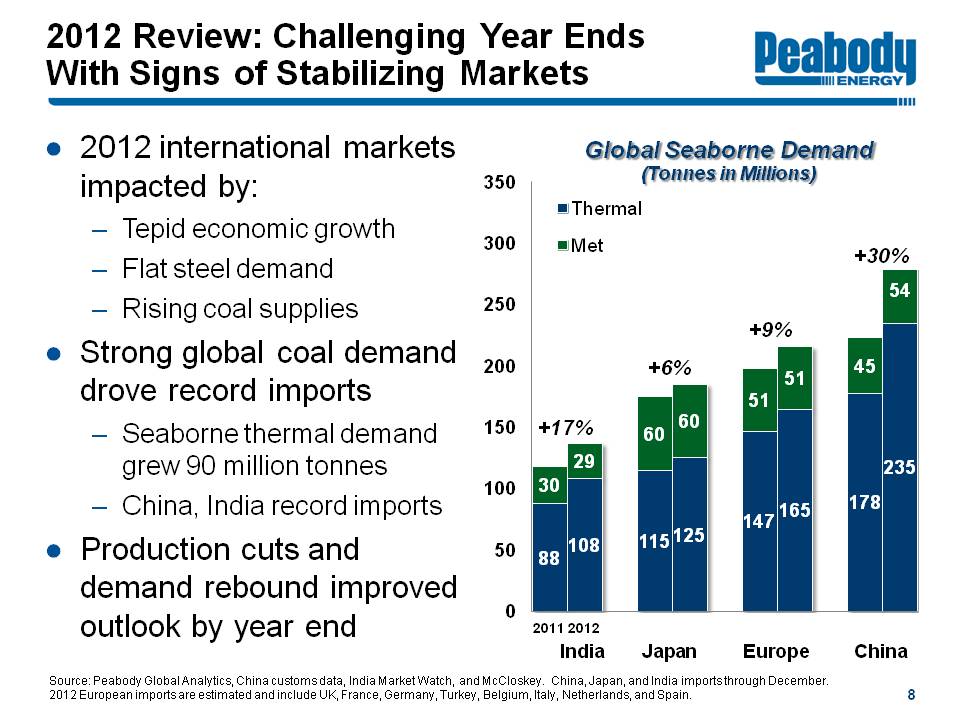

2012 Review: Challenging Year Ends With Signs of Stabilizing Markets Peabody Energy

2012 international markets impacted by: Tepid economic growth Flat steel demand Rising coal supplies

Strong global coal demand drove record imports Seaborne thermal demand grew 90 million tones China, India record imports

Production cuts and demand rebound improved outlook by year end

Global Seaborne Demand (Tonnes in Millions) 0 50 100 150 200 250 300 350

India 2011 Thermal 88 Met 30 2012 Thermal 108 Met 29 +17%

Japan 2011 Thermal 115 Met 60 2012 Thermal 125 Met 60 +6%

Europe 2011 Thermal 147 Met 51 2012 165 Met 51 +9%

China 2011 Thermal 178 Met 45 2012 Thermal 235 Met 54 +30%

Source: Peabody Global Analytics, China customs data, India Market Watch, and McCloskey. China, Japan, and India imports through December. 2012 European imports are estimated and include UK, France, Germany, Turkey, Belgium, Italy, Netherlands, and Spain.

8

2013 Markets: Early Indications of Demand Rebound Peabody Energy

Signs of accelerating Chinese growth

Expect global steel production growth of ~3% driving increased need for metallurgical coal

75W of coal generation expected to come on line, requiring 250 MTPY of coal at full capacity

Seaborne thermal market expected to increase 40+ million tonnes on growing Asian demand

Source: Peabody Global Analytics, World Steel Association

9

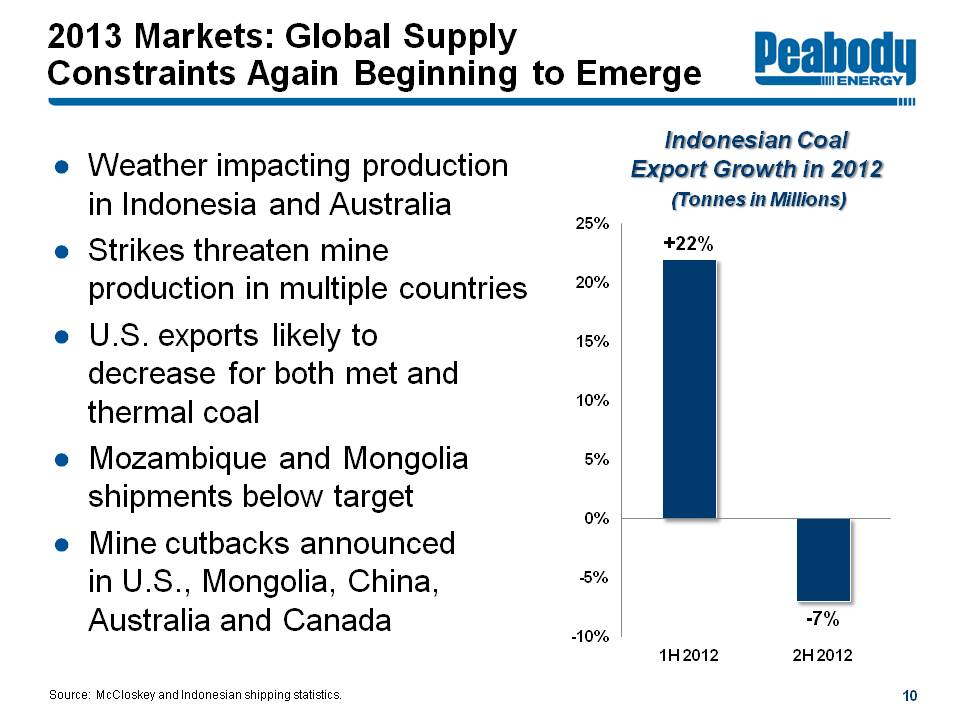

2013 Markets: Global Supply Constraints Again Beginning to Emerge Peabody Energy

Weather impacting production in Indonesia and Australia

Strikes threaten mine production in multiple countries

U.S. exports likely to decrease for both met and thermal coal

Mozambique and Mongolia shipments below target

Mine cutbacks announced in U.S., Mongolia, China, Australia and Canada

Indonesian Coal Export Growth in 2012 (Tonnes in Millions) -10% -5% 0% 5% 10% 15% 20% 25% 1H 2012 +22% 2H 2012 -7%

Source: McCloskey and Indonesian shipping statistics.

10

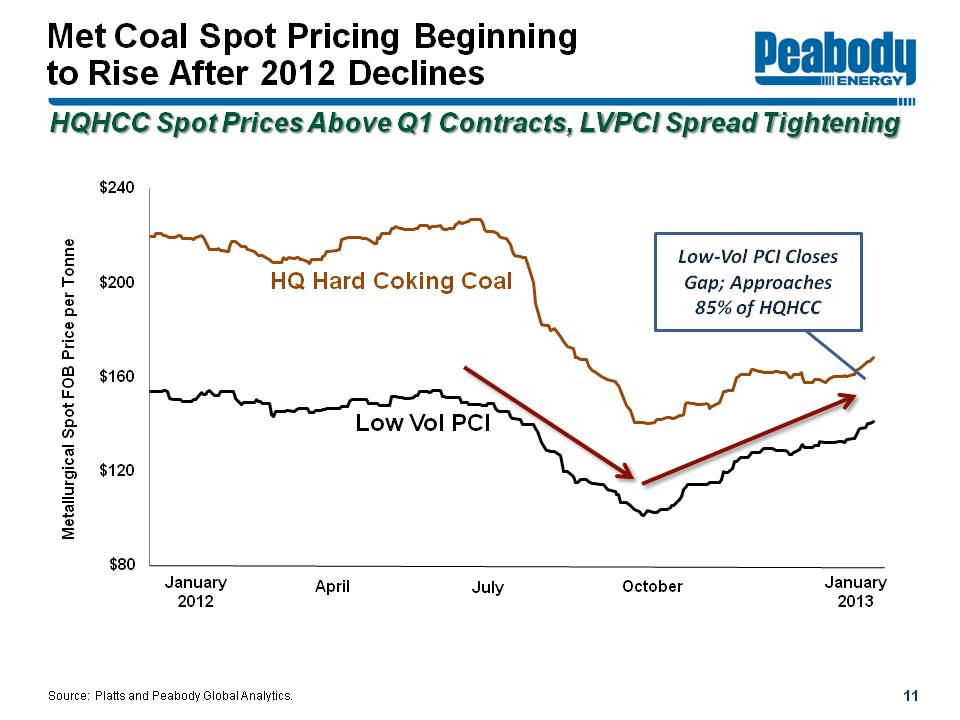

Met Coal Spot Pricing Beginning to Rise After 2012 Declines Peabody Energy

HQHCC Spot Prices Above Q1 Contracts, LVPCI Spread Tightening

Metallurgical Spot FOB Price per Tonne $80 $120 $160 $200 $240

January 2012 April July October January 2013HQ Hard Coking Coal Low Vol PCI Low-Vol PCI Closes Gap; Approaches 85% of HQHCC

Source: Platts and Peabody Global Analytics

11

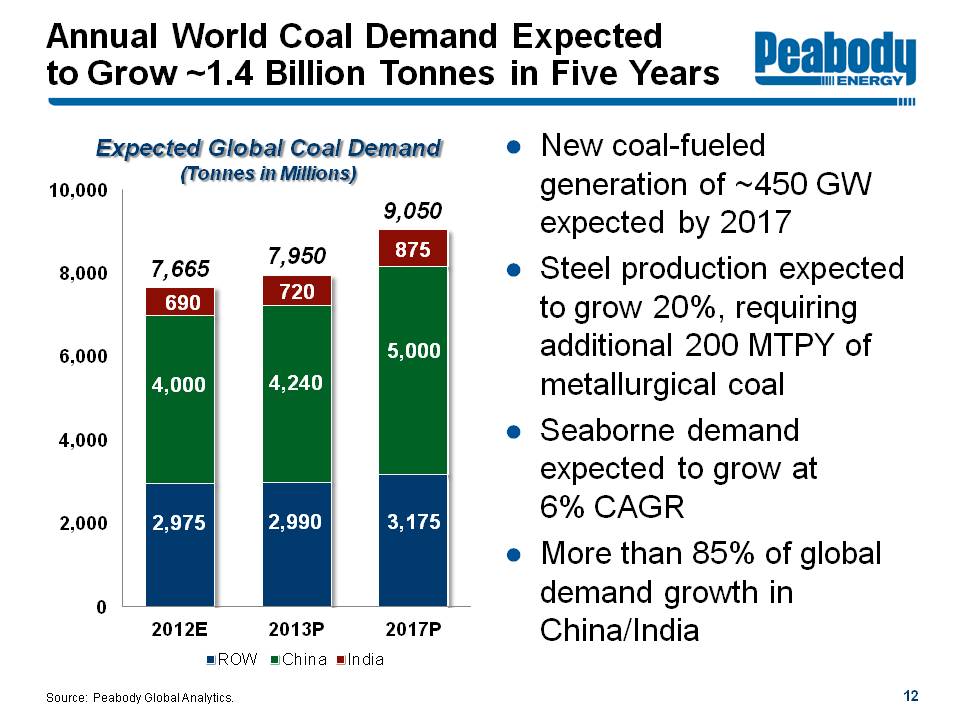

Annual World Coal Demand Expected to Grow ~1.4 Billion Tonnes in Five Years Peabody Energy

Expected Global Coal Demand (Tonnes in Millions) 0 2,000 4,000 6,000 8,000 10,000

ROW China India 2012E 7,665 2,975 4,000 690 2013P 7,950 2,990 4,240 720 2017P 9,050 3,175 5,000 875

New coal-fueled generation of ~450 GW expected by 2017

Steel production expected to grow 20%, requiring additional 200 MTPY of metallurgical coal

Seaborne demand expected to grow at 6% CAGR

More than 85% of global demand growth in China/India

Source: Peabody Global Analytics.

12

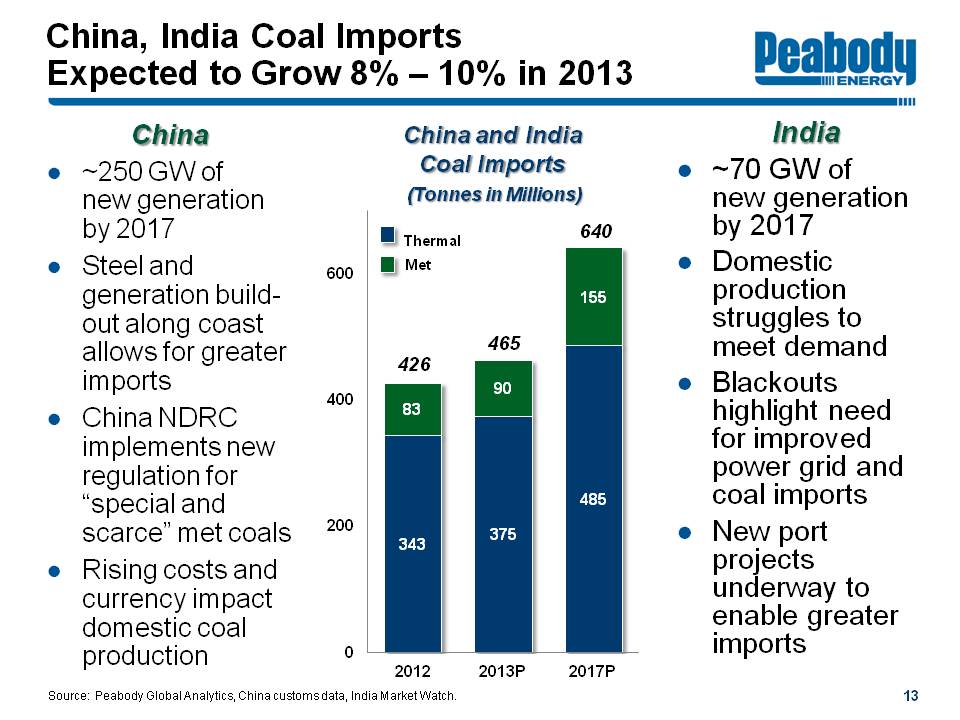

China, India Coal Imports Expected to Grow 8% - 10% in 2013 Peabody Energy

China ~250 GW of new generation 2017

Steel and generation build-out along coast allows for greater imports

China NDRC implements new regulation for “special and scarce” met coals

Rising costs and currency impact domestic production

China and India Coal Imports (Tonnes in Millions) 0 200 400 600

2012 426 Thermal 343 Met 83 2013P 465 Thermal 375 Met 90 2017P 640 Thermal 485 Met 155

India ~70 GW of new generation by 2017

Domestic production struggles to meet demand

Blackouts highlight need for improved power grid and coal imports

New port projects underway to enable greater imports

Source: Peabody Global Analytics, China customs data, India Market Watch.

13

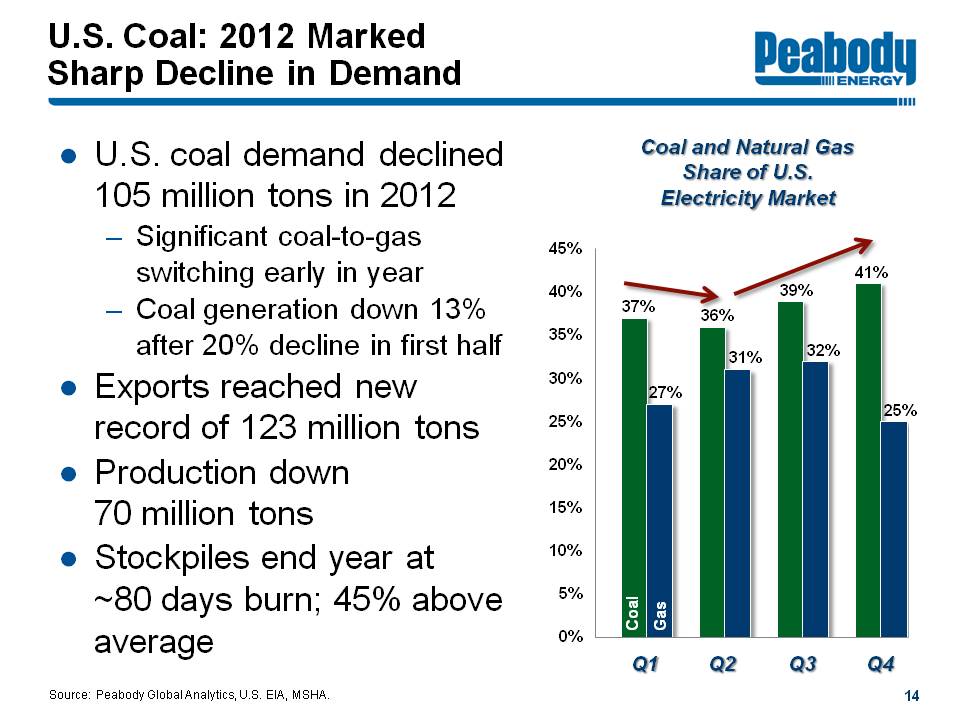

U.S. Coal: 2012 Marked Sharp Decline in Demand Peabody Energy

U.S. coal demand declined 105 million tons in 2012 Significant coal-to-gas switching early in year Coal generation down 13% after 20% decline in first half

Exports reached new record of 123 million tons

Production down 70 million tons

Stockpiles end year at ~80 days burn; 45% above average

Coal and Natural Gas Share of U.S. Electricity Market 0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Coal Gas Q1 37% 27% Q2 36% 31% Q3 39% 32% Q4 41% 25%

Source: Peabody Global Analytics, U.S. EIA, MSHA.

14

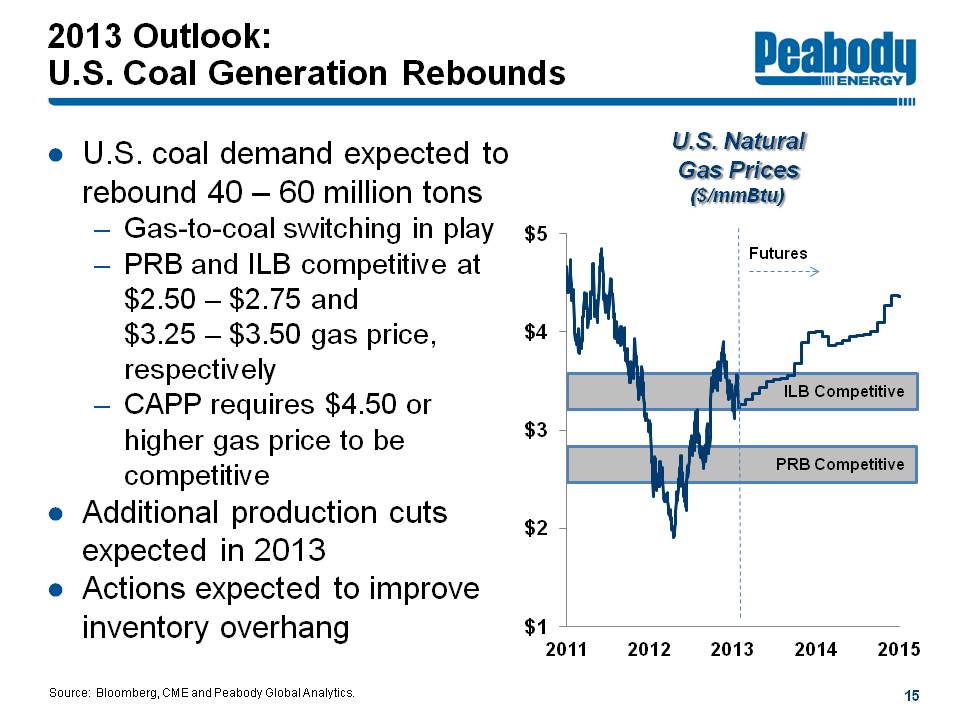

2013 Outlook: U.S. Coal Generation Rebounds Peabody Energy

U.S. coal demand expected to rebound 40 - 60 million tons Gas-to-coal switching in play PRB and ILB competitive at $2.50 - $2.75 and $3.25 - $3.50 gas price, respectively CAPP requires $4.50 or higher gas price to be competitive

Additional production cuts expected in 2013

Actions expected to improve inventory overhang

U.S. Natural Gas Prices ($/mmBtu) $1 $2 $3 $4 $5 2011 2012 2013 2014 2015

Futures ILB Competitive PRB Competitive

Source: Bloomberg, CME and Peabody Global Analytics.

15

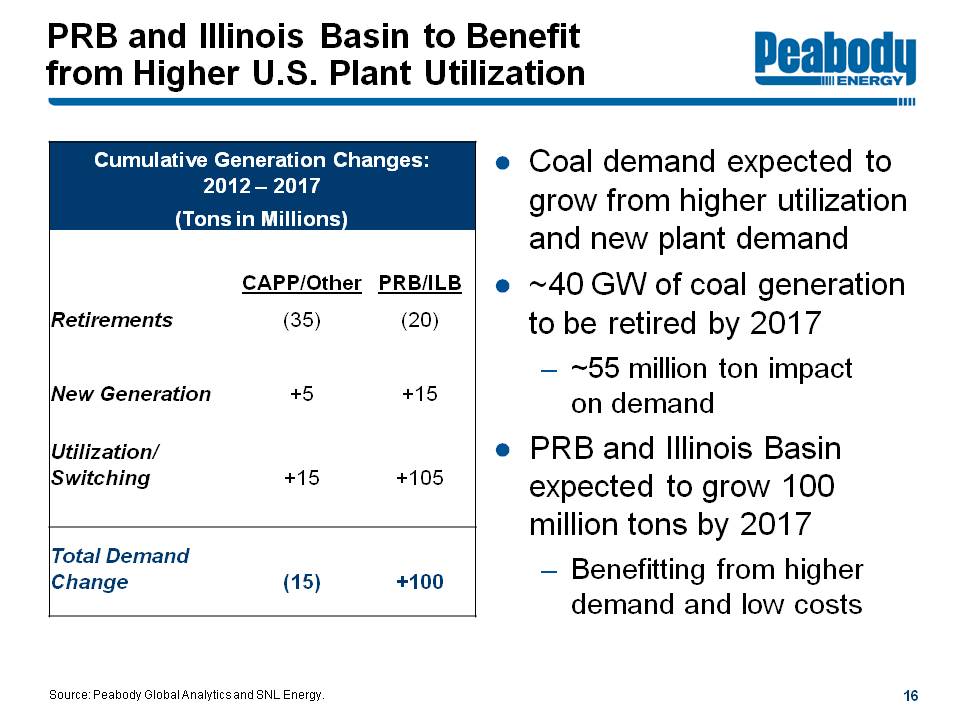

PRB and Illinois Basin to Benefit from Higher U.S. Plant Utilization Peabody Energy

Cumulative Generation Changes: 2012 - 2017 (Tons in Millions)

CAPP/Other Retirements (35) New Generation +5 Utilization/Switching +15 Total Demand Change (15)

PRB/ILB Retirements (20) New generation +15 Utilization/Switching +105 Total Demand Change +100

Coal demand expected to grow from higher utilization and new plant demand

~40 GW of coal generation to be retired by 2017 ~55 million ton impact on demand

PRB and Illinois Basin expected to grow 100 million tons by 2017 Benefitting from higher demand and low costs

Source: Peabody Global Analytics and SNL Energy.

16

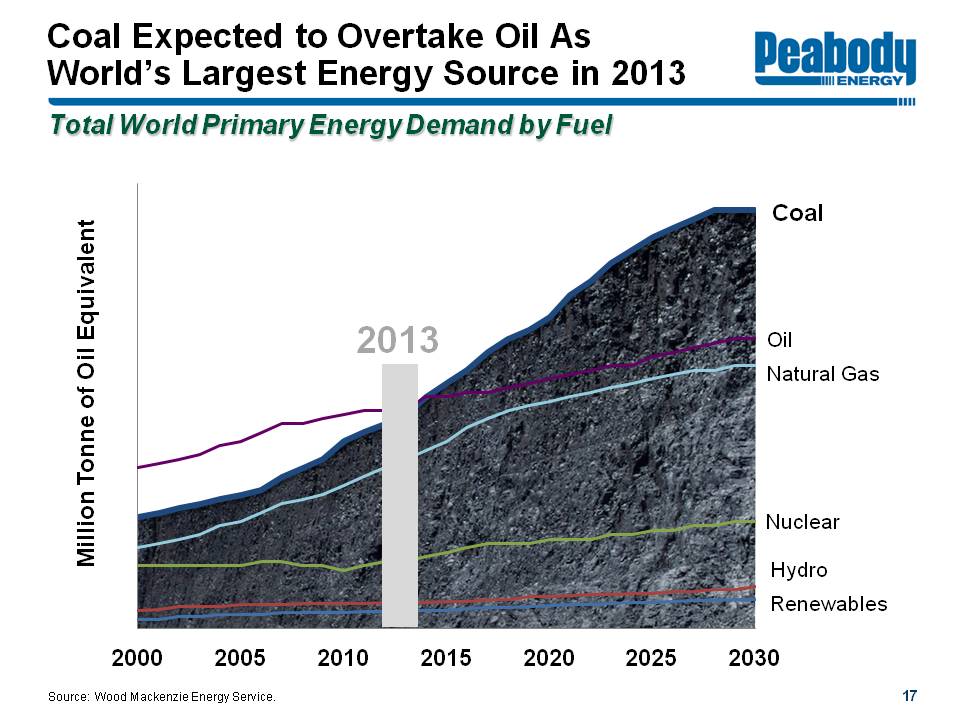

Coal Expected to Overtake Oil As World's Largest Energy Source in 2013 Peabody Energy

Total World Primary Energy Demand by Fuel

Million Tonne of Oil Equivalent 2000 2005 2010 2013 2015 2020 2025 2030 Coal Oil Natural Gas Nuclear Hydro Renewables

Source: Wood Mackenzie Energy Service

17

Peabody Focus Areas in 2013

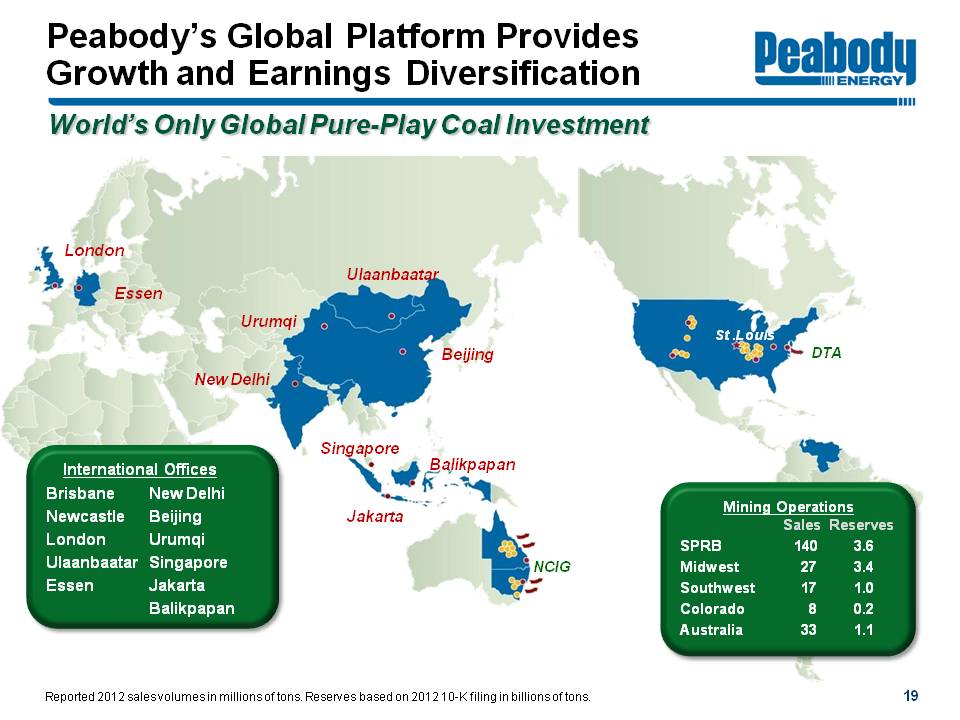

Peabody's Global Platform Provides Growth and Earnings Diversification Peabody Energy

World's Only Global Pure-Play Coal Investment

London Essen New Delhi Urumqi Ulaanbaatar Beijing Singapore Jakarta Balikpapan NCIG St. Louis DTA

International Offices Brisbane Newcastle London Ulaanbaatar Essen New Delhi Beijing Urumqi Singapore Jakarta Balikpapan

Mining Operations Sales Reserves

S. PRB 140 3.6 Midwest 27 3.4 Southwest 17 1.0 Colorado 8 0.2 Australia 33 1.1

Reported 2012 sales volumes in millions of tons. Reserves based on 2012 0-K filing in billions of tons.

19

Peabody Positioned for Success in 2013 Peabody Energy

2013 Focus Areas

Achieve operational excellence in safety, productivity and production

Reduce costs and capital at all levels of the organization

Maximize cash flow to pursue debt reduction

Position Peabody to benefit when markets recover

20

U.S. Platform Well Positioned in Current Market Peabody Energy

Maintaining highly priced 2013 position given market conditions

Targeting 180 - 190 million tons of production in 2013 90% - 95% priced for 2013; 50% - 60% priced for 2014 Revenues per ton expected to be 5% - 10% below 2012 levels

Intense focus on cost containment and capital reduction Expect stable costs per ton in 2013

Optimizing operations to maximize margins

Positioned to capitalize on U.S. coal exports

Note: Priced position as of January 29, 2013.

21

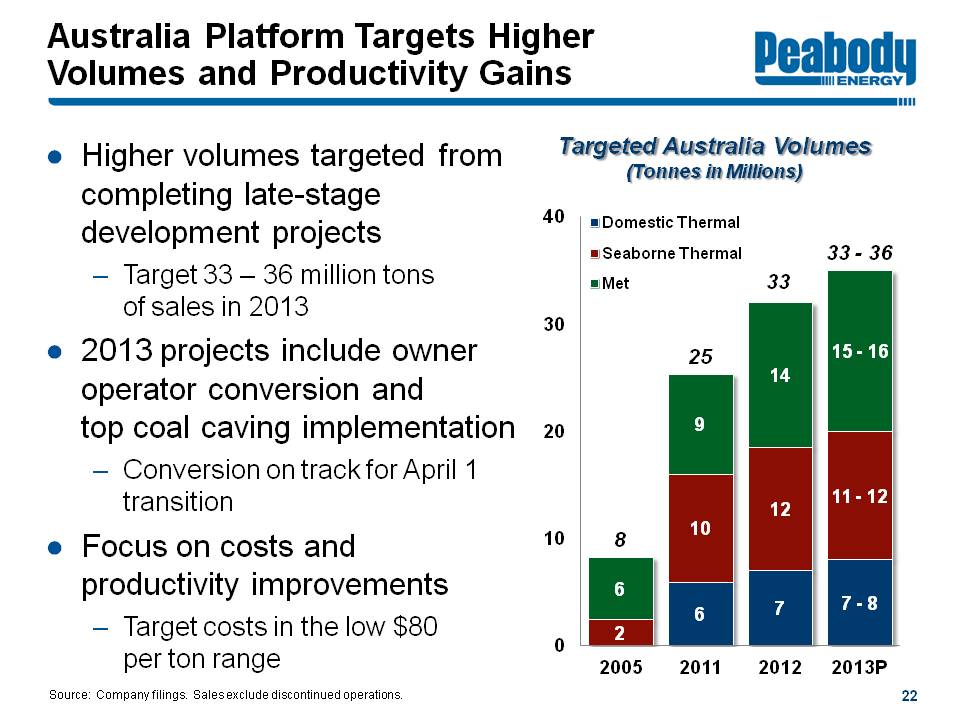

Australia Platform Targets Higher Volumes and Productivity Gains Peabody Energy

Higher volumes targeted from completing late-stage development projects Target 33 - 36 million tons of sales in 2013

2013 projects include owner operator conversion and top coal caving implementation Conversion on track for April 1 transition

Focus on costs and productivity improvements Target costs in the low $80 per ton range

Targeted Australia Volumes (Tonnes in Millions) 0 10 20 30 40

2005 8 Seaborne Thermal 2 Met 6

2011 25 Domestic Thermal 6 Seaborne Thermal 10 Met 9

2012 33 Domestic Thermal 7 Seaborne Thermal 12 Met 14

2013P 33-36 Domestic Thermal 7-8 Seaborne Thermal 11-12 Met 15-16

Source: Company filings. Sales exclude discontinued operations.

22

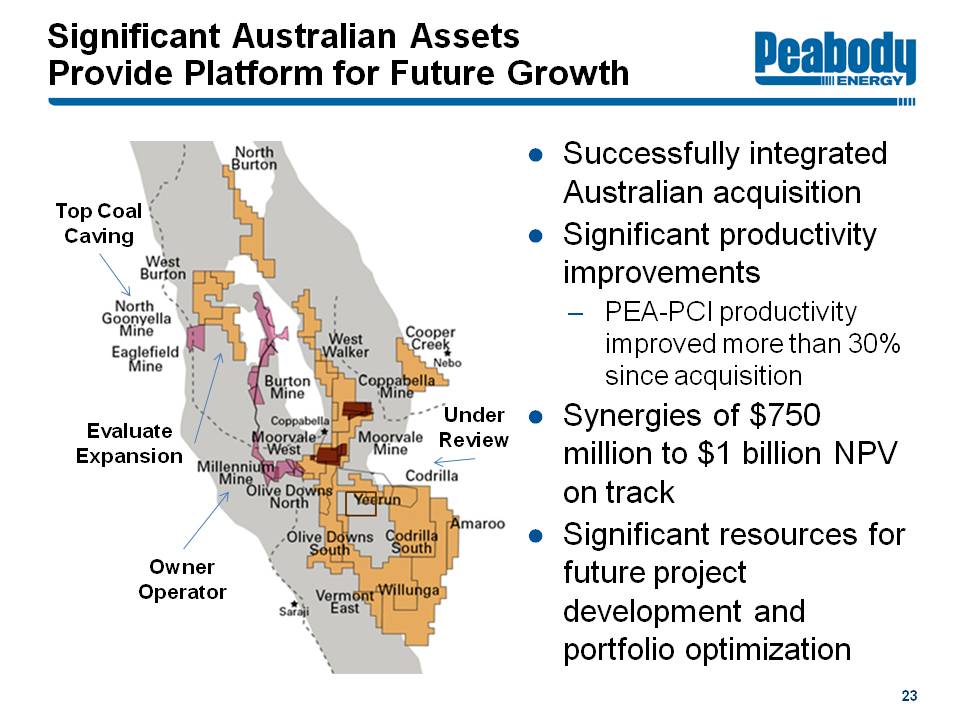

Significant Australian Assets Provide Platform for Future Growth Peabody Energy

Successfully integrated Australian acquisition

Significant productivity improvements PEA-PCI productivity improved more than 30% since acquisition

Synergies of $750 million to $1 billion NPV on track

Significant resources for future project development and portfolio optimization

Top Coal Caving North Goonyella Mine Evaluate Expansion Owner Operator Millennium Mine Under Review Codrilla

North Burton West Burton Eaglefield Mine Burton Mine West Walker Cooper Creek Nebo Coppabella Mine Coppabella Moorvale West Moorvale Mine Olive Downs North Olive Downs South Yeerun Codrilla South Amaroo Vermont East Willunga Saraji

23

2013 Outlook: Expected Increases in Earnings Following First Quarter Peabody Energy

Q1 2013 Adjusted EBITDA target: $200 - $270 million Adjusted Diluted Loss Per Share of ($0.26) - ($0.04) Reflects timing of additional overburden removal and transition costs to owner operator

Target 2013 capital spend of $450 - $550 million ~50% below 2012 spend

Full year DD&A expected to be ~10% higher than 2012 levels

Expect earnings to improve from Q1 levels on growing Australian volumes and price

24

Peabody Positioned to Meet Needs of Changing Markets Peabody Energy

Rising metallurgical and thermal coal exports from Australia

Leading position in low-cost PRB and Illinois Basin

Managing through near-term headwinds and tempering growth projects

Aggressive focus on cost control across platform

Solid operating cash flows, low maintenance capex needs and focus on debt reduction

25

Energizing The World One BTU At A Time

Raymond James Annual Institutional Investors Conference

Vic Svec Senior Vice President Investor Relations and Corporate Communications

March 6, 2013

Peabody Energy

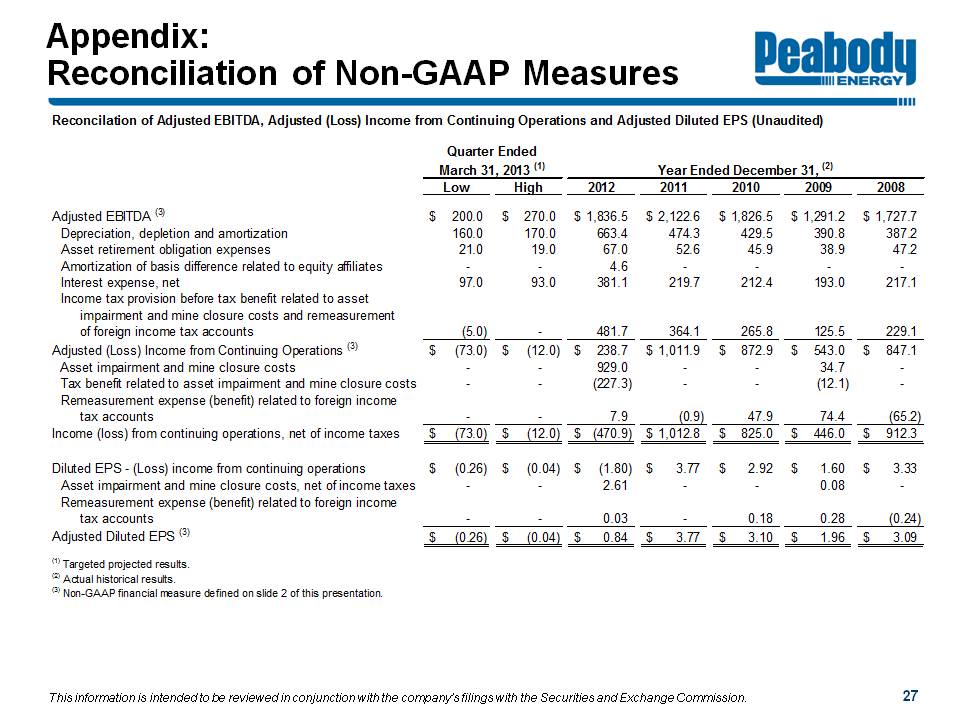

Appendix: Reconciliation of Non-GAAP Measures Peabody Energy

Reconciliation of Adjusted EBITDA, Adjusted (Loss) Income from Continuing Operations and Adjusted Diluted EPS (Unaudited)

Quarter Ended March 31, 2013(1) Year Ended December 31, (2)

Low High 2012 2011 2010 2009 2008

Adjusted EBITDA(3) $200.0 $270.0 $1,836.5 $2,122.6 $1,826.5 $1,291.2 $1,727.7

Depreciation, depletion and amortization 160.0 170.0 663.4 474.3 429.5 390.8 387.2

Asset retirement obligation expenses 21.0 19.0 67.0 52.6 45.9 38.9 47.2

Amortization of basis difference related to equity affiliates - - 4.6 - - - -

Interest expense, net 97.0 93.0 381.1 219.7 212.4 193.0 217.1

Income tax provision before tax benefit related to asset impairment and mine closure costs and remeasurement of foreign tax accounts (5.0) - 481.7 364.1 265.8 125.5 229.1

Adjusted (Loss) Income from Continuing Operations (3) $(73.0) $(12.0) $238.7 $1,011.9 $872.9 $543.0 $847.1

Asset impairment and mine closure costs - - 929.0 - - 34.7 -

Tax benefit related to asset impairment and mine closure costs - - (227.3) - - (12.1) -

Remeasurement expense (benefit) related to foreign income tax accounts - - 7.9 (0.9) 47.9 74.4 (65.2)

Income (loss) from continuing operations, net of income taxes $(73.0) $(12.0) $(470.9) $1,012.8 $ 825.0 $446.0 $912.3

Diluted EPS - (Loss) income from continuing operations $(0.26) $(0.04) $(1.80) $2.92 $1.60 $ 3.33

Asset impairment and mine closure costs, net of income taxes - - 2.61 - - 0.08 -

Remeasurement expense (benefit) related to foreign income tax accounts - - 0.03 - 0.18 0.28 (0.24)

Adjusted Diluted EPS (3) $(0.26) $(0.04) $0.84 $3.77 $ 3.10 $1.96 $3.09

(1) Targeted projected results.

(2) Actual historical results

(3) Non-GAAP financial measure defined on slide 2 of this presentation.

This information is intended to be reviewed in conjunction with the company's filings with the Securities and Exchange Commission

27