Attached files

| file | filename |

|---|---|

| 8-K - 8-K - FNB CORP/PA/ | d491475d8k.htm |

Vincent J. Delie, Jr.

President and Chief Executive Officer

Vincent J. Calabrese, Jr.

Chief Financial Officer

F.N.B. Corporation

Investor Presentation

KBW Boston Bank Conference

Dated: February 26, 2013

Exhibit 99.1 |

This

presentation

and

the

reports

F.N.B.

Corporation

files

with

the

Securities

and

Exchange

Commission

often

contain

“forward-looking

statements”

relating

to

present or future trends or factors affecting the banking industry and, specifically, the

financial operations, markets and products of F.N.B. Corporation. These

forward-looking statements involve certain risks and uncertainties. There are a number of

important factors that could cause F.N.B. Corporation’s future results to differ

materially from historical performance or projected performance. These factors include, but are not limited to: (1) a significant increase in competitive

pressures

among

financial

institutions;

(2)

changes

in

the

interest

rate

environment

that

may

reduce

interest

margins;

(3)

changes

in

prepayment

speeds,

loan

sale volumes, charge-offs and loan loss provisions; (4) general economic conditions; (5)

various monetary and fiscal policies and regulations of the U.S. government that may

adversely affect the businesses in which F.N.B. Corporation is engaged; (6) technological issues which may adversely affect F.N.B.

Corporation’s financial operations or customers; (7) changes in the securities markets;

(8) housing prices; (9) job market; (10) consumer confidence and spending habits; (11)

estimates of fair value of certain F.N.B. Corporation assets and liabilities; (12) in connection with the pending mergers with Annapolis Bancorp, Inc.

and Parkview Financial Corp., difficulties encountered in expanding into a new market; or (13)

the effects of current, pending and future legislation, regulation and

regulatory

actions;

or

(14)

other

risk

factors

mentioned

in

the

reports

and

registration

statements

F.N.B.

Corporation

files

with

the

Securities

and

Exchange

Commission. F.N.B. Corporation undertakes no obligation to revise these

forward-looking statements or to reflect events or circumstances after the date of this

presentation.

To

supplement

its

consolidated

financial

statements

presented

in

accordance

with

Generally

Accepted

Accounting

Principles

(GAAP),

the

Corporation

provides

additional measures of operating results, net income and earnings per share (EPS) adjusted to

exclude certain costs, expenses, and gains and losses. The Corporation believes

that these non-GAAP financial measures are appropriate to enhance the understanding of its past performance as well as prospects for its

future performance. In the event of such a disclosure or release, the Securities and

Exchange Commission’s Regulation G requires: (i) the presentation of the most

directly comparable financial measure calculated and presented in accordance with GAAP and (ii) a reconciliation of the differences between the non-GAAP

financial

measure

presented

and

the

most

directly

comparable

financial

measure

calculated

and

presented

in

accordance

with

GAAP.

The

required

presentations

and

reconciliations

are

contained

herein

and

can

be

found

at

our

website,

www.fnbcorporation.com,

under

“Shareholder

and

Investor

Relations”

by

clicking

on

“Non-GAAP Reconciliation.”

The Appendix to this presentation contains non-GAAP financial measures used by the

Corporation to provide information useful to investors in understanding the

Corporation's operating performance and trends, and facilitate comparisons with the

performance of the Corporation's peers. While the Corporation believes that these

non-GAAP financial measures are useful in evaluating the Corporation, the information should be considered supplemental in nature and not as a

substitute

for

or

superior

to

the

relevant

financial

information

prepared

in

accordance

with

GAAP.

The

non-GAAP

financial

measures

used

by

the

Corporation

may differ from the non-GAAP financial measures other financial institutions use to

measure their results of operations. This information should be reviewed in

conjunction with the Corporation’s financial results disclosed on January 23, 2013 and in

its periodic filings with the Securities and Exchange Commission. Cautionary

Statement Regarding Forward-Looking Information and Non-GAAP

Financial Information 2 |

Additional Information About the Mergers

3

INFORMATION ABOUT THE MERGER WITH PVFC

F.N.B. Corporation (FNB) and PVF Capital Corp. (PVFC) will file a proxy statement/prospectus

and other relevant documents with the SEC in connection with their pending

merger. SHAREHOLDERS OF PVF CAPITAL CORP. ARE ADVISED TO READ THE PROXY

STATEMENT/PROSPECTUS WHEN IT BECOMES AVAILABLE AND ANY OTHER RELEVANT DOCUMENT FILED

WITH THE SEC, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THOSE DOCUMENTS, BECAUSE THEY WILL CONTAIN

IMPORTANT INFORMATION.

FNB, PVFC and certain of their directors and executive officers may be deemed to be

participants in the solicitation of proxies from shareholders of PVFC in connection

with the proposed merger. The proxy statement/prospectus, when it becomes available, will describe any interest in the merger they may have.

INFORMATION ABOUT THE MERGER WITH ANNB

In

connection

with

the

pending

merger

between

FNB

and

Annapolis

Bancorp,

Inc.

(ANNB),

FNB

has

filed

a

Registration

Statement

on

Form

S-4

(Registration

No. 333-186159) with the SEC, which includes a Proxy Statement of ANNB and a Prospectus of

FNB. STOCKHOLDERS OF ANNAPOLIS BANCORP, INC. ARE ADVISED TO READ THE REGISTRATION

STATEMENT AND THE PROXY STATEMENT/PROSPECTUS REGARDING

THE

MERGER

AND

ANY

OTHER

RELEVANT

DOCUMENTS

FILED

WITH

THE

SEC,

AS

WELL

AS

ANY

AMENDMENTS

OR

SUPPLEMENTS

TO

THOSE

DOCUMENTS, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION.

FNB, ANNB and certain of their directors and executive officers may be deemed to be

participants in the solicitation of proxies from the stockholders of ANNB in connection

with the merger. A description of their interests in the merger is included in the proxy statement/prospectus of ANNB and FNB.

HOW TO OBTAIN ADDITIONAL INFORMATION

Free copies of the documents referred to above may be obtained, free of charge, at the

SEC’s website at www. sec.gov, or by contacting any of the persons listed

below: For documents filed by FNB --

James G. Orie, Chief Legal Officer, F.N.B. Corporation, One F.N.B. Boulevard, Hermitage, PA

16148, telephone (724) 983-3317 For documents filed by PVFC --

Jeffrey N. Male, Secretary, PVF Capital Corp., 30000 Aurora Road, Solon, OH 44139, telephone

(440) 248-7171 For documents filed by ANNB --

Edward J. Schneider, Treasurer and Chief Financial Officer, Annapolis Bancorp, Inc., 1000

Bestgate Road, Suite 400, Annapolis, MD 21401, telephone (410) 224-4455

This communication does not constitute an offer of any securities for sale.

|

4

F.N.B. Corporation |

Key

Investment Considerations 5

Positioned to Achieve Long-Term Growth

1.

Experienced leadership

2.

Sustainable business model

3.

Attractive market position

4.

Consistent, strong operating results and favorable trends

5.

Proven, disciplined acquisition strategy

6.

Investment thesis geared toward shareholder value creation |

F.N.B. Corporation

6

(1) Pro-forma for pending acquisitions of ANNB, scheduled to close 4/2013 with expected

total assets of $0.4 billion, loans of $0.3 billion, deposits of $0.3 billion

and

8

banking

locations

and

PVFC,

expected

to

close

3Q13

with

expected

assets

of

$0.8

billion,

loans

of

$0.6

billion,

deposits

of

$0.6

billion

and

16

baking locations; (2) SNL Financial, Pro-forma, Excludes custodian bank; (3) As of

February 21, 2013 |

Years of

Banking

Experience

Joined FNB

Prior Experience

President and CEO

Vincent J. Delie, Jr.

26

2005

National City

President, First National Bank

John C. Williams, Jr.

42

2008

Huntington

National City

Mellon Bank

Chief Financial Officer

Vincent J. Calabrese, Jr.

25

2007

People’s United

Chief Credit Officer

Gary L. Guerrieri

27

2002

FNB

Promistar

Experienced Leadership

7

Experienced and respected executive management team |

Sustainable Business Model

8

Sustainable Business Model

Risk Management

Maintain low risk

profile

Target neutral interest

rate risk position

Fund loan growth with

deposits

Adhere to consistent

underwriting and

pricing standards

Maintain rigid expense

control

Efficient capital

management

Growth

Organic growth:

Investments in people,

product development,

high-growth potential

market segments

Acquisition-related

growth:

Culture

Attract, retain and

develop top talent

Strong cross-sell

environment

Holistic incentive

compensation

structure supports

cross-functional focus

Monitor external and

internal service

excellence, quality and

satisfaction

Recognize

accomplishments and

innovation

Shareholder Value

Disciplined, growth

oriented focus guided

by commitment to

shareholder value

Long-term investment

thesis centered on:

Regional model

Best-in-class,

enterprise-wide

sales management

Deep product set

Disciplined,

strategic, accretive

Targeted EPS

growth

Strong dividend |

9

Reposition and Reinvest Strategy |

Reposition and

Reinvest Strategy 10

Talent

Management

Geographic

Segmentation

Sales

Management/Cross-Sell

Product

Development

Branch

Optimization

Electronic

Delivery

Investment

Expansion

Through

Acquisition

Consistent, strong operating results

Revenue growth

Consistent, organic growth

14 consecutive quarters organic total loan growth

15 consecutive quarters organic core commercial

loan growth

Attractive market position

Expanded market share potential via entry and expansion

in attractive markets

Strong 3-year total shareholder return

Strategic Actions Drive Long-Term Growth and Performance

Actions

Results |

Reposition and

Reinvest Strategy – 2009-2013 Significant Actions

11

2009

2010

2011

2012

2013

PEOPLE

Talent Management

Strengthened team through key

hires; Continuous team

development

Attract, retain, develop best talent

Geographic Segmentation

Regional model

Regional

Realignment

PROCESS

Sales Management/Cross Sell

Proprietary sales management

system developed and

implemented: Balanced

scorecards, cross-functional

alignment

Consumer

Banking

Scorecards

Consumer Banking Refinement/Daily Monitoring

Commercial

Banking Sales

Management

Expansion to additional lines of business

PRODUCT

Product Development

Deepened product set and niche

areas allow FNB to successfully

compete with larger banks and

gain share

Private Banking

Capital Markets

Online and mobile banking investment /implementation

Asset Based

Lending

Small Business

Realignment

Treasury

Management

PRODUCTIVITY

Branch Optimization

Continuous evolution of branch

network to optimize profitability

and growth prospects

De-Novo Expansion

Consolidate 37

Branches

Continued

Evaluation

Acquisitions

Opportunistically expand

presence in attractive markets

CB&T

Parkvale

ANNB and PVFC |

Cross-Functional Sales Management Drives Growth

12

“What Gets Measured Gets Done”

A cross-functional, disciplined sales

management process drives loan growth and

growth in lower-cost transaction deposits,

supporting the net interest margin, delivering

greater profitability and deepening the client

relationship.

$4.4

$3.9

$3.3

$3.1

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

$4.5

$5.0

12/31/2012

12/31/2011

12/31/2010

12/31/2009

Commercial Loan Portfolio

$2.8

$2.2

$1.7

$1.5

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

12/31/2012

12/31/2011

12/31/2010

12/31/2009

DDA's and Customer Repos

$2.6

$2.2

$2.0

$1.9

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

12/31/2012

12/31/2011

12/31/2010

12/31/2009

Consumer Loan Portfolio

(1)

(2)

Balances shown are period-end balances, $ in billions.

(1)

Core commercial loan portfolio, excluding the Florida portfolio;

(2) Consumer loans excludes the residential portfolio. |

13

Market Position |

Top

Market Overall Position 14

Source: SNL Financial, deposit data as of June 30, 2012, pro-forma as of February

21, 2013, excludes custodian bank FNB Pennsylvania Counties of Operation

Rank

Institution

Branch

Count

Total Market

Deposits

($ 000)

Total

Market

Share

(%)

1

PNC Financial Services

306

53,477,806

34.1

2

Royal Bank of Scotland

209

10,728,368

6.5

3

F.N.B. Corporation

228

8,548,326

5.7

4

M&T Bank Corp.

130

6,703,099

4.5

5

Wells Fargo & Co.

65

4,776,100

3.2

6

First Commonwealth

101

3,957,651

2.6

7

Banco Santander

75

3,854,650

2.6

8

Dollar Bank

37

3,453,494

2.3

9

First Niagara Financial

74

3,147,291

2.1

10

Susquehanna Bancshares

80

3,123,468

2.1

Total (1-134)

2,456

149,889,192

100.0

FNB

holds

the

#3

overall

retail

market

position

for

Pennsylvania

counties

of

operation

and

#5

position

for

all

counties

FNB All Counties of Operation

Rank

Institution

Branch

Count

Total Market

Deposits

($ 000)

Total

Market

Share

(%)

1

PNC Financial Services

460

60,155,071

25.9

2

Royal Bank of Scotland

298

14,949,617

6.4

3

KeyCorp

99

11,129,246

4.8

4

Huntington Bancshares

224

10,492,839

4.5

5

F.N.B. Corporation

270

10,135,228

4.4

6

M&T Bank Corp.

151

8,603,725

3.7

7

FirstMerit Corp.

104

6,513,189

2.8

8

TFS Financial Corp

22

6,162,459

2.6

9

Wells Fargo & Co.

76

5,575,216

2.4

10

Dollar Bank

66

5,172,305

2.2

Total (1-213)

3,822

232,660,382

100.0 |

Banking Footprint –

Regional View

15

Source: SNL Financial, Pro-Forma

(1) Includes expected regions associated with pending acquisitions.

FNB’s

regional

model

utilizes

six

regions,

including

three

in

top

30

MSA

markets,

with

each

region

having

a

regional

headquarters

housing

cross-functional

teams.

(1)

Top 30 MSA Presence

MSA

Population

Baltimore

2.7 million

(#20 MSA)

Pittsburgh

2.4 million

(#22 MSA)

Cleveland

2.1 million

(#28 MSA) |

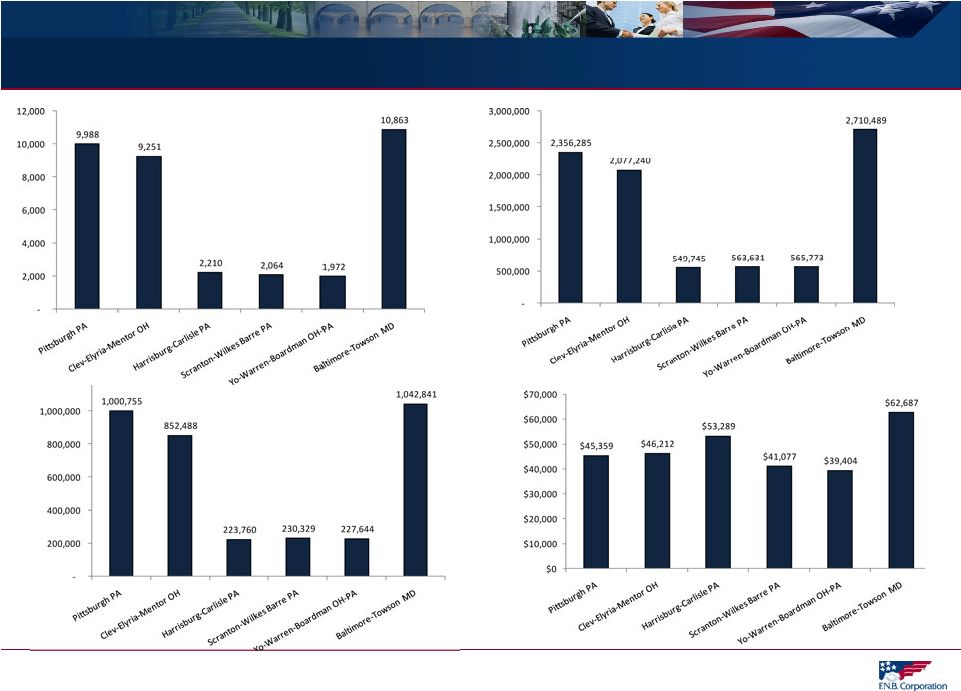

Market Position and Opportunity

16

MSA Statistics

Pittsburgh, PA

Cleveland, OH

Baltimore, MD

FNB Presence

Deposits

(1)

$3.5 billion

$0.06 billion

$0.34 billion

% of FNB Total Deposits

(1)

39%

1%

4%

Deposit Market Share

(1) (2)

4.5%

0.1%

0.5%

Deposit Market Rank

(1) (2)

#3

#27

#20

FNB’s market presence

Established,

achieving #3 rank in

2012

Expanded,

via pending PVFC

acquisition

Entry,

via pending ANNB

acquisition

Market

Deposits

(2)

$96.7 billion

$50.3 billion

$63.6 billion

U.S. Deposit Rank 2012

#17

#32

#25

Population

(2)

2.4 million

2.1 million

2.7 million

U.S. Population Rank

#22

#28

#20

Households

(2)

1.0 million

0.9 million

1.0 million

Median Household Income

$45,359

$46,212

$62,687

Unemployment

(3)

7.2%

6.5%

7.0%

Companies with Revenue >$1 Million

9,988

9,251

10,863

(1)

Pro-forma,

as

of

June

30,

2012,

market

share

rank

excludes

custodian

bank;

(2)

Data

per

SNL

(3)

Data

per

the

Bureau

of

Labor

Statistics

for

December

2012

FNB’s presence in major MSA’s provides opportunity

|

Market Opportunity

17

Note: Above metrics at the MSA level

(1)

Data per Hoover’s as of February 2, 2013

(2)

Data per SNL Financial

# of Companies with Revenue Greater Than $1 Million

(1)

Population

(2)

Median Household Income

(2)

# of Households

(2) |

#3

Position in the Pittsburgh MSA 18

Source: MSA population per U.S. Census Bureau 2010 data; Deposit market share per SNL

Financial as of June 30, 2012, pro-forma as of January 25, 2013 Population

Rank

MSA

(000's)

#1

#2

#3

1

New York

(1)

18,897

JPM

BofA

Citi

2

Los Angeles

12,829

BofA

Wells Fargo

Mitsubishi UFJ

3

Chicago

9,461

JPM

BMO

BofA

4

Dallas

6,372

BofA

JPM

Wells Fargo

5

Philadelphia

5,965

TD

Wells Fargo

HSBC

6

Houston

5,947

JPM

Wells Fargo

BofA

7

Washington

5,582

Capital One

Wells Fargo

BofA

8

Miami

5,565

Wells Fargo

BofA

Citi

9

Atlanta

5,269

SunTrust

Wells Fargo

BofA

10

Boston

4,552

BofA

RBS

Banco Santander

11

San Francisco

4,335

BofA

Wells Fargo

Citi

12

Detroit

4,296

JPM

Comerica

BofA

13

Riverside

4,225

BofA

Wells Fargo

JPM

14

Phoenix

4,193

Wells Fargo

JPM

BofA

15

Seattle

3,440

BofA

Wells Fargo

U.S. Bancorp

16

Minneapolis

(1)

3,280

Wells Fargo

U.S. Bancorp

TCF

17

San Diego

3,095

Wells Fargo

Mitsubishi UFJ

BofA

18

St. Louis

2,813

U.S. Bancorp

BofA

Commerce

19

Tampa

2,783

BofA

Wells Fargo

SunTrust

20

Baltimore

2,710

BofA

M&T

PNC

21

Denver

2,543

Wells Fargo

FirstBank

U.S. Bancorp

22

Pittsburgh

(1)

2,356

PNC

RBS

23

Portland

2,226

BofA

U.S. Bancorp

Wells Fargo

24

Sacramento

2,149

Wells Fargo

BofA

U.S. Bancorp

25

San Antonio

2,143

Cullen/Frost

BofA

Wells Fargo

Top 3 Banks in MSA by Deposit Market Share

FNB is uniquely

positioned as

one of only very

few community

banks to hold a

Top 3 deposit

market rank in

one of the

nation’s 25

largest

metropolitan

statistical areas.

F.N.B. Corporation |

19

Strong Operating Results

Favorable Trends |

Strong Operating Results and Favorable Trends

20

2012

2011

2010

Consistent

Earnings

Growth

(1)

Net income -

operating

$117,835

$90,285

$68,201

Earnings per diluted share –

operating

$0.84

$0.72

$0.60

Profitability

Performance

ROTE

(1)

18.77%

16.32%

14.71%

ROTA

(1)

1.12%

1.02%

0.87%

Net interest margin

3.73%

3.79%

3.77%

Efficiency ratio

57.7%

59.7%

60.7%

Strong Organic

Balance Sheet

Growth

Trends

(2)

Total loan growth

(3)

7.0%

6.7%

5.1%

Commercial loan growth

(3)

9.8%

9.6%

5.7%

Consumer loan growth

10.2%

6.2%

4.6%

Transaction deposits and customer repo growth

(4)

13.3%

5.8%

8.9%

(1) Adjusted results, refer to Appendix for details; (2)Period-end organic growth results

(organic reflects adjustments for balances acquired via the Parkvale and

CBT

acquisitions

where

applicable);

(3)

Excludes

the

Florida

commercial

portfolio;

(4)

Excludes

time

deposits |

Earnings Per Share Trends

21

10%

2012 Year-over-Year

PPNR EPS Growth

17%

2012 Year-over-Year

EPS Growth

(1) Operating results, refer to Appendix for details

Pre-Provision Net Revenue EPS

(1)

$1.45

$1.32

$1.30

$0.75

$0.85

$0.95

$1.05

$1.15

$1.25

$1.35

$1.45

$1.55

2012

2011

2010

$0.84

$0.72

$0.60

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90

2012

2011

2010

Operating EPS

(1) |

58%

60%

61%

30%

35%

40%

45%

50%

55%

60%

65%

2012

2011

2010

Profitability Trends

22

Efficiency Ratio

3.73%

3.79%

3.77%

3.00%

3.10%

3.20%

3.30%

3.40%

3.50%

3.60%

3.70%

3.80%

3.90%

2012

2011

2010

Net Interest Margin

18.77%

16.32%

14.71%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

2012

2011

2010

ROTE

(1)

1.12%

1.02%

0.87%

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

2012

2011

2010

ROTA

(1)

(1) Operating results, refer to Appendix for details |

Industry Leading Loan Growth

23

14

th

consecutive quarter of total loan growth

15

th

consecutive quarter of Core commercial portfolio growth

(1)

Reflects linked-quarter average organic loan growth results on an annualized basis

Total Loans

Over three years of consecutive quarterly organic loan growth accomplished

Core Commercial Portfolio |

Net

Interest Margin Trends 24

Net Interest Margin Trends |

Asset Quality Results

(1)

25

$ in thousands

2012

2011

2010

NPL’s+OREO/Total loans+OREO

1.60%

2.15%

2.74%

Total delinquency

1.64%

2.08%

2.31%

Provision for loan losses

(2)

$31,302

$33,641

$47,323

Net charge-offs (NCO’s)

(2)

$27,590

$39,099

$45,858

NCO’s/Total average loans

(2)

0.35%

0.58%

0.77%

NCO’s/Total average originated loans

0.41%

0.62%

0.77%

Allowance for loan losses/

Total loans

1.39%

1.54%

1.74%

Allowance for loan losses/

Total non-performing loans

(2)

123.88%

94.76%

78.44%

(1)

Metrics

shown

are

originated

portfolio

metrics

unless

noted

as

a

total

portfolio

metric

(applicable

for

years

2012

and

2011).

“Originated

portfolio”

or

“Originated loans”

excludes loans acquired at fair value and accounted for in accordance with ASC 805 (effective

January 1, 2009), as the risk of credit loss has been considered by virtue of the

Corporation’s estimate of fair value. (2)

Total portfolio metric |

Asset Quality Trends

26

1.60%

2.15%

2.74%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

2012

2011

2010

NPL's+OREO/

Originated Loans+OREO

(1)

0.41%

0.62%

0.77%

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

0.70%

0.80%

0.90%

2012

2011

2010

NCO's/Average Originated Loans

(1)

(1)

“Originated portfolio”

or “Originated loans”

excludes loans acquired at fair value and accounted for in accordance with ASC 805 (effective

January 1, 2009), as the risk of credit loss has been considered by virtue of the

Corporation’s estimate of fair value. |

Capital Position

27

Dividend Payout Ratio & Dividend Yield

2012

2011

2010

FNB –

Dividend Payout Ratio

61.3%

69.7%

74.0%

Regional Peer Group Median

38.0%

31.1%

40.0%

FNB –

Dividend Yield

4.52%

4.24%

4.89%

Regional Peer Group Median

2.93%

2.28%

1.35%

12.2%

10.6%

8.2%

6.0%

12.2%

10.7%

8.3%

6.1%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Total Risk-Based

Tier One

Leverage

Tangible Common Equity

September 30, 2012

December 31, 2012

Regulatory

“Well-Capitalized”

xxxx

xxxx |

28

Acquisition Strategy |

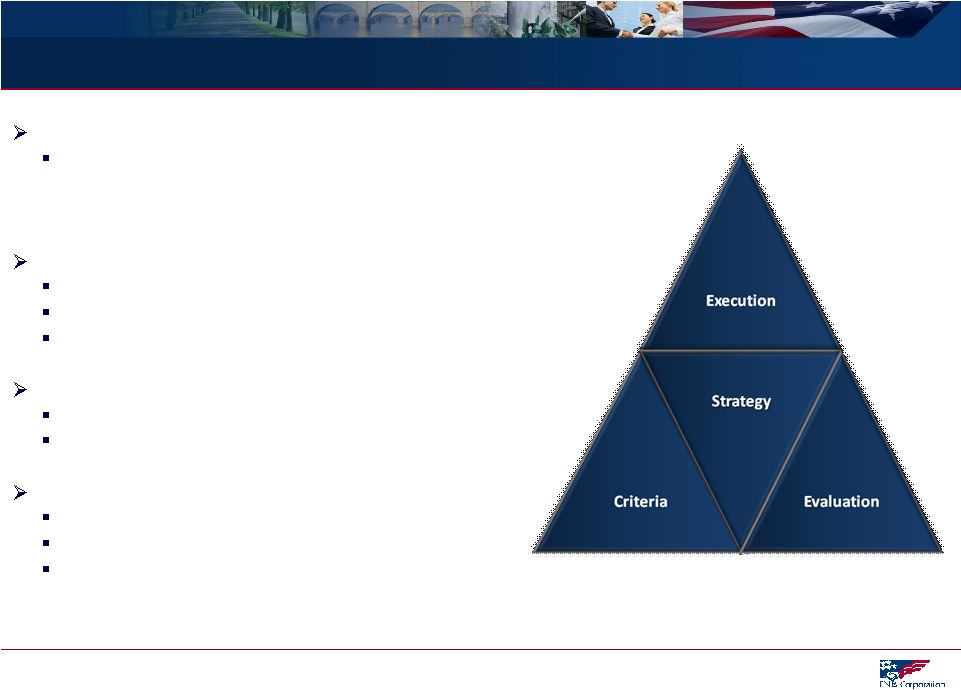

Acquisition Strategy

29

Disciplined and Consistent Acquisition Strategy

Strategy

Disciplined identification and focus on markets that

offer potential to leverage core competencies and

growth opportunities

Criteria

Create shareholder value

Meet strategic vision

Fit culturally

Evaluation

Targeted financial and capital recoupment hurdles

Proficient and experienced due diligence team

Execution

Superior post-acquisition execution

Execute FNB’s proven, scalable, business model

Proven success assimilating FNB’s strong sales culture |

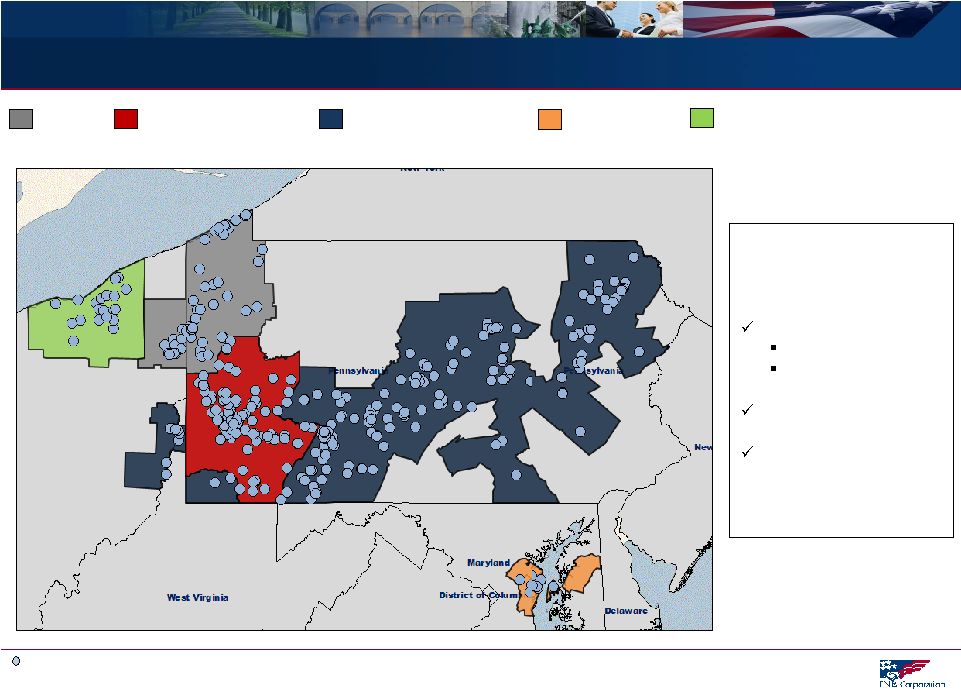

Acquisition-Related Expansion

30

FNB Banking Location (pro-forma)

11th

bank acquisition since

2002 announced

February 19, 2013 (PVFC)

Two currently pending

ANNB: April, 2013

PVFC: 3Q13

Four since 2010

(1)

Nine since 2005

(1)

(1) Includes two pending acquisitions

Pre-2002

Presence

Additional

Acquisition-Related Expansion

Pittsburgh

MSA Acquisition Expansion

Pending

ANNB Acquisition

Pending

PVFC Acquisition

Pittsburgh

Hermitage

State College

Harrisburg

Cleveland

Scranton

Philadelphia

Erie

Baltimore |

Natural

progression Consistent with stated expansion strategy

Market opportunity

Attractive demographics

Significant commercial banking opportunities

Excellent retail and wealth opportunities

Access to greater Baltimore and Washington

D.C. markets

Execute FNB’s scalable, proven business

model and strong sales management culture

Establishes a 5th

FNB region (refer to page 5)

Attractive partner

ANNB is a relationship-focused bank with

strong community ties and presence

Annapolis Bancorp, Inc. (ANNB) Opportunity Overview

31

Source:

Deposit

and

demographic

data

per

SNL

Financial;

deposits

as

of

June

30,

2012

(1) Includes branch opened October, 2012 in Waugh Chapel

County

Branches

Deposits in

Market ($000)

HH Income

($ -

2011)

Anne Arundel, MD

(1)

7

298,251

79,692

Queen Anne’s, MD

1

45,107

72,774

FNB Current Wtd Avg. by County

42,350

Annapolis Bancorp (ANNB) (8 branches)

(1)

F.N.B. (FNB) (246 branches)

Attractive Market Entry Opportunity

Markets conducive to FNB’s model |

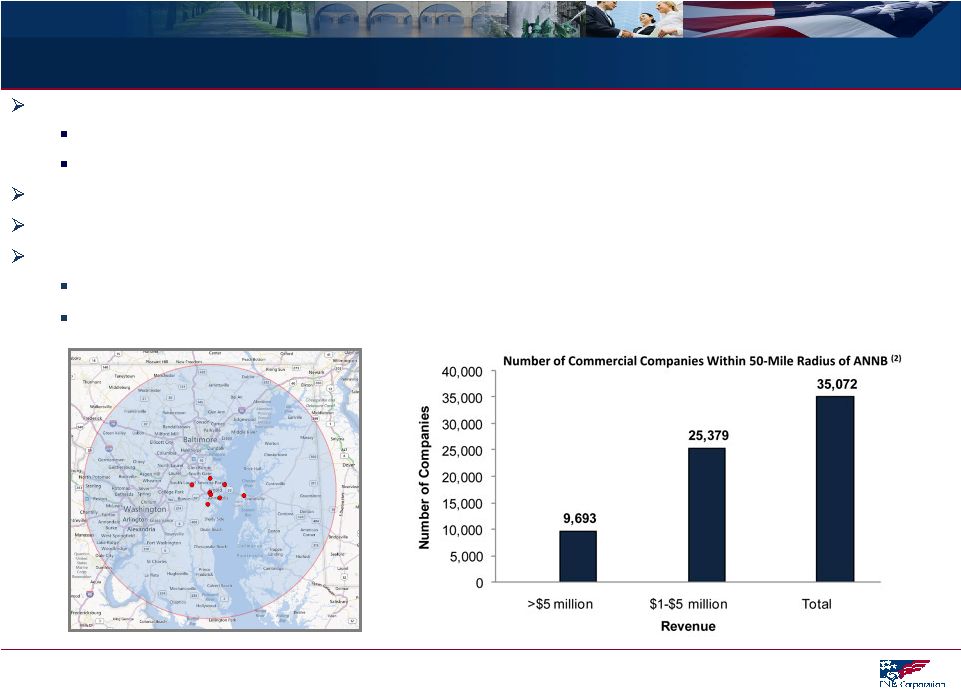

Annapolis Bancorp, Inc. (ANNB) Market Opportunity

32

Leverage FNB’s core competencies and proven business model in a high growth market

Execute FNB’s scalable, cross-functional sales management process

Regional model with local decision making, market leaders, credit authority and functional

support Competitive environment : Similar to FNB’s larger markets

Future opportunity for expansion: 25 identified banks in close proximity

(1)

Attractive markets present commercial and retail opportunities

Strong demographics present retail, wealth management, private banking and insurance

opportunities Strong commercial opportunities with access to more than 35,000 companies

within 50-mile radius (1)

Source: SNL Financial; Includes banks with assets between $200 million and $5 billion with

NPA’s/assets<4%; Excludes MHC’s, merger targets and banks with 5 or fewer

branches (2)

Source: Hoover’s; Includes companies within a 50-mile radius of ANNB headquarters

with revenue >$5 million, between $1 and $5 million and total companies with

revenue >$1 million |

Cuyahoga

Geauga

Lake

Lorain

Medina

Portage

Summit

Cuyahoga

Geauga

Lake

Lorain

Medina

Portage

Summit

Parkview Financial Corp. (PVFC) Pro Forma Franchise

Rank

Institution (ST)

Number

of

Branches

Deposits in

Market

($mm)

Market

Share

(%)

1

KeyCorp (OH)

76

9,961

19.8

2

PNC Financial Services Group (PA)

81

5,758

11.5

3

TFS Financial Corp (MHC) (OH)

19

5,629

11.2

4

RBS

66

4,421

8.8

5

Huntington Bancshares Inc. (OH)

88

4,212

8.4

6

Fifth Third Bancorp (OH)

64

3,531

7.0

7

FirstMerit Corp. (OH)

67

3,350

6.7

8

JPMorgan Chase & Co. (NY)

42

2,739

5.4

9

U.S. Bancorp (MN)

66

1,979

3.9

10

Dollar Bank FSB (PA)

27

1,663

3.3

14

Pro Forma

15

624

1.2

14

PVF Capital Corp. (OH)

12

564

1.1

27

F.N.B. Corp. (PA)

3

60

0.1

Totals (1-10)

596

43,243

86.0

Totals (1-39)

723

50,255

100.0

Cleveland, OH MSA

Source: SNL Financial and Microsoft MapInfo

Deposit data as of 6/30/2012 and pro forma for pending and completed

transactions WV

Pro Forma Branch Franchise

Branch Overlap

Distance

Branches

% of Franchise

< 1 mi:

1

6.3%

< 5 mi:

3

18.8%

FNB (246)

ANNB (8)

PVFC (16)

FNB Headquarters

Pittsburgh MSA

Cleveland MSA

Baltimore MSA

33 |

59,240

65,169

52,149

Pittsburgh

MSA

Baltimore

MSA

Cleveland

MSA

7.2%

7.0%

6.5%

Pittsburgh

MSA

Baltimore

MSA

Cleveland

MSA

1,001

1,043

852

Pittsburgh

MSA

Baltimore

MSA

Cleveland

MSA

Parkview Financial Corp. (PVFC) Market Opportunity

Total Households -

2011 (000)

Businesses

(2)

Unemployment Rate

(1)

Source: SNL Financial

(1) As of December 2012

(2) Per U.S. Census Bureau

•

Third consecutive acquisition in a major MSA

•

Cleveland,

Pittsburgh

and

Baltimore

have

an

aggregate

population

of

7.1

million,

significant

commercial

lending

opportunities

and

favorable demographics

•

The Cleveland market is conducive to FNB’s commercial banking model and strong

cross sell culture Opportunity to replicate FNB’s proven Pittsburgh

success in a market with similar characteristics Significantly enhances

number of commercial banking prospects within FNB footprint Retail locations

in attractive markets expected to benefit consumer banking, Wealth Management and Private Banking

Strong Opportunity

Expansion in Cleveland Market

34 |

35

Investment Thesis |

Long-Term Investment Thesis

36

Long-Term Investment Thesis:

Targeted EPS Growth

5-6%

Expected Dividend Yield

(Targeted Payout Ratio 60-70%)

4-6%

Total Shareholder Return

9-12%

FNB’s long-term investment thesis reflects a commitment to efficient capital management

and creating value for our shareholders |

Relative Valuation Multiples

37

FNB

Regional Peer

Group Median

National Peer

Group Median

(1)

Price/Earnings

Ratio

(2)

FY13 Consensus EPS (FNB=$0.86)

13.6x

14.0x

14.4x

FY 14 Consensus EPS (FNB=$0.92)

12.7x

13.0x

13.8x

Price/Tangible

Book

Value

(2)

2.4x

1.6x

1.5x

Price/Book

Value

(2)

1.2x

1.1x

1.1x

Dividend

Yield

(2)

4.1%

2.8%

2.4%

per

SNL

Financial:

Price/Earnings

Ratio

based

on

analyst

consensus

estimates

for

FNB

and

peers;

(1)

National

peer

group

consists

of

banks

with

assets

between $5 and $25 billion; (2) As of February 20, 2013 closing prices (FNB=$11.62)

FNB has a modest P/E valuation relative to peers given its higher-quality earnings stream,

stronger dividend yield and future growth potential |

FNB

Among Top Performing Banks 38

Notes: Data per SNL Financial and FNB. Year-to-date performance represents

Full Year 2012. Relative valuation metrics and total return as February 20, 2013.

FNB ROTCE represents operating ROTCE –

refer to Supplemental Information.

Assets

($ billions)

ROTCE (%)

Efficiency

Ratio (%)

Net Charge

Offs (%)

Net

Interest

Margin

Price/TBV (x)

Price/ 2013E

EPS (x)

Dividend

Yield (%)

Total Return

3 Yr (%)

Peer Median Results

Regional Peer Group

$9.6

11.86

60.2

0.55

3.73

1.57x

12.86x

2.82

28.47

Top 100 Banks/Thrifts Based on Asset Size

$14.1

11.82

62.2

0.46

3.58

1.47x

12.59x

2.26

25.63

Top 100 Trading at > 2.0x Tangible Book

$14.6

16.75

55.9

0.23

3.56

2.20x

12.10x

2.72

42.96

F.N.B. Corporation

$12.0

18.77

57.7

0.35

3.73

2.36x

12.68x

4.13

83.73

Year-to-Date Performance

Relative Valuation/Total Return |

Relative Valuation Analysis

Where a bank trades relative to tangible book value is highly correlated with its projected

return on tangible capital

Source: SNL Financial as of 2/20/13; Note: Data set above includes FNB’s regional peer

group; (1)R-squared represents the percentage of the variation in price to tangible

book value (P/TBV) that can be explained by variation in 2013E projected return on average tangible equity (ROATE); (2)Based on

consensus mean estimates for FY2013.

39 |

Relative Valuation –

Price/TBV Trends

FNB consistently trades at a premium to regional and national peers

based on price to tangible book value per share

(1)

(1) Market data per SNL Financial as of February 21, 2013.

40

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Price/Tangible Book Value

FNB

Regional Peers

National Peers |

41

Supplemental Information |

42

Supplemental Information Index

Diversified Loan Portfolio

Deposits and Customer Repurchase Agreements

Investment Portfolio

Loan Risk Profile (December 31, 2012)

Regency Finance Company Profile

Marcellus and Utica Shale Exposure and Focus

Regional Peer Group Listing

GAAP to Non-GAAP Reconciliation |

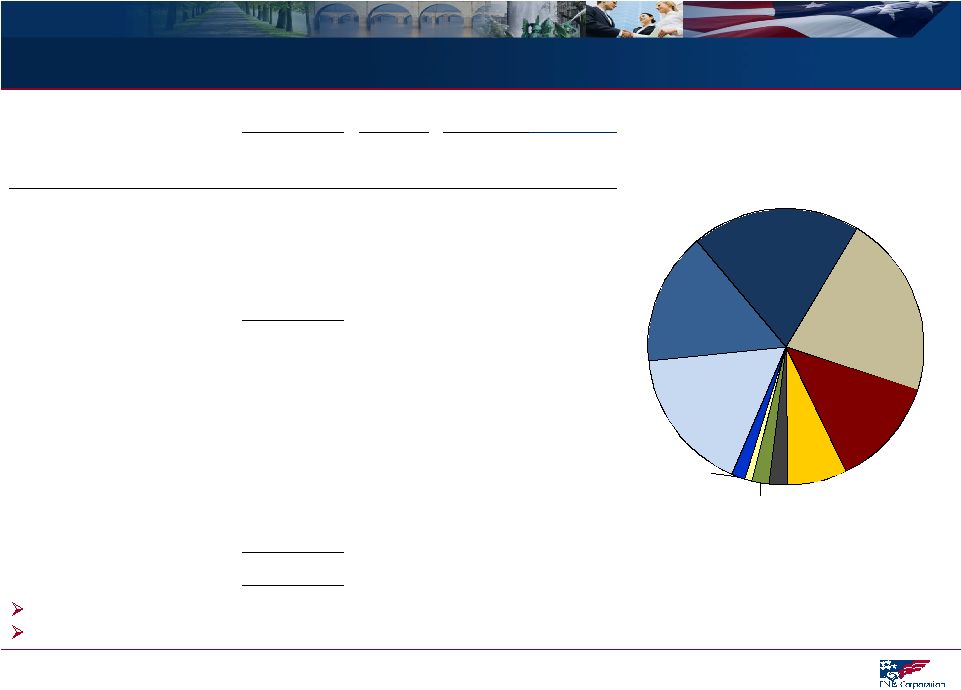

Diversified Loan Portfolio

43

Note: Balance, CAGR and % of Portfolio based on period-end balances

12/31/12

CAGR

% of Portfolio

($ in millions)

Balance

12/08-

12/12

12/31/08

12/31/12

C&I

$1,602

14.1%

16%

20%

CRE: Non-Owner Occupied

1,381

4.0%

17%

15%

CRE: Owner Occupied

1,258

8.8%

16%

17%

Commercial Leases

130

22.9%

1%

2%

Total Commercial

$4,371

9.4%

50%

54%

Consumer Home Equity

1,742

10.1%

21%

21%

Residential Mortgage

1,045

17.6%

10%

13%

Indirect

568

2.8%

9%

7%

Other

172

2.8%

3%

2%

Regency

171

1.4%

3%

2%

Florida

69

-27.1%

5%

1%

Total Loan Portfolio

$8,138

8.6%

100%

100%

Well diversified portfolio

Strong growth results driven by commercial loan growth

$8.1 Billion Loan Portfolio

December 31, 2012

Commercial &

Industrial 20%

Consumer

Home Equity

21%

Residential

Mortgage 13%

Indirect 7%

Other 2%

Regency 2%

Florida 1%

Commercial

Leases 2%

CRE: Owner

Occupied 17%

CRE: Non-

Owner

Occupied 15% |

Non-Interest

Bearing 18%

Savings, NOW,

MMDA 46%

Customer

Repos 10%

Time Deposits

26%

Deposits and Customer Repurchase Agreements

44

Note: Balance, CAGR and % of Portfolio based on period-end balances; (1) Transaction

deposits include savings, NOW, MMDA and non-interest bearing deposits; (2) December

31, 2008 through December 31, 2012; 12/31/2012

CAGR

Mix %

($ in millions)

Balance

12/08-

12/12

12/31/08

12/31/12

Savings, NOW, MMDA

$4,591

13.0%

44%

46%

Time Deposits

2,536

2.3%

36%

26%

Non-Interest Bearing

1,738

17.3%

14%

18%

Customer Repos

1,025

25.4%

6%

10%

Total Deposits and

Customer Repo Agreements

$9,890

11.2%

100%

100%

Transaction Deposits

(1)

and

Customer Repo Agreements

$7,354

16.5%

64%

74%

Loans to Deposits and Customer Repo Agreements Ratio =

82% at December 31, 2012

New client acquisition and relationship-based focus reflected in favorable deposit

mix –

16.5%

average

growth

for

transaction

deposits

and

customer

repo

agreements

(2)

–

74%

of

total

deposits

and

customer

repo

agreements

are

transaction-based

deposits

(1)

$9.9 Billion Deposits and

Customer Repo Agreements

December 31, 2012 |

%

Ratings

($ in millions

(1)

)

Portfolio

Investment %

Agency MBS

$1,055

46%

AAA

100%

Highly Rated $2.3 Billion Investment Portfolio

December 31, 2012

CMO Agency

604

26%

AAA

100%

Agency Senior Notes

383

17%

AAA

100%

Municipals

172

7%

AAA

AA

A

BBB

2%

88%

9%

1%

Trust Preferred

(2)

30

1%

A

BBB

BB

B

CCC

C

2%

5%

15%

16%

9%

53%

Short Term

23

1%

AAA

100%

CMO Private Label

17

1%

AA

A

BBB

BB

CCC

18%

13%

23%

24%

22%

Corporate

15

1%

A

BBB

70%

30%

Bank Stocks

2

-

Non-Rated

Commercial MBS

1

-

AAA

100%

US Treasury

1

-

AAA

100%

Total Investment Portfolio

$2,302

100%

Investment Portfolio

45

(1) Amounts reflect GAAP; (2) Original cost of $106 million, adjusted cost of $43 million,

fair value of $30 million AAA, 89.9%

AA, 6.8%

A, 1.2%

BBB,BB,B

CCC,CC,C

Non-Rated

2%

–

Highly rated with an average rating of AA and 97.9%

of the portfolio rated A or better

–

General obligation bonds = 99.5% of portfolio

–

77.4% from municipalities located throughout

Pennsylvania

97% of total portfolio rated AA or better

Relatively low duration of 2.7

Municipal bond portfolio |

46

Loan Risk Profile

(1)

Originated portfolio metric

$ in millions

Balance 12/31/12

% of Loans

NPL's/Loans

(1)

Net Charge-

Offs/Loans

(1)

Total Past

Due/Loans

(1)

Commercial and Industrial

$1,602,314

19.7%

0.39%

0.43%

0.89%

CRE: Non-Owner Occupied

1,380,671

17.0%

1.17%

0.15%

1.43%

CRE: Owner Occupied

1,257,747

15.5%

1.94%

0.37%

2.17%

Home Equity and Other Consumer

1,874,410

23.0%

0.46%

0.14%

0.89%

Residential Mortgage

1,045,319

12.8%

1.04%

0.07%

3.39%

Indirect Consumer

567,561

7.0%

0.19%

0.36%

1.14%

Regency Finance

170,999

2.1%

3.99%

3.58%

3.49%

Commercial Leases

130,133

1.6%

0.74%

0.23%

2.03%

Florida

68,627

0.8%

17.30%

1.08%

17.30%

Other

39,938

0.5%

6.76%

1.70%

8.89%

Total

$8,137,719

100.0%

1.12%

0.41%

1.64% |

Conservatively run consumer finance business with over 80 years of consumer lending

experience Good credit quality: Year-to-date net charge-offs to average

loans of 3.58% Strong returns: Full Year 2012: ROA 3.44%, ROE 36.33%, ROTE 40.88%

Regency Finance Company Profile

(1)

Return on average tangible common equity (ROTCE) is calculated by dividing net

income less amortization of intangibles by average common equity less

average intangibles. Tennessee

Ohio

Pennsylvania

Kentucky

47

71 Locations

Spanning Four

States

Regency Finance Company

$171 Million Loan Portfolio

86% of Real Estate Loans are First Mortgages

59%

27%

14%

Direct

Real Estate

Sales Finance |

Marcellus and Utica Shale Exposure

48

(1)

Sources:

www.marcellus.psu.edu,

retrieved

January

29,

2013;

(2)

www.dnr.state.oh.us,

retrieved

May

31,

2012;

(3)

Sterne

Agee

June

7,

2010

and

FBR

Capital Markets, March 2, 2011.

FNB Banking Locations

Pennsylvania

Ohio

FNB is well-positioned in the Marcellus Shale and Utica

Shale regions with a Pennsylvania footprint that closely

aligns with the Marcellus Shale concentration and

exposure to the Utica Shale region in Ohio.

FNB has been noted by analysts as being one of the

best geographically positioned banks to benefit from

the Marcellus Shale.

(3)

This presents opportunity for FNB given the expected

positive economic lift across much of FNB’s footprint.

Ohio Utica Shale Well Locations

(2)

(1) |

Marcellus and Utica Shale FNB Strategic Focus

49

Opportunity for FNB relates to potential indirect and induced economic benefits across

footprint Direct Effect:

Oil and Gas

Directly associated with the extraction, processing and

delivery of the gas

Drilling, extraction and support activities

Indirect Effect:

Supply Chain

Provides goods and services to the energy industry

e.g.: Iron and steel, transportation, commodity traders,

heavy equipment, surveyors, utilities, rig parts,

attorneys, real estate, machinery manufacturers, etc.

Induced Benefit:

Consumption

Resulting benefit to industries and individuals from positive

direct and indirect effects

e.g.: Higher education, travel, housing, food and drink,

entertainment, utilities, etc.

FNB

Strategic Focus:

Supply Chain and

Consumption |

Regional Peer Group Listing

50

ASBC

Associated Bancorp

NPBC

National Penn Bancshares, Inc.

CBSH

Commerce Bancshares, Inc.

ONB

Old National Bancorp

CBU

Community Bank Systems, Inc.

PRK

Park National Corp

CHFC

Chemical Financial Corp.

PVTB

Private Bancorp, Inc.

CRBC

Citizens Republic Bancorp, Inc.

SBNY

Signature Bank

CSE

CapitalSource, Inc.

SUSQ

Susquehanna Bancshares, Inc.

FCF

First Commonwealth Financial

TCB

TCF Financial Corp.

FFBC

First Financial Bancorp, Inc.

UBSI

United Bankshares, Inc.

FMBI

First Midwest Bancorp, Inc.

UMBF

UMB Financial Corp.

FMER

First Merit Corp.

VLY

Valley National Bancorp

FULT

Fulton Financial

WSBC

WesBanco, Inc.

MBFI

MB Financial, Inc.

WTFC

Wintrust Financial Corp.

NBTB

NBT Bancorp, Inc. |

GAAP to Non-GAAP Reconciliation

51

Return on Average Tangible Equity

Return on Average Tangible Assets

December 31, 2012

September 30, 2012

December 31, 2011

2012

2011

Net income

$28,955

$30,743

$23,737

$110,410

$87,047

Return on average tangible equity

Net income, annualized

$115,189

$122,304

$94,175

$110,410

$87,047

Amortization of intangibles, net of tax, annualized

5,800

5,798

4,689

5,938

4,698

$120,989

$128,102

$98,864

$116,348

$91,745

Average shareholders' equity

$1,400,429

$1,385,282

$1,219,575

$1,376,493

$1,181,941

Less: Average intangible assets

715,962

714,501

599,352

717,031

599,851

Average tangible equity

$684,467

$670,781

$620,223

$659,462

$582,089

Return on average tangible equity

17.68%

19.10%

15.94%

17.64%

15.76%

Return on average tangible assets

Net income, annualized

$115,189

$122,304

$94,175

$110,410

$87,047

Amortization of intangibles, net of tax, annualized

5,800

5,798

4,689

5,938

4,698

$120,989

$128,102

$98,864

$116,348

$91,745

Average total assets

$11,988,283

$11,842,204

$9,947,884

$11,782,821

$9,871,164

Less: Average intangible assets

715,962

714,501

599,352

717,031

599,851

Average tangible assets

11,272,320

$

11,127,704

$

9,348,532

$

11,065,789

$

9,271,313

$

Return on average tangible assets

1.07%

1.15%

1.06%

1.05%

0.99%

For the Quarter Ended

Year Ended December 31 |

GAAP to Non-GAAP Reconciliation

52

Operating Return on Average Tangible Equity

Operating Return on Average Tangible Assets

December 31, 2012

September 30, 2012

December 31, 2011

2012

2011

2010

Operating net income

Net income

$28,955

$30,743

$23,737

$110,410

$87,047

$74,652

Add: Merger and severance costs, net of tax

(3)

57

255

5,203

3,238

402

Add: Litigation settlement accrual, net of tax

1,950

1,950

Add: Branch consolidation costs, net of tax

1,214

1,214

Less: Gain on sale of building

942

942

Less: One-time pension expense credit

6,853

Operating net income

$32,116

$29,858

$23,992

$117,835

$90,285

$68,201

Operating diluted earnings per share

Diluted earnings per share

$0.21

$0.22

$0.19

$0.79

$0.70

$0.65

Add: Merger and severance costs, net of tax

-

-

-

0.04

0.02

-

Add: Litigation settlement accrual, net of tax

0.01

-

-

0.01

-

-

Add: Branch consolidation costs, net of tax

0.01

-

-

0.01

-

-

Less: Gain on sale of building

-

0.01

0.01

Less: One-time pension expense credit

-

-

-

-

-

0.05

Operating diluted earnings per share

$0.23

$0.21

$0.19

$0.84

$0.72

$0.60

Operating return on average tangible equity

Operating net income (annualized)

$127,762

$118,784

$95,183

$117,835

$90,285

$68,201

Amortization of intangibles, net of tax (annualized)

5,800

5,798

4,689

5,938

4,698

4,364

$133,562

$124,582

$99,873

$123,773

$94,983

$72,565

Average shareholders' equity

$1,400,429

$1,385,282

$1,219,575

$1,376,493

$1,181,941

$1,057,732

Less: Average intangible assets

715,962

714,501

599,352

717,031

599,851

564,448

Average tangible equity

$684,467

$670,781

$620,223

$659,462

$582,089

$493,284

Operating return on average tangible equity

19.51%

18.57%

16.10%

18.77%

16.32%

14.71%

Operating return on average tangible assets

Operating net income (annualized)

$127,762

$118,784

$95,183

$117,834

$90,285

$68,201

Amortization of intangibles, net of tax (annualized)

5,800

5,798

4,689

5,938

4,698

4,364

$133,562

$124,582

$99,873

$123,772

$94,983

$72,565

Average total assets

$11,988,283

$11,842,204

$9,947,884

$11,782,821

$9,871,164

$8,906,734

Less: Average intangible assets

715,962

714,501

599,352

717,031

599,851

564,448

Average tangible assets

11,272,320

$

11,127,704

$

9,348,532

$

11,065,789

$

9,271,313

$

8,342,286

$

Operating return on average tangible assets

1.18%

1.12%

1.07%

1.12%

1.02%

0.87%

For the Quarter Ended

Year Ended December 31 |

GAAP to Non-GAAP Reconciliation

53

Pre-Provision Net Revenue

2012

2011

2010

Pre-Provision Net Revenue (PPNR)

Net interest income (FTE)

$380,233

$324,404

$291,642

Non-interest income

131,463

119,918

115,972

Non-interest expense

318,829

283,734

251,103

Pre-Provision Net Revenue

$192,867

$160,588

$156,511

Less: Non-operating non-interest income

(172)

3,587

621

Add: Non-operating

non-interest expense 11,159

8,310

(7,655)

Operating Pre-Provision Net Revenue

$204,198

$165,312

$148,235

PPNR Earnings per Diluted Share

$1.45

$1.32

$1.30

Non-Operating Items Detail

Branch consolidation costs

-$1,713

-

Gain on sale of building

1,449

Net securities gains/losses/OTTI

92

$3,587

$621

Non-interest income non-operating items

-$172

$3,587

$621

Merger and severance

$8,004

$4,982

$619

Branch consolidation costs

155

Litigation accrual

3,000

FHLB pre-pay penalty

3,328

2,269

One-time pension credit

-10,543

Non-interest expense non-operating items

$11,159

$8,310

-$7,655

Year Ended December 31 |