Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Magyar Bancorp, Inc. | form8k-127598_mgyr.htm |

2013 Annual Shareholders Meeting 1 February 14, 2013

Forward Looking Statements This presentation contains statements about future events that constitute forward - looking statements within the meaning of the Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward - looking statements may be identified by reference to a future period or periods, or by the use of forward - looking terminology, such as “may,” “will,” “believe,” “expect,” or similar terms or variations on those terms, or the negative of those terms. Forward - looking statements are subject to numerous risks and uncertainties, including, but not limited to, those risks previously disclosed in the Company’s filings with the SEC, general economic conditions, changes in interest rates, regulatory considerations, competition, technological developments, retention and recruitment of qualified personnel, and market acceptance of the Company’s pricing, products and services, and with respect to the loans extended by the Bank and real estate owned, the following: risks related to the economic environment in the market areas in which the Bank operates, particularly with respect to the real estate market in New Jersey; the risk that the value of the real estate securing these loans may decline in value; and the risk that significant expense may be incurred by the Company in connection with the resolution of these loans. The Company wishes to caution readers not to place undue reliance on any such forward - looking statements, which speak only as of the date made. The Company does not undertake and specifically declines any obligation to publicly release the result of any revisions that may be made to any forward - looking statements to reflect events or circumstances after the date of such statements or to reflect the occurrence of anticipated or unanticipated events. 2

Company Overview

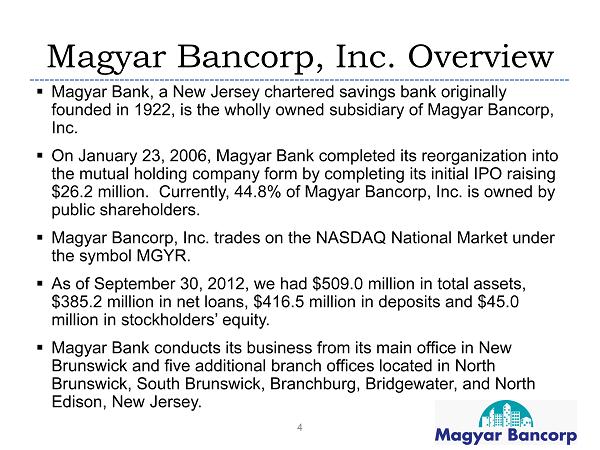

Magyar Bancorp, Inc. Overview ▪ Magyar Bank, a New Jersey chartered savings bank originally founded in 1922, is the wholly owned subsidiary of Magyar Bancorp, Inc. ▪ On January 23, 2006, Magyar Bank completed its reorganization into the mutual holding company form by completing its initial IPO raising $26.2 million. Currently, 44.8% of Magyar Bancorp, Inc. is owned by public shareholders. ▪ Magyar Bancorp, Inc. trades on the NASDAQ National Market under the symbol MGYR. ▪ As of September 30, 2012, we had $509.0 million in total assets, $385.2 million in net loans, $416.5 million in deposits and $45.0 million in stockholders’ equity. ▪ Magyar Bank conducts its business from its main office in New Brunswick and five additional branch offices located in North Brunswick, South Brunswick, Branchburg, Bridgewater, and North Edison, New Jersey. 4

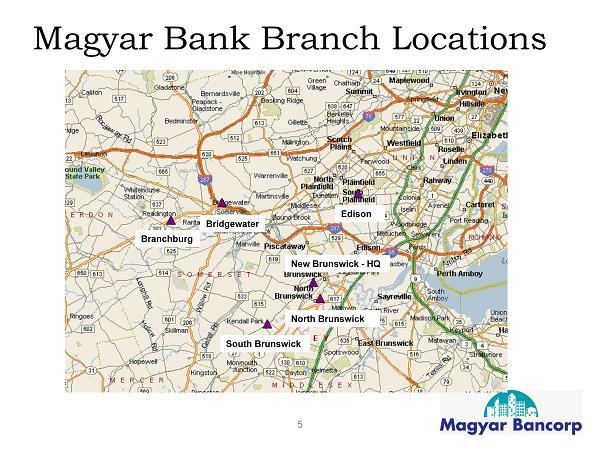

5 Magyar Bank Branch Locations Branchburg Bridgewater New Brunswick - HQ North Brunswick Edison South Brunswick

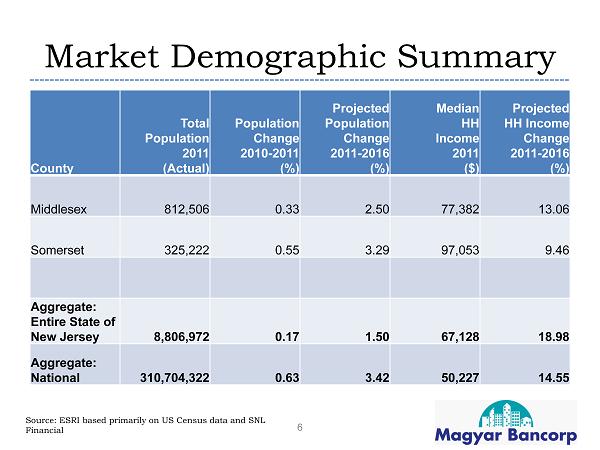

Market Demographic Summary 6 County Total Population 2011 (Actual) Population Change 2010 - 2011 (%) Projected Population Change 2011 - 2016 (%) Median HH Income 2011 ($) Projected HH Income Change 2011 - 2016 (%) Middlesex 812,506 0.33 2.50 77,382 13.06 Somerset 325,222 0.55 3.29 97,053 9.46 Aggregate: Entire State of New Jersey 8,806,972 0.17 1.50 67,128 18.98 Aggregate: National 310,704,322 0.63 3.42 50,227 14.55 Source: ESRI based primarily on US Census data and SNL Financial

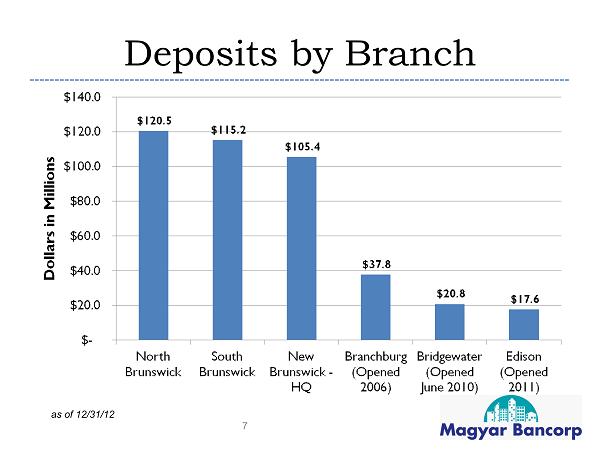

Deposits by Branch 7 as of 12/31/12

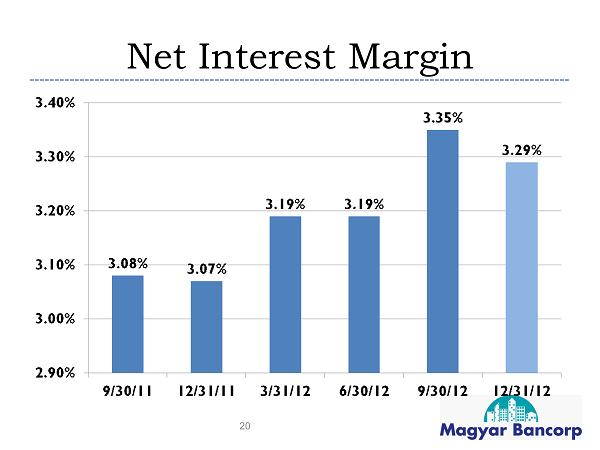

2012 Review ▪ Consent Order Removed in March, 2012 ▪ Sold six properties with a carrying value of $7.6 million in OREO property during Fiscal Year 2012 ▪ Non - performing loans declined 28% in Fiscal Year 2012 ▪ Non - performing assets declined 25% in Fiscal Year 2012 ▪ Net Interest Margin increased 10bps during the year to 3.21% as of 9/30/12, compared to 3.11% as of 9/30/11 ▪ Capital continued to strengthen – Tier 1 leverage ratio increased to 8.40% as of 9/30/12, Total Risk Based capital at 13.21% as of 9/30/12 8

2012 Review, (cont’d.) ▪ Checking deposits as a percentage of total deposits increased to 22.9% as of 9/30/12 from 19.3% as of 9/30/11 ▪ Certificates of deposit (including IRAs) as a percentage of total deposits declined to 37.1% as of 9/30/12 from 41.3% on 9/30/11. ▪ Non - Interest Expense declined 4.5% year over year ▪ Completed conversion to new core provider in June, 2012 which will provide the Company with significant cost savings ▪ Launched eStatements in June, 2012 – Adoption Rate of 19% in the program’s first 6 months. Estimated savings, $10/year per account. 9

Financial Highlights 10

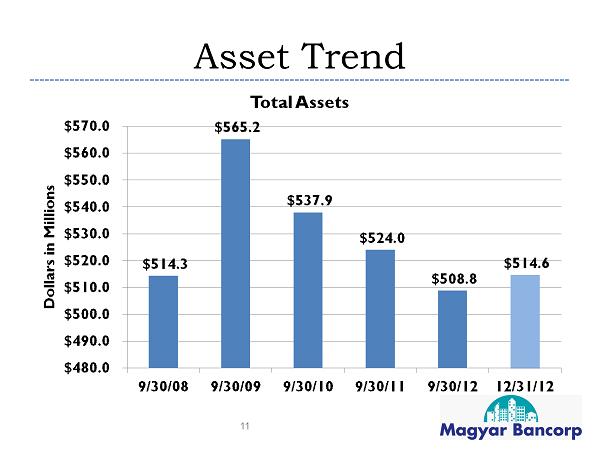

Asset Trend 11

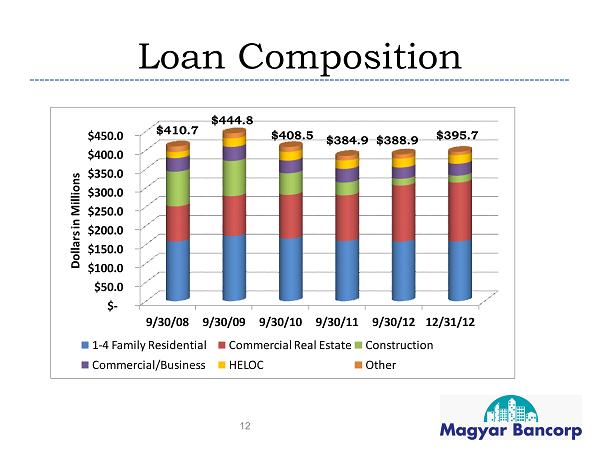

Loan Composition $ - $50.0 $100.0 $150.0 $200.0 $250.0 $300.0 $350.0 $400.0 $450.0 9/30/08 9/30/09 9/30/10 9/30/11 9/30/12 12/31/12 Dollars in Millions 1 - 4 Family Residential Commercial Real Estate Construction Commercial/Business HELOC Other 12 $410.7 $444.8 $408.5 $384.9 $388.9 $395.7

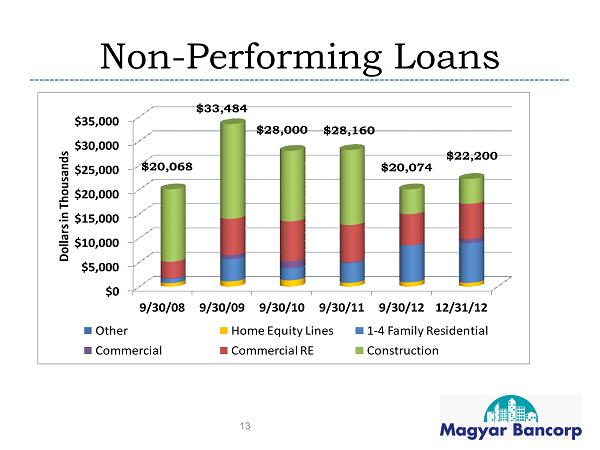

Non - Performing Loans $0 $5,000 $10,000 $15,000 $20,000 $25,000 $30,000 $35,000 9/30/08 9/30/09 9/30/10 9/30/11 9/30/12 12/31/12 Dollars in Thousands Other Home Equity Lines 1 - 4 Family Residential Commercial Commercial RE Construction $28,000 $20,068 $33,484 $28,160 $20,074 $22,200 13

Other Real Estate Owned $4,666 $5,562 $12,655 $16,595 $13,381 $12,979 $ - $2,000 $4,000 $6,000 $8,000 $10,000 $12,000 $14,000 $16,000 $18,000 9/30/08 9/30/09 9/30/10 9/30/11 9/30/12 12/31/12 Dollars in Thousands 14

Sale of Real Estate Owned (REO) ▪ Fiscal Year 2012 - Magyar Bank sold six REO properties with an aggregate carrying value of $7.6 million for a net loss of $22,000. ▪ 1 st Quarter of Fiscal Year 2013 – Magyar Bank sold 3 properties with an aggregate carrying value of $554,000 for a net loss of $8,000 ($.99 cents on the dollar). ▪ Magyar Bank was able to secure the title for seven other properties totaling $5.8 million. ▪ Potential strategies in addressing REO properties ▪ Hold property until real estate market improves ▪ Selling properties to a developer and completing partially completed homes ▪ Transition from sales to rentals to offset carrying costs 15

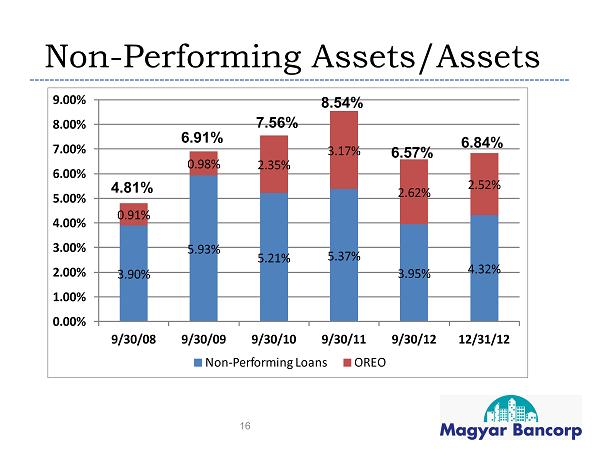

Non - Performing Assets/Assets 3.90% 5.93% 5.21% 5.37% 3.95% 4.32% 0.91% 0.98% 2.35% 3.17% 2.62% 2.52% 0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00% 7.00% 8.00% 9.00% 9/30/08 9/30/09 9/30/10 9/30/11 9/30/12 12/31/12 Non - Performing Loans OREO 16 4.81% 6.91% 7.56% 8.54% 6.57% 6.84%

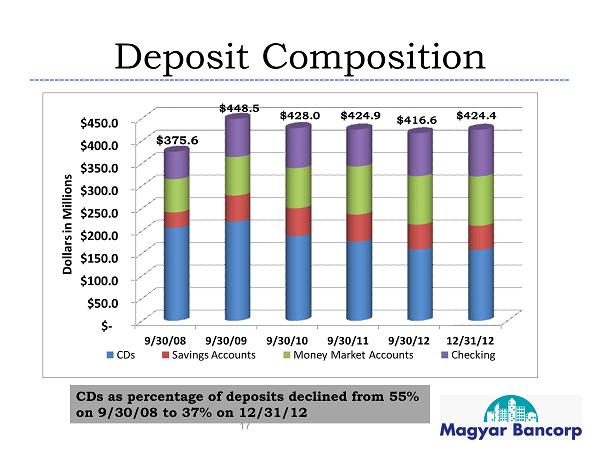

Deposit Composition $ - $50.0 $100.0 $150.0 $200.0 $250.0 $300.0 $350.0 $400.0 $450.0 9/30/08 9/30/09 9/30/10 9/30/11 9/30/12 12/31/12 Dollars in Millions CDs Savings Accounts Money Market Accounts Checking $448.5 $428.0 $424.9 $416.6 $424.4 17 $375.6 CDs as percentage of deposits declined from 55% on 9/30/08 to 37% on 12/31/12

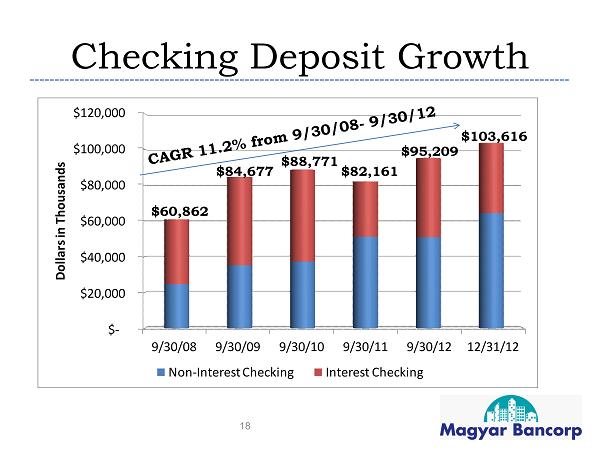

Checking Deposit Growth $ - $20,000 $40,000 $60,000 $80,000 $100,000 $120,000 9/30/08 9/30/09 9/30/10 9/30/11 9/30/12 12/31/12 Dollars in Thousands Non - Interest Checking Interest Checking 18 $60,862 $84,677 $88,771 $82,161 $95,209 $103,616

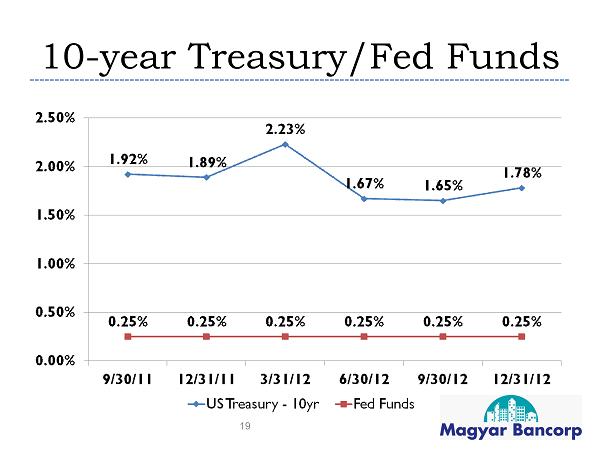

10 - year Treasury/Fed Funds 19

Net Interest Margin 20

Net Interest Margin – MHC Peer Group 21 MHCs in Northeast Region with Assets $200M - $1.5B – as of 12/31/12 Source: SNL Financial

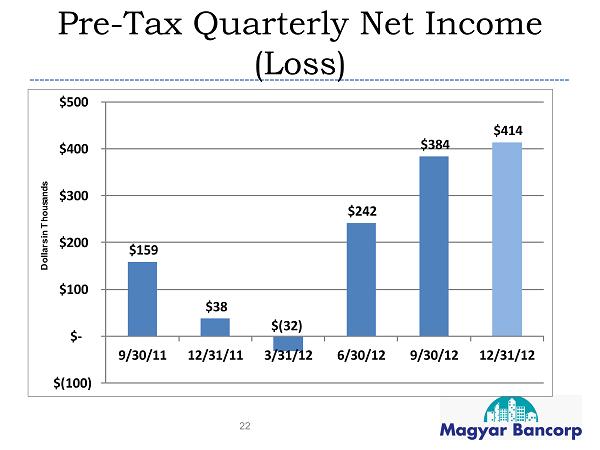

Pre - Tax Quarterly Net Income (Loss) $159 $38 $(32) $242 $384 $414 $(100) $ - $100 $200 $300 $400 $500 9/30/11 12/31/11 3/31/12 6/30/12 9/30/12 12/31/12 Dollars in Thousands 22

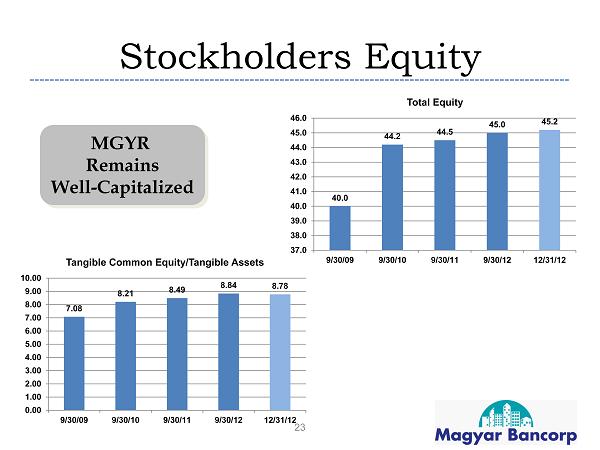

Stockholders Equity 23 MGYR Remains Well - Capitalized 7.08 8.21 8.49 8.84 8.78 0.00 1.00 2.00 3.00 4.00 5.00 6.00 7.00 8.00 9.00 10.00 9/30/09 9/30/10 9/30/11 9/30/12 12/31/12 Tangible Common Equity/Tangible Assets 40.0 44.2 44.5 45.0 45.2 37.0 38.0 39.0 40.0 41.0 42.0 43.0 44.0 45.0 46.0 9/30/09 9/30/10 9/30/11 9/30/12 12/31/12 Total Equity

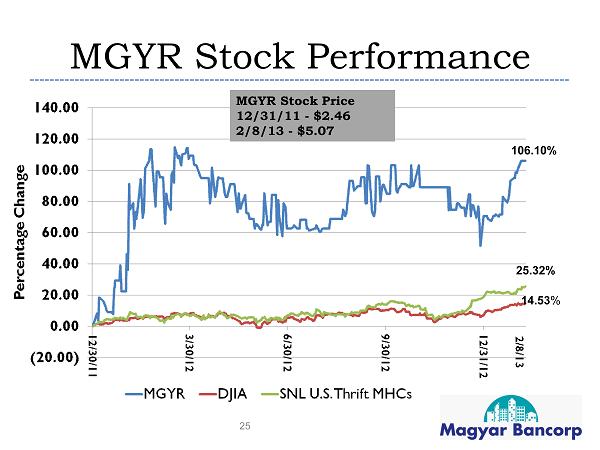

Stock Price Performance 24

MGYR Stock Performance 25 MGYR Stock Price 12/31/11 - $2.46 2/8/13 - $5.07 106.10% 25.32% 14.53 %

Fiscal Year 2013 Outlook 26

Fiscal Year 2013 • Reduce non - performing assets • Increase core earnings • Growth in residential and commercial lending • Dodd - Frank Impact • Continued Focus on Non - Interest Expenses 27

Questions? 28