Attached files

| file | filename |

|---|---|

| 8-K - 8-K - CAPITAL ONE FINANCIAL CORP | d469245d8k.htm |

| EX-99.2 - EXHIBIT 99.2 - CAPITAL ONE FINANCIAL CORP | d469245dex992.htm |

| EX-99.1 - EXHIBIT 99.1 - CAPITAL ONE FINANCIAL CORP | d469245dex991.htm |

Fourth Quarter 2012 Results

January 17, 2013

Exhibit 99.3 |

| Forward-Looking Statements

Please note that the following materials containing information regarding

Capital One's financial performance speak only as of the particular date or dates indicated

in these materials. Capital One does not undertake any obligation to

update or revise any of the information contained herein whether as a result of new information,

future events or otherwise.

Certain statements in this presentation and other oral and written

statements made by Capital One from time to time are forward-looking statements, including those

that discuss, among other things: strategies, goals, outlook or other

non-historical matters; projections, revenues, income, returns, expenses, capital measures,

accruals for claims in litigation and for other claims against Capital

One, earnings per share or other financial measures for Capital One; future financial and

operating results; Capital One's plans, objectives, expectations and

intentions; the projected impact and benefits of the acquisitions of ING Direct and HSBC's U.S.

credit card business (the "Transactions"); and the assumptions

that underlie these matters.

To the extent that any such information is forward-looking, it is

intended to fit within the safe harbor for forward-looking information provided by the Private

Securities Litigation Reform Act of 1995. Numerous factors could cause

Capital One's actual results to differ materially from those described in such forward-looking

statements, including, among other things: general economic and business

conditions in the U.S., the U.K., Canada and Capital One’s local markets, including

conditions affecting employment levels, interest rates, consumer income

and confidence, spending and savings that may affect consumer bankruptcies, defaults,

charge-offs and deposit activity; an increase or decrease in credit

losses (including increases due to a worsening of general economic conditions in the credit

environment); financial, legal, regulatory, tax or accounting changes or

actions, including the impact of the Dodd-Frank Wall Street Reform and Consumer

Protection Act and the regulations promulgated thereunder and regulations

governing bank capital and liquidity standards, including Basel-related initiatives; the

possibility that Capital One may not fully realize the projected cost

savings and other projected benefits of the Transactions; difficulties and delays in integrating the

assets and businesses acquired in the Transactions; business disruption

following the Transactions; diversion of management time on issues related to the

Transactions, including integration of the assets and businesses

acquired; reputational risks and the reaction of customers and counterparties to the Transactions;

disruptions relating to the Transactions negatively impacting Capital

One’s ability to maintain relationships with customers, employees and suppliers; changes in

asset quality and credit risk as a result of the Transactions; the

accuracy of estimates and assumptions Capital One uses to determine the fair value of assets acquired

and liabilities assumed in the Transactions; developments, changes or

actions relating to any litigation matter involving Capital One; the inability to sustain revenue

and earnings growth; increases or decreases in interest rates; Capital

One’s ability to access the capital markets at attractive rates and terms to capitalize and fund its

operations and future growth; the success of Capital One’s marketing

efforts in attracting and retaining customers; increases or decreases in Capital One’s aggregate

loan balances or the number of customers and the growth rate and

composition thereof, including increases or decreases resulting from factors such as shifting

product mix, amount of actual marketing expenses Capital One incurs and

attrition of loan balances; the level of future repurchase or indemnification requests

Capital One may receive, the actual future performance of mortgage loans

relating to such requests, the success rates of claimants against it, any developments in

litigation and the actual recoveries Capital One may make on any

collateral relating to claims against it; the amount and rate of deposit growth; changes in the

reputation of or expectations regarding the financial services industry

or Capital One with respect to practices, products or financial condition; any significant

disruption in Capital One’s operations or technology platform;

Capital One’s ability to maintain a compliance infrastructure suitable for the nature of its business;

Capital One’s ability to control costs; the amount of, and rate of

growth in, its expenses as its business develops or changes or as it expands into new market areas;

Capital One’s ability to execute on its strategic and operational

plans; any significant disruption of, or loss of public confidence in, the United States Mail service

affecting Capital One’s response rates and consumer payments;

Capital One’s ability to recruit and retain experienced personnel to assist in the management and

operations of new products and services; changes in the labor and

employment markets; fraud or misconduct by Capital One’s customers, employees or business

partners; competition from providers of products and services that

compete with Capital One’s businesses; and other risk factors set forth from time to time in

reports that Capital One files with the Securities and Exchange

Commission, including, but not limited to, the Annual Report on Form 10-K for the year ended

December 31, 2011.

You should carefully consider the factors discussed above in evaluating

these forward-looking statements. All information in these slides is based on the

consolidated results of Capital One Financial Corporation, unless

otherwise noted. A reconciliation of any non-GAAP financial measures included in this

presentation can be found in Capital One's most recent Current Report on

Form 8-K filed January 17, 2013, available on its website at www.capitalone.com

under "Investors." |

| 3

January 17, 2012

Highlights

•

Full year 2012 net income was $3.5B or $6.16 per share

–

Completed acquisitions of ING Direct & HSBC’s US Credit Card

business –

Significant impact from acquisition-related credit accounting

–

Enhanced

balance

sheet

strength,

Tier

1

Common

Ratio

of

11%

as

of

12/31/12

•

Q4 2012 net income was $843MM or $1.41 per share vs.

$1.18B or $2.01 per share in Q3 2012

–

Ending loan balance growth of $2.8B; Average loan balances flat

–

Net Interest Margin compression due largely to higher card revenue suppression

and higher cash & investment balances

–

Higher non-interest expense

•

Outlook

–

Expect fourth quarter pre-provision earnings rate to continue

•

Modest decline in earning assets and improvement in margin

•

2013 non-interest expense of ~$12.5B (inclusive of ~$1.5B of marketing)

–

Expect strong capital trajectory above Basel III target; begin planned

capital distribution to shareholders |

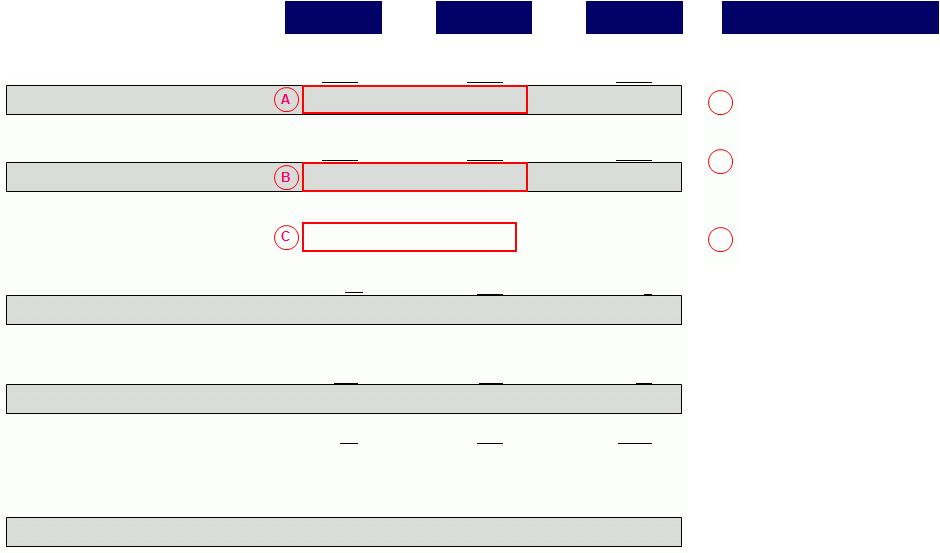

4

January 17, 2013

Fourth quarter results

Net interest income

Non-interest income

Total net revenue

Q4’12

Q3’12

Q2’12

Marketing

Operating expense

Non-interest expense

Net charge-offs

Allowance build/(release)

Provision for credit losses

Other

Pretax income from continuing operations

Income tax provision

Operating earnings, net of tax

Discontinued operations, net of tax

Pre-provision earnings

Net income

Diluted earnings per common share

4,646

1,136

5,782

316

2,729

3,045

2,737

887

156

(29)

1,014

1,723

535

1,188

(10)

1,178

$2.01

4,001

1,054

5,055

334

2,808

3,142

1,913

738

938

1

1,677

236

43

193

(100)

93

$0.16

$ and shares in millions, except per share data

Highlights

Wtd avg common shares outstanding

584.1

582.8

Net income avail to common stockholders

1,173

92

4,528

1,096

5,624

393

2,862

3,255

2,369

2

(1)

1,151

1,218

370

848

(5)

843

$1.41

585.6

825

Total

Revenue

decline

driven

primarily by higher Card

revenue suppression

Non-Interest Expense

increase driven by year-

end expense patterns

including marketing

Charge-offs

increase largely

from a lack of SOP 03-3

impact on charge-offs

A

B

C

1,150 |

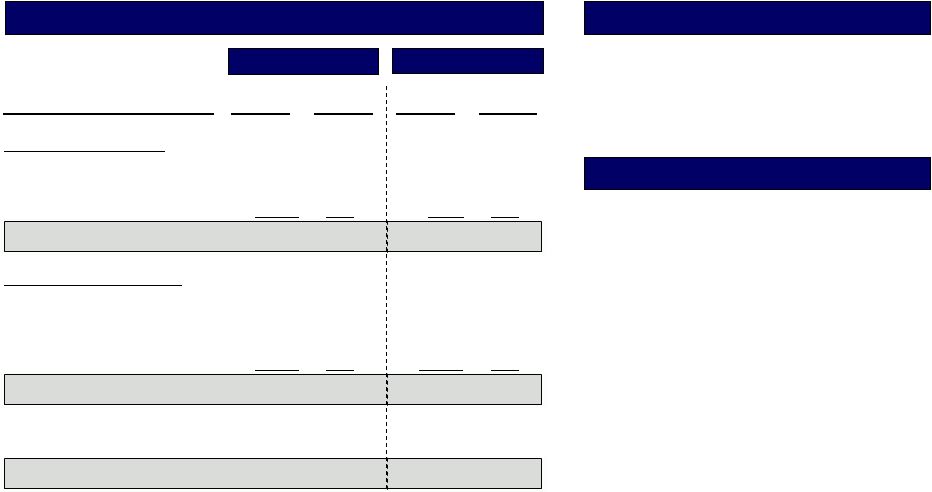

5

January 17, 2013

Yield/

Rate

Average

Balance

Q3’12

Net Interest Margin decreased in the quarter

Average Balances & Margin Highlights

(Dollars in millions)

Interest-earning

assets:

Loans held for investment

$

202,856

9.66

%

Investment securities

57,928

2.31

Cash equivalents and other

6,019

1.20

Total interest-earning assets

$

266,803

7.88

%

Interest-bearing

liabilities:

Total interest-bearing deposits

$

193,700

0.77

%

Securitized debt obligations

13,331

1.92

Senior and subordinated notes

3.08

Other borrowings

2.91

Interest-bearing liabilities

$

1.06

%

Impact of non-interest bearing funding

0.15

%

Net interest margin

6.97

%

11,035

12,085

230,151

Yield/

Rate

Average

Balance

Q4’12

$

202,944

9.31

%

64,174

2.25

10,768

1.04

$

277,886

7.36

%

$

192,122

0.72

%

12,119

1.91

2.95

1.87

$

0.99

%

0.15

%

6.52

%

11,528

20,542

236,311

Margin Outlook

Stable to modestly higher NIM

•

Expect stable earning asset yield

•

Expect lower cost of funds

•

TruPS called

•

Deposit management

Q4 Margin Decrease

•

Lower asset yields driven by higher

Card revenue suppression

•

Higher level of cash & securities |

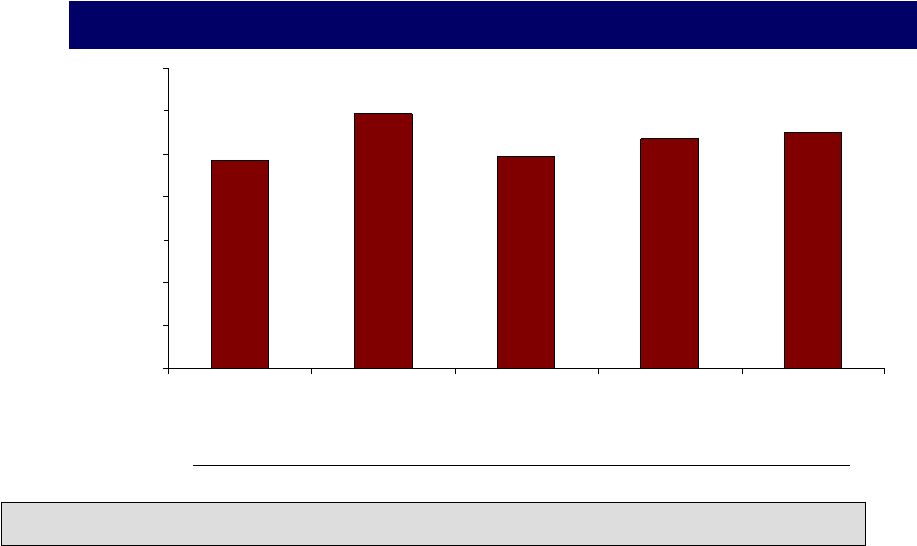

6

January 17, 2012

Our capacity to generate capital is strong

Tier

1

Common

Ratio

(Basel

I)

1

11.0%

10.7%

9.9%

11.9%

9.7%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Q4'11

Q1'12

Q2'12

Q3'12

Q4'12

Disallowed DTA

RWA

EOP Loans

Tier 1 common capital

excluding disallowed DTA

($B)

Tier 1 common capital

(0.5)

156

15.6

15.1

136

(0.9)

183

22.6

21.7

174

216

22.3

21.5

203

(0.8)

218

23.5

23.3

203

(0.2)

223

24.5

24.5

206

0.0

Basel III

equivalent

Tier 1 Ratio

of

~8%

2

1

Tier 1 common ratio is a regulatory capital measure calculated based on Tier 1

common capital divided by risk-weighted assets. See "Exhibit 99.2—Table 13: Reconciliation of Non-

GAAP Measures and Calculation of Regulatory Capital Measures" for the

calculation of this ratio. 2

Estimated based on our current interpretation, expectations and understanding of

the Basel III capital rules and other capital regulations proposed by U.S. regulators and the application

of such rules to our businesses as currently conducted.

regulations, model calibration and other implementation guidance, changes in our

businesses and certain actions of management, including those affecting the composition of our

balance sheet.

We believe this ratio provides useful information to investors and others by

measuring our progress against expected future regulatory capital standards.

Basel III calculations are necessarily subject to change based on, among other

things, the scope and terms of the final rules and |

7

January 17, 2012

Consumer Banking

Commercial Banking

Domestic Card

Our businesses continue to deliver solid results

•

Ending loans increased 3.1% in

the quarter, in line with

seasonal patterns; Excluding

expected HSBC and IL run-off,

card grew 4.1%

•

Ending loans were flat year

over year excluding HSBC

and run-off of Installment

Loans

•

Purchase

volumes

grew

9.4%

1

year-over-year, excluding

HSBC portfolio

•

Net revenue margin of 16.8%,

in line with expected seasonal

patterns and franchise

enhancements

•

Charge-off rate of 4.4%

–

Absence of merger-related

impacts

–

Expected seasonal patterns

•

Ending loan balances declined

–

$2.1B in expected run-off of

Home Loans

–

$700MM growth in Auto

loans

•

Seasonal decline in Auto

originations

•

Revenue decreased by 6%

quarter-over-quarter

–

Absence of Q3 favorable

valuation adjustment to

retained mortgage interests

•

Charge-off rate of 0.9%, up

5bps quarter-over-quarter,

driven by Auto seasonality

1

Reported purchase volume growth of 36% year-over-year

•

Strong growth continued with

ending loans up 4% in the

quarter and 13% year-over-

year

•

Net revenue up 3% in the

quarter and 11% for the full

year of 2012

•

Non-interest expense up 16%

in the quarter, driven by non-

recurring items. Full year

expenses were up 15%

•

Charge-off rate of 0.1% as

credit discipline continues to

drive low losses |

8

January 17, 2012

Focus on Execution

Capital Generation &

Allocation

Great Businesses with

Attractive Returns

We are well positioned and focused on delivering sustained shareholder

value, even in an environment of modest growth and low rates

•

Relevant scale

where it matters

most

•

Leading market

positions and

market share

•

Resilient risk-

adjusted returns

•

Two large integrations

on track

•

Solid progress toward

delivering a great

customer experience

•

Tightly managing

operating expense

•

At or near assumed

Basel III destination

•

Expect significant capital

generation to continue

beyond targets

•

Capital allocation principles

–

Fund growth with attractive

and resilient returns and pay

consistent, meaningful

dividend

–

Repurchase shares |